Corticosteroids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.20 Billion |

| Market Size (2031) | USD 8.02 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

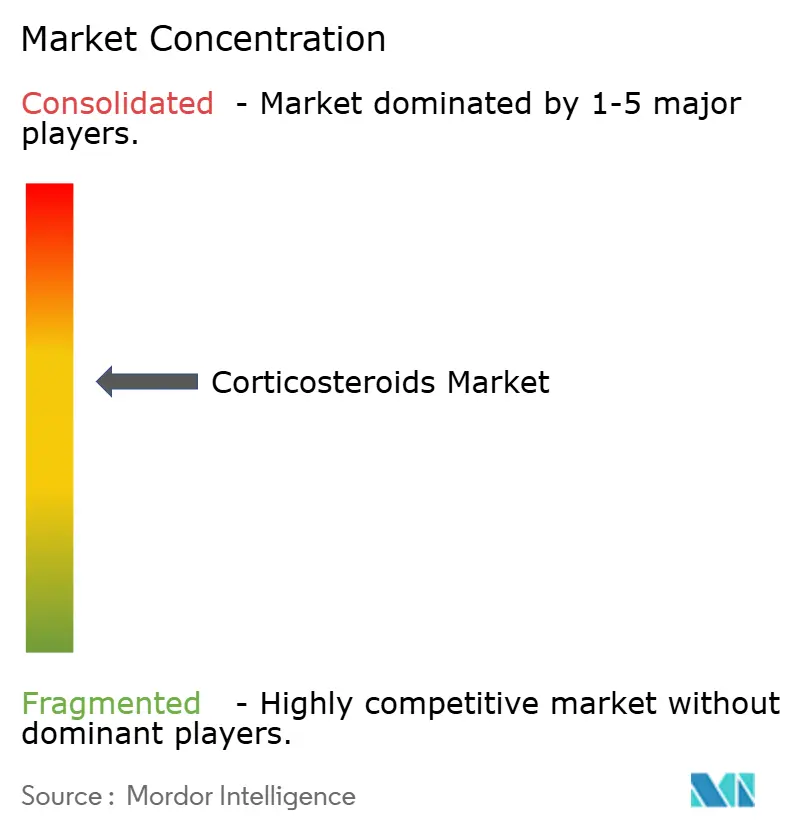

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Corticosteroids Market Analysis by Mordor Intelligence

The Corticosteroids Market size is projected to be USD 5.89 billion in 2025, USD 6.20 billion in 2026, and reach USD 8.02 billion by 2031, growing at a CAGR of 5.27% from 2026 to 2031.

Demand is rising as revised clinical guidelines move inhaled therapies to first-line status, while regulators fast-track safer oral and parenteral formulations. Digital inhalers, selective glucocorticoid receptor modulators, and combination products are broadening therapeutic utility. Competitive behavior is shifting toward lifecycle management ahead of looming patent cliffs, and manufacturers are localizing production to meet pricing pressure. Asia-Pacific, led by regulatory convergence and OTC liberalization, is the fastest-growing region, whereas North America continues to generate the highest revenue.

Key Report Takeaways

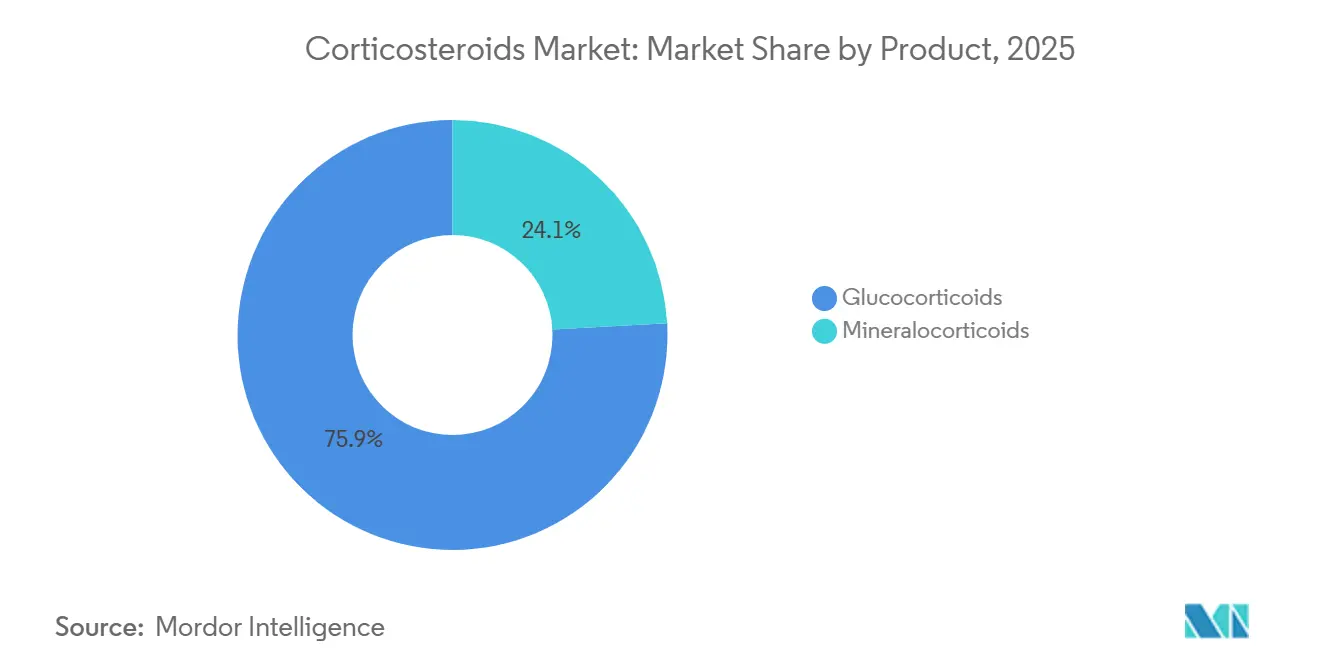

- By product, glucocorticoids held 75.86% of corticosteroids market share in 2025; mineralocorticoids are set to advance at a 6.02% CAGR to 2031.

- By route of administration, inhaled steroids commanded 38.47% revenue share in 2025; systemic and parenteral forms are forecast to expand at 6.05% CAGR through 2031.

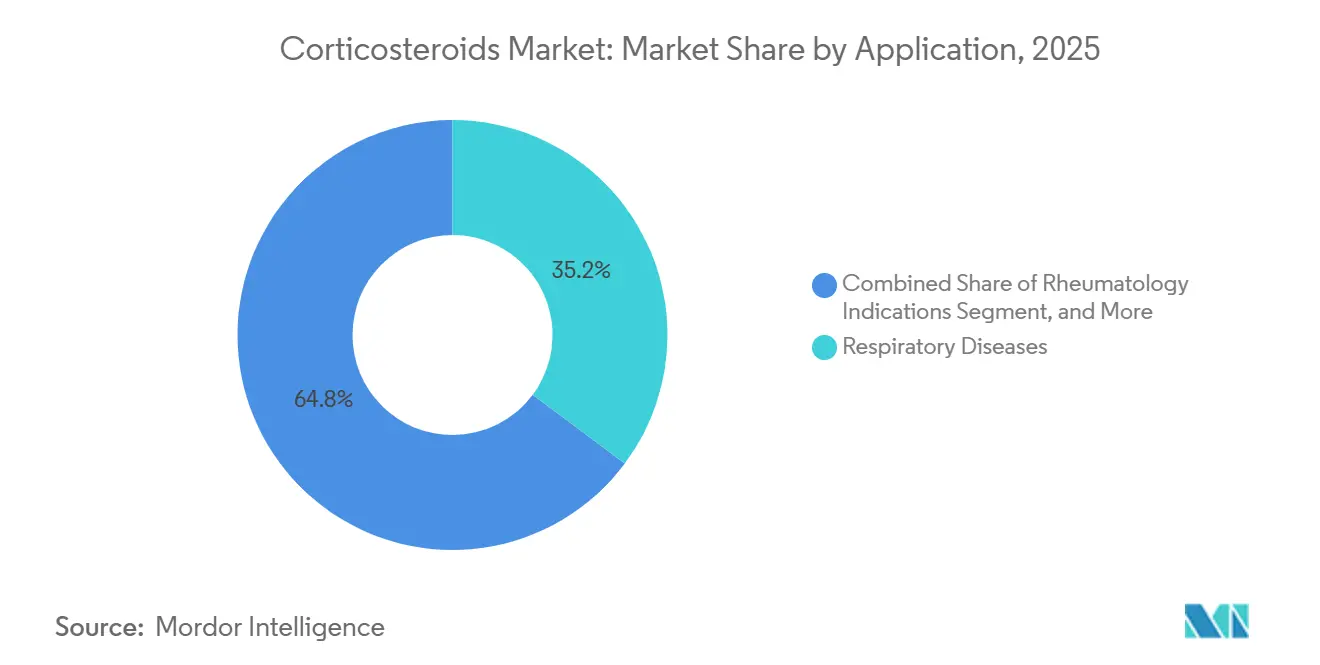

- By application, respiratory diseases accounted for 35.22% share of the corticosteroids market size in 2025, while rheumatology indications are growing at a 6.13% CAGR to 2031.

- By distribution channel, hospital pharmacies led with 54.10% share in 2025; online pharmacies are projected to grow at 6.22% CAGR through 2031.

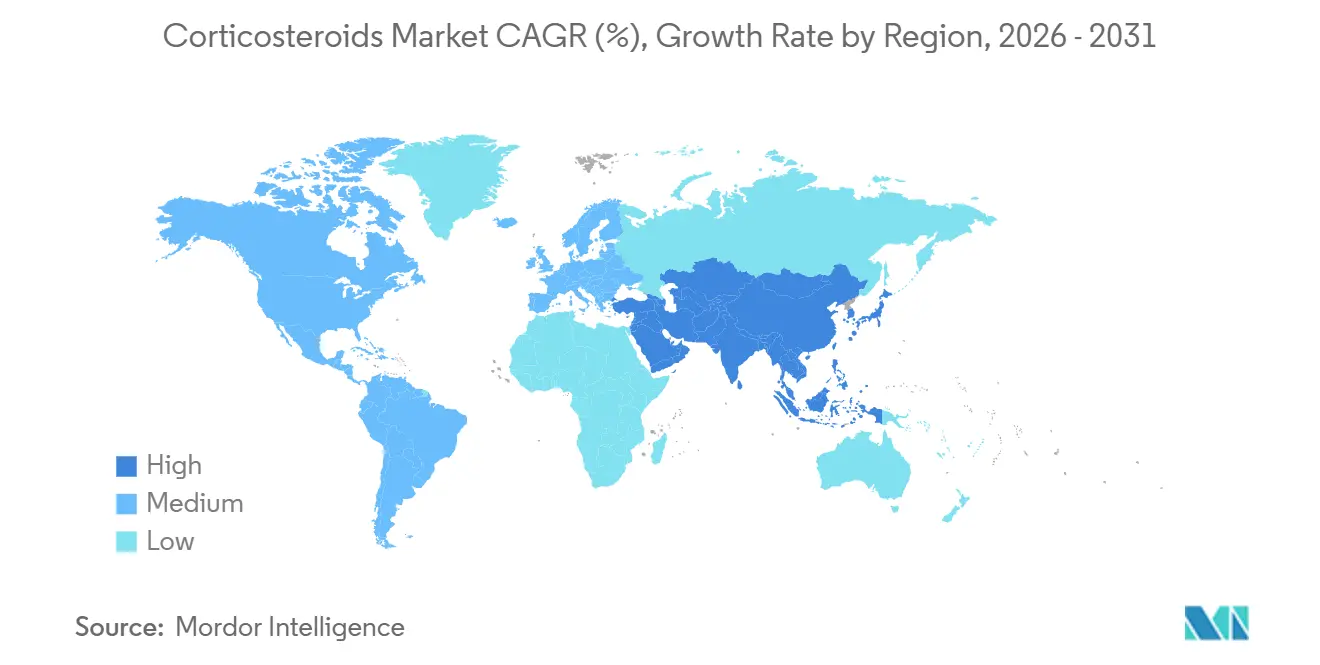

- By geography, Asia-Pacific is the fastest-growing region at 6.34% CAGR; North America remained the largest revenue contributor with 39.98% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corticosteroids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population & chronic diseases | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rising prevalence of autoimmune & inflammatory disorders | +0.9% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Expanding use of inhaled corticosteroids in updated asthma/COPD guidelines | +1.1% | Global, with early adoption in North America & Europe | Short term (≤ 2 years) |

| Broader OTC availability of low-potency topical steroids in emerging markets | +0.8% | APAC, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Development of selective glucocorticoid receptor modulators (SEGRMs) | +0.7% | North America & Europe initially, global expansion | Long term (≥ 4 years) |

| Digital/connected drug-delivery devices improving adherence | +0.6% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population & Chronic Diseases

Population aging is lifting chronic inflammatory case-loads, prompting earlier steroid intervention and longer treatment windows. Critical-care updates list corticosteroids for septic shock and ARDS, widening systemic use.[1]Chaudhuri, Dipayan, "2024 Focused Update: Guidelines on Use of Corticosteroids in Sepsis, Acute Respiratory Distress Syndrome, and Community-Acquired Pneumonia," Critical Care Medicine, journals.lww.com Healthcare systems are also backing steroid-sparing research partnerships that target toxicity reduction. The combined trend sustains baseline demand while opening niches for low-dose and extended-release versions that maintain efficacy yet curb adverse events.

Rising Prevalence of Autoimmune & Inflammatory Disorders

Autoimmune disease incidence is climbing, compelling personalized, multidisciplinary care pathways. Consensus statements now advocate tailored glucocorticoid regimens and combo biologics for eosinophil-driven disease, supporting corticosteroid-sparing yet still relying on baseline steroids.[2]Al-Moamary, "The Saudi initiative for asthma – 2024 update: Guidelines for the diagnosis and management of asthma in adults and children," Annals of thoracic Medicine, journals.lww.comData from combination reliever therapies show markedly fewer exacerbations, reinforcing inhaled steroid positioning. Expanded recognition of inflammatory pathways in new diseases is stretching addressable populations.

Expanding Use of Inhaled Corticosteroids in Updated Asthma/COPD Guidelines

Respiratory societies in the United States, Canada, and Europe have moved away from SABA-only regimens, installing inhaled corticosteroid/formoterol inhalers as initial therapy.[3]British Thoracic Society (BTS), "BTS/NICE/SIGN joint guideline on asthma: diagnosis, monitoring and chronic asthma management (November 2024) - summary of recommendations," Thorax, thorax.bmj.com Single-inhaler triple therapy receives preference for high-risk COPD, driving multi-drug inhaler uptake. Digital health add-ons demonstrate improved adherence and better Asthma Control Test scores, amplifying demand for connected ICS devices.

Broader OTC Availability of Low-Potency Topical Steroids in Emerging Markets

Emerging-market regulators are approving prescription-to-OTC switches for mild topical corticosteroids under new nonprescription frameworks. Self-medication surveys in the Gulf show topical steroid use without guidance surpassing 40%, highlighting both the market’s growth potential and stewardship needs. Multinationals and local generics firms are accelerating affordable product rollouts while governments weigh safe-use labeling requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government pricing pressure & generic erosion | -1.4% | Global, with highest impact in North America & Europe | Short term (≤ 2 years) |

| Adverse events from prolonged corticosteroid use | -0.8% | Global, with regulatory focus in developed markets | Medium term (2-4 years) |

| Stringent regulatory scrutiny for new formulations | -0.6% | North America & Europe primarily, expanding globally | Medium term (2-4 years) |

| Biologics & JAK-inhibitors as steroid-sparing alternatives | -0.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Pricing Pressure & Generic Erosion

Negotiated drug pricing schemes in the United States and aggressive reimbursement talks in China are compressing branded margins. Key inhalers and topical brands face 2025 exclusivity loss, inviting low-cost generics that quickly cannibalize share. Companies front-load price increases and shift rebate structures but these levers offer only short-term relief.

Adverse Events from Prolonged Corticosteroid Use

Long-term systemic exposure is linked to adrenal insufficiency and metabolic complications, prompting guideline writers to trim dosing windows and promote alternate therapies. Regulators flag safety warnings, resulting in more intensive risk-management plans. Manufacturers are steering R&D toward receptor-selective modulators and targeted delivery systems that lower systemic load, yet reimbursement bodies demand clear safety-benefit evidence before granting premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Glucocorticoids Dominate Through Innovation

Glucocorticoids held 75.86% of 2025 revenue, underpinned by continual advances in delivery technologies and receptor-selective chemistry. The corticosteroids market size attributed to glucocorticoids stood at USD 4.47 billion in 2025, and the segment is projected to grow at 5.19% CAGR. High clinical familiarity and broad label coverage shield revenue even as biologics encroach on some indications. Mineralocorticoids, although small in value, will outpace at 6.02% CAGR as products such as finerenone show cardio-renal benefit.

Pipeline data point to next-wave selective modulators and nanoparticle carriers that aim to keep anti-inflammatory potency yet diminish adverse profiles. Approvals like crinecerfont for congenital adrenal hyperplasia illustrate combination strategies that trim glucocorticoid dose without losing disease control. Capacity expansions in South Korea and Ireland signal readiness to meet expected volume growth.

By Route of Administration: Systemic Forms Accelerate Growth

Inhaled therapies captured 38.47% share in 2025 and remain essential owing to updated respiratory guidelines. Yet systemic and parenteral products will chart a faster 6.05% CAGR as critical-care protocols broaden and extended-release injectables prolong dosing intervals.

Engineering improvements are driving this trend. Extended-release IA injections deliver months-long osteoarthritis pain relief, while nano-aerosol generators lower particle size for deeper lung deposition. Nasal, ophthalmic, and topical platforms are also adopting in-situ gel matrices to extend mucosal residence time and curb dosing frequency.

By Application: Rheumatology Indications Drive Growth

Respiratory conditions represented 35.22% of 2025 demand, but rheumatology will grow quickest at 6.13% CAGR through 2031. Combination regimens that pair low-dose corticosteroids with disease-modifying antirheumatic drugs are being calibrated to minimize systemic burden. Renal, dermatology, and endocrine uses retain steady volume, and new orphan approvals in adrenal and eosinophilic disorders are nudging overall case numbers upward.

Early adoption of corticosteroid-sparing adjuncts does not diminish market relevance; instead it pushes innovation toward receptor-selective and tissue-targeted molecules. Oral budesonide suspension receiving first-in-class approval for eosinophilic esophagitis showcases continued expansion into gastroenterology niches.

By Distribution Channel: Online Pharmacies Reshape Access

Hospital pharmacies accounted for 54.10% of turnover in 2025 given their control over systemic injectables and critical-care protocols. However, online outlets will post 6.22% CAGR, underpinned by prescription-digital linkage and doorstep delivery that suits chronic maintenance regimens.

National rules permitting e-prescription and teleconsultation in markets such as Vietnam, India, and Brazil catalyze this transition. Specialty pharmacy services further support complex dosing schedules, while pharmacist prescribing expansion enhances community access where physician density is low.

Geography Analysis

North America retained the largest revenue share at 39.98% in 2025 on the back of high diagnosis and treatment penetration, comprehensive insurance cover, and rapid uptake of new formulations. The corticosteroids market size in the region reached USD 2.36 billion in 2025. Pricing reforms under the Inflation Reduction Act are squeezing margins, yet large installed user bases and clinical guideline alignment sustain volume.

Asia-Pacific is the fastest-growing territory, clocking a 6.34% CAGR as regulators streamline drug registration and broaden OTC access. Domestic producers are winning national tenders following aggressive price cuts, but multinationals bolster competitiveness by localizing manufacturing and launching connected inhalers that address adherence. Regional clinical panels now endorse nebulized budesonide in both stable and acute respiratory settings, reinforcing demand.

Europe follows steady mid-single-digit growth. EMA harmonization allows cross-border launches that reduce time-to-market for niche formulations. Evidence-based medicine culture accelerates adoption of receptor-selective modulators and steroid-sparing combos. Eastern Europe, with rising healthcare spend, offers incremental upside. Latin America and the Middle East & Africa record moderate gains as infrastructure and reimbursement expand, though affordability hurdles still limit inhaled steroid access in low-income settings.

Competitive Landscape

Competition remains moderate with consolidation trends intensifying. The Mallinckrodt–Endo merger combines generics, sterile injectables, and specialty brands, creating scale across respiratory and autoimmune portfolios. Leading firms prioritize lifecycle extensions—prefilled syringes, line extensions, and digital inhalers—to defend share before patent expiries. Selective receptor modulators, like relacorilant, progress through Phase III programs across oncology and endocrine diseases, pointing toward differentiated, premium-priced niches.

Digital health integration is emerging as a key point of differentiation. Connected inhalers track adherence and relay data to clinicians, while mobile prompts reduce errors. Pediatric and orphan-disease formulations offer white-space for smaller innovators; ANI’s acquisition of ocular steroid implants demonstrates bolt-on portfolio strategy. Manufacturing prowess is critical as price-controlled tenders favor low-cost but quality-assured suppliers. Firms are investing in continuous-flow and high-potency sterile factories to ensure regulatory compliance and cost efficiency.

Intellectual-property cliffs in 2025 for several inhaled and topical brands invite a wave of generics. Established players seek volume deals with group purchasing organizations to offset unit price decline. Biosimilars in adjacent immunology categories set pricing precedents that may spill into systemic corticosteroid biologic adjuncts, intensifying longer-term margin pressure.

Corticosteroids Industry Leaders

-

Pfizer Inc.

-

Novartis AG

-

GSK

-

Merck KGaA

-

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Codex Labs announced that it has secured two U.S. patents for its innovative steroid-free eczema treatment technology.

- June 2025: Amneal Pharmaceuticals won FDA approval for prednisolone acetate ophthalmic suspension 1% referencing Pred Forte, with launch slated for Q3 2025.

- May 2025: Eton Pharmaceuticals secured FDA clearance for Khindivi (hydrocortisone) oral solution for pediatric adrenocortical insufficiency.

- March 2025: Mallinckrodt and Endo announced a strategic merger to create a diversified global pharmaceuticals entity.

Global Corticosteroids Market Report Scope

Corticosteroids are the steroid hormones that are either produced by the body (Systemic corticosteroids) or man-made (Synthetic corticosteroids). When the adrenal cortex ceases the production of required corticosteroids, synthetic corticosteroids are given to the patients. They are often used as part of treatment for different diseases like asthma, various skin allergies, and arthritis, among others.

The corticosteroids market is segmented by Product type (Glucocorticoids, Mineralocorticoids), Route of Administration (Topical steroids, Inhaled steroids, Oral forms, Systemic forms), Application (Rheumatology indications, Skin allergies, Endocrinology, Gastroenterology, Acute respiratory diseases, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Glucocorticoids |

| Mineralocorticoids |

| Topical Steroids |

| Inhaled Steroids |

| Oral Forms |

| Systemic / Parenteral Forms |

| Others |

| Rheumatology Indications |

| Dermatology / Skin Allergies |

| Endocrinology |

| Gastroenterology |

| Respiratory Diseases |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Glucocorticoids | |

| Mineralocorticoids | ||

| By Route of Administration | Topical Steroids | |

| Inhaled Steroids | ||

| Oral Forms | ||

| Systemic / Parenteral Forms | ||

| Others | ||

| By Application | Rheumatology Indications | |

| Dermatology / Skin Allergies | ||

| Endocrinology | ||

| Gastroenterology | ||

| Respiratory Diseases | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the corticosteroids market?

The corticosteroids market size stands at USD 6.20 billion in 2026 and is projected to reach USD 8.02 billion by 2031.

Which product type holds the largest corticosteroids market share?

Glucocorticoids lead with 75.86% market share, supported by wide therapeutic use and ongoing formulation upgrades.

Why is Asia-Pacific the fastest-growing region?

Regulatory convergence, broader OTC access, and expanding manufacturing capabilities drive a 6.34% CAGR in Asia-Pacific.

How are digital inhalers influencing market growth?

Connected inhalers boost adherence and improve Asthma Control Test scores, lifting demand for inhaled corticosteroid products.

What threat do biologics pose to traditional corticosteroids?

Biologics and JAK-inhibitors provide steroid-sparing options, trimming high-dose usage but simultaneously encouraging development of selective receptor modulators that preserve steroid advantages.

Page last updated on: