Airway Stent/Lung Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

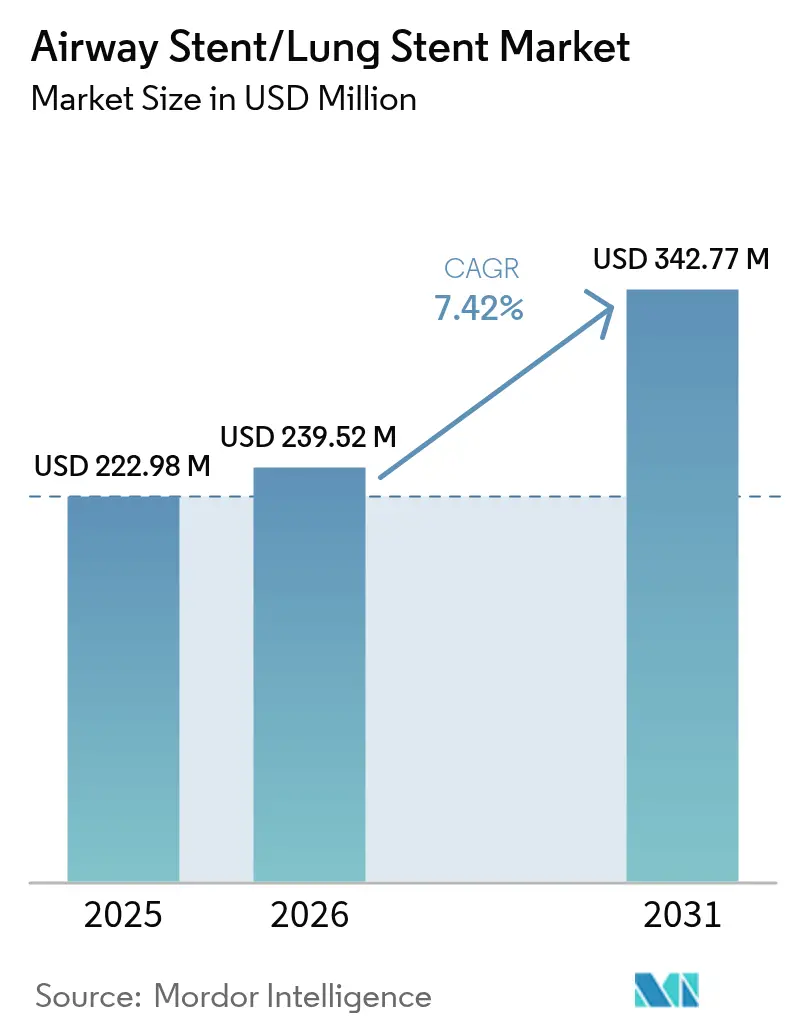

| Market Size (2026) | USD 239.52 Million |

| Market Size (2031) | USD 342.77 Million |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

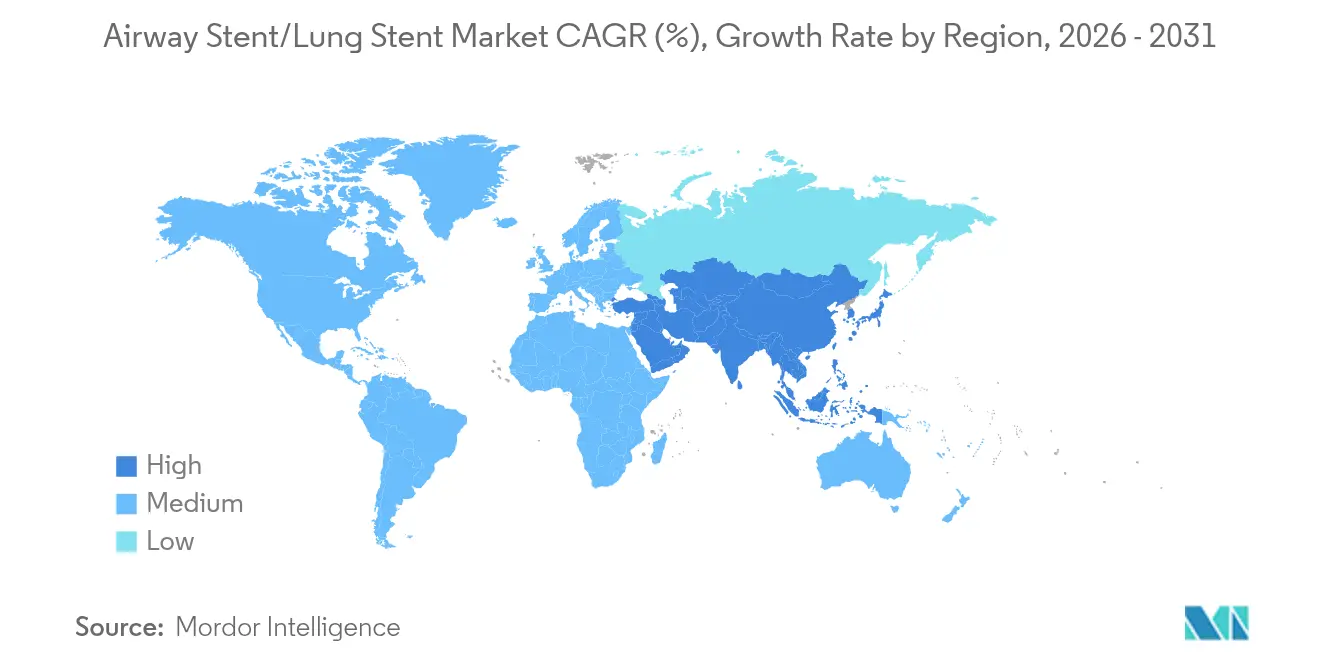

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airway Stent/Lung Stent Market Analysis by Mordor Intelligence

The airway stent/lung stent market size was valued at USD 222.98 million in 2025 and estimated to grow from USD 239.52 million in 2026 to reach USD 342.77 million by 2031, at a CAGR of 7.42% during the forecast period (2026-2031). Demand is fueled by rapid developments in device design, including 3D-printed patient-specific implants, biodegradable polymers that dissolve once the airway has healed, and drug-eluting coatings that inhibit granulation tissue formation. North America remains the anchor of global revenue, thanks to its mature reimbursement frameworks and early adoption of robotic bronchoscopy. In contrast, the Asia-Pacific region leads growth, driven by rising incidence of COPD and lung cancer, broader health insurance coverage, and government investments in tertiary respiratory care centers. Material-level innovation accelerates product turnover as hospitals and specialty clinics transition from durable metals to resorbable polymers, which eliminate the need for removal surgeries. At the same time, competition intensifies as incumbents such as Boston Scientific and Cook Group defend their share against start-ups focused on custom bioresorbable devices and AI-guided placement platforms. Regulatory convergence, notably the United States' Quality System Regulation revisions effective in 2026, is set to smooth cross-border approvals and hasten the diffusion of technology.

Key Report Takeaways

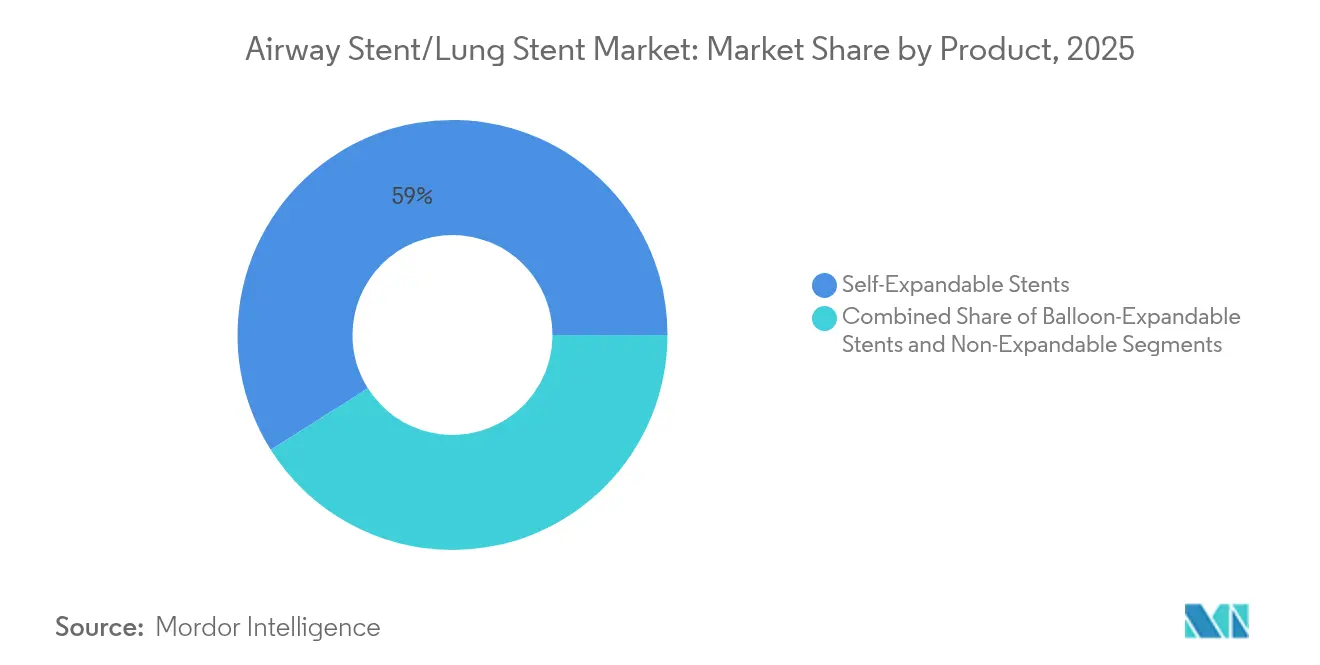

- By product category, self-expandable stents held a 58.96% revenue share in 2025, while non-expandable and customized 3D-printed devices are projected to post the fastest growth rate of 8.78% through 2031.

- By material, metal frameworks accounted for 50.83% of the airway stent/lung stent market size in 2025; bioresorbable polymers are projected to grow at a 9.07% CAGR between 2026 and 2031.

- By type, tracheobronchial designs accounted for 65.52% of the revenue share in 2025, whereas Y-shaped carinal models are forecasted to advance at an 8.66% CAGR through 2031.

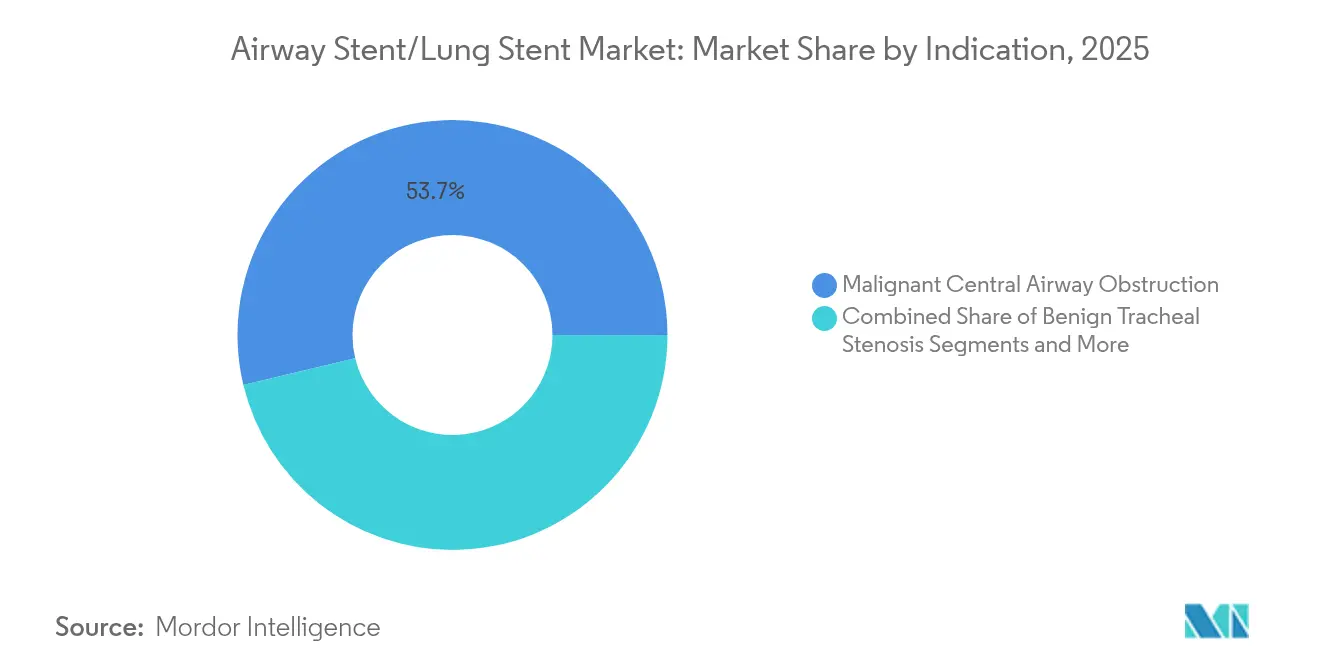

- By indication, malignant central airway obstruction accounted for 53.73% of the airway stent/lung stent market size in 2025, and post-lung-transplant complications are expected to register the highest CAGR of 9.32% through 2031.

- By end user, hospitals led with 66.22% revenue share in 2025; specialty pulmonology clinics are anticipated to record a 10.06% CAGR over the forecast period.

- By geography, North America dominated the airway stent/lung stent market with a 38.45% market share in 2025, while the Asia-Pacific region is projected to expand at the fastest CAGR of 9.2% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Airway Stent/Lung Stent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Lung & Chronic Respiratory Disorders | +1.8% | Global, with highest impact in APAC and emerging markets | Long term (≥ 4 years) |

| Growing Preference For Minimally Invasive Procedures | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rapid Material Innovation: 3D-Printed & Drug-Eluting Bioresorbable Stents | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Benefits Associated with Usage of Pulmonary Stents | +0.9% | Global | Short term (≤ 2 years) |

| Emergence Of Fully Biodegradable Stents and Innovative Stents | +1.0% | North America & EU, with spillover to APAC | Long term (≥ 4 years) |

| Robotic Bronchoscopy Enabling Precise Stent Placement | +0.8% | North America, EU, and select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Lung and Chronic Respiratory Disorders

Respiratory Research reported 213.39 million COPD cases in 2024, reflecting better diagnostics and longer survival that in turn keep interventional demand high.[1]Jinping Zheng, “Global, Regional, and National Burden of Chronic Obstructive Pulmonary Disease,” Respiratory Research, biomedcentral.com Lung-cancer-related airway obstruction frequently requires palliative stents that restore patency and improve breathing comfort. Smoking, which still drives 34.8% of COPD disability-adjusted life-years, and ambient particulate pollution at 22.2% sustain a large patient pipeline. Aging populations amplify case volumes in developed economies, whereas India alone tallied 37.8 million COPD cases, underscoring opportunity in fast-growing Asia-Pacific markets.[2]Prakash P. Doke, “Chronic Respiratory Diseases: A Rapidly Emerging Public Health Concern,” Indian Journal of Public Health, journals.lww.com

Growing Preference for Minimally Invasive Procedures

High-frequency jet ventilation using silicone catheters achieved 84% procedural success in 2024 with median operating times of 35 minutes and no postoperative complications, strengthening the clinical case for bronchoscopic stenting over open surgery.[3]Onur Küçük et al., “Long-Term Results of Intensive Care Patients with Post-Intubation Tracheal Stenosis,” BMC Pulmonary Medicine, bmcpulmmed.biomedcentral.comHospitals embrace outpatient protocols to contain costs and accelerate recovery, while cone-beam CT and digital tomosynthesis sharpen placement accuracy. Robotic bronchoscopy systems deliver diagnostic yields of 88-94% for peripheral lesions, further easing physician adoption.

Rapid Material Innovation in 3D-Printed and Drug-Eluting Bioresorbable Stents

The United States FDA cleared Peytant Solutions’ covered stent system under the De Novo pathway in 2024, signaling regulatory openness to next-generation platforms.[4]FDA Center for Devices and Radiological Health, “Minima Stent System – P240003,” fda.gov Michigan Medicine launched a 35-patient infant trial for 3D-printed bioresorbable devices in March 2025, advancing personalized implants that dissolve after airway remodeling. Iron-based bioresorbable scaffolds showed 95.4% absorption within three years while keeping structural integrity during healing in EuroIntervention’s first-in-human study.

Benefits Linked to Pulmonary Stent Usage

Airway stenting delivers immediate dyspnea relief and improves functional scores according to Journal of Bronchology & Interventional Pulmonology findings. In lung-transplant patients, Y-shaped carinal stents cut intervention frequency from 15.6 to 4.8 procedures and extended treatment intervals up to 85.8 days, reducing hospital utilization. The reversibility of silicone devices affords safety margins over permanent surgery and keeps infection rates comparatively low.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability Of Alternative Interventions | -0.8% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Device-Related Complications | -1.1% | Global | Short term (≤ 2 years) |

| Reimbursement Gaps For Customized & Biodegradable Stents | -0.6% | North America & EU primarily | Medium term (2-4 years) |

| Regulatory Ambiguity For Patient-Specific 3D-Printed Devices | -0.4% | Global, led by regulatory-stringent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Interventions

Balloon dilation solves many benign strictures with 88.9% efficacy and leaves no implant behind, while surgical reconstruction offers definitive cures for localized stenosis in fit patients. Techniques such as laser, cryotherapy, and argon plasma coagulation recanalize blocked airways quickly, and Montgomery T-tubes provide another removable option in post-tracheotomy stenosis.

Device-Related Complications

Migration, granulation, and fracture remain leading concerns, with metallic devices often requiring complex extraction that carries bleeding and perforation risks. Up to 75% granulation incidence imposes repeated bronchoscopies, and infection risk escalates in immunocompromised patients. Long-term Mayo Clinic data showed a 22-month average before complications necessitated metallic-stent removal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Self-Expandable Dominance Drives Innovation

Self-expandable devices accounted for 58.96% of 2025 revenue, confirming their versatility in treating both benign and malignant obstructions. These stents expand gently after deployment and maintain steady radial force, helping physicians manage variable airway diameters. Balloon-expandable units are designed for scenarios that require precise sizing, such as pediatric tracheal narrowing. Non-expandable and 3D-printed custom designs are projected to achieve an 8.78% CAGR through 2031. The shift toward personalized implants reflects a growing awareness that geometric differences necessitate tailored solutions. AnatomikModeling and Toulouse University Hospital executed one of the earliest custom placements in 2016 and have since demonstrated improved migration profiles in validation studies. Michigan Medicine’s 2025 infant trial marks a new frontier in resorbable, bespoke devices.

Self-expandable devices are reliable in collapse-prone segments, yet physicians increasingly prescribe custom-printed stents for airways distorted by tumors or postsurgical changes. This trend aligns with hospital investment in point-of-care 3D-printing labs that compress turnaround times and lower logistic costs. As these centers mature, non-expandable personalized units will claim a larger slice of the airway stent/lung stent market, even as self-expandable lines remain workhorse solutions for general obstruction.

By Material: Metal Leadership Faces Polymer Challenge

Metal frameworks remain the default in rapidly progressing tumors due to their high radial strength and radiopaque profiles, which facilitate imaging follow-up. They captured 50.83% of 2025 sales. Yet, biodegradable polymers are the fastest risers, with a 9.07% CAGR through 2031, as clinicians prize temporary support without the burden of removal surgery. Silicone options remain popular in benign diseases because they are less prone to infection and can be easily extracted. Composite designs that combine metal skeletons with polymer linings aim to achieve the best of both worlds, incorporating drug-eluting layers to mitigate granulation.

In adult trials, polydioxanone devices demonstrated 89.7% clinical effectiveness and subsequently resorbed, thereby freeing the airway from foreign material. Iron-scaffold data revealed 95.4% absorption within three years with no loss of mechanical stability. Surface laser texturing promoted endothelial growth while reducing smooth-muscle proliferation by approximately 75%, which can lower the risk of restenosis. As price gaps narrow, polymer adoption will accelerate, shrinking metal’s share of the airway stent/lung stent market.

By Type: Tracheobronchial Stents Lead Specialized Applications

Tracheobronchial models delivered 65.52% of 2025 revenue due to their broad utility in both central airways. Y-shaped carinal stents, though with a smaller base, are expanding briskly at an 8.66% CAGR, driven by transplant-associated bifurcation complications. Laryngeal devices cover niche indications where upper-airway patency is threatened after trauma or oncologic resections.

The clinical benefit of Y-stents in lung transplant recipients is notable; secondary carina placements reduce repeat procedures by two-thirds while tripling the time between interventions. Angulated designs targeting post-tuberculosis bronchostenosis highlight how geometry-specific engineering enhances dwell time and reduces migration. As surgical volumes rise and transplant survival extends, the need for complex bifurcation devices will grow in the airway stent/lung stent market.

By Indication: Malignant Obstruction Drives Core Demand

Lung-cancer-related obstruction made up 53.73% of 2025 sales, and the palliative benefit of restoring airflow remains central to demand. Post-transplant complications, although smaller, constitute the fastest-growing indication at 9.32% CAGR, fueled by expanding transplant programs and lengthening graft survival. Benign tracheal stenosis maintains a stable user base that is increasingly opting for resorbable stents. Tracheoesophageal fistulas need covered models that isolate the airway from the digestive tract.

Standardized grading from the International Society for Heart and Lung Transplantation aids uniform decision-making and builds a stable case volume for interventional pulmonologists. In esophageal carcinoma with airway involvement, median survival stretches to 97 days post-stenting, underscoring life-quality gains even in late-stage disease.

By End User: Hospitals Dominate While Specialty Clinics Surge

Hospitals retained a 66.22% share in 2025, supported by intensive care units and on-call thoracic surgery teams for emergencies. However, specialty pulmonology clinics are expected to experience a 10.06% CAGR to 2031, driven by the adoption of outpatient bronchoscopy and robotic platforms that reduce procedure times. Ambulatory surgical centers win business with transparent pricing and same-day discharge policies.

A scoping review on intensive-care pulmonology confirms stent placement as a critical option for mechanically ventilated patients with central obstruction. Jet-ventilation success rates of 84% show that specialized centers can achieve high efficiency. As payers push care into lower-cost settings, clinics that can combine advanced imaging, custom printing, and robotic guidance will capture an incremental share of the airway stent/lung stent market volume.

Geography Analysis

North America generated 38.45% of revenue in 2025, underpinned by advanced reimbursement policies and rapid adoption of precision placement technologies. The FDA’s 2024 De Novo clearance for Peytant’s stent system demonstrates a supportive regulatory climate. The forthcoming Quality System Regulation alignment with ISO standards by 2026 will streamline manufacturing compliance and help innovative devices reach hospitals more quickly. Robotic bronchoscopy diagnostic yields of up to 94% solidify the region’s leadership in technology-driven care. While Medicare covers core interventional pulmonology codes, payment gaps persist for customized implants, tempering near-term adoption of 3D-printed solutions.

The Asia-Pacific region is the growth engine, with a 9.2% CAGR projected to 2031. COPD prevalence, 37.8 million cases in India alone, aligns with high urban air-pollution exposure and smoking rates. China’s hospital build-out and a rising middle class are expanding the treated population, despite a 22% decline in medtech investment in 2024 amid tighter capital markets. Japan’s so-called device-lag underscores approval delays, but recent harmonization initiatives aim to shorten the time to market. Together, these dynamics create a sizable addressable base for the airway stent/lung stent market.

Europe offers steady expansion supported by universal healthcare and a strong evidence culture. AnatomikModeling’s collaboration with Toulouse University Hospital showcases the continent’s prowess in custom 3D stents. Multi-center biodegradable trials report 89.7% effectiveness, keeping Europe at the forefront of resorbable research [bmcpulmmed.biomedcentral.com]. The Medical Device Regulation establishes uniform safety benchmarks that facilitate cross-border device adoption, although cost pressures necessitate demonstrable value before large-scale deployment.

Competitive Landscape

The airway stent/lung stent market is moderately fragmented. Boston Scientific leverages its Ultraflex line to maintain surgeon loyalty through proven performance and broad support services. Cook Group partnered with Getinge to expand the distribution of covered vascular stents, a strategy that may be applied to airway products. Taewoong Medical and other mid-sized Asian manufacturers compete on price and export reach, although stringent regulations in North America and Europe pose entry hurdles. Future differentiation is tilting toward resorbable polymers, drug-eluting coatings, and AI-assisted placement tools that reduce complication rates.

Regulatory evolution remains a competitive lever. The United States Quality System Regulation overhaul will harmonize design-control documentation with ISO 13485, reducing redundant audits for global manufacturers. Firms that invest early in system upgrades will gain smoother paths to global clearances, while those that lag behind risk extended review cycles. Partnering with hospital-based 3D printing labs could grant incumbents faster access to custom device revenue streams. Meanwhile, emerging players bet on dissolving scaffolds and shape-memory alloys to leapfrog metal incumbents and capture share among physicians wary of permanent implants.

Airway Stent/Lung Stent Industry Leaders

Boston Scientific Corporation

Taewoong Medical Co., Ltd.

Cook Group

Micro-Tech (Nanjing) Co., Ltd.

Merit Medical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Michigan Medicine opened a multi-site trial of 3D-printed bioresorbable airway devices for infants with tracheobronchomalacia, aiming for full FDA approval after years of expanded-access use.

- October 2024: Peytant Solutions received De Novo clearance for the forAMStent tracheobronchial covered system, highlighting regulator willingness to back innovative platforms.

- October 2024: FDA set the regulatory review period for the GORE TAG thoracic branch endoprosthesis, clarifying patent-extension timelines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the airway stent market as every factory-sterilized tracheobronchial tube, metal, silicone, hybrid, or patient-specific 3-D printed, inserted bronchoscopically to re-establish airflow in malignant or benign central or distal airway obstruction.

Scope exclusion: vascular, biliary, gastrointestinal, ureteral, and any other non-pulmonary stents are outside this analysis.

Segmentation Overview

- By Product

- Self-Expandable Stents

- Balloon-Expandable Stents

- Non-Expandable / Customized 3D-Printed Stents

- By Material

- Metal

- Silicone

- Hybrid (Covered / Composite)

- Bioresorbable Polymers

- By Type

- Tracheobronchial Stents

- Laryngeal Stents

- Y-Shaped Carinal Stents

- By Indication

- Malignant Central Airway Obstruction

- Benign Tracheal Stenosis

- Post-Lung-Transplant Airway Complications

- Tracheoesophageal Fistula

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Pulmonology Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor interview programs engage interventional pulmonologists, thoracic surgeons, hospital buyers, and device distributors across North America, Europe, and Asia-Pacific. These discussions validate treated-patient ratios, price corridors, the move toward biodegradable designs, and fine-tune clinic versus hospital volume splits.

Desk Research

Our analysts begin with open datasets from the WHO Global Health Observatory, Global Cancer Observatory, and OECD Health Statistics to ground disease incidence and procedure counts. Trade flows in UN Comtrade clarify export volumes of self-expandable tubes, while clinical guidelines from the American College of Chest Physicians explain therapy adoption. Company 10-Ks, investor decks, and news archived in D&B Hoovers and Dow Jones Factiva reveal price shifts and manufacturer revenue mix. The sources noted here are illustrative; many additional public records supported data gathering and checks.

Market-Sizing & Forecasting

We open with a top-down prevalence to treated-patient build, then reconcile outputs with selective bottom-up supplier roll-ups and channel checks. Key variables like repeat stent rate, aging demographics, reimbursement changes, regulatory approvals, ASP drift, and new clinic openings feed a multivariate regression that projects value through 2030. Regional expert consensus bridges any visibility gaps before figures are locked.

Data Validation & Update Cycle

Model outputs pass anomaly scans, peer-dataset comparison, and a multi-analyst review. Reports refresh yearly, with interim updates triggered by major recalls, price shocks, or guideline changes, ensuring clients always receive the latest baseline.

Why Mordor's Airway Stent/lung Stent Market Baseline Commands Reliability

Published estimates often diverge because providers differ on geography mix, inclusion of patient-specific units, ASP escalation logic, and refresh cadence. By selecting a transparent scope, live variables, and an annual update rhythm, we give decision makers a steadier view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 222.98 M (2025) | Mordor Intelligence | - |

| USD 161.70 M (2024) | Global Consultancy A | Omits patient-specific units and several emerging nations |

| USD 122.72 M (2024) | Regional Consultancy B | Uses constant ASP and ignores distributor mark-ups |

| USD 87.83 M (2024) | Trade Journal C | Tracks only hospital procurement, excludes specialty clinics |

The comparison shows that Mordor's mixed top-down checks, selective bottom-up validation, and disciplined scope deliver a balanced, reproducible baseline that users can trust for strategic decisions.

Key Questions Answered in the Report

What is the current size of the airway stent/lung stent market?

The airway stent/lung stent market is valued at USD 239.52 million in 2026 and is projected to hit USD 342.77 million by 2031.

Which product type holds the largest share?

Self-expandable designs led with 58.96% revenue share in 2025, reflecting their adaptability across airway anatomies.

Which region is expanding the fastest?

Asia-Pacific shows a 9.2% CAGR through 2031 due to rising COPD and lung-cancer incidence alongside improving healthcare access.

Why are biodegradable stents gaining traction?

They provide temporary support and then dissolve, avoiding removal surgery and reducing long-term complications.

How will regulatory changes affect the market?

The 2026 alignment of United States Quality System Regulation with international standards should streamline approvals and hasten global rollout of new technologies.

What is the main restraint the market faces?

Device-related complications, especially migration and granulation tissue, remain the top challenge and can require repeated interventions.

Page last updated on: