Screen Print Label Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

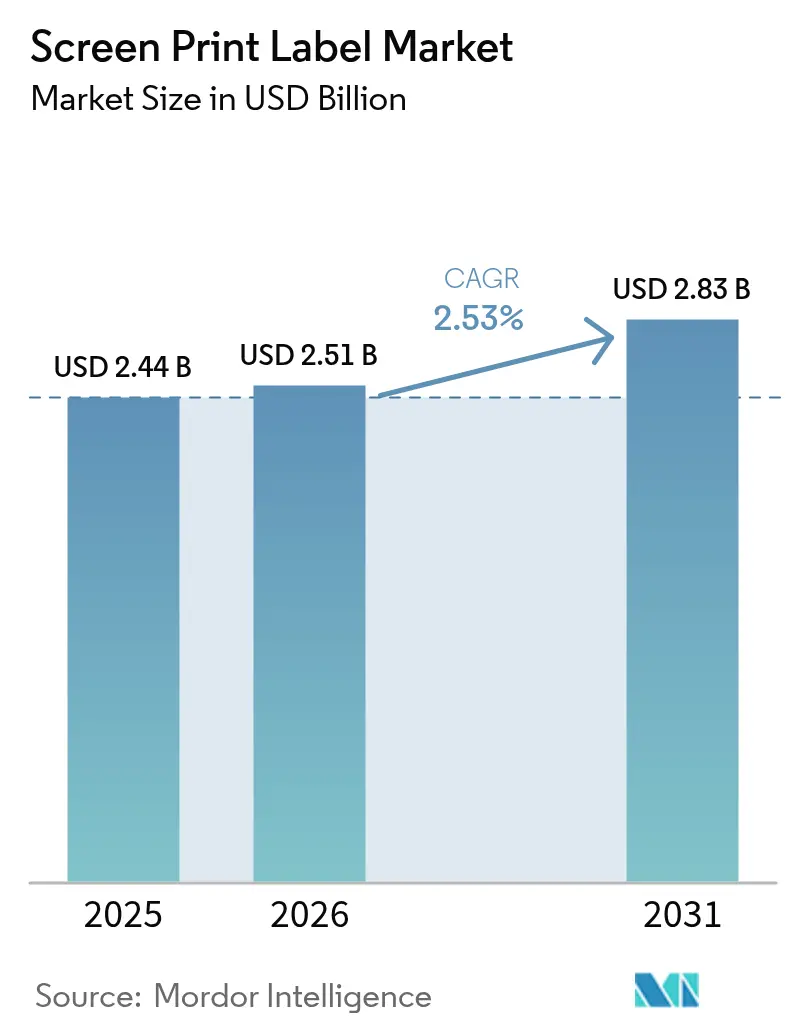

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 2.53% CAGR |

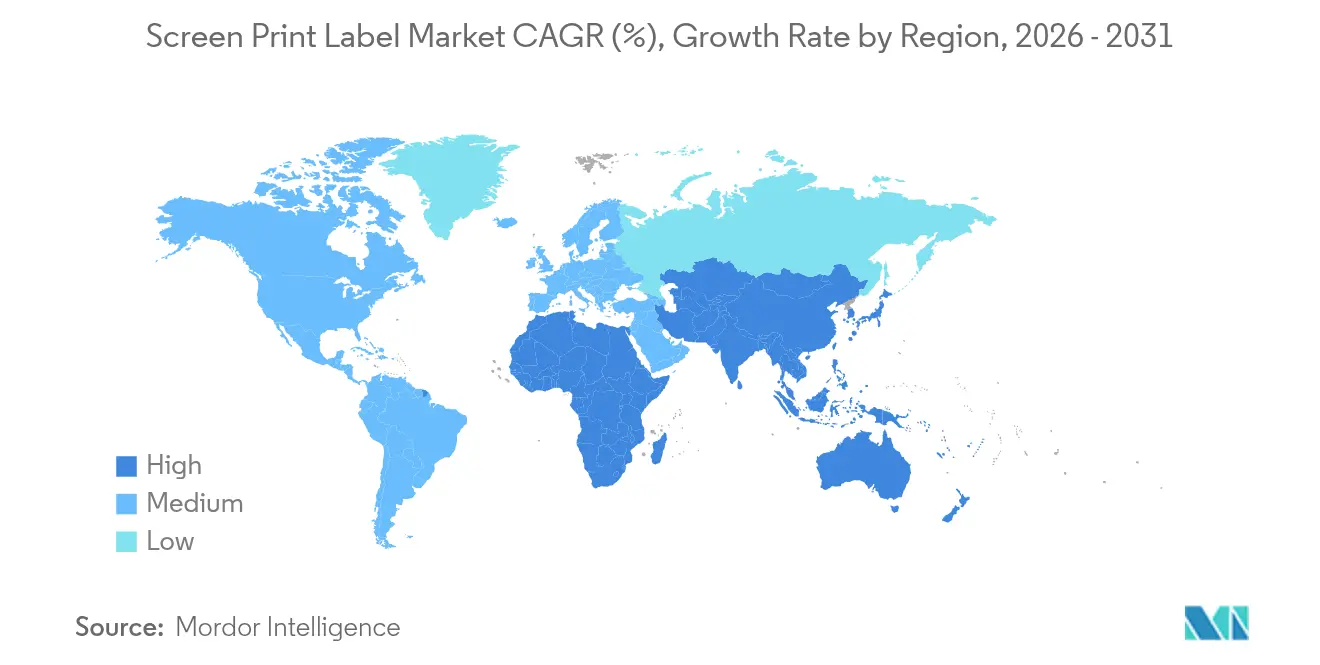

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Screen Print Label Market Analysis by Mordor Intelligence

Screen print label market size in 2026 is estimated at USD 2.51 billion, growing from 2025 value of USD 2.44 billion with 2031 projections showing USD 2.83 billion, growing at 2.53% CAGR over 2026-2031. Converters are moving away from commodity shrink-sleeve runs toward high-margin smart labels and heat-resistant constructions that sell at 20-40% premiums over standard paper. E-commerce shipping, electric vehicle battery identification, and stricter ISTA 3L humidity-cycle rules are driving investments in UV-LED screen presses that print conductive inks and embed near-field communication antennas. California’s Rule 1130 VOC cap and Asia-Pacific traceability mandates further shift demand toward durable, solvent-free inks and humidity-tolerant substrates. Consolidation is underway, yet the top five suppliers still account for only about one-third of sales, so pricing power remains limited. Capital requirements of USD 800,000-1.2 million for rotary presses, plus volatile petrochemical feedstock prices, temper near-term capacity additions.

Key Report Takeaways

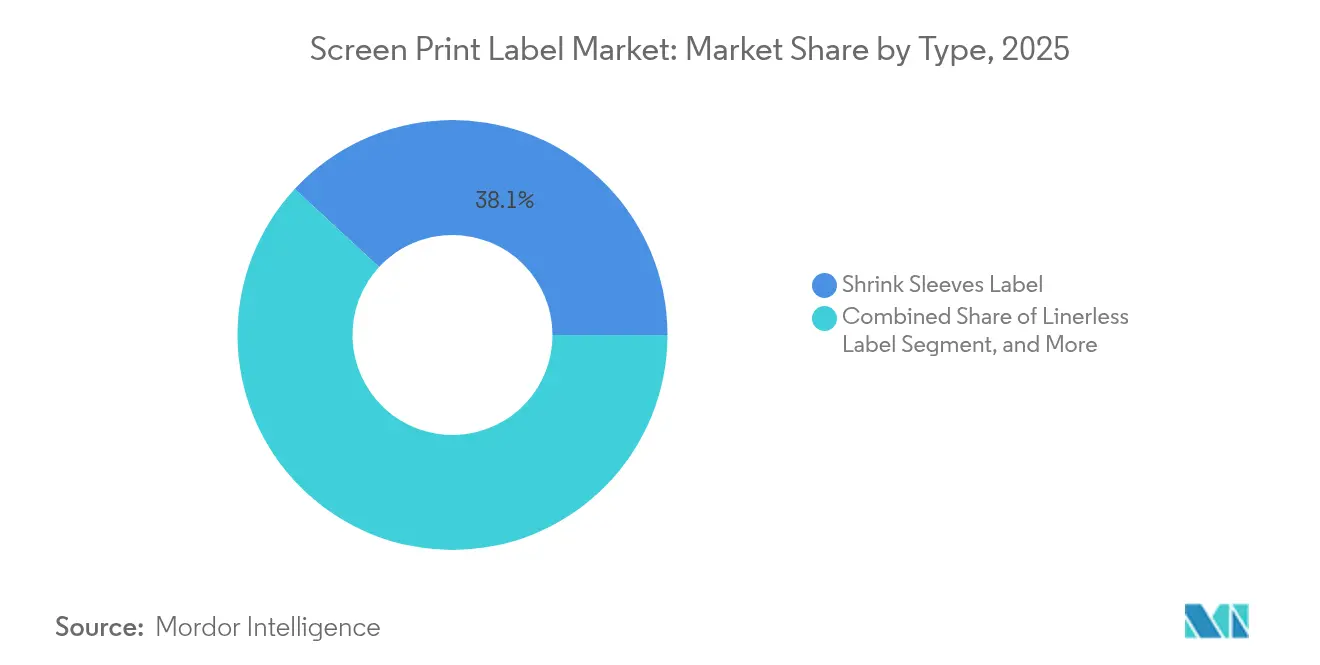

- By type, shrink sleeves led with 38.12% of the screen print label market share in 2025 and are expected to expand at a 3.38% CAGR through 2031.

- By end user, cosmetics and personal care posted the fastest growth rate of 4.38%, while food retained the largest revenue share of 28.10% in 2025.

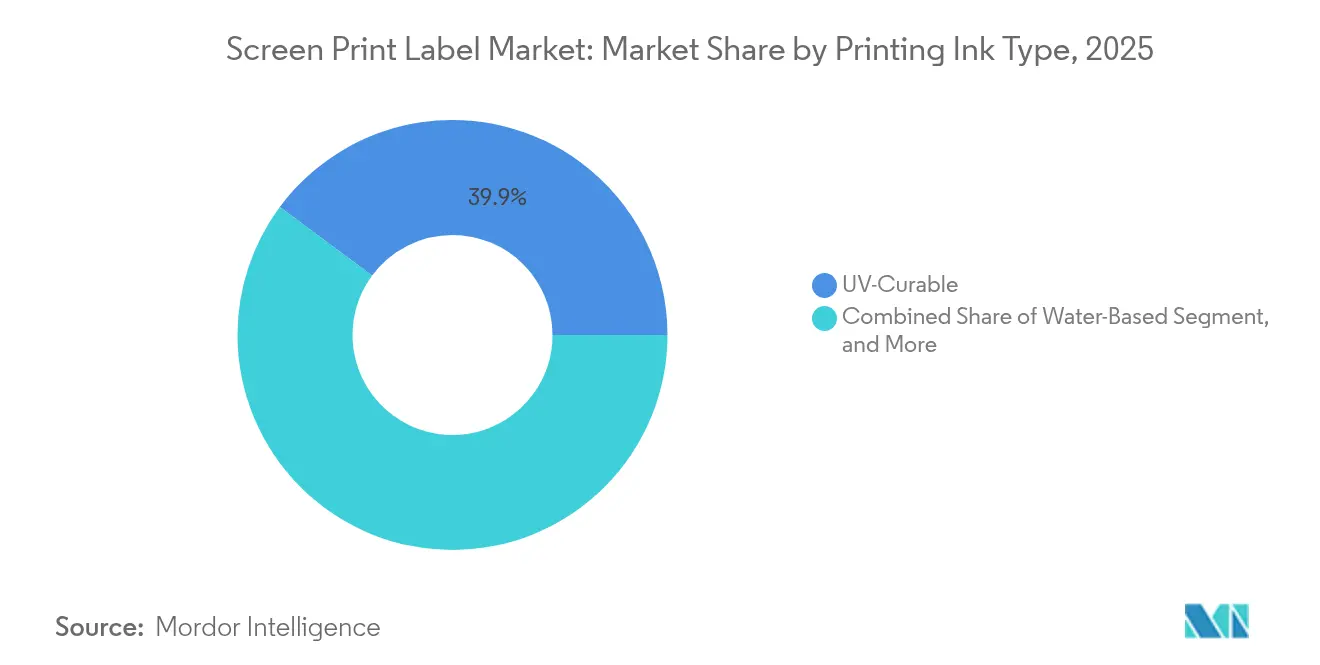

- By printing ink, UV-curable systems held 39.85% of the 2025 screen print label market share, whereas water-based inks are projected to advance at a 4.20% CAGR through 2031.

- By substrate, plastic films captured 45.98% revenue in 2025, with paper growing at a 3.62% CAGR on recycling mandates.

- By geography, North America accounted for 39.70% of 2025 revenue, while the Asia-Pacific region is forecast to grow at a 4.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Screen Print Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Durable Branding Solutions in Fast-Moving Consumer Goods | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growth of E-Commerce Requiring Robust Packaging Labels | +0.7% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Advancements in UV-LED Screen Printing Equipment | +0.6% | North America, Europe, and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Proliferation of Smart Label Features Integrating RFID and QR Codes | +0.5% | Asia-Pacific core, spillover to North America and Europe | Long term (≥ 4 years) |

| Sustainability Push Toward Solvent-Free Screen Printing Inks | +0.4% | Europe and North America, early adoption in select Asia-Pacific markets | Medium term (2-4 years) |

| Increasing Adoption of Heat-Resistant Labels in Electric Vehicle Batteries | +0.3% | Asia-Pacific and Europe, emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Durable Branding for Fast-Moving Consumer Goods

Brand owners mandate labels that survive xenon-arc exposure, repeated abrasion, and refill-pack cycles. Unilever requires color stability within Delta E 2.0 after 2,000 hours of light aging, which water-based screen inks achieve through high titanium dioxide loading. Procter and Gamble’s 50-double-rub threshold under ASTM D5264 keeps solvent-based digital inks off qualified lists. As Europe shifts to refillable packs, labels must also withstand 15-20 hot-wash cycles without delaminating.

Robust Labels for E-Commerce Fulfillment

Amazon’s 2024 packaging rules require labels that remain intact after 48 hours of water immersion, directing fulfillment centers toward polyester screen constructions with acrylic adhesives. ISTA 3L drop tests add 40-60 G shock loads, so converters raise adhesive coverage to 85% of the footprint. [1]International Safe Transit Association, “ISTA 3L Test Procedure,” ista.org FedEx specifies a minimum peel adhesion of 16 oz/in after 72 hours, which solvent-acrylic screen inks exceed by up to 35%. [2]FedEx Corporation, “Labeling Specifications,” fedex.com

Advancements in UV-LED Screen Printing Equipment

New UV-LED arrays deliver 15 W/cm² at 395 nm, curing 25 µm ink films at 80 m/min and reducing energy use by up to 85%. Lower peak web temperatures allow direct printing on polylactic-acid films that distort above 55 °C. Lamp life exceeds 20,000 hours, cutting annual downtime from 120 hours to under 15 hours and lifting overall equipment effectiveness.

Smart-Label Integration with RFID and QR Codes

Screen printing deposits conductive silver traces for near-field antennas, saving USD 0.08-0.12 per unit versus inlay attachment. GS1’s Digital Link standard packs batch data inside a single QR symbol, but a resolution of 600 dpi within a 15 mm square is essential.[3]GS1, “Digital Link Standard,” gs1.org China’s GB 38507-2020 rule requires QR codes on all packaged food by late 2025, creating hundreds of millions of square meters of extra demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of multicolor screen-printing setups | -0.5% | Global, especially emerging markets | Short term (≤ 2 years) |

| Competition from digital inkjet label printing | -0.6% | North America and Europe, rising in Asia | Medium term (2-4 years) |

| Volatile petrochemical input prices | -0.4% | Import-dependent regions | Short term (≤ 2 years) |

| VOC rules on screen-printing operations | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Multicolor Screen-Printing Setups

Rotary equipment needs USD 800,000-1.2 million upfront, four to five times the ticket price of an entry-level digital press. Make-ready still takes 45-90 minutes, delaying short runs and increasing scrap. Emerging-market converters, therefore, delay capacity additions until interest rates ease or orders shift to longer repeats.

Competition from Digital Inkjet Label Printing

Inkjet systems now reach 1,200 × 1,200 dpi at 13.5 m²/h with an ink outlay of USD 0.18-0.22 per m², which is lower than the screen’s USD 0.28-0.35 for runs under 5,000 linear meters. Piezo heads last up to 10 liters, stretching replacement cycles and narrowing the cost gap. HP’s Indigo 25K meets 97% Pantone accuracy. Yet, rub resistance remains 30-40% lower than that of UV-screen films, so screen printing still dominates shrink sleeves and heat-transfer graphics that require 200% elongation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrink Sleeves Dominate Through Full-Body Branding

Shrink sleeves accounted for 38.12% of 2025 revenue and are expected to advance at a 3.38% CAGR, helping the screen print label market outpace commodity pressure-sensitive formats. The segment benefits from 360-degree graphic coverage, steam tunnel shrinkage of up to 78%, and compatibility with irregular container designs. Energy-efficient films such as Pentalabel Boost cut steam use by 30%, shaving USD 0.008-0.012 per container. Linerless solutions lag in share but appeal to logistics customers seeking waste-free workflows. Wet-glued labels cling to legacy glass-bottle lines in beer, yet this niche is shrinking as cans gain traction. Heat-transfer decals for apparel and in-mold options for durable goods complete the mix, each serving specialized requirements that sustain price premiums.

Sustainability and authentication extend the growth runway. Screen-printed holographic foils deter counterfeiters in the spirits and cosmetics industries, while washable inks enable the use of returnable packaging loops. Craft beverage brands exploit raised varnish and tactile effects that digital cannot replicate at production speed. Although shrink-film recycling remains a hurdle, mono-material polyethylene sleeves and delaminating adhesives promise end-of-life gains that align with retailer targets.

By End User: Cosmetics Outpaces Food in Premium Positioning

Food brands held 28.10% of 2025 sales as allergen and tamper-evidence rules kept volumes high, but cosmetics and personal care is set for the fastest 4.38% CAGR. Prestige lines demand metallic inks, soft-touch varnish, and chemical endurance that only UV-screen builds provide. L’Oréal now specifies ink cross-link density above 85% to survive 30-day immersion in oily formulations. Upcoming FDA healthy-claim labels add more variable data, a task that hybrid screen-digital workflows solve without color drift.

Beverage applications enjoy mid-teens share as craft breweries order textured labels that reinforce artisanal cues. Pharmaceutical serialization utilizes two-dimensional codes at 600 dpi, whereas industrial applications require labels that withstand exposure to mineral spirits. Fashion labels grow modestly as fast-fashion brands adopt direct-to-garment printing; yet, luxury houses still favor woven satin with screen-printed logos for their brand heritage.

By Printing Ink Type: Water-Based Gains on Regulatory Tailwinds

UV-curable inks accounted for 39.85% of 2025 revenue, thanks to their instant curing and high chemical resistance. Water-based chemistries, advancing at a 4.20% CAGR, comply with California’s 250 g⁄L VOC ceiling and European green-deal targets. Hybrid systems, such as AquaGrip, merge water rheology with UV crosslinking to deliver a 22 oz/in peel on polyethylene at under 200 g/L VOC.

Solvent lines remain necessary for low-surface-energy polypropylene unless corona-treated, while silicone and conductive silver inks address niche heat-transfer and RFID needs. Advances in nano-silica reinforcement extend abrasion life to 250 double rubs, giving converters fresh talking points for premium segments.

By Substrate Material: Paper Advances on Circular-Economy Rules

Plastic films kept a 45.98% share in 2025, driven by the 120-180% elongation that shrink sleeves require. Paper prices rise by 3.75% due to Forest Stewardship Council mandates and kerbside recyclability requirements. Mondi’s EcoWicket paper survives injection-molding yet recovers 95% fiber in municipal streams. Film producers respond with alkali-soluble adhesives, such as CleanFlake, that detach during bottle washes, thereby boosting the purity of recycled PET above 94%. Specialty glass and metal labels carry ceramic or epoxy inks for dishwasher and salt-spray endurance, while polylactic-acid, stone-paper, and bio-polymer substrates open new compostable paths.

Geography Analysis

North America accounted for 39.70% of 2025 revenue, driven by the Drug Supply Chain Security Act serialization, which spurred double-digit reprint demand. United States converters invested up to USD 220 million in UV-LED capacity, winning craft beverage and specialty food contracts that crave metallic inks and tactile finishes. Canada’s bilingual label law increased information density, a benefit for opaque screen inks. Mexico’s electronics maquiladoras specified polyimide labels rated for 260 °C reflow, reinforcing regional demand.

Europe accounted for roughly one-quarter of sales. The Packaging and Packaging Waste Regulation mandates 65% recycled content in labels by 2030, prompting converters to shift toward mono-material builds. Germany’s VerpackG fees on non-recyclables and the United Kingdom’s UKCA symbol changeover fueled short-run orders that favored screen printing. Security holograms for authenticating the origin of olive oil and wine remain a resilient niche.

The Asia-Pacific region is expected to post a 4.98% CAGR through 2031 due to China’s late-2025 QR-code deadline, which will affect billions of packaged food units. India’s IS 17142:2024 adhesion rule accelerates the adoption of wet glue in humid coastal corridors. Japanese tax credits for solvent-free presses, South Korean deposit fees on label waste, and Australian ISO 22000 export standards further expand regional uptake. Middle East and African growth hovers near mid-single digits, with Saudi localization rules and South African local-content thresholds prompting domestic press installations.

Competitive Landscape

The screen print label market remains moderately fragmented, with the five largest suppliers controlling just 28-32% of sales, leaving room for regional specialists. CCL Industries acquired Tapp Technologies to bring NFC chip embedding in-house, reducing lead times to under a week and eliminating external mark-ups.

Energy-saving UV-LED retrofits and conductive-ink antenna printing differentiate leaders that target heat-sensitive substrates and smart-packaging use cases. White-space opportunities include electric vehicle battery labels that require UL 969 approval across -40 °C to 150 °C temperature cycles.

Sustainability is a strong wedge for challengers. Avery Dennison’s CleanFlake adhesive raises the purity of recycled PET to 94-96%, earning resin premiums that offset higher label costs. Patent filings concentrate on silver-nanoparticle inks with sub-0.5 Ω⁄sq resistance for contactless payments. Hybrid workflows pair digital variable data with screen stations for spot colors, reducing make-ready time to 20 minutes. California’s VOC rule forces solvent shops to either retrofit their ink recirculation systems for USD 400,000-600,000 or exit the state market.

Screen Print Label Industry Leaders

Fort Dearborn Company

Autajon Group

CCL Industries Inc.

Mondi PLC

Ahistrom Munksjo Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: North American beverage groups adopt alkali-soluble CleanFlake adhesives on PET shrink sleeves to meet upcoming recycled-content targets, accelerating full-body screen-printed graphics demand.

- June 2025: Global e-commerce platforms, led by Amazon and Alibaba, roll out abrasion-resistant, polyester screen-printed shipping labels across regional fulfillment hubs after successful 2024 pilots.

- October 2024: CCL Industries completed the acquisition of Tapp Technologies, securing in-house NFC embedding capability.

- September 2024: UPM Raflatac rolled out Forest Film linerless labels that remove silicone release liners and cut material costs by up to 20%.

Global Screen Print Label Market Report Scope

Screen printing allows for printing on substrates of any shape, thickness, and size, as well as printing on both the front and back sides of a clear label. These labels are widely used on bags, luggage, and garments, as well as in beverages and cosmetics.

The Screen Print Label Market Report is Segmented by Type (Shrink Sleeves Label, Linerless Label, Wet-Glued Label, Other Types), End User (Fashion and Apparels, Food, Beverages, Cosmetics and Personal Care, Other End Users), Printing Ink Type (Solvent-Based, Water-Based, UV-Curable, Silicone Ink, Other Printing Ink Types), Substrate Material (Paper, Plastic Films, Glass, Metal, Fabric, Other Substrates), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Shrink Sleeves Label |

| Linerless Label |

| Wet-Glued Label |

| Other Types |

| Fashion and Apparels |

| Food |

| Beverages |

| Cosmetics and Personal Care |

| Other End Users |

| Solvent-Based |

| Water-Based |

| UV-Curable |

| Silicone Ink |

| Other Printing Ink Types |

| Paper |

| Plastic Films |

| Glass |

| Metal |

| Fabric |

| Other Substrates |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Type | Shrink Sleeves Label | ||

| Linerless Label | |||

| Wet-Glued Label | |||

| Other Types | |||

| By End User | Fashion and Apparels | ||

| Food | |||

| Beverages | |||

| Cosmetics and Personal Care | |||

| Other End Users | |||

| By Printing Ink Type | Solvent-Based | ||

| Water-Based | |||

| UV-Curable | |||

| Silicone Ink | |||

| Other Printing Ink Types | |||

| By Substrate Material | Paper | ||

| Plastic Films | |||

| Glass | |||

| Metal | |||

| Fabric | |||

| Other Substrates | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the screen print label market?

The screen print label market size is USD 2.51 billion in 2026 and is projected to reach USD 2.83 billion by 2031.

Which application type leads sales?

Shrink sleeves hold 38.12% of 2025 revenue and maintain the largest stake thanks to full-body graphics and 360-degree branding.

Why are UV-LED presses gaining traction?

They cut energy use by up to 85%, cure inks at higher web speeds, and allow printing on heat-sensitive and compostable films.

What region will grow the fastest?

Asia-Pacific posts a 4.98% CAGR through 2031, driven by China’s mandatory QR-code traceability and cost-competitive labor.

How do digital presses affect the sector?

Inkjet equipment undercuts screen printing on short runs, yet lower abrasion resistance keeps screen processes dominant in durable and shrink applications.

Which regulation most influences sustainability choices?

California’s Rule 1130 VOC cap and the European Packaging and Packaging Waste Regulation push converters toward water-based inks and recyclable substrates.

Page last updated on: