Higher Education Game-Based Learning Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

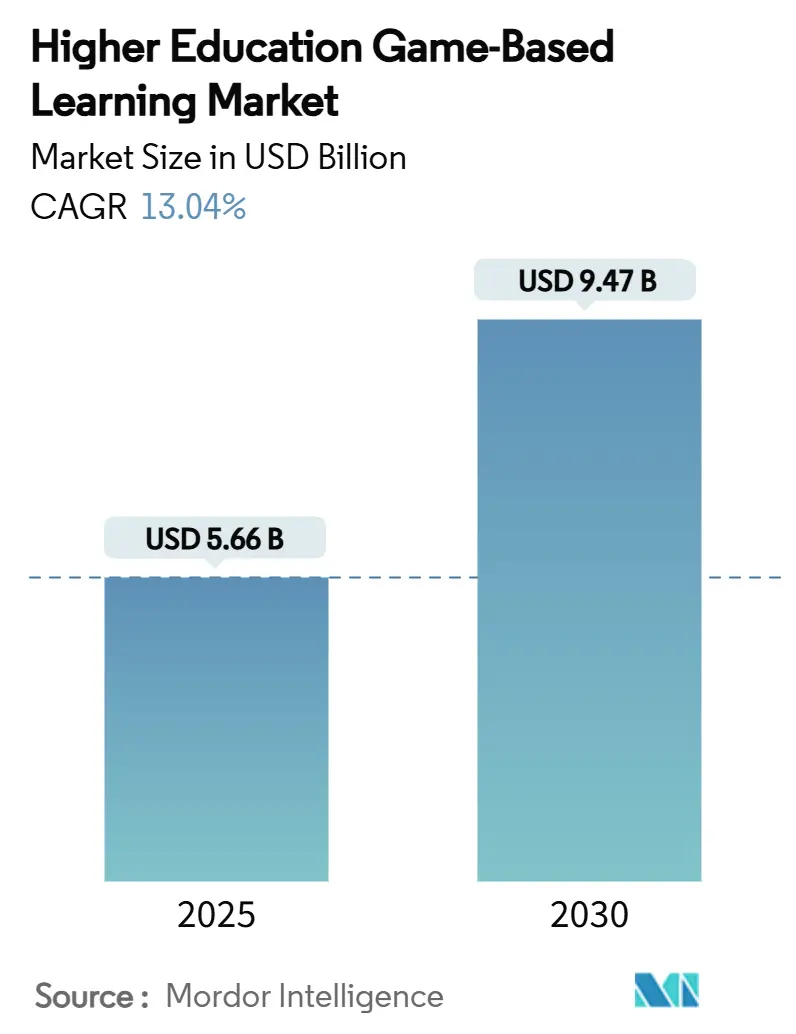

| Market Size (2025) | USD 5.66 Billion |

| Market Size (2030) | USD 9.47 Billion |

| Growth Rate (2025 - 2030) | 13.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Higher Education Game-Based Learning Market Analysis by Mordor Intelligence

The higher education game-based learning market size reached USD 5.66 billion in 2025 and is forecast to reach USD 9.47 billion in 2030, translating into a robust 13.04% CAGR across the outlook period. This momentum reflects universities’ decisive move toward interactive learning formats that demonstrably raise engagement and completion metrics while supporting competency-based assessment strategies. Post-pandemic modernizations of blended-learning infrastructure, heightened demand for experiential instruction that fuses theory with practice, and the worldwide spread of affordable mobile devices collectively underpin sustained expansion. Institutions are channelling capital toward immersive simulations that replicate laboratory and workplace scenarios, thereby lowering physical-resource costs and mitigating safety risks. The market also benefits from cloud deployment models that enable device-agnostic access, widening participation among commuter and international students, and addressing equity gaps exposed during emergency remote learning. Stakeholders increasingly evaluate investment proposals on pedagogical impact and also on data-driven evidence that interactive formats raise retention and employment outcomes, making the higher education game-based learning market a strategic priority for boards of trustees and finance committees.

Key Report Takeaways

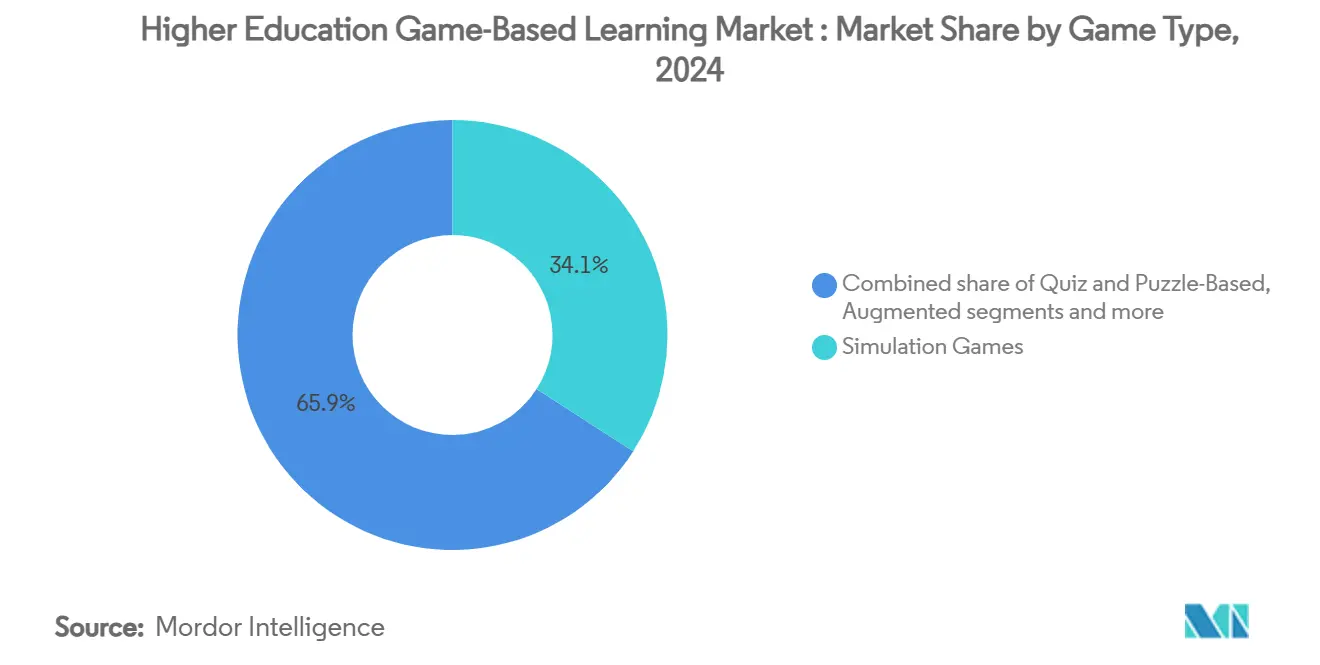

- By game type, simulation titles held 34.1% of the higher education game-based learning market share in 2024. Augmented & virtual reality games are projected to record a 14.12% CAGR through 2030, the fastest among all game types.

- By platform, web-based solutions captured 62.3% of the higher education game-based learning market size in 2024, while cloud gaming is expanding at a 13.83% CAGR to 2030.

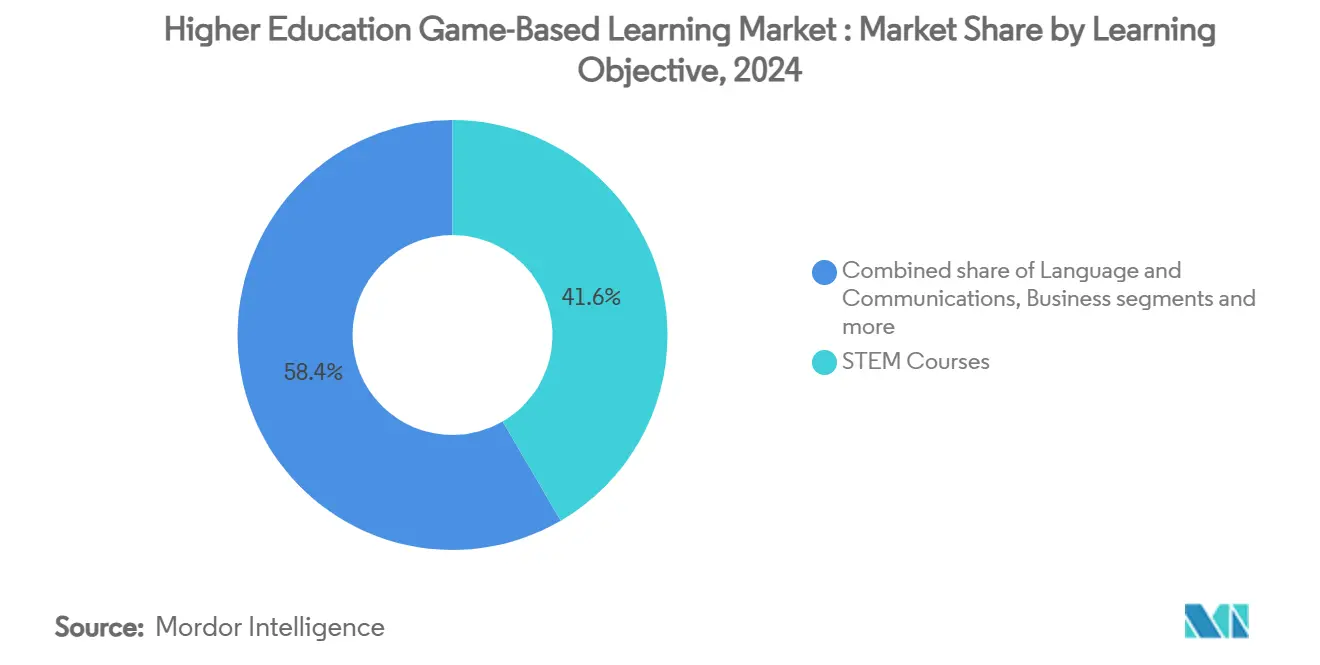

- By learning objective, STEM courses commanded 41.6% of the 2024 revenue of the higher education game-based learning market, whereas business & management applications are advancing at a 14.64% CAGR through 2030.

- By end user, public universities contributed 33.6% of the 2024 value of the higher education game-based learning market; MOOCs & online-only institutions demonstrate the top CAGR at 13.73% through 2030.

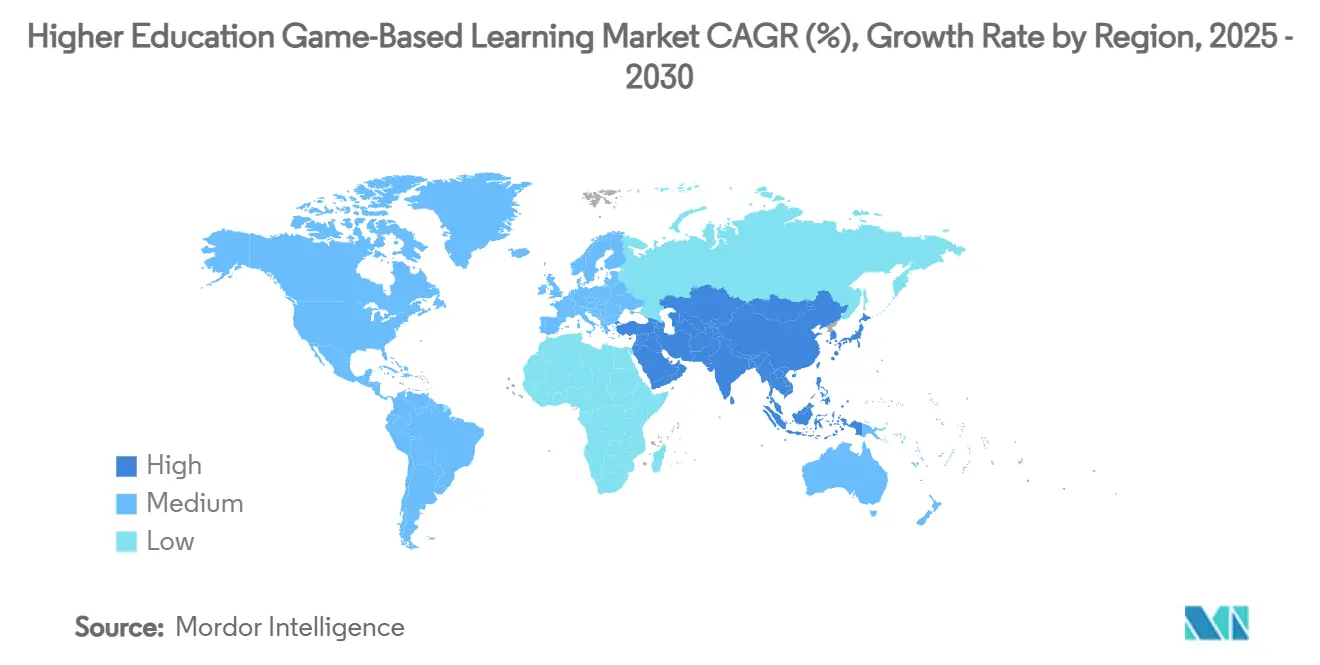

- By geography, North America led with 34.1% revenue share of the higher education game-based learning market in 2024, yet Asia-Pacific is tracking a 15.12% CAGR over the projection horizon.

Global Higher Education Game-Based Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for interactive & immersive learning experiences | +2.8% | Global, early uptake in North America & EU | Medium term (2-4 years) |

| Increasing penetration of mobile devices & high-speed internet | +2.1% | Core growth in APAC, spill-over to MEA | Short term (≤ 2 years) |

| Growing adoption of blended & remote learning post-COVID-19 | +1.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Low-code / no-code authoring tools for faculty-created content | +1.4% | North America & EU, expanding in APAC | Medium term (2-4 years) |

| Blockchain-based credentialing & tokenized rewards | +0.8% | Pilot projects worldwide | Long term (≥ 4 years) |

| University–e-sports partnerships for credit courses | +0.6% | North America, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for interactive & immersive learning experiences

Universities are redesigning curricula as digital natives expect coursework that mirrors their high-tech daily environment. Arizona State University’s required VR biology sequence improved lab grades and retained more STEM majors among 4,000 students between 2022 and 2024[1]INSIDE HIGHER ED, “ASU’s Required Virtual Reality Lab Boosted Grades, Retention,” insidehighered.com . Commercial titles repurposed for credit, such as Age of Empires IV at the University of Arizona, prove entertainment IP can deliver rigorous historical analysis when paired with structured assessment. Dedicated educational hardware reinforces the trend; zSpace’s headset-free workstations already serve more than 3,700 campuses and simplify hygiene and accessibility compliance. Collectively, these deployments signal that immersive experiences have evolved from discretionary pilots into mainstream instructional assets across the higher education game-based learning market.

Increasing penetration of mobile devices & high-speed internet

Ubiquitous smartphones and affordable data plans have erased the access barrier to sophisticated learning games, especially in Asia-Pacific, where 5G subscriptions exceeded 1.4 billion in 2025. Universities now stream processor-intensive simulations from the cloud, relieving campus labs of hardware upgrades and letting commuter students participate on personal devices. VMware’s device-agnostic workspace shows how institutions can cap costs while maintaining security controls and single-sign-on convenience for learners. Mass-scale language platform Duolingo demonstrates the model’s reach, topping ~90 million monthly active users with mobile-first game design that personalizes lessons across 40 languages[2]DUOLINGO, “Interim Corporate Responsibility & Impact Factsheet 2024,” duolingo.com. Adaptive algorithms now tailor challenge levels in real time, elevating completion rates and proving that mobile ubiquity not only drives adoption but also supports data-driven pedagogy.

Growing adoption of blended & remote learning post-COVID-19

Hybrid delivery is now a permanent fixture and game-based modules occupy the engagement gap left by synchronous video lectures. Community colleges lead equity-focused innovation through laptop-lending and subsidized-bandwidth programs that embed simulations into gateway courses. The 2025 EDUCAUSE Horizon Report lists game-based learning among essential technologies for maintaining attention in mixed-modality classrooms. LMS plug-ins now auto-sync gameplay data to grade books, easing faculty workload and aligning with accreditation reporting standards. Competency-based frameworks pair naturally with level-progression mechanics, allowing students to demonstrate mastery through interactive milestones rather than sit-down exams. Institutions that integrated games during emergency remote teaching still report higher course-completion and student-satisfaction scores relative to purely video-based sections, validating permanent budget lines for these tools.

Low-code / no-code authoring tools enabling faculty-created content

Intuitive editors are turning instructors into designers, solving the content-gap problem that once slowed the higher education game-based learning market. Agent Sheets, validated by Stanford research, equips educators to code full simulations without prior programming expertise. Universities are building on-campus studios staffed by graduate assistants who iterate games from faculty storyboards, shortening development cycles and lowering license fees. AI-powered generators showcased by LearningverseVR now draft 3-D environments and non-player-character scripts, letting academics focus on learning outcomes rather than asset creation. These capabilities are invaluable for niche subjects such as linguistics field methods or paleoclimatology, where commercial off-the-shelf titles rarely exist. The spread of faculty-authored content supports cultural relevance and multilingual localization, two factors critical to global expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development costs for premium games | -2.3% | Global, acute in budget-constrained institutions | Short term (≤ 2 years) |

| Faculty resistance & limited design skills | -1.8% | Worldwide, cultural variation by region | Medium term (2-4 years) |

| Data-privacy regulations curbing analytics | -1.2% | EU & North America, expanding worldwide | Long term (≥ 4 years) |

| Limited accessibility in VR/AR experiences | -0.9% | Global, stricter enforcement in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High development costs for high-quality educational games

Creating cinematic-grade simulations typically requires multidisciplinary teams, multi-year cycles, and budgets edging into seven figures, straining institutions already juggling deferred-maintenance backlogs and enrolment declines. Cost uncertainty often deters custom projects that address niche curricula, leaving gaps where off-the-shelf titles do not fit. New consortium models pool funds across universities, yet they introduce governance questions around intellectual property and revenue-sharing on commercial spin-offs. Vendor subscription pricing lowers entry barriers but locks institutions into annual renewals that can exceed original build estimates over time. Until open-source engines mature with education-specific templates, high upfront capital will continue to constrain adoption.

Faculty resistance & lack of instructional-design expertise

Surveys of community-college departments reveal instructors cite time scarcity, reward structures favouring research output, and unfamiliarity with game-design theory as primary barriers to adoption. Workshops alone rarely shift entrenched pedagogical habits; sustained coaching and exemplar courses prove more effective but demand budget and leadership commitment. Generational divides magnify scepticism toward game mechanics perceived as frivolous, despite mounting evidence of learning gains. Institutions are responding with faculty-fellow programs that pair instructional designers with subject experts to co-produce pilot modules. Early adopters who publish peer-reviewed outcome data gradually move department cultures toward an evidence-based embrace of the higher education game-based learning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Simulation maturity and immersive acceleration

Simulation titles account for 34.1% of 2024 revenue, underscoring their role as the pedagogical workhorse of the higher education game-based learning market. Labster’s virtual labs, used by more than 6 million tertiary students, deliver fivefold improvements in STEM course retention while eliminating consumables and safety liabilities[3]LABSTER, “Impact | Labster Enhances STEM Outcomes,” labster.com. Familiarity, measurable outcomes, and seamless LMS integration position simulations as the default choice when faculty require proof of efficacy for curriculum committees.

Augmented & virtual reality games, growing at 14.12% CAGR, extend simulations into multi-sensory contexts that traditional labs cannot mirror, such as micro-scale molecular interactions or hazardous engineering scenarios. Quiz- and puzzle-based formats retain niche appeal for low-stakes formative assessment because they offer instant feedback and minimal technology overhead, yet they often feed data into larger adaptive-learning platforms that personalize subsequent simulation difficulty. Emerging genres, including location-based storytelling and esports-linked coursework, signal a future in which entertainment cultural capital becomes a direct driver of academic motivation, widening the experiential palette available to educators across the higher education game-based learning market.

By Platform: Web primacy meets cloud disruption

Browser-based products captured 62.3% of spending in 2024, validating universities’ preference for zero-install solutions that align with device-diverse classrooms and centralized cybersecurity policies. However, cloud gaming’s 13.83% CAGR is reshaping procurement as vendors stream GPU-intensive content, rendering local hardware nearly irrelevant and facilitating equitable access for low-income learners. EON Reality’s 2025 freemium XR hub exemplifies this shift by decoupling immersive quality from end-user device specifications.

Mobile apps remain critical for micro-learning, yet screen size and battery limits constrain their use for complex labs, positioning them more as analytics dashboards and revision tools than primary delivery channels. Stand-alone PC/console deployments persist in media-arts and aerospace programs where high-fidelity rendering and joystick controllers are pedagogically integral, but even these labs now link to cloud servers for after-hours remote practice. Hybrid architectures will likely dominate as institutions stitch together web, mobile, and cloud pathways to produce frictionless learner journeys within the higher education game-based learning market.

By Learning Objective: STEM cornerstone and business breakout

In 2024, STEM courses accounted for 41.6% of total revenue, underscoring the inherent link between interactive visualization and scientific experimentation in the higher education game-based learning market. This quantitative alignment facilitates detailed assessment rubrics, positioning simulations as a preferred accreditation tool for faculties in engineering and health sciences. Meanwhile, titles in business and management are surging, boasting a 14.64% CAGR, as MBA students engage in crisis management and strategic planning through scenarios like GoVenture’s entrepreneurship sandbox.

Language and communication studies leverage gamified repetition loops for enhanced learning. Notably, Duolingo's AI-led foray into math and music underscores the versatility of its engagement model. Humanities and social sciences are increasingly adopting commercial games, such as Age of Empires IV, to deepen students' understanding of historical causality and cultural nuances. Furthermore, a diverse range of cross-disciplinary segments spanning from environmental ethics adventures to public-policy debate games underscore the market's shift towards holistic curricular integration.

By End User: Public scale and digital-native momentum

In 2024, public universities contributed 33.6% of the market value by leveraging their extensive enrollments and research mandates to drive innovation while complying with state accessibility requirements, supported by centralized instructional-design centers that distribute development costs across numerous course sections each term. MOOCs and online-only institutions demonstrated the highest growth rate at 13.73% CAGR, utilizing gamification strategies to address historically low completion rates and differentiate their credential offerings in an increasingly competitive online education market.

Private universities focused on deploying premium XR experiences as a strategic branding tool to attract international fee-paying students, while community colleges advanced through collaborative consortia that shared licenses and faculty training to optimize limited budgets. Blockchain-verified micro-credentials, issued upon game-based mastery, gained traction across all institution types by providing secure, employer-recognized validation of competencies, aligning with the long-term growth potential of the higher education game-based learning market. These developments underscore the diverse strategies employed by institutions to adapt to evolving market demands and enhance their value propositions. The integration of innovative technologies and collaborative frameworks continues to shape the competitive landscape of the higher education sector.

Geography Analysis

North America generated 34.1% of 2024 revenue, supported by mature EdTech ecosystems and generous technology budgets that fund large-scale simulation rollouts, including state-wide community-college initiatives. U.S. universities such as Arizona State and the University of Arizona provide case-study validation that sustains federal grant interest, while Canada’s tri-council research funding encourages experimental game-based projects in nursing and engineering. Mexico’s national digital-literacy agenda has catalysed cross-border vendor partnerships, though currency fluctuations modulate purchasing cycles.

Asia-Pacific is the growth engine with a 15.12% forecast CAGR as China, India, and ASEAN members pour capital into smart-campus infrastructure to expand tertiary enrolment and meet employability targets. UNESCO’s blended-learning framework guides policy directives that explicitly reference game-based learning as a tool for equitable access and quality assurance. Government grants in India now subsidize VR labs at technical institutes, while China’s “Internet + Education” policy accelerates domestic game studios’ pivot to academic markets.

Europe maintains steady adoption underpinned by Erasmus-funded collaboration networks that co-develop multilingual content, although GDPR heightens scrutiny over in-game analytics. The European Blockchain Partnership’s diploma-verification pilots underscore the region’s leadership in secure credentialing that complements experiential learning. German and French universities lead deployment of accessibility-compliant VR, leveraging EU research grants to retrofit headsets and controllers for visually impaired learners. The Middle East & Africa remains nascent yet promising, with the UAE vision documents allocating smart-campus budgets and South African universities exploring low-bandwidth mobile simulations to bridge infrastructure gaps.

Competitive Landscape

The higher education game-based learning market shows moderate fragmentation, as the top five vendors account for less than half of the combined revenue, leaving room for nimble specialists. Consolidation is on the rise: In 2024, Goldman Sachs and Lego Group's EUR 1.5 billion acquisition of Kahoot! Underscores institutional investors' belief in its long-term value. Pearson's partnerships with Microsoft and Google are not just alliances; they're integrating Gemini and Azure AI to scale personalized content and adding blockchain-verified badges. This move signals Pearson's intent to merge traditional curricula with cutting-edge technology to stay competitive.

Start-ups are carving out niches with VR focused on accessibility, low-code content creation, and tokenized reward systems, often collaborating with LMS providers through white-label agreements. While entry barriers are minimal for quiz platforms with light content, they escalate for those requiring photorealistic simulations and AAA-grade art pipelines. To address these challenges, many companies are co-developing with mainstream game engines like Unity to deliver high-quality solutions. This trend highlights the growing demand for advanced tools and partnerships in the market.

In this evolving landscape, firms that meld pedagogical research, adaptive analytics, and credentialing attributes are gaining an edge. These capabilities resonate with procurement committees that prioritize measurable ROI, positioning such firms as leaders in the market. The ability to combine innovative technology with proven educational methodologies is becoming a key driver of competitive advantage. As the market matures, companies that align with these priorities are likely to secure long-term growth opportunities.

Higher Education Game-Based Learning Industry Leaders

Kahoot!

Labster

Coursera

Pearson

Classcraft Studios

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pearson and Google launched a multiyear partnership to build AI-powered instructional tools on Google Cloud’s Vertex AI, embedding Gemini models into higher-education courseware.

- June 2025: EON Reality unveiled a global freemium XR platform, expanding beyond institutional contracts to individual learners.

- May 2025: Echo360 acquired GoReact to integrate real-time video feedback within skill-based simulations.

- January 2025: Duolingo released an AI video-call feature enabling realistic conversation practice with virtual characters.

Global Higher Education Game-Based Learning Market Report Scope

| Simulations Games |

| Quiz & Puzzle-Based Games |

| Augmented & Virtual Reality Games |

| Others |

| Web-based |

| Mobile Apps |

| Stand-alone PC/Console |

| Cloud Gaming |

| STEM Courses |

| Language & Communications |

| Business & Management |

| Humanities & Social Sciences |

| Others |

| Public Universities |

| Private Universities & Colleges |

| Community Colleges |

| MOOCs & Online-only Institutions |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (SG, MY, TH, ID, VN, PH) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Game Type (Value) | Simulations Games | |

| Quiz & Puzzle-Based Games | ||

| Augmented & Virtual Reality Games | ||

| Others | ||

| By Platform (Value) | Web-based | |

| Mobile Apps | ||

| Stand-alone PC/Console | ||

| Cloud Gaming | ||

| By Learning Objective (Value) | STEM Courses | |

| Language & Communications | ||

| Business & Management | ||

| Humanities & Social Sciences | ||

| Others | ||

| By End-user (Value) | Public Universities | |

| Private Universities & Colleges | ||

| Community Colleges | ||

| MOOCs & Online-only Institutions | ||

| By Geography (Value) | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (SG, MY, TH, ID, VN, PH) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How fast is revenue growing in the higher education game-based learning market?

Global value is projected to rise from USD 5.66 billion in 2025 to USD 9.47 billion in 2030, reflecting a 13.04% CAGR.

Which game type currently generates the most spending?

Simulation titles lead with 34.1% of 2024 revenue, driven by their proven effectiveness in STEM and health-science programs.

Why are Asia-Pacific universities adopting game-based learning so aggressively?

Government digitization mandates and surging enrollment make immersive platforms a cost-effective way to scale quality instruction, pushing regional CAGR to 15.12% through 2030.

What limits adoption at resource-constrained colleges?

High development costs for AAA-grade content and limited faculty training budgets remain primary inhibitors, reducing CAGR potential by an estimated 2.3 percentage points.

How does blockchain integrate with educational gaming?

Institutions pilot tokenized reward systems and verifiable micro-credentials that record in-game skill mastery on decentralized ledgers, streamlining employer verification and reducing fraud.

Page last updated on: