Europe Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

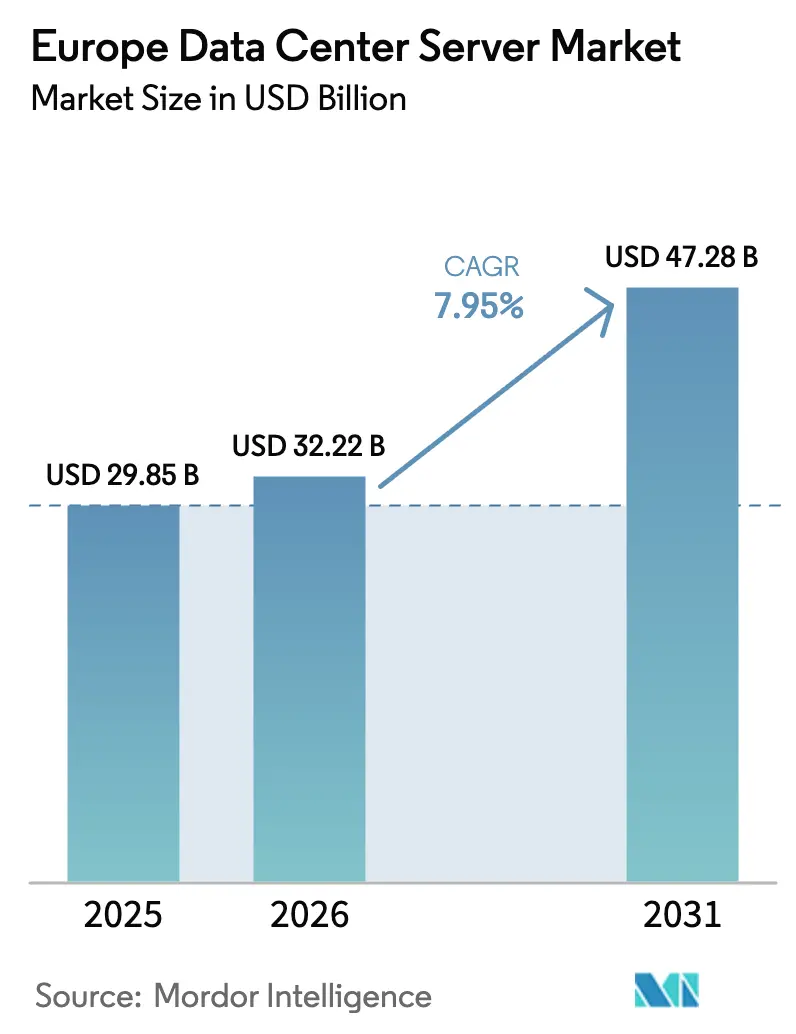

| Base Year Market Size (2025) | USD 29.85 Billion |

| Market Size (2026) | USD 32.22 Billion |

| Market Size (2031) | USD 47.28 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center Server Market Analysis by Mordor Intelligence

The Europe data center server market size is expected to grow from USD 29.85 billion in 2025 to USD 32.22 billion in 2026 and is forecast to reach USD 47.28 billion by 2031 at 7.95% CAGR over 2026-2031. Demand is accelerating as hyperscalers, telecom operators, and enterprises deploy AI-optimized infrastructure, refresh legacy estates, and comply with new EU sustainability mandates. GPU-dense designs, liquid cooling, and edge nodes are reshaping procurement patterns, while the EU Data Act and national sovereignty programs promote in-region compute. Supply-chain tightness for advanced GPUs has lifted lead times well beyond 52 weeks, forcing hybrid sourcing strategies. Meanwhile, rising power costs and land scarcity in FLAPD hubs (Frankfurt, London, Amsterdam, Paris, Dublin) channel new-build activity toward Central & Eastern Europe and Nordic sites.

Key Report Takeaways

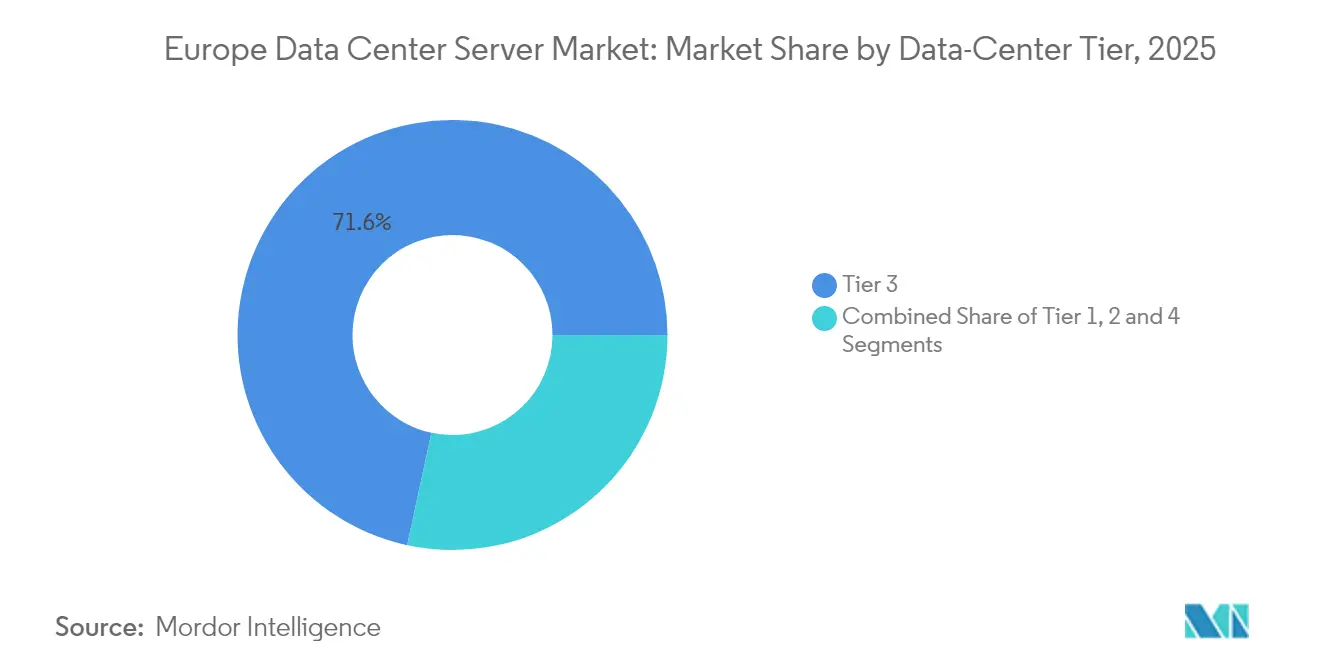

- By data-center tier, Tier 3 led with 71.62% of Europe data center server market share in 2025; Tier 4 is forecast to expand at a 9.98% CAGR to 2031.

- By form factor, half-height blades held 63.85% revenue share in 2025; quarter/micro blades record the highest projected CAGR at 8.35% through 2031.

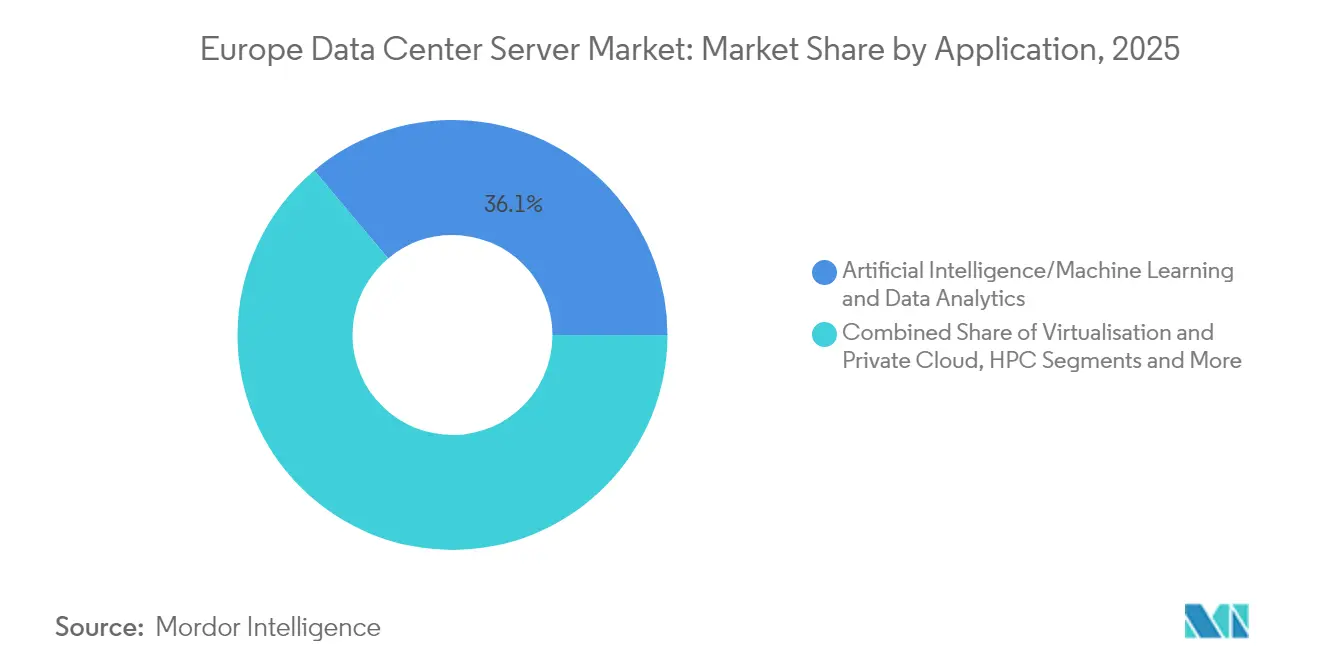

- By application, AI/ML workloads accounted for 36.12% share of the Europe data center server market size in 2025, while virtualization/private cloud advances at an 8.06% CAGR to 2031.

- By data-center type, colocation facilities captured 53.12% revenue share in 2025; hyperscaler/cloud providers are growing fastest at 8.72% CAGR.

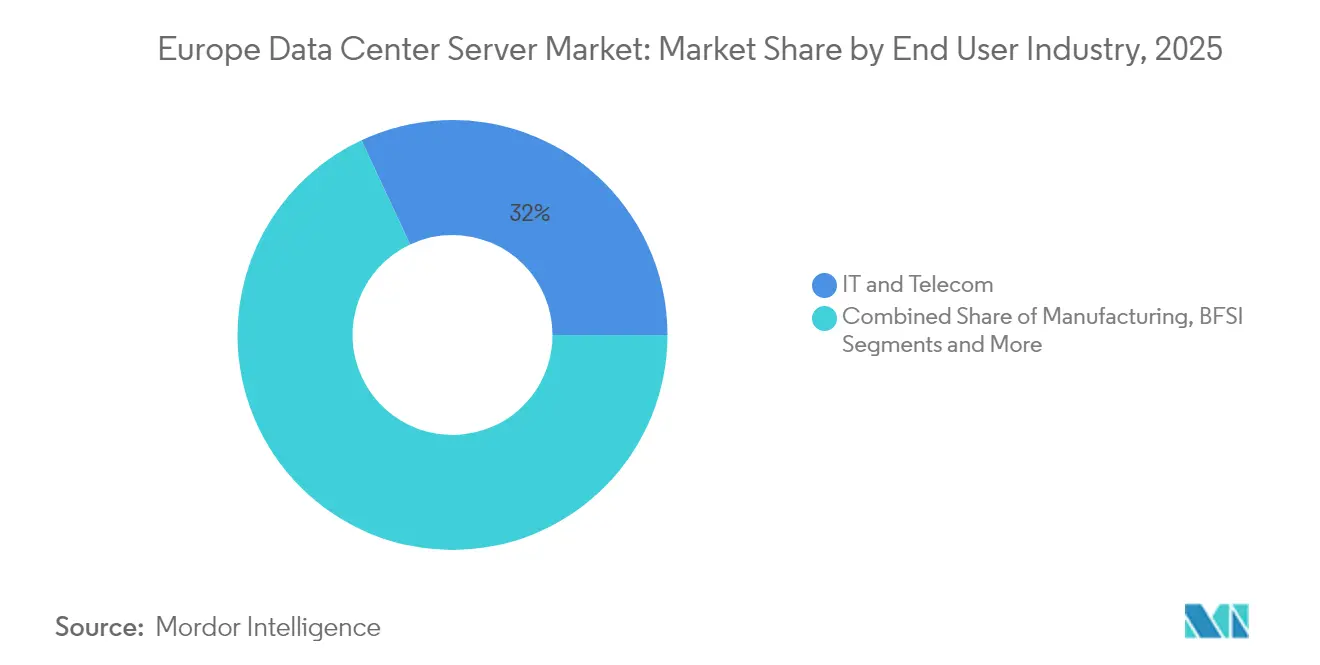

- By end-use industry, IT & telecom commanded 31.96% share in 2025; manufacturing and Industry 4.0 register the quickest growth at 9.14% CAGR.

- By Country, Germany held 24.78% of Europe data center server market size in 2025; Poland is the fastest-growing market at a 10.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The pace and direction of global change depend on shifts occurring across regions simultaneously, not within any one of them alone. The global data center server market outlook research of Mordor Intelligence reflects this combined progression.

Europe Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of cloud computing and X-as-a-Service | +2.1% | Global, with FLAPD markets leading | Medium term (2-4 years) |

| Rapid commercial roll-out of 5G and edge nodes | +1.8% | Germany, Netherlands, Nordic region | Short term (≤ 2 years) |

| Hyperscale refresh cycle toward GPU/AI servers | +2.5% | France, Germany, UK core markets | Short term (≤ 2 years) |

| EU Green Deal incentives for liquid-cooled racks | +1.2% | EU-wide, Nordic emphasis | Long term (≥ 4 years) |

| Sovereign AI / EU Data Act pushing in-region compute | +1.9% | France, Germany, Netherlands | Medium term (2-4 years) |

| Rise of modular, prefabricated micro-data-centers | +0.9% | Edge markets, secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud computing & X-as-a-Service adoption

Hyperscalers are building region-specific availability zones, driving sustained demand for rack-scale servers. Microsoft confirmed three new data centers in Northern France, while AWS formed a standalone European Sovereign Cloud entity to satisfy residency rules aws.amazon.com. Dutch operators estimate that data centers now add 7.6% to the national GDP due to such activity. [1]European Commission, “EU Edge Observatory,” europeancommission.europa.eu Enterprise case studies, such as Uniper’s migration of 10,000 employees to Azure, resulting in 50% fewer IT incidents, illustrate tangible operational gains.

5G rollout & edge nodes

Operators deploy micro-data-centers at base-station sites to meet sub-20 ms latency targets under the EU Edge Observatory program. Ericsson’s private 5G network at Calpak’s Greek solar-heater plant shows manufacturing use cases, while German Edge Cloud powers Rittal’s Industry 4.0 factory with 250+ networked machines.

Hyperscale refresh toward GPU/AI servers

Dell logged USD 12.1 billion in AI-optimized server orders during Q1 2025, reflecting corporate urgency to train generative models.[2]Dell Technologies, “Q1 FY 2026 Results,” dell.comHPE secured a USD 1 billion contract to build Elon Musk’s X platform AI cluster, underscoring single-deal scale. NVIDIA is shipping Blackwell systems that will deliver 3,000 exaflops across four EU countries, Europe’s largest coordinated AI build-out.

EU Green Deal incentives for liquid cooling

Operators can claim energy-efficiency tax breaks when PUE improves, catalyzing the adoption of immersion systems. GlobalConnect’s submerged solution cuts power use by 90% and shrinks footprint 80% globalconnect.dk. OVHcloud reports a 1.28 PUE with hybrid water-immersion loops, well below the 1.55 regional average.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating CapEx for new facilities | -1.8% | High-cost markets: London, Frankfurt, Amsterdam | Short term (≤ 2 years) |

| Volatile electricity & carbon prices | -1.4% | Germany, UK, industrial regions | Medium term (2-4 years) |

| Supply-chain squeeze on advanced GPUs/CPUs | -2.1% | Global impact, acute in AI-focused deployments | Short term (≤ 2 years) |

| Stricter waste-heat reuse & PUE regulations | -0.7% | EU-wide, Nordic region leading compliance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating CapEx for new facilities

Land costs for 50-acre plots in tier-1 hubs climbed 23% in 2025, while power-allocation queues exceed 36 months.[3]Cushman & Wakefield, “2025 Global Data Center Construction Costs,” cushmanwakefield.comVantage Data Centers tapped a EUR 720 million (USD 829.16 million) securitization to fund four German builds, showcasing creative financing. Labor scarcity also inflates budgets, prompting developers to pivot toward Poland and Spain where costs remain 15-20% lower.

Supply-chain squeeze on advanced GPUs/CPUs

NVIDIA H100/H200 substrates are concentrated in Taiwan and Japan, elevating geopolitical risk. High-bandwidth memory demand could reach USD 21 billion in 2025, crowding out legacy component lines. A grey market has emerged, with secondary prices exceeding MSRP by 70%, pushing enterprises to dual-source and lock in multi-year supply agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Tier 3 Dominance Drives Reliability Standards

Tier 3 facilities accounted for 71.62% of Europe data center server market share in 2025, a testament to their cost-to-resilience balance. Financial institutions accelerated upgrades after recent outages, adopting Tier 3 for transaction-critical workloads. DZ BANK deployed Hitachi Vantara EverFlex to secure always-on storage, reinforcing this preference. The Europe data center server market size for Tier 4 is projected to expand 9.98% annually as AI and sovereign-cloud operators demand fault-tolerant uptime. Government supercomputer projects, such as Serbia’s Eviden contract, validate the rising appeal of Tier 4.

Edge rollouts sustain limited use of Tier 1/2 suites for development environments where proximity matters more than redundancy. However, stricter EU directives on incident reporting could gradually shift even peripheral sites toward Tier 3 certification, underpinning a structural uplift in specification requirements across the Europe data center server market.

By Form Factor: Half-Height Blades Lead Dense Computing Evolution

Half-height blades retained 63.85% revenue in 2025, anchoring legacy virtualization estates. Lenovo’s ThinkSystem V4 line, built on Intel Xeon 6, refreshes this mainstream segment. Europe data center server market size for quarter-height blades is rising fastest at 8.35% CAGR as operators outfit micro-edge nodes inside retail outlets and cell towers.

Full-height blades remain vital for GPU clusters; Cisco’s UCS C845A packs eight NVIDIA GPUs within 4 RU, meeting tight rack-power budgets. Modular reference architectures such as NVIDIA MGX allow operators to drop new accelerator cards without replacing rails, extending asset life and lowering TCO.

By Application/Workload: AI/ML Transforms Server Requirements

AI/ML workloads captured 36.12% Europe data center server market share in 2025, surpassing HPC for the first time. Enterprises train large language models on clusters built around AMD EPYC and NVIDIA H100; CHARM Therapeutics moved its 128-GPU estate from the UK to Iceland to blend green energy with performance. Storage-intensive analytics also expands as NVMe and E3.S drives push I/O latency below 50 µs.

Virtualization/private cloud registers an 8.06% CAGR through 2031 as banks and insurers phase out on-prem mainframes. HPE’s Blue Lion supercomputer at Leibniz Center, cooled 100% by direct liquid, delivers 30× speed-ups, proving advanced cooling’s role in AI and HPC consolidation.

By Data-Center Type: Colocation Facilities Bridge Enterprise and Hyperscale Demands

Colocation providers captured 53.12% of the European data center server market size in 2025 by offering compliance-ready environments without capital strain. Equinix’s acquisition of BT’s Irish facilities reflects a pivot toward green-energy geographies. Hyperscalers show a 8.72% CAGR as Microsoft, Google, and Meta pre-provision capacity for AI.

Hybrid tenancy is emerging: enterprises offload steady workloads to colos while bursting AI jobs to the cloud. Vantage Data Centers’ EUR1.4 billion expansion demonstrates large-scale build-to-suit campuses for this trend.

By End-use Industry: IT & Telecom Lead Digital Infrastructure Investment

IT & telecom owned 31.96% revenue in 2025, driven by 5G core upgrades and OTT growth. Deutsche Bank cut server count by 25% using Google Distributed Cloud on its Autobahn FX platform. Manufacturing is the fastest-growing vertical at 9.14% CAGR, as edge analytics optimizes production lines. Rittal’s Haiger plant, managed by German Edge Cloud, illustrates real-time quality control at scale.

Healthcare continues its cautious cloud migration; the NHS shutters legacy rooms yet retains on-prem servers for GDPR-classed datasets. Energy utilities such as Vattenfall run Databricks Intelligence to model renewables dispatch, highlighting diverse demand drivers.

Geography Analysis

Germany retained leadership with a 24.78% share of Europe data center server market in 2025. Frankfurt’s DE-CIX internet exchange and ample corporate tenants sustain high rack absorption. Revenues may reach USD 25.3 billion by 2029 as new Rhein-Main campuses secure 600 MW of incoming grid power. Land scarcity and 18-month power-hook-up queues, however, nudge operators toward Berlin and NRW.

Poland is emerging fastest, tracking a 10.22% CAGR as Warsaw becomes a cloud on-ramp hub. Google, Microsoft, and Oracle have all commissioned 50 MW-plus availability zones, leveraging attractive electricity tariffs and proximity to Western Europe. The government’s PLN 11 billion digital-decade plan allocates incentives for regional colos, accelerating rack-supply pipelines.

Mordor Intelligence examines the data center server market across diverse other regional markets as well, including Middle East, Africa, and North America, while also offering granular country-level perspectives for Sweden, Denmark, Italy, Norway, Germany, and Switzerland and more.

Competitive Landscape

Competition is intensifying as AI refresh cycles disrupt entrenched positions. Intel responds with Sierra Forest E-cores targeting cloud workloads, but availability only in 2H 2025 stalls momentum. NVIDIA’s near-monopoly on high-end GPUs is both a boon and a bottleneck; allocations favor the top eight OEMs, creating scarcity for mid-tier integrators.

European champions leverage sovereignty narratives. OVHcloud markets in-region AI clusters cooled by proprietary water loops; global players are compelled to match such sustainability metrics. Liquid-cooling vendors like Submer and GRC partner with colos to retrofit existing halls, creating a secondary competitive layer around energy efficiency. Supply-chain resilience becomes a deciding factor; vendors able to secure substrate and HBM allocations lock in orders 12 months ahead, squeezing slower rivals.

Europe Data Center Server Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

Lenovo Group

Cisco Systems

Fujitsu

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA begins shipping 3,000 exaflops of Blackwell systems to France, Italy, Spain, and the UK, Europe’s largest AI hardware roll-out

- June 2025: AWS incorporates European Sovereign Cloud subsidiary to satisfy EU data-residency rules.

- June 2025: Vantage Data Centers raises EUR 720 million (USD 829.16 million) via Europe’s first data-center securitization to fund four German sites

- May 2025: HPE unveils private-cloud portfolio claiming 90% VM-license savings and 2.5× lower TCO.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the European data-center server market covers all new, rack-mounted compute nodes, blade, rack, and micro-blade designs that ship into hyperscale, colocation, enterprise, and edge facilities across 19 European countries. Sales include CPU- and GPU-based configurations, associated chassis, and integrated management modules, valued at factory gate prices.

Scope exclusion: Stand-alone refurbished servers, pure software virtualization platforms, and white-box kits assembled in-house by hyperscalers are not counted.

Segmentation Overview

- By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

- By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

- By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

- By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

- By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

- By Geography

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with server OEM product managers, Nordic colocation operators, German electrical contractors, and large French banking IT heads. These discussions validate refresh cycles, GPU attach rates, and power budgets, and they flag regional quirks, such as Ireland's build moratoriums, that secondary sources miss.

Desk Research

We start with public statistics from Eurostat, the European Commission's Digital Economy reports, customs import codes for HS 847141, and energy-use registers such as ENTSO-E. Trade bodies, including the European Data Centre Association and Uptime Institute, supply rack density and tier uptake ratios, while patent feeds from Questel hint at upcoming form-factor shifts. Company 10-Ks, investor decks, and earnings calls gathered through Dow Jones Factiva, plus financial snapshots from D&B Hoovers, round out revenue and ASP checkpoints. The sources cited above illustrate our approach and are not exhaustive; numerous other open datasets inform variable calibration.

Market-Sizing & Forecasting

A top-down model translates import-adjusted production and trade data into an installed-base refresh pool, which is then stress tested against sampled bottom-up roll-ups of supplier shipments and channel checks. Key variables include average rack density, GPU attach share, server ASP progression, data-center build completions, and enterprise virtualization penetration. A multivariate regression relates those drivers to historical server revenue, producing the baseline value. Scenario analysis overlays EU energy-efficiency mandates and AI workload ramp-up to generate forecasts through the forecast period. Gaps in bottom-up samples are bridged with weighted averages from adjacent facility cohorts before final alignment.

Data Validation & Update Cycle

Outputs undergo variance screening versus independent metrics such as UPS shipments and power-capacity additions. Senior reviewers sign off only after anomalies are resolved; reports refresh annually, and mid-year re-contacts trigger updates when suppliers shift guidance or regulations change.

Why Our Europe Data Center Server Baseline Earns Decision-Maker Trust

Published values often diverge because firms mix data-center gear with wider infrastructure, apply differing refresh windows, or convert currencies late.

Key gap drivers include wider facility hardware scopes, omission of GPU premiums, and slower refresh cadence assumptions that rival publishers adopt, while Mordor's model centers strictly on new server nodes, uses constant-currency 2024 USD, and updates every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.85 B (2025) | Mordor Intelligence | - |

| USD 27.58 B (2024) | Global Consultancy A | Excludes micro-blade launches and GPU mark-ups |

| USD 13.00 B (2024) | Regional Consultancy B | Counts only enterprise refresh, omits hyperscalers |

| USD 47.23 B (2024) | Industry Journal C | Bundles power, cooling, and storage with servers |

The comparison shows that once differing scopes and variables are stripped away, Mordor's disciplined, annually refreshed approach delivers a balanced, transparent baseline that clients can trace back to clear data points and confidently build plans upon.

Key Questions Answered in the Report

What is the current size of the Europe data center server market?

The market is valued at USD 32.22 billion in 2026 and is projected to reach USD 47.28 billion by 2031.

Which country leads server demand in Europe?

Germany leads with 24.78% share in 2025 thanks to Frankfurt’s connectivity and large enterprise base.

How fast is AI driving server upgrades?

AI/ML workloads already hold 36.12% market share and hyperscale GPU refreshes add about +2.5 percentage points to the market’s CAGR.

Why are operators adopting liquid cooling?

EU Green Deal incentives and higher rack densities allow operators to cut power use by up to 90% and achieve PUE below 1.3.

Page last updated on: