Global Soft Tissue Repair Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.23 Billion |

| Market Size (2031) | USD 20.33 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

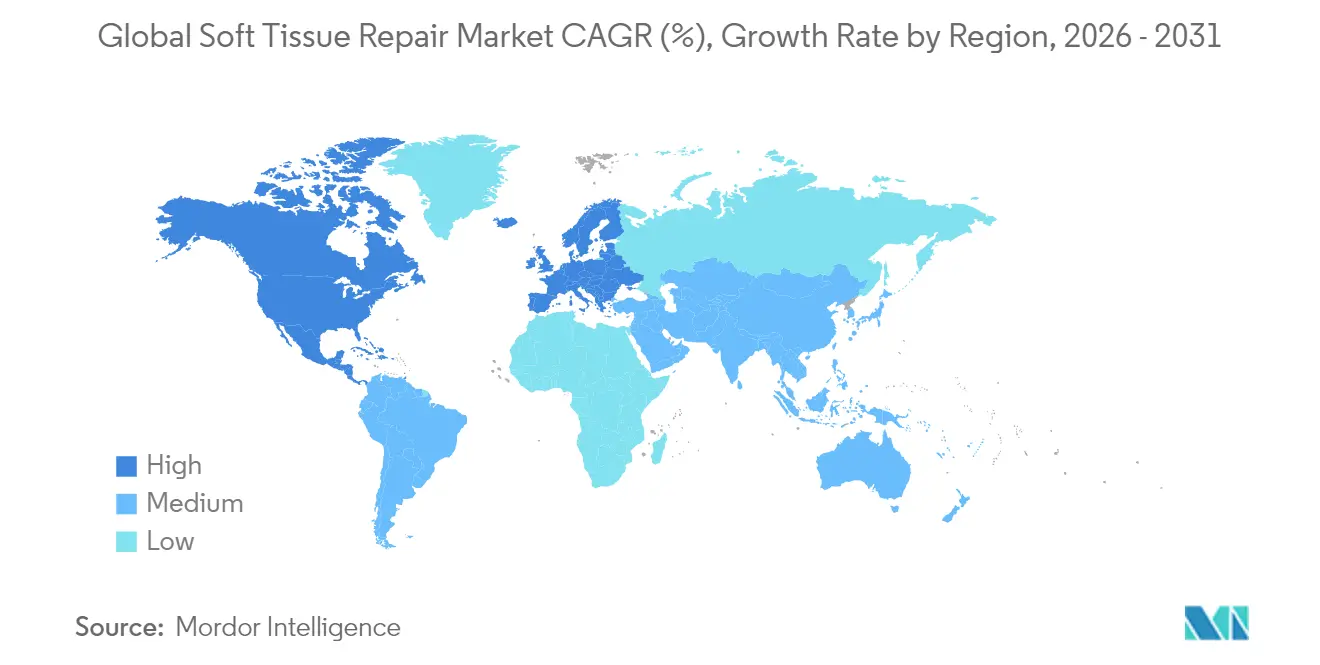

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

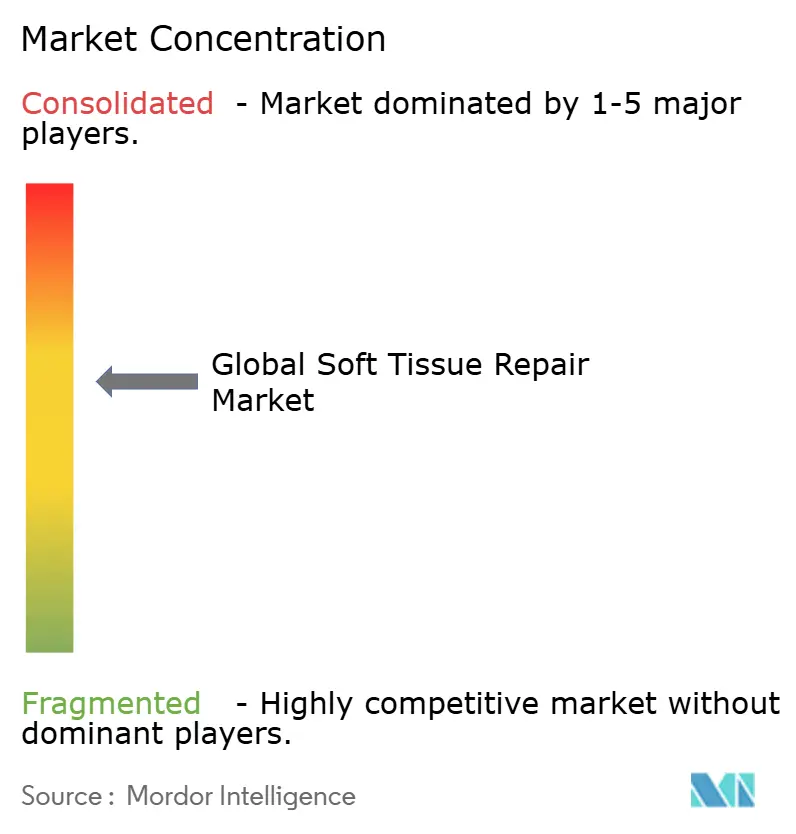

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Soft Tissue Repair Market Analysis by Mordor Intelligence

The global soft tissue repair market size was valued at USD 15.51 billion in 2025 and estimated to grow from USD 16.23 billion in 2026 to reach USD 20.33 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). Demand is underpinned by aging demographics, a steady rise in sports injuries, and the accelerating shift of procedures to ambulatory surgical centers (ASCs). Rapid product innovation—spanning bio-engineered meshes, 3D-printed scaffolds, and suture-less fixation systems—continues to refresh the competitive landscape. Intensifying regulatory scrutiny of legacy synthetic meshes is steering surgeons toward biologic and hybrid alternatives that promise better biocompatibility. At the same time, payer cost-containment policies are amplifying the need for devices optimized for outpatient settings without sacrificing clinical outcomes.

Key Report Takeaways

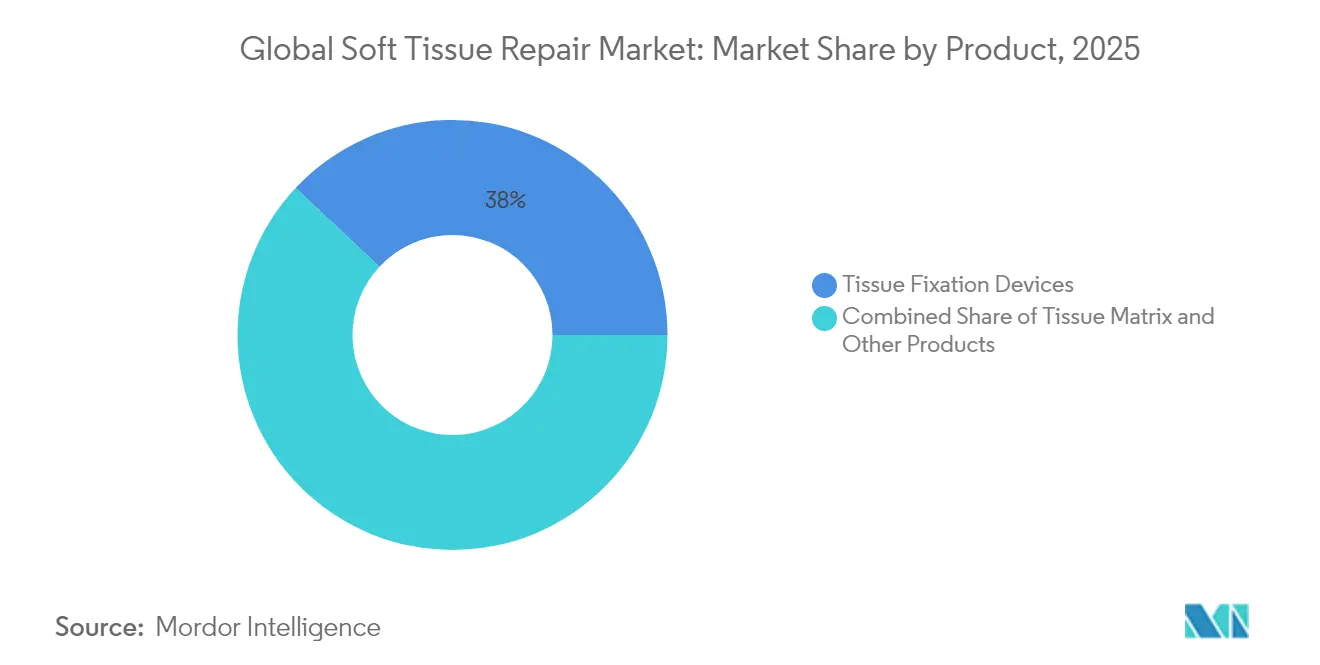

- By product, tissue fixation devices led with a 38.02% revenue share of the soft tissue repair market in 2025; tissue matrices are forecast to expand at a 5.15% CAGR through 2031.

- By application, hernia repair accounted for 28.05% of the soft tissue repair market share in 2025, while orthopedics & sports medicine is projected to grow at 5.55% CAGR between 2026 and 2031.

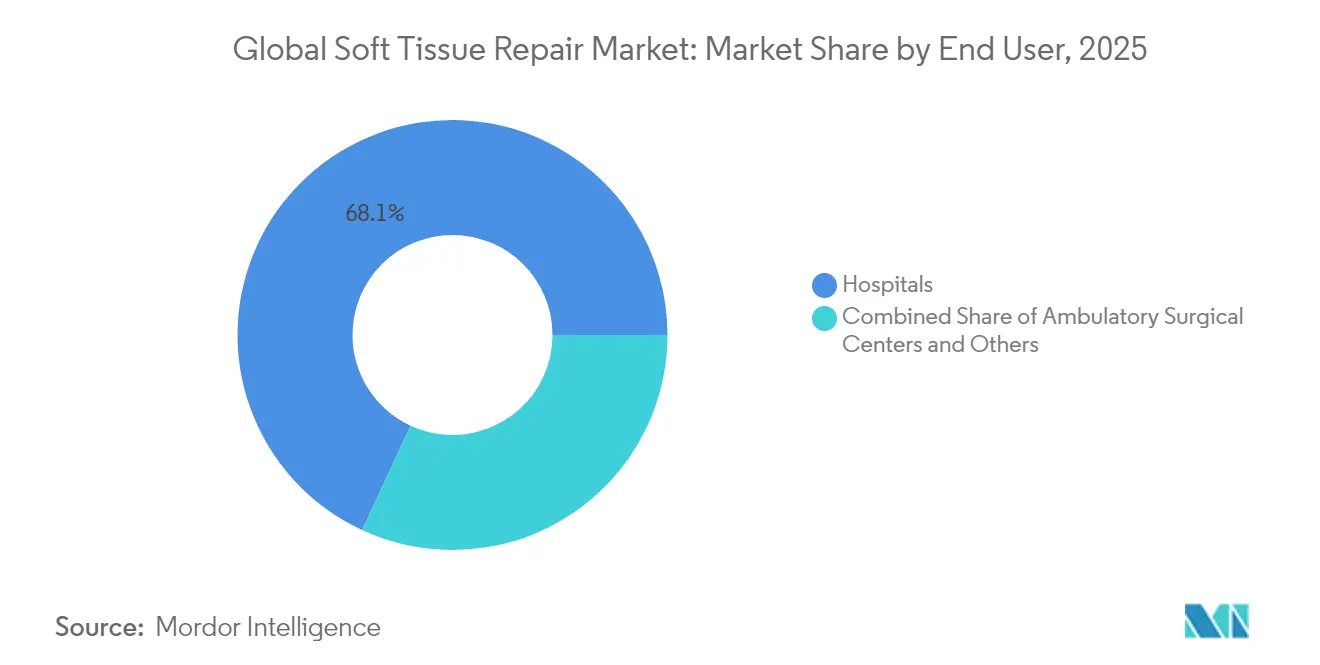

- By end user, hospitals retained 68.10% of the soft tissue repair market in 2025; ASCs are expected to record the fastest growth at 5.65% CAGR over the forecast period.

- By geography, North America commanded 42.55% of the soft tissue repair market in 2025; Asia-Pacific is set to register the highest regional CAGR of 5.90% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soft Tissue Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising sports-related injuries | +0.8% | North America & Europe | Medium term (2-4 years) |

| Increasing trauma & road-accident cases | +0.6% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Growing geriatric population | +1.2% | Global, amplified in developed economies | Long term (≥ 4 years) |

| Technological advances in bio-engineered meshes & fixation devices | +0.9% | North America & Europe; adoption spreading worldwide | Medium term (2-4 years) |

| Outpatient ASC expansion | +1.1% | North America, moving into Europe | Short term (≤ 2 years) |

| 3D-printed patient-specific scaffolds | +0.7% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Sports-Related Injuries

A steady uptick in athletic participation across age groups keeps the soft tissue repair market on a growth trajectory. Incidence of surgically treated hamstring injuries climbed more than threefold in Sweden between 2001 and 2023. Similar trends appear in upper-extremity trauma, where hand injury cases rose 2% annually from 2007 to 2022. Older recreational athletes often present diminished tissue quality, fueling demand for advanced biologic grafts and load-sharing fixation systems that shorten rehabilitation timelines. Device makers able to document quicker functional recovery in this cohort gain a clear competitive edge.

Increasing Trauma & Road-Accident Cases

Road traffic accidents remain a major global health burden, markedly in emerging economies. Complex extremity injuries often involve multiple soft tissue layers, prompting surgeons to favor integrated repair platforms combining fixation, scaffold, and hemostatic functions. Regional disparities in trauma patterns compel manufacturers to tailor training and inventory models to local needs. As governments in Asia and Latin America roll out trauma system upgrades, procedure volumes are expected to lift the soft tissue repair market further.

Growing Geriatric Population

Nearly half of postmenopausal women are projected to suffer musculoskeletal disorders by 2045. Age-linked hernia prevalence is also on the rise, with 6.75 million existing adult cases tallied in 2021. Older patients exhibit slower healing and a higher risk of recurrence, heightening interest in collagen-based and bio-inductive implants that support tissue regeneration. Suppliers with long-term clinical data in geriatric cohorts are poised to capture share.

Technological Advances in Bio-Engineered Meshes & Fixation Devices

Extracellular-matrix (ECM) hydrogel coatings significantly dampen chronic inflammation around polypropylene mesh. Light-activated polymers eliminate sutures in peripheral nerve repair, underscoring a wider push toward less invasive, time-saving techniques. Continuous product improvements help manufacturers meet the dual challenge of ASC cost constraints and hospital performance metrics, strengthening the overall soft tissue repair market.

Outpatient ASC Expansion Driving Procedure Volumes

ASCs performed 72% of all U.S. surgeries in 2024 and are on track for 21% volume growth by 2034 [1]Mukerji S., “High Growth in ASC Volume,” ascfocus.org . Same-day discharge protocols compel device makers to prove shorter setup and operating times. Companies able to bundle implants with disposable instruments tailored for ASCs can grow revenue streams even as per-unit prices face downward pressure.

3D-Printed Patient-Specific Scaffolds

Additive manufacturing now generates anatomically matched patches and conduits that fit complex defects with minimal trimming. Early studies on coral-inspired grafts show full integration within 6-12 months, compared with longer timelines for conventional allografts. As printer access broadens beyond academic hubs, patient-specific constructs are expected to form a meaningful revenue segment within the soft tissue repair market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & device costs | -0.9% | Global, sharper impact in emerging economies | Medium term (2-4 years) |

| Infection litigation & stringent mesh regulations | -1.2% | North America & Europe | Short term (≤ 2 years) |

| Reimbursement pushback on novel biologic meshes | -0.8% | North America & Europe | Medium term (2-4 years) |

| Limited surgeon training in emerging markets | -0.6% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs

Premium biologic matrices can cost multiples of standard polypropylene mesh. U.S. payers now cap the number of applications for certain skin substitutes and demand comparative evidence of superiority [2]Centers for Medicare & Medicaid Services, “Skin Substitute Grafts LCD,” cms.gov. Similar scrutiny by private insurers has tagged many novel grafts as investigational. Without sustained outcome data, adoption in cost-sensitive settings stalls, slowing the pace at which the soft tissue repair market converts to newer materials.

Infection Litigation & Stringent Mesh Regulations

Mesh-related litigation has surpassed USD 1 billion in settlements for a single manufacturer. The FDA’s reclassification of transvaginal mesh to Class III heightened premarket approval requirements, and its ongoing hernia mesh reviews weigh on surgeon confidence. Resulting risk aversion can curb first-time implantations and dampen replacement demand.

Reimbursement Pushback on Novel Biologic Meshes

U.S. carriers increasingly label high-priced dermal matrices as experimental when randomized data are sparse. European agencies exhibit similar caution, urging value-based procurement. These moves compel vendors to embark on lengthier, costlier trials, tempering near-term revenue expansion within the soft tissue repair market.

Limited Surgeon Training in Emerging Markets

In Asia-Pacific and Latin America, deficits in advanced laparoscopic and arthroscopic training slow uptake of next-generation implants. Government efforts to enforce marketing codes and device laws, while enhancing safety, prolong approval timelines. Vendors must invest in proctoring programs and local evidence to unlock growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Fixation Devices Remain Cornerstone, Matrices Accelerate

Fixation devices held a 38.02% share of the soft tissue repair market in 2025, underpinned by surgeon familiarity with suture anchors, interference screws, and medical adhesives. FDA clearance for CONMED’s expanded BioBrace indications in 2025 adds over 50 orthopedic procedures to its label . TELA Bio’s liquid adhesive, launched in 2024, offers a suture-less option for hernia closure. Continuous innovation secures this segment’s revenue stream.

Tissue matrices are forecast to outpace all other categories at a 5.15% CAGR. Collagen-elastin hybrids and ECM-coated polypropylene meshes are demonstrating reduced recurrence and lower inflammatory profiles in pre-clinical models. As payers warm to the long-term cost savings of fewer re-operations, this fast-growing segment is poised to enlarge its slice of the soft tissue repair market size.

By Application: Hernia Repair Dominates, Orthopedics & Sports Medicine Surges

Hernia repair accounted for 28.05% of the soft tissue repair market size in 2025, bolstered by more than 1.2 million annual procedures in the United States alone. Standardized coding keeps reimbursement predictable, sustaining high volumes.

Orthopedics & sports medicine is projected to expand at 5.55% CAGR, the quickest among applications. FDA clearance for the first regenerative meniscus implant in 2024 opened a new therapeutic frontier. Bio-inductive shoulder patches have delivered up to 86% reductions in rotator cuff re-tear rates in multicenter trials. These successes are raising surgeon confidence and funneling R&D investment.

By End User: Hospitals Hold Sway, ASCs Capture Momentum

Hospitals generated 68.10% of 2025 revenue thanks to infrastructure suited for complex, high-acuity cases. However, the pronounced migration to outpatient settings is starting to tilt case mix. Medicare reported 3.4 million ASC procedures for its beneficiaries in 2023, reflecting a 5.7% rise year-on-year. ASCs, benefiting from 45-60% lower costs and shorter wait times, are projected to grow fastest at 5.65% CAGR, making them a critical battleground within the soft tissue repair market.

Geography Analysis

North America commanded 42.55% of the soft tissue repair market in 2025 and is expected to maintain leadership through 2031. A mature ASC network now delivers 72% of U.S. surgeries, enhancing throughput while containing costs. The FDA continues to clear breakthrough devices such as Humacyte’s acellular vessel for trauma repair, reinforcing the region’s innovation ecosystem.

Europe retains solid positioning thanks to universal health systems and CE-mark harmonization. Nevertheless, fiscal pressures are prompting stricter health-technology assessments, which slow reimbursement for premium biologic matrices. Ongoing investments in robotics and additive manufacturing keep local suppliers competitive, sustaining the region’s role in shaping next-generation solutions for the soft tissue repair market.

Asia-Pacific is the fastest-growing region, forecast at 5.90% CAGR. Regulatory modernization in China and India is clarifying approval pathways, while an aging population widens the candidate pool for hernia and rotator cuff procedures. Japan’s adoption of bio-inductive implants underscores the region’s appetite for advanced yet clinically validated technologies.

Competitive Landscape

Market concentration remains moderate. Johnson & Johnson leads with 13% revenue share via Ethicon and DePuy Synthes portfolios, underpinned by sizeable R&D budgets. Stryker fortified its fixation lineup by acquiring Artelon in 2024 and closed a USD 4.9 billion deal for Inari Medical in 2025 to enter the vascular-trauma space.

Smith+Nephew, active across orthopedics and wound care, released 16 new products in 2024 and is leveraging its REGENETEN platform to deepen ties with sports-medicine surgeons.

Innovation pipelines concentrate on three avenues: biologic or hybrid meshes that lower re-operation risk, personalized 3D-printed scaffolds for complex defects, and liquid or light-activated fixation systems that shorten operative time—key for high-turnover ASCs. Companies delivering evidence of faster recovery and lower complication rates are expected to consolidate their positions within the soft tissue repair market.

Global Soft Tissue Repair Industry Leaders

Arthrex, Inc.

Boston Scientific Corporation

Stryker

Medtronic

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Johnson & Johnson MedTech signed an exclusive U.S. distribution pact with Responsive Arthroscopy, expanding its sports-medicine soft-tissue offering.

- June 2024: Axogen introduced Avive+ resorbable soft-tissue matrix for peripheral-nerve protection.

- February 2024: Smith+Nephew unveiled CARTIHEAL AGILI-C cartilage implant alongside REGENETEN at AAOS, strengthening its sports franchise.

Global Soft Tissue Repair Market Report Scope

As per the scope of the report, soft tissue repair procedure refers to a series of processes in which the soft tissues are repaired by regeneration, and reconstruction by using various medical devices. But a soft tissue injury is characterized by damage to muscles, ligaments, or tendons throughout the body. It often occurs during sports and exercise activities, but sometimes simple daily activities can also cause soft tissue injuries. The Soft Tissue Repair Market is Segmented By Product (Tissue Fixation Devices (Suture Anchors, Sutures, Interference Screws, and Other Devices), Tissue Matrix (Synthetic Mesh and Biologic Mesh), Application (Orthopedics, Dental Repair, Hernia Repair, Breast Reconstruction, Skin Repair, Pelvic and Vaginal Prolapse Repair, and Others), and Geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Tissue Fixation Devices | Suture Anchors |

| Sutures & Staples | |

| Interference Screws | |

| Cyanoacrylate & Fibrin Glues | |

| Tissue Matrix | Synthetic Mesh |

| Biologic / Hybrid Mesh | |

| Other Products |

| Orthopedics & Sports Medicine |

| Dental Repair |

| Hernia Repair |

| Breast Reconstruction |

| Skin & Burn Repair |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Tissue Fixation Devices | Suture Anchors |

| Sutures & Staples | ||

| Interference Screws | ||

| Cyanoacrylate & Fibrin Glues | ||

| Tissue Matrix | Synthetic Mesh | |

| Biologic / Hybrid Mesh | ||

| Other Products | ||

| By Application | Orthopedics & Sports Medicine | |

| Dental Repair | ||

| Hernia Repair | ||

| Breast Reconstruction | ||

| Skin & Burn Repair | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Global Soft Tissue Repair Market?

The Global Soft Tissue Repair Market size is expected to reach USD 16.23 billion in 2026 and grow at a CAGR of 4.62% to reach USD 20.33 billion by 2031.

Which product segment is expanding most rapidly?

Tissue matrices, encompassing biologic and hybrid meshes, are projected to grow at a 5.15% CAGR through 2031.

Who are the key players in Global Soft Tissue Repair Market?

Arthrex, Inc., Boston Scientific Corporation, Stryker, Medtronic and Baxter International Inc. are the major companies operating in the Global Soft Tissue Repair Market.

Why are ASCs important for market growth?

ASCs now perform the majority of U.S. surgeries and offer lower costs and faster turnarounds, driving device adoption optimized for outpatient use.

Which region has the biggest share in Global Soft Tissue Repair Market?

In 2025, the North America accounts for the largest market share in Global Soft Tissue Repair Market.

Page last updated on: