Hybrid Label Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

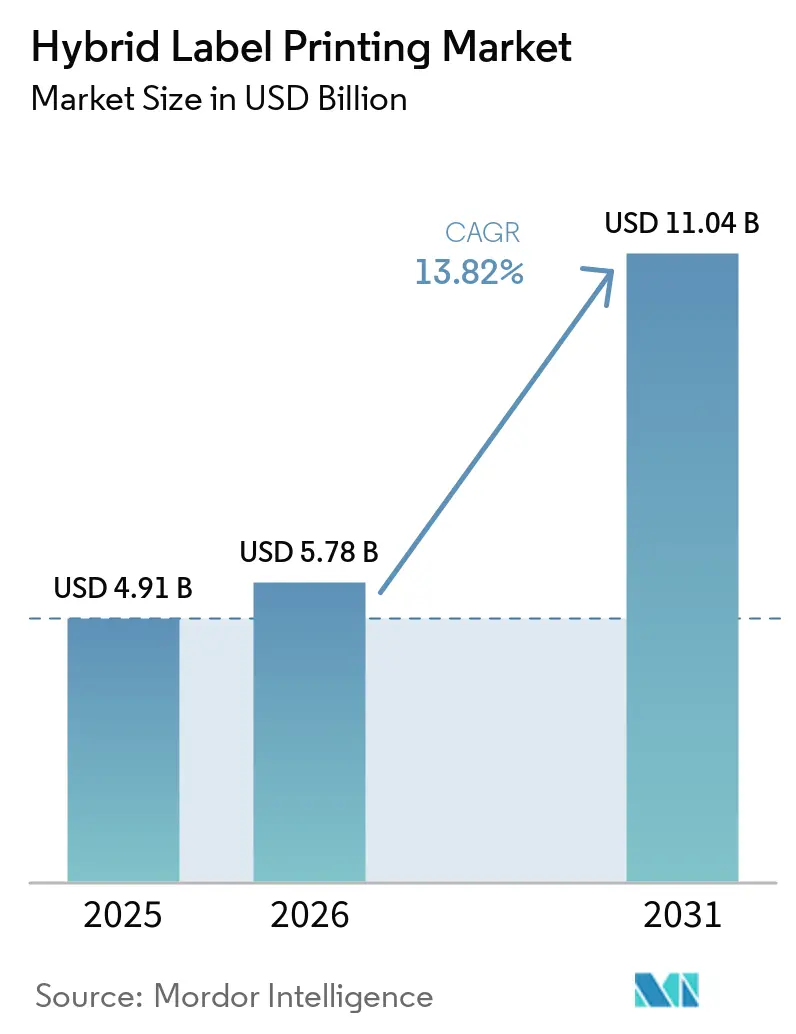

| Market Size (2026) | USD 5.78 Billion |

| Market Size (2031) | USD 11.04 Billion |

| Growth Rate (2026 - 2031) | 13.82% CAGR |

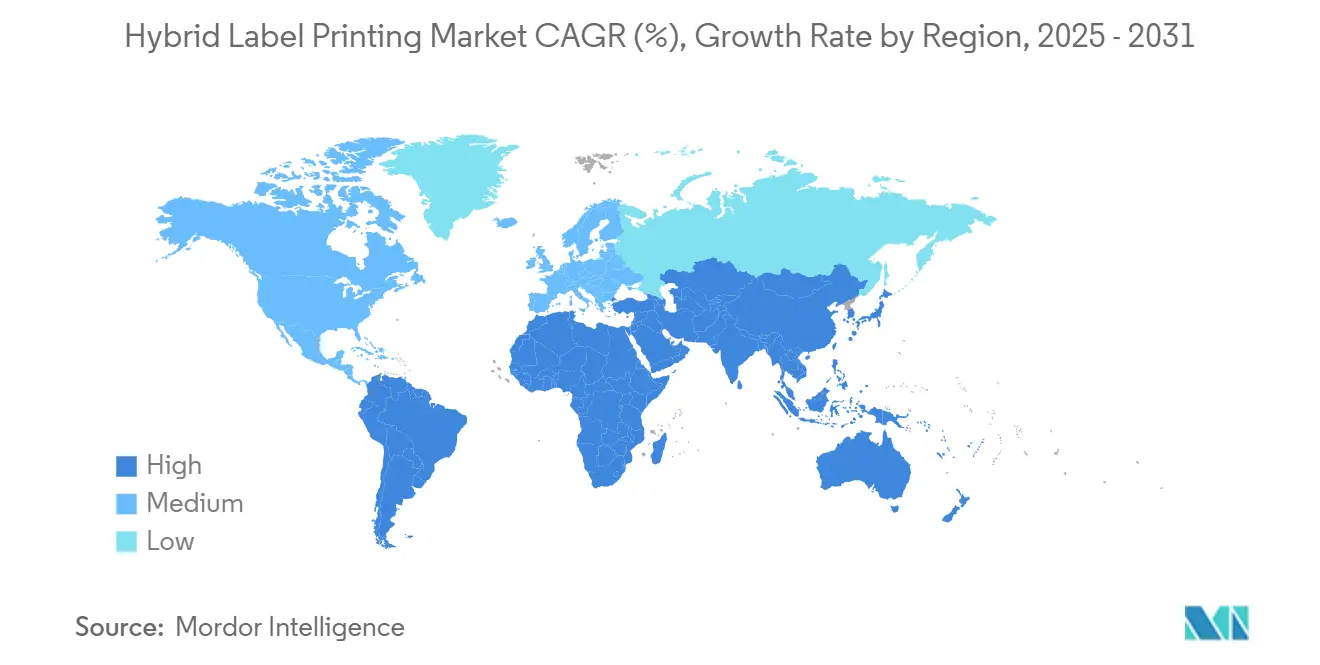

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Label Printing Market Analysis by Mordor Intelligence

The hybrid label printing market size was valued at USD 4.91 billion in 2025 and is estimated to grow from USD 5.78 billion in 2026 to reach USD 11.04 billion by 2031, at a CAGR of 13.82% during the forecast period (2026-2031). Rapid SKU fragmentation, brand-owner demand for mass personalization, and the technical parity now achieved between UV-inkjet and flexographic processes have realigned converter economics in favor of hybrid workflows. Wide-web platforms capable of handling larger formats for e-commerce logistics are expanding fastest, while low-migration LED ink sets have moved from niche to mainstream as regulators tighten chemical migration thresholds for food and pharmaceuticals. Asia-Pacific’s lead is cemented by concentrated manufacturing clusters, fast-growing online retail, and national Industry 4.0 programs that subsidize digital upgrades, whereas North America leverages stringent serialization laws to accelerate system replacements. Meanwhile, ongoing shortages of operators skilled in both flexo and digital disciplines, as well as price volatility for electronic components, temper near-term growth but do not alter the market’s long-term trajectory toward high-volume, fully integrated production lines.

Key Report Takeaways

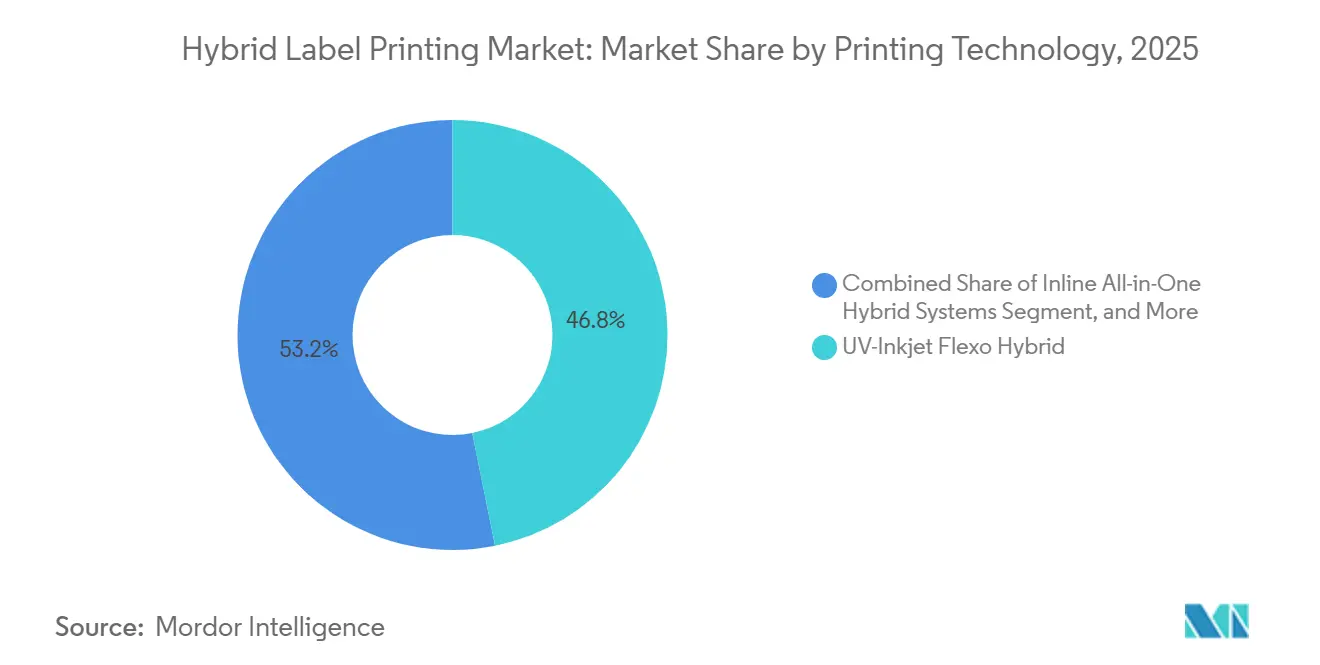

- By printing technology, UV-inkjet flexo hybrid systems captured 46.83% of the hybrid label printing market share in 2025.

- By press type, the hybrid label printing market size for wide-web platforms is projected to grow at a 15.18% CAGR between 2026-2031.

- By ink type, UV-LED curable formulations captured 53.41% of the hybrid label printing market share in 2025.

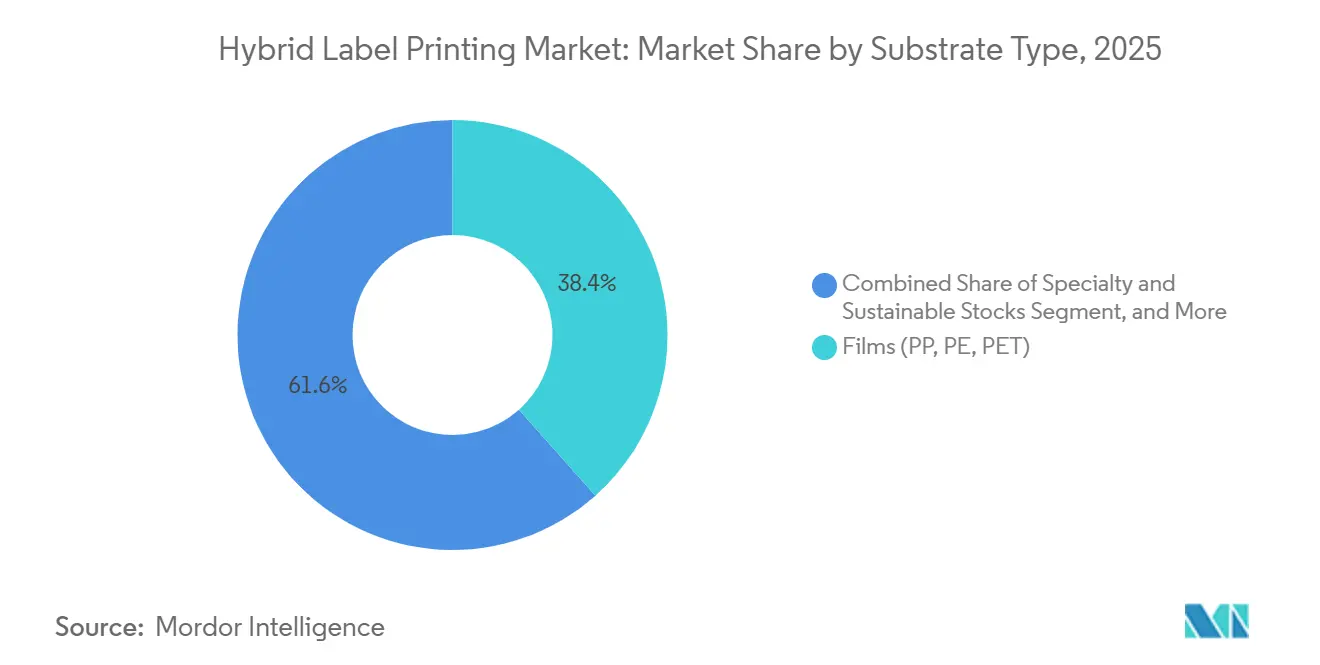

- By substrate type, the hybrid label printing market size for specialty and sustainable materials is projected to grow at a 15.78% CAGR between 2026-2031.

- By end-user industry, food applications captured 52.28% of the hybrid label printing market share in 2025.

- By geography, the hybrid label printing market size for Asia-Pacific is projected to grow at a 15.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Label Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-run SKU proliferation and personalization demand | +2.3% | Global, highest in North America and Europe | Medium term (2–4 years) |

| Rising quality parity of UV-inkjet with flexo | +2.1% | Global, led by Asia-Pacific | Short term (≤ 2 years) |

| Converter pushes for single-pass inline finishing | +1.8% | North America and Europe core, expanding to Asia-Pacific | Medium term (2–4 years) |

| Hybrid presses embedded with AI predictive maintenance | +1.5% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Leasing models lowering the Capex hurdle | +1.2% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Brand-owner demand for QR-enabled digital product passports | +1.4% | Europe is leading, expanding globally | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Short-Run SKU Proliferation and Personalization Demands

Consumer-goods suppliers now juggle hundreds of product variants, slashing minimum order quantities by 60% since 2024 and making runs of under 1,000 meters routine. Hybrid presses excel under this workload because they seamlessly switch between digital and flexo printing on the fly without requiring recalibration, thereby preserving unit economics across variable-length jobs. Europe's incoming Digital Product Passport scheme accelerates uptake by hard-coding variable data into packaging legislation. Brands that previously printed region-specific promotions annually now refresh graphics quarterly, a cadence only feasible with integrated hybrid workflows. In tandem, beverage marketers have linked QR codes on shrink sleeves to loyalty programs, raising converter demand for precise, in-register digital embellishment within flexographic supply chains.

Rising Quality Parity of UV-Inkjet with Flexo

Fujifilm Dimatix heads operating at 1,200 × 1,200 dpi and ±5 µm drop accuracy have erased the historic gap in opacity and fine text clarity between inkjet and anilox-based printing.[1]Fujifilm Holdings Corporation, “Annual Report 2024,” fujifilm.com This parity unlocks pharmaceutical and cosmetic labels that previously defaulted to offset or gravure printing. Converters now run full-bleed color, microtext, and barcodes in one pass, confident that inspectors cannot distinguish between them. The removal of quality compromises also simplifies brand audits, driving hybrid adoption into highly regulated supply chains across Asia, where audits are rigorous yet speed expectations remain high.

Converter Push for Single-Pass Inline Finishing

Hybrid lines fitted with die-cutters, laminators, and automatic inspection cameras now complete jobs 40% faster than multi-station workflows, slashing labor by the same margin. North American converters serving the nutraceutical and ready-to-eat meal markets cite single-pass coating and die-cutting as decisive factors for achieving two-day turnaround service-level agreements. Inline finishing also reduces the risk of cross-contamination because rolls remain on a single spindle, a prime concern for allergen-free food producers. Financially, the consolidation of stages yields floor-space savings that operators are reallocating to warehousing, thereby improving just-in-time logistics for raw materials.

Hybrid Presses Embedded with AI Predictive Maintenance

Machine learning now predicts component failures up to 72 hours before stoppage, reducing unplanned downtime by 35% on early HP Indigo deployments. Algorithms monitor flexo doctor-blade wear and inkjet jetting consistency concurrently, scheduling service during planned idle windows. Pharmaceutical converters using this capability in France reported 98% line availability during blister-pack serialization campaigns. Over time, the data lake produced by networked presses is expected to feed prescriptive analytics that adjust tension settings in real-time, further reducing waste and makeready sheets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure | -1.8% | Global, highest impact in emerging markets | Short term (≤ 2 years) |

| Shortage of Dual-Skilled (Flexo + Digital) Operators | -1.5% | North America and Europe primarily | Medium term (2-4 years) |

| Supply-Risk on Platinum-Based Silicone Liners | -0.9% | Global, concentrated supplier base | Long term (≥ 4 years) |

| Tariff Volatility on Electronic Components for Inkjet Heads | -1.1% | Global trade-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Fully integrated hybrid platforms range from USD 2 million to USD 8 million, a 40-60% premium over single-technology presses, keeping many mid-size converters on the sidelines. Although leasing schemes from Heidelberger Druckmaschinen cut up-front payments by 70%, interest expenses still erode early cash flows. Smaller Asian converters often pool volumes into consortium-owned equipment parks, but ownership fragmentation complicates preventive maintenance planning and lengthens ROI timelines. Emerging-market governments have started offering accelerated depreciation to offset Capex, yet such incentives remain patchy.

Shortage of Dual-Skilled (Flexo and Digital) Operators

Hybrid systems require crews to be competent in anilox roll maintenance and RIP-based color management; however, 65% of converters report gaps in this dual skill set. Apprenticeship programs last 18-24 months, delaying productivity gains from new installs. U.S. operators commanding 25-35% wage premiums over single-technology peers have inflated operating costs, compelling firms to accelerate investments in closed-loop color automation. Europe faces a similar squeeze as retirement rates among veteran flexographers outpace the influx of new talent, placing a ceiling on press utilization, even where equipment funding is secure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Inline Systems Drive Innovation

In 2025, UV-inkjet flexo hybrids accounted for a 46.83% share of the hybrid label printing market, reinforcing their status as the baseline architecture for converters seeking multi-process agility. Inline all-in-one hybrids, though smaller today, are forecast to log a 16.21% CAGR to 2031, indicating the segment’s pivot toward tightly integrated, software-orchestrated production cells. Notably, electrophotographic hybrids find sustained interest in luxury cosmetics where opaque white layers and metallic foils require ultra-precise registration. Retrofittable digital bars, priced under USD 400,000 per station, provide smaller firms with an incremental pathway into variable-data jobs without triggering full-line replacement costs.

AI-powered vision systems embedded in these platforms already pare waste by 15-20% compared with legacy offline inspection. That efficiency further solidifies the hybrid label printing market's position in quality-critical verticals, especially the pharmaceutical industry. Over the forecast horizon, software upgrades rather than hardware swaps will deliver most productivity gains, reinforcing the subscription-based revenue models adopted by leading OEMs. Consequently, the hybrid label printing market occupies a decisive position in technology roadmaps across every tier of converter, from boutique craft-beer labelers to multinational packaging conglomerates.

By Press Type: Wide-Web Dominance Accelerates

Wide-web hybrids accounted for 48.26% of revenue in 2025 and are projected to expand at a 15.18% CAGR through 2031, underscoring their central role in large-format logistics labels, which have grown 30% in area since 2025 Narrow-web units, while ceding share, remain indispensable for electronics and medical devices that demand micron-level registration. Mid-web presses bridge these extremes, serving converters that require format agility without incurring wide-web floor-space penalties, thus anchoring a competitive mid-market niche.

E-commerce warehouses adopting RFID-enabled shipping labels are prompting wide-web investments that unlock two-lane printing, doubling throughput without new headcount. Narrow-web players counter by automating web-guiding and turret-rewind systems, achieving an operator-to-press ratio of 1:3 and thereby trimming labor costs. Mid-web platforms are increasingly acting as transitional assets for firms scaling from artisanal runs to industrial work, supporting the hybrid label printing market share ecosystem by keeping the technology ladder financially accessible.

By Ink Type: Low-Migration Formulations Surge

UV-LED curables constituted 53.41% of ink volume in 2025 and remain the de facto standard for fast-curing, energy-efficient production. Low-migration LED sets, however, are expected to record a 14.35% CAGR, driven by FDA rule changes that narrow the permissible extractables in food contact layers. Water-based inkjet chemistries, which are slower to cure, are still gaining traction where sustainability metrics outweigh speed, especially among European organic food brands. LED dual-cure flexo inks occupy a hybrid space, marrying UV stability with flexo cost structures.

As curing energy for LED systems drops below 1 W/cm², converters can print on heat-sensitive bio-films without shrinkage, broadening material choice and reinforcing the hybrid label printing industry’s green credentials. Suppliers are racing to certify ink sets against EuPIA and Nestlé standards, using blockchain certificates to prove batch-level compliance. Regulatory convergence across the United States and Europe ensures that investments in low-migration technology yield global benefits, solidifying the hybrid label printing market as a compliance hedge for multinational brand owners.

By Substrate Type: Sustainability Drives Material Innovation

Films made from PP, PE, and PET comprise 38.43% of the 2025 print volume, benefiting from superior barrier properties in the food and beverage segments. Specialty and sustainable substrates, led by post-consumer recycled films and bio-based polymers, are expected to accelerate at a 15.78% CAGR as corporate ESG targets become more stringent. Paper and paperboard remain cost-efficient for dry-goods labelling, whereas metallic foils retain importance for top-shelf spirits and nutraceuticals.

Brands now mandate recycled content minimums of 30% by weight, steering converters toward hybrid-compatible adhesives that maintain lay-flatness on thinner gauge films. The Ellen MacArthur Foundation reports that such eco-design policies have doubled demand for recyclable facestocks since 2024. Concurrently, linerless label trials using silicone-free backings aim to cut platinum consumption, mitigating one of the supply-risk restraints on the hybrid label printing market. Such substrate diversification embeds resilience into raw-material sourcing while amplifying the sustainability narrative central to premium brand positioning.

By End-User Industry: Pharmaceutical Compliance Accelerates Growth

Food applications generated 52.28% of revenue in 2025 and continue to absorb capacity as allergen and nutritional disclosures become more granular. The pharmaceutical segment is expected to outpace all others, with a 16.34% CAGR to 2031, driven by global serialization mandates, such as the EU Falsified Medicines Directive. Personal care labels, which demand rapid artwork revisions and photo-realistic finishes, constitute a lucrative mid-volume sweet spot, while beverages capitalize on seasonal promotions that hybrid workflows execute efficiently.

Industrial chemicals and lubricants, exposed to harsh operating environments, lean on hybrid platforms for durable varnishes and scuff-resistant films, consolidating an ancillary but stable revenue stream. Across segments, the hybrid label printing market size will increasingly hinge on its ability to embed machine-readable codes within graphics, enabling supply-chain transparency from factory to curbside recycling. This data-first paradigm solidifies hybrid technology as the cornerstone for brand integrity and regulatory compliance across all use cases.

Geography Analysis

Asia-Pacific generated 35.27% of 2025 revenue and is poised for a 15.25% CAGR, driven by China’s manufacturing scale, India’s pharmaceutical expansion, and state-backed smart factory initiatives across ASEAN economies. Chinese converters deploy wide-web hybrids to serve cross-border e-commerce platforms that ship millions of parcels daily, while Indian drug exporters invest in low-migration systems to meet U.S. FDA import standards. Japan and South Korea contribute high-end R&D, especially in AI-enabled vision systems and ceramic inkjet nozzle technologies, amplifying regional innovation cycles.[2]U.S. Food and Drug Administration, “Food Safety Modernization Act Implementation Timeline,” fda.gov

North America, though mature, sustains healthy upgrade momentum as the Food Safety Modernization Act compels real-time traceability, encouraging converters to retire legacy flexo lines in favor of hybrid platforms capable of variable QR code placement. The United States further benefits from large-scale contract packaging hubs in the Midwest, which consolidate pharmaceutical and nutraceutical label runs under one roof. Mexico emerges as a near-shoring winner, importing hybrid equipment duty-free under USMCA rules and exporting finished goods into the wider region.

Europe’s growth reflects policy-led digitalization: the Digital Product Passport, REACH chemicals management, and extended producer responsibility fees all favor hybrid workflows for on-demand variable data. Germany anchors equipment adoption through its sizable Mittelstand converter base, while the United Kingdom’s life-science corridor boosts pharmaceutical demand. Eastern Europe offers cost-competitive labor but adopts top-tier machinery to differentiate against Western rivals, reinforcing a pan-European upgrade cycle that sustains the hybrid label printing market through 2031.

Competitive Landscape

The hybrid label printing market remains moderately fragmented, with the top five suppliers accounting for roughly 45% of combined revenue in 2024. HP’s acquisition of Industrial Inkjet Ltd. augments its polymer chemistries for low-migration workflows, narrowing gaps with Bobst and Heidelberg, which integrate proprietary AI modules into flexo backbones. Bobst’s USD 120 million Singapore plant will localize production and shorten lead times for Asia-Pacific converters, intensifying regional competition. Meanwhile, Fujifilm’s Samba G5L heads raise productivity ceilings, pushing rivals to accelerate nozzle-density roadmaps.

Smaller innovators, such as Nilpeter and Durst, target modular kits and sustainability certifications to carve out defensible niches. Intellectual property filings surged past 200 in 2024 as vendors patented AI-driven color correction and LED dual-cure ink sets.[3]World Intellectual Property Organization, “Patent Activity Report: Printing Technologies,” wipo.int Supply-chain vulnerabilities persist around platinum-based liners and custom ASICs for printhead drivers, prompting OEMs to dual-source or redesign around commodity components, a strategy that could rewrite cost structures and widen the field for new entrants.

Strategic alliances dominate go-to-market tactics: Mark Andy’s collaboration with Domino bakes serialized coding into hybrid lines, while Konica Minolta’s German innovation center partners with sustainability-minded substrate suppliers to future-proof material compatibility. Collectively, these maneuvers consolidate an ecosystem approach where hardware, ink, software, and service bundles differentiate offerings, heightening switching costs and shaping customer loyalty.

Hybrid Label Printing Industry Leaders

Bobst Group SA

Heidelberger Druckmaschinen AG

Mark Andy Inc.

Durst Group AG

HP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: HP Inc. completed the USD 85 million acquisition of Industrial Inkjet Ltd., adding low-migration ink expertise for pharmaceutical packaging.

- September 2025: Bobst Group announced a USD 120 million hybrid press plant in Singapore, with production slated for Q2 2026.

- August 2025: Fujifilm launched the Dimatix Samba G5L printhead series, boosting throughput by 30% versus prior models.

- July 2025: Mark Andy partnered with Domino Printing Sciences to embed inline serialization into Digital Series hybrid lines.

Global Hybrid Label Printing Market Report Scope

| Flexo-UV Inkjet Hybrid |

| Flexo-Electrophotographic Hybrid |

| Retrofitted Digital Print Bars |

| Inline All-in-One Hybrid Systems |

| Other Printing Technologies |

| Narrow-web |

| Mid-web |

| Wide-web |

| UV-LED Curable Inks |

| Water-based Inkjet Inks |

| LED Dual-Cure Flexo Inks |

| Low-migration Inks |

| Paper and Paperboard |

| Films (PP, PE, PET) |

| Metallic and Foil |

| Specialty and Sustainable Stocks |

| Other Substrates |

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Printing Technology | Flexo-UV Inkjet Hybrid | ||

| Flexo-Electrophotographic Hybrid | |||

| Retrofitted Digital Print Bars | |||

| Inline All-in-One Hybrid Systems | |||

| Other Printing Technologies | |||

| By Press Type | Narrow-web | ||

| Mid-web | |||

| Wide-web | |||

| By Ink Type | UV-LED Curable Inks | ||

| Water-based Inkjet Inks | |||

| LED Dual-Cure Flexo Inks | |||

| Low-migration Inks | |||

| By Substrates | Paper and Paperboard | ||

| Films (PP, PE, PET) | |||

| Metallic and Foil | |||

| Specialty and Sustainable Stocks | |||

| Other Substrates | |||

| By End-user Industry | Food | ||

| Beverages | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the hybrid label printing market?

The market is valued at USD 5.78 billion in 2026 and is projected to reach USD 11.04 billion by 2031.

Which region leads to revenue for hybrid label printing?

The Asia-Pacific region held 35.27% of global revenue in 2025 and is also the fastest-growing region, with a 15.25% CAGR.

Why are hybrid presses gaining popularity in pharmaceutical packaging?

Tight serialization laws and low-migration ink requirements favor hybrid systems that combine variable data capability with the durability of flexography.

How does AI contribute to hybrid label printing efficiency?

Predictive-maintenance algorithms cut unplanned downtime by 35%, while real-time vision systems lower waste by 15-20%.

Which ink type shows the fastest growth?

Low-migration LED inks lead growth at a 14.35% CAGR, driven by stricter food and drug safety regulations.

What is the primary barrier to hybrid label press adoption?

High initial capital expenditure, ranging from USD 2 million to USD 8 million per line, remains the primary hurdle, despite the emergence of leasing models.

Page last updated on: