Gemcitabine Hydrochloride Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

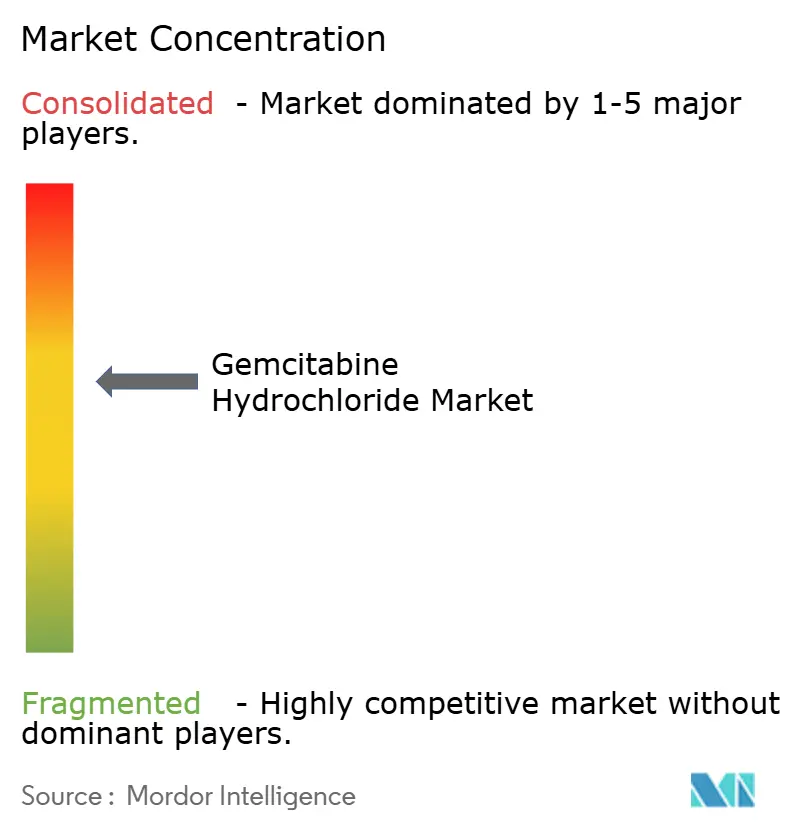

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gemcitabine Hydrochloride Market Analysis by Mordor Intelligence

Gemcitabine hydrochloride market size in 2026 is estimated at USD 885.44 million, growing from 2025 value of USD 0.83 billion with 2031 projections showing USD 1.22 billion, growing at 6.68% CAGR over 2026-2031. This solid mid-single-digit growth underscores the drug’s continuing relevance across multiple solid-tumor protocols despite surging investment in immuno-oncology. Uptake is reinforced by widespread clinical familiarity, reliable supply, and the molecule’s compatibility with next-generation regimens that seek to modulate, rather than replace, established cytotoxic backbones. The expansion of label-extension trials in hard-to-treat cancers, rapid regulatory approvals of gemcitabine-anchored combinations, and operational advantages of ready-to-use infusions in busy oncology centers also buoy demand. Strategic consolidation, such as Cheplapharm’s 2024 purchase of Gemzar, illustrates how specialty players are unlocking new value from mature assets while big pharma pivots to targeted therapies. At the same time, localized API incentives in India and China are compressing costs and improving global supply resilience, sharpening competition on both price and formulation innovation.

Key Report Takeaways

- By product type, injections held 71.56% of gemcitabine hydrochloride market share in 2025; ready-to-use IV solutions are projected to expand at a 7.71% CAGR through 2031.

- By indication, pancreatic cancer accounted for 39.22% of gemcitabine hydrochloride market size in 2025, whereas non-small cell lung cancer is forecast to deliver the fastest 7.63% CAGR to 2031.

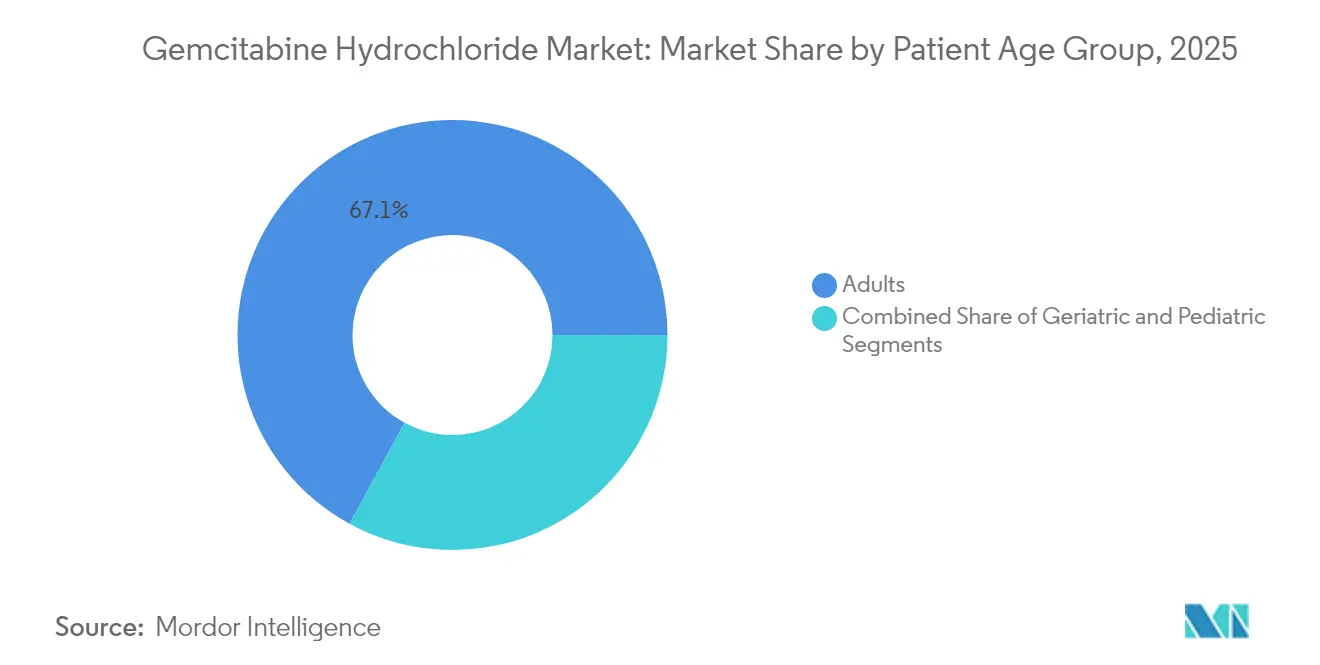

- By patient age group, adults captured 67.05% share of the gemcitabine hydrochloride market size in 2025, while the pediatric segment is set to grow at an 7.74% CAGR between 2026-2031.

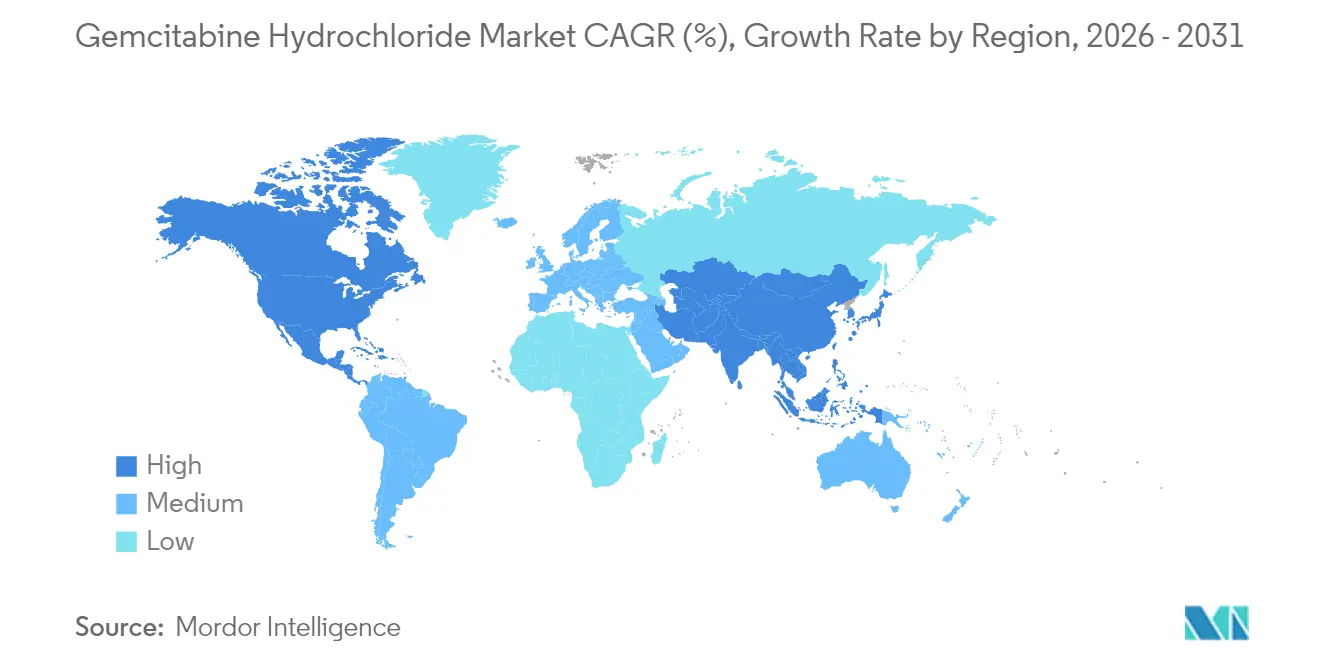

- By geography, North America led with 40.58% of gemcitabine hydrochloride market share in 2025; Asia-Pacific is on track for the quickest 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gemcitabine Hydrochloride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of solid-tumor cancers | +1.8% | Global – highest in APAC & MEA | Long term (≥ 4 years) |

| Oncology R&D pipelines & label-expansion | +1.5% | North America & EU; spill-over to APAC | Medium term (2-4 years) |

| Rapid genericisation in emerging markets | +1.2% | APAC core; Latin America; MEA | Short term (≤ 2 years) |

| High-dose cisplatin-sparing regimens | +0.9% | North America & EU; emerging in APAC | Medium term (2-4 years) |

| Localised API incentives in India & China | +0.8% | APAC core; global supply impact | Short term (≤ 2 years) |

| Nano-liposomal and depot delivery platforms | +1.0% | North America & EU; early APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Solid-Tumor Cancers

Rising incidence of pancreatic, lung, breast and bladder cancers is widening the addressable population for gemcitabine, especially in low- and middle-income countries undergoing rapid urbanisation. The compound’s proven efficacy across these tumors keeps it embedded in first-line and adjuvant protocols, and recent approvals pairing gemcitabine with novel checkpoint inhibitors further cement its role in multimodal therapy. Younger patient cohorts in Asia and Africa are contributing incremental volume, driving demand for paediatric-friendly dosing formats and protocols that mitigate haematological toxicity.

Intensifying Oncology R&D Pipelines & Label-Expansion Trials

More than 700 active or planned studies globally are exploring gemcitabine combinations, leveraging its well-characterised safety record to accelerate development timelines [1]European Medicines Agency, “EU Clinical Trials Register,” europa.eu . Roche’s Phase III STARGLO trial showed a 41% reduction in mortality when Columvi was combined with gemcitabine-oxaliplatin, securing European approval in April 2025 [2]F. Hoffmann-La Roche Ltd, "European Commission approves Roche’s Columvi as the first bispecific antibody for diffuse large B-cell lymphoma after initial therapy," roche.com. Such successes illustrate how synergistic regimens can extend the molecule’s lifecycle, open orphan indications, and justify premium pricing even after base-compound patent expiry.

Rapid Genericisation Driving Price Elasticity in Emerging Markets

Generic launches by Teva, Dr. Reddy’s and Sun Pharma are pushing unit prices down while unlocking new patient volumes in public health systems across APAC and Latin America. India’s Production-Linked Incentive scheme and three new Bulk Drug Parks are lowering API costs, enabling aggressive tenders that expand access without eroding total value because of higher utilisation. Premium ready-to-use formats, however, remain insulated from deep discounting, sustaining healthy margins for differentiated players.

Use in Novel Nano-Liposomal and Depot Delivery Platforms

Liposomal encapsulation exploits the enhanced permeation and retention effect for tumour-selective delivery, boosting intratumoral drug levels while sparing healthy tissue [3]Matthew S. Gatto, "Targeted Liposomal Drug Delivery: Overview of the Current Applications and Challenges," MDPI, mdpi.com. Microfluidics technologies now deliver tight control over particle size, scalability and reproducibility, addressing historical CMC hurdles. Stimuli-responsive carriers and theranostic constructs integrating imaging contrast agents enable real-time tracking of gemcitabine release, a feature attracting venture funding and partnership deals across North American biotech hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmacovigilance & cytotoxic regulations | -0.8% | Global – highest in North America & EU | Long term (≥ 4 years) |

| Severe haematological toxicity | -0.7% | Global – higher in resource-constrained | Long term (≥ 4 years) |

| Tender-based price erosion | -0.9% | Global – highest in emerging markets | Short term (≤ 2 years) |

| Displacement by immune checkpoint inhibitors | -0.6% | North America & EU core; rising in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Pharmacovigilance & Cytotoxic Handling Regulations

FDA crack-downs on sterile injectables led to 30 ANDA withdrawals in 2024, underscoring scrutiny on manufacturing controls for cytotoxics. Hospitals must invest in closed-system transfer devices, negative-pressure rooms and specialised waste streams, raising total treatment costs and discouraging smaller facilities in Latin America and Africa from stocking gemcitabine. Compliance heterogeneity across jurisdictions complicates multi-site production and forces generic entrants to allocate significant capex before first revenue.

Competitive Displacement by Immune Checkpoint Inhibitors

Pembrolizumab, nivolumab and durvalumab have rewritten care standards in several solid tumors, prompting clinicians to reassess chemotherapy intensity. Yet cost constraints and limited single-agent efficacy in pancreatic cancer keep gemcitabine relevant, especially in doublets that balance cytotoxic debulking with immune activation. Small-molecule checkpoint inhibitors in early development may strike better pharmacoeconomic ratios, but until they mature, gemcitabine remains a pragmatic backbone in price-sensitive health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready-to-Use Solutions Drive Premium Positioning

In 2025 injections dominated with a 71.56% gemcitabine hydrochloride market share, supported by universal familiarity in oncology pharmacies. Ready-to-use solutions, although niche, are forecast to advance at 7.71% CAGR, riding workflow efficiency, reduced error risk and lower exposure events for pharmacy staff. The launch of Infugem showed that hospitals will pay a premium for reconstitution-free bags, especially amid persistent staff shortages. Manufacturing sterility and shelf-life hurdles deter rapid generic entry, allowing innovators to defend price differentials and capture incremental value even in tender markets.

Workflow data from large US oncology networks show a 28% cut in compounding time when ready-to-use bags replace powder vials, freeing infusion chairs for higher throughput and raising revenue per square foot of clinic space. This operational upside, combined with lower hazardous waste volumes, resonates with value-analysis committees struggling to reconcile staff safety mandates with budget ceilings. As more hospital groups bundle drug acquisition costs with total labour savings, premium ready-to-use formats are expected to gain ground, lifting the overall gemcitabine hydrochloride market.

By Indication: NSCLC Growth Outpaces Pancreatic Dominance

Pancreatic protocols continued to command 39.22% of gemcitabine hydrochloride market size in 2025, reflecting entrenched first-line status and limited immunotherapy alternatives. NSCLC, however, is projected to register the stoutest 7.63% CAGR, leveraged by combination regimens pairing gemcitabine with PD-1/L1 antibodies or EGFR inhibitors in biomarker-selected populations. Growing evidence from Chinese and Brazilian real-world datasets indicates improved progression-free survival when gemcitabine anchors platinum-doublet maintenance, driving formulary inclusions.

As precision diagnostics proliferate, clinicians identify micro-segments—such as KRAS-mutated, PD-L1-low cases—where gemcitabine-based doublets outperform expensive monotherapies in quality-adjusted life-year terms. Orphan designations in biliary tract and gallbladder cancers offer further upside by granting market exclusivity for new fixed-dose combinations, translating into higher average selling prices. Consequently, the indication mix tilts progressively towards NSCLC and rare tumors, diversifying revenue streams away from pancreatic dependence.

By Patient Age Group: Pediatric Expansion Challenges Adult Dominance

Adults represented 67.05% of gemcitabine hydrochloride market share in 2025, aligned with the age clustering of solid-tumor incidence. Yet paediatrics will be the fastest-growing segment at 7.74% CAGR, fuelled by expanding data sets in malignant rhabdoid tumours, medulloblastoma and osteosarcoma. Regulatory incentives—priority review vouchers and 6-month exclusivity extensions—are encouraging sponsors to invest in child-specific PK/PD studies and palatable low-volume presentations.

Formulation science must confront small-volume accuracy, excipient tolerability and long-term stability, but payoff potential is underscored by the readiness of children’s hospitals in the US, EU and Japan to adopt regimens that show even incremental survival benefits. Age-tailored supportive care protocols that mitigate gemcitabine-induced neutropenia also foster clinician confidence, smoothing the path for broader paediatric uptake and supporting a wider risk-benefit acceptance curve.

Geography Analysis

North America commanded 40.58% of the gemcitabine hydrochloride market in 2025 on the back of premium branded pricing, extensive clinical trial pipelines and payer coverage that cushions hospital formulary budgets. Continued domestic manufacturing investment—exemplified by Lilly’s USD 50 billion multi-site expansion—reinforces supply security and keeps the region a priority launch market. Nonetheless, chronic shortages of companion agents such as cisplatin have spotlighted gemcitabine as a substitution backbone, driving episodic demand spikes and creating openings for agile suppliers.

Asia-Pacific is forecast to deliver the most robust 7.82% CAGR through 2031 as cancer incidence climbs and regional governments court API self-sufficiency. India’s three Bulk Drug Parks and China’s 169-acre WuXi STA site illustrate policy-backed scale advantages that translate to cost-competitive exports. Concurrently, local regulatory harmonisation with ICH guidelines is elevating quality benchmarks, shrinking the trust gap between Western buyers and Asian producers and accelerating ANDA approvals for APAC-sourced injectables.

Europe maintains a sizeable share owing to high per-patient spending and early adoption of innovative combinations such as Columvi-gemcitabine-oxaliplatin authorised in April 2025. Stringent pharmacovigilance keeps average selling prices above global means, offsetting lower procedure volumes compared with the US and China. Moreover, collaborative procurement under the EU Joint Clinical Assessment is expected to expand access while safeguarding margins for quality-verified suppliers, preserving a stable revenue pillar for multinational and specialty firms alike.

Competitive Landscape

Competitive intensity is moderate: originator companies still own differentiated formulations while a widening pool of Indian and Chinese generics competes on vials. Cheplapharm’s worldwide rights to Gemzar outside South Korea, acquired from Eli Lilly in December 2024, exemplify the carve-out model whereby specialty firms exploit mature oncology brands that no longer fit big-pharma pipelines. Such deals unlock residual brand equity while freeing innovators to reinvest in immuno-oncology assets.

Fresenius Kabi posted 11% revenue growth in 2024, helped by double-digit expansion of its injectables franchise, demonstrating how integrated API-to-fill-finish capabilities can shield earnings amid price erosion. Pfizer continues to capitalise on its early-mover advantage in ready-to-use gemcitabine with Infugem, defended by proprietary formulation IP that raises the entry bar for copycats. Meanwhile, emerging Chinese CDMOs are partnering with Western biotech firms on liposomal and polymer-conjugated variants, seeking joint FDA filings that secure 3-7 year data exclusivity.

Supply chain resilience remains a differentiator. USP’s Medicine Supply Map assigns gemcitabine a low 15% vulnerability score, yet cascading shortages of complementary agents elevate its strategic importance. Companies with dual-source API networks, on-site sterility labs and validated cold-chain fleets are better positioned to win hospital tenders when competitors encounter regulatory or logistical setbacks. Forward-looking players are also investing in digital-traceability solutions to meet forthcoming DSCSA serialisation milestones, further reinforcing moat effects.

Gemcitabine Hydrochloride Industry Leaders

-

Eli Lilly & Co.

-

Apotex Inc.

-

Fressenius Kabi USA

-

Pfizer Inc. (Hospira Inc.)

-

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Genentech received an FDA Complete Response Letter for Columvi plus gemcitabine-oxaliplatin in relapsed or refractory DLBCL; the agency cited underlying data insufficiency despite a 41% death-risk reduction.

- April 2025: European Commission approved Roche’s Columvi combined with gemcitabine-oxaliplatin as the first bispecific for DLBCL following positive STARGLO results.

- April 2025: FDA cleared penpulimab-kcqx with cisplatin/carboplatin and gemcitabine for first-line recurrent or metastatic nasopharyngeal carcinoma.

- September 2024: RenovoRx scaled production of its RenovoCath catheter to meet demand for TAMP delivery of intra-arterial gemcitabine in locally advanced pancreatic cancer.

Global Gemcitabine Hydrochloride Market Report Scope

As per the scope of the market, gemcitabine hydrochloride is the antimetabolite-antineoplastic agent with synthetic pyrimidine nucleoside. It can be used with other oncology agents in combination, such as paclitaxel, cisplatin, and others.

The Gemcitabine Hydrochloride Market is segmented By Product Type (Injection, Solution), By Indication (Breast Cancer, Non-small Cell Lung Cancer, Pancreatic Cancer, Others), and by Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD million) for the above segments.

| Injection |

| Ready-to-use IV Solution |

| Pancreatic Cancer |

| Non-Small Cell Lung Cancer |

| Breast Cancer |

| Others |

| Adults |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Injection | |

| Ready-to-use IV Solution | ||

| By Indication | Pancreatic Cancer | |

| Non-Small Cell Lung Cancer | ||

| Breast Cancer | ||

| Others | ||

| By Patient Age Group | Adults | |

| Geriatric | ||

| Pediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current gemcitabine hydrochloride market size and projected growth?

The market is valued at USD 885.44 million in 2026 and is expected to reach USD 1.22 billion by 2031, reflecting a 6.68% CAGR.

Which region leads gemcitabine hydrochloride market share today?

North America holds 40.58% of global share, driven by premium pricing, robust clinical trials, and strong manufacturing infrastructure.

Which formulation segment is expanding the fastest?

Ready-to-use IV solutions are projected to grow at 7.71% CAGR owing to workflow efficiency and reduced contamination risk.

Why is the pediatric segment gaining attention?

It is forecast to expand at 7.74% CAGR as new clinical evidence in childhood tumors and regulatory incentives spur development of child-friendly formulations.

What impact does immunotherapy have on gemcitabine demand?

Immune checkpoint inhibitors exert competitive pressure; however, combination regimens often retain gemcitabine due to cost advantages and synergistic efficacy, limiting outright displacement.

How vulnerable is the gemcitabine supply chain?

USP assigns a low 15% vulnerability score, yet recent shortages of companion agents make secure gemcitabine sourcing strategically important for oncology centers.

Page last updated on: