Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.18 Billion |

| Market Size (2026) | USD 12.49 Billion |

| Market Size (2031) | USD 14.49 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

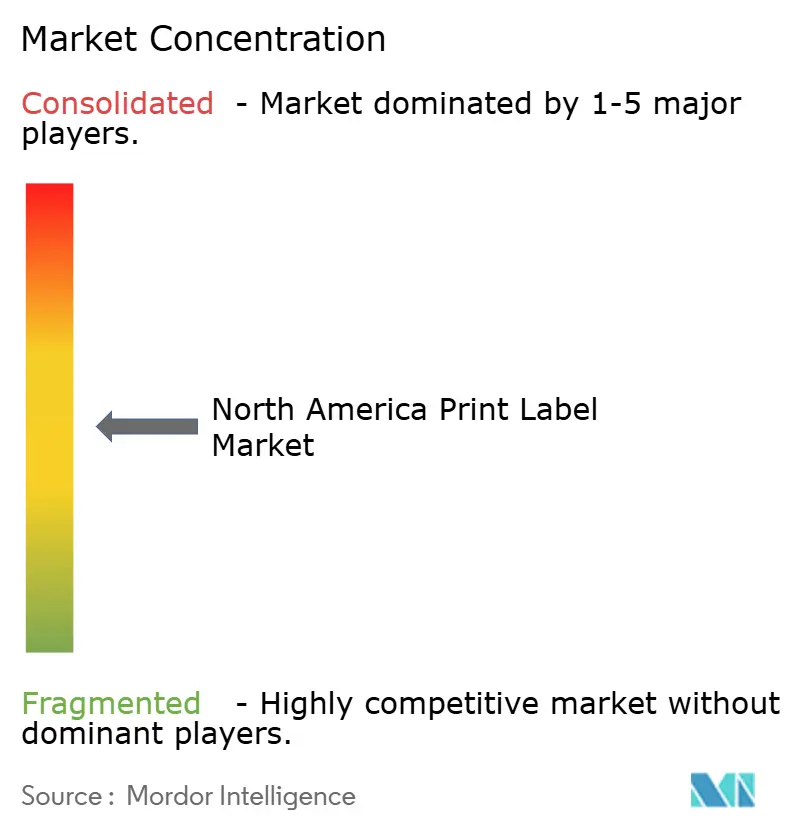

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Print Label Market Analysis by Mordor Intelligence

The North America print label market size is expected to increase from USD 12.18 billion in 2025 to USD 12.49 billion in 2026 and reach USD 14.49 billion by 2031, growing at a CAGR of 3.02% over 2026-2031. The outlook reflects stable replacement demand from packaged food and beverage lines, coupled with rising variable-data orders tied to e-commerce shipping labels. Converters are investing in digital presses that shorten changeover time and eliminate plate costs, a shift reinforced by brand owners that refresh SKUs every quarter to remain visible on omnichannel shelves. Regulatory pressure is steering ink systems toward water-based and ultraviolet-curable chemistries that meet tighter volatile organic compound limits, while healthcare mandates for unique device identification are lifting demand for serialized, tamper-evident constructions. Despite expanding volumes, mid-tier converters face margin compression when raw-material prices spike, prompting further consolidation among regional players that lack purchasing leverage.

Key Report Takeaways

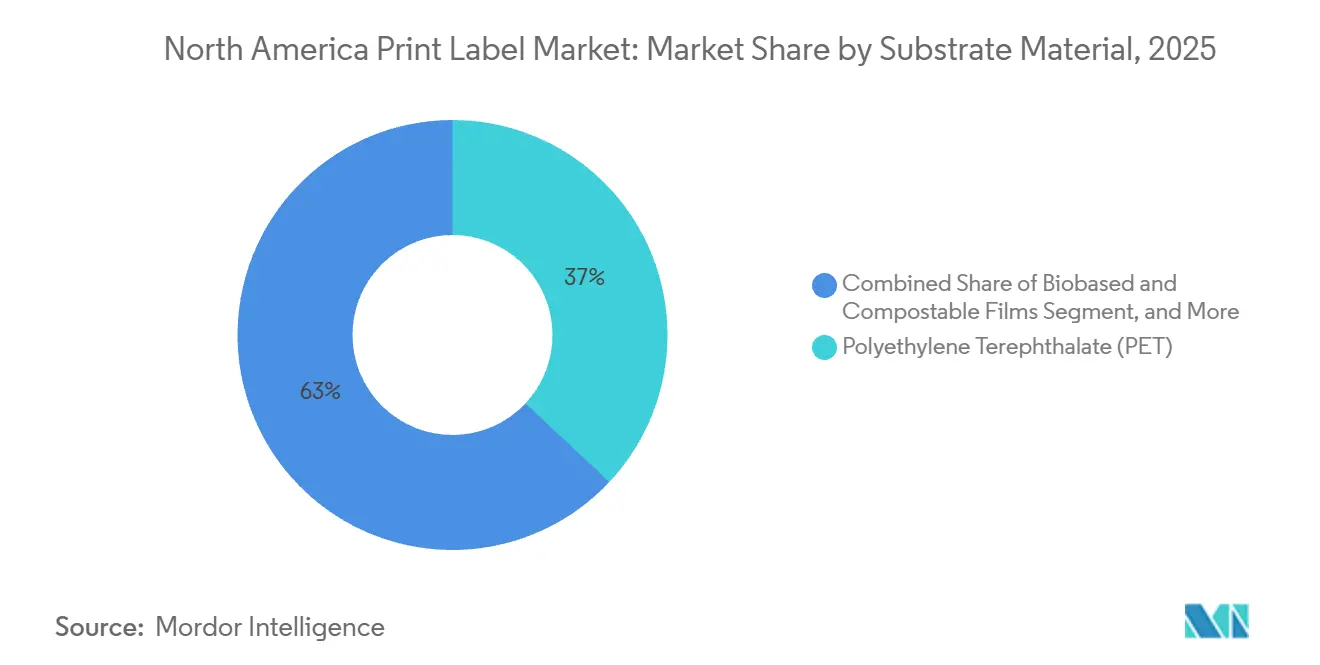

- By substrate material, polyethylene terephthalate held the largest 36.98% North America print label market share in 2025, while biobased and compostable films are projected to register the fastest 4.56% CAGR through 2031.

- By print technology, flexography accounted for 44.96% of market share in 2025, whereas digital printing is forecast to post the highest 4.32% CAGR over 2026-2031.

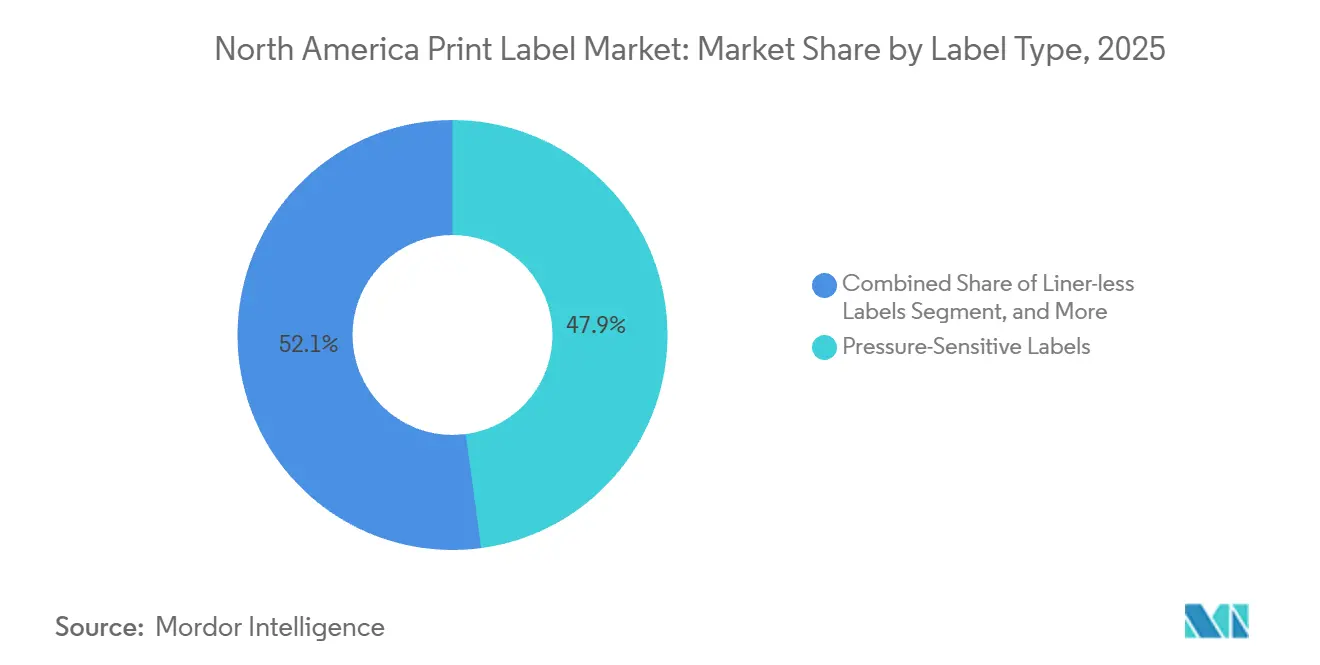

- By label type, pressure-sensitive constructions commanded 47.87% of market share in 2025, yet liner-less formats are expected to advance at the quickest 4.48% CAGR during the forecast period.

- By end-user industry, food applications led with a 29.79% share in 2025; healthcare and pharmaceuticals represent the fastest-growing vertical, projected at a 4.71% CAGR to 2031.

- By geography, the United States dominated with 75.16% of market share in 2025, while Mexico is anticipated to expand at the region’s strongest 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Print Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Digital Print Technologies | +0.8% | United States and Canada | Medium term (2-4 years) |

| Surge In Variable Data Printing for E-Commerce Logistics | +0.7% | United States fulfillment hubs | Short term (≤ 2 years) |

| Sustainability-Driven Switch to Liner-Less and Shrink-Sleeve Formats | +0.6% | North America, led by California and select Canadian provinces | Long term (≥ 4 years) |

| Healthcare UDI-Labeling Mandates | +0.5% | United States with spill-over to Mexican exporters | Medium term (2-4 years) |

| AI-Enabled Print Workflow Automation | +0.4% | Multi-site converters across North America | Long term (≥ 4 years) |

| Brand Protection and Anti-Counterfeit Features Integration | +0.3% | Pharmaceuticals, spirits, cosmetics across the region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Digital Print Technologies

Digital presses are changing the economics of the North America print label market by making runs under 5 000 linear feet financially viable. RR Donnelley installed an HP Indigo 120K press in June 2025, pairing it with robotic material handling to streamline short-run production.[1]RR Donnelley, “RRD Completes Digital Transformation of Georgia Facility,” RRD.COM Cimpress committed in May 2025 to add up to 20 more HP Indigo units across its network, signaling confidence in personalized packaging demand through 2027.[2]Cimpress plc, “Indigo Fleet Expansion Announcement,” CIMPRESS.COM Taylor Corporation’s in-house data pegs the digital break-even point versus flexography at roughly 3 000 feet, down from 8 000 feet five years ago. These economics allow smaller converters to compete on 48-hour turnaround times that national retailers increasingly expect. The flexibility of digital platforms also supports serialization, unique QR codes, and augmented-reality triggers that are impractical on analog lines.

Surge in Variable Data Printing for E-commerce Logistics

Rapid expansion of online retail has multiplied the number of shipping labels that require unique barcodes, return data, and branded messaging. Major U.S. third-party logistics operators now specify radio-frequency identification (RFID)- enabled labels to automate pallet sortation, a requirement accelerated by Amazon’s mandate that inbound pallets carry RFID tags from 2025. Avery Dennison’s APR-recognized mono-material RFID label, introduced in June 2025, demonstrates how converters are merging sustainability with smart-label functionality. The boom in serialized labels obliges converters to deploy digital front-end software capable of ingesting high-volume data streams directly from customer enterprise systems. In parallel, fulfillment centers prefer liner-less formats that reduce waste on high-speed applicators, reinforcing volume growth for direct-wound constructions.

Sustainability-Driven Switch to Liner-Less and Shrink-Sleeve Formats

Brand owners are pivoting toward formats that reduce waste and simplify recycling, a trend especially visible in jurisdictions with extended producer responsibility laws. California’s SB 54 imposes escalating fees on packaging components that cannot enter established recycling streams, thereby penalizing silicone-coated release liners.[3]State of California, “SB 54 Extended Producer Responsibility Law,” CA.GOV UPM Raflatac’s liner-less range eliminates the liner entirely and lowers packaging mass up to 50% per unit, gaining adoption in fresh produce and meat channels. Shrink sleeves, now produced in polyethylene terephthalate glycol-modified formulations that pass compatibility tests in PET recycling, offer 360-degree graphics without compromising post-consumer processing. Compostable substrates from TIPA, certified under ASTM D6400 and EN 13432, attract premium organic food brands even though resin costs remain higher than petroleum-based films. Transition costs include specialized applicators and heat-tunnel upgrades that can deter smaller bottlers, yet life-cycle assessments increasingly justify the capital outlay.

Healthcare UDI-Labeling Mandates

Full enforcement of U.S. Food and Drug Administration unique device identification rules under 21 CFR Part 801 is stimulating advanced label specifications. Medical device firms must now apply GS1-compliant barcodes linking each package to the Global UDI Database, driving demand for high-resolution digital printing that accommodates frequent lot changes. Biogen disclosed a USD 12 million spend on serialization infrastructure in its 2024 annual report, covering label-verification cameras and data-management software. Pharmaceutical producers handling biologics stored at −80 °C also require adhesives with glass-transition points below −40 °C, favoring acrylic-based systems recommended by RxSource technical guidance. Converters that certify materials under good manufacturing practice protocols gain a pricing premium, which offsets the higher cost of cryogenic-grade facestocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Durability in Extreme Cold-Chain Applications | -0.4% | United States and Canada, focused on biologics distribution | Medium term (2-4 years) |

| Supply Volatility of Specialty Label-Stock Papers | -0.5% | Region-wide shortages in release-liner grades | Short term (≤ 2 years) |

| Capital-Intensive Transition from Analog to Digital Presses | -0.3% | Mid-tier converters across the United States and Canada | Medium term (2-4 years) |

| Stringent VOC and Ink-Migration Regulations Tightening in 2026 | -0.4% | United States, especially California and northeastern states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inadequate Durability in Extreme Cold-Chain Applications

Messenger RNA vaccines and cell therapies shipped at ultra-low temperatures have exposed adhesive and facestock failures within the North America print label market. RxSource identified delamination and barcode fading during freeze-thaw cycles and recommends acrylic systems with sub-40 °C glass-transition points plus polypropylene facestocks that resist embrittlement. FDA good manufacturing practice rules obligate labels to remain legible throughout shelf life, elevating converters’ liability when materials fail. Biogen validates labels through 10 accelerated freeze-thaw tests at −80 °C, a protocol spreading across biotech customers. Reformulating adhesives increases material cost by up to 25%, squeezing margins on contracts already tendered at tight pricing. Niche converters able to certify cryogenic constructions capture a share in this specialized pocket of demand.

Supply Volatility of Specialty Label-Stock Papers

Closure of Pixelle Specialty Solutions’ Spring Grove, Pennsylvania mill in 2024 removed roughly 200 000 tons of coated base stock, tightening availability of wine and premium food label paper. Earlier labor action at UPM’s Finnish operations also disrupted global release-liner supply, and inventory normalization extended into 2025. North American converters scrambled to qualify alternate mills, often accepting longer lead times that complicate just-in-time production. ATP Adhesive Systems responded with a USD 50 million expansion in Kentucky to localize silicone-coated liner capacity. Even so, restricted supply enables upstream mills to quickly pass through price increases, a cost challenge that small and medium converters struggle to offset with customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: Biobased Films Gain Traction Amid PET Dominance

Polyethylene terephthalate maintained a 36.98% share of the North America print label market in 2025, supported by its toughness, transparency, and suitability for high-speed bottling. Brand owners pursuing circular-economy goals are adding biobased and compostable films that are advancing at a 4.56% CAGR, though current cost premiums confine adoption to premium organic and wellness lines. Paper retains relevance for wine and artisanal food where a natural look matters, while polypropylene dominates squeezable packaging that demands conformability. Polyvinyl chloride continues to retreat under environmental scrutiny, yet it persists in industrial chemicals where its solvent resistance remains unmatched. Association of Plastic Recyclers design protocols now influence specification sheets, encouraging converters to avoid facestocks that contaminate polyethylene recycling streams.

Supply shocks exacerbate substrate decisions. Pixelle’s mill shutdown left converters scrambling for specialty coated papers, pushing some wine brands to test textured polypropylene facestocks that mimic paper aesthetics without supply-chain risk. UPM’s expansion in North Carolina added release-liner output that partly offsets lost European tonnage, but market anxiety lingers. Beontag invested USD 40 million to install a specialty line in Ohio that localizes high-end self-adhesive materials. Smart-label growth is another driver, as RFID antennas demand substrates that limit signal attenuation; Avery Dennison’s mono-material polyethylene construction meets this need while aligning with recycler acceptance criteria.

By Print Technology: Digital Platforms Erode Flexography’s Long-Run Advantage

Flexography held 44.96% of the market share in 2025, thanks to its productivity on runs exceeding 10,000 feet and its compatibility with low-VOC water-based inks. Digital systems, led by HP Indigo, Xeikon, and inkjet hybrids, are expanding at 4.32% across 2026-2031 as converters chase orders for regional craft beer, limited-edition cosmetics, and direct-to-consumer replenishment packs. RR Donnelley’s Georgia facility integrates a new HP Indigo 120K with automated finishing, an illustration of analog and digital coexistence at scale. Cimpress’s planned fleet expansion confirms sustained appetite for personalized prints, especially across mass-customization web portals.

Offset and screen retain niche roles where metallic inks or heavy lay-downs are critical. Meanwhile, the U.S. Environmental Protection Agency will tighten 40 CFR Part 60 Subpart RR limits in 2026, pushing converters reliant on solvent inks toward UV-curable or aqueous systems. California air districts have already enacted stricter thresholds, effectively accelerating the pivot to lower-emission platforms that naturally align with digital presses. Capital remains a barrier: entry-level inkjet models cost near USD 500 000 and high-volume toner lines exceed USD 1 million, driving mergers among printers seeking economies of scale.

By Label Type: Liner-Less Constructions Challenge Pressure-Sensitive Hegemony

Pressure-sensitive designs represented 47.87% of market share in 2025, favored for their versatility on high-speed bottling and pharmaceutical lines. Liner-less alternatives are forecast to climb at 4.48% CAGR as retailers remove release-liner waste to satisfy provincial extended producer responsibility rules. UPM Raflatac’s direct-wound tapes lower per-unit packaging mass by half and meet throughput targets on rotary applicators. Shrink sleeves, which use PET-G formulations that can be recycled alongside clear PET bottles, are growing in personal care because full-body graphics stand out on crowded shelves.

Wet-glue labels linger on legacy beer lines optimized for cold glue, yet breweries upgrading equipment opt for pressure-sensitive solutions that simplify SKU proliferation. In-mold labels embed decoration during container formation, saving a secondary step and enhancing tamper evidence in dairy tubs. Multi-part tracking labels, crucial in logistics and clinical trials, leverage digital printing to embed unique IDs in tear-off slips. As RFID and near-field communication migrate into mainstream packaging, the functional divide between label genres blurs further, encouraging converters to master multiple constructions within a single workflow.

By End-User Industry: Pharmaceutical Serialization Outpaces Food Demand

Food retained 29.79% of overall market share in 2025, anchored by mandatory nutrition disclosures under 21 CFR Part 101. Healthcare labels, propelled by serialization and tamper-evident requirements, are on track for a 4.71% CAGR through 2031. Biogen’s multimillion-dollar serialization rollout exemplifies biopharma’s capital commitment to traceability. Demand also stems from cold-chain biologics that require cryogenic adhesives certified to good manufacturing practice standards. Beverage labels support frequent seasonal releases from craft brewers, which favor digitally printed pressure-sensitive stocks for flexibility.

Cosmetics testers compete on shelf impact, pushing for holographic foils and metallic spot colors that translate into premium unit pricing. Industrial users prioritize durability and Globally Harmonized System pictogram compliance, often specifying chemical-resistant screen or flexo inks. Logistics labels represent a fast-moving niche where every parcel requires a unique identifier, aligning naturally with digital workflows that print serialized barcodes in real time. Growing interest in connected packaging enabling refill reminders or authenticity validation further amplifies healthcare and premium cosmetics orders.

Geography Analysis

The United States generated 75.16% of the market share in 2025, reflecting its large consumer-goods base, advanced pharmaceutical manufacturing, and dense e-commerce fulfillment infrastructure. National converters operate multi-site networks that balance flexographic mass production with digital short-runs, and many sites are adding AI-driven scheduling systems that cut makeready waste. State-level regulation shapes substrate decisions, most notably in California, where extended producer responsibility fees accelerate the adoption of liner-less formats and recyclable PET-G shrink sleeves. Volatile organic compound rules in the Northeast further push converters toward ultraviolet-curable and water-based chemistries.

Canada maintains a smaller but sophisticated market characterized by mandatory bilingual labeling under the Consumer Packaging and Labelling Act. Provincial extended producer responsibility schemes reward recyclable substrates, and pressure-sensitive stocks that pair polyethylene facestocks with removable wash-off adhesives are gaining share in beverage applications. Domestic converters increasingly pursue liner-less investments to comply with waste-reduction benchmarks set in Ontario and British Columbia. Importantly, U.S. and Canadian food brands often print unified art that meets both English and French text requirements, so digital presses that accommodate micro-lot production minimize inventory risk.

Mexico, while a smaller share contributor today, records the region’s briskest percentage growth as nearshoring places automotive, consumer electronics, and personal-care assembly closer to North American buyers. Industrial parks in cities such as Tijuana and Monterrey recruit local label converters to supply just-in-sequence parts identification and compliance stickers. Avery Dennison opened an RFID facility in Querétaro in 2024, exceeding USD 100 million, adding regional capacity for intelligent labels serving both cross-border and South American exports. Mexican plants also print serialized barcodes for apparel bound for U.S. fulfillment centers, leveraging duty-free flows under the United States-Mexico-Canada Agreement.

Competitive Landscape

The North America print label market is moderately fragmented with players like Avery Dennison Corporation, CCL Industries Inc, and others. CCL Industries completed nine acquisitions between 2023-2025, most recently the October 2025 purchase of IDESCO Holding for CAD 19.0 million (USD 13.6 million) that expands its pharmaceutical and nutraceutical footprint. Large groups exploit procurement leverage to secure long-term film and liner contracts at stable pricing, an advantage unavailable to independent printers.

Below the tier-one firms, hundreds of regional converters have carved niches by combining digital presses, rapid art-to-press workflows, and value-added embellishments such as augmented-reality codes. Many quote 48-hour turnaround for runs under 5 000 linear feet, courting craft brewers and direct-to-consumer brands that need frequent SKU changes. Multi-Color Corporation, Brady Corporation, and WestRock Company compete chiefly on end-market specialization; for example, Brady dominates industrial durables while WestRock cross-sells labels with corrugated and folding carton programs.

Technology is an emerging wedge. World Wide Technology documented a 30% cut in setup time at a converter that deployed machine-learning algorithms for color management. HiFlow Solutions’ software automates job batching and raw-material allocation, producing 20% higher first-pass yield across pilot plants. Domino Printing’s AI-driven inspection heads verify every barcode at line speed and link quality data directly to regulatory documentation, especially valuable on healthcare lines that cannot tolerate mis-prints. Competitive intensity is poised to rise as private-equity platforms consolidate smaller shops to build regional super-networks capable of national service levels.

North America Print Label Industry Leaders

Avery Dennison Corporation

Ahlstrom-Munksjö Oyj

Brady Corporation

Cenveo Worldwide Limited

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Velocity Group acquired Label Interactive Technologies, adding digital capacity in Ontario and strengthening support for direct-to-consumer accounts.

- October 2025: CCL Industries bought IDESCO Holding for CAD 19.0 million (USD 13.6 million), expanding its specialty pharmaceutical label portfolio.

- October 2025: DecisionPoint Technologies purchased Imprint Enterprises, enhancing reach across southeastern U.S. retail and consumer-goods accounts.

- September 2025: Labelink acquired L'Empreinte, marking its fifteenth deal and boosting pressure-sensitive and shrink-sleeve output in Canada.

North America Print Label Market Report Scope

The print label is a piece of paper, plastic film, cloth, metal, or other material affixed to a container or product, on which is printed information or symbols about the product or item. There can also be information printed directly on a container or article. Print labels are the major source of communication between a company and its customers. Labels contribute significantly to how a consumer gets an idea about a particular product while looking at a product label and its impact on the consumer. Print labels are used across multiple end-user industries, including food and beverage, healthcare, cosmetics, and industrial.

The North America Print Label Market Report is Segmented by Substrate Material (Paper and Paperboard, Polyethylene Terephthalate, Polypropylene and BOPP, Polyvinyl Chloride, Biobased and Compostable Films, and Other Substrate Materials), Print Technology (Offset, Flexography, Screen, Digital Printing, and Other Print Technologies), Label Type (Wet-glued Labels, Pressure-Sensitive Labels, Liner-less Labels, In-mold Labels, Shrink Sleeve Labels, and Other Label Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care, Industrial, and Other End-user Industries), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Substrate Material

| Paper and Paperboard |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP and BOPP) |

| Polyvinyl Chloride (PVC) |

| Biobased and Compostable Films |

| Other Substrate Materials |

By Print Technology

| Offset |

| Flexography |

| Screen |

| Digital Printing |

| Other Print Technologies |

By Label Type

| Wet-glued Labels |

| Pressure-Sensitive Labels |

| Liner-less Labels |

| In-mold Labels |

| Shrink Sleeve Labels |

| Other Label Types |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Substrate Material | Paper and Paperboard |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP and BOPP) | |

| Polyvinyl Chloride (PVC) | |

| Biobased and Compostable Films | |

| Other Substrate Materials | |

| By Print Technology | Offset |

| Flexography | |

| Screen | |

| Digital Printing | |

| Other Print Technologies | |

| By Label Type | Wet-glued Labels |

| Pressure-Sensitive Labels | |

| Liner-less Labels | |

| In-mold Labels | |

| Shrink Sleeve Labels | |

| Other Label Types | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will North America print labels spending be by 2031?

It is forecast to reach USD 14.49 billion, rising at a 3.02% CAGR over 2026-2031.

Which substrate leads current demand?

Polyethylene terephthalate holds 36.98% share because it balances clarity, strength, and application speed.

What technology is growing fastest?

Digital presses, expanding at 4.32% CAGR, outpace all other print methods as converters chase short-run personalization.

Why are liner-less labels gaining momentum?

They eliminate silicone-coated release liners, reduce unit weight up to 50%, and help brand owners meet extended producer responsibility rules.

How are healthcare regulations influencing label design?

FDA serialization and unique device identification mandates drive demand for serialized barcodes, tamper evidence, and cold-chain compliant adhesives.

Page last updated on: