E-learning Packaged Content Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

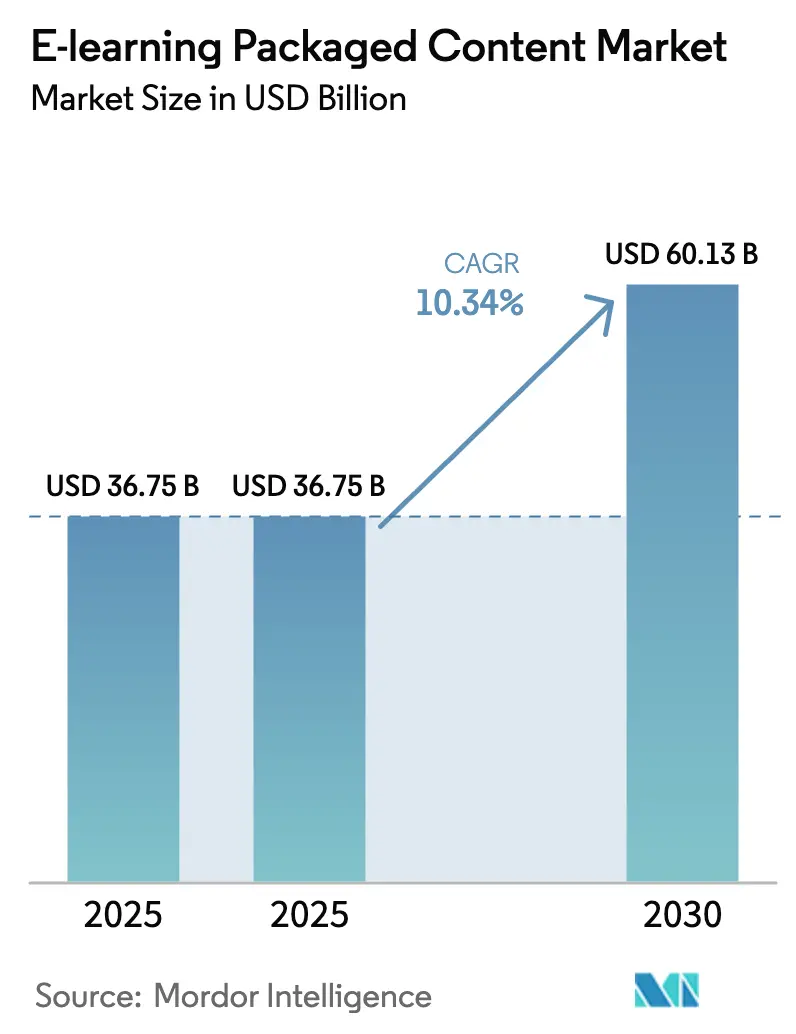

| Market Size (2025) | USD 36.75 Billion |

| Market Size (2030) | USD 60.13 Billion |

| Growth Rate (2025 - 2030) | 10.34% CAGR |

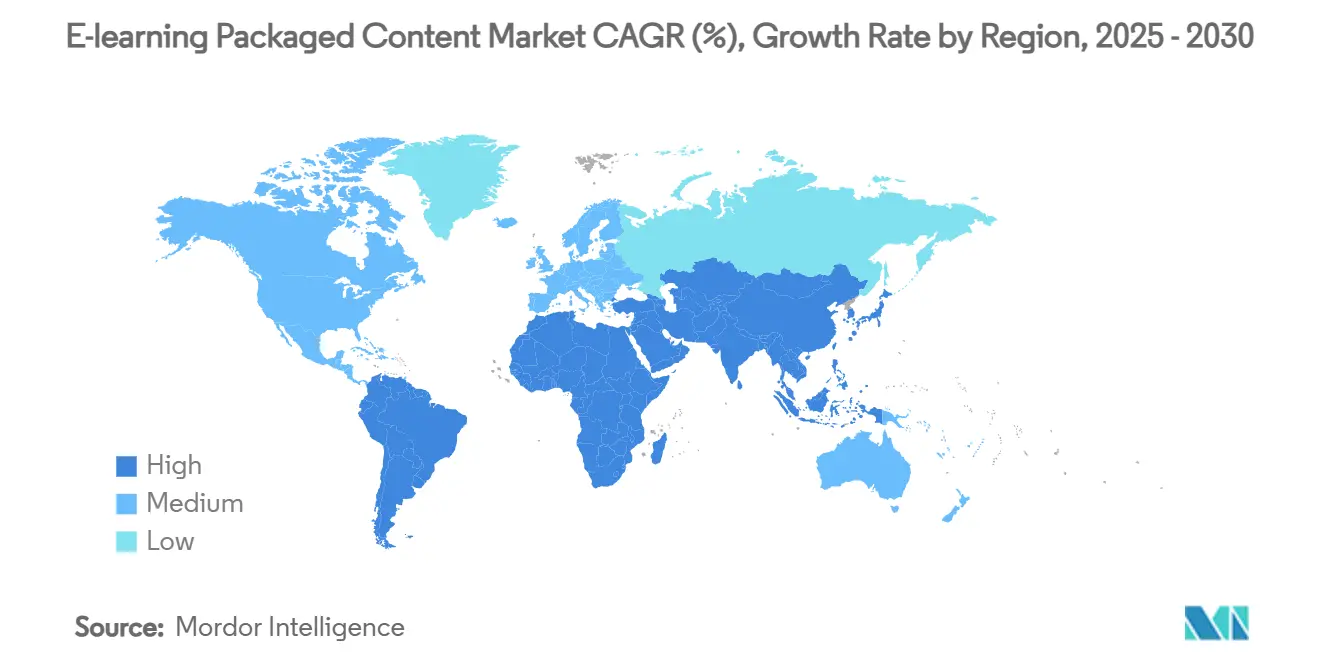

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

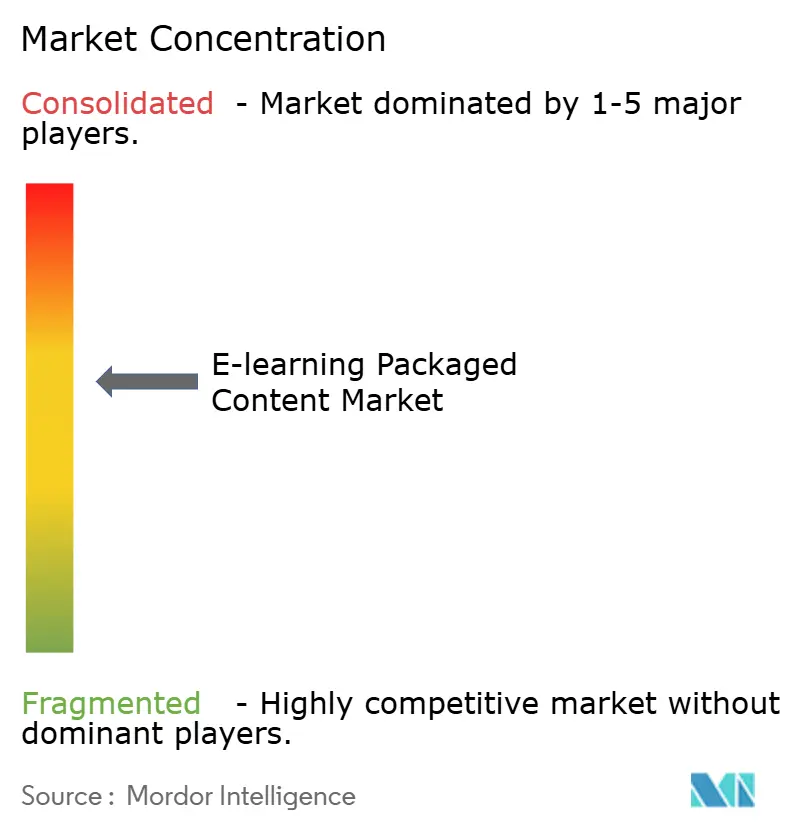

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-learning Packaged Content Market Analysis by Mordor Intelligence

The E-learning Packaged Content Market size was valued at USD 36.75 billion in 2025 and is estimated to grow from USD 36.75 billion in 2025 to reach USD 60.13 billion by 2030, at a CAGR of 10.34% during the forecast period (2025-2030).

Growth accelerates as enterprises tie reskilling budgets to digital-transformation targets, governments direct stimulus toward online learning ecosystems, and AI engines personalise modules at scale. Corporate compliance drives repeat purchases of certified libraries, while mobile-first microlearning helps distributed teams finish courses rapidly. Content portfolios shift from passive videos to immersive Simulation/VR assets as 5G roll-outs solve bandwidth limits[1]GSMA, “Cloud AR/VR Streaming,” gsma.com . Vendors bundle analytics with libraries, turning learner data into measurable ROI, even as piracy and GPU scarcity temper momentum.

Key Report Takeaways

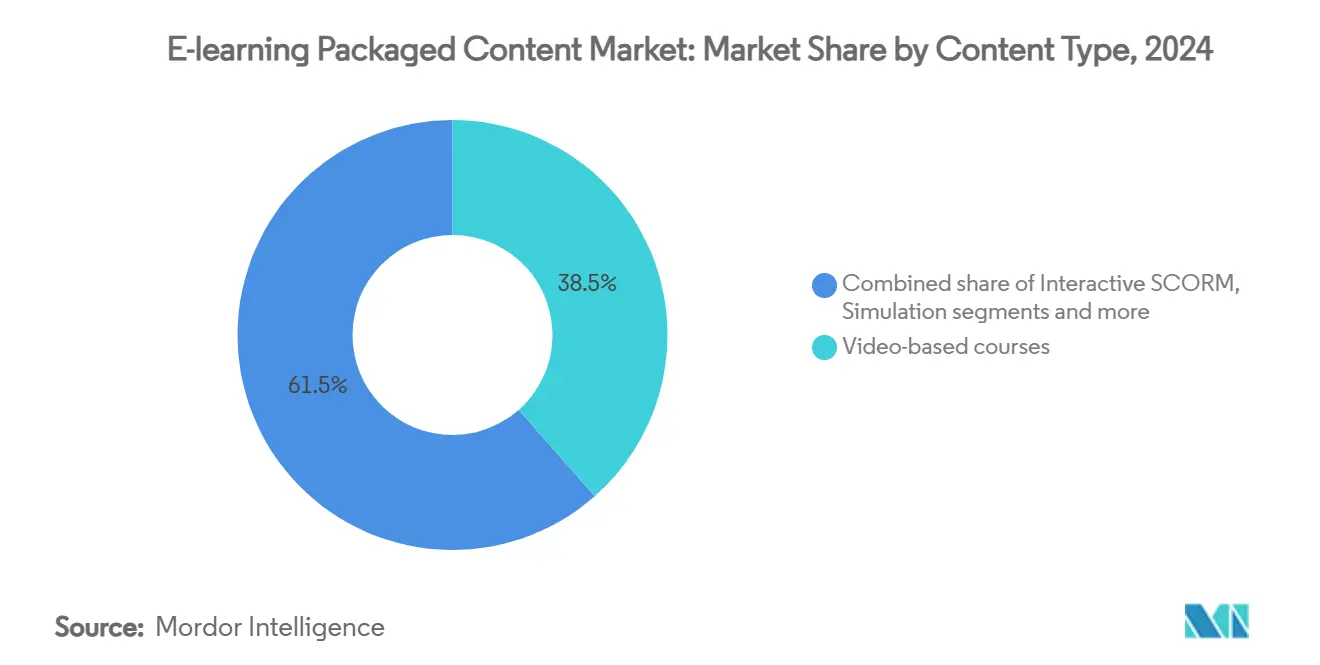

- By content type, video-based courses led with 38.5% revenue share of the E-learning packaged content market in 2024; simulation/VR & AR assets are projected to expand at a 14.2% CAGR through 2030.

- By learning model, self-paced formats held 60.6% of the E-learning packaged content market share in 2024, while instructor-led packaged kits are set to grow at 10.7% CAGR to 2030.

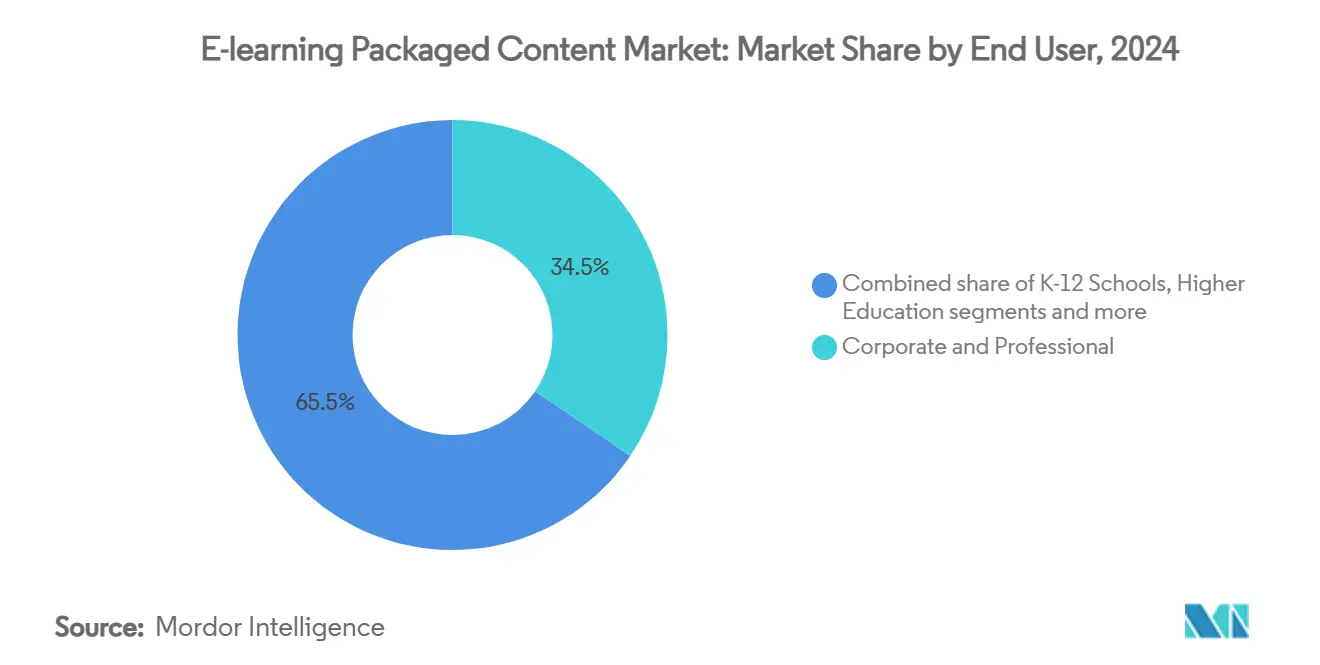

- By end user, the corporate & professional segment commanded 34.5% of the E-learning packaged content market size in 2024; vocational & skill-training institutes record the highest projected CAGR at 13.8% through 2030.

- By geography, North America captured 32.8% revenue share in 2024, whereas Asia-Pacific is advancing at 12.6% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-learning Packaged Content Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of mobile-first microlearning | +2.1% | Global with Asia-Pacific leadership | Medium term (2-4 years) |

| Corporate reskilling & compliance mandates | +2.8% | North America and Europe | Short term (≤ 2 years) |

| Government digital-education stimulus | +1.9% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Data-driven personalised learning engines | +1.7% | Global, enterprise focused | Long term (≥ 4 years) |

| API-ready LMS–LXP connector bundles | +1.2% | North America and Europe | Short term (≤ 2 years) |

| AI-generated multilingual localisation | +1.5% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Mobile-first Microlearning

Mobile-optimized micro-modules deliver two- to three-minute lessons that slot naturally into work breaks, raising completion rates compared with desktop courses. Field technicians, retail associates, and healthcare staff adopt smartphone learning because it requires no fixed location. Enterprises that deploy microlearning report 30% faster certification cycles for new hires and lower support-desk tickets due to intuitive interfaces. Expanding 5G coverage removes latency for HD video and interactive quizzes, allowing richer content without buffering. Asia-Pacific leads adoption because smartphone penetration outpaces desktop use, making mobile the primary gateway to the E-learning packaged content market.

Corporate Reskilling & Compliance Mandates

Automation and generative AI reshape job roles each budget cycle. Large employers reserve multiyear reskilling funds and license curated libraries to reach global workforces quickly[2]World Economic Forum, “Reskilling the Workforce,” weforum.org. Regulated industries such as banking and life sciences purchase off-the-shelf compliance modules that meet audit requirements and provide immutable completion logs. Integration with HRIS platforms lets managers link certifications to career pathways, reinforcing continuous learning cultures. Vendors with deep regulatory catalogs, therefore, secure sticky renewals within the E-learning packaged content market.

Government Digital-Education Stimulus

Public spending injects fresh capital into school districts, vocational institutes, and municipal training centres that lack in-house content studios. The USD 122 billion American Rescue Plan earmarked funds for high-quality digital resources to counter pandemic learning loss[3]U.S. Department of Education, “American Rescue Plan ESSER,” ed.gov. Similar schemes in India, China, and Southeast Asia pay for multilingual libraries that comply with accessibility rules, giving pre-approved vendors multi-year revenue visibility. Procurement guidelines often emphasise inclusive design, prompting suppliers to add captions, screen-reader tags, and low-bandwidth options. These requirements raise barriers to entry and elevate established players in the E-learning packaged content market.

Data-driven Personalised Learning Engines

AI recommendation engines analyse quiz scores, clickstream data, and time-on-task to adjust lesson sequence and difficulty. Predictive analytics flags disengaged users, prompting nudges that lift overall completion rates by double digits. Competency dashboards feed succession plans and identify company-wide skill gaps, letting HR allocate training spend more precisely. Personalisation also trims seat-time waste by delivering only material aligned to learner needs, reducing opportunity cost for billable employees. Vendors that fuse large catalogs with granular analytics command premium licences across the E-learning packaged content industry.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High content-obsolescence velocity | -1.8% | Global, tech-focused subjects | Short term (≤ 2 years) |

| Intellectual-property piracy & spoof sites | -1.1% | Global, heightened in emerging markets | Medium term (2-4 years) |

| EU Data-Act API-licence conflicts | -0.9% | Europe with global spillover | Medium term (2-4 years) |

| GPU-cloud scarcity for 3-D/VR objects | -1.3% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Content-Obsolescence Velocity

As software versions evolve and new coding frameworks emerge, digital-skills curricula struggle to keep pace. A study by The Evolllution reveals that 40% of online content becomes outdated or unreachable within ten years, highlighting the rapid obsolescence of digital learning materials. Consequently, providers find themselves dedicating limited instructional-design hours to upkeep rather than groundbreaking innovation, leading to heightened costs and resource constraints. While modular micro-units offer some relief by breaking content into smaller, more manageable segments, the need for regular updates continues to challenge budgets in the E-learning packaged content market. In response, buyers are opting for shorter contract durations, compelling vendors to demonstrate their speed of updates and ability to maintain content relevance prior to any renewal. This shift underscores the growing demand for agility and adaptability in the E-learning industry.

Intellectual-Property Piracy & Spoof Sites

Piracy rings are undermining legitimate revenue by distributing premium courses through torrents and imitation portals. These spoof sites issue counterfeit certificates and manage to deceive casual HR checks, thereby diminishing the market value of authentic credentials. This widespread piracy impacts the revenue streams of vendors and erodes trust in the certification process, making it harder for genuine learners to showcase their skills effectively. While vendors are countering these threats with watermarking and blockchain credentials, the enforcement of these measures is straining their legal budgets and operational resources. This issue is particularly pronounced in price-sensitive markets where copyright enforcement is lax, creating a significant barrier for smaller studios to compete. Consequently, the E-learning packaged content market is witnessing a decline in content diversity, which could hinder innovation and limit the availability of niche or specialized learning materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Video Dominance Faces Interactive Disruption

Video courses secured the largest contribution to the E-learning packaged content market size with a 38.5% share in 2024. Although videos remain popular for onboarding and compliance, enterprises increasingly favour Simulation/VR assets, which are projected to grow at 14.2% CAGR through 2030. Interactive SCORM/xAPI modules integrate seamlessly with corporate LMS environments, supporting granular tracking. Text and slide-based microcourses retain relevance where bandwidth or accessibility constraints persist, ensuring inclusivity across diverse workforce profiles. Growing 5G coverage and cloud AR/VR streaming reduce hardware barriers, making immersive training affordable for mid-sized firms.

Demand for experiential learning underscores a shift from passive consumption toward active competency development. Simulation content lets workers practise dangerous or costly scenarios safely, improving skill transfer. Organisations in aviation, energy, and healthcare now allocate larger budgets to immersive modules than to traditional video. Vendors that blend video intros with interactive layers create adaptive pathways suited to various learner styles. Competitive differentiation, therefore, hinges on the depth, realism, and update frequency of interactive assets within the E-learning packaged content market.

By Learning Model: Self-paced Preference Drives Flexibility Demand

Self-directed modules accounted for 60.6% of the E-learning packaged content market share in 2024, reflecting employees' desire for flexible study windows. Asynchronous access aligns with hybrid work schedules and minimises conflict with billable hours. Instructor-led kits, although smaller, will grow 10.7% annually to 2030 as enterprises balance self-learning with human coaching for complex leadership or safety topics. Virtual facilitation features such as breakout rooms and real-time polling enhance engagement, boosting knowledge retention.

Hybrid programmes blend self-paced learning with live workshops, enhancing understanding while optimizing costs without compromising quality. These programs allow learners to build foundational knowledge at their own pace while benefiting from interactive, real-time sessions that reinforce and expand their skills. Integrated platforms track progress across both modes, offering managers a holistic view of skill development and enabling data-driven decision-making. With increasing regulation and talent mobility, blended strategies have emerged as the gold standard for addressing diverse learning needs. Providers adept at harmonizing both formats stand poised to tap into larger client budgets within the E-learning packaged content sector, as they cater to the growing demand for flexible and comprehensive learning solutions.

By End User: Corporate Leadership Meets Vocational Acceleration

In 2024, enterprises accounted for 34.5% of total revenue, spurred by compliance mandates and an ongoing need for upskilling. This growth highlights the increasing importance of aligning workforce capabilities with evolving regulatory requirements and technological advancements. As Industry 4.0 technologies take hold on factory floors, vocational and skill-training institutes are projected to see a robust growth rate of 13.8% CAGR through 2030. These institutes are playing a critical role in equipping workers with the skills needed to operate and maintain automated systems. Meanwhile, in emerging economies, government stimulus is channeling funds into digitised curricula, covering trades from welding and robotics maintenance to renewable-energy installation. Such initiatives aim to bridge skill gaps and support economic development. Both K-12 and higher-education sectors are witnessing steady growth, increasingly adopting packaged content to enhance traditional teaching methods and improve learning outcomes.

Corporate buyers are now emphasising the integration of talent-management suites, ensuring that certifications align with role progression. This trend underscores the growing need for seamless systems that connect employee development with organizational goals. On the other hand, vocational institutes are pushing for competency-based modules, customised to resonate with local industry clusters, presenting a lucrative avenue for specialised publishers. These tailored solutions enable institutes to address specific workforce demands effectively. Furthermore, non-profit and public-sector agencies are investing in libraries that standardise training, ensuring consistency across expansive social programmes. This approach supports large-scale initiatives aimed at workforce development and social upliftment. The merging of enterprise and vocational demands is expanding the total addressable market for E-learning packaged content, creating opportunities for innovation and growth across the industry.

Geography Analysis

In 2024, North America secured 32.8% of the market revenue, bolstered by substantial corporate budgets and stringent regulatory frameworks mandating ongoing training. Federal initiatives, like the American Rescue Plan, fuel demand for content that aligns with procurement standards, ensuring compliance and quality. Canada promotes bilingual resources for vital skills training, addressing the needs of its diverse workforce and enhancing accessibility. Meanwhile, Mexico standardises content throughout its maquiladora supply chains, fostering consistency and efficiency in cross-border operations.

Asia-Pacific will post the fastest regional growth at 12.6% CAGR through 2030, propelled by smartphone-centric consumption patterns and government digital-literacy drives. India’s National Digital Education Architecture and China’s enterprise reskilling subsidies expand platform onboarding rates. Southeast Asian economies adopt microlearning to upskill youthful populations quickly, bypassing desktop-heavy infrastructure. High mobile penetration and rising disposable income solidify the region as a pivotal growth engine for the E-learning packaged content market.

Europe maintains stable expansion aided by the Pact for Skills, which cultivates public-private alliances to close sectoral gaps. Stringent data-privacy rules push vendors toward open APIs and privacy-preserving analytics. Latin America and the Middle East & Africa exhibit uneven growth. Oil-exporting Gulf states invest in VR safety-training centres, whereas connectivity shortfalls in parts of sub-Saharan Africa limit adoption to low-bandwidth microcourses. Nevertheless, improving infrastructure and favourable policy signals present future opportunities across these regions.

Competitive Landscape

The E-learning packaged content market is moderately concentrated, with key players leveraging advanced technologies to maintain their competitive edge. Skillsoft's Percipio platform, supported by AI-guided libraries, serves slightly more than half of the Fortune 1000 companies, showcasing its strong market presence. Microsoft integrates LinkedIn Learning content directly into Teams, utilizing Azure analytics to deliver personalized learning paths. Udemy Business reported a Q1 2025 revenue of USD 200.3 million, positioning AI-powered reskilling as a core differentiator in its offerings. Pearson continues to expand its virtual-school franchise, incorporating AI-enhanced English programs to cater to evolving educational needs.

Competitive dynamics in the market are increasingly driven by vertical integration. Vendors are combining authoring tools, delivery platforms, and assessment analytics to secure enterprise clients and strengthen their value propositions. Niche specialists are targeting specific sectors such as advanced manufacturing, cybersecurity, and sustainable engineering, where in-depth domain expertise outweighs the need for high-volume content. Additionally, AI-native entrants are disrupting the market by auto-generating microcourses from real-time data, challenging established players with their speed and cost efficiency. These developments highlight the growing importance of innovation and adaptability in the E-learning packaged content market.

Strategic collaborations and mergers, and acquisitions (M&A) are further shaping the competitive landscape. Partnerships between VR headset manufacturers and content studios are emerging to create turnkey simulation solutions, addressing the demand for immersive learning experiences. Meanwhile, M&A activity remains robust as incumbents seek to expand their language offerings and geographic reach to defend and grow their market share. These strategic moves underscore the dynamic nature of the E-learning packaged content market, as players continuously adapt to meet the demands of a rapidly evolving industry.

E-learning Packaged Content Industry Leaders

Skillsoft

LinkedIn Learning (Microsoft)

Udemy Business

Pluralsight

Coursera Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Udemy posted USD 200.3 million revenue for Q1 2025 and highlighted AI-driven reskilling as a strategic focus.

- March 2025: The United Kingdom earmarked GBP 45 million to boost school connectivity and establish digital standards by 2030.

- February 2025: Microsoft reported training more than 14 million learners through AI-based programmes in its 2024 annual report.

- January 2025: Tennessee launched a USD 17 million Digital Skills and Workforce Development grants programme to improve statewide digital literacy.

Global E-learning Packaged Content Market Report Scope

| Video-based courses |

| Interactive SCORM/xAPI modules |

| Text & slide-based microcourses |

| Simulation / VR & AR assets |

| Self-paced packaged content |

| Instructor-led packaged kits |

| K-12 Schools |

| Higher Education |

| Corporate & Professional |

| Government & Non-profit |

| Vocational / Skill-training institutes |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Content Type | Video-based courses | |

| Interactive SCORM/xAPI modules | ||

| Text & slide-based microcourses | ||

| Simulation / VR & AR assets | ||

| By Learning Model | Self-paced packaged content | |

| Instructor-led packaged kits | ||

| By End User | K-12 Schools | |

| Higher Education | ||

| Corporate & Professional | ||

| Government & Non-profit | ||

| Vocational / Skill-training institutes | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large will the E-learning packaged content market be in 2030?

It is projected to reach USD 60.13 billion by 2030.

Which region shows the highest future growth for packaged digital learning?

Asia-Pacific is forecast to record a 12.6% CAGR through 2030.

Why do enterprises favour self-paced modules?

They align with flexible work patterns and currently hold 60.6% market share.

What content format is gaining the fastest?

Simulation/VR & AR assets, advancing at a 14.2% CAGR.

How concentrated is vendor competition?

The top five firms control slightly over half of revenue, indicating moderate concentration.

Page last updated on: