Packaged Honey Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.1 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

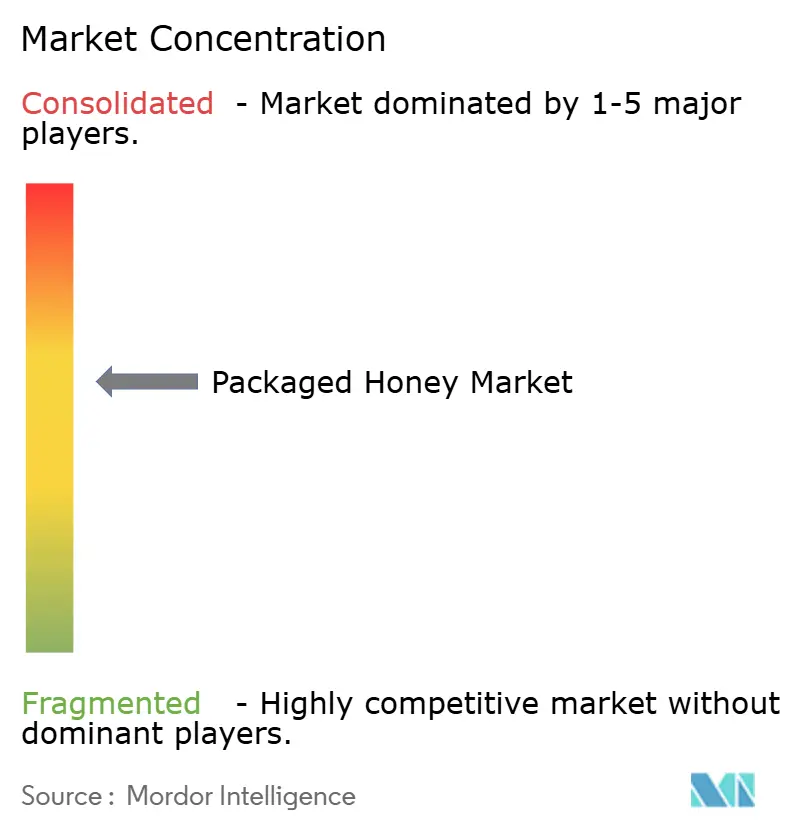

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Packaged Honey Market Analysis by Mordor Intelligence

The packaged honey market size was valued at USD 10.61 billion in 2025 and estimated to grow from USD 11.1 billion in 2026 to reach USD 13.92 billion by 2031, at a CAGR of 4.63% during the forecast period (2026-2031). The market demonstrates resilience despite increasing challenges from counterfeit products and mounting environmental pressures, including bee colony collapse, habitat loss, and climate change impacts on flower populations. Consumer preference for natural sweeteners, growing awareness of honey's health benefits, including its antibacterial and antioxidant properties, and the rapid expansion of e-commerce distribution channels support market growth. The industry's steady progression emphasizes the critical importance of quality differentiation and product authenticity verification as key competitive factors, particularly as consumers become more discerning about honey sourcing, production methods, and purity standards. The market's evolution is further shaped by increasing demand for organic and monofloral honey varieties, stringent food safety regulations, and technological advancements in honey testing and traceability systems.

Key Report Takeaways

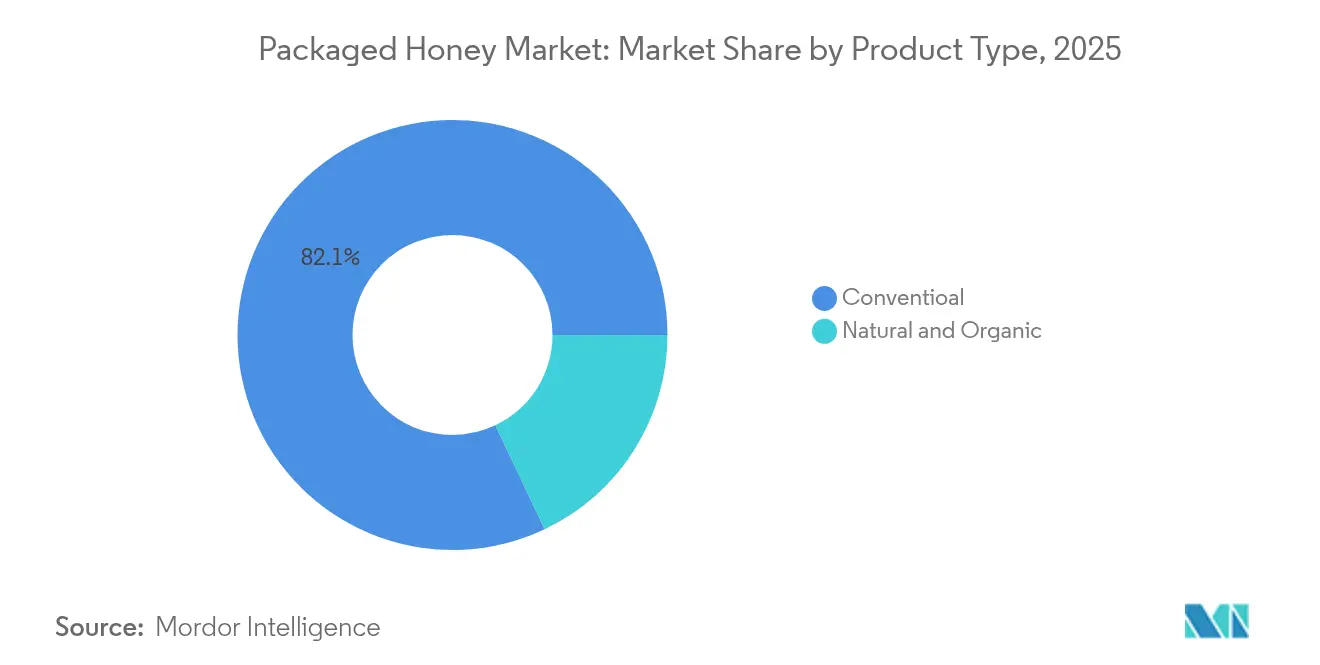

- By product category, conventional honey led with 82.05% revenue share in 2025; natural and organic variants are projected to expand at a 4.98% CAGR through 2031.

- By price range, the mass-market segment accounted for 68.12% of 2025 revenue; premium honey is forecast to grow at a 5.2% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets captured 39.12% of 2025 sales; online retail stores are poised for a 6.05% CAGR between 2026-2031.

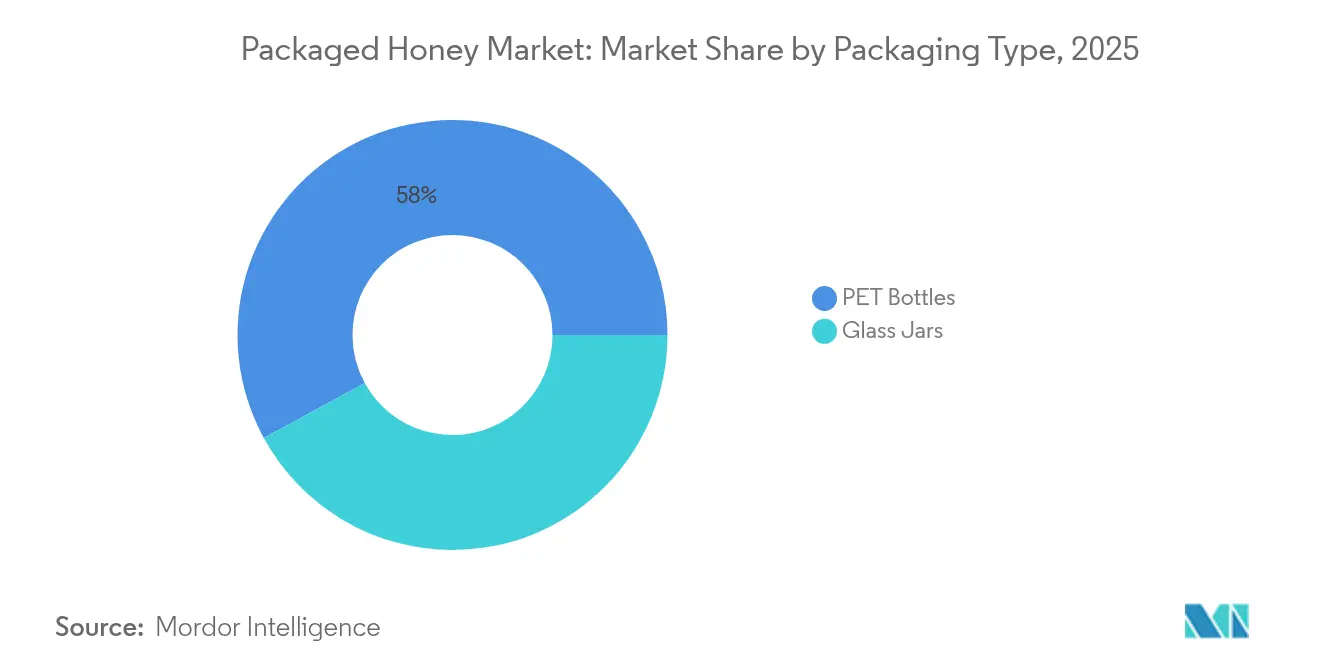

- By packaging type, PET bottles dominated with 57.96% share in 2025; glass jars are expected to register 5.65% CAGR through 2031.

- By geography, Europe held 36.74% of 2025 global revenue; Asia-Pacific is set to post a 6.4% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaged Honey Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Preference for Natural and Healthier Sweeteners | +0.7% | Global, with stronger adoption in North America and Europe | Medium term (2-4 years) |

| Rising Awareness of Medicinal and Therapeutic Properties | +0.6% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Technological Advancements in Product Development | +0.9% | North America and EU leading, APAC adoption accelerating | Short term (≤ 2 years) |

| Increasing Demand for Organic and Sustainable Products | +0.7% | Europe dominant, North America and APAC growing | Medium term (2-4 years) |

| Government Initiatives for Honey Production | +0.5% | National, with early gains in India, China, New Zealand | Long term (≥ 4 years) |

| The Growing Popularity of Quick Commerce | +0.6% | Urban centers globally, led by APAC and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Natural and Healthier Sweeteners

Consumer migration toward natural sweeteners reflects broader health consciousness trends that position honey as a premium alternative to processed sugars and artificial substitutes. The National Honey Board's [1]Source: National Honey Board, “2024 Attitudes & Usage Study,” honey.com2024 Attitudes and Usage study revealed that honey ranks as the most used sweetener across various meal occasions, with 75% of consumers willing to support bee-friendly products. This preference shift gains momentum as food manufacturers integrate honey into mainstream products, evidenced by the 2024 Queen's Choice Award winners, including Honey Nut PEP Bars and Wheaties Protein Honey Pecan variants. The trend extends beyond direct consumption to ingredient applications, where honey's functional properties in baking and processing create value-added opportunities for manufacturers seeking clean-label positioning. However, supply constraints from declining bee populations and authentication challenges could limit this driver's full potential if not addressed through technological solutions and regulatory frameworks.

Rising Awareness of Medicinal and Therapeutic Properties

Scientific validation of honey's therapeutic benefits drives premium market segments, particularly for specialized varieties like Manuka honey that command significant price premiums due to documented antimicrobial properties. This scientific backing enables honey producers to target health-conscious consumers willing to pay premium prices for functional foods. The medicinal positioning gains traction in traditional medicine markets, where honey serves as a carrier for other therapeutic compounds, expanding addressable market opportunities. Quality standardization becomes critical as therapeutic claims require consistent bioactive compound profiles, driving investment in analytical testing and certification processes. Geographic variations in medicinal honey acceptance create regional opportunity pockets, with Asian markets showing strong cultural affinity for honey-based remedies while Western markets increasingly embrace evidence-based functional food concepts.

Technological Advancements in Product Development

Recent technological developments in honey authentication and processing address key market challenges and support product innovation. McGill University developed artificial intelligence methods in April 2024 that use high-resolution mass spectrometry to create chemical fingerprints for verifying honey origin, enabling rapid identification in various forms. This technology allows producers and regulators to accurately determine the geographical source of honey samples and detect potential adulterations. Cranfield University introduced Spatial Offset Raman Spectroscopy (SORS) and DNA barcoding techniques that efficiently detect sugar syrup adulteration. These methods provide reliable results within minutes, significantly reducing testing time and costs compared to traditional laboratory analyses. Processing improvements include ultrasound methods for controlling crystallization, which enhance product quality and extend shelf life. The ultrasound technology enables precise control over honey crystallization patterns, resulting in improved texture and longer-lasting products. Companies that invest in these authentication and quality assurance technologies gain competitive advantages in the market through enhanced product integrity and consumer trust.

Increasing Demand for Organic and Sustainable Products

Organic honey market expansion reflects consumer willingness to pay premiums for environmentally responsible production methods. European markets lead this trend, accounting for 48% of global certified honey imports valued at USD 1,146.16 million in 2023, driven by government procurement policies ensuring product authenticity and traceability, according to the Government of the Netherlands[2]Source: Government of Netherlands, "The European market potential for certified honey", www.cbi.eu. Sustainability positioning extends beyond organic certification to encompass bee welfare initiatives, carbon footprint reduction, and biodiversity conservation programs that resonate with environmentally conscious consumers. The market players are launching new products in the market to cater to the rising demand for organic honey in the market. For instance, in January 2024, Apis India launched new organic honey in the market. The honey is sourced from Kashmir and is certified organic.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of counterfeit products | -0.4% | Global, with highest impact in Europe and North America | Short term (≤ 2 years) |

| Environmental and Climatic Factors | -0.3% | Global, with severe impact in traditional production regions | Long term (≥ 4 years) |

| Supply Chain Disruptions | -0.2% | Global, with higher vulnerability in import-dependent regions | Medium term (2-4 years) |

| Stringent Regulatory and Certification Requirements | -0.2% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Counterfeit Products

Globally, honey ranks among the most counterfeited foods. Beekeepers face increasing challenges in maintaining the health and productivity of their colonies. The financial burden of competing with low-cost counterfeit honey further strains their operations. Illegal imports that bypass tariffs have driven down the price of authentic honey, resulting in substantial financial losses and a decline in the domestic honey production sector. For instance, in France, customs officials reported a significant increase in seizures, with 131 cases of adulterated honey recorded in 2023. Counterfeit honey often contains additives such as corn syrup to replicate the taste and texture of genuine honey. These adulterants compromise honey's nutritional and medicinal properties, stripping it of essential enzymes, antioxidants, and antibacterial benefits. Such practices hinder the growth of the global honey market and increase the risk of diabetes among consumers. These additives pose significant health concerns by misleading consumers into believing they are purchasing a healthy product. Without stringent regulatory measures and industry-wide collaboration, the honey market will continue to face challenges in maintaining its integrity and achieving sustainable growth.

Environmental and Climatic Factors

Climate change and environmental degradation threaten honey production through multiple pathways, including habitat loss, pesticide exposure, and extreme weather events that disrupt bee populations and flowering cycles. The 2023 U.S. honey production data showed an 11% increase to 139 million pounds despite a 6% decrease in colony numbers, indicating productivity gains that may not be sustainable under continued environmental pressure, as per the USDA. Bee truck accidents exemplify supply chain vulnerabilities, with single incidents potentially causing USD 160,000+ losses for commercial operations carrying 450 colonies. Research into pollen-replacing foods offers potential mitigation, with Washington State University developing nutritionally complete bee feeds expected to be available by mid-2026. However, these solutions require widespread adoption and may not fully address ecosystem-level challenges affecting wild bee populations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Organic Premiumization Accelerates

Natural and organic honey variants are experiencing robust 4.98% CAGR growth through 2031, despite conventional honey maintaining an 82.05% market share in 2025. This growth differential reflects consumer willingness to pay premiums for perceived health benefits and environmental responsibility, with organic honey sales outperforming conventional varieties in recent assessments. The organic segment benefits from regulatory tailwinds, including the EU's strengthened traceability requirements and the U.S. Strengthening Organic Enforcement rule, effective March 2024, which mandates certification for all organic operations, including imports, according to the United States Department of Agriculture.

Conventional honey's dominant position stems from price accessibility and widespread availability, yet faces mounting pressure from authentication challenges that disproportionately affect mass-market segments where margins cannot support extensive testing protocols. Research comparing conventional versus organically produced honey reveals measurable differences in physicochemical and nutritional characteristics that justify premium positioning. The segment bifurcation creates distinct value propositions, with conventional products competing primarily on price and availability while organic variants leverage quality, sustainability, and health positioning to command higher margins.

By Price Range: Premium Growth Outpaces Mass Market

The premium honey segment is projected to grow at a CAGR of 5.2% through 2031, outpacing mass market growth despite the latter holding a 68.12% market share in 2025. Premium honey products, particularly Manuka honey, command higher prices due to their therapeutic properties and limited production regions. This growth trend reflects increasing consumer preference for high-quality, specialized honey varieties and their willingness to pay premium prices for products with proven health benefits and authentic sourcing. The expansion of the premium segment is further driven by growing awareness of honey's medicinal properties, rising disposable incomes in developing markets, and sophisticated marketing strategies that emphasize product uniqueness and quality certifications.

Mass market segments face intensifying pressure from low-cost imports and counterfeit products that undermine pricing power, forcing producers to compete primarily on distribution efficiency and brand recognition. The premium segment's resilience during economic uncertainty demonstrates Honey's positioning as an affordable luxury where consumers maintain spending on perceived health benefits. Geographic variations in premium acceptance create regional opportunity pockets, with developed markets showing stronger premium adoption while emerging markets gradually develop appreciation for quality differentiation.

By Packaging Type: Sustainability Drives Glass Innovation

Glass jars are capturing market momentum with 5.65% CAGR growth through 2031, outpacing PET bottles despite the latter maintaining 57.96% market share in 2025. This packaging evolution reflects consumer sustainability concerns and premium positioning strategies that associate glass with product quality and environmental responsibility. Glass packaging enables superior product preservation, particularly important for specialty honey varieties where flavor profiles and therapeutic properties require protection from light and oxygen exposure. Owing to this, the market players are launching new packaging in the market. For instance, in February 2024, Saffola launched a new packaging material to celebrate Sundarband Day. The newly redesigned packaging for Saffola Honey Active is rolled out across various markets, including Hyderabad, Mumbai, Kolkata, Chennai, Delhi, and Bangalore.

PET bottles retain dominance through cost advantages and convenience factors, particularly in mass market segments where price sensitivity outweighs sustainability concerns. However, the packaging landscape is evolving as environmental regulations tighten and consumer preferences shift toward sustainable alternatives. Innovation in glass packaging includes lightweight designs and improved closure systems that maintain convenience while addressing sustainability demands. The packaging choice increasingly serves as a brand differentiation tool, with premium producers leveraging glass to signal quality positioning while mass market brands optimize PET designs for cost efficiency and distribution advantages.

By Distribution Channel: Digital Transformation Accelerates

Online retail stores are experiencing rapid 6.05% CAGR expansion through 2031, challenging traditional supermarket and hypermarket dominance despite the latter maintaining 39.12% market share in 2025. This digital transformation enables direct-to-consumer relationships that bypass traditional distribution intermediaries, potentially improving margins while providing detailed product information that supports premium positioning. Quick commerce platforms facilitate same-day delivery of honey products, addressing convenience demands while maintaining product freshness.

Convenience and grocery stores, along with other distribution channels, serve specialized market niches but face pressure from e-commerce expansion and changing consumer shopping patterns. The distribution evolution particularly benefits specialty honey varieties that require consumer education and detailed product information, areas where digital platforms excel over traditional retail formats. However, authentication challenges intensify in online channels where consumers cannot physically inspect products, making brand reputation and certification credentials critical success factors for digital distribution success.

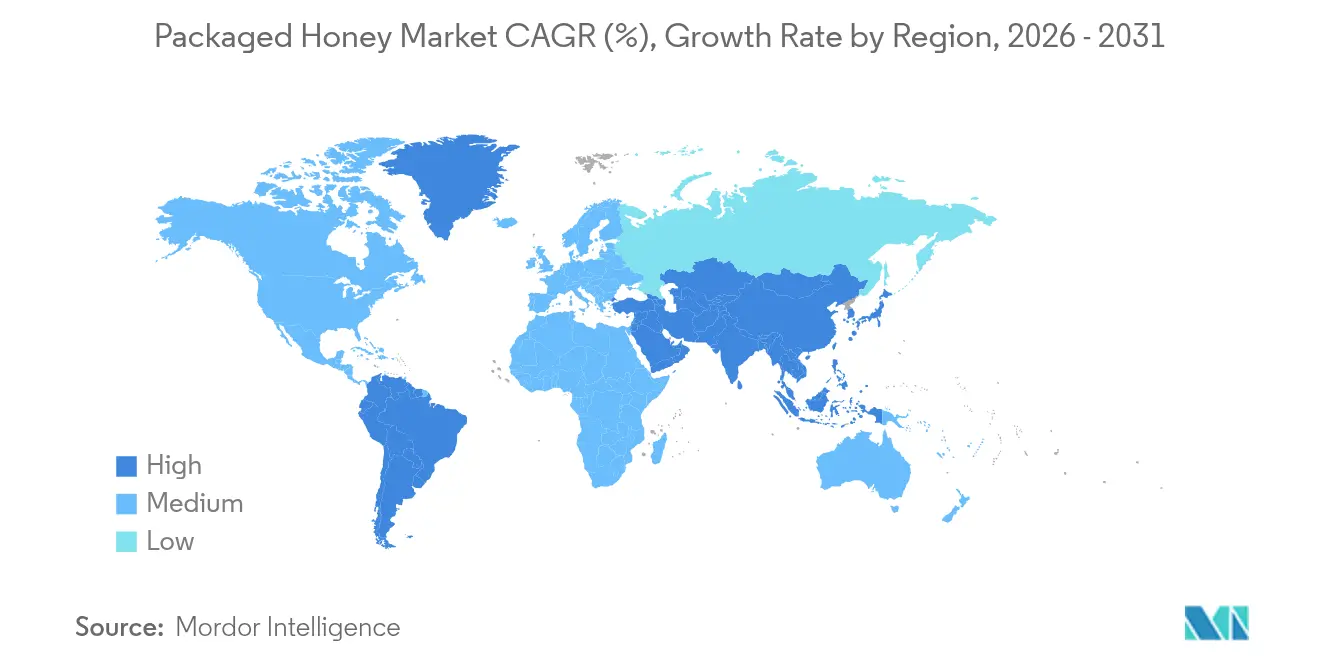

Geography Analysis

Europe maintains market leadership with a 36.74% share in 2025, driven by sophisticated import infrastructure and stringent quality standards. The region's growth reflects market maturity and regulatory complexity, with the revised EU Directive EU 2024/1438 mandating country-of-origin labeling by June 2026 and establishing a 90-expert Honey Platform for harmonized traceability standards. Germany leads European imports, followed by the UK, France, and Belgium, with growing demand for certified and monofloral honey varieties. Austria's implementation of monthly DNA testing on 100 honey samples demonstrates emerging regulatory responses to combat the 46% adulteration rate identified in EU investigations.

Asia-Pacific emerges as the fastest-growing region with 6.4% CAGR through 2031, propelled by China's dual role as the world's largest producer and expanding importer. According to the National Bureau of Statistics of China, data from 2024, the annual production volume of honey in China was 444.8 thousand metric tons. The region benefits from rising disposable incomes and growing health consciousness that drives premium honey consumption. China's expanding import requirements for countries like Tanzania and Rwanda demonstrate growing market access opportunities supported by bilateral trade agreements, though antidumping duties on various countries create trade flow complexities.

North America also shows steady growth in the market, owing to the rising inclination towards a healthy lifestyle and food choices. Other regions such as South America, the Middle East, and Africa are also showing mature growth, with the market players penetrating the market. For instance, in April 2025, Anthology Honey, a premium brand, launched its products in the United Arab Emirates. The brand's exquisite collection showcases four rare honey varieties, each with unique medicinal properties and gourmet flavors: Evergreen Oak, Sidr, Mediterranean Blossoms, Silver Fir, and Vanilla Fir.

Competitive Landscape

The honey market exhibits moderate concentration, indicating fragmented competition where both established players and niche entrants can capture market share through differentiation strategies. This competitive structure reflects the industry's geographic dispersion and product variety, where regional preferences and specialty segments create multiple competitive niches. Companies increasingly compete on authentication capabilities and quality assurance systems rather than price alone, as widespread fraud issues make credibility a primary competitive advantage.

The major players are indulging in strategies, like product launches, mergers and acquisitions, expansions, and partnerships, to establish a strong consumer base and esteemed position in the market. They also compete on different factors, including product offerings, quality, packaging, and price, to gain a competitive advantage in the market. The major players in the market include Dabur India Ltd, Sioux Honey Association Co-op, Sweet Harvest Foods, Barkman Honey LLC, and Hive and Wellness (Capilano). Strategic patterns center on vertical integration and technology adoption, with leading players investing in supply chain traceability and authentication technologies to differentiate from counterfeit products. The competitive landscape favors companies with robust certification frameworks and direct supplier relationships that enable quality control throughout the value chain. White-space opportunities exist in premium organic segments and emerging markets where established players have limited presence, while technology-enabled authentication services represent emerging disruptor potential.

Packaged Honey Industry Leaders

-

Dabur India Ltd

-

Sioux Honey Association Co-op

-

Sweet Harvest Foods

-

Barkman Honey LLC

-

Hive and Wellness (Capilano)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Country Delight has launched its newest product, Farm Honey, certified through rigorous Nuclear Magnetic Resonance (NMR) testing. This certification was carried out by a certified laboratory in Germany. Beyond being a natural sweetener, honey is gaining recognition for its myriad functional benefits.

- October 2024: Farmery, a direct-to-consumer (D2C) brand, has unveiled two new honey variants: 'Organic Honey' and 'Wild Forest Honey'. Sourced from certified organic farms, 'Organic Honey' guarantees customers a pure, chemical-free, and nutrient-rich experience. Meanwhile, 'Wild Forest Honey' offers a distinct flavor profile, drawing from the diverse flora of untouched forests.

- June 2024: Nature Nate’s Honey Co. (Nate’s), renowned for its 100% pure honey, has introduced revamped packaging for its Nate’s honey minis. The products are available in single-serve packaging, allowing consumers to have honey on-the-go.

- January 2024: Dabur, one of the leading firms in the Ayurvedic and personal care space, recently invested approximately INR 135 crore in expanding its manufacturing facility in South India. This move is geared toward bolstering the production capacity of its flagship products, including Dabur Honey, Dabur Red Paste, and Odonil air fresheners.

Global Packaged Honey Market Report Scope

Honey is a sweet and viscous food substance obtained from honeybees and other bees.

The global packaged honey market is segmented by product category (conventional and organic), packaging type (pet bottles, glass jars, and other packaging types), and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Natural and Organic |

| Conventional |

| Mass |

| Premium |

| PET Bottles |

| Glass Jars |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Category | Natural and Organic | |

| Conventional | ||

| By Price Range | Mass | |

| Premium | ||

| By Packaging Type | PET Bottles | |

| Glass Jars | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the honey market?

The honey market is valued at USD 11.1 billion in 2026 and is projected to reach USD 13.92 billion by 2031.

Which region leads global honey sales?

Europe accounts for 36.74% of 2025 global revenue, benefiting from stringent quality standards and a mature import network.

Which segment is expanding the fastest?

Premium honey is advancing at a 5.2% CAGR, outpacing mass-market growth due to rising demand for origin-verified and functional varieties.

Why is glass gaining popularity as a honey package?

Glass jars are growing at 5.65% CAGR because consumers associate them with sustainability and product purity, reinforcing premium positioning.

Page last updated on: