Czechia Data Center Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

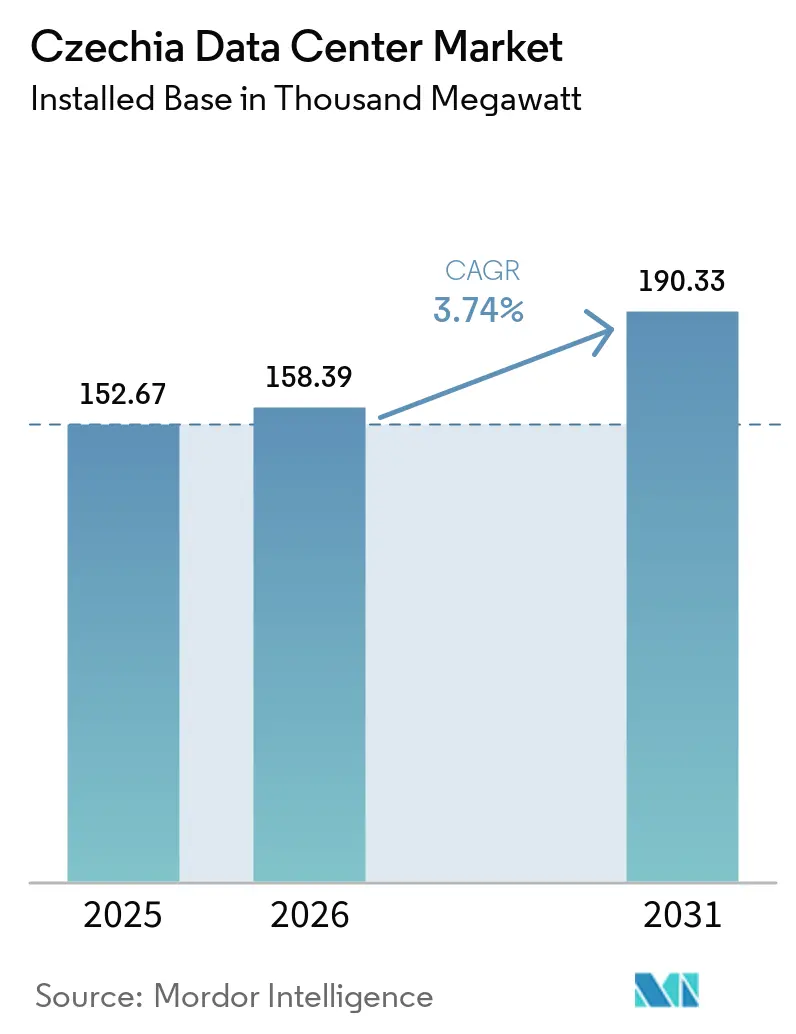

| Base Year Market Size (2025) | 152.67 Thousand megawatt |

| Market Volume (2026) | 158.39 Thousand megawatt |

| Market Volume (2031) | 190.33 Thousand megawatt |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czechia Data Center Market Analysis by Mordor Intelligence

The Czechia data center market size is projected to be 152.67 MW in 2025, 158.39 MW in 2026, and reach 190.33 MW by 2031, growing at a CAGR of 3.74% from 2026 to 2031. The market entered 2026 with immediate momentum from steady colocation absorption in Prague and early capacity additions in South Moravia. This growth in installed IT power shows that the Czechia data center market is moving beyond its earlier role as a relatively small regional node and is becoming a more important part of Central Europe’s digital backbone. Developers are now focusing more on efficient, liquid-cooling-ready facilities than on small rack additions, and that is lifting power density in the incoming pipeline. Demand is also broadening because enterprise cloud migration, public-sector digital programs, and AI-linked hardware and research activity are all adding to the need for secure third-party infrastructure. Competition remains moderate, but grid bottlenecks, higher specialized construction costs, and stricter sovereignty requirements are directing new investment toward larger and better-capitalized operators while creating fresh opportunities outside the most constrained parts of Prague.

Key Report Takeaways

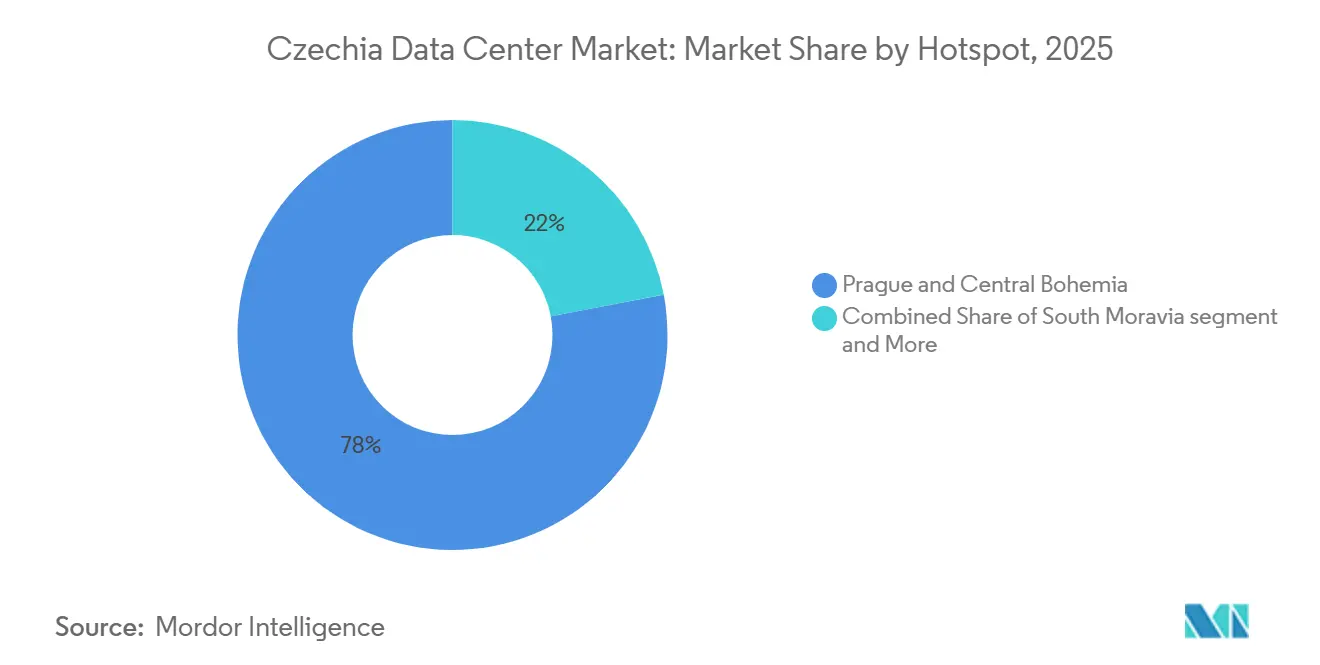

- By hotspot, Prague and Central Bohemia led with a 78.0% share of installed capacity in 2025, while South Moravia is forecast to expand at an 18.3% CAGR from 2026 to 2031.

- By data-center size, medium-sized facilities held a 38.4% share in 2025, while large facilities recorded the highest projected CAGR at 16.2% through 2031.

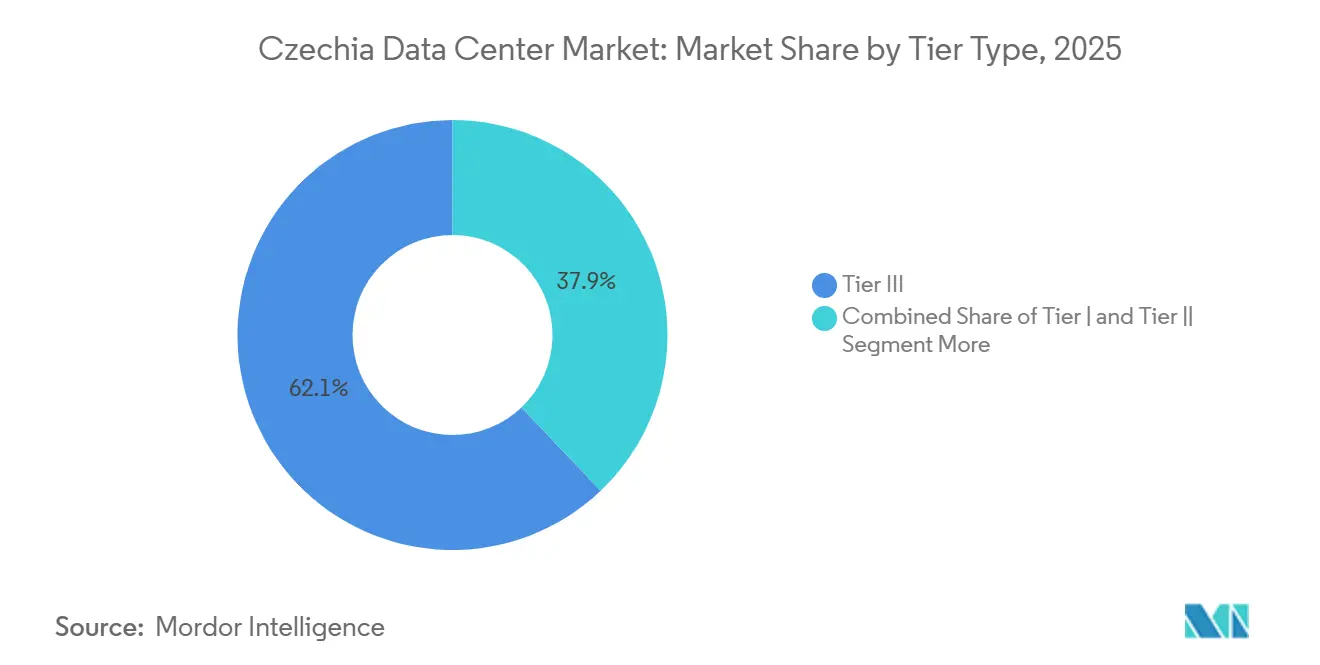

- By tier standard, Tier III installations captured 62.1% of installed capacity in 2025, while Tier IV deployments are projected to grow at a 14.8% CAGR through 2031.

- By absorption, utilized capacity accounted for 83.2% of installed capacity in 2025, while hyperscale colocation is the fastest-growing utilized sub-segment with a 24.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Czechia Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cloud and Hyperscale Adoption Boom. | +1.4% | Prague and Central Bohemia, spillover to South Moravia | Medium term (2-4 years) |

| 5G-Enabled Edge Computing Demand. | +0.8% | Prague, Brno, and Ostrava, corridors along transport and industrial zones | Long term (≥ 4 years) |

| EU and National Digital-Transition Incentives. | +0.6% | National, with early gains in Prague, Brno, and Ostrava | Short term (≤ 2 years) |

| Prague Emerging as DR Hub for DACH Corporates. | +0.4% | Prague and Central Bohemia | Medium term (2-4 years) |

| HPC Manufacturing Footprint Pull-Through. | +0.3% | Central Bohemia, Kutná Hora, with secondary demand in Prague | Long term (≥ 4 years) |

| Peering.cz Traffic Surge and Low-Latency Clustering. | +0.2% | Prague metro carrier-neutral cluster sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud and Hyperscale Adoption Boom

The disparity between large firms and SMEs suggests that as smaller companies modernize and shift away from in-house server rooms, they are increasingly outsourcing workloads. The Czech Recovery and Resilience Plan is investing EUR 1.9 billion (approximately USD 2.05 billion) into digital transition programs.[1]European Commission, “Digital Decade 2025 Country Report - Czechia,” European Commission, digital-strategy.ec.europa.eu This bolsters areas like cloud services, cybersecurity, and managed infrastructure. As a result, the Czechia data center market sees an expanded demand base, with organizations transitioning from initial digital use cases to broader, production-level deployments. In 2025, AWS will secure certification as a trusted cloud provider for Czech government systems, meeting the Security Tier 2 Cloud Act standards. This certification paves a clearer path for public entities to migrate workloads into compliant environments. Furthermore, it bolsters certified colocation and managed hosting providers in the Czechia data center market, as government-linked demand now has a more defined migration route.

5G-Enabled Edge Computing Demand

By 2024, Czechia achieved a notable 99.08% coverage for its 5G population, surpassing the EU's average of 94.35%. In the same year, mobile network investments surged to EUR 422.1 million (equivalent to CZK 10.5 billion or USD 455.9 million), marking a significant 23.6% increase from the previous year. The count of edge nodes skyrocketed from 10 in 2023 to 21 in 2024, with a national goal set at 144 nodes by 2030. Such growth indicates a denser network of carrier-connected micro facilities and local aggregation points, strategically positioned across transport corridors and industrial zones. Furthermore, industrial users are increasingly relocating machine control and Industrial IoT functions closer to data sources. This shift amplifies the demand for near-site computing, bolstered by robust backhaul connections to larger facilities. While the 3.4-3.8 GHz band achieved 42.36% coverage in 2024, it lagged behind the EU's 67.72% average. This gap underscores a sustained demand for edge-related infrastructure throughout the forecast period. Such developments bode well for Czechia's data center market in the long run. Edge locations will rely on a robust national backbone of resilient facilities for traffic aggregation, processing, and exchange.

EU and National Digital-Transition Incentives

The Czech government has earmarked CZK 19 billion (approximately USD 830 million) in its national AI Strategy 2030, bolstering demand for HPC-ready halls and dense colocation pods. The EU Recovery and Resilience Plan, on the other hand, allocates EUR 227 million (around USD 245 million) to projects centered on connectivity, cybersecurity, and cloud initiatives. Notably, a significant 23% of the total Czech allocation from the EU is directed towards digital objectives. Launched in December 2024, the TWIST Programme boasts a budget of EUR 200.88 million (about CZK 5 billion or USD 217 million) and serves as an institutional conduit for quantum, AI, and semiconductor endeavors, all of which necessitate a secure computing infrastructure. Together, these initiatives are creating immediate demand from public institutions, research entities, and private companies as they work to strengthen their digital capabilities in the Czech Republic. Furthermore, Act No. 469/2023 Coll. mandates that data centers consuming over 500 kW report their energy and water usage. Additionally, facilities exceeding 1 MW must adopt waste-heat recovery measures. Such regulations are driving facility upgrades throughout the Czech data center landscape, particularly benefiting operators adept at balancing compliance with efficiency enhancements.

Prague emerging as DR hub for DACH corporates

Prague's direct fiber links to Frankfurt ensure round-trip latency remains under 10 milliseconds. This positions Prague as an optimal disaster recovery hub for DACH users seeking geographic separation while remaining within the European Union. Such connectivity enhances Prague's role in compliance and resilience, surpassing basic cost considerations. CRA's Prague Gateway DC project is designed to deliver 26 megawatts and 2,000 racks. The company has strategically positioned it to address larger international demand, which the current Czech supply has not fully accommodated. The Czech jurisdiction, with its European Union membership, provides separation from Germany, Austria, and Switzerland. This is critical for disaster recovery and active-active deployment strategies for cross-border users. CRA's project pipeline indicates that operators are addressing this broader use case rather than focusing solely on domestic demand. As a result, the Czechia data center market is strengthening its position as a preferred secondary hub for DACH enterprises, emphasizing low latency, legal clarity, and operational distance from primary sites.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid-Power Constraints in Prague Metro | -0.5% | Prague and Central Bohemia, immediate, national grid, medium term | Short term (≤ 2 years) |

| Escalating Construction and Financing Costs | -0.3% | Prague, high land costs, national, materials inflation | Medium term (2-4 years) |

| Talent Shortage of Certified DC Engineers | -0.2% | National, with concentration risk in Prague | Long term (≥ 4 years) |

| Emerging Czech Data-Sovereignty Clauses | -0.1% | National, with cross-border implications for EU customers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Power Constraints in Prague Metro

Prague's transmission grid has become the primary bottleneck for large-scale developments in Czechia's data center market. Connection queues for allocations exceeding 20 MW can extend from 3 to 5 years, delaying delivery for expansive campuses even when demand is evident.[2]Czech Transmission System Operator, “Hosting Capacity Map,” ČEPS, ceps.cz Source: European Commission, “Grid Connection and Energy Infrastructure Policy Materials,” European Commission, energy.ec.europa.eu In July 2025, a grid incident resulted in a 2,300 MW load loss, representing 28% of the pre-incident demand in the control area, highlighting the rapid escalation of stress due to equipment failures. The European Commission identified Czechia as a member state grappling with grid connection backlogs and suggested sequencing strategies for substantial loads such as data centers. Developers are increasingly relocating projects to peri-urban or regional sites. However, this shift does not entirely eliminate delays, as permitting and local engagement still require time. Consequently, while market demand is evident, power delivery poses a significant constraint for Czechia's data center market in the foreseeable future.

Escalating Construction and Financing Costs

In Czechia, the costs of specialized construction have risen, driven by surges in prices for reinforced concrete, precision cooling systems, and electrical switchgear. Additionally, land premiums in Prague pose challenges for smaller operators. A testament to the escalating costs, CRA has earmarked CZK 2 billion (approximately USD 89 million) for a 26 MW facility in Zbraslav, highlighting the premium on purpose-built, high-density campuses over previous retrofit projects. These heightened capital demands predominantly benefit operators with robust balance sheets or backing from infrastructure funds, sidelining smaller domestic players from independent scaling. Furthermore, financing conditions across Europe have remained tighter through 2024 and into 2025 compared to pre-2022 levels, amplifying interest burdens on multi-year construction endeavors. This scenario heightens consolidation risks, as the Czechia data center market increasingly prioritizes capital depth alongside technical expertise. Consequently, while total capacity may expand, the diversity of the supply pipeline could diminish.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotspot: Prague Holds The Core Capacity While Brno Builds AI-Led Growth

In 2025, Prague and Central Bohemia commanded a dominant 78.0% share of the Czechia data center market, underscoring the region's evolution into a hub of carrier-grade infrastructure, particularly along the capital's fiber corridors. Beyond its market share, Prague stands out as the nation's internet exchange nexus and a primary disaster recovery site for users in the DACH region. Commercial zones in Prague 3, 6, and 10 have cultivated dense connectivity, enabling operators to boost rack counts and power density in response to enterprise demands. Even as challenges related to power and land became evident, this robust infrastructure ensured Prague's centrality in the Czechia data center landscape. South Moravia is emerging as the fastest-growing hotspot, boasting a projected CAGR of 18.3% from 2026 to 2031. This growth is bolstered by the presence of cybersecurity institutions, active research, and a focus on AI development. With NÚKIB situated in Brno and the CEITEC research cluster nearby, the region is carving out a niche for security-sensitive and advanced computing tasks. MasterDC's ambitious AI data center in Kanice, engineered for workloads reaching 120 kW per rack, signals a regional pivot towards high-density use cases, moving away from traditional enterprise colocation.[3] While the rest of Czechia, including CRA facilities in Ostrava, Pardubice, and Zlín, caters to regional enterprise and edge demands, its national influence remains modest. As Prague grapples with tighter utilizations in certified facilities, South Moravia and other locales present the land and power resources essential for the forthcoming growth surge. Further solidifying South Moravia's significance, Inventec inaugurated a sprawling 52,000 m² campus at CTPark Blučina, close to Brno, in September 2025. This facility, poised to enhance server production capacity by 15%, acts as a pivotal hardware supply-chain anchor, facilitating nearby staging and validation tasks. Thus, South Moravia emerges as a critical player, not just for IT migration but also for compute activities linked to production and testing.

By Data-Center Size: Medium Facilities Lead Today While Large Builds Drive Growth

In 2025, medium-sized facilities accounted for 38.4% of the Czechia data center market. Meanwhile, the large-facility segment is set to grow at a robust 16.2% CAGR through 2031. This distribution highlights the traditional landscape of the Czechia data center market. Historically, domestic operators expanded incrementally, and many clients opted for multi-rack or multi-megawatt setups instead of entire hyperscale campuses. Medium facilities have been pivotal for sectors such as banking, telecom, government, and enterprise consolidation. While small facilities play a role in edge deployments and regional managed hosting, they do not fully meet the density demands of emerging AI and wholesale contracts. Although massive and mega-scale developments face constraints due to current power conditions, projects such as CRA’s 26 MW Prague Gateway DC and MasterDC’s ambitious 25 MW Kanice plan indicate a shift, suggesting that larger-scale operations are becoming a reality in Czechia.

HPE’s facility in Kutná Hora, which produces HPE Cray EX liquid-cooled supercomputer systems for clients across Europe, is driving a secondary demand for data centers. These centers are now increasingly required to handle dense staging and acceptance testing. This heightened demand from high-performance computing is steering the Czechia data center landscape towards larger, advanced facilities equipped with superior cooling systems and redundant power setups. Regulatory measures, such as Act No. 469/2023 Coll., further bolster this trend. The act mandates reporting for facilities exceeding 500 kW and imposes waste-heat recovery duties on those above 1 MW. Such compliance costs pose challenges for smaller operators, gradually diminishing the economic viability of sub-megawatt sites. Consequently, while medium facilities hold significance today, the market's trajectory leans towards larger, denser setups capable of catering to AI, cloud, and wholesale demands.

By Tier Standard: Tier III Defines The Base While Tier IV Moves Up

In 2025, Tier III installations dominated the Czechia data center landscape, claiming 62.1% of the market share. Meanwhile, Tier IV is on track to expand at a robust 14.8% CAGR, projected through 2031. Tier III has emerged as the de facto standard in Czechia's data center arena, offering robust uptime with N+1 redundancy in power and cooling. This comes without the hefty price tag of concurrent maintainability. Such a setup aligns perfectly with the needs of BFSI, cloud, and government sectors, which prioritize resilience but remain cost-conscious. Operators bolster their credibility by publishing Tier III design documentation, complemented by ISO 27001 and ISO 9001 certifications. While Tier I and Tier II sites continue to cater to edge nodes, SME hosting, and backup workloads, they are increasingly feeling the heat as demands for efficiency and compliance intensify.

The growing emphasis on Tier IV is evident. High-stakes sectors, from AI inference clusters to financial services and essential government operations, are now treating zero-downtime designs as non-negotiable contractual terms. New wholesale entrants in the Czechia data center scene view Tier III as the baseline, often opting to invest more for the assurances that Tier IV offers, especially when continuity is paramount. Expectations from the Czech National Bank, coupled with broader EU directives on digital finance, are pushing tier upgrades from mere marketing labels to essential operational mandates. As a result, while Tier III installations continue to dominate, the trajectory of future investments leans towards Tier IV. The Czechia data center sector is thus evolving, not just in terms of raw capacity, but also in the depth of its certifications.

By Absorption: Utilized Capacity Leads While Hyperscale Changes The Mix

In 2025, 83.2% of the installed capacity in Czechia's data center market was already tied to active, revenue-generating deployments. Hyperscale colocation emerged as the fastest-growing sub-segment, boasting a projected CAGR of 24.5% from 2026 to 2031. This surge signals a pronounced shift from a market predominantly focused on retail and enterprise-managed hosting to one leaning toward larger wholesale-style contracts. While non-utilized capacity lingers in commissioning, reserve, or decommissioning stages, its share diminishes as operators expedite delivery schedules. Retail colocation continues to cater to SMEs and mid-market users, but there is a notable uptick in wholesale demand. Financial institutions, DACH corporations, and larger domestic entities are increasingly consolidating their distributed server rooms into specialized facilities.

Demand is broadening across sectors, including BFSI, cloud, e-commerce, government, manufacturing, media and entertainment, and telecom. Government demand holds particular significance. With SPCSS anchoring public-sector sourcing and the April 2025 Cybersecurity Act extending compliance obligations to over 6,000 Czech entities (data center service providers included), there is a pronounced regulatory shift. This shift bolsters certified domestic facilities, as buyers now prioritize enhanced security, reporting, and territorial availability. Both global cloud giants and Czech sovereign cloud operators are aggressively expanding their footprint in the Czech data center landscape. Additionally, as latency-sensitive workloads transition from local server rooms to facilities boasting superior uptime and network resilience, sectors such as manufacturing, media, and telecom further amplify the demand. Thus, while the Czechia data center industry witnesses a broadening in demand, hyperscale contracts are leading the growth charge.

Geography Analysis

In 2025, Prague and Central Bohemia commanded a dominant 78.0% share of the installed capacity, solidifying their status as the epicenter of the Czechia data center market. This region's allure lies in its blend of fiber density, robust exchange traffic, strong enterprise demand, and strategic cross-border reach. Highlighting the capital's peering prowess, peak traffic throughput reached 5.071 Tbps, alongside 178 member autonomous system numbers and 24 customer ports operating at 400G each. Such metrics underscore the capital's pivotal role in the peering ecosystem. This exchange layer not only facilitates low-latency traffic handling but also bolsters Prague's significance for domestic hosting and DACH disaster recovery frameworks. The Prague Gateway DC, situated in Zbraslav, boasts a design capacity of 26 MW, with rack densities reaching up to 30 kW. The facility's inaugural 700-rack phase is on track to go live by the close of 2027. Despite facing power constraints that complicate the delivery of additional supply, the region maintains its dominance in the Czechia data center landscape.

South Moravia is emerging as the fastest-growing region, with projections indicating an 18.3% CAGR from 2026 to 2031. This surge is intricately linked to the region's burgeoning AI and semiconductor ecosystem. An expansive 52,000 m² production center at CTPark Blučina is set to boost server manufacturing capacity by 15%. This development positions South Moravia as a pivotal player in the cloud and AI supply chains. Meanwhile, the Kanice facility is gearing up to commence operations in autumn 2026. Starting with an initial capacity of 4 MW, the facility has a trajectory aimed at reaching 25 MW, catering to chip design, quantum modeling, and AI model training tasks. Additionally, Brno's market is further strengthened by the presence of institutional support, ensuring a focus on security-sensitive procurement and certified infrastructure.

While other regions in Czechia account for a smaller slice of the national capacity, their significance is growing, especially for distributed enterprise, research, and edge workloads. The LUMI-Q consortium project in Ostrava, backed by EUR 5 million and USD 5.4 million funding, is enhancing the advanced compute infrastructure landscape beyond the traditional hubs of Prague and Brno. Regional locations are capitalizing on advantages like lower land costs and improved grid access at select substations. The hosting capacity map indicates multiple nodes outside Prague as conditionally suitable to suitable for development. Given these dynamics, as the primary metro hubs near saturation, the Czechia data center market is poised to increasingly lean on regional expansions.

Competitive Landscape

In the Czechia data center market, no single operator commands more than 15% of the installed IT power capacity, highlighting its moderate fragmentation. Recognizable players such as TTC TELEPORT, CE Colo, CRA, T-Mobile Czech Republic, and Seznam.cz dominate the purpose-built third-party colocation scene, particularly in Prague. The market is shifting focus from price-driven retail hosting to managed, wholesale, and hyperscale service models. Under the ownership of Cordiant Digital Infrastructure, CRA has pivoted from a broadcast-centric approach to emphasizing cloud and data center revenues, underscoring a broader trend of incumbents realigning with the surging demand for digital infrastructure. Consequently, competition in the Czechia data center arena now hinges more on factors such as power access, certification depth, and service capabilities, rather than just basic rack pricing.

CE Colo stands out by securing ISO 14001, ISO 27001, and ISO 9001 certifications at its DC7 campus and by offering direct connectivity to NIX.CZ and Peering.cz. T-Mobile Czech Republic bolstered its renewable energy stance by entering a cross-border virtual power purchase agreement with Rezolv Energy, a move that resonates in a market increasingly prioritizing sustainability. While global giants Equinix and Interxion have established a presence in Czechia and nurtured customer relationships, they have yet to develop expansive owned campuses. This gap presents a prime opportunity for domestic operators and infrastructure fund-backed platforms to seize emerging demand before the global competition intensifies.

MasterDC emerges as a formidable contender, with its Kanice design accommodating liquid cooling up to 120 kW per rack, surpassing the density capabilities of many legacy sites. HPE’s Kutná Hora facility, one of just four global HPE HPC production sites, bolsters the local ecosystem's expertise in advanced computing and liquid cooling. This synergy not only fortifies the Czechia data center landscape but also positions it as an attractive hub for international AI and HPC clientele. As smaller operators grapple with escalating capex and stringent compliance mandates, MandA activities are poised to surge. Firms such as SafeDX and DataSpring, teetering on the market's fringes, emerge as potential consolidation targets. While the Czechia data center market appears fragmented, the trajectory suggests a consolidation trend favoring operators with robust capital and execution prowess.

Czechia Data Center Industry Leaders

Colo Czech s.r.o.

TTC TELEPORT, s.r.o.

Equinix (Czech Republic), s.r.o.

Interxion Czech Republic s.r.o.

České Radiokomunikace a.s. (CRA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: MasterDC announced plans for Czechia's first AI-focused data center in Kanice, near Brno, with operations expected to commence in autumn 2026. Located in a repurposed military complex, the facility features secure telecom bunkers and an initial capacity of 4 MW, scalable to 25 MW. Specifications include liquid cooling for up to 120 kW per rack, a target PUE of 1.2, and a 5 MWp photovoltaic plant. The project received logistical support from the Ministry of Industry and Trade, the South Moravian Region, and the City of Brno, with endorsement from the Czech National Semiconductor Cluster.

- September 2025: Inventec Corporation inaugurated a 52,000 m² advanced technology manufacturing campus at CTPark Blučina, near Brno. The campus consolidates production, logistics, and service operations, aiming to increase server production capacity by 15 percent. Targeting cloud-computing and AI clients under a nearshoring strategy of "in Europe for Europe," the facility is expected to create up to 1,000 jobs in South Moravia.

- August 2025: České Radiokomunikace (CRA) initiated the Prague Gateway DC project in Zbraslav-Jíloviště, outside Prague, following the receipt of a building permit. The first phase, comprising a 700-rack building, is expected to be operational by the end of 2027. The full site spans 56,000 m² and includes a 26 MW capacity, 2,000 racks, 4 meet-me rooms, dual power feeds, and waste-heat reuse capabilities, with a total investment of CZK 2 billion (USD 89 million).

- May 2025: Seznam.cz, a.s. launched its third data center in Prague, expanding its computing infrastructure. This development addresses increased demand from its advertising technology, search, and AI-powered content platform services, which experienced significant traffic growth following the expansion of its generative AI product suite.

Czechia Data Center Market Report Scope

The Czechia Data Center Market Report is Segmented by Hotspot (Prague and Central Bohemia, South Moravia, Rest of Czechia), Data-Center Size (Small, Medium, Large, Massive, Mega), Tier Standard (Tier I-II, Tier III, Tier IV), and Absorption (Utilized, Non-Utilized). The Market Forecasts are Provided in Terms of Volume (MW).

| Prague and Central Bohemia |

| South Moravia (Brno) |

| Rest of Czechia |

| Small |

| Medium |

| Large |

| Massive |

| Mega |

| Tier I-II |

| Tier III |

| Tier IV |

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-User | ||

| Non-Utilized | ||

| By Hotspot | Prague and Central Bohemia | ||

| South Moravia (Brno) | |||

| Rest of Czechia | |||

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Massive | |||

| Mega | |||

| By Tier Standard | Tier I-II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Utilized | By Colocation Type | Hyperscale |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-User | |||

| Non-Utilized | |||

Key Questions Answered in the Report

How large is the Czechia data center market?

The Czechia data center market measured 152.67 MW in 2025, enters 2026 at 158.39 MW, and is projected to reach 190.33 MW by 2031 at a 3.74% CAGR.

Which region leads installed capacity in Czechia?

Prague and Central Bohemia led with 78.0% of installed capacity in 2025 because the region combines exchange traffic, fiber density, and enterprise demand.

Which location is growing the fastest for new capacity?

South Moravia is the fastest-growing hotspot, with an 18.3% CAGR from 2026 to 2031, supported by AI, cybersecurity, and semiconductor-linked activity around Brno.

What facility size is expanding the fastest?

Large facilities are projected to grow at a 16.2% CAGR through 2031 as hyperscale and wholesale users prefer denser and more consolidated campuses.

Why is Tier IV gaining traction in Czechia?

Tier IV is forecast to grow at a 14.8% CAGR because AI inference, financial platforms, and critical public workloads are pushing buyers toward stronger uptime guarantees.

What are the main risks facing developers and operators?

The biggest near-term risks are Prague grid connection delays, higher construction and financing costs, and compliance requirements that favor larger operators with deeper capital.

Page last updated on: