Hungary Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

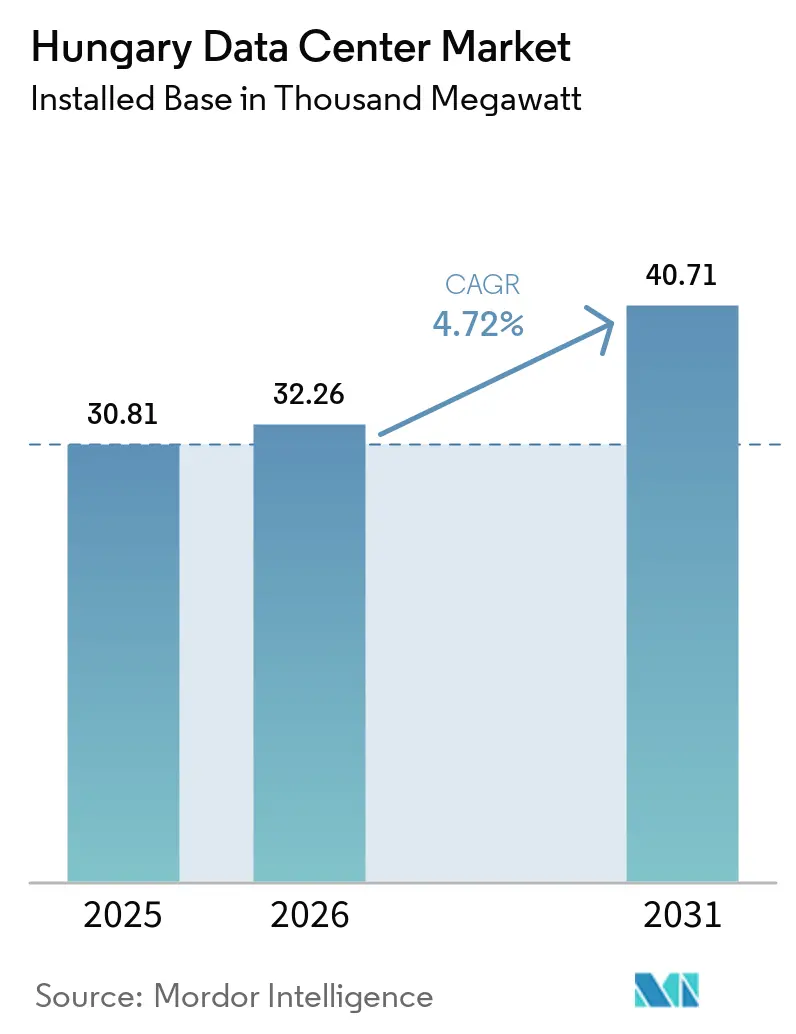

| Base Year Market Size (2025) | 30.81 Thousand megawatt |

| Market Volume (2026) | 32.26 Thousand megawatt |

| Market Volume (2031) | 40.71 Thousand megawatt |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Data Center Market Analysis by Mordor Intelligence

The Hungary data center market size is expected to increase from 30.81 MW in 2025 to 32.26 MW in 2026 and reach 40.71 MW by 2031, growing at a CAGR of 4.72% over 2026-2031. In 2026, Hungary data center market witnessed a significant capacity surge, signaling a departure from its previously slower colocation trend. This shift is largely driven by heightened enterprise digitalization, sovereign cloud mandates, and public investment initiatives, all of which are bolstering domestic computing workloads. While large corporations have swiftly embraced cloud solutions, small and medium-sized enterprises lag, presenting a substantial opportunity for further migration to hosted infrastructures.[1] This trend not only extends Hungary data center market's growth trajectory through 2031 but also underscores the demand for operators who can provide robust power solutions, enhanced interconnectivity, and facilities compliant with regulatory standards, moving beyond mere basic rack offerings. However, challenges persist, as electricity price fluctuations and protracted permitting processes influence the pace at which new projects transition from the drawing board to operational status.

Key Report Takeaways

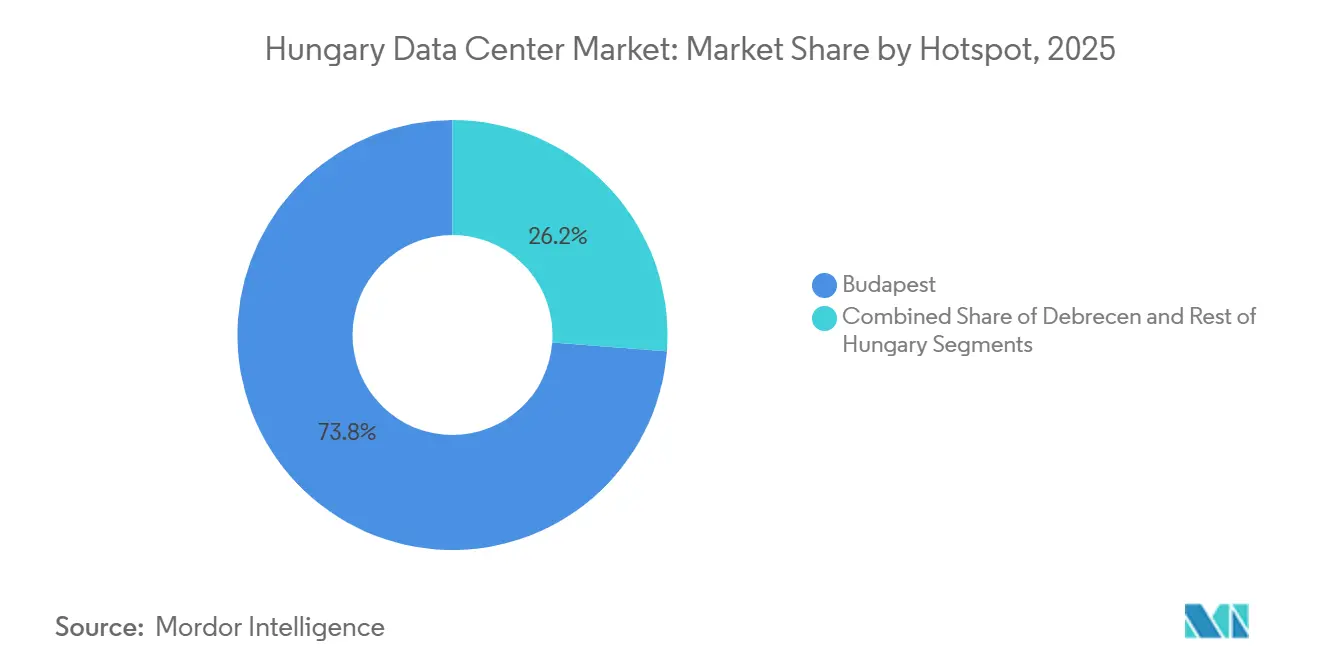

- By hotspot, Budapest held 73.8% of the Hungary data center market share in 2025, while Debrecen recorded the highest projected CAGR at 11.4% through 2031.

- By data-center size, medium facilities accounted for 37.6% of the Hungary data center market size in 2025, while mega-scale campuses are projected to expand at a 12% CAGR through 2031.

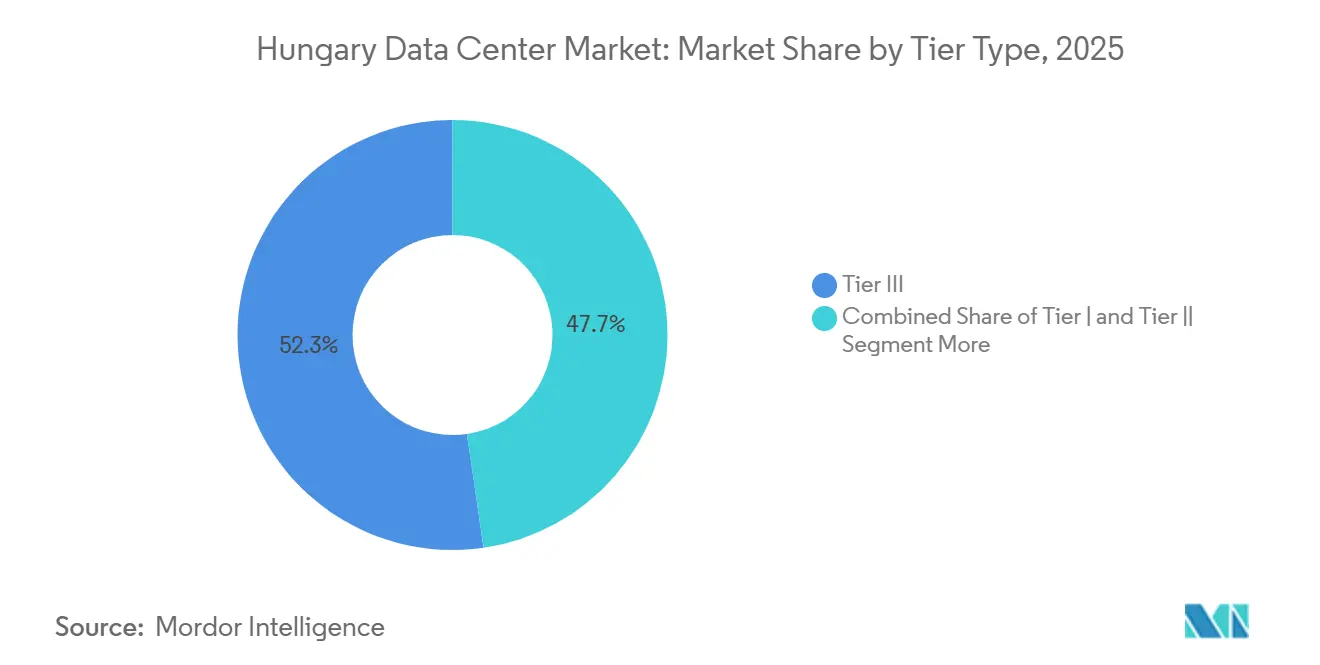

- By tier type, Tier 3 held 52.3% of the Hungary data center market share in 2025, while Tier 4 recorded the fastest projected CAGR at 14.2% through 2031.

- By absorption, the utilized segment captured 70.7% of total installed capacity in 2025, while hyperscale colocation is forecast to grow at a 15.5% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hungary Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Cloud-Service Uptake Among Hungarian SMEs | +1.8% | National, with early concentration in Budapest and Debrecen | Medium term (2-4 years) |

| Government Digital Success Program 2030 Incentives | +1.0% | National, public-sector nodes concentrated in Budapest | Medium term (2-4 years) |

| EU-Funded 5G and National Fiber Backbone Expansion | +0.7% | National, spill-over gains along Budapest-Debrecen corridor | Short term (≤ 2 years) |

| Low-Latency Demand From Hungary's Fast-Growing Online-Gaming Sector | +0.4% | Budapest metro, with secondary signal in Debrecen | Short term (≤ 2 years) |

| In-Country Data-Sovereignty Regulations | +0.2% | National, government and BFSI nodes only | Long term (≥ 4 years) |

| Long-Term Renewable-Energy PPAs Lowering Power-Cost Volatility | +0.2% | National, with early uptake near southern solar corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud-Service Uptake Among Hungarian SMEs

Over the past decade, SMEs in Hungary have increasingly turned to cloud solutions. However, despite this growth, Hungary's adoption rate still lags behind the EU average, indicating untapped potential for local hosting migrations. Research indicates that while service-oriented sectors have rapidly embraced cloud solutions, the manufacturing sector has been slower to adapt. This delay suggests that a significant portion of industrial demand remains untransformed, pointing to a future increase in colocation transitions. Reports indicate that 37.12% of Hungarian enterprises have adopted cloud solutions. Large enterprises have notably outpaced SMEs in this adoption, highlighting a structural gap that could drive future data center demand. Projections suggest that aligning Hungary's cloud adoption with the EU average could increase the nation's GDP by 1.7 to 2.7 percent annually over the next decade. This potential economic growth underscores the ongoing policy support for digital workload migrations. For the Hungary data center market, the rise in SME cloud adoption not only increases traffic but also broadens the customer base, extending beyond the largest enterprises.[2]European Commission, “Commission Staff Working Document Digital Decade 2025 Country Reports: Hungary,” European Commission, europa.eu This evolving trend supports consistent demand for retail colocation, managed hosting, backup solutions, and hybrid deployments across the nation.

Government Digital Success Program 2030 Incentives

Hungary has rolled out 44 measures under its updated national roadmap, part of the broader Digital Decade initiative, with a budget allocation of EUR 2.489 billion (USD 2.69 billion). Of this total, EUR 1.822 billion (USD 1.97 billion) is sourced mainly from public budgets, with the European Union stepping in as the predominant financier. The allocated funds aim to boost connectivity, propel digitalization, and strengthen key technology programs. This strategic move highlights the intertwined nature of public-sector IT demands and the deployment of domestic infrastructure. Hungary's government cloud, Kormányzati Adatközpont, has successfully onboarded 179 specialized systems tailored for public administration. This move underscores the tangible nature of Hungary's sovereign infrastructure policy, marking it as an essential element for the nation. Such advancements hold considerable weight for Hungary data center market. Public-sector operations often necessitate heightened resilience, rigorous audit preparedness, and prolonged contract oversight, distinguishing them from commercial demands. These elevated standards frequently tilt the preference towards premium colocation services rather than standard hosting. Additionally, they amplify the importance of Budapest and other secure domestic hubs for operators keen on tapping into state-led digital ventures.

EU-Funded 5G and National Fiber Backbone Expansion

In last year, Hungary's fiber-to-the-premises penetration reached 79.86%, surpassing the European Union's average of 69.24%. Additionally, 39.81% of households in Hungary accessed fixed broadband speeds of at least 1 Gbps, significantly exceeding the European Union average of 22.25%. Under the Gigabit Hungary Programme, optical connectivity is being deployed to over 195,000 service locations, 1,000 mobile base stations, and 731 public institutions across all 174 districts outside Budapest. Notably, the majority of this expansion is mandated to utilize FTTH technology. This broader access network is critical, as it extends the reach for cloud, edge, and managed infrastructure demands beyond the capital. In a related development, EXA Infrastructure initiated Project Visegrád in September 2025, aiming to connect Budapest directly with its networks in Berlin, Frankfurt, and Vienna. The first routes are expected to become operational by mid-2026. For the Hungary data center market, enhanced domestic fiber and a robust cross-border backbone not only strengthen local service delivery but also increase the region's interconnection appeal. This combination reinforces Budapest's central role while also elevating secondary nodes, enabling them to meet institutional and industrial demands with reduced latency and improved backhaul.

Low-Latency Demand From Hungary's Fast-Growing Online-Gaming Sector

In Hungary's data center market, the demand for low-latency digital services is surging, driven by a premium on proximity, interconnection density, and stable urban network access. This trend is particularly pronounced in Budapest, where the strength of carrier-neutral connectivity outshines other domestic locales, bolstering the delivery of time-sensitive applications. By 2026, Hungary boasted high-speed broadband availability that met stringent EU standards, enhancing access for end-users reliant on latency-sensitive digital services. As digital entertainment platforms increasingly prioritize swift local response times, urban facilities boasting dense peering and a multitude of carrier options stand poised to capture a larger share of traffic and hosting demand. While this trend is overshadowed by cloud and policy influences, it nonetheless bolsters premium colocation sites where network quality is as crucial as physical space. Furthermore, it benefits operators adept at merging deep interconnection capabilities with elevated rack density in city-centric facilities.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Electricity-Price Volatility Tied to Regional Gas Supply | -0.8% | National, most acute in Budapest metro grid | Short term (≤ 2 years) |

| Lengthy Permitting and Environmental-Impact Clearances | -0.5% | National, with bottlenecks concentrated around Greater Budapest nodes | Medium term (2-4 years) |

| Shortage of Certified Data-Center Engineers and Technicians | -0.4% | National | Long term (≥ 4 years) |

| Grid-Connection Congestion in Greater Budapest Nodes | -0.3% | Greater Budapest metro only | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Electricity-Price Volatility Tied To Regional Gas Supply

Electricity cost volatility poses a significant operational risk for Hungary data center market, given that energy constitutes a major portion of recurring facility expenses. In 2024, Hungary's day-ahead market averaged EUR 87 per MWh, with a notable spike in November reaching EUR 163.72 per MWh. The report further highlighted that during peak summer hours from July to September, prices in Hungary surpassed EUR 300 per MWh on over 104 occasions, driven by system pressures from a heatwave and limited import flexibility. Such price fluctuations complicate multi-year cost modeling for operators, particularly in a market that is still expanding its capacity and exploring new build economics. The challenge intensifies for mixed-vintage facilities, where varying efficiency levels mean that power-price shocks impact margins unevenly. Consequently, strategies like power hedging, procurement, and renewable sourcing are gaining equal importance to location and connectivity in project planning.

Lengthy Permitting and Environmental-Impact Clearances

In Hungary, the data center market grapples with significant hurdles due to stringent permitting processes. Large-scale projects often face multi-stage environmental reviews before breaking ground. According to Government Decree 314/2005, environmental impact assessments can involve up to 30 days of public commentary, possible hearings, and municipal input. Notably, for projects meeting certain thresholds (Annex 1 or Annex 3), this process can stretch from 18 to 24 months. Starting January 2025, Act C of 2023 on Hungarian Architecture introduced a more pronounced brownfield-first strategy. Furthermore, projects on plots exceeding 5,000 m² now mandate a green area certificate. While these regulations have not deterred investments, they have heightened the value of sites with clear planning, utility access, and minimal land-use disputes. Additionally, grid-connection tasks for high-voltage substations (over 35 kV) necessitate preliminary examinations. This intertwines power and site approvals. Consequently, for newcomers eyeing greenfield projects, these timing risks are significant, warranting careful consideration in capital expenditure planning and customer commitment timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotspot: Budapest's Scale Meets Debrecen's Industrial Momentum

In 2025, Budapest dominated Hungary's data center landscape, boasting a commanding 73.8% share of the total installed capacity. This stronghold can be attributed to the capital's robust carrier-neutral density, well-established colocation clusters, and a rich interconnection environment, all of which consistently draw in enterprise and network traffic. This concentration is not merely a historical artifact; it is bolstered by network effects that secondary cities find challenging to replicate swiftly. Facilities linked to the primary exchange fabric enjoy enhanced routing options and heightened commercial significance for national enterprises.

Debrecen, on the other hand, is poised for rapid expansion, forecasting an 11.4% CAGR through 2031. Unlike Budapest, Debrecen's demand is more closely aligned with manufacturing-driven digitalization. The region's substantial industrial investments are fueling local needs, from predictive maintenance to data exchanges with suppliers. This positions Debrecen as a significant growth hub for Hungary's data center industry, complementing the capital's dominance. While other regions in Hungary hold a smaller stake, they are not without notable projects. For instance, the University of Debrecen inaugurated its UDBD-Health hybrid data warehouse in November 2025, aimed at bolstering health analytics and AI research. Furthermore, the potential Paks Data Centre Campus, backed by a July 2025 letter of intent from ParTec AG and 3D Lézertechnika Zrt. for a modular hyperscale AI data center eyeing a 2027 launch, could further diversify Hungary's data center geography.[3]Magyar Nemzet, “Modellértékű Adattárházat Sikerült Kialakítani Debrecenben,” Magyar Nemzet, magyarnemzet.hu If realized, this project could dilute the current concentration of Hungary's data center market, traditionally centered around the Budapest-Debrecen axis.

By Data-Center Size: Medium Facilities Lead While Larger Campuses Gain Ground

In 2025, medium facilities commanded a dominant 37.6% share, underscoring the entrenched position of national enterprise colocation in Hungary's data center landscape. Historically, domestic operators tailored many facilities to cater to enterprise and mid-market demands, steering clear of hyperscale campus deployments. While small facilities catered to retail hosting and SME needs, larger sites focused on clients requiring dedicated power blocks, stopping short of true campus-scale expansions. This diverse mix elucidates why medium facilities maintained their lead, even as the development pipeline began to evolve.

Projected to grow at a 12% CAGR through 2031, mega-scale data centers are signaling a shift in procurement behaviors, not just an expansion in building sizes. The demands of AI workloads and GPU-centric infrastructures necessitate contiguous power, advanced cooling systems, and site designs that accommodate denser technical configurations. While the massive-scale segment is still nascent in Hungary's data center scene, its significance is on the rise, especially with the Paks proposal and other large-site opportunities gaining traction. Concurrently, the European Energy Efficiency Directive has spotlighted PUE reporting for data centers boasting over 500 kW of installed IT power. This emphasis is steering operators toward enhanced cooling and power management practices. Consequently, the competition for size has evolved; it is now as much about the ability to provide dense power efficiently and in compliance as it is about the sheer amount of available white space.

By Tier Type: Tier 3 Holds The Base While Tier 4 Expands Faster

In 2025, Tier 3 facilities dominated the Hungary data center market, capturing 52.3% of the total capacity. This dominance underscores a significant shift in the commercial colocation landscape, moving away from lower-spec environments. For many enterprises, Tier 3 strikes an ideal balance, offering robust service-level commitments suitable for most business workloads, all without the need for a fully fault-tolerant architecture.

Tier 4 facilities are set to experience a robust growth spurt, with projections indicating a 14.2% CAGR through 2031. This surge is largely attributed to customer segments demanding heightened resilience and security. Supporting this trend, Act LXIX of 2024, which addresses Hungary's Cybersecurity, has categorized critical digital infrastructure into higher-risk tiers. This classification bolsters the demand for facilities that adhere to stringent operating standards. Notably, sectors like BFSI and government are at the forefront, emphasizing the importance of audit readiness, continuity, and mission-critical uptime. While Tier 1 and Tier 2 facilities still cater to legacy on-premise and mid-market scenarios, their significance is waning as client expectations escalate. Consequently, operators are now challenged to demonstrate resilience through design, disciplined processes, and certifications, rather than merely offering available space.

By Absorption: Utilized Capacity Leads While Hyperscale Changes the Mix

In 2025, Hungary's data center market showcased a robust demand, with utilized capacity reaching 70.7% of the total installed capacity. This indicates that the market's activity was driven by genuine demand rather than speculative oversupply. The non-utilized capacity primarily stemmed from newly commissioned spaces and projects initiated ahead of their anticipated demand. Among the utilized segments, hyperscale colocation is projected to lead with a rapid growth rate of 15.5% CAGR through 2031, highlighting a significant shift in the drivers of capacity absorption.

While retail colocation remains vital, catering to SMEs and mid-sized enterprises with their incremental space and power needs, the landscape is evolving. Cloud services and government workloads are increasingly gravitating towards high-spec facilities, particularly those offering substantial resilient power. In September 2025, 4iG's ITU-EKIP presentation highlighted the establishment of 4,500 m² of data center infrastructure and a power capacity of 3.4 MW at its sites in Budapest and Southern Great Plain. The presentation also underscored the active planning of hyperscaler data center projects in Hungary. On the government front, the significance is underscored by the central KAK facility's connection to 179 public administration systems, bolstering a consistent domestic IT load and reinforcing the demand for compliant hosting. For Hungary's data center operators, this evolving landscape suggests that future absorption will hinge more on tenant profiles, resilience needs, and contract quality than mere occupancy rates.

Geography Analysis

In 2025, Budapest dominated Hungary's data center landscape, boasting a commanding 73.8% share of the nation's total installed capacity. The capital city enjoys the advantage of housing the country's most concentrated network of carrier-neutral infrastructures, well-established campuses, and key interconnection routes. In January 2025, GNM.NET inaugurated its inaugural Hungarian presence at Dataplex, rolling out over 600 ASN internet exchange services. This move not only catered to enterprises in Hungary but also extended its reach to the broader Central and Eastern European (CEE) region, underscoring Budapest's status as the primary interconnection hub for international carriers. Furthermore, in 2024, Hungary achieved a notable 39.81% uptake in fixed broadband subscriptions at speeds of 1 Gbps or higher, bolstering Budapest's position as a pivotal hub for latency-sensitive operations.

Debrecen is emerging as a significant player, with projections indicating an 11.4% CAGR from 2026 to 2031. This positions Debrecen as the most promising contender in Hungary's data center landscape, trailing only Budapest. Unlike Budapest, Debrecen's demand is predominantly industrial rather than exchange-driven. This shift is largely attributed to heightened manufacturing investments in the region, spurring local demands for IT operations, process monitoring, and data management in supply chains. Further solidifying Debrecen's growing prominence, 2Connect, a subsidiary of 4iG, secured HUF 11.59 billion (USD 30.9 million) from the second phase of the Gigabit Hungary Programme. This funding aims to extend fiber connectivity into 16 new districts, notably those linked to eastern Hungary's burgeoning industrial corridor. Additionally, the University of Debrecen's UDBD-Health initiative highlights the city's diverse demand. This project, a hybrid environment, is tailored for extensive clinical and research tasks, emphasizing that the region's needs extend beyond just industrial factories.

While other regions in Hungary currently hold a modest share of the data center market, they are starting to draw attention with project-led capacities, hinting at a potential shift in the national landscape post-2027. A prime illustration is ParTec AG's ambitious plan for a EUR 3 billion (USD 3.24 billion) AI-centric data center campus adjacent to the Paks nuclear power plant. This expansive project is set to feature a power consumption of up to 96 MW, a sprawling 530-hectare agro-photovoltaic park, and integrated battery storage. Until such monumental projects come to fruition, these non-core regions will primarily cater to local enterprises, institutions, and public services, all bolstered by an ever-expanding fiber network. Yet, this trajectory suggests a promising evolution for Hungary's data center market, steering towards a more geographically diverse capital landscape.

Competitive Landscape

In 2026, Hungary's data center market exhibited moderate fragmentation. Key players like 4iG, Magyar Telekom, and Telekom Rendszerintegráció Zrt., often linked to telecoms, secured significant positions in enterprise colocation. Meanwhile, neutral operators such as RackForest, VIVAnet DC, and Servergarden Kft. vied for dominance, emphasizing network flexibility and closeness to primary exchange environments. A notable strategic maneuver was 4iG's infrastructure consolidation in June 2025. In a significant move, AH Infrastruktúra, Invitech ICT Infrastructure, V-Hálózat, and D-Infrastruktúra unified under the banner of 2Connect BSE.HU. This consolidation aggregated an impressive 42,000 km of optical backbone and 12 data center sites into a singular carrier infrastructure, bolstering 4iG's stature in Hungary's data center arena. Furthermore, this maneuver amplified the strategic significance of independent operators, especially those offering carrier-neutral pricing, alleviating concerns tied to reliance on a single provider. Another pivotal moment unfolded in July 2025, as 4iG inked a non-binding MoU with Emirates Telecommunications Group, signaling intentions for expansive data center developments in both Hungary and Albania.

While larger players dominate, smaller operators carve their niche in the competitive landscape, emphasizing targeted efficiency and connectivity over sheer scale. VIVAnet DC proudly announced the operational launch of its first phase, boasting 140 racks, a PUE of 1.39, and dual redundant 1 MW transformers. They also secured a direct BIX connection via dark fiber from four distinct providers. This model underscores the viability of a compact, carrier-neutral site in Hungary's data center landscape, sidestepping the need to rival the expansive footprints of telecom giants. It further underscores the allure of efficient urban facilities for enterprise clients prioritizing interconnection and service adaptability. While Debrecen's industrial colocation and Tier 4 contracts in sectors like healthcare and finance remain less saturated than Budapest's core, they present selective expansion opportunities.

In December 2025, 4iG Informatikai Zrt. made headlines by acquiring a 90% stake in Mobil Adat Kft. This strategic acquisition aims to bolster 4iG's portfolio in managed IoT and M2M data communications, targeting sectors like manufacturing, utilities, and EV charging. The significance of this transaction lies in its potential to closely integrate sensor and communication services with backend infrastructure. Such a synergy could seamlessly transition data transmission demands into hosting demands in the foreseeable future. Insights from the ITU-EKIP presentation revealed 4iG's forward-thinking approach, as they sculpt their infrastructure roadmap around emerging hyperscaler prospects. This indicates a strategic pivot, with competitive positioning extending beyond traditional retail colocation realms. Ultimately, Hungary's data center landscape is being sculpted by a confluence of scale, certification, network neutrality, and capital access, transcending mere pricing considerations.

Hungary Data Center Industry Leaders

Dataplex Kft. (Telehouse)

4iG Nyrt. (incl. Invitech)

T-Systems Hungary

RackForest Kft.

Servergarden Kft.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: In Hungary, GoldenPeaks Capital signed a long-term "Pay as Nominated" corporate power purchase agreement with Hankook Tire and Technology Co., Ltd. This initiative not only broadens Hungary's corporate PPA market but also provides a benchmark transaction for Hungary data center operators aiming to mitigate HUPX price volatility by securing renewable energy.

- January 2026: Hungary's energy transition planning receives support as FEAK Független Energetikai Adatközpont Zrt., a state-owned energy data center, begins operations. Leveraging AI, the center processes vast amounts of electricity consumption data, positioning itself as the nation's independent energy data management hub.

- December 2025: 4iG Informatikai Zrt. has secured a deal to purchase a 90% stake in Mobil Adat Kft. Mobil Adat, a Hungarian expert in IoT and M2M data transmission, will bolster 4iG's offerings. This acquisition aims to seamlessly integrate services from sensors to Hungary data center, establishing 4iG as a comprehensive provider of IoT and data communication solutions. The focus is on key sectors in Hungary: manufacturing, utilities, and electric vehicle charging.

- December 2025: Under the second phase of the Gigabit Hungary Programme, 4iG's subsidiary, 2Connect, secured a non-repayable EU funding of HUF 11.59 billion (USD 30.9 million). This funding will extend coverage to 16 more districts, linking over 1,000 mobile base stations and 731 public institutions to a fiber infrastructure, crucial for meeting the rising demand of Hungary data center demand.

- September 2025: EXA Infrastructure has unveiled Project Visegrád, marking the most significant cross-border fiber backbone deployment in Central Europe in a quarter-century. This initiative connects Budapest to EXA's expansive hyperscale network spanning Berlin, Frankfurt, and Vienna. The inaugural routes are slated to go live by mid-2026, bolstering Budapest's position as the chief low-latency interconnection hub for the Central and Eastern European (CEE) region, further supporting the Hungary data center market.

Hungary Data Center Market Report Scope

The Hungary Data Center Report is Segmented by Hotspot (Budapest, Debrecen, Rest of Hungary), Data-Center Size (Small, Medium, Large, Mega, Massive), Tier Type (Tier 1 and 2, Tier 3, Tier 4), and Absorption (Utilized [Colocation: Hyperscale, Retail, Wholesale; End-User: BFSI, Cloud, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom], Non-Utilized). The Market Forecasts are Provided in Terms of Volume (MW).

| Budapest |

| Debrecen |

| Rest of Hungary |

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-User | ||

| Non-Utilized | ||

| By Hotspot | Budapest | ||

| Debrecen | |||

| Rest of Hungary | |||

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Absorption | Utilized | By Colocation Type | Hyperscale |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-User | |||

| Non-Utilized | |||

Key Questions Answered in the Report

How large will the Hungary data center market become by 2030?

Forecasts indicate capacity will reach 38.81 MW by 2030, expanding at a 4.72% CAGR from 2025.

Which city is growing fastest in data-center capacity?

Debrecen leads with a projected 5.5% CAGR through 2030, outpacing Budapest due to major automotive and battery investments.

What segment is expected to post the highest growth?

Mega facilities larger than 15 MW are set to grow at 6.9% CAGR, driven by AI-centric hyperscale demand.

How is Hungary addressing power-price volatility for data centers?

Operators increasingly sign long-term renewable PPAs and will benefit from 50 planned grid-storage projects announced in 2024.

Why are Tier IV builds accelerating?

Financial services and government workloads require near-zero downtime to comply with EU NIS2 and ESG mandates.

What role does 5G play in future capacity planning?

EU-funded 5G rollout will raise nationwide availability to 67% by 2025, spawning edge facilities that support latency-critical applications.

Page last updated on: