Romania Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

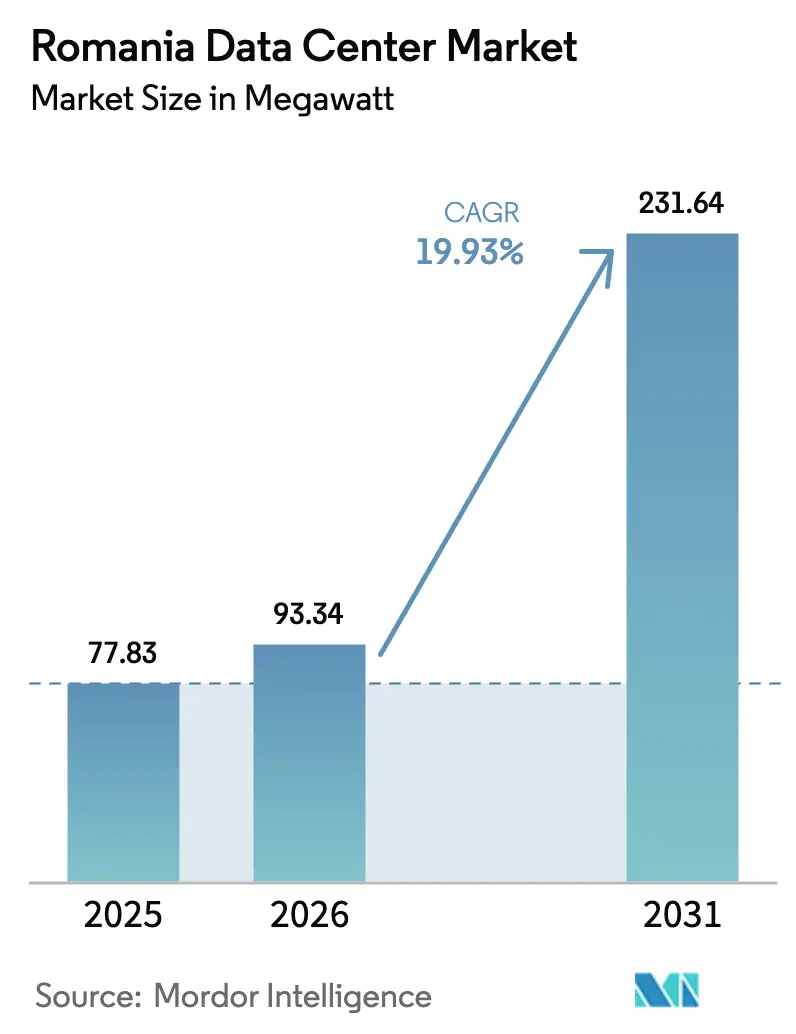

| Base Year Market Size (2025) | 77.83 megawatt |

| Market Volume (2026) | 93.34 megawatt |

| Market Volume (2031) | 231.64 megawatt |

| Growth Rate (2026 - 2031) | 19.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Data Center Market Analysis by Mordor Intelligence

Romania Data Center market size in 2026 is estimated at 93.34 MW, growing from 2025 value of 77.83 MW with 2031 projections showing 231.64 MW, growing at 19.93% CAGR over 2026-2031. The impressive growth trajectory reflects the country’s role as a digital bridge between Western Europe and the Balkans, ample EU funding for cloud adoption, and rising deployment of renewable-powered facilities. Local operators capitalize on Bucharest’s rich fiber connectivity, while secondary cities gain traction as enterprise customers pursue hybrid-cloud strategies. Hyperscale cloud providers are accelerating green-energy power-purchase agreements to control electricity costs that account for 35–40% of operating expenditure. Momentum also stems from 5G-enabled edge demand, EU-backed digital government projects, and Black Sea cable landings that lower latency for cross-border traffic. Competitive intensity remains moderate but technology-centric, with operators differentiating through sustainability credentials such as ClusterPower’s 1.1 PUE and expanding carrier-neutral connectivity.

Key Report Takeaways

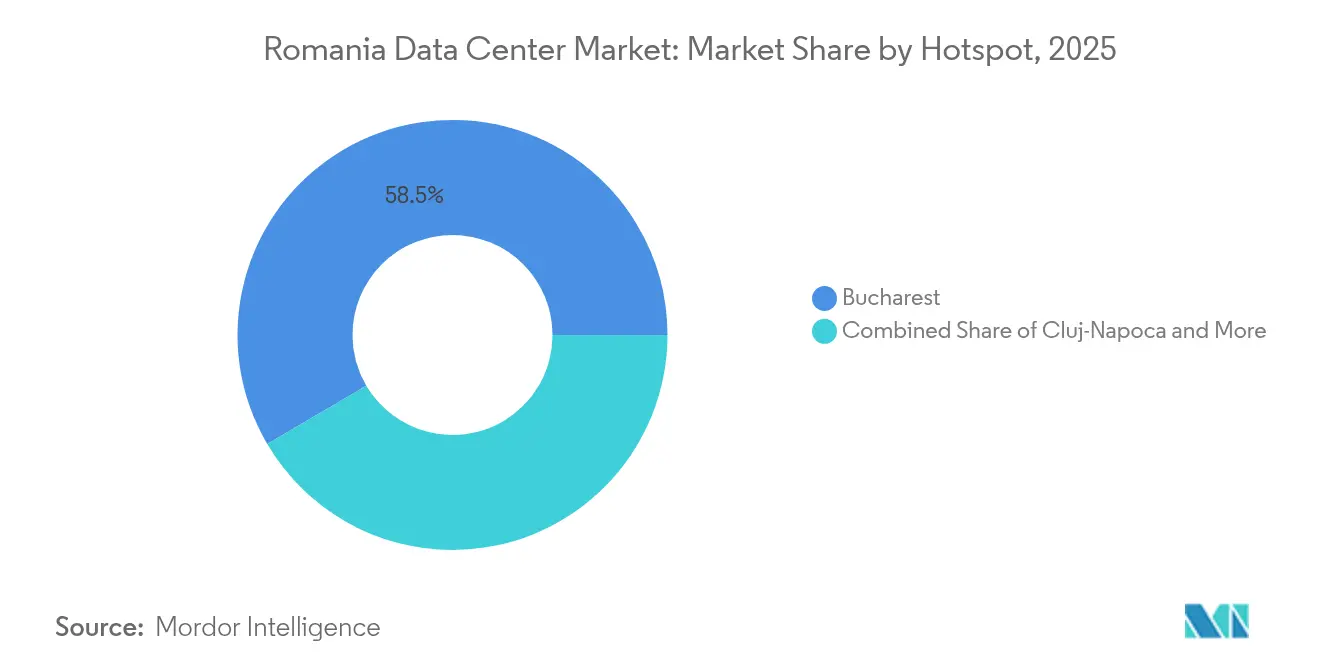

- By hotspot, Bucharest led with 58.47% of Romania Data Center market share in 2025, while Constanța is forecast to expand at a 20.35% CAGR through 2031.

- By data center size, the Large segment commanded 43.26% share of the Romania Data Center market size in 2025, whereas the Mega segment is projected to grow at 21.74% CAGR.

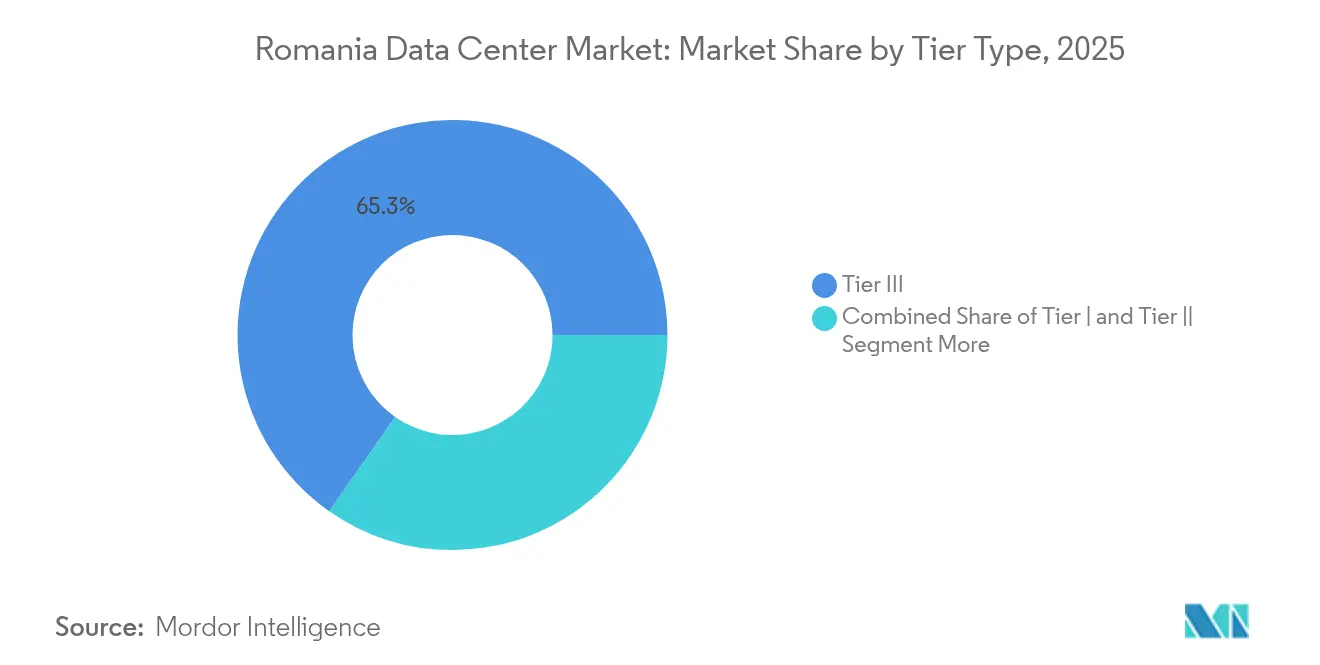

- By tier type, Tier III captured 65.28% share of the Romania Data Center market size in 2025; Tier IV is advancing at a 20.18% CAGR.

- By absorption, utilized capacity represented 46.35% of the Romania Data Center market size in 2025 and the hyperscale sub-segment within utilized space is growing at 22.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EU-funded digitalisation projects | +3.2% | National, concentrated in Bucharest-Ilfov region | Medium term (2-4 years) |

| Accelerated shift to hybrid-cloud by Romanian enterprises | +4.1% | National, with spillover to regional cities | Short term (≤ 2 years) |

| Rapid roll-out of 5G driving edge demand | +2.8% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Entry of hyperscale cloud regions (Microsoft, AWS) | +5.3% | Bucharest primary, Cluj-Napoca secondary | Long term (≥ 4 years) |

| Rising green-energy PPAs for data-centre power | +2.1% | National, concentrated in renewable-rich regions | Long term (≥ 4 years) |

| Black-Sea subsea cable landing in Constanţa | +1.9% | Constanţa region, extending to Bucharest corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-Funded Digitalisation Projects Accelerate Infrastructure Demand

The EUR 6 billion National Recovery and Resilience Plan (NRRP) earmarks EUR 500 million for sovereign cloud, prompting immediate capacity additions as four Tier IV facilities are scheduled before 2026.[1]European Commission, “Romania’s Recovery and Resilience Plan,” commission.europa.eu Public-sector digitization elevates demand for domestic hosting that complies with GDPR, while 25 cloud-native citizen services generate traffic that enterprises must interoperate with. Ministries are consolidating legacy IT into modern data centers, establishing baseline specifications—often Tier III—to balance cost and resilience. As government workloads shift to cloud, private firms mirror architecture choices for seamless public–private data exchange. The multiplier effect cascades to local integrators and fiber carriers that connect municipal offices, extending the Romania Data Center market across rural regions.

Accelerated Shift to Hybrid-Cloud by Romanian Enterprises

Banks, manufacturers, and retailers prioritize hybrid-cloud to improve digital customer journeys and process automation. Banca Transilvania’s BT ONE platform completes personal account opening in five minutes, a latency threshold that encourages on-premise compute proximity.[2]Banca Transilvania, “Platforma interna BT ONE…,” banca-transilvania.ro Manufacturing upgrades, such as BMW’s Cluj-Napoca IT hub, require secure edge workloads for IIoT and predictive maintenance. Romanian businesses also view local hosting as a hedge against fluctuating energy prices by signing renewable PPAs and consolidating equipment into energy-efficient campuses. These patterns enlarge the Romania Data Center market as enterprises migrate from server closets to colocation halls with redundant power and multi-cloud interconnects.

Rapid Roll-out of 5G Driving Edge Demand

Orange covers 50 cities with 5G/5G+, and Vodafone’s Open RAN program accelerates nationwide availability, reducing latency targets below 10 ms for smart-manufacturing and AR use cases.[3]Business Review, “Orange Romania now has 5G/5G+ coverage in 50 cities,” business-review.eu Government plans connect 945 localities with fiber backhaul, spawning micro-data centers to cache content locally. Telecom operators virtualize radio stacks and house them in carrier-neutral facilities, making edge real estate central to the Romania Data Center market. Secondary cities like Cluj-Napoca deploy smart-parking and traffic-management platforms that multiply low-footprint data-center nodes.

Entry of Hyperscale Cloud Regions Creates Market Transformation

Google’s memorandum with the Romanian government and Microsoft’s European cloud blueprint signal incoming hyperscale regions. Typical deployment phases start with colocation tenancy before purpose-built campuses arise, injecting multi-megawatt demand spikes. Local vendors supply land, dark fiber, and renewable power, while absorbing operational know-how from global partners. Hyperscale presence magnetizes SaaS ecosystems and fintech innovators who prefer intra-country latency, thereby amplifying the Romania Data Center market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile electricity prices post-2022 energy crisis | -2.7% | National, acute in industrial regions | Short term (≤ 2 years) |

| Limited dark-fiber outside Bucharest | -1.4% | Regional cities, rural areas excluded | Medium term (2-4 years) |

| Earthquake-zone construction cost premium | -0.8% | Seismic zones, particularly Vrancea region | Long term (≥ 4 years) |

| Scarcity of critical-facility engineers | -1.9% | National, concentrated in technical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Electricity Prices Post-2022 Energy Crisis

Day-ahead prices spiked to EUR 865 per MWh in July 2024, the EU’s highest, hampering budgeting for power-hungry facilities. Government caps through 2025 offer relief yet complicate 10-year investment models. Operators hedge by over-specifying backup diesel and locking in renewables, but smaller firms struggle with capital needs, slowing capacity adds and tempering Romania Data Center market expansion.

Limited Dark-Fiber Outside Bucharest

Despite Europe’s top residential fiber penetration, carrier-neutral dark fiber rings remain scarce beyond the capital, forcing operators in Cluj-Napoca or Timișoara to lease single-provider routes vulnerable to outages. Capital outlays for new ducts raise entry barriers and prolong ROI, affecting secondary-city rollout within the Romania Data Center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotspot: Bucharest Dominance Faces Regional Challenge

Bucharest anchors 58.47% of 2025 installed capacity, equal to 45.5 MW of the Romania Data Center market size, owing to 850 km of metro fiber, dense enterprise demand, and proximity to regulators. Utilization hovers near 50%, enabling quick absorption of hyperscale ramps. Enterprise tenants include financial institutions that need government-interactive workloads and hence prefer intra-city latency of sub-2 ms. Bucharest’s growth, though solid, is outpaced by coastal Constanța that leverages new submarine cables to carve 20.35% CAGR, attracting CDN nodes and logistics tech firms. Cluj-Napoca, nurtured by tech outsourcing boom, advances steadily with university-industry collaborations that raise cloud workload volumes.

Secondary cities Timișoara and Iași entice auto and electronics manufacturers deploying smart-factory infrastructure, investing in smaller Tier III halls for OT-IT convergence. Brașov and Craiova witness early commitments linked to logistics corridors and regional e-commerce fulfilment. Distributed architecture gains impetus as 5G mini-data centers appear along highway corridors to meet sub-10 ms requirements, broadening the Romania Data Center market across the country.

By Data Center Size: Mega Facilities Drive Market Evolution

Large facilities led 2025 with 43.26% of the Romania Data Center market share, equal to about 33.7 MW. Enterprises perceive them as cost-efficient yet manageable footprints that simplify SLA negotiations. However, Mega sites above 15 MW promise 21.74% CAGR as hyperscale arrivals demand contiguous blocks and governments consolidate workloads. ClusterPower’s campus exemplifies next-wave design, bundling combined-cycle gas turbines, solar arrays, and sleeved PPAs to assure green redundancy.

Small and Medium halls remain relevant. Edge nodes at motorway exchanges meet streaming latencies, while compliance-heavy verticals like healthcare deploy medium sites for sensitive data isolation. Government’s NRRP assigns EUR 500 million to four Tier IV data centers that approach Massive category, cementing Romania’s ability to host sovereign workloads. This portfolio diversity secures continuous expansion for the Romania Data Center market.

By Tier Type: Tier III Balances Performance and Cost

Tier III constituted 65.28% share in 2025, roughly 50.8 MW of the Romania Data Center market size, making it the default choice for mission-critical yet cost-conscious businesses. NAV Communications guarantees 99.99% uptime through N+1 power, dual-feed fiber, and advanced DDoS scrubbing, illustrating maturity without Tier IV price premiums. Enterprises value this equilibrium for ERP and digital banking platforms that demand availability but tolerate short maintenance windows.

Tier IV demand accelerates at 20.18% CAGR due to public-sector cloud and hyperscale benchmarks. Financial trading systems and telecom cores gravitate to concurrently maintainable, fault-tolerant environments. Tier I and II footprints shrink as virtualization lowers per-rack cost and clients retire on-premise rooms. Long term, a hybrid of Tier III colocation and edge micro-sites characterizes the Romania Data Center market.

By Absorption: Utilization Rates Signal Market Opportunity

Utilized capacity reached 46.35% in 2025, translating into 36.1 MW, while the balance remains pre-built inventory poised for rapid onboarding. Operators purposely maintain headroom to court hyperscale land-and-expand models. Within utilized space, hyperscale tenancy records 22.12% CAGR, largely driven by cloud regions aligning with GDPR and neighboring non-EU customers.

Retail colocation persists for mid-market firms seeking predictable opex, whereas wholesale blocks entice SaaS providers consolidating racks. Non-utilized buffers permit just-in-time expansion without overbuilding, sustaining pricing discipline and attractive returns that fuel continuous reinvestment in the Romania Data Center market.

Geography Analysis

The Romania Data Center market centers on Bucharest, which claimed 58.47% share in 2025 through formidable connectivity, mature enterprise clusters, and government proximity. Fiber-dense metro rings ensure cross-carrier diversity and sub-2 ms latency for fintech and state e-services. Cluj-Napoca spearheads secondary-city growth with software development centers from BMW and SITA. Constanța charts the fastest expansion at 20.35% CAGR, leveraging Black Sea cable latency gains to Russia, Turkey, and the Caucasus. Timișoara and Iași profit from university talent and automotive industry modernization, spurring Tier III builds sized for localized workloads. Western counties such as Brașov and Craiova integrate logistics and manufacturing digitalization, requiring regional edge nodes. The resulting mosaic broadens the Romania Data Center market beyond the capital while retaining Bucharest as the national interconnection core.

Competitive Landscape

The Romania Data Center market exhibits moderate fragmentation, with no operator exceeding 15% share. ClusterPower differentiates through energy-integrated campuses achieving 1.1 PUE, combining on-site generation and AI-driven cooling optimization. NAV Communications focuses on high-availability services with multi-carrier BGP routing and ISO 27001 compliance. M247 Europe markets environmentally friendly facilities, tapping over 50 IXPs to lure content providers. New entrants target secondary cities, bundling edge colocation with local dark-fiber builds to challenge incumbents. Strategic moves include renewable PPAs, microgrid adoption, and carrier-neutral meet-me rooms, moving competition away from price wars toward sustainability and network performance upgrades that propel the Romania Data Center market.

Romania Data Center Industry Leaders

Nx Data

Infinite Chain

VPS House Technology Group LLC

MEDIA SAT

BinBox Global Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Trendyol opened a warehouse in Ștefănești to support two-day delivery across CEE, underscoring e-commerce workload growth.

- March 2025: The government allocated EUR 180 million to an AI R&D program led by Politehnica Bucharest, boosting demand for HPC infrastructure.

- February 2025: Banca Transilvania rolled out BT ONE platform via FLOWX.AI, hitting 100,000 daily users.

- December 2024: AtkinsRéalis won USD 2.85 billion contract to extend Cernavoda nuclear plant life, ensuring long-term baseload power.

Romania Data Center Market Report Scope

| Bucharest |

| Cluj-Napoca |

| Rest of Romania |

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| By Hotspot | Bucharest | ||

| Cluj-Napoca | |||

| Rest of Romania | |||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Type | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

Key Questions Answered in the Report

How large is the Romania Data Center market in 2026?

Installed capacity totals 93.34 MW, with forecasts pointing to 231.64 MW by 2031 at a 19.93% CAGR.

Which city hosts most Romanian data-center capacity?

Bucharest accounts for 58.47% of installed capacity, benefiting from superior fiber density and enterprise demand.

What drives hyperscale interest in Romania?

EU cloud compliance, low-carbon power options, and new Black Sea connectivity attract Microsoft, AWS, and Google.

How volatile are electricity costs for operators?

Prices peaked at EUR 865 per MWh in July 2024, making energy 35-40% of operational expenditure, so PPAs with renewables are common.

Which size category grows fastest?

Mega facilities above 15 MW project a 21.74% CAGR as hyperscale tenants secure large contiguous blocks.

What is the main restraint outside Bucharest?

Limited carrier-neutral dark fiber in secondary cities raises connectivity costs and delays facility commissioning.

Page last updated on: