Gamified Cybersecurity Learning Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

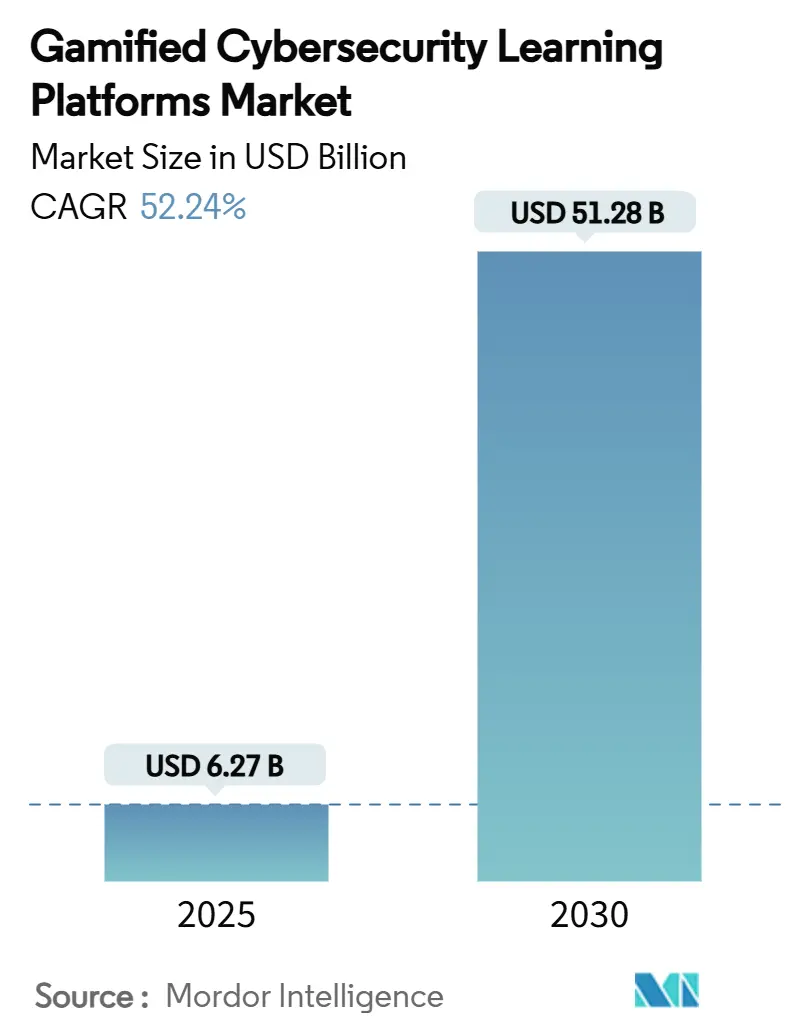

| Market Size (2025) | USD 6.27 Billion |

| Market Size (2030) | USD 51.28 Billion |

| Growth Rate (2025 - 2030) | 52.24% CAGR |

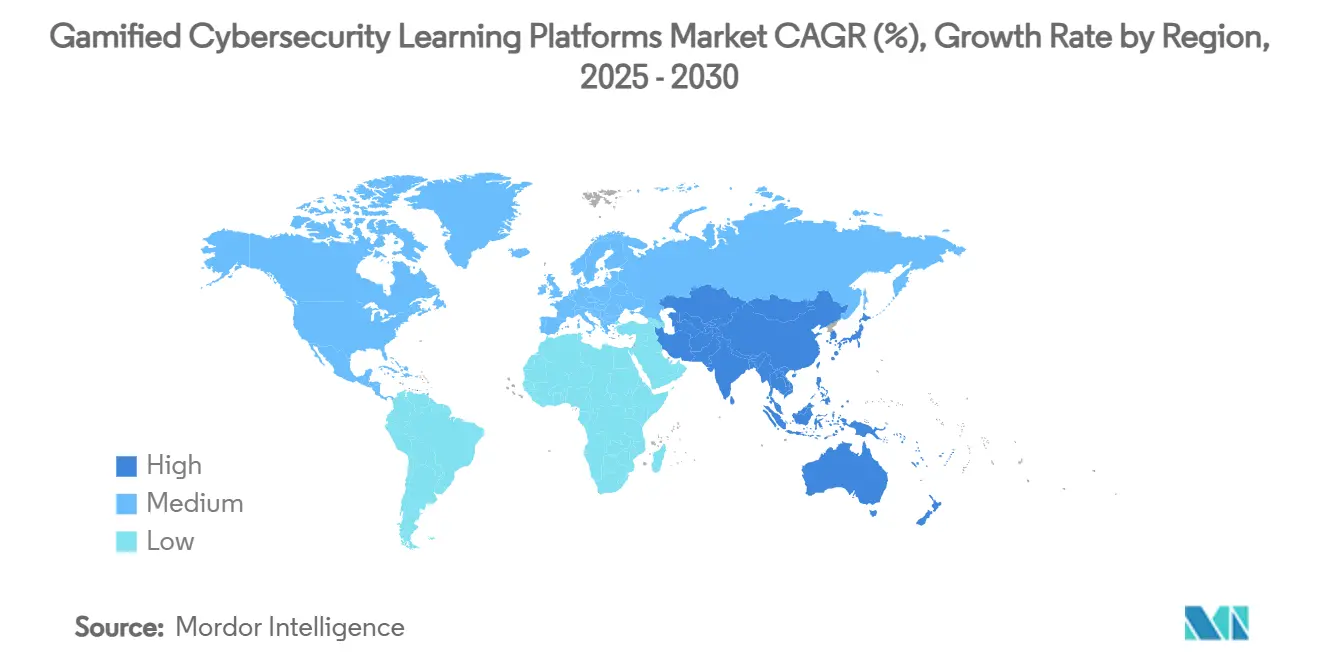

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gamified Cybersecurity Learning Platforms Market Analysis by Mordor Intelligence

The gamified cybersecurity learning platforms market size stands at USD 6.27 billion in 2025 and is projected to reach USD 51.28 billion by 2030, advancing at a 52.24% CAGR. Cloud deployment dominance, surging phishing sophistication, and tightening global regulations form a powerful growth triad that keeps budgets flowing into advanced training solutions. Enterprises continue to swap legacy slide-based programs for immersive simulations because knowledge retention rises while incident-response times fall.[1]U.S. Government Accountability Office, “Immersive Technologies: Most Civilian Agencies Are Using or Plan to Use Augmented Reality, Virtual Reality, and More,” gao.govVendors answer this demand by fusing artificial intelligence with game mechanics to adjust difficulty in real time, personalise content, and measure behaviour change more precisely. Growing remote workforces widen attack surfaces and push organisations toward scalable, always-on training that fits distributed teams. Competitive intensity remains moderate as new entrants exploit white spaces in vertical-specific content and multilingual localisation capabilities.

Key Report Takeaways

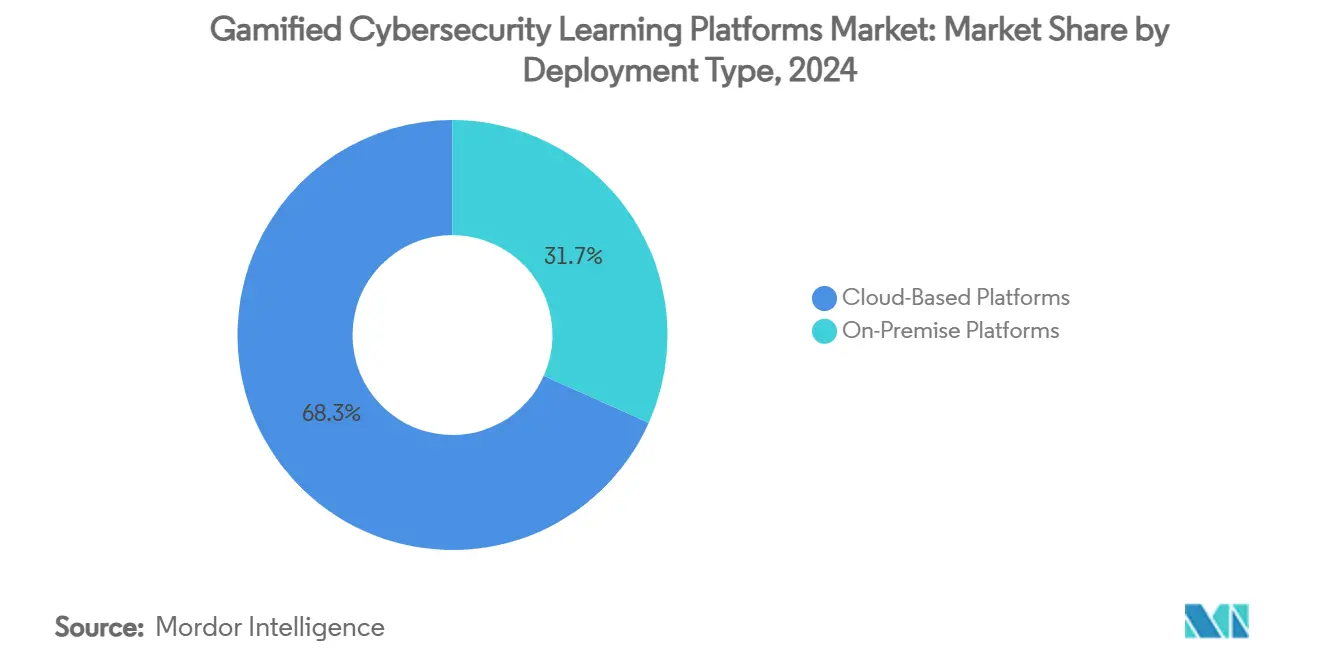

- By deployment type, cloud platforms led with 68.3% revenue share in 2024; the same segment is forecast to expand at a 59.3% CAGR to 2030.

- By learning modality, phishing-simulation suites captured 30.2% of the gamified cybersecurity learning platforms market share in 2024, while VR/AR immersive training advances at a 68.3% CAGR through 2030.

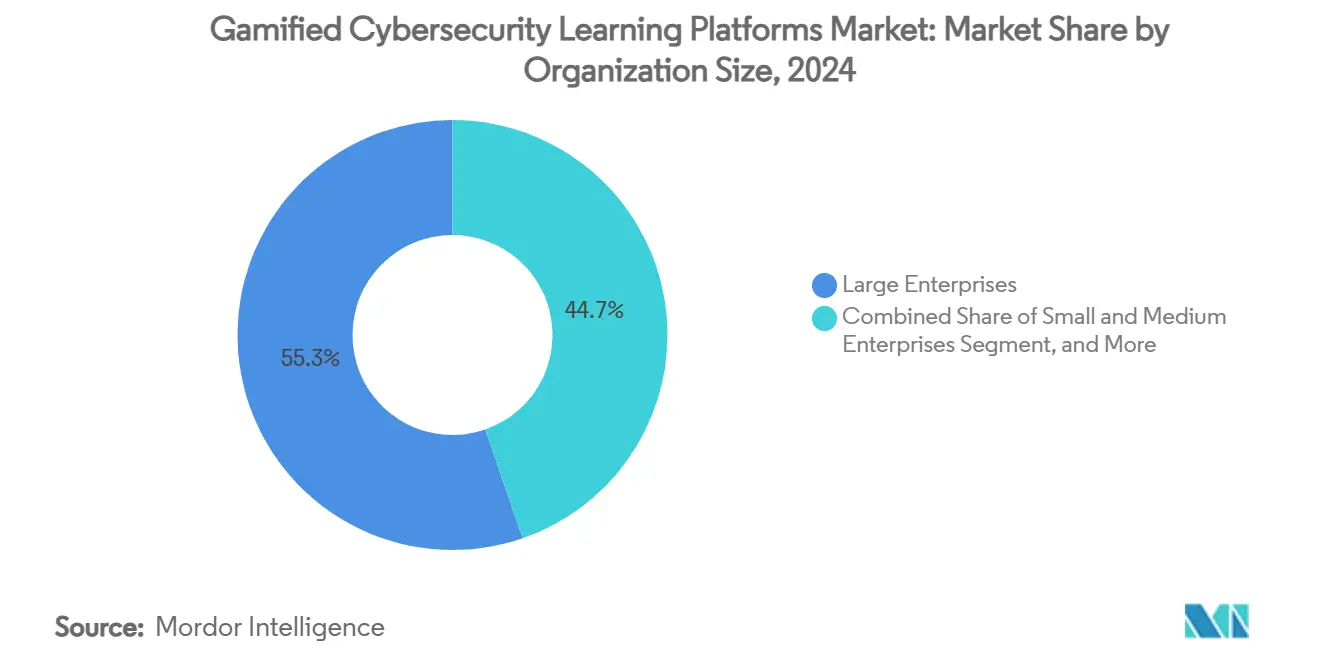

- By organisation size, large enterprises held a 55.3% share of the gamified cybersecurity learning platforms market size in 2024, and SMEs are growing at a 66.3% CAGR to 2030.

- By end-user industry, BFSI commanded a 25.1% share of the gamified cybersecurity learning platforms market size in 2024, and healthcare is progressing at a 58.3% CAGR through 2030.

- By geography, North America accounted for a 38.2% share of the gamified cybersecurity learning platforms market size in 2024, whereas Asia-Pacific records a 57.3% CAGR to 2030.

Global Gamified Cybersecurity Learning Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in sophisticated phishing and social-engineering attacks | +12.8% | Global | Short term (≤ 2 years) |

| Regulatory mandates elevating security-awareness budgets | +11.2% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Proven ROI of gamification on incident-response speed | +9.6% | Global, with early adoption in North America | Medium term (2-4 years) |

| Expansion of remote/hybrid workforces | +8.4% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| AI-driven adaptive-difficulty engines boost engagement | +7.3% | North America and the EU spill over to the Asia-Pacific | Long term (≥ 4 years) |

| Cyber-range adoption in cyber-insurance underwriting | +3.1% | North America and the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sophisticated Phishing and Social-Engineering Attacks

Generative AI tools enable attackers to craft highly personalised lures that evade spam filters and fool well-trained employees. Recorded incidents rose 4,151% between 2024 and 2025, with one Indian bank losing customer data after an email thread hijack that mirrored internal language patterns. Deepfake voice calls reinforce written deception and increase success rates. Because 95% of data breaches still stem from human error, organisations pivot to gamified simulations that mirror live attack chains, provide instant feedback, and recalibrate difficulty when users master tasks.[2]Eliot Baker, “Phishing Trends Report (Updated for 2025),” Hoxhunt, hoxhunt.com These adaptive cycles help sustain vigilance even after the novelty wears off.

Regulatory Mandates Elevating Security-Awareness Budgets

The Digital Operational Resilience Act, in force from January 2025, obliges every European financial employee to complete certified security training, thereby ring-fencing funding despite budget scrutiny. Similar clauses appear across 19 global frameworks, from ISO 27001 to HIPAA updates that now prescribe regular vulnerability drills. Cyber-insurance carriers increasingly require documented training records before issuing or renewing coverage, turning voluntary programmes into de facto obligations. In Asia-Pacific, Malaysia’s new Cyber Security Act sets a target of 25,000 trained professionals by 2025, signalling sustained public investment.

Proven ROI of Gamification on Incident-Response Speed

Organizations that embed game mechanics report 40% cost returns versus lecture-based formats and cut phishing incidents by 86%. A Ponemon study shows firms saving USD 70,000 a year after adopting immersive labs that shrink detection-to-containment windows. Verizon’s VR rollout to 22,000 associates boosted learner confidence to 97%. Strong retention stems from intrinsic motivation, real-time scoring, and peer leaderboards that make repetitive drills enjoyable rather than burdensome.

Expansion of Remote / Hybrid Workforces

Hybrid models extend attack surfaces into private homes, cafés, and co-working hubs that lack enterprise-grade protection. Employees juggle personal devices, unsecured Wi-Fi, and unfamiliar collaboration apps, raising breach odds. Gamified micro-learning modules delivered through mobile devices keep security front-of-mind without interrupting workflow. Employers also value language toggles and culturally aligned scenarios that accommodate globally scattered staff. As more companies embrace asynchronous schedules, demand rises for cloud platforms that orchestrate training across time zones and sync progress into existing HR dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints within SMBs | -8.7% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| High content-localization costs for multi-language roll-outs | -6.2% | Global, concentrated in multinational enterprises | Medium term (2-4 years) |

| Gamification fatigue after a 12-month usage window | -4.8% | Global | Medium term (2-4 years) |

| Privacy scrutiny on SaaS telemetry and analytics | -3.3% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Within SMBs

Resource-strapped firms view security training as an expense rather than an investment, despite 66% suffering breaches in 2024. Only 17% of these businesses trust their current skill levels, yet licence fees, custom content, and staff downtime create adoption hurdles.[3]Miranda Fraraccio, “How SMBs Can Tackle Cybersecurity Challenges,” U.S. Chamber of Commerce, uschamber.com Cloud subscription models partly alleviate up-front costs, but ongoing updates still strain thin margins. Vendors courting this segment respond with tiered pricing, pre-built scenario bundles, and automated reporting that reduces administrative effort. Government grants and insurer discounts also help close the affordability gap.

High Content-Localization Costs for Multi-Language Roll-Outs

Global enterprises must adapt narratives, visuals, and compliance references for dozens of regions, driving content budgets up to three times higher than single-language versions. Data residency laws often require separate hosting environments, further inflating operational spend. Maintaining currency with evolving threats and local regulations compounds the burden. Platforms that offer modular templates, AI translation hygiene checks, and centralised version control gain favour because they cut iteration cycles while preserving cultural relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates

Cloud platforms represented 68.3% of 2024 revenue as enterprises embraced on-demand scalability and avoided hardware upkeep. The gamified cybersecurity learning platforms market size tied to cloud delivery is forecast to compound at 59.3% through 2030. Factors include seamless integration with identity providers, automatic content updates, and elastic capacity during peak campaigns. On-premises solutions persist in defence and critical infrastructure where data sovereignty rules prohibit external hosting, yet their share erodes as vendors secure additional compliance certifications for public clouds. Federal agencies in the United States already train 10,000 staff via cloud-hosted immersive ranges, a signal that perceived security barriers continue to fall.

Second-generation offerings bundle analytics dashboards that benchmark user risk scores against industry peers. Administrators can spin up phishing drills for thousands of employees in minutes, reducing deployment cycles from weeks to hours. Subscription pricing shifts expenditure from capital to operating budgets, aligning with CFO preferences and feeding sustained uptake among midsize firms. Emerging vendors now provide private-cloud instances that blend control and convenience, further blurring the line between traditional hosting models.

By Learning Modality: VR/AR Disrupts Traditional Training

Phishing-simulation suites retained a 30.2% lead in 2024 thanks to low entry costs and simple email integration. Yet VR/AR sessions deliver a 275% uplift in preparedness, prompting a 68.3% CAGR that will reshape the modality mix. Immersive headsets replicate high-pressure breach scenarios, letting users practice forensic analysis and incident containment without risking live systems. Cyber-range exercises go deeper, linking red-team attacks with blue-team responses to teach collaborative defence. For budget-sensitive buyers, interactive video and mobile micro-learning supply bite-sized lessons that still leverage branching logic and real-time scoring.

Many organisations layer modalities instead of choosing one. Employees might start with email phishing drills, graduate to virtual reality breach rooms, then cement habits through monthly quizzes on smartphones. Such blended pathways align with adult learning principles, recycling concepts across different contexts to cement long-term memory. Vendors increasingly package these tracks inside one licence, simplifying procurement.

By Organization Size: SMEs Drive Growth Despite Challenges

Large enterprises contributed 55.3% of 2024 spend, but SMEs posted the strongest 66.3% CAGR because targeted ransomware attacks highlight their vulnerability. Flexible cloud subscriptions let smaller firms adopt best-practice curricula that once required in-house laboratories. Government incentives and cyber-insurance premium discounts add momentum. The gamified cybersecurity learning platforms market share held by SMEs is likely to rise as vendors roll out onboarding wizards, pre-configured policy templates, and managed-service wrappers that offset limited internal expertise.

In parallel, multinational corporations scale programmes across tens of thousands of staff, demanding granular analytics and localisation. That requirement spurs platform providers to refine multi-tenant architectures, boosting overall R&D that later benefits the SME segment through feature trickle-down. The mutual reinforcement between ends of the size spectrum accelerates innovation tempo across the ecosystem.

By End-User Industry: Healthcare Accelerates Compliance-Driven Adoption

BFSI kept a 25.1% revenue lead in 2024 because client trust and capital adequacy rules enforce zero tolerance for breach risk. However, healthcare’s 58.3% CAGR signals the next spending wave as electronic medical records proliferate and ransomware gangs target hospitals. The gamified cybersecurity learning platforms market size devoted to clinical settings grows rapidly because HIPAA revisions now stipulate regular social-engineering drills. IT and telecommunications firms remain fast adopters owing to cultural familiarity with agile tech rollouts, whereas energy companies explore cyber-range simulations to secure operational technology.

Retailers, manufacturers, and educational institutions also raise investment after supply-chain and point-of-sale attacks revealed training blind spots. Vendors respond by tailoring content: factory floor scenarios stress physical-digital convergence safeguards, while campus modules address student device hygiene. The breadth of vertical demand supports a healthy pipeline of niche providers alongside platform majors.

Geography Analysis

North America held 38.2% of 2024 revenue, sustained by robust corporate budgets, an active threat environment, and early acceptance of gamification. Federal directives such as FISMA and sector regulations like SOX compel ongoing awareness programmes, underpinning stable spending. Case studies from telecom giants and federal agencies showcase measurable ROI, encouraging late adopters to follow suit. Venture capital infusions into training startups further reinforce regional leadership by funding rapid feature expansion.

Asia-Pacific records the steepest 57.3% CAGR to 2030. Public-private initiatives, including Japan’s International Cybersecurity Challenge and ASEAN-Japan training collaborations, cultivate local talent pools and spark procurement.[4]Hiroshi Kotani, “Southeast Asia Boosts Cybersecurity Training with Bangkok Center,” Nikkei Asia, asia.nikkei.com Governments strive to shield fast-digitising economies from escalating ransomware campaigns, so they subsidise upskilling programmes and promote standards alignment. Multinational corporations relocating supply chains into the region also import stringent security-awareness expectations, widening addressable demand.

Europe shows consistent mid-teen growth as the Digital Operational Resilience Act obliges finance institutions to certify workforce readiness. Strict GDPR provisions make data residency and privacy dashboards mandatory platform checkboxes, shaping vendor roadmaps. Multi-language requirements intensify content localisation needs, favouring providers with scalable template engines. Meanwhile, cyber-insurance penetration rises, magnifying training’s economic case.

Latin America and the Middle East, and Africa trail but register rising interest. Oil-exporting states fund national academies, and South American regulators strengthen breach disclosure laws that elevate board-level attention. Market penetration remains modest owing to budget and infrastructure gaps, yet pilot projects often progress quickly once funding clears, hinting at latent upside.

Competitive Landscape

The market shows moderate fragmentation. KnowBe4, Immersive Labs, and SimSpace collectively hold about one-eighth of global revenue. Scale advantages stem from broad content libraries, SOC 2-compliant clouds, and channel alliances with MSSPs. Private-equity activity underscores commercial appeal; Vista Equity’s USD 24.90-per-share KnowBe4 buyout in 2024 became a bellwether for further consolidation. Post-deal, KnowBe4 acquired Egress to wrap email defence around training modules, signalling a shift toward unified human-risk platforms.

Challenger firms pursue edge niches. Jericho Security raises venture capital for AI-authored micro-scenarios that adapt wording, tone, and threat vector to user seniority. RangeForce delivers modular cyber-ranges that insurers use to score client resilience, forging a route into underwriting workflows. OffSec, now backed by Leeds Equity, concentrates on advanced offensive curricula that attract penetration testers and red teams. These differentiators keep pricing power intact even as basic phishing-simulation offerings commoditise.

Technology roadmaps converge on adaptive learning engines, machine-vision analytics, and embedded behavioural nudges inside everyday collaboration software. Strategic partnerships with endpoint vendors, email gateways, and SIEM tools grow common, letting platforms ingest live telemetry to tailor drills on the fly. Vendors quickest to deliver demonstrable risk-score reductions and clear audit trails secure renewals and expansion licences.

Gamified Cybersecurity Learning Platforms Industry Leaders

KnowBe4, Inc.

Immersive Labs Ltd.

RangeForce Inc.

Cofense Inc.

Hack The Box Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cycurion formed a diamond-level partnership with NACCHO to secure local health departments via the Cyber Shield managed platform.

- June 2025: INE Security reported USD 16.6 billion in 2024 cybercrime losses, reinforcing demand for threat-detection labs.

- May 2025: INE Security teamed with Abadnet Institute to run Saudi Arabia bootcamps enrolling 200 students in their first cohort.

- May 2025: Commvault and SimSpace unveiled the Commvault Recovery Range to practice full incident lifecycles in immersive labs.

Global Gamified Cybersecurity Learning Platforms Market Report Scope

| Cloud-Based Platforms |

| On-Premise Platforms |

| Cyber-Range Simulations |

| Interactive Video Scenarios |

| VR / AR Immersive Training |

| Mobile Micro-learning Apps |

| Phishing-Simulation Suites |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Government and Defense Agencies |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecommunications |

| Energy and Utilities |

| Education |

| Retail and E-Commerce |

| Manufacturing |

| Government Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Type | Cloud-Based Platforms | ||

| On-Premise Platforms | |||

| By Learning Modality | Cyber-Range Simulations | ||

| Interactive Video Scenarios | |||

| VR / AR Immersive Training | |||

| Mobile Micro-learning Apps | |||

| Phishing-Simulation Suites | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| Government and Defense Agencies | |||

| By End-User Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| IT and Telecommunications | |||

| Energy and Utilities | |||

| Education | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Government Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on gamified cybersecurity platforms growing?

Global revenue is set to climb from USD 6.27 billion in 2025 to USD 51.28 billion by 2030, reflecting a 52.24% CAGR driven by cloud adoption and tougher regulations.

Which deployment model attracts most buyers?

Cloud solutions held 68.3% of 2024 revenue because they scale quickly, cut hardware costs, and ease remote roll-outs.

Why is Asia-Pacific viewed as the growth engine?

Digital transformation, state-funded capacity-building, and expanding tech workforces give Asia-Pacific a 57.3% CAGR, the fastest worldwide.

What evidence proves gamification works?

Organisations report 40% ROI gains and an 86% drop in phishing incidents after shifting from slide decks to interactive simulations.

Which sector is adopting platforms the quickest?

Healthcare shows the fastest 58.3% CAGR as revised HIPAA rules push hospitals to verify staff readiness against ransomware.

How concentrated is vendor competition?

The top three suppliers control roughly 12% of global revenue, signalling moderate concentration and ample room for niche innovators.

Page last updated on: