Czech Republic Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

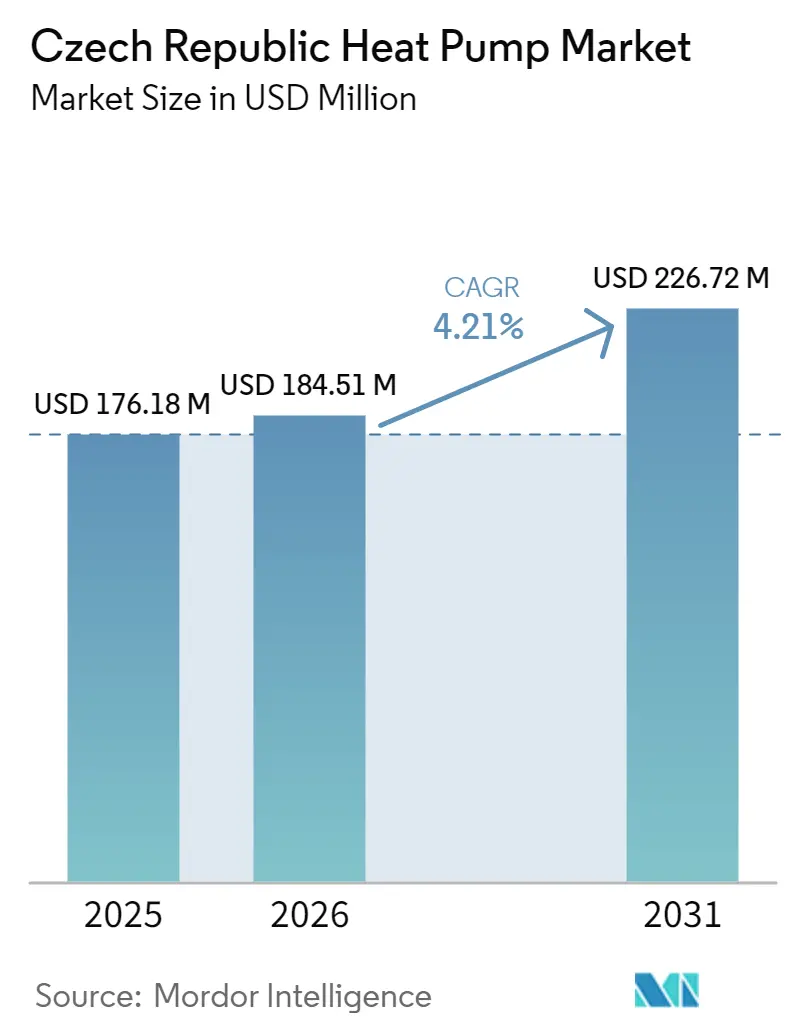

| Base Year Market Size (2025) | USD 176.18 Million |

| Market Size (2026) | USD 184.51 Million |

| Market Size (2031) | USD 226.72 Million |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Heat Pump Market Analysis by Mordor Intelligence

The Czech Republic Heat Pump market size is expected to increase from USD 176.18 million in 2025 to USD 184.51 million in 2026 and reach USD 226.72 million by 2031, growing at a CAGR of 4.21% over 2026-2031. Post-slump recovery is visible as subsidy frameworks stabilize and multinational producers scale local capacity, cushioning the market against the 2024 demand shock. Consolidation of manufacturing in Pilsen and Brno is shortening supply chains, while high fossil-fuel prices keep the electricity-to-gas cost ratio favorable for electrified heating. However, district-heating coverage above 40% caps the residential addressable base, installer shortages lengthen project lead times, and grid constraints hamper PV-heat-pump hybrids.

Key Report Takeaways

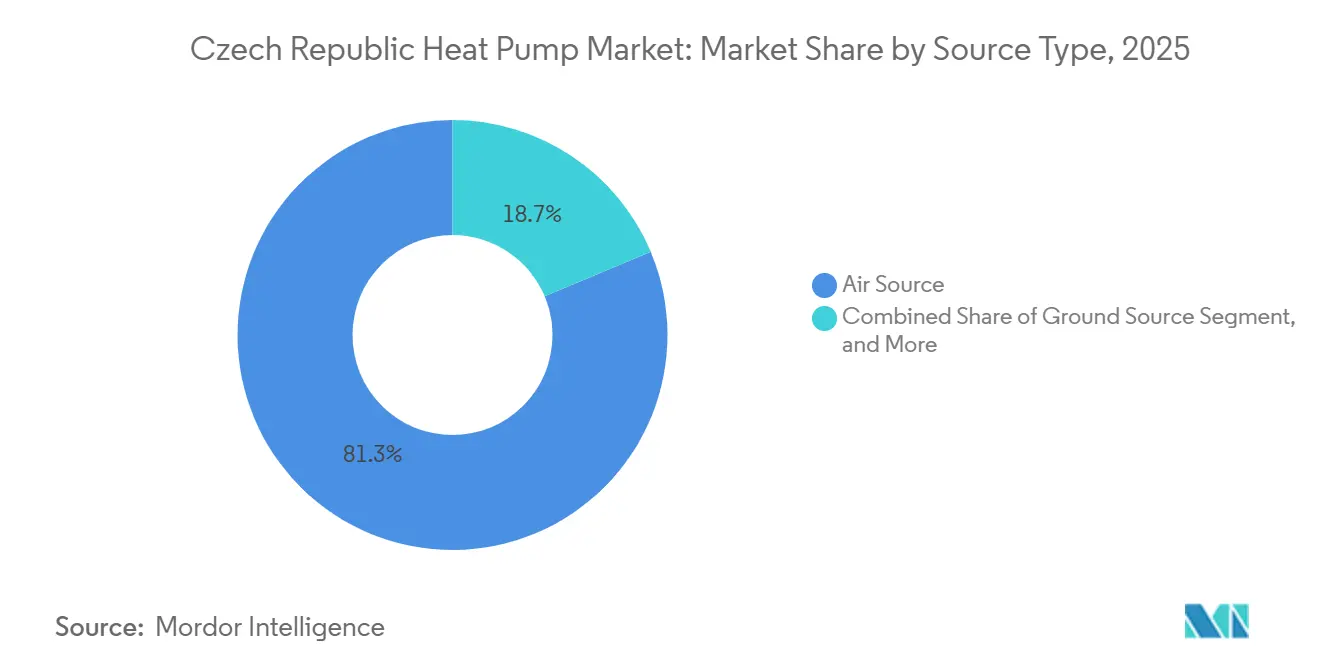

- By source type, air source systems led with 81.32% revenue in 2025, while hybrid configurations are forecast to expand at a 4.91% CAGR to 2031.

- By technology, air-to-water held a 72.31% share of the Czech Republic Heat Pump market size in 2025 and ground-to-water is projected to advance at a 4.34% CAGR through 2031.

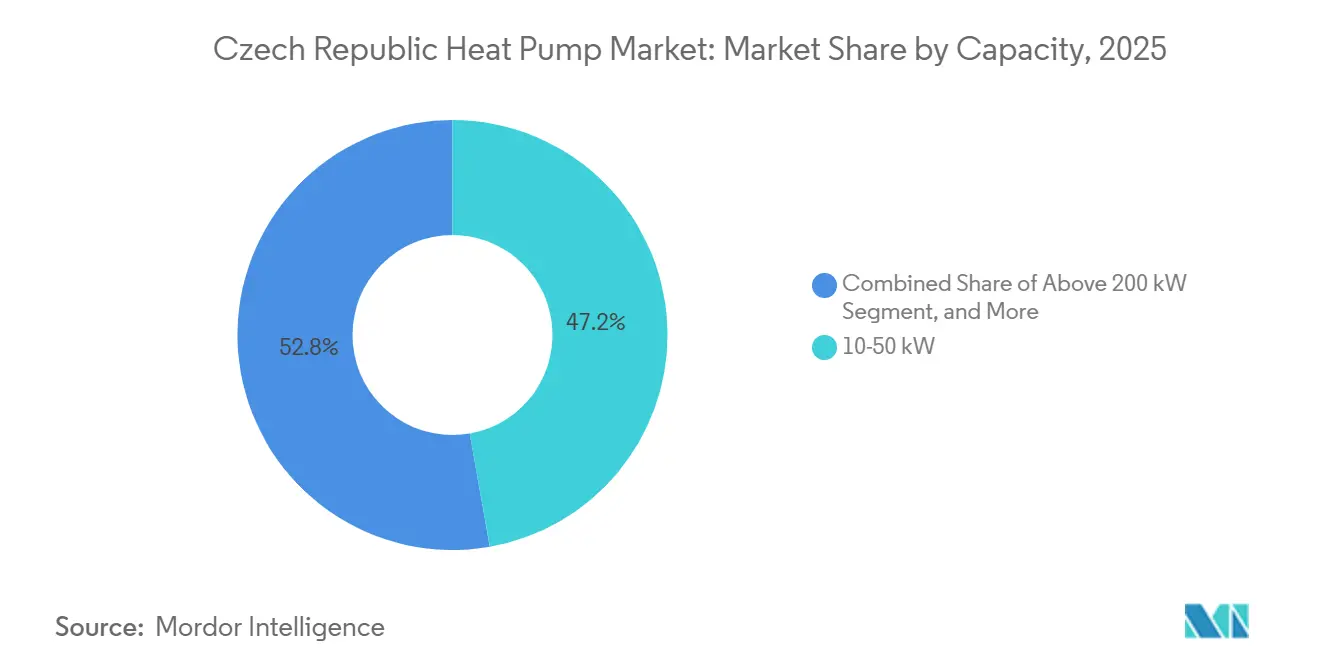

- By capacity, 10-50 kW units commanded 47.23% of the Czech Republic Heat Pump market share in 2025, whereas systems above 200 kW register the fastest 4.96% CAGR to 2031.

- By application, space heating captured 61.82% revenue in 2025; industrial and process heating is set to grow at a 4.83% CAGR through 2031.

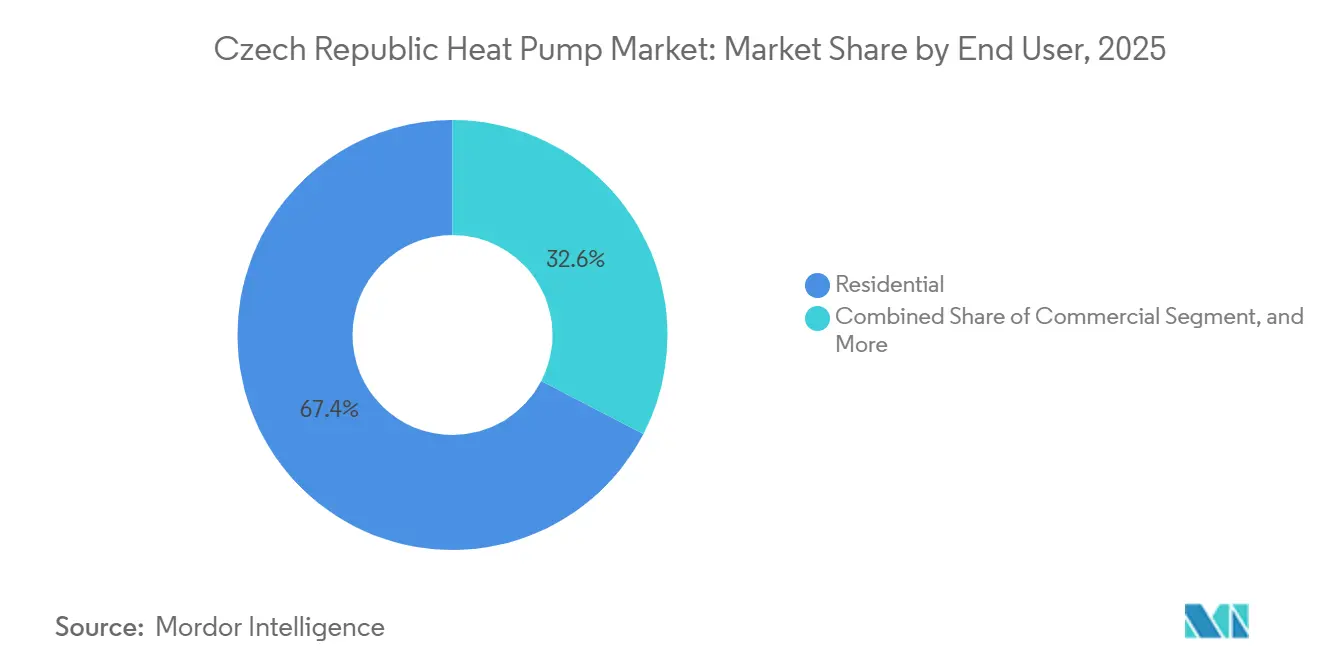

- By end user, residential retrofits accounted for 67.39% of 2025 sales, even as industrial customers are poised for 4.52% CAGR over 2026-2031.

- By installation, retrofit projects held 54.43% of 2025 turnover, yet new-build installations are projected to climb at a 4.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Czech Republic Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies and Incentive Programs | +1.2% | Prague, Brno, Pilsen | Medium term (2-4 years) |

| Rising Fossil Fuel Prices and Electricity-Gas Price Ratio | +0.9% | National, with spillover to Moravian-Silesian region | Short term (≤ 2 years) |

| EU and National Decarbonization Targets | +0.7% | National | Long term (≥ 4 years) |

| Expansion of Local Manufacturing Capacity by Multinationals | +0.6% | Pilsen and Brno zones | Medium term (2-4 years) |

| Surge in High-Temperature R290 Heat Pump Adoption | +0.4% | Ostrava and Brno industrial sites | Medium term (2-4 years) |

| Smart-Grid Ready Tariff Pilots with Utilities | +0.3% | ČEZ and PRE distribution areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies and Incentive Programs

The 2026 redesign of Nová zelená úsporám replaced grants with interest-free loans of CZK 75,000-90,000 (USD 3,180-3,816) for air-to-water and CZK 110,000-130,000 (USD 4,664-5,512) for ground-source units, sustaining affordability for credit-worthy households while easing fiscal pressure.[1]Ministry of Environment of the Czech Republic, “Nová zelená úsporám Program Guidelines 2026,” MZP.CZ Earlier sequencing rules that forced insulation upgrades before heat-pump subsidies caused the 2024 demand collapse, but current disbursements under the Czech Recovery and Resilience Plan aim to accelerate uptake. Administrative bottlenecks and installer shortages slow drawdown, yet the International Energy Agency urges expansion of support to hybrid and industrial systems. Credit-screening now risks excluding lower-income rural dwellings, potentially widening energy-efficiency gaps.

Rising Fossil Fuel Prices and Electricity-Gas Price Ratio

Natural-gas prices averaged EUR 35 (USD 40) /MWh in 2024, still 60% above pre-pandemic levels, anchoring the economic case for the Czech Republic Heat Pump market.[2]European Energy Exchange, “Gas and Power Price Data 2024-2025,” EEX.COM Although wholesale electricity is expected to fall 15% in 2025, the electricity-to-gas ratio remained at 3.2 in 2024, discouraging adoption without time-of-use tariffs. A ČEZ pilot covering 75% of test customers cut annual bills by 10%, compressing residential payback to below seven years.[3]ČEZ Group, “Dynamic Tariff Pilot Results 2025,” CEZ.CZ Detached homes outside district-heating grids face full fossil-fuel volatility, whereas connected properties benefit from biomass and waste-heat integration.

EU and National Decarbonization Targets

REPowerEU calls for 10 million extra heat pumps annually by 2030, and the Czech VAT on installations fell to 12% in 2024. The national climate plan mandates electrifying 25% of residential heating by decade-end, implying around 200,000 units between 2026 and 2030. Building-code updates in 2025 obligate new homes to secure 30% of heat from renewables, effectively embedding heat pumps. Low-carbon electricity from Dukovany and Temelín nuclear plants strengthens lifecycle emissions credentials, while a 42 km pipeline will channel nuclear waste-heat to Brno by 2028.[4]AFRY, “Dukovany-Brno District Heating Pipeline Project,” AFRY.COM

Expansion of Local Manufacturing Capacity by Multinationals

Panasonic’s EUR 320 million (USD 341 million) expansion lifted Pilsen floor-space to 140,000 m², targeting 1.4 million units a year by 2030.[5]Panasonic Newsroom, “Panasonic Expands Pilsen Heat Pump Factory,” NEWS.PANASONIC.COM Eighty robots already enhance throughput, and full component-automation is slated for 2028. Daikin’s EUR 50 million (USD 53.3 million) Brno upgrade relocates hydrobox and hydrokit lines from Germany, trimming cross-border logistics risk. Seven domestic factories identified by the Joint Research Centre underpin a skilled-labor cluster that accelerates R290 product rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Costs and Tight Credit Conditions | -0.8% | Rural and lower-income regions | Short term (≤ 2 years) |

| Installer Capacity and Skills Shortage | -0.6% | Moravian-Silesian and Karlovy Vary regions | Medium term (2-4 years) |

| Policy Volatility Driving 2024 Demand Slump | -0.4% | National | Short term (≤ 2 years) |

| Grid Connection Delays for PV-Heat Pump Hybrids | -0.3% | South Bohemia and South Moravia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs and Tight Credit Conditions

Installed prices range from CZK 200,000-400,000 (USD 8,840-16,960) for air-to-water and CZK 500,000-800,000 for ground-source systems, equal to 8-12 months of median income and the chief barrier cited by 42% of surveyed households.[6]STIEBEL ELTRON, “Czech Household Heating Survey 2025,” STIEBEL-ELTRON.COM Transition from grants to loans introduces credit checks that sideline customers with irregular incomes. Commercial banks tightened lending after the central-bank policy rate held at 4.25%, lifting home-improvement financing costs by 150 basis points.[7]Czech National Bank, “Monetary Policy Report 2024,” CNB.CZ Without aid, payback stretches to 8-12 years, above homeowner thresholds.

Installer Capacity and Skills Shortage

Qualification 26-074-M requires a CZK 5,000 (USD 212) exam, yet annual certificate output covers under 30% of projected installs.[8]ENBRA, “Professional Qualification Requirements,” ENBRA.CZ Limited instructor capacity means lead times balloon to 6-9 months in peak seasons. EU upskilling projects will train fewer than 1,500 Czech installers, far below the 8,000-10,000 needed by 2030. Labor scarcity pushes wages 20-30% above Western European benchmarks, eroding the cost edge and triggering quality issues in rushed jobs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Systems Prevail, Hybrid Growth Quickens

Air source units dominated 2025 sales with an 81.32% share thanks to simpler installation and lower capital cost, securing a central role in the Czech Republic Heat Pump market. Hybrid heat-pump-boiler combinations, however, are projected to post the swiftest 4.91% CAGR to 2031 as commercial operators blend fuels in response to real-time price signals. Water source systems remain niche because of strict groundwater permitting, while ground source installations appeal to industrial sites despite higher drilling costs. Panasonic’s propane-charged air units, produced in Pilsen, illustrate local capacity that meets EU F-Gas curbs.

Ground loops deliver consistent performance in sub-zero winters, a trait valuable to process industries in Ostrava. The EU refrigerant phase-down accelerates adoption of R290 models from PZP Heating and HOTJET. Yet air source efficiency drops below -15 °C, driving interest in hybrids across the Moravian-Silesian region. Ground-water solutions need specialized drilling teams, compounding installer shortages. Water-body access limits water-source potential to riverside cities such as Hradec Králové, where environmental oversight is strict.

By Technology: Retrofit-Friendly Air-to-Water Leads, Ground-to-Water Finds Industrial Niche

Air-to-water platforms held 72.31% of 2025 revenue because they integrate with hydronic radiators without ductwork, making them the first choice in the Czech Republic Heat Pump market. The Czech Republic Heat Pump market size for ground-to-water units is projected to climb at a 4.34% CAGR to 2031, led by food processing and pharma sites that value stable year-round temperatures. Air-to-air machines serve offices needing cooling but lack traction in homes that use radiators.

Water-to-water heat pumps hover at the fringes, constrained by river-use permits. Panasonic’s work with the Technical University of Ostrava cuts borehole depth, trimming costs by about 15%. Insulation-first subsidy rules burden air-to-water retrofits with extra façade upgrades. Daikin’s Brno factory will shorten hydrobox lead times, customizing units for Czech housing archetypes.

By Capacity: Mid-Range Dominates, Large Industrial Units Accelerate

Systems rated 10-50 kW account for 47.23% of 2025 turnover, supplying detached homes and small commercial buildings. Above 200 kW equipment, however, should grow at 4.96% through 2031 as industrial operators respond to ETS carbon prices and decarbonization pledges. Sub-10 kW units serve new super-insulated dwellings but face cost comparisons with simple electric heaters.

The Czech Republic Heat Pump market share for mid-range units is pressured by Panasonic’s plan to bring air-to-water prices below EUR 1,000 (USD 1,150) per set by 2030. Large-capacity R290 machines already deliver 90 °C output, replacing gas burners in breweries and chemical plants. Robur’s Flexi Park case in Prague demonstrated 30% energy savings for a 50-200 kW application. Seasonal performance factors above 4.5 at the Cézava seniors’ home underscore the efficiency of large ground loops.

By Application: Space Heating Rules, Process Heating Gathers Pace

Space heating claimed 61.82% of 2025 sales owing to roughly 5,000 heating-degree days each year. Industrial and process heating is forecast for the highest 4.83% CAGR through 2031 as factories pursue Scope 1 reductions. Sanitary hot water usually rides piggyback on space heaters, while dedicated hot-water pumps remain marginal.

The Czech Republic Heat Pump market size tied to process heating will expand as high-temperature R290 units mature, with outputs up to 90 °C now viable. Space cooling lags because July averages near 20 °C, limiting demand. Retrofit challenges in multi-tenant blocks, where landlords bear costs but tenants save, still restrain uptake.

By End User: Households Lead, Industry Moves Fastest

Residential retrofits delivered 67.39% of 2025 revenue, supported by a 1.5 million-home detached-house stock. Industrial clients, however, are projected for the quickest 4.52% CAGR on the back of carbon pricing near EUR 80 (USD 90) / tonne. Commercial premises trail, constrained by district-heating connections and split incentives.

Survey data show cost anxiety remains the main hurdle for homeowners. In industry, long commissioning times and the need for custom controls favor incumbents with service depth. Expansion of certified installer ranks is pivotal for sustaining household momentum, whereas technology breakthroughs in 90 °C compressors will unlock new factory uses.

By Installation: Retrofits Still Majority, New-Build Share Rising

Retrofits held 54.43% of 2025 sales as aging boilers reached end-of-life. New construction, though, is expected to grow at a 4.52% CAGR as the 2025 code requires 30% renewable heat in new homes. Retrofits often need insulation and radiator upgrades that add CZK 100,000-200,000 (USD 4,240-8,480) to project budgets, stretching timelines to nine months.

The Czech Republic Heat Pump industry benefits when architects specify underfloor heating in greenfield projects, cutting equipment sizes and installation labor. Suburban developments around Prague and Brno account for most new-build installations because district-heating grids are sparse. Retrofit economics improve as Daikin localizes hydrobox supply, but sequencing rules still deter some owners who cannot afford envelope work upfront.

Geography Analysis

Prague, Brno, and Pilsen dominate installations thanks to higher incomes, dense installer networks, and proximity to Panasonic and Daikin hubs. Detach-home suburbs in Praha-západ and Praha-východ demonstrate rapid uptake as residents seek freedom from district-heating tariffs. Brno leverages Daikin’s expansion and a biomass CHP upgrade funded by a EUR 75 million (USD 85 million) European Investment Bank loan, coupling waste heat with heat-pump networks.

Pilsen’s 140,000 m² Panasonic complex magnetizes component suppliers, cementing the city as Central Europe’s heat-pump cluster. Ostrava in Moravian-Silesian faces heavy industrial loads and a legacy coal base, so grid upgrades and high-temperature equipment are pivotal. Rural Karlovy Vary and Ústí nad Labem lag because of lower incomes and only about 20 certified installers, leading to one-year waitlists.

South Bohemia and South Moravia grapple with saturated PV interconnection queues that stalled hybrid projects after 170 GW of speculative reservations clogged the system. Smart-grid pilots by ČEZ and PRE in Prague and Central Bohemia demonstrate 50% off-peak tariff cuts, improving heat-pump economics. The July 4 2025 grid event, which shed 2,300 MW, pushed authorities to accelerate smart-meter rollouts.

Competitive Landscape

Multinationals, Daikin, Panasonic, NIBE, Vaillant, Bosch, control roughly 60% of sales, while Czech firms such as MasterTherm, PZP Heating, and Regulus export more than 70% of output to Western Europe. Panasonic’s robotized Pilsen line and Daikin’s Brno relocation demonstrate a shift toward Central European supply resilience. Seven domestic factories create a deep talent pool but spark rivalry for installer alliances.

Product competition now hinges on R290 refrigerant, factory automation, and digital demand-response compatibility. Panasonic targets full component automation by 2028, compressing lead times to under four weeks. Czech brands roll out propane models to meet F-Gas quotas without transport hurdles.

ČEZ’s dynamic tariff scheme creates a premium segment for smart-grid-ready units. Industrial specialists Oilon and Robur chase process-heating niches where 90 °C output displaces gas burners. Bundled PV-battery-heat-pump packages from energy retailers add a new channel threatening pure-play manufacturers.

Czech Republic Heat Pump Industry Leaders

Daikin Industries, Ltd.

Vaillant Group

Carrier Global Corporation

STIEBEL ELTRON GmbH & Co. KG

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Daikin confirmed hydrobox and hydrokit lines will shift from Germany to Brno by Jun 2026, cutting lead times 30% and adding 200 jobs.

- February 2026: ČEZ signed with Prague city to equip 5,000 municipal buildings with smart-grid-ready heat pumps by 2030, leveraging dynamic tariffs for 40% bill cuts.

- January 2026: The environment ministry revamped Nová zelená úsporám, swapping grants for interest-free loans to maintain fiscal room while preserving affordability.

- September 2025: Panasonic inaugurated the expanded 140,000 m² Pilsen factory after a EUR 320 million (USD 340 million) upgrade, aiming for 1.4 million units annually by 2030.

Czech Republic Heat Pump Market Report Scope

| Air Source |

| Water Source |

| Ground Source |

| Hybrid |

| Air-to-Air |

| Air-to-Water |

| Water-to-Water |

| Ground-to-Water |

| Below 10 kW |

| 10-50 kW |

| 50-200 kW |

| Above 200 kW |

| Space Heating |

| Space Cooling |

| Domestic and Sanitary Hot Water |

| Industrial and Process Heating |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| New Installation |

| Retrofit |

| By Source Type | Air Source |

| Water Source | |

| Ground Source | |

| Hybrid | |

| By Technology | Air-to-Air |

| Air-to-Water | |

| Water-to-Water | |

| Ground-to-Water | |

| By Capacity | Below 10 kW |

| 10-50 kW | |

| 50-200 kW | |

| Above 200 kW | |

| By Application | Space Heating |

| Space Cooling | |

| Domestic and Sanitary Hot Water | |

| Industrial and Process Heating | |

| Other Applications | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Installation | New Installation |

| Retrofit |

Key Questions Answered in the Report

How large is the Czech Republic Heat Pump market in 2026?

The market is valued at USD 184.51 million in 2026, on track to reach USD 226.72 million by 2031.

Which source type leads deployments in the Czech Republic?

Air source systems dominate with 81.32% of 2025 revenue, owing to easier installation and lower cost.

What is driving industrial adoption of heat pumps in the country?

Carbon prices near EUR 80 / tonne and the availability of 90 °C R290 units shorten payback to under five years for many factories.

Why are installer shortages a concern?

Only about 30% of the technicians needed by 2030 are currently being certified, causing project lead times of up to nine months.

How do the new subsidy rules work?

Since January 2026, direct grants have been replaced by interest-free loans of up to CZK 90,000 (USD 3,816) for air-to-water and CZK 130,000 (USD 5,512) for ground-source systems.

Which cities show the highest uptake?

Prague, Brno, and Pilsen lead because of higher household incomes, dense installer networks, and nearby manufacturing hubs.

Page last updated on: