Austria Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 244.48 Million |

| Market Size (2026) | USD 251.52 Million |

| Market Size (2031) | USD 238.07 Million |

| Growth Rate (2026 - 2031) | 2.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Heat Pump Market Analysis by Mordor Intelligence

The Austria heat pump market size is expected to grow from USD 244.48 million in 2025 to USD 251.52 million in 2026 and is forecast to reach USD 283.07 million by 2031 at a 2.39% CAGR over 2026-2031. Retrofit activity, which represented 63.43% of 2025 installations, still dominates, yet policy mandates and subsidy layers continue to attract first-time buyers in new construction. Vienna’s plan to eliminate 600,000 gas heaters, Austria’s 83.1% renewable-electricity mix, and the 2040 carbon-neutrality target collectively reinforce the long-term relevance of the Austria heat pump market. Domestic suppliers keep their edge through alpine-climate product customization, while multinational brands leverage scale to bring R290 propane solutions to price-sensitive segments. Skilled-labor shortages, permitting delays in karst regions, and rural grid constraints temper the growth curve but do not derail the market’s structural shift away from fossil boilers.

Key Report Takeaways

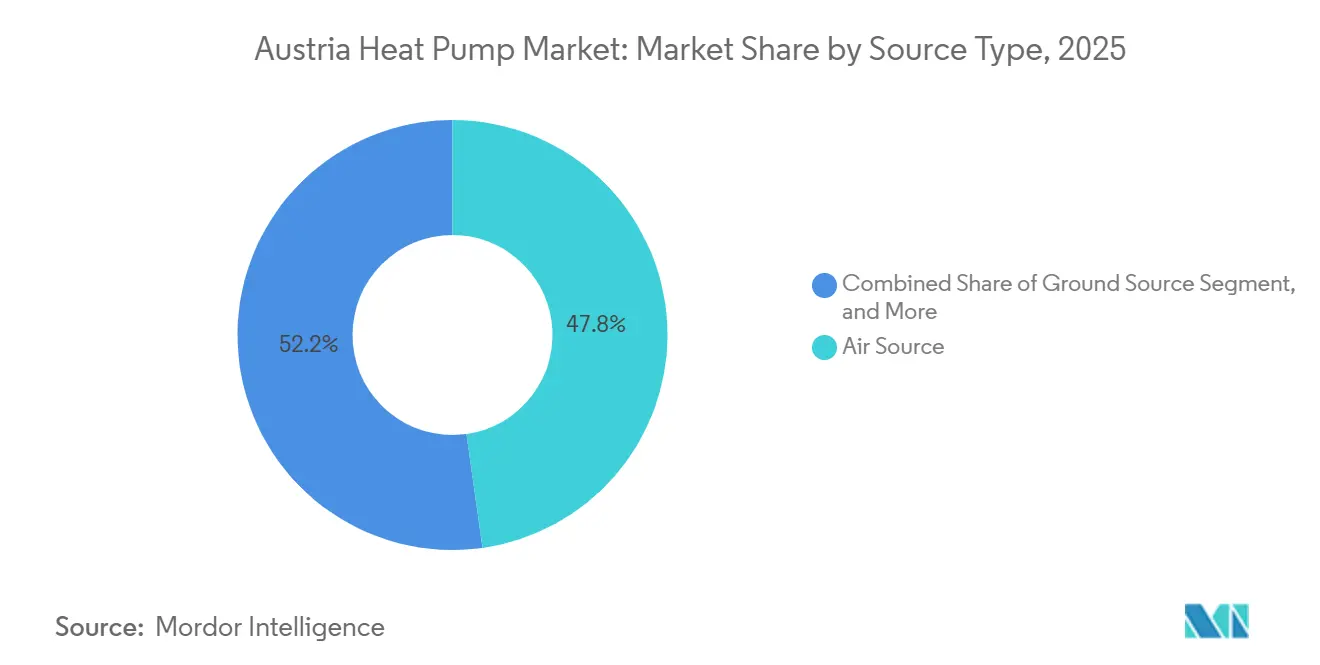

- By source type, air-source systems led with 47.78% revenue share in 2025 while hybrid configurations are projected to advance at a 3.03% CAGR through 2031.

- By technology, air-to-water units accounted for 46.31% of 2025 deployments and ground-to-water solutions are expected to expand at a 2.87% CAGR to 2031.

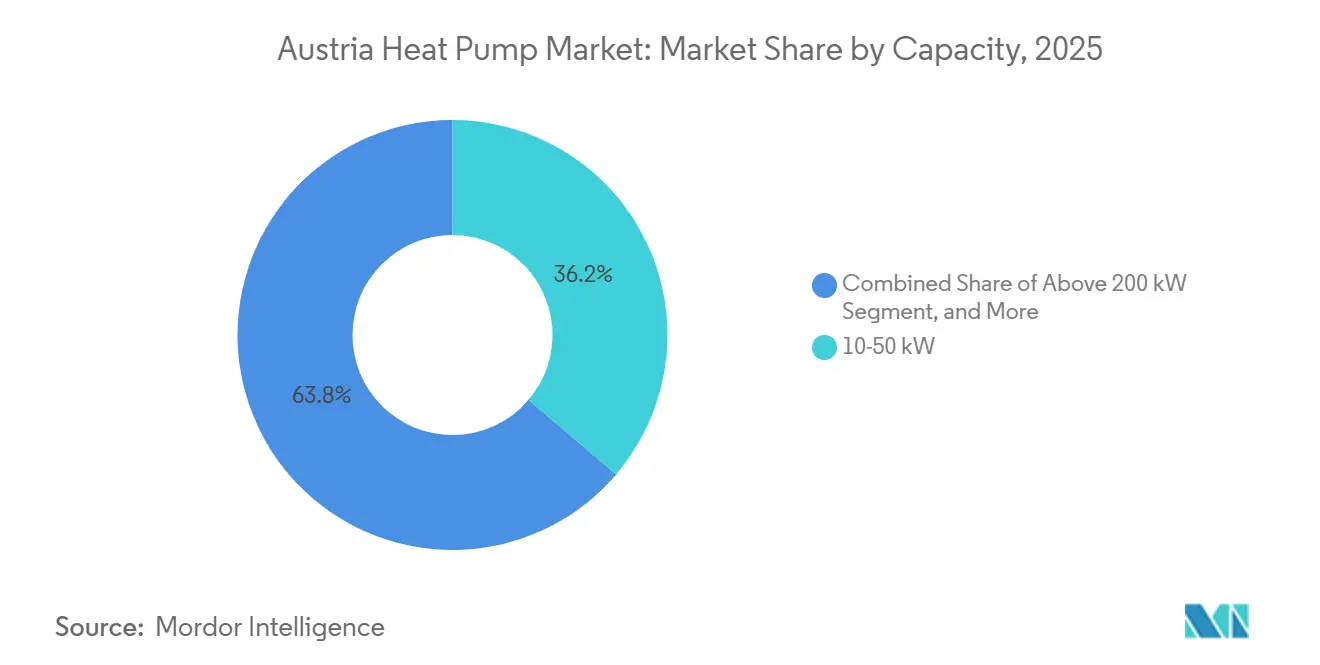

- By capacity, the 10-50 kilowatt range captured 36.23% of 2025 revenue and the 50-200 kilowatt band is forecast to rise at a 2.69% CAGR over the same horizon.

- By application, domestic and sanitary hot water held 50.82% share in 2025, whereas industrial and process heating is poised for a 3.24% CAGR through 2031.

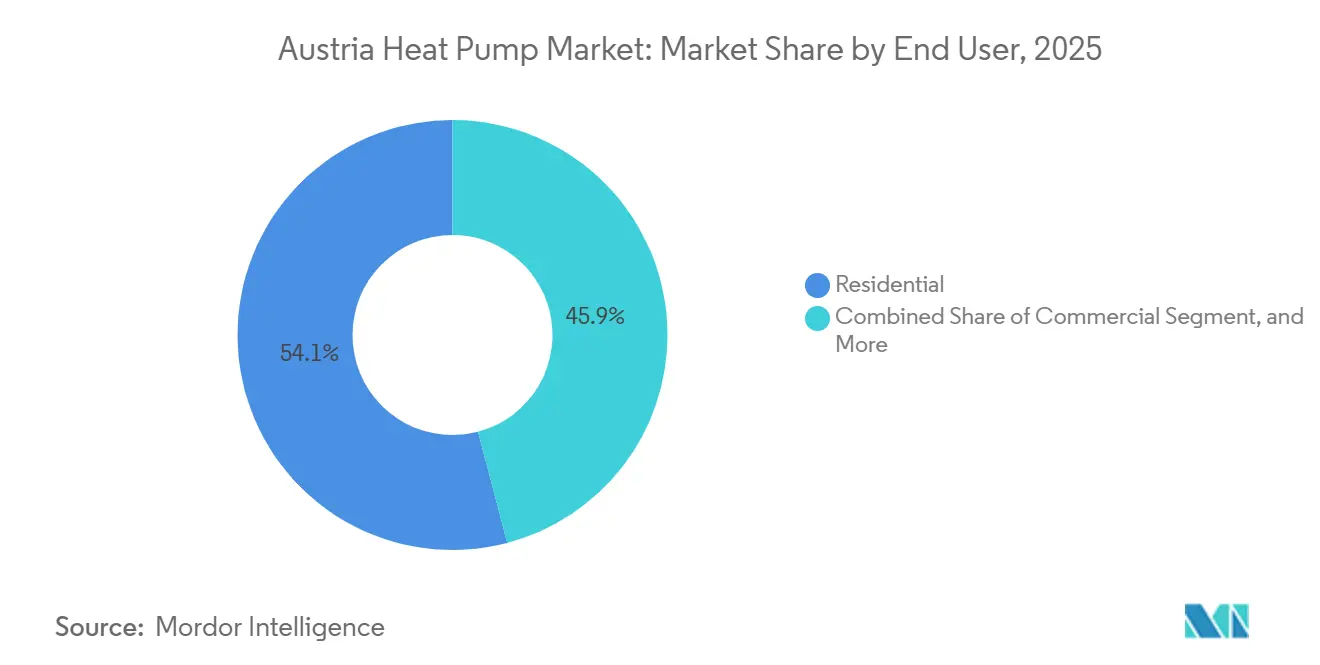

- By end user, residential premises represented 54.09% of 2025 installations, while commercial buildings are set to climb at a 2.58% CAGR to 2031.

- By installation type, retrofit projects comprised 63.43% of 2025 activity and new builds are projected to grow at a 2.47% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded Renovation Subsidies Under "Raus Aus Öl Und Gas" Scheme | +0.8% | National, stronger in Vienna, Lower Austria, Styria | Short term (≤ 2 years) |

| Ambitious 2040 Carbon-Neutrality Target Mandating One Million Heat Pumps by 2030 | +0.6% | National | Long term (≥ 4 years) |

| EU REPowerEU Directive Accelerating Heat-Pump Adoption | +0.4% | National | Medium term (2-4 years) |

| Rising Renewable Electricity Share Lowering Operating Costs | +0.3% | Hydro-rich provinces | Medium term (2-4 years) |

| Surge in Heat-Pump Snow-Melt Systems for Alpine Ski Resorts | +0.2% | Tyrol, Salzburg, Vorarlberg | Medium term (2-4 years) |

| Vienna Façade-Integrated Micro Heat-Pump Ordinance in Dense Districts | +0.1% | Vienna | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanded Renovation Subsidies Under "Raus aus Öl und Gas" Scheme

Austria earmarked EUR 360 million (USD 406 million) in 2026 to help households replace oil and gas boilers with heat pumps. Grants of up to EUR 7,500 (USD 8,475) can slash the net price of a typical 10 kW air-source unit by half, compressing payback to roughly seven years.[1]Austrian Federal Ministry for Climate Action, “Sanierungsoffensive 2026,” bmk.gv.at Provinces such as Lower Austria and Styria stack extra funds for ground-source projects, narrowing the gap between drilling costs and air-source solutions. Application volumes rose sharply in early 2026, forcing municipalities to improve processing times. The program’s clear rules and generous caps keep retrofit momentum high across the Austria heat pump market.

Ambitious 2040 Carbon-Neutrality Target Mandating One Million Heat Pumps by 2030

Austria’s climate law sets a firm 2040 deadline for net-zero emissions and calls for one million cumulative heat pump installations by 2030. Meeting that milestone requires annual sales near 92,600 units, a steep jump from the roughly 60,000 units sold in 2025. The phased ban on new fossil boilers, effective from 2025, gives builders and homeowners a clear replacement signal. Vienna’s plan to retire 600,000 gas heaters anchors demand in the nation’s largest urban hub.[2]City of Vienna, “Vienna Climate Roadmap 2040,” wien.gv.at Together, these commitments lock in a sizeable forward order book for manufacturers and installers.

EU REPowerEU Directive Accelerating Heat-Pump Adoption

Under REPowerEU, Austria must add about 150,000 heat pumps by 2027, backed by EUR 200 million (USD 226 million) in European grants.[3]European Commission, “REPowerEU Plan,” ec.europa.eu Low-interest loans from the Austrian Development Bank further trim financing costs for households and businesses. The directive also streamlines permitting for renewable projects, cutting red tape that once deterred applicants. Domestic suppliers have responded by expanding factory lines, reducing lead times for mid-size commercial units. These policy and finance tools together create a supportive runway for steady market expansion through the decade.

Rising Renewable Electricity Share Lowering Operating Costs

Renewables supplied 83.1% of Austria’s power in 2025, dominated by hydropower and wind.[4]Eurostat, “Renewable Energy Statistics,” ec.europa.eu This clean mix shrinks the carbon footprint of electric heating to a fraction of that from gas boilers. At current tariffs, a heat pump with a seasonal coefficient of 4 can deliver thermal energy for EUR 0.05-0.06 (USD 0.06-0.07) per kWh, undercutting natural gas by at least one-third. Provinces rich in hydropower enjoy even lower rates, shortening payback in alpine valleys. Planned additions of wind and solar capacity promise price stability that should keep running costs attractive well past 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor Shortage of Certified Refrigeration Technicians | -0.5% | Nationwide, especially rural and alpine districts | Medium term (2-4 years) |

| High Upfront Capital Cost Versus Gas Boilers | -0.4% | Nationwide, larger burden for low-income households and small firms | Short term (≤ 2 years) |

| Permitting Bottlenecks for Deep Boreholes in Karst Regions | -0.2% | Styria, Lower and Upper Austria karst zones | Medium term (2-4 years) |

| Transformer Capacity Constraints on Rural Three-Phase Feeders | -0.2% | Rural Burgenland, Lower and Upper Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage Of Certified Refrigeration Technicians

Austria lacks roughly 2,000 technicians certified to handle R290 propane systems, which lengthens installation lead times by four to eight weeks across the Austria heat pump market. Vocational schools graduate only 300-400 specialists per year, while the 2024 revision of the EU F-Gas Regulation attracted installers to neighboring countries, deepening the domestic gap. Rural districts feel the crunch most acutely because contractors travel long distances between jobs, inflating labor charges by up to 15%. The SKILLSAFE program, launched in 2025, offers augmented-reality modules that cut classroom hours by 30%, yet enrollment remains below capacity because small firms cannot spare apprentices during peak retrofit season. Ground-source projects are hit hardest since drilling, hydraulic balancing, and refrigerant handling demand multiprong expertise that fewer than 150 Austrian companies possess.[5]Austrian Economic Chamber, “Skilled Labor Market Analysis 2025,” wko.at Without rapid workforce expansion, subsidy funds risk under-spending, slowing the timetable to one million units by 2030. Municipalities now explore fast-track credentialing for experienced plumbers and electricians, but insurance providers still insist on full certification for R290 work, limiting near-term flexibility. The labor constraint therefore shaves an estimated 0.5 percentage points from the Austria heat pump market CAGR through 2031.

High Upfront Capital Cost Versus Gas Boilers

An 8-12 kilowatt air-source unit installed in a single-family home costs EUR 12,000-18,000 (USD 13,560-20,340), at least triple the price of a condensing gas boiler. Even after the “Raus aus Öl und Gas” grant of EUR 7,500 (USD 8,475), many households face a residual bill that equals half of their annual disposable income, curbing order pipelines in the Austria heat pump market. Ground-source systems widen the delta further, often topping EUR 30,000 (USD 33,900) once drilling and hydrogeological reports are included. Low-interest OeEB loans lower present-value costs by about 25%, but applicants must supply energy audits, credit scores, and property deeds, documents that delay closing by six to ten weeks. Small businesses confront similar arithmetic: a 100-kilowatt commercial heat pump requires EUR 80,000-120,000 (USD 90,400-135,600) upfront, while subsidy caps at EUR 30,000 (USD 33,900) leave a large financing hole.[6]Austrian Energy Agency, “Heat Pump Market Analysis 2025,” energyagency.at Price sensitivity shows up in provincial uptake: Tyrol, Vorarlberg, and Salzburg, where electricity tariffs are 10-15% below the national average, register faster adoption because life-cycle savings offset capex sooner. Until component prices fall or subsidy ceilings rise, sticker shock will continue to lop roughly 0.4 percentage points from the Austria heat pump market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Systems Hedge Grid Limits

Air-source units captured the largest slice of 2025 installations, accounting for 47.78% of the Austria heat pump market share in that year. Cost-effective outdoor placement and minimal civil work make them the go-to solution for multi-family retrofits, especially in Vienna’s dense districts. Hybrid configurations are the fastest climber at a 3.03% CAGR through 2031, as owners in rural villages pair heat pumps with biomass or gas boilers to avoid transformer overload notices from grid operators. Water-source machines remain tiny in number yet post high efficiencies near riverside factories and lakeside hotels. Ground-source adoption inches upward where geology is favorable, but drilling bans in karst belts impose extra paperwork and EUR 5,000-10,000 (USD 5,650-11,300) in survey fees.

The hybrid trend gives contractors a transitional sales story: run the heat pump during shoulder seasons, then switch to the legacy boiler in deep winter, squeezing operating costs while containing capex. In alpine valleys, where outdoor design temperatures plunge to -15 °C, that dual-fuel resilience reassures risk-averse buyers. Policy still recognizes hybrid systems as renewable when the annual energy share from the heat pump tops 50%, so subsidy eligibility remains intact. The Austria heat pump market size tied to hybrid models therefore rises steadily even if all-electric penetration plateaus in grid-strained postal codes.

By Technology: Air-to-Water Leads, Ground-to-Water Gains

Air-to-water machines supplied 46.31% of 2025 deployments, reflecting their plug-and-play compatibility with Austria’s radiator network. Design tweaks such as inverter-driven compressors and R290 refrigerant chemistries now push flow temperatures to 75 °C, allowing one-for-one boiler swaps without radiator upsizing. Ground-to-water units show a 2.87% annual growth outlook, underpinned by new-build codes that hard-wire geothermal loops into foundation designs and by district projects like Aspern Seestadt. Air-to-air remains a marginal choice in homes but pops up in retail spaces with existing ductwork.

Seasonal performance remains the trump card for ground-coupled systems; coefficients north of 5.0 cut electricity bills sharply, a critical hook in provinces where tariffs hover around EUR 0.22 (USD 0.25) per kWh. Yet upfront drilling costs and six-month permit queues temper the climb. Meanwhile, water-to-water installations in Vienna’s waste-to-energy plant and Carinthia’s lakeside resorts prove the viability of niche aquatic loops. As high-temperature R290 units mature, the Austria heat pump market size for air-to-water is expected to hold its lead without ceding much ground to the more expensive borehole category

By Capacity: Mid-Range Dominates While 50-200 kW Surges

Systems rated 10-50 kW delivered 36.23% of 2025 revenue, solidifying their role in small hotels, multi-family blocks, and farmhouses. Product catalogs are standardized in this band, which trims engineering hours and lets installers complete jobs in two to three days. The 50-200 kW tier is projected to expand at a 2.69% CAGR through 2031, riding industrial decarbonization budgets in food processing, brewing, and light manufacturing. Below-10 kW units chase single-family homes but face intense price competition that erodes margins.

Large-capacity growth is tied to steam temperatures above 150 °C. Ecop Technologies’ 700 kW platform, now moving into serial build, can reach 200 °C with a coefficient as high as 7, creating attractive payback math under rising EU ETS carbon prices. For utilities contemplating district heat pumps, modular cascades of 250-500 kW skids lower capital risk and simplify phased buildouts. Therefore, while mid-range machines hold volume leadership, the Austria heat pump market size within the 50-200 kW corridor posts the fastest euro growth.

By Application: Hot Water Still Leads, Industrial Heat Climbs

Domestic and sanitary hot water retained 50.82% share in 2025 because Austrian code demands 60 °C storage to control Legionella. Eighty-gallon integrated tanks with R290 charge sizes under 150 g keep compliance simple and subsidy eligibility intact. Industrial and process heat registers the quickest expansion at 3.24% CAGR, as pharmaceutical clean-steam loops and dairy pasteurization lines pivot from gas boilers to high-temperature heat pumps.

Space heating grows more modestly in line with renovation cycles, while reversible units unlock summer cooling for office retrofits without new chiller plants. Niche uses such as snow-melt systems and swimming pools widen market visibility in alpine resorts but add limited volume. Still, every new industrial pilot that replaces a 10 bar steam boiler strengthens the credibility of high-temperature solutions and pulls additional capex into the Austria heat pump market.

By End User: Residential Still Front-Runner, Commercial Accelerates

Residential properties produced 54.09% of 2025 installations, driven by the replacement of about 600,000 oil boilers and 1.2 million gas units. Application forms on the Austrian Energy Agency portal now auto-fill subsidy fields, trimming paperwork and keeping conversion momentum high. Commercial premises, hotels, retail centers, and hospitals, show a 2.58% CAGR, spurred by net-zero pledges and 2030 EPC class-C mandates. Industrial clients remain smaller in count but supply outsized euro value when they commit to megawatt-scale units.

Landlords grapple with split-incentive dynamics: they fund the heat pump, tenants pocket the energy savings. Some provinces now allow rent surcharges pegged to measured efficiency gains, easing subsidy cash-flow gaps. Meanwhile, business owners calculate carbon levies under the EU ETS and conclude that a seven-year payback beats open-ended emission charges. The Austria heat pump market therefore spreads more evenly across user groups each year, diversifying revenue risk.

By Installation: Retrofit Commands, New Build Advances

Retrofits accounted for 63.43% of 2025 orders because the fossil boiler fleet is both old and extensive. Courtyard noise limits under 30 dB force contractors to select ultra-quiet outdoor units or small façade cassettes, yet subsidy generosity keeps closing rates high. New construction posts a 2.47% CAGR through 2031 as every permit issued after January 2025 requires a renewable primary system, typically a ground-loop heat pump paired with underfloor heating.

For new builds, design engineers choose 35-40 °C flow temperatures that lift seasonal COPs above 5.0, making the Austria heat pump market size in this slice the efficiency champion. Retrofit officers meanwhile must juggle 60-70 °C radiator circuits that dock COPs by 15-25%. Vienna’s single-window portal sliced permit times from twelve to four weeks, a best-practice now spreading to Graz and Linz, ensuring both segments maintain solid volume growth.

Geography Analysis

Vienna leads national demand thanks to its goal of retiring 600,000 gas heaters by 2040, a target equal to one-quarter of Austria’s fossil units. Façade-mounted micro heat pumps and shallow geothermal fields in projects like Aspern Seestadt demonstrate how dense districts can scale electrified heating without new chimney stacks. Lower Austria and Styria excel in ground-source penetration because provincial grants layer EUR 2,000-3,000 (USD 2,260-3,390) atop federal subsidies, yet drilling moratoriums in sensitive karst pockets stretch project times by nine months.

Tyrol, Salzburg, and Vorarlberg enjoy hydro-rich grids that supply 0.18-0.20 EUR (USD 0.20-0.23) per kWh retail tariffs, trimming residential paybacks to six-eight years. Ski resorts repurpose lift-motor waste heat for snow-melt systems, shaving 80,000 L of heating oil each season and broadcasting success stories that ripple through the Austria heat pump market. Rural Burgenland and parts of Upper Austria face transformer overload alerts that limit simultaneous installations; substation upgrades cost EUR 50,000-150,000 (USD 56,500-169,500) and queue behind regional budgets, elongating adoption curves.

Graz and Linz mirror Vienna’s district-heating decarbonization on smaller grids, anchoring multi-megawatt heat pumps to waste-water streams and geothermal wells. Carinthia’s lakefront villas dabble in water-source systems, but strict ecological caps temper volume. Vorarlberg already mandates renewable heat in every new home, whereas Burgenland permits hybrid systems until 2027, reflecting divergent provincial politics. A EUR 50 million (USD 56.5 million) Climate and Energy Fund tranche steers installers toward towns under 10,000 people, rebalancing geographic equity within the Austria heat pump market.

Competitive Landscape

The Austria heat pump market remains moderately fragmented. Domestic makers, OCHSNER, iDM Energiesysteme, Heliotherm, M-TEC, and OVUM, command strong dealer networks and alpine-focused R&D, securing about 60% combined share. Multinationals such as Vaillant, Bosch, Daikin, Mitsubishi Electric, and LG Electronics leverage larger component pipelines to sharpen R290 pricing and erode local margins. Chinese firms are courted by distributors but still battle tariff walls and brand perceptions.

Strategic tie-ups shift the chessboard. In August 2025, Windhager teamed with Heliotherm on modular systems spanning 3 kW-1 MW at seasonal COPs above 6.0, giving district operators a turnkey menu. January 2025 saw VERBUND partner with Viessmann and a major bank to bundle gear, finance, and maintenance in one bill, simplifying residential take-up. Ecop Technologies scales 700 kW high-temperature machines to 200 °C, courting dairy, pharma, and paper plants that need clean steam. Acoustic engineering is another battlefield: Daikin’s Altherma 4 hits 28 dB at one meter, passing Vienna’s strict courtyard test.

Software adds differentiation. iDM’s Navigator platform integrates tariff forecasts and PV self-consumption, cutting running costs 10-15%. Bosch rolls out remote diagnostics via 4G modems, slashing service truck rolls by one-third. As EU F-Gas quotas tighten, firms able to certify multi-circuit R290 designs will widen their moat. With the five largest vendors holding roughly 60% share, the market concentration score is 6, signaling balanced rivalry with room for niche innovators.

Austria Heat Pump Industry Leaders

Vaillant Group

Bosch Group

Stiebel Eltron GmbH & Co. KG

Carrier Global Corporation

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ECOTHERM Austria began in-house production of 50-500 kW commercial heat pumps to localize supply and reduce import risk.

- January 2026: Heizma secured EUR 2.5 million (USD 2.8 million) and named Viessmann as core supplier to scale its installer network nationwide.

- December 2025: Airvance Group bought a majority interest in distributor IPK, adding EUR 17 million (USD 18.4 million) in Central European sales.

- October 2025: Daikin Austria launched the ultra-quiet R290 Altherma 4 series aimed at urban retrofits with 28 dB sound pressure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Austria heat pump market as annual revenue generated from newly manufactured air-source, water-source, and ground-source units rated below 1 MW that provide space heating, space cooling, or sanitary hot water to residential, commercial, industrial, and institutional end users.

Scope exclusion: Used equipment, chillers primarily designed for cooling, and packaged VRF systems are left out to keep the focus squarely on purpose-built heat pumps.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Austrian installers, heat pump OEM sales managers, utility program officers, and energy efficiency consultants across Vienna, Upper Austria, and Styria. These conversations tested adoption hurdles, average selling prices, and subsidy pass-throughs, letting us fine-tune assumptions surfaced during desk work.

Desk Research

We begin by compiling installation, building stock, and energy mix data from bodies such as Statistik Austria, the European Heat Pump Association, the International Energy Agency, and the Ministry for Climate Action, which give us baseline technology penetration and policy signals. Next, trade statistics from Eurostat COMEXT, customs tariff 841861, and patent trends mined through Questel help us gauge import intensity and innovation pipelines. Company filings, investor decks, and reputable press articles supplement pricing corridors and channel behavior. Paid resources like D&B Hoovers and Dow Jones Factiva provide hard-to-find financials and news. This list is illustrative, not exhaustive; many other public and proprietary sources were referenced while validating numbers and clarifying definitions.

Market-Sizing & Forecasting

A top-down model reconstructs demand from the dwelling stock, new housing completions, non-residential floor area additions, and historical replacement cycles, which are then valued through weighted average selling prices verified in interviews. Bottom-up cross-checks, sampled supplier revenue roll-ups and distributor channel checks flag mismatches. Key variables include subsidy uptake rates, electricity-to-gas price spreads, seasonal performance factors, building renovation rates, and installer capacity. A multivariate regression projects each driver through 2030, while scenario analysis tests policy or fuel price shocks. Gaps in segment totals are bridged using conservative midpoint estimates from verifiable ranges before aggregation.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, followed by variance checks against EHPA unit sales and Statistik Austria construction data. Models refresh every twelve months, with interim revisions triggered by material subsidy changes or major fuel price swings, ensuring clients receive the latest view.

Why Mordor's Austria Heat Pump Valuation Commands Reliability

Published figures often diverge because firms choose different product baskets, base years, and forecast logics. We acknowledge those gaps up front and explain them so decision makers see where numbers separate.

Key gap drivers include: (1) whether air-to-air units are counted, (2) use of nominal versus transaction prices, (3) assumptions on subsidy-driven demand spikes, and (4) refresh cadence. Mordor's scope aligns with EHPA definitions yet removes legacy cooling-centric products, and our model is recalibrated annually, limiting drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 244.5 M (2025) | Mordor Intelligence | - |

| USD 773.8 M (2024) | Regional Consultancy A | Includes air-to-air units and applies aggressive subsidy uptake curve |

| USD 40 M (2024) | Trade Journal B | Tracks only Prodcom 28251380 exports; excludes domestic air-source sales and retail mark-ups |

These comparisons show why our balanced product scope, dual-track modeling, and annual updates give stakeholders a dependable baseline that is traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of Austria’s heat pump market and how much is it expected to be worth by 2031?

Revenue stood at USD 244.48 million in 2025 and is forecast to climb to USD 283.07 million by 2031, reflecting steady uptake in both retrofit and new-build applications.

Which factors are driving the strongest year-on-year growth in Austrian heat pump sales?

Generous "Raus aus Öl und Gas" renovation grants, a legally binding 2040 net-zero target, and the EU REPowerEU program collectively accelerate adoption by reducing payback times and clarifying long-term policy signals.

Why are hybrid heat pump systems particularly attractive in rural Austria?

They let owners rely on the heat pump under moderate loads and switch to an existing biomass or gas boiler during extreme cold, avoiding costly feeder upgrades where three-phase grid capacity is limited.

Which capacity range is expanding fastest among commercial and light-industrial buyers?

Units rated 50-200 kW post the quickest advance as hotels, dairies, and food processors replace mid-size gas boilers with high-temperature models delivering up to 200 °C process heat.

How does Vienna's decarbonization roadmap influence nationwide installation trends?

By targeting the phase-out of 600,000 gas heaters by 2040, the capital sets high volume requirements, speeds permitting with a one-stop portal, and establishes façade-mounted micro units as a template for other dense cities.

What technical hurdle most often delays ground-source projects in Styria and Lower Austria?

Karst-zone borehole permits require hydrogeological surveys and monitoring wells, adding EUR 5,000-10,000 in costs and up to nine months of additional approvals before drilling can begin.

Page last updated on: