Oxygen Therapy Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

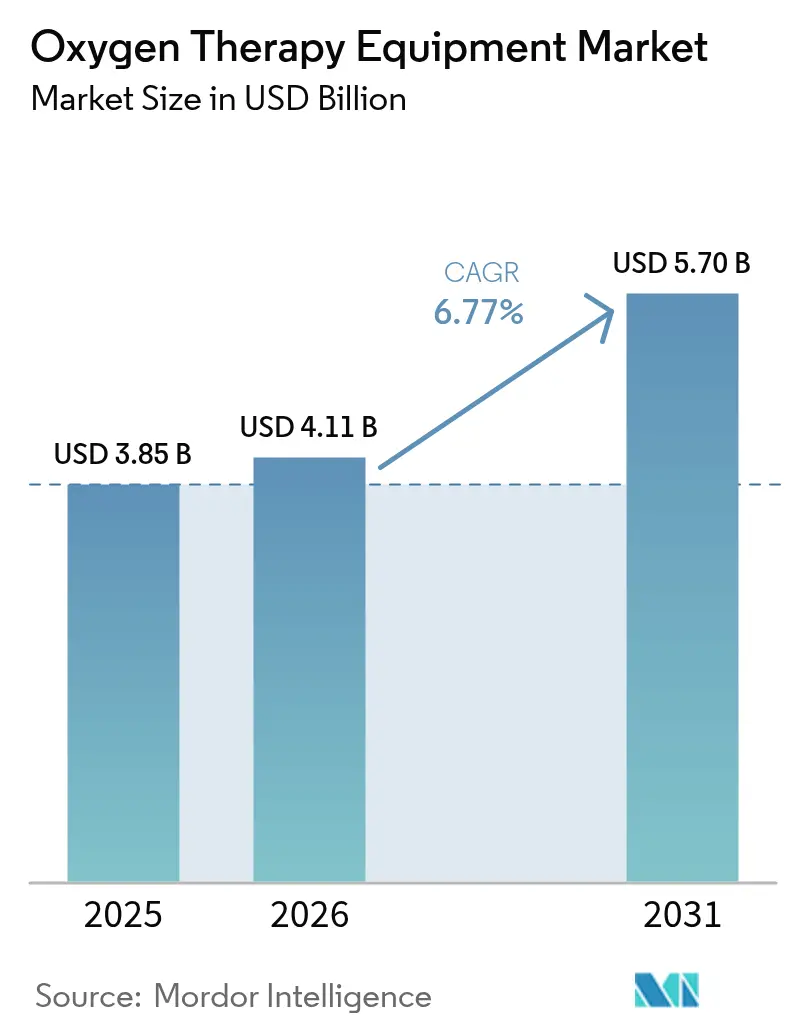

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 5.7 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

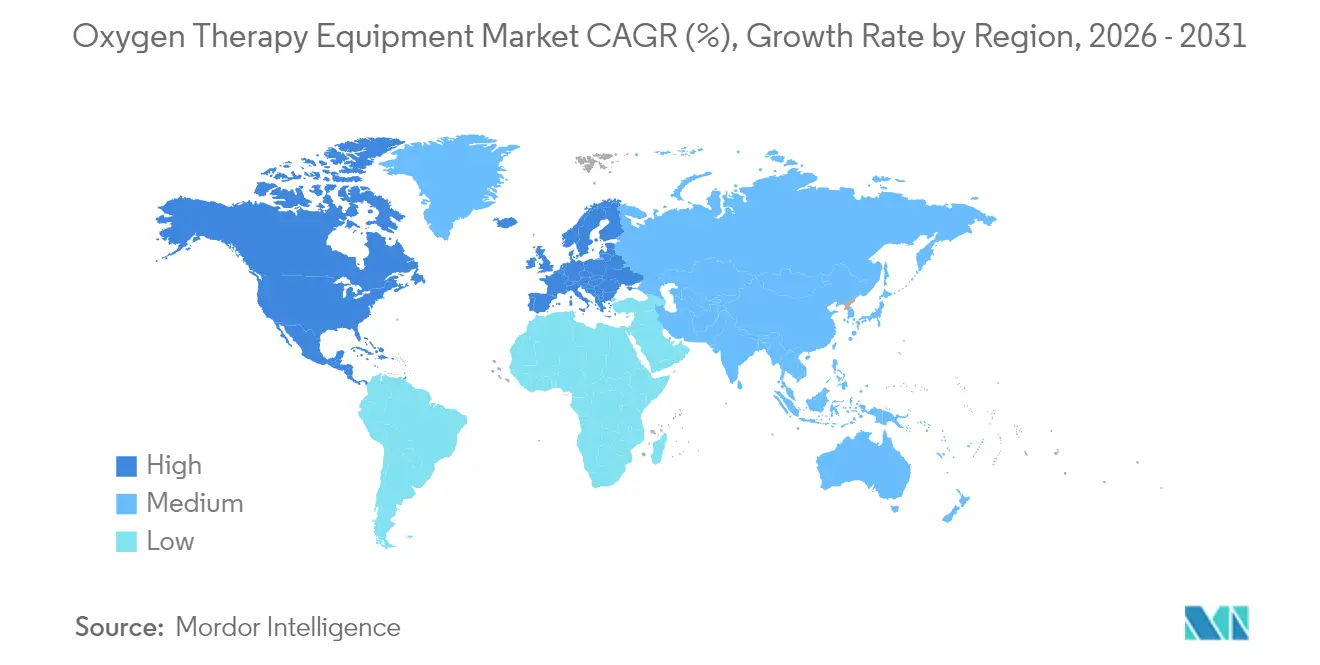

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

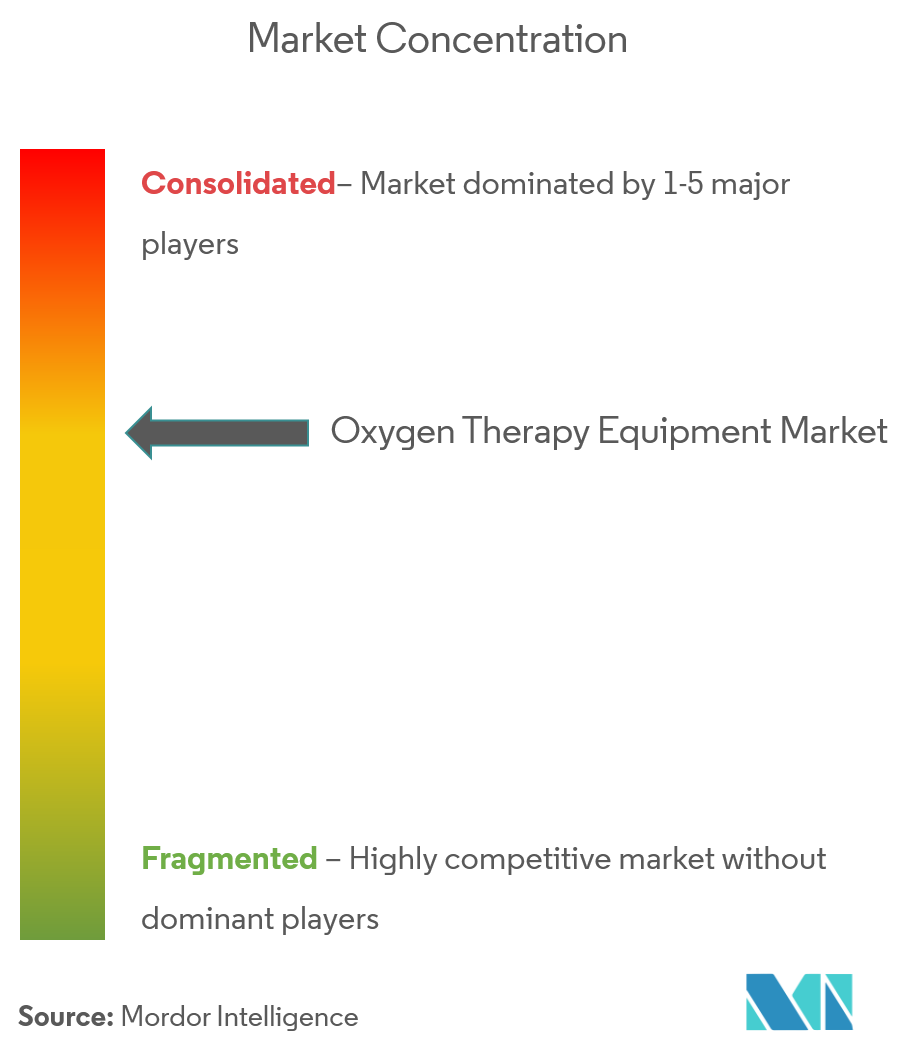

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oxygen Therapy Equipment Market Analysis by Mordor Intelligence

The oxygen therapy equipment market size is expected to grow from USD 3.85 billion in 2025 to USD 4.11 billion in 2026 and is forecast to reach USD 5.7 billion by 2031 at 6.77% CAGR over 2026-2031. Growth is propelled by the rising global burden of chronic respiratory diseases, rapid device miniaturization, sustained investment in home healthcare, and supportive reimbursement frameworks. Intensifying product recalls and exits by prominent manufacturers are widening supply gaps that agile competitors are filling, while IoT-enabled monitoring is redefining care pathways across acute and chronic settings. At the same time, evolving regulatory regimes and component-level supply chain vulnerabilities are shaping competitive strategies and capital allocation priorities. Heightened clinical demand for portable concentrators, telehealth integration, and advanced battery chemistries underscores the market’s pivot toward patient-centric, data-driven respiratory care solutions.

Key Report Takeaways

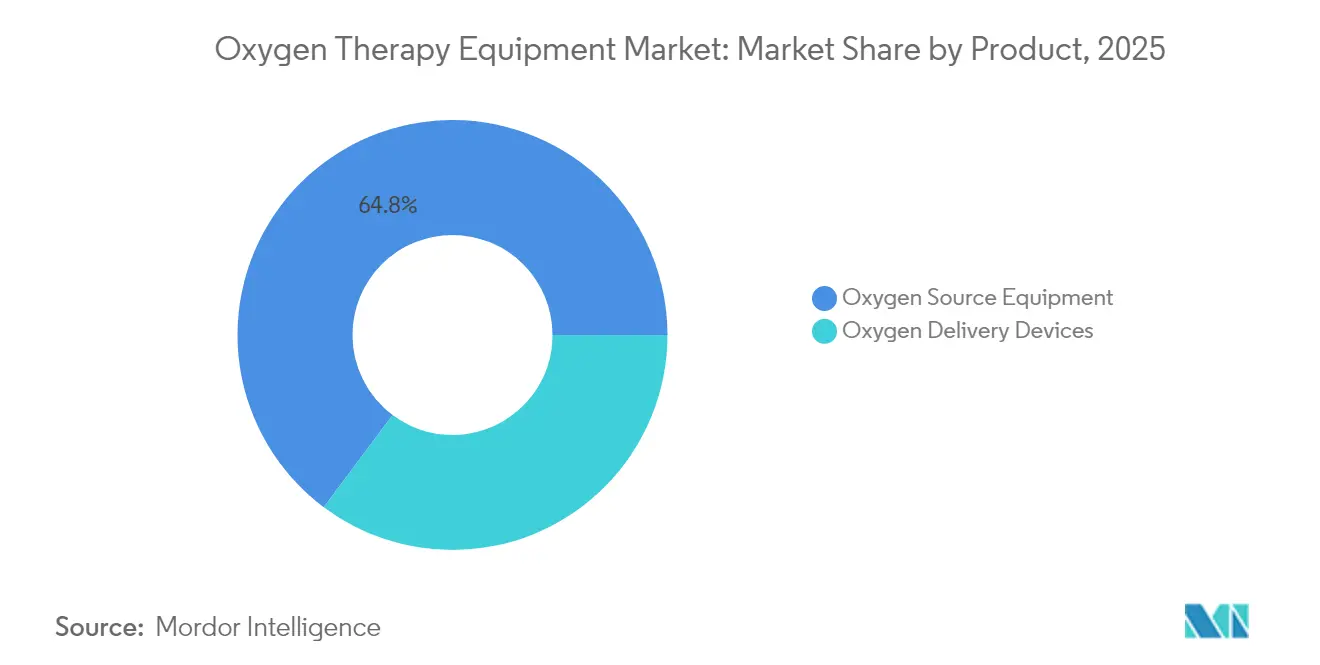

- By product category, Oxygen Source Equipment led with 64.78% of the oxygen therapy equipment market share in 2025; Oxygen Delivery Devices are projected to expand at a 7.02% CAGR to 2031.

- By portability, Stationary Devices held 53.10% of the oxygen therapy equipment market size in 2025, while Portable Devices record the fastest forecast CAGR at 8.42% through 2031.

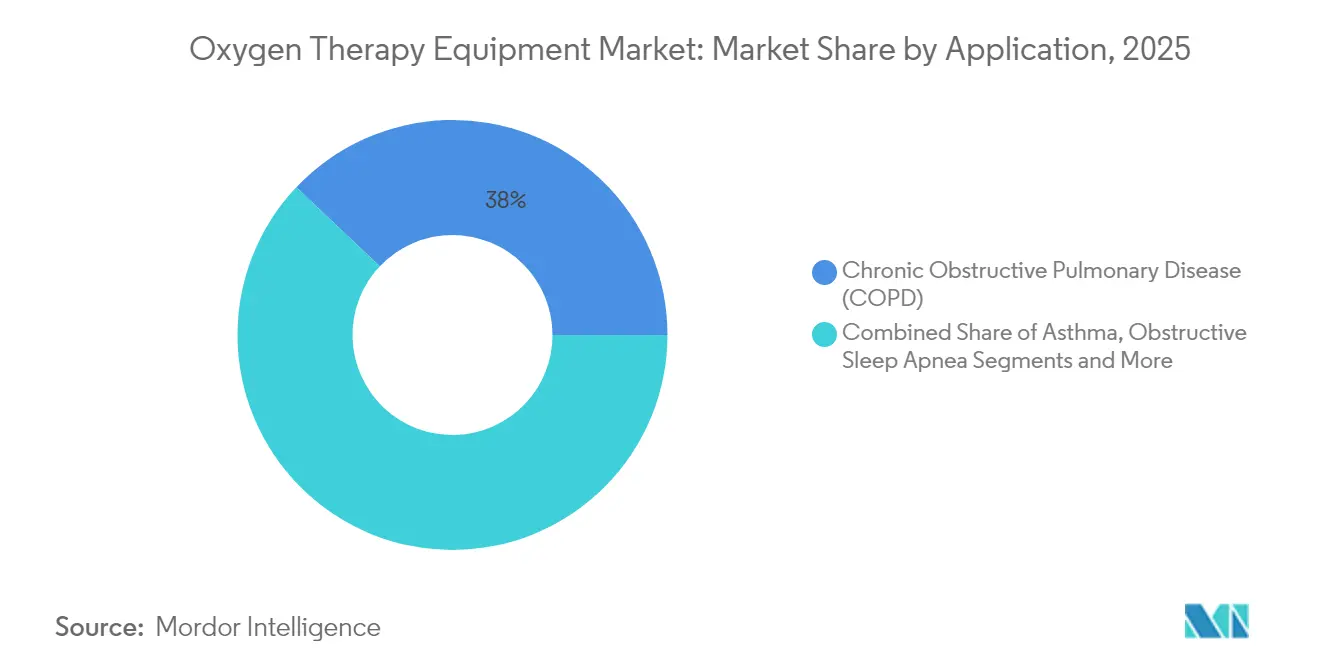

- By application, COPD accounted for 37.95% of the oxygen therapy equipment market size in 2025; Obstructive Sleep Apnea is growing at an 7.81% CAGR through 2031.

- By end user, Home Healthcare is advancing at an 8.02% CAGR, outpacing Hospitals that commanded 40.92% of 2025 revenue.

- North America captured 43.05% revenue share in 2025; Asia-Pacific is the fastest-growing region at 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oxygen Therapy Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising COPD & other respiratory disease prevalence | +1.8% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Shift toward home-based oxygen therapy & portable devices | +1.5% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Rapid device miniaturisation & IoT-enabled monitoring | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Stricter hospital accreditation standards that mandate 24/7 pulse-oximetry and reliable oxygen supply | +1.0% | North America & EU primarily, expanding to APAC | Medium term (2-4 years) |

| Next-gen lithium-sulfur batteries enabling ultra-light POCs | +0.8% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Telehealth-integrated remote oxygen management demand | +0.7% | North America & EU, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising COPD & Other Respiratory Disease Prevalence

The escalating incidence of COPD, asthma, and interstitial lung diseases is a critical demand driver for the oxygen therapy equipment market. Nearly 90% of COPD-related deaths occur in low- and middle-income countries, underscoring unmet therapeutic needs [1]World Health Organization, “Chronic Obstructive Pulmonary Disease,” who.int. Environmental pollution accounts for 41.79% of COPD risk factors among younger cohorts, while smoking contributes 19.81%, indicating structural demand independent of tobacco trends. As global populations age, prevalence rises in tandem, particularly across Asia-Pacific economies experiencing rapid demographic shifts.

Shift Toward Home-Based Oxygen Therapy & Portable Devices

Cost-containment imperatives and patient preference for independence are accelerating the transition from facility-based to home-based therapy. US home healthcare expenditures for 3 million Medicare beneficiaries totaled USD 125.2 billion in 2024. The Home Health Value-Based Purchasing Model now links payments to quality outcomes, stimulating adoption of connected portable concentrators that support real-time monitoring. Inogen’s Rove 4—which delivers 840 ml/min oxygen at under 1.36 kg—exemplifies how design advances eliminate mobility barriers.

Rapid Device Miniaturization & IoT-Enabled Monitoring

Technology convergence is reshaping respiratory care into an intelligent, data-rich ecosystem. Platforms such as Pneulytics integrate clinical data with real-time parameters to enable personalized COPD management. IoT frameworks employing edge computing, like Monit4Healthy, minimize latency and protect data security while transmitting oxygen saturation metrics. Advances in nanosized zeolite sieves have pushed portable concentrator oxygen purity to 90% through optimized pressure-swing adsorption cycles.

Next-Gen Lithium-Sulfur Batteries Enabling Ultra-Light POCs

Lithium-sulfur pouch cells delivering gravimetric energy densities above 750 Wh kg–1 are dismantling historical weight constraints that limited portable oxygen concentrator adoption. Sulfurized polyacrylonitrile cathodes slash mass while improving safety over conventional lithium-ion chemistries. As electric-vehicle scale economies drive down cost curves, medical device suppliers are integrating these batteries to extend run-time without compromising form factor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulatory approvals & compliance costs | -1.1% | Global, most severe in EU and North America | Medium term (2-4 years) |

| High capital/reimbursement burden for long-term therapy | -0.9% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Supply-chain fragility of zeolite molecular-sieves | -0.7% | Global manufacturing hubs | Short term (≤ 2 years) |

| Rising fire-safety & insurance restrictions in home use | -0.5% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulatory Approvals & Compliance Costs

The European Union Medical Device Regulation (EU 2017/745) mandates broader clinical evidence, post-market surveillance, and Unique Device Identification by 2027-2028, materially escalating compliance spending [2]European Commission, “Medical Device Regulations,” ec.europa.eu. Smaller manufacturers face disproportionate burdens, potentially hastening consolidation. In the United States, the FDA’s updated medical gas regulations effective December 2025 revise CGMP standards and safety reporting obligations, adding documentation layers for oxygen suppliers [3]US FDA, “Medical Gases; Current Good Manufacturing Practice Final Rule,” federalregister.gov.

High Capital/Reimbursement Burden for Long-Term Therapy

Medicare’s 36-month capped rental policy obliges suppliers to provide equipment beyond the payment window, squeezing margins. A 2024 industry survey found 93.5% of home medical equipment suppliers implemented operational cuts after blended payment expirations; 65.4% reduced product lines and 53.3% trimmed staff. Low-income countries lacking systematic reimbursement must rely on donor programs, with the Lancet Global Health Commission estimating USD 6.8 billion annual outlays to close oxygen access gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Source Equipment Dominance Faces Delivery Innovation

Oxygen Source Equipment held 64.78% of the oxygen therapy equipment market share in 2025. Concentrators drive this segment through pressure-swing adsorption efficiency gains, while liquid systems cater to high-purity therapeutic niches. Compressed cylinders remain vital for emergency back-up, particularly in EMS fleets. The oxygen therapy equipment market size for delivery devices is refining at a 7.02% CAGR, fueled by patient comfort innovations such as Fisher & Paykel’s F&P Nova Nasal mask with integrated humidity control. Smart cannulas fitted with saturation sensors relay adherence data, improving regulatory compliance with emerging quality-of-life metrics.Supporting this shift, concentric supply disruptions—most notably Philips Respironics’ 2024 discontinuation of 19 respiratory SKUs—have encouraged hospitals and distributors to dual-source delivery interfaces.

Rapid regulatory approvals for alternative interfaces accelerated portfolio diversification. Digital fit-testing, 3-D-printed adapter options, and antimicrobial tubing coatings have entered mainstream procurement discussions across US hospital groups.

By Portability: Stationary Growth Defies Mobility Trends

Stationary concentrators still captured 53.10% of the oxygen therapy equipment market size in 2025 even as consumer discourse focuses on portability. Reliability and continuous high-flow capabilities suit severe hypoxemic COPD patients, and payers often reimburse these devices preferentially under capped rental models. Recent releases like Caire’s IntenOxy 5 deliver 95.5% purity at 5 LPM while drawing under 330 W, reducing electricity costs for seniors on fixed incomes. Manufacturers also add smart-grid interfaces to balance residential power loads and claim sustainability credits.

Portable devices account for the remaining share but post the market’s fastest absolute revenue gains. The oxygen therapy equipment market demonstrates 8.42% CAGR for ultra-portable devices as battery energy densities climb, extending run-time beyond 6 hours at pulse setting 3. Companies are bundling service subscription models that cover consumables, firmware upgrades, and telemonitoring analytics. Integrators experiment with modular ecosystems pairing a bedside station with a backpack-size concentrator using interchangeable sieve cartridges, ensuring continuity during travel or outages.

By Application: Sleep Apnea Emerges as High-Growth Opportunity

COPD occupied 37.95% of 2025 revenue and remains the cornerstone application for the oxygen therapy equipment market. Clinical guidelines endorse long-term oxygen therapy in severe hypoxemia, anchoring predictable demand. Yet, Obstructive Sleep Apnea (OSA) now shows the fastest expansion at 7.81% CAGR. While CPAP remains first-line, oxygen supplementation is gaining traction among CPAP-intolerant and residual hypoxemia cohorts. Asthma, Respiratory Distress Syndrome, pneumonia recovery, and heart failure collectively form a diversified tail, each requiring tailored flow-rate algorithms. IoT-enabled devices that auto-adjust FiO₂ in response to nocturnal desaturation or exertional hypoxia extend therapy versatility.

Clinical trials exploring closed-loop oxygen titration for heart failure patients indicate hospital-readmission reductions, bolstering insurer interest in multiparameter telemonitoring bundles.

By End User: Home Healthcare Acceleration Reshapes Care Delivery

Hospitals represented 40.92% of 2025 sales yet face volume migration as payers incentivize lower-cost care sites. The oxygen therapy equipment market size in home healthcare channels is rising fastest at 8.02% CAGR, reflecting demographic pressures and post-pandemic telehealth normalization. Providers bundle concentrators with RPM dashboards, creating subscription revenue streams that offset device commoditization.

Ambulatory surgical centers are equipping recovery bays with lightweight cylinders and compact concentrators to meet same-day discharge criteria. Long-term care and skilled nursing facilities adopt pooled-fleet models that rotate assets between residents, optimizing utilization. Emergency medical services are piloting hybrid lithium-sulfur battery packs to extend cylinder life during regional disaster responses.

Geography Analysis

North America generated 43.05% of 2025 revenue, supported by robust reimbursement systems, high COPD prevalence, and mature distribution networks. The FDA’s December 2025 medical gas mandate intensifies audit preparation among US manufacturers, while Canada’s federal-provincial drug plans continue to integrate portable concentrator benefits. Mexico’s Seguro Popular expansion drives localized assembly partnerships to reduce import duties.Asia-Pacific is the fastest-growing territory, posting 8.66% CAGR thanks to healthcare spending growth, universal insurance rollouts, and aging demographics. China’s medical device market is projected to reach USD 138 billion by 2027. Though COPD prevalence is stabilizing, absolute patient volumes remain huge. India witnesses double-digit demand growth as public-private partnerships upgrade district hospitals with oxygen plants. Japanese and South Korean suppliers leverage domestic R&D to export connected concentrators across ASEAN markets, while Australian telehealth frameworks accelerate cross-border RPM adoption.Europe maintains steady growth underpinned by MDR-compliant product refresh cycles and aging populations. Germany’s sickness funds reimburse portable concentrators when paired with adherence-monitoring apps, boosting smart device uptake. The United Kingdom’s NHS Community Oxygen Service deploys remote titration pilots aimed at reducing clinic visits. Southern European economies align procurement criteria with EU medical gas standards, expanding opportunities for value-focused vendors. The Middle East & Africa region records double-digit growth from a low base as governments establish pressure swing adsorption plants following COVID-19 shortages. MedAccess and development banks finance manufacturing hubs to localize sieve production, enhancing regional self-sufficiency. Latin America’s trajectory is mixed: Brazil’s Unified Health System rolls out oxygen concentrators to secondary hospitals, yet currency volatility challenges importer margins in Argentina and Colombia.

Competitive Landscape

The oxygen therapy equipment market landscape is moderately fragmented, though exits such as Philips Respironics’ 2024 retreat have altered share dynamics. Inogen’s acquisition of Physio-Assist for USD 32 million signaled vertical diversification beyond oxygen into airway clearance, aligning with its strategy to own overlapping respiratory pathways.

Technology differentiation underpins competitive advantage. Leading firms deploy AI algorithms that predict exacerbations and auto-adjust flow rates, while mid-tier entrants emphasize low-cost, robust designs for emerging markets. Component scarcity—particularly zeolite molecular sieves—prompted several suppliers to secure long-term offtake agreements with chemical producers to avoid pandemic-like disruptions.

Consolidation attempts face regulatory hurdles: Owens & Minor’s proposed USD 1.36 billion acquisition of Rotech Healthcare collapsed due to FTC concerns over supplier concentration. Consequently, strategists favor bolt-on acquisitions under USD 100 million or joint ventures that sidestep antitrust thresholds. Intellectual-property portfolios around battery chemistries and digital platforms are now key valuation determinants during deal due diligence.

Oxygen Therapy Equipment Industry Leaders

DeVilbiss Healthcare

Hersill

Invacare Corporation

Koninklijke Philips N.V.,

TECNO-GAZ SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Inogen launched Voxi 5, a stationary concentrator targeting long-term care settings in the United States, broadening the company’s reach beyond portable devices.

- January 2025: Caire introduced IntenOxy 5 in the United States and Puerto Rico, featuring 95.5% purity at 5 LPM and low power consumption.

- July 2023: O2 Worx partnered with Submarine Manufacturing and Products to widen access to hyperbaric oxygen chambers across rehabilitation centers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the oxygen therapy equipment market as every FDA- or CE-cleared device that produces, stores, or delivers medical-grade oxygen, namely concentrators, cylinders, liquid systems, masks, cannulas, and basic accessories used in hospitals and home settings.

Scope exclusion: Bulk oxygen gas, full ventilators, and hyperbaric chambers remain outside this measurement.

Segmentation Overview

- By Product

- Oxygen Source Equipment

- Oxygen Cylinders

- Oxygen Concentrators

- Liquid Oxygen Devices

- Others

- Oxygen Delivery Devices

- Oxygen Masks

- Nasal Cannula

- Venturi Masks

- Non-Rebreather Masks

- Others

- Oxygen Source Equipment

- By Portability

- Stationary Devices

- Portable Devices

- By Application

- Asthma

- Obstructive Sleep Apnea

- Chronic Obstructive Pulmonary Disease (COPD)

- Respiratory Distress Syndrome

- Others

- By End User

- Hospitals

- Home Healthcare

- Ambulatory Surgical Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

We gathered foundational numbers from open datasets issued by the World Health Organization, Eurostat COMEXT, UN Comtrade, and the US Centers for Medicare & Medicaid Services; these mapped patient pools, import flows, and reimbursement ceilings. Insights from trade associations such as the European Industrial Gases Association and peer-reviewed journals in Respiratory Medicine clarified technology shifts and average selling prices. Paid repositories, D&B Hoovers for company splits and Dow Jones Factiva for regulatory updates, added depth. The sources cited are illustrative; many further public and paid references guided our work.

Primary Research

Mordor analysts spoke with respiratory therapists, biomedical engineers, hospital buyers, and home-care distributors across North America, Europe, and Asia. These discussions confirmed utilization hours, replacement cycles, and the real-world mix of portable versus stationary devices, sharpening every assumption built from desk findings.

Market-Sizing & Forecasting

A single-pass top-down model begins with country COPD prevalence, long-term oxygen therapy penetration, and average device life to size demand. It is then checked against sampled supplier roll-ups and channel audits. Key variables include lithium battery price trends, import tariffs on concentrators, hospital PSA plant counts, reimbursement caps, and seasonality in respiratory admissions. Multivariate regression projects each driver, while scenario analysis captures possible policy or recall shocks. Gaps in bottom-up data are bridged with calibrated utilization multipliers vetted in interviews.

Data Validation & Update Cycle

Outputs pass variance tests against shipment ledgers, public financials, and sentinel price trackers before a senior analyst review. The model refreshes annually, with interim updates triggered by major recalls, reimbursement changes, or pandemic-level demand spikes.

Why Mordor's Oxygen Therapy Equipment Baseline Stands Firm

Published estimates often diverge because analysts fold gases into hardware, select different pricing years, or freeze exchange rates.

Our device-only scope, mid-case reimbursement scenario, and annual refresh differ from figures that bundle consumables, assume aggressive subsidies, or rely on 2022 price decks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.85 B (2025) | Mordor Intelligence | - |

| USD 3.80 B (2024) | Regional Consultancy A | Static ASPs, omits wearable sensors |

| USD 3.43 B (2024) | Trade Journal B | Excludes liquid systems, lower COPD baseline |

| USD 4.20 B (2025) | Global Consultancy C | Adds hyperbaric chambers and accessories |

Taken together, the comparison shows that when scope and pricing assumptions are normalized, Mordor's continuously refreshed figure offers the balanced, transparent baseline procurement teams can lean on with confidence.

Key Questions Answered in the Report

What is the current Oxygen Therapy Equipment Market size?

The Oxygen Therapy Equipment Market stands at USD 4.11 billion in 2026 and is projected to reach USD 5.7 billion by 2031.

Who are the key players in Oxygen Therapy Equipment Market?

DeVilbiss Healthcare, Hersill, Invacare Corporation, Koninklijke Philips N.V., and TECNO-GAZ SpA are the major companies operating in the Oxygen Therapy Equipment Market.

Which is the fastest growing region in Oxygen Therapy Equipment Market?

Asia-Pacific posts the highest growth, advancing at a 8.66% CAGR thanks to rising healthcare investments and an aging population

Which product category currently leads the market?

Oxygen Source Equipment, including concentrators and liquid systems, holds 64.78% of 2025 revenue, making it the dominant segment.

Page last updated on: