Beeswax Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 606.91 Million |

| Market Size (2031) | USD 764.56 Million |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beeswax Market Analysis by Mordor Intelligence

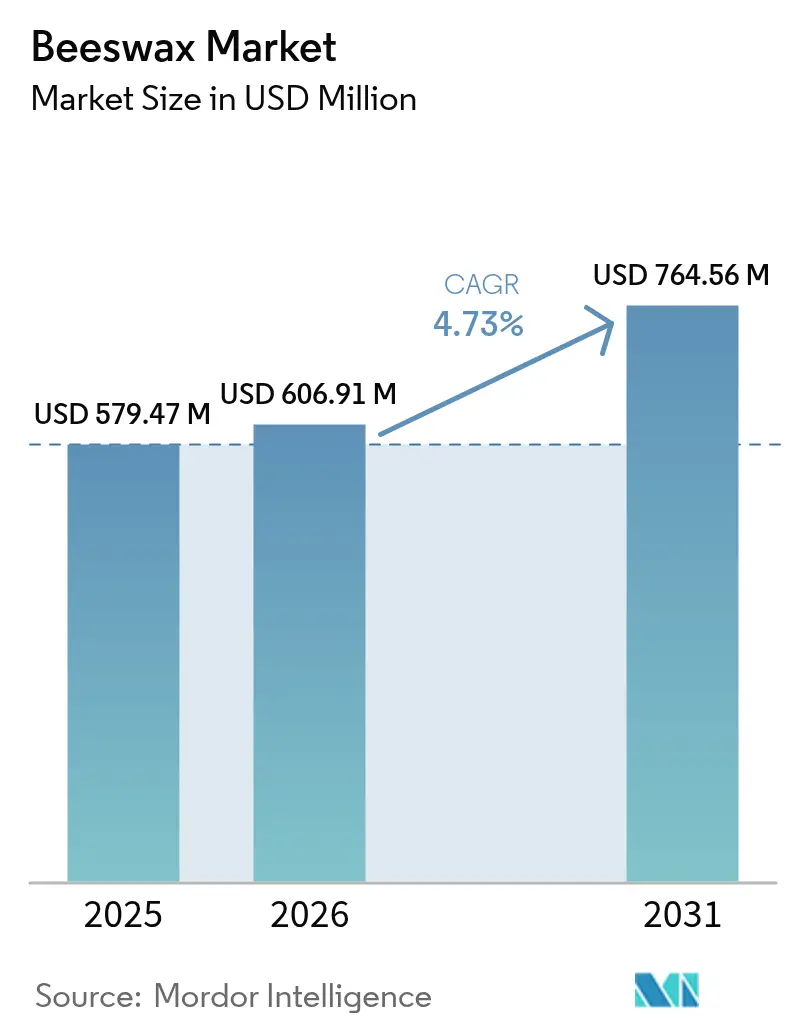

The global beeswax market size was valued at USD 579.47 million in 2025 and estimated to grow from USD 606.91 million in 2026 to reach USD 764.56 million by 2031, at a CAGR of 4.73% during the forecast period (2026-2031). The global beeswax market is driven by several interconnected factors, primarily the increasing consumer preference for natural, organic, and sustainable ingredients, as individuals move away from synthetic chemicals. This trend has particularly enhanced the use of beeswax in cosmetics, personal care, pharmaceuticals, and food products due to its moisturizing, emulsifying, and non-toxic properties. Additionally, rising disposable incomes and urbanization have further fueled the demand for beauty and wellness products containing beeswax. The eco-friendly nature of beeswax and its growing application as a biodegradable alternative in packaging and other industrial uses have also contributed to its appeal.

Key Report Takeaways

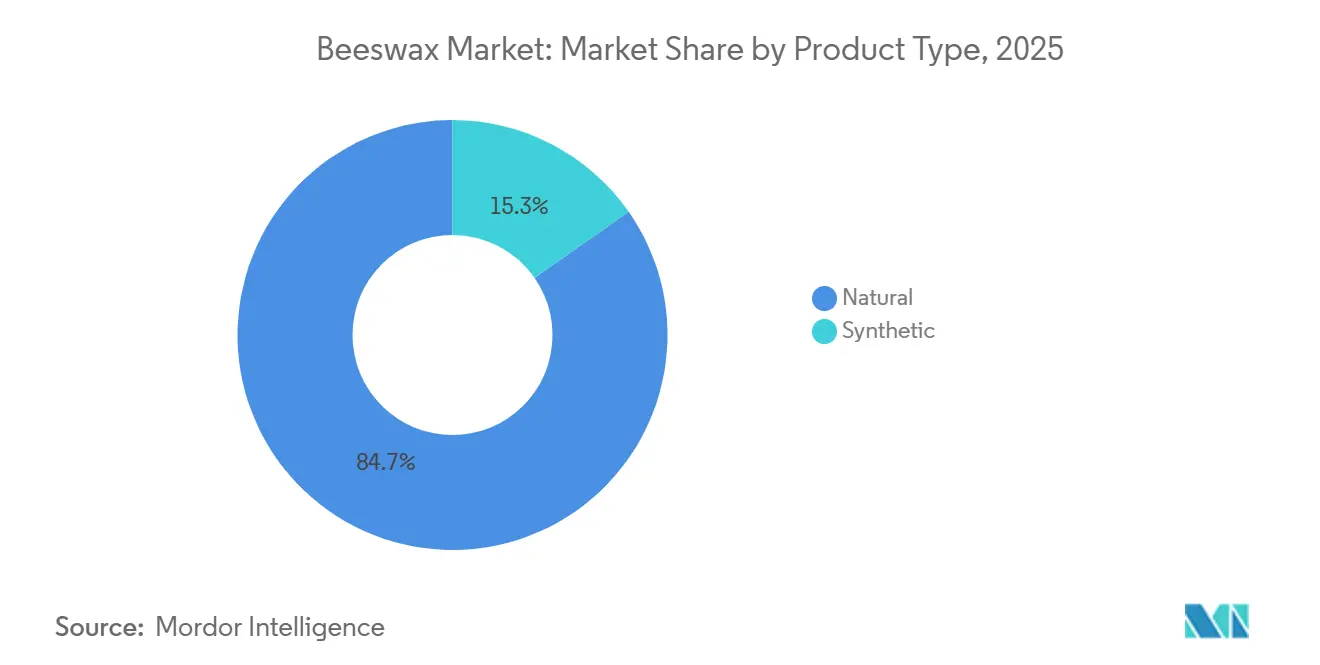

- By product type, natural beeswax held 84.71% of the 2025 beeswax market share, and synthetic grades are projected to post a 5.91% CAGR through 2031.

- By form, blocks led with 42.85% of 2025 revenue, while sheets/beads are forecast to expand at a 6.05% CAGR between 2026-2031.

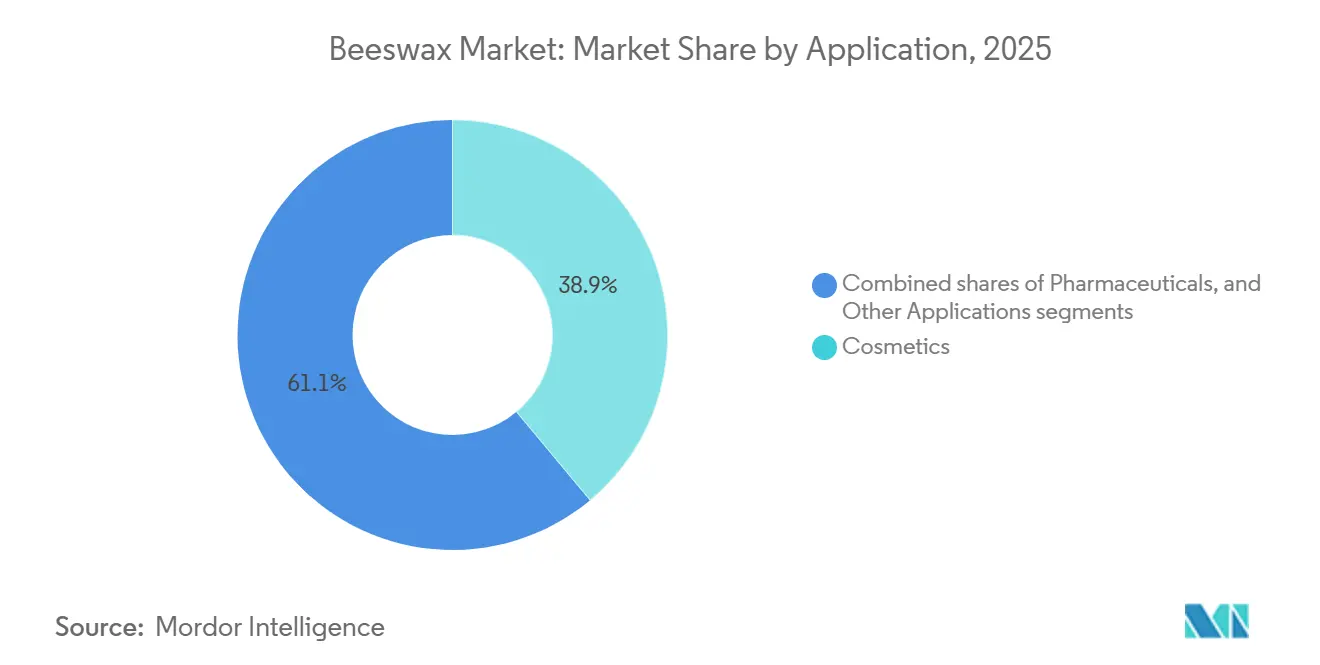

- By application, cosmetics contributed 38.94% of the 2025 value and are poised for a 6.23% CAGR over the forecast period.

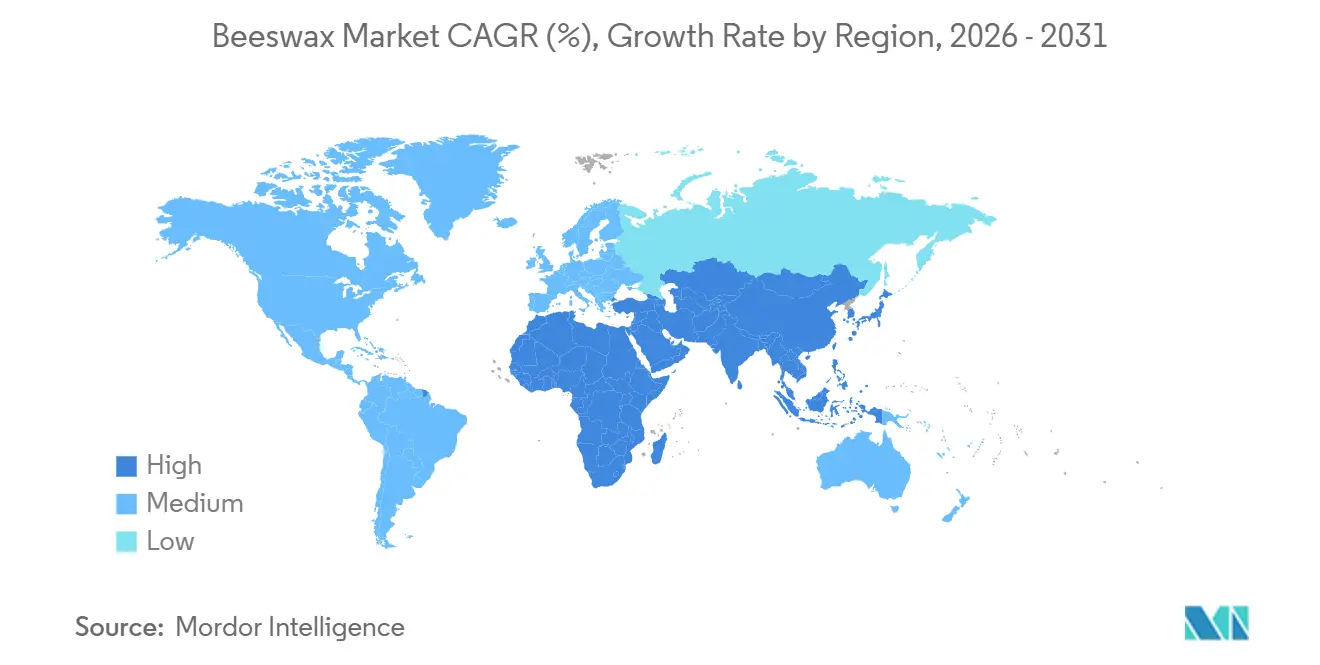

- By geography, Asia-Pacific accounted for 37.69% of global revenue in 2025 and is projected to advance at a 6.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Beeswax Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for natural and organic ingredients in personal care | +1.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Clean beauty and ingredient transparency movement | +0.9% | North America and European Union core, spillover to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expanding pharmaceutical applications | +0.7% | Global, led by North America and Europe for regulatory approvals | Long term (≥ 4 years) |

| Rising demand for non-toxic and allergen-free food additives and coatings | +0.6% | Global, with early gains in European Union and North America organic segments | Medium term (2-4 years) |

| Rising popularity of handmade and traditional crafts | +0.5% | North America, Europe, and Asia-Pacific artisanal markets | Short term (≤ 2 years) |

| Advancement in purification and processing technologies | +0.4% | Global, with technology hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing preference for natural and organic ingredients in personal care

The growing consumer preference for natural and organic ingredients in personal care products is a key driver of growth in the global beeswax market. As awareness of sensitivities to synthetic chemicals and concerns about long-term skin health increase, manufacturers are reformulating skincare, lip care, haircare, and cosmetic products with plant- and hive-derived ingredients that are perceived as safer and more sustainable. Beeswax is particularly valued for its emollient, protective, and stabilizing properties, making it a preferred multifunctional ingredient in clean-label formulations. Regulatory standards further support this trend; for instance, the EU’s COSMOS standard mandates that at least 95% of physically processed agro-ingredients must be organic, positioning certified beeswax as a critical compliance component for brands targeting environmentally conscious consumers[1]Source: COSMOS Certification, "COSMOS-standard Cosmetics Organic and Natural Standard," media.cosmos-standard.org . This alignment between regulatory requirements and consumer preferences continues to drive the adoption of beeswax across both premium and mass-market personal care segments.

Clean beauty and ingredient transparency movement

The growing emphasis on clean beauty and ingredient transparency is a significant driver for the global beeswax market. Consumers are increasingly examining product labels and preferring formulations with recognizable, minimally processed, and naturally derived ingredients over synthetic alternatives. Beeswax benefits from this trend due to its natural origin, versatile properties, and established history of safe use in skincare and cosmetic products. Additionally, regulatory changes are strengthening transparency standards across the industry. The U.S. Modernization of Cosmetics Regulation Act of 2022 mandates cosmetic manufacturers to register their facilities with the FDA, disclose product ingredients in a public database, and report adverse events, thereby raising compliance requirements for all cosmetic raw materials, including beeswax[2]Source: U.S. Food and Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)," fda.gov . As brands adjust to stricter regulations and rising consumer expectations, beeswax emerges as a compliant and appealing ingredient for transparent, clean-label product lines.

Expanding pharmaceutical applications

Pharmaceutical applications are driving significant growth in the global beeswax market. Beeswax is extensively used in ointments, creams, suppositories, and controlled-release formulations due to its biocompatibility, stability, and natural thickening and binding properties. Its protective and moisture-retention characteristics make it ideal for topical treatments, wound care products, and dermatological preparations. With increasing demand for semi-solid dosage forms and plant-based excipients, pharmaceutical manufacturers are incorporating beeswax as a functional, naturally derived ingredient. Additionally, rising healthcare expenditure, an aging population, and a growing focus on skin-related therapies are further boosting beeswax usage in pharmaceutical manufacturing, solidifying its importance as a valuable excipient in modern drug formulations.

Rising demand for non-toxic and allergen-free food additives and coatings

The increasing demand for non-toxic and allergen-free food additives and coatings is driving growth in the global beeswax market. As consumers focus more on clean-label and minimally processed foods, manufacturers are adopting naturally derived ingredients to replace synthetic glazing agents and preservatives. Beeswax is extensively used as a food-grade coating for fruits, confectionery, and bakery products due to its moisture-barrier properties, ability to extend shelf life, and recognized safety profile. Its application in edible films and protective coatings supports efforts to reduce chemical additives while preserving product quality and freshness. With heightened regulatory scrutiny of artificial ingredients and growing awareness of food sensitivities, beeswax is gaining prominence as a reliable, naturally sourced alternative in food processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material supply variability due to climate and environmental factors | -0.8% | Global, acute in North America, Europe, and Asia-Pacific regions with intensive agriculture | Medium term (2-4 years) |

| Strict regulatory requirements in food and pharmaceutical sectors | -0.5% | North America and European Union, with spillover to Asia-Pacific export-oriented producers | Long term (≥ 4 years) |

| Risk of pesticide residues and contamination | -0.4% | Global, concentrated in regions with high agrochemical use | Short term (≤ 2 years) |

| Labor-intensive nature of beekeeping | -0.3% | North America and Europe high-wage economies, emerging pressure in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Variability in raw material supply, driven by factors such as climate change, disease outbreaks, and environmental stressors, significantly restrains the global beeswax market. Beeswax production is closely tied to the health and survival rates of honey bee colonies. Survey data from the United States for 2023-2024 illustrate the severity of this issue, with beekeepers reporting an estimated annual colony loss rate of 55.1%, significantly higher than the long-term average of 40.3%. Summer losses were recorded at 30.4%, while winter losses reached 37.3%[3]Source: Apiary Inspectors of America, "Preliminary Results from the 2023-2024 US Beekeeping Survey: Colony Loss and Management," apiaryinspectors.org. Commercial operators, who manage most colonies, faced even higher losses, with an annual mortality rate of 55.7%, well above historical averages[4]Source: Apiary Inspectors of America, "Preliminary Results from the 2023-2024 US Beekeeping Survey: Colony Loss and Management," apiaryinspectors.org. State-level data revealed substantial variation, with annual losses ranging from 17.7% to 76.2%, highlighting the uneven and unpredictable effects of environmental factors[5]Source: Apiary Inspectors of America, "Preliminary Results from the 2023-2024 US Beekeeping Survey: Colony Loss and Management," apiaryinspectors.org. These elevated and fluctuating colony mortality rates disrupt beeswax production, leading to supply instability and increased procurement costs for industries such as cosmetics, pharmaceuticals, and food processing, thereby limiting consistent market growth.

Strict regulatory requirements in food and pharmaceutical sectors

Strict regulatory requirements in the food and pharmaceutical industries constrain the global beeswax market by increasing compliance complexity and operational costs for manufacturers. Beeswax used in applications such as edible coatings, food glazing agents, medicinal ointments, and drug formulations must adhere to stringent standards for purity, contamination, and traceability to ensure consumer safety. Regulatory authorities mandate detailed specifications on factors such as pesticide residues, heavy metals, microbiological limits, and processing methods, necessitating extensive testing and certification prior to market approval. Additionally, variations in regulatory frameworks across regions complicate international trade, as suppliers must comply with differing labeling, quality, and documentation requirements. These rigorous standards, while critical for safety and quality assurance, can extend approval timelines, elevate production costs, and restrict market entry for smaller producers, thereby tempering overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Dominance Anchors Value Chain

In 2025, natural beeswax accounted for 84.71% of the market share, underscoring its essential role in organic-certified cosmetics, pharmaceutical excipients, and food-grade coatings. The demand for natural beeswax is primarily driven by the increasing preference for plant- and hive-derived ingredients in cosmetics, personal care, pharmaceuticals, and clean-label food applications. Consumers are showing a growing inclination toward minimally processed, biodegradable, and sustainably sourced materials, positioning natural beeswax as a reliable alternative to petrochemical-based waxes. The rising popularity of organic beauty products, eco-friendly candles, and natural food coatings further boosts demand. Additionally, premiumization trends in skincare and wellness products are driving higher-value applications for certified and traceable natural beeswax.

Meanwhile, synthetic beeswax is projected to grow at a compound annual growth rate (CAGR) of 5.91% through 2031, driven by cost-conscious industrial formulators seeking paraffin-free alternatives with predictable melting points. The synthetic beeswax market benefits from the need for cost-effective, consistent, and scalable wax alternatives in large-volume industrial applications. Manufacturers prefer synthetic variants due to their uniform quality, controlled melting points, and stable supply, which is unaffected by climatic or apiculture-related fluctuations. The expanding use of synthetic beeswax in cosmetics, polishes, coatings, adhesives, and pharmaceutical formulations, where performance consistency is crucial, further supports market growth. Additionally, synthetic beeswax appeals to vegan and cruelty-free product segments, enabling brands to align with ethical positioning while maintaining formulation efficiency.

By Form: Blocks Lead While Sheets/Beads Gain Traction

Blocks accounted for a share 42.85% in 2025. The demand for block-form beeswax is primarily driven by bulk industrial buyers and traditional craft sectors that require raw, unprocessed wax for further customization. Cosmetic and pharmaceutical manufacturers often prefer block formats for large-batch melting, blending, and formulation processes, as blocks are easier to transport and store in high volumes. The candle-making industry, including artisanal and religious candle producers, also favors blocks due to their flexibility in shaping and remolding. Additionally, block beeswax is typically associated with lower processing costs, making it an economical choice for buyers in large-scale applications.

In contrast, sheets and beads are projected to grow at a compound annual growth rate (CAGR) of 6.05%. The growth of these forms is supported by their convenience, precision dosing, and ease of handling in small- to medium-scale production. Beeswax beads are particularly popular among cosmetic formulators and DIY skincare brands because they melt quickly and allow for accurate measurement, reducing waste and improving production efficiency. Beeswax sheets are widely used in candle rolling and craft applications, especially in educational, hobbyist, and decorative segments. The increasing popularity of home-based cosmetic production, handmade candles, and creative craft activities continues to drive demand for these user-friendly and value-added beeswax formats.

By Application: Cosmetics Leadership Drives Market Growth

In 2025, cosmetics accounted for 38.94% of application-based revenue and are projected to grow at a CAGR of 6.23%. The demand for beeswax in cosmetics is driven by its multifunctional properties as a natural thickener, emulsifier, and protective barrier agent. It is widely used in products such as lip balms, creams, mascaras, and lotions. Increasing consumer preference for clean-label, plant- and hive-derived ingredients has prompted brands to replace synthetic stabilizers with naturally sourced alternatives. Beeswax enhances texture, improves product stability, and provides moisture retention benefits, making it valuable for both premium and mass-market formulations. Additionally, the rising demand for organic, sustainable, and biodegradable personal care products further supports its adoption in skincare and color cosmetics.

In pharmaceutical applications, the demand for beeswax is driven by its role as a safe and biocompatible excipient in ointments, topical creams, suppositories, and controlled-release formulations. Its ability to provide structural consistency, stabilize active ingredients, and create protective barriers makes it suitable for dermatological and wound-care preparations. The increasing focus on semi-solid dosage forms, the expanding geriatric population requiring topical treatments, and the growing interest in naturally derived excipients are further encouraging its use. Additionally, pharmaceutical manufacturers value beeswax for its stability and compatibility with a wide range of therapeutic compounds.

Geography Analysis

In 2025, Asia-Pacific accounted for 37.69% of the global market value and is projected to grow at a CAGR of 6.32% through 2031. The growth of the beeswax market in the Asia-Pacific is driven by the expansion of cosmetics and personal care manufacturing, rising disposable incomes, and increasing consumer preference for natural and herbal products. Countries such as China, India, Japan, and South Korea are experiencing strong demand for skincare, lip care, and traditional medicine products that utilize naturally derived ingredients. Additionally, growth in candle production, food processing, and pharmaceutical manufacturing supports regional consumption. The availability of raw materials, supported by large apiculture bases in parts of Asia, and the rapid growth of e-commerce platforms further enhance the distribution of beeswax-based products in the region.

In North America and Europe, the demand for beeswax is driven by established clean beauty markets, stringent regulatory standards promoting safer ingredients, and a strong consumer preference for organic and sustainable products. The growing interest in eco-friendly candles, natural food coatings, and plant-based pharmaceutical excipients is broadening its application scope. Trends toward premiumization in skincare and cosmetics, coupled with heightened awareness of ingredient transparency, further support beeswax adoption among both established brands and niche artisanal producers. Additionally, regulatory oversight and quality certifications in these regions strengthen confidence in responsibly sourced and traceable beeswax supplies.

Latin America and the Middle East represent emerging opportunities, with Brazil and Argentina expanding apiculture to serve domestic food-coating and export markets, while Saudi Arabia and the United Arab Emirates import pharmaceutical-grade beeswax to support growing cosmetics manufacturing hubs. Brazil's tropical climate enables year-round honey and beeswax production, though quality-control infrastructure lags North American and European standards, limiting access to premium pharmaceutical and organic-certified segments. The Middle East's cosmetics sector is adopting halal-certification frameworks that align with beeswax's natural provenance, creating niche demand streams that complement conventional applications. Africa's beekeeping potential remains underexploited due to limited refining capacity and export logistics, yet initiatives by development agencies to promote apiculture as a rural-livelihood strategy may unlock supply over the medium term.

Competitive Landscape

The beeswax market is moderately fragmented, with established refiners such as Koster Keunen, Strahl & Pitsch, and British Wax Refining utilizing vertical integration, proprietary derivatives, and multi-country sourcing to target premium market segments. These companies leverage their control over the supply chain and advanced processing techniques to produce high-quality products that meet the stringent requirements of premium buyers. In contrast, regional processors and commodity traders cater to price-sensitive industrial buyers by focusing on cost-effective production and bulk supply.

Opportunities remain underexplored in pharmaceutical applications, including tamper-resistant formulations, buccal films, and transdermal patches, where beeswax's hydrophobic matrix properties provide potential advantages such as moisture resistance and controlled release, which are not fully leveraged compared to synthetic polymers. Additionally, in biodegradable food packaging, beeswax-shellac composites and corn-husk hybrids demonstrate performance comparable to plastic films at competitive costs, offering an eco-friendly alternative that aligns with increasing consumer demand for sustainable packaging solutions.

Emerging players, such as PLA-stearate wax producers, are appealing to cost-conscious formulators with renewable feedstock options. However, their inability to obtain USDA organic or COSMOS certification limits their access to premium cosmetics and food-grade markets, where certifications are critical for consumer trust and regulatory compliance. Technology adoption, including blockchain traceability, IoT-enabled hive monitoring, and AI-driven quality prediction, is still in its early stages. These advancements are primarily utilized by top-tier refiners who can distribute digital investment costs across large volumes, enabling them to enhance supply chain transparency, optimize hive productivity, and ensure consistent product quality. Meanwhile, mid-tier players rely on manual processes and third-party testing, leading to longer lead times and greater variability in quality, which can hinder their competitiveness in the market.

Beeswax Industry Leaders

-

Koster Keunen Inc.

-

Strahl & Pitsch Inc.

-

British Wax Refining Co. Ltd.

-

New Zealand Beeswax Ltd.

-

Paramold Manufacturing LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Northern Roots Bee Co. produces beeswax sustainably by harvesting old combs and wax cappings to preserve bee colonies. The company uses a melting and filtering process to create pure, natural wax that performs better than paraffin and soy alternatives.

- October 2023: Procudan launches ProCera Natural, the first fossil-free cheese wax formulated from natural ingredients including beeswax, after six years of development supported by Innovation Fund Denmark, targeting dairy industry sustainability requirements

- June 2023: Koster Keunen launched “The Bee Story,” a sustainable beeswax program promoting ethical sourcing, biodiversity, and community empowerment in West Africa. The initiative enhances supply chain stability, supports local beekeepers, reduces environmental impact, and aligns with rising consumer demand for sustainability in cosmetics.

Global Beeswax Market Report Scope

Naturally generated and secreted by honeybees, beeswax is a substance derived directly from the honeycomb and exudes the aroma of honey. Due to its properties and composition, beeswax is widely used in aromatherapy, cosmetics, pharmaceuticals, and food manufacturing.

The report on beeswax provides a segmental market analysis according to product type, application, and geography. The market is segmented into pharmaceuticals, cosmetics, and other applications based on application. By product type, the market is segmented into organic and conventional. By geography, the study analyzes the market into emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The market sizing has been done in value terms in USD for all the above-mentioned segments.

| Natural |

| Synthetic |

| Blocks |

| Pellets/Pastilles |

| Sheets/Beads |

| Cosmetics |

| Pharmaceuticals |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Morocco | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Natural | |

| Synthetic | ||

| By Form | Blocks | |

| Pellets/Pastilles | ||

| Sheets/Beads | ||

| By Application | Cosmetics | |

| Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Morocco | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the estimated global value of the beeswax market in 2026?

The beeswax market size reached USD 606.91 million in 2026.

Which application segment consumes the most beeswax?

Cosmetics lead, accounting for 38.94% of 2025 revenue and expanding at a 6.23% CAGR through 2031.

Why are synthetic waxes gaining traction?

They offer consistent quality and residue-free profiles, supporting a 5.91% CAGR, particularly in pharmaceutical and food-contact uses.

Which region dominates beeswax production?

Asia-Pacific supplies 37.69% of global revenue, driven primarily by India’s large-scale output.

Page last updated on: