Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

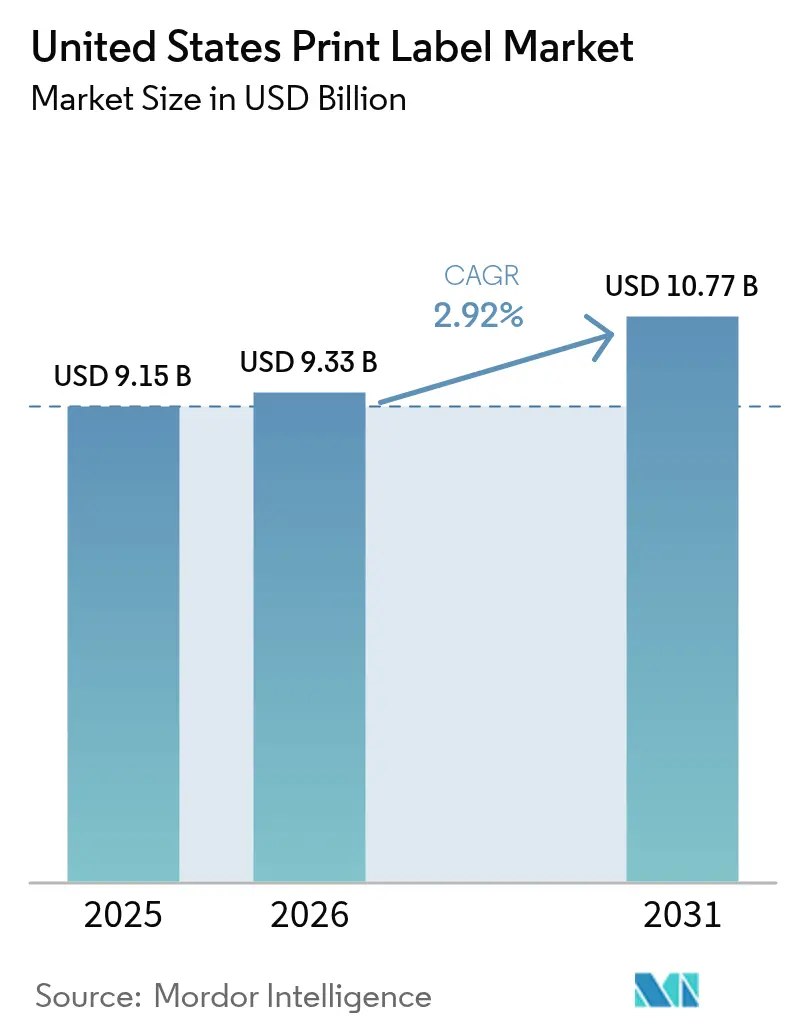

| Base Year Market Size (2025) | USD 9.15 Billion |

| Market Size (2026) | USD 9.33 Billion |

| Market Size (2031) | USD 10.77 Billion |

| Growth Rate (2026 - 2031) | 2.92% CAGR |

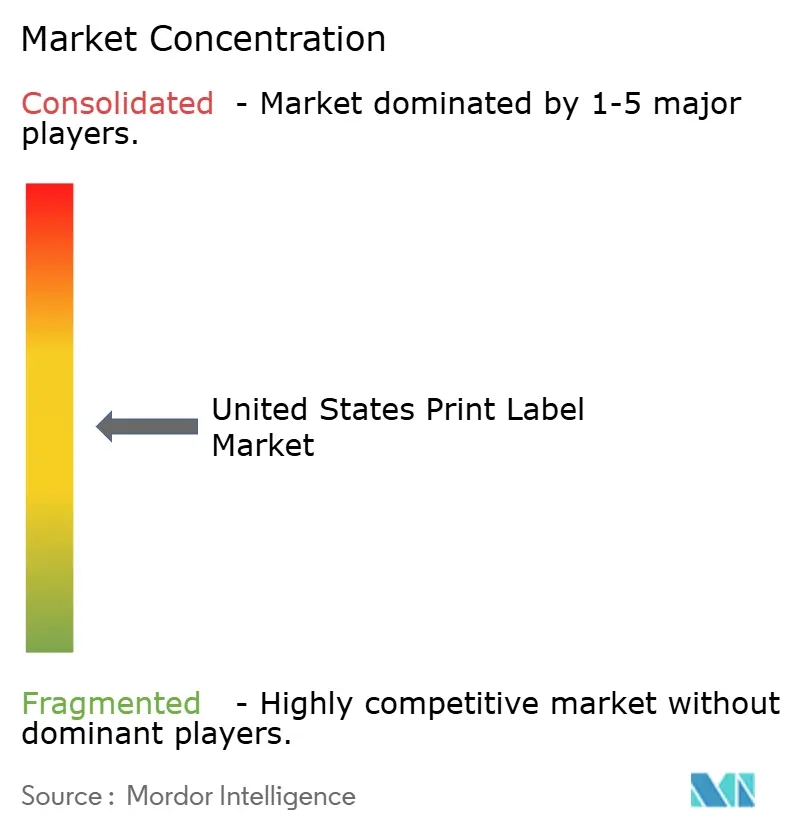

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Print Label Market Analysis by Mordor Intelligence

The United States print label market size is projected to expand from USD 9.15 billion in 2025 and USD 9.33 billion in 2026 to USD 10.77 billion by 2031, registering a CAGR of 2.92% between 2026 to 2031. Substrate leaders are feeling cost pressure from acrylic and hot-melt resins, yet converters continue to invest in recyclable polyethylene terephthalate (PET) and biobased films to comply with state Extended Producer Responsibility (EPR) mandates. Brand owners are asking for shorter runs, lot-specific variable data, and sustainability certifications, thereby accelerating the migration from analog flexography toward toner and inkjet presses that eliminate plate waste and permit 48-hour lead times. Consolidation among roughly 2,000 independent converters is reshaping the competitive balance as private-equity-backed roll-ups acquire regional shops and standardize their workflows, raising the minimum efficient scale for new entrants. At the same time, skilled-labor scarcity and volatile substrate lead times are holding back capacity additions, which explains the moderate growth trajectory relative to faster-growing Asian counterparts.

Key Report Takeaways

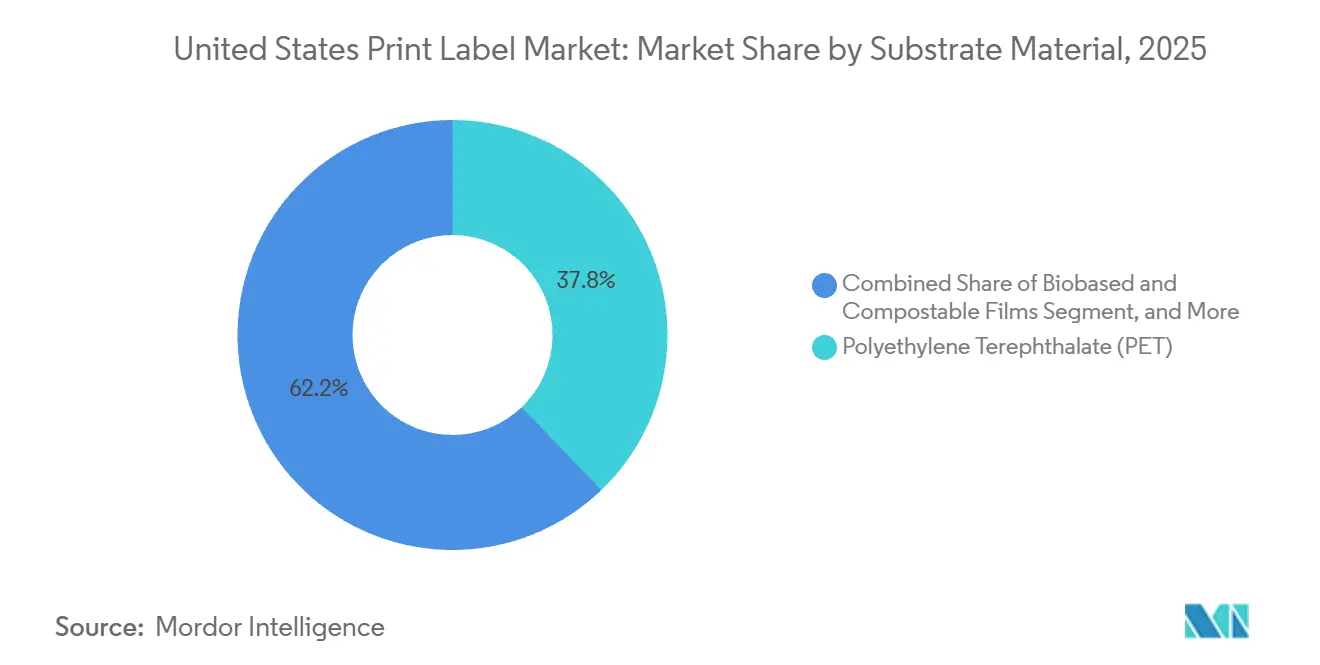

- By substrate material, PET captured 37.83% market share of the United States print label market in 2025, while biobased and compostable films are forecast to record a 3.57% CAGR through 2031.

- By print technology, flexography held 45.63% of the United States print label market share in 2025, whereas digital printing is projected to grow at a 3.21% CAGR between 2026-2031.

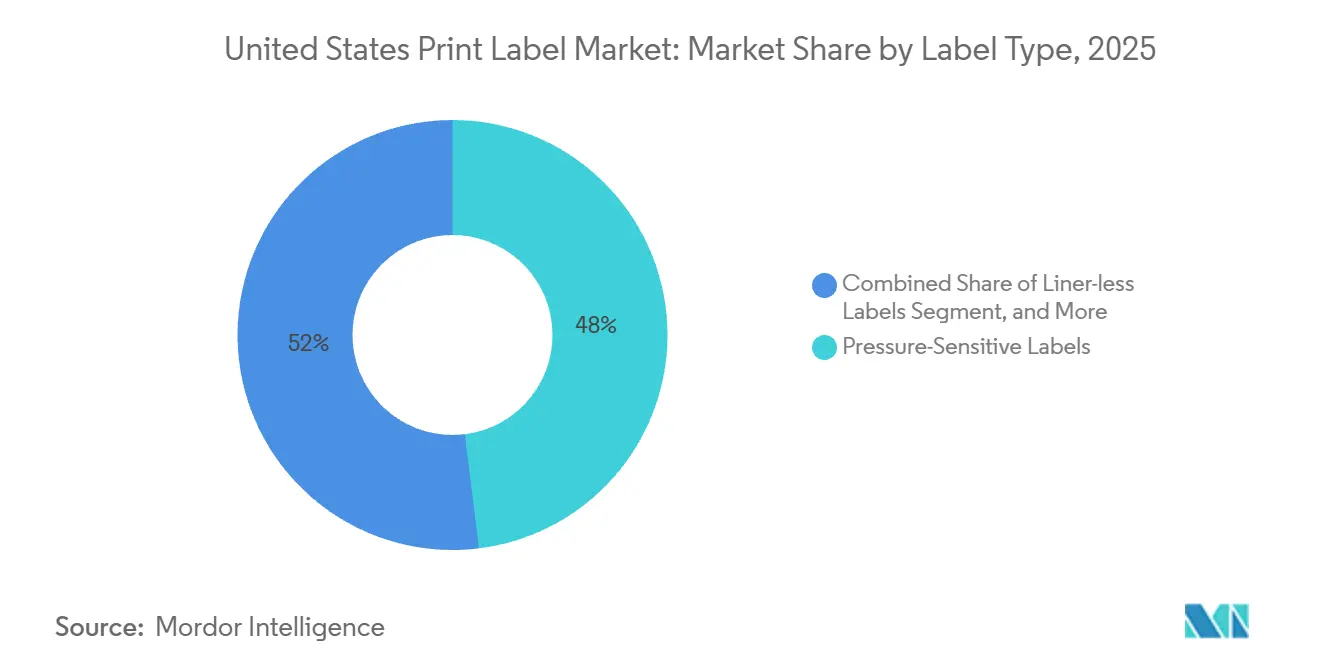

- By label type, pressure-sensitive formats led the United States print label market with 48.04% of the market in 2025, and linerless alternatives are poised for a 3.68% CAGR through 2031.

- By end-user industry, healthcare and pharmaceuticals represented a smaller base but are forecast to post a 3.45% CAGR, the fastest among all segments through 2031. whereas, Food retained the highest contribution at 28.16% in 2025, reflecting stable replenishment of packaged SKUs across U.S. retail channels.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Print Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Print Technology Penetration | +0.5% | United States—early adoption in Northeast and West Coast metro areas | Medium term (2-4 years) |

| Healthcare and Cosmetics Label Uptake | +0.4% | United States—pharmaceutical hubs in New Jersey, Massachusetts, California and cosmetics centers in New York, California | Medium term (2-4 years) |

| E-commerce and Logistics Label Volumes | +0.6% | United States—fulfillment-center corridors in Ohio, Pennsylvania, Texas, California | Short term (≤ 2 years) |

| EPR-Driven Shift to Linerless and Recyclable Labels | +0.4% | United States—led by California, Colorado, Maine, Oregon with spillover to national brands | Long term (≥ 4 years) |

| Smart and IoT Labels for Supply-Chain Traceability | +0.3% | United States—early gains in apparel, pharmaceuticals, perishable food | Long term (≥ 4 years) |

| Near-Shoring Driving Short-Run Variable-Data Print | +0.3% | United States—manufacturing reshoring in Southeast and Southwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Print Technology Penetration

Digital printing already accounts for roughly one-fifth of United States print label market value even though it represents less than one-tenth of unit volume. Converters report that most digital orders run below 5,000 pieces and ship within 48 hours, metrics unattainable for plate-based flexography, so brand owners pay a premium for rapid SKU proliferation and late-stage customization. Hybrid presses that combine flexographic white or spot colors with digital overprints allow converters to amortize their existing narrow-web infrastructure while capturing high-margin short runs. Inline finishing die-cutting, lamination, and foil stamping eliminates secondary steps, slashing makeready waste and supporting sustainability scorecards. Equipment vendors are responding with wider-web digital units, which should lower the cost per square meter and lift digital’s share of the United States print label market over the medium term.[1]Printfuture and Wissler and Partner, “Print Horizons Report,” drupa, drupa.com

Healthcare and Cosmetics Label Uptake

Serialization deadlines under the Drug Supply Chain Security Act forced pharmaceutical plants to encode National Drug Code, lot, and expiration data on every saleable unit by November 2024, providing a durable tailwind for pressure-sensitive and booklet labels that can carry significant variable information. Parallel FDA enforcement of Unique Device Identification for Class II and III medical devices expanded demand for durable labels resistant to autoclave and gamma-sterilization environments. Cosmetics brands faced new ingredient-disclosure rules under the Modernization of Cosmetics Regulation Act and California’s Right to Know statute, triggering SKU revisions and smaller-batch production. The biological therapeutics pipeline also calls for cryogenic adhesives and tamper-evident seals, lifting the value density of each label sold into this channel. Collectively these factors support the fastest end-user CAGR inside the United States print label market.

E-commerce and Logistics Label Volumes

Parcel volume handled by the United States Postal Service climbed 8% in 2024, with private carriers posting comparable growth, and each shipped item needs at least one thermal or pressure-sensitive label. Same-day delivery hubs process thousands of SKUs per hour, driving the uptake of linerless thermal media that reduce changeovers and cut waste by 30% to 40% by weight. Brands running subscription boxes and meal kits add QR codes linking to unboxing content or returns portals, jobs ideally suited to digital printing. Lithium-battery shipment regulations add separate hazmat pictograms, boosting multi-part label demand. These logistics dynamics explain the +0.6 percentage-point swing to the overall CAGR in the United States print label market.[2]United States Postal Service, “Postal Facts 2024,” usps.com

EPR-Driven Shift to Linerless and Recyclable Labels

Four U.S. states enacted EPR laws that impose escalating fees on hard-to-recycle formats, prompting national brands to specify wash-off adhesives and mono-material constructions validated by the Association of Plastic Recyclers. Wash-off pressure-sensitive labels detach at 60 °C in alkaline baths, preserving PET flake purity for bottle-to-bottle loops. Retailers value linerless alternatives because they eliminate silicone-coated release paper entirely, lowering both disposal costs and Scope 3 carbon metrics. Converter interest has spurred capital spending on specialized coating lines and adhesive chemistries optimized for high-speed logistics printers. Although dispenser compatibility remains a hurdle, the regulatory direction is clear, giving this driver a long-term tailwind inside the United States print label market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability Limits in Harsh Conditions | -0.2% | United States—industrial, automotive, outdoor uses | Medium term (2-4 years) |

| Volatile Paper and Resin Input Costs | -0.3% | United States—nationwide across all converters | Short term (≤ 2 years) |

| Skilled Narrow-Web Labor Shortages | -0.2% | United States—Midwest and Southeast corridors | Long term (≥ 4 years) |

| Recycling-Stream Fragmentation | -0.2% | United States—EPR states and municipal programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Paper and Resin Input Costs

Bleached-kraft pulp prices peaked in mid-2024 and were still 18% above 2023 averages in early 2025, while acrylic and hot-melt resin indices held 12% higher than pre-spike levels, compressing converter margins on fixed-price contracts.[3]Bureau of Labor Statistics, “Producer Price Index,” bls.gov Smaller converters without hedging programs endure working-capital swings when specialty film lead times triple and post-consumer recycled PET trades at premiums of USD 200-400 per metric ton. Inventory buffers tie up cash, limit capital upgrades, and slow the shift to sustainable materials, shaving 0.3 percentage points off the forecast CAGR for the United States print label market.

Skilled Narrow-Web Labor Shortages

Commercial-printing employment declined 3.2% between 2019-2024, and wage premiums for flexographic press operators now exceed 15% in key Midwest and Southeast clusters. With fewer apprentices entering the trade, converters delay press-line expansions and pay overtime, elevating total cost of ownership for new capacity. Automation can offset some of the gap, yet full Job Definition Format integration covers only a minority of pressrooms. Persistent talent scarcity therefore trims 0.2 percentage points from United States print label market growth over the coming four years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: PET Dominance Meets Biobased Disruption

Polyethylene terephthalate sustained a 37.83% market share in 2025, making it the anchor substrate for beverage, personal-care, and pharmaceutical applications that value clarity and recyclability. That prominence keeps PET as the single largest slice of the United States print label market size at both dollar and volume levels. Yet EPR fee structures and retailer scorecards are steering incremental growth toward polylactic-acid and cellulose-based films that meet ASTM D6400 compostability criteria. Biobased offerings are set to grow 3.57% per year to 2031, outpacing every legacy polymer. The premium they command, often 40%-60% higher than standard PET, encourages converters to carve out specialized production cells rather than cannibalize mainstream lines. Over the medium term, broader municipal composting infrastructure will determine how fast these new materials convert trial orders into baseline specifications in the United States print label market.

Investments in recyclable label technologies are picking up. Clean-flake adhesive systems now allow pressure-sensitive labels to float off during caustic washing, unlocking equivalent resin quality to virgin PET for bottle-to-bottle loops. Such innovations not only reinforce PET leadership but also protect its share against polypropylene, which suffers from lower curbside recovery rates. Looking ahead, federal recycled-content mandates, if enacted, could reprice virgin inputs and accelerate brand migration toward both post-consumer recycled PET and bio-based substitutes, reshaping the material hierarchy inside the United States print label market.

By Print Technology: Flexography’s Installed Base Versus Digital’s Agility

Flexography generated 45.63% of market share in 2025 because converters retain decades of investment in narrow-web presses, anilox inventories, and inline finishing assets. These sunk costs keep cost-per-thousand labels low on jobs beyond 10,000 units, anchoring flexo’s role in high-volume food and beverage programs that dominate the United States print label market share figure. However, digital printing’s 3.21% forecast CAGR demonstrates a clear pivot toward short runs and variable data requirements. Hybrid presses now marry flexo for solid backgrounds and white underprints with digital heads for versioning, effectively blurring the boundary between the two technologies.

The economic breakeven between flexo and digital continues to creep upward as inkjet manufacturers release wider-web models and raise maximum linear speed. Concurrently, LED-curable inks improve energy efficiency on newer flexo units, narrowing the total-cost gap. Converters that invest today in workflow automation and color-management software will capture margin from both halves of the technology split, but laggards risk ceding premium work to digitally native entrants as the United States print label market evolves.

By Label Type: Pressure-Sensitive Versatility Challenged by Linerless Efficiency

Pressure-sensitive constructions occupied 48.04% of market share in 2025, thanks to dependable application speeds above 600 units per minute and compatibility with nearly every container shape. That versatility will keep them central to the United States print label market, yet linerless rolls are the fastest-growing, with a 3.68% CAGR, propelled by retailers and carriers looking to slash waste sent to landfill. Converters are resolving lingering adhesive bleed issues by developing micro-pattern coatings and climate-controlled inventory protocols, improving machine uptime on high-speed applicators.

Shrink-sleeve labels retain share in craft beverages and personal-care promotions that leverage 360-degree decoration, but PETG and oriented polystyrene are gradually replacing polyvinyl chloride to solve recycling compatibility challenges. Traditional wet-glue paper formats hold on in beer bottling lines where capital depreciation has ended and changeover times are minimal. These sub-trends illustrate how no single format will dominate; instead, converters must maintain multi-technology portfolios to defend their slice of the United States print label market size across diverse end-use cases.

By End-User Industry: Food Stability Versus Healthcare Dynamism

Food applications accounted for 28.16% of market share in 2025, as grocery shelves require constant replenishment of branded and private-label SKUs. This segment yields high volumes yet low margins, and private-label penetration tempers unit expansion. Healthcare and pharmaceuticals, in contrast, will be the fastest-growing vertical at 3.45% CAGR through 2031 as cold-chain biologics and regulatory serialization multiply label formats per vial, carton, and shipper.

Beverage labels benefit from craft-beer proliferation and premium spirits, both of which demand tactile embellishments and variable barcodes for deposit tracking. Cosmetics grow in line with the overall United States print label market, but new ingredient disclosure rules force frequent artwork updates, favoring digital printing. Finally, industrial and logistics labels command the highest value per square meter due to their extreme durability requirements, yet volumes are smaller and cyclical, exposing converters to resin price swings and macro slowdowns.

Geography Analysis

The United States print label market is heavily concentrated in the Northeast, Midwest, and West Coast, which together represented roughly 70% of market share in 2025. These three corridors host most large food processors, pharmaceutical campuses, and consumer-goods headquarters, delivering a steady base of high-volume flexographic work. California has an outsized influence because SB 54 sets a 65% recycling or composting threshold by 2032, forcing national brands to pilot wash-off adhesives and linerless formats in the state first before rolling them out nationwide. The Northeast benefits from dense population centers and proximity to global brand owners that require multilingual artwork and frequent regulatory updates. Meanwhile, the Pacific Northwest attracts early adopters of RFID-enabled shelf tags, leveraging technology sector expertise to roll out frictionless checkout programs that drive incremental smart-label demand.

The Southeast corridor stretching from Georgia through Tennessee is the fastest-growing region thanks to reshored manufacturing in food, apparel, and home-care categories. New facilities specify digital presses that can handle small batches and multilingual packaging without expensive plate changes, thereby enlarging the digital share of the United States print label market in this geography. Texas has become a logistics powerhouse after carriers opened several megasortation hubs around Dallas-Fort Worth and Houston, lifting thermal and linerless shipping-label volumes. Mountain and Plains states remain smaller in absolute terms, yet they post above-average percentage gains tied to craft beverage and organic food brands that favor short-run digital jobs. These dynamics explain why converters continue to add narrow-web sites in Arizona, Colorado, and Utah despite the lower population density.

The Midwest faces competing trends that balance growth and constraint. On one hand, legacy flexographic press builders, large food canners, and brewing facilities provide a stable pipeline of label orders that favor long-run flexo economics. On the other hand, skilled-labor shortages are acute; wage premiums for experienced press operators rose above 15% between 2023-2025, and some converters now recruit from technical colleges as far away as Florida to staff new shifts. State-level regulations create further complexity, as California’s Proposition 65 warnings, Maine’s stewardship rules, and New York’s textile-labeling standards each impose unique copy and formatting, fragmenting SKUs and raising artwork management costs. Municipal composting pilots in Seattle, San Francisco, and Portland encourage brands to test polylactic-acid labels, yet real landfill diversion lags because many facilities cannot hold the 55 °C temperatures needed for rapid biodegradation. Collectively, these cross-currents ensure that no single region can dictate nationwide substrate or print-technology choices, compelling converters to maintain multi-plant networks and agile workflows tailored to local requirements.

Competitive Landscape

The United States print label industry posts moderate fragmentation. Approximately 2,000 independent converters populate the United States print label market, but the ownership map is shifting as private-equity roll-ups accelerate. Fortis Solutions, Resource Label Group, and Brook and Whittle alone closed more than 20 acquisitions since 2024, typically targeting family-owned shops with USD 10 million-USD 50 million in sales to build national footprints. Their combined share rose beyond 12% in 2025, forcing regional independents to consider specialty niches, geographic alliances, or outright sale. Valuation multiples climbed because strategic buyers prize converters that already run digital presses, hold pharmaceutical serialization certifications, or possess sustainability credentials aligned with EPR mandates. As scale increases, large platforms negotiate sharper substrate discounts, hedge resin exposure, and secure priority film allocations during supply crunches.

Technology adoption widens the performance gap between consolidators and stand-alone plants. Leading groups deploy end-to-end Job Definition Format workflows that integrate estimating, scheduling, color management, and inline inspection, shaving hours off makeready and enabling 48-hour ship windows demanded by e-commerce brands. They also invest in predictive-maintenance sensors and automated turret rewinders that raise uptime on both flexo and digital lines, an expense many independents cannot justify. Smaller converters typically defend share by offering ultra-responsive service to local accounts, low-volume prototype runs, or boutique embellishments such as tactile varnishes and holographic foils. Yet even those competitive moats narrow as roll-ups acquire specialty shops and standardize their processes across a multi-plant network, bringing premium finishes to a broader customer base.

Material science and smart-label integration now serve as key differentiators for growth-minded players. Avery Dennison’s CleanFlake adhesive portfolio, recognized by the Association of Plastic Recyclers, helps converters win beverage contracts that must hit rPET usage targets without compromising bottle clarity. RFID and near-field-communication inlays dropped below USD 0.05 per tag in high-volume orders, encouraging grocery and general-merchandise retailers to embed item-level intelligence that reduces shrink and supports frictionless checkout. Converters able to laminate antennas inline or insert chips during press runs capture higher value per square meter than competitors offering only printed graphics. As a result, competitive intensity will continue to hinge on the ability to pair capital scale with specialized functionality, keeping market concentration moderate even as the biggest groups enlarge their footprints.

United States Print Label Industry Leaders

Avery Dennison Corporation

Multi-Color Corporation

AWT Labels & Packaging

Taylor Corporation

CCL Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Multi-Color Corporation completed a recapitalization, reducing debt service and freeing capital for digital and sustainable-substrate investments.

- December 2025: Inovar Packaging Group acquired Enterprise Marking Products, adding flexographic capacity for industrial and automotive clients.

- October 2025: Wise Packaging Group bought Apex Color assets in Georgia, enlarging its Southeast footprint for forms and labels.

- July 2025: TedPack purchased Wisconsin operations from Fairview International, marking its first U.S. manufacturing base.

United States Print Label Market Report Scope

The print label is a piece of paper, plastic film, cloth, metal, or other material affixed to a container or product, on which is printed information or symbols about the product or item. There can also be information printed directly on a container or article. Moreover, print labels are the primary source of communication between a company and its customers. Labels contribute majorly to how a consumer perceives a product while looking at a product label and how much impact it makes on the consumer's mind. Various printing processes such as flexography, Gravure, Screen, among others, with different label formats such as wet-glue labels, linerless labels, among others, and end-user industries such as food and beverage, healthcare, cosmetics, industrial, among others, are analyzed as a part of the study.

The United States Print Label Market Report is Segmented by Substrate Material (Paper and Paperboard, PET, PP and BOPP, PVC, Biobased and Compostable Films, and Other Substrate Materials), Print Technology (Offset, Flexography, Screen, Digital Printing, and Other Technologies), Label Type (Wet-glued, Pressure-Sensitive, Liner-less, In-mold, Shrink Sleeve, and Other Label Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care, Industrial, and Other End-users).The Market Forecasts are Provided in Terms of Value (USD).

By Substrate Material

| Paper and Paperboard |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP and BOPP) |

| Polyvinyl Chloride (PVC) |

| Biobased and Compostable Films |

| Other Substrate Materials |

By Print Technology

| Offset |

| Flexography |

| Screen |

| Digital Printing |

| Other Print Technologies |

By Label Type

| Wet-glued Labels |

| Pressure-Sensitive Labels |

| Liner-less Labels |

| In-mold Labels |

| Shrink Sleeve Labels |

| Other Label Types |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

| By Substrate Material | Paper and Paperboard |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP and BOPP) | |

| Polyvinyl Chloride (PVC) | |

| Biobased and Compostable Films | |

| Other Substrate Materials | |

| By Print Technology | Offset |

| Flexography | |

| Screen | |

| Digital Printing | |

| Other Print Technologies | |

| By Label Type | Wet-glued Labels |

| Pressure-Sensitive Labels | |

| Liner-less Labels | |

| In-mold Labels | |

| Shrink Sleeve Labels | |

| Other Label Types | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries |

Key Questions Answered in the Report

How fast is digital printing growing inside the United States print label market?

Digital printing is forecast to advance at a 3.21% CAGR through 2031 as brand owners request short runs and variable data.

Which substrate commands the largest revenue share today?

PET leads with a 37.83% revenue share because of its clarity, stability, and recycling compatibility.

Why are linerless labels gaining traction?

Retailers and logistics carriers adopt linerless rolls to cut label waste by up to 40% and extend run length between applicator changeovers.

What is driving label demand in healthcare and pharmaceuticals?

Serialization under the Drug Supply Chain Security Act and biologics cold-chain growth lift healthcare label demand at a 3.45% CAGR.

How fragmented is the converter landscape?

About 2,000 independent converters exist, yet recent private-equity roll-ups have pushed the top three players to roughly 12% combined share.

Which U.S. regions show the strongest growth?

The Southeast and Texas lead growth due to reshored manufacturing and e-commerce fulfillment center expansion.

Page last updated on: