Surgical Glue Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

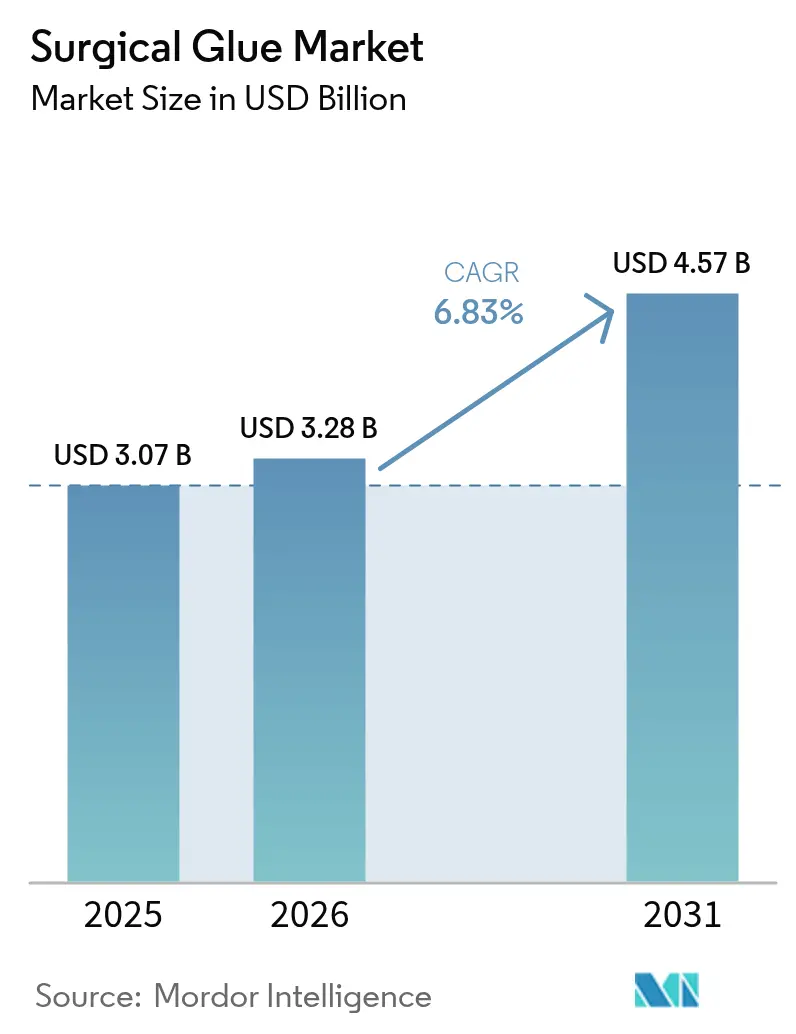

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 4.57 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

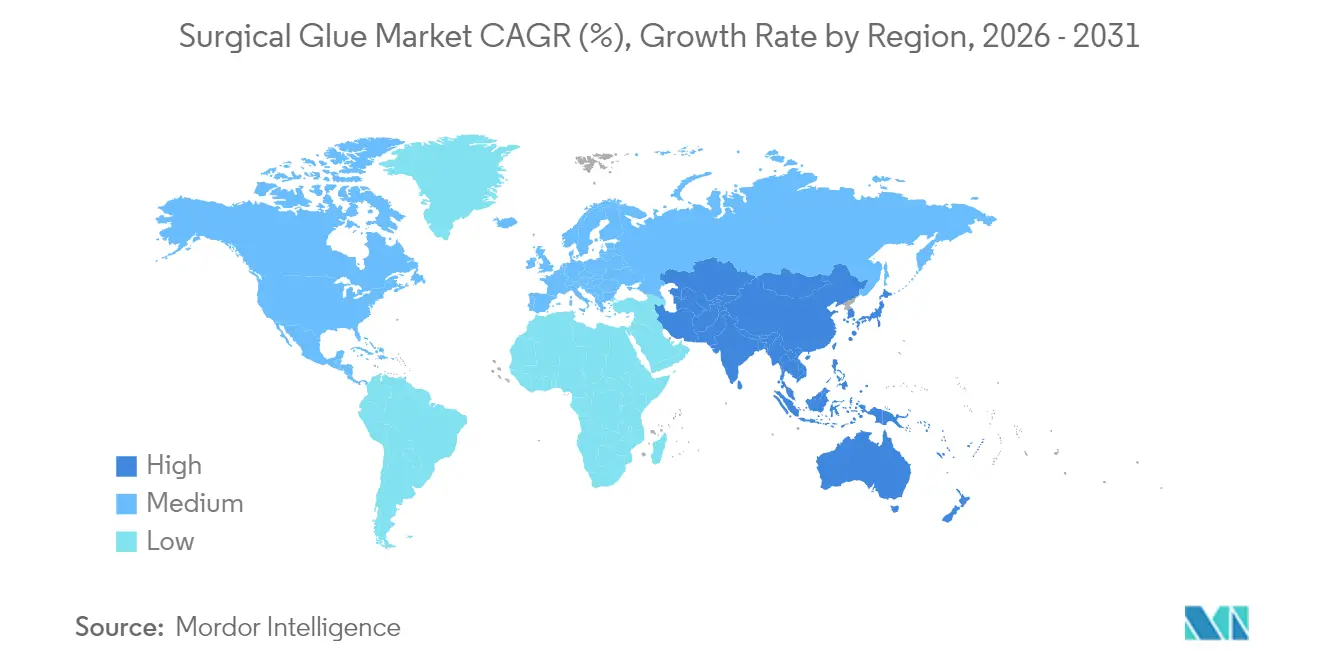

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

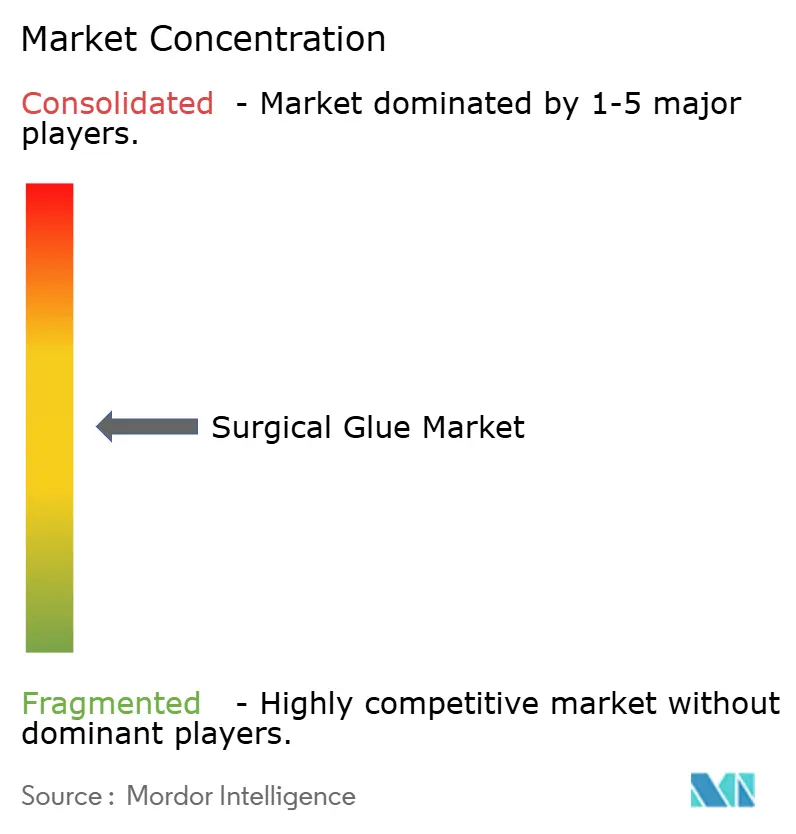

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Glue Market Analysis by Mordor Intelligence

The surgical glue market size was valued at USD 3.07 billion in 2025 and estimated to grow from USD 3.28 billion in 2026 to reach USD 4.57 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). Robust growth follows rising procedure volumes, continual formulation breakthroughs, and the shift toward faster wound closure methods that align with robotic‐assisted surgery requirements. Hospitals accelerate product uptake as they standardize protocols that limit infection risk and shorten operating room time. Synthetic and semi-synthetic products penetrate high-value specialties where engineered consistency outperforms biologic predecessors. North American leadership rests on efficient regulatory pathways, while Asia-Pacific expansion reflects health-system investments that widen access to advanced adhesives. Competitive intensity rises as incumbents and start-ups integrate sensor-enabled dispensers and develop bio-resorbable variants that address sustainability targets.

Key Report Takeaways

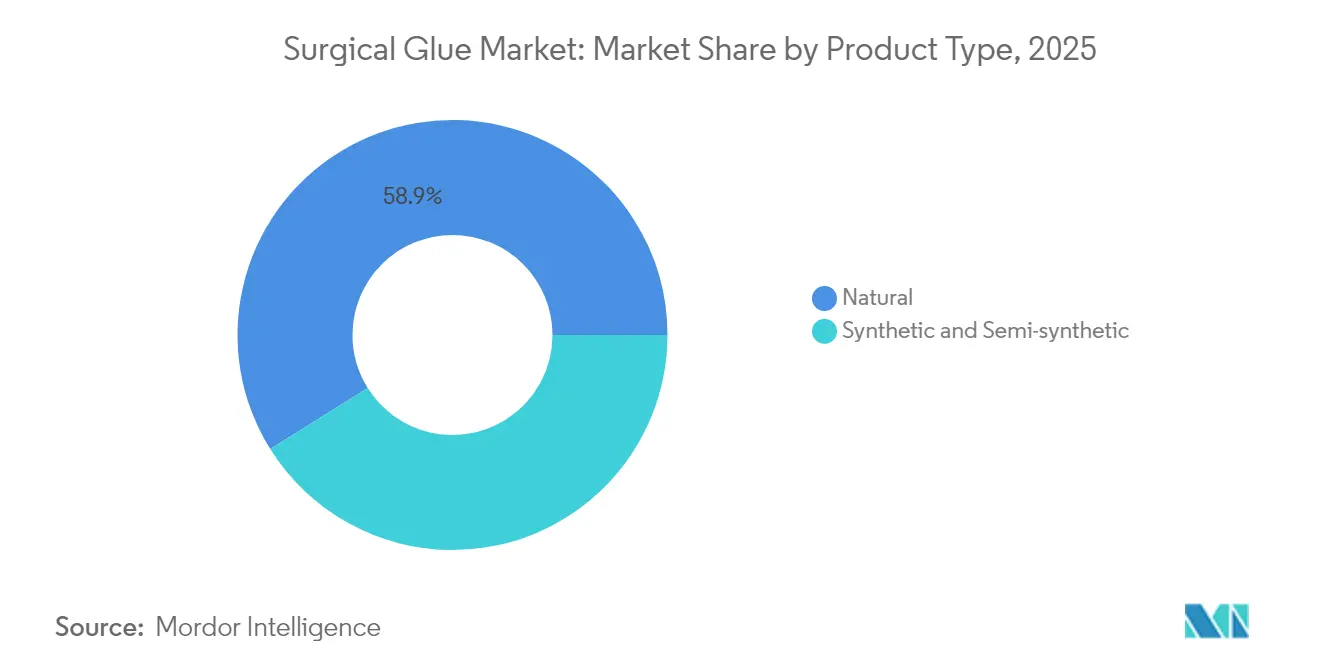

- By product type, natural adhesives held 58.90% of surgical glue market share in 2025, while synthetic and semi-synthetic formulations are projected to grow at a 12.62% CAGR through 2031.

- By application, Cardiovascular surgery captured 32.10% revenue share of the surgical glue market size in 2025 and cosmetic surgery is advancing at a 11.54% CAGR through 2031.

- By end user, Hospitals controlled 64.35% of the surgical glue market size in 2025 and ambulatory surgical centers are set to expand at a 9.18% CAGR to 2031.

- By geography, North America led with 38.85% of surgical glue market share in 2025 whereas Asia-Pacific is forecast to record a 9.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Glue Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes | +1.5% | Global, concentrated in North America & Asia-Pacific | Medium term (2-4 years) |

| Growing preference for faster wound closure and lower infection risk | +1.8% | Global, particularly developed markets | Short term (≤ 2 years) |

| Technological advances in cyanoacrylate & hydrogel formulations | +1.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing incidences of road accidents | +0.9% | Asia-Pacific & Middle East, spillover to emerging markets | Medium term (2-4 years) |

| Adoption of robotic surgery demanding high-precision adhesives | +0.7% | North America & Europe core, expanding globally | Long term (≥ 4 years) |

| Demand for bio-resorbable “green-OR” glues | +0.6% | Europe & North America, early adoption in select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes

Global procedure counts exceed pre-pandemic levels as health systems clear backlogs and expand capacity. Ageing populations in developed economies undergo more complex interventions that favour adhesive solutions over sutures due to shorter closure times and reduced needle-related trauma. Medicare spending on ambulatory surgical center procedures rose 5.7% to USD 6.8 billion in 2024, underscoring a shift toward outpatient care models that prioritise rapid turnover[1]Medicare Payment Advisory Commission, “Report to Congress: Medicare Payment Policy,” medpac.gov. Synthetic cyanoacrylate and hydrogel brands benefit because providers seek standardized performance across specialties. In emerging markets, growth in orthopaedic and trauma surgeries adds incremental volume that sustains double-digit regional demand. Suppliers that maintain broad regulatory clearances capture volume wherever procedure mix widens.

Growing Preference for Faster Wound Closure & Lower Infection Risk

Clinical evidence shows contemporary adhesives shorten operating room time by up to 30% compared with sutures, which frees staff and reduces anaesthesia exposure. Products like the DERMABOND PRINEO system form waterproof microbial barriers that help lower surgical site infection rates. Financial models confirm that shorter stays and lower complication rates improve margins in value-based reimbursement frameworks. Cosmetic and paediatric surgeons adopt glues to enhance aesthetic outcomes and avoid needle marks. Payors recognise the downstream savings and increasingly reimburse premium closure kits that demonstrate cost-effectiveness. This environment accelerates uptake of next-generation cyanoacrylate blends and polymeric hydrogels that deliver rapid set times and secure microbial seals.

Technological Advances in Cyanoacrylate & Hydrogel Formulations

Advances in adhesive chemistry focus on reducing cytotoxicity and expanding tissue compatibility. A polyethylene glycol hydrogel achieved 100% cerebrospinal fluid leak prevention in a 111-patient study[2]Cosgrove G. Rees, “Safety and Efficacy of a Novel Polyethylene Glycol Hydrogel Sealant for Watertight Dural Repair,” Journal of Neurosurgery, thejns.org. Elastomeric sealants delivered 88% hemostasis success in heparinised cardiac cases. Manufacturers tailor viscosity for laparoscopic delivery and design cross-linkers that enable predictable degradation profiles. Innovation extends to hybrid constructs that merge biologic scaffolds with synthetic backbones to balance biocompatibility with mechanical strength. Firms that invest in multi-centre trials position their portfolios for premium pricing in neurosurgery and cardiovascular settings.

Traffic growth in Asia-Pacific and parts of Africa raises trauma caseloads that require rapid haemostatic control. Emergency departments value adhesives that seal wounds quickly without extensive preparatory steps. Governments in India and Indonesia budget for trauma centre upgrades that include stocking of sprayable fibrin glues. Vendors offering shelf-stable kits capture share because supply chains in developing regions face cold-chain constraints. Product registrations that permit pre-hospital use by paramedics address the golden-hour treatment window and further widen demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward minimally-invasive & suture-free devices | -0.8% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Adverse reactions & cytotoxicity of some synthetic glues | -0.5% | Global, heightened scrutiny in North America & Europe | Short term (≤ 2 years) |

| Plasma-derived glue sterilisation & supply-chain bottlenecks | -0.4% | Global, acute impact in Europe & North America | Short term (≤ 2 years) |

| Reimbursement caps on premium sealants in ambulatory settings | -0.3% | North America & Europe, spillover to developed Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Minimally-Invasive & Suture-Free Devices

Energy-based closure tools such as ultrasonic sealers and staple-free laparoscopic clips lessen reliance on adhesives in certain gastrointestinal and thoracic procedures. Device OEMs market these alternatives on claims of faster application and zero chemical residue. In response, glue suppliers engineer sprayable formats and extend cannula lengths to suit reduced port sizes. Partnerships with trocar manufacturers aim to keep adhesives embedded within evolving minimally invasive workflows. Success will depend on demonstrating comparable or better leak rates than staple-free devices under real-world conditions.

Adverse Reactions & Cytotoxicity of Some Synthetic Glues

Regulators issued safety notices following dermatitis and dehiscence cases linked to cyanoacrylate overexposure. Hospitals tighten evaluation criteria, especially for paediatric and immunocompromised cohorts. Manufacturers reformulate catalysts, add buffering agents, and publish post-market surveillance data to rebuild confidence. Bio-resorbable biopolymer lines receive favourable clinical commentary, but longer validation timelines delay revenue ramp. Firms that invest in transparent adverse event reporting expedite approvals and foster trust among surgical teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engineered Adhesives Challenge Natural Primacy

Natural biomaterials dominated surgical glue market share at 58.90% in 2025, reflecting clinician familiarity with fibrin and collagen compositions that align with innate healing pathways. Their leadership is visible in neurosurgery, where fibrin sealants achieved 92.1% watertight closure versus 38% for sutures. Nonetheless synthetic and semi-synthetic lines are on course to expand at a 12.62% CAGR to 2031, driven by cyanoacrylate blends that bond rapidly and hydrogels that swell to fill irregular voids. Polyurethane and elastomeric chemistries capture specialised cardiothoracic niches where elastic modulus must match beating tissue. Polymeric hybrid platforms further narrow the performance gap by embedding biologic peptides within synthetic scaffolds. As these materials gain clinical validation, the surgical glue market size attributed to synthetic products is expected to overtake biologics in high-acuity service lines after 2028.

Natural glues retain an edge in regulatory clearance due to extensive safety histories, which simplifies hospital value analysis committee reviews. They also fit green procurement policies, because manufacturing leverages renewable raw materials. Conversely, synthetic suppliers tout batch-to-batch consistency and longer shelf stability that appeal to large integrated delivery networks. Guidance from the PMDA encourages dual sourcing to ensure continuity during plasma shortages. Vendors that masterfully blend bio-resorbability with tensile strength will consolidate leadership positions in this intensifying duel between nature and chemistry.

By Application: Cosmetic Surgery Disrupts Cardiovascular Leadership

Cardiovascular surgery currently commands 32.10% of the surgical glue market size thanks to relentless demand for aortic root and bypass procedures that require rapid hemostasis under anticoagulation. Elastomeric sealants that achieve 88% success at hemostasis form essential components of cardiac theatre kits. Cosmetic surgery, however, is the fastest-rising application, forecast to grow at a 11.54% CAGR as global middle classes seek elective enhancements that prioritise scar minimisation. Surgeons in aesthetic clinics prefer transparent cyanoacrylate films that obviate suture removal and enable showering within 24 hours. Orthopaedics leverages calcium-compatible glues that anchor grafts without metallic screws, and pulmonary teams employ Progel to reduce air leaks by 77% compared with controls. In spinal and cranial surgery, polyethylene glycol hydrogels achieve near-universal leak prevention which secures reimbursement despite higher unit costs.

Procedural reimbursement influences uptake across applications. Cardiovascular surgeons often benefit from diagnosis-related group add-ons that cover sealant costs, but cosmetic surgeons pass expenses directly to patients who accept premiums in exchange for aesthetic outcomes. Trauma units value speed of application more than material cost, again favouring synthetic instant bonds. Suppliers fine-tune viscosity and cross-link density to match the fluidic and mechanical demands of each specialty, ensuring they participate in the value creation of every surgical discipline.

By End User: Ambulatory Centres Erode Hospital Dominance

Hospitals retained 64.35% of surgical glue market share in 2025 because complex multi-service institutions perform high-acuity surgeries that rely on diverse adhesive types. They adopt smart dispensers with RFID cartridges to track consumption, aligning with infection-control audits. The setting also rewards bio-resorbable products that shorten readmissions by avoiding foreign body reactions. Ambulatory surgical centres are nevertheless on track to grow at a 9.18% CAGR through 2031 as reimbursement shifts favour same-day discharge. Cosmetic and ophthalmic procedures dominate their case mix, and both rely heavily on fast-setting skin adhesives that support early patient ambulation.

Growth in ambulatory environments drives package redesign toward single-dose vials that reduce waste. Suppliers collaborate with group purchasing organisations to bundle consumables across multiple outpatient sites. Specialty trauma centres and emergency departments represent emerging niches where pre-filled syringes facilitate rapid deployment during golden-hour interventions. As outpatient volume rises, the surgical glue market size attributable to non-hospital facilities will increasingly shape manufacturer pricing and distribution strategy.

Geography Analysis

North America led the global landscape with 38.85% surgical glue market share in 2025. High procedure volumes within United States academic medical centres, favourable CMS coverage, and FDA clearance of innovations such as Cutiva PLUS in August 2024 underpin the region’s primacy. Canadian health systems adopt similar adhesives through reciprocal regulatory pathways, while Mexico expands private hospital capacity that sources technology via cross-border distributors. Market leaders co-locate clinical research units near U.S. teaching hospitals to accelerate post-market studies and guideline inclusion.

Asia-Pacific is projected to post the fastest 9.09% CAGR through 2031. Japan’s PMDA streamlined review process shortens approval cycles for high-risk medical devices including bio-resorbable glues, stimulating domestic R&D collaboration. China’s hospital build-out raises demand for trauma sealants, and provincial governments allocate budgets for robotic suites that require precision adhesives. India’s medical tourism growth spurs aesthetic and cardiac surgeries, fostering import demand. South Korea and Australia reinforce regional momentum via early adoption of sensor-guided dispensers in tertiary centres.

Europe remains a mature yet innovation-friendly environment. EMA harmonisation allows rapid multi-country launches of PEG hydrogels that prevent cerebrospinal leaks. Germany and France favour products that meet strict biocompatibility and sustainability criteria, catalysing interest in green-OR adhesives. The United Kingdom’s NHS procurement consortia negotiate value-based contracts that bundle sealants with laparoscopic toolkits, thus shaping supplier margins. Middle East and Africa progress at varied paces; Gulf states invest in robotics-ready operating rooms, while sub-Saharan markets emphasise trauma adhesives for road-traffic injury response. South American growth concentrates in Brazil, where ANVISA alignment with ISO 10993 accelerates clearance of polyurethane and fibrin blends that serve orthopaedic and cardiothoracic procedures.

Competitive Landscape

Market concentration is moderate. Ethicon, Medtronic, and Baxter collectively anchor portfolio depth and global distribution. Ethicon markets the DERMABOND family and invests in mesh-adhesive hybrids that shorten closure times in laparoscopic surgery. Baxter’s TISSEEL fibrin line holds entrenched neurosurgical loyalty. Medtronic leverages its cardiac footprint to bundle sealants with ventricular assist and valve repair systems. H.B. Fuller strengthened its medical adhesive unit through the 2024 acquisitions of Medifill and GEM, adding hydrogel and polyurethane chemistries that complement industrial know-how.

Emerging players target niches. Resivant Medical gained FDA clearance for Cutiva adhesives that fuse cyanoacrylate strength with silicone flexibility, giving surgeons a skin-level bond that stretches with underlying tissue. Integra LifeSciences publishes economic data demonstrating cost savings of PEG hydrogels over fibrin in posterior fossa surgery, bolstering tender success across Europe. Biodegradable polymer start-ups in Boston and Berlin raise venture funding to propel green-OR pipelines into first-in-human trials by 2026.

Digital integration becomes the next battleground. Leading companies pair RFID cartridges with cloud dashboards that monitor usage, flag expiration dates, and generate auto-reorder triggers. Robotics system vendors collaborate with adhesive formulators to validate no-drip application through 8-mm cannulas. Global health systems seeking supply resilience oblige suppliers to expand multi-continent manufacturing footprints. The net effect is a competitive environment where scale, innovation cadence, and proof-of-value dictate long-term share capture.

Surgical Glue Industry Leaders

CryoLife Inc.

Integra LifeSciences Corporation

Baxter International Inc

Advanced Medical Solutions Group plc

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space in surgical glue is widening where providers want faster, more standardized closure while managing adverse-reaction scrutiny and tighter ambulatory reimbursement. Topical skin approximation continues to attract line extensions through the FDA Class II 510(k) pathway, supported by 2025 clearances for CUTIVA Topical Skin Adhesive/CUTIVA PLUS (Resivant Medical, K250950) and BondEase 2 (OptMed, K243990). This is creating room for differentiated delivery formats (single-dose, prefilled, and controlled-dispense systems), alongside formulations positioned around lower cytotoxicity and easier protocol standardization across hospital networks and outpatient sites.

Higher-acuity use cases keep opportunity concentrated in hemostasis and internal sealing, where regulatory and clinical evidence requirements are more demanding but pricing power is typically stronger. Ethicon received FDA PMA (P240035) in December 2025 for ETHIZIA as an absorbable hemostatic agent adjunct in open liver surgery, reinforcing investment and commercialization focus on complex bleeding indications. On the biologics side, Grifols received FDA approval in October 2024 to extend a plasma-protein based fibrin sealant indication to pediatric surgical bleeding, supporting portfolio strategies centered on indication expansion and pediatric formulary wins. Supply resilience also remains a practical white-space for plasma-derived and sterilized products, highlighted by CryoLife (Artivion) obtaining an FDA approval supplement (P010003 S042) in March 2025 for an alternate sterilization site for BioGlue Surgical Adhesive, aligning with procurement demand for continuity and dual sourcing.

Recent Industry Developments

- June 2026: Advanced Medical Solutions Group plc reported advanced discussions with H.B. Fuller regarding a potential acquisition, with the board recommending the approach to shareholders. The transaction, if completed, would bring a larger chemicals and adhesives owner closer to surgical sealants and cyanoacrylate devices, potentially reshaping investment capacity and cross-category bundling in wound closure.

- December 2025: Ethicon received FDA Premarket Approval (PMA P240035) for ETHIZIA, an absorbable hemostatic agent indicated as an adjunct to hemostasis in open liver surgery. The approval strengthens Ethicon's biosurgery portfolio in high-acuity procedures where clinical evidence and regulatory barriers are higher, influencing competitive positioning in hemostasis-adjunct products adjacent to surgical glues and sealants.

- July 2024: Advanced Medical Solutions Group plc completed the acquisition of Peters Surgical for an initial cash payment of EUR 132.5 million, adding specialty surgical sutures, mechanical haemostasis, and internal cyanoacrylate devices. The deal broadened AMS's platform across closure and tissue repair, supporting cross-selling strategies where hospitals prefer integrated procurement of sutures, sealants, and adhesives.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The surgical glue market is defined as revenue generated from medical-grade adhesives used in surgeries for tissue bonding, sealing, and wound closure, where the product is applied inside the operating or procedural setting and billed as a surgical consumable.

Scope exclusions: This sizing excludes non-medical industrial adhesives and routine consumer wound-closure products sold mainly for home first-aid use.

Segmentation Overview

- By Product Type

- Natural

- Fibrin

- Collagen

- Gelatin

- Synthetic & Semi-synthetic

- Cyanoacrylate

- Polymeric Hydrogel

- Urethane-based Adhesive

- Natural

- By Application

- Cardiovascular Surgery

- Orthopedic Surgery

- General Surgery

- Cosmetic Surgery

- Pulmonary Surgery

- Central Nervous System Surgery

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear demand setting for surgical procedures where glues are typically used, and then matching it with product and pricing signals. We refer to public sources such as the US FDA device and safety databases, CDC procedure and healthcare utilization statistics, and OECD health statistics to anchor procedure volumes and care settings.

To keep the product view grounded, published clinical literature in peer-reviewed journals, as well as guidance and resources from the World Health Organization and major surgical societies, are reviewed for use patterns, indications, and adoption constraints. Company filings, annual reports, and investor presentations help confirm portfolio exposure, regional priorities, and broad revenue direction. In parallel, paid subscriptions for company financials and intelligence, news and financials, and patent databases are used selectively to cross-check timelines and technology shifts. These desk sources are illustrative, and many other public and paid references were used for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary inputs are taken through expert interviews and structured surveys with manufacturers, distributors, and clinical stakeholders who influence product selection and usage. We use these discussions to confirm procedure-level usage, price bands, hospital procurement behavior, and the pace of switching between synthetic and natural formats, with coverage across APAC, EMEA, and the Americas to reduce single-region bias.

We also use the respondent input to tighten the assumptions on where surgical glue is clinically acceptable versus where hospitals continue to favor sutures or staples.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 47% |

| Mid tier: 44% | Functional/Unit leaders: 42% | EMEA: 31% |

| Smaller Players: 22% | Managers: 43% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure volumes and care-setting mixes are reconstructed from health statistics, and then converted into glue demand using adoption and usage assumptions. To keep the totals realistic, we corroborate outputs with selective bottom-up checks, such as sampled average selling price ranges multiplied by estimated unit use in high-volume procedures, followed by distributor and channel sanity checks.

Key inputs in the model include the number of relevant surgeries by specialty, the share of procedures where glue is clinically acceptable versus sutures or staples, average units used per procedure, and region-level pricing bands that reflect tendering and hospital purchasing. We also track the mix shift between natural and synthetic formats, reimbursement sensitivity in higher-cost indications, and regulatory or safety events that can change adoption for specific chemistries.

Forecasting is done using multivariate regression supported by scenario analysis, where procedure growth, aging population signals, minimally invasive surgery trends, and pricing pressure are treated as the main drivers. When primary inputs show a data gap for smaller countries or sub-specialties, proxy ratios are applied from comparable markets and then adjusted using interview-based adoption differences before finalizing the series.

Data Validation & Update Cycle

Validation is done by triangulating model outputs against independent signals, including procedure growth rates, reported category momentum in public company disclosures, and visible price direction in hospital procurement discussions. Outliers are flagged through variance checks across regions and product types, and then reviewed in more than one analyst pass before sign-off.

When large deviations appear, we re-contact interviewees to confirm whether the shift is driven by a real adoption change, a pricing move, or a one-time regulatory or supply event. The report is refreshed annually, and interim updates are triggered when material events occur. Before delivery, a final review pass is completed so the numbers reflect the latest available information.

Mordor Intelligence's Surgical Glue Market Size Compared With Other Published Estimates

Published market values for surgical glue often do not match because different studies count different product sets, use different base years, and apply different pricing and adoption assumptions. Some sources also mix procedure-related sealants with general wound-closure glue, which can widen the reported totals.

The biggest gaps typically come from whether the scope counts only surgical-use products across hospitals and ambulatory surgical centers, or whether adjacent categories and broader clinical settings are added in. Differences also show up in how average selling prices are progressed over time, how currency conversion timing is handled, and whether procedure growth is validated with real-world surgeon and procurement feedback before forecasting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.28 B (2026) | |

| Industry Publisher A | USD 3.42 B (2025) | Uses a different base year and a longer horizon, and its product list appears to bundle multiple adhesive and sealant families with broader care-site coverage, which can lift the starting value compared with a surgery-only demand pool. |

| Market Report B | USD 3.80 B (2024) | Shows a higher early-year value that likely reflects wider inclusion of clinical applications and faster assumed adoption, and the large long-term forecast suggests more aggressive price and penetration growth without the same level of procedure-based cross-checks. |

The spread is mainly explained by scope and timing, since the 2026 figure is tied to surgical procedures and validated price bands, while some other estimates start earlier and expand the counted use cases. By keeping the demand pool anchored to procedure volumes, aligning currency timing, and re-checking adoption assumptions with clinical and procurement inputs, the market total remains traceable to clear steps, a choice applied by Mordor Intelligence near the end of the modeling workflow.

Key Questions Answered in the Report

What is the current surgical glue market size and growth outlook?

The surgical glue market size is USD 3.28 billion in 2026 and is projected to reach USD 4.57 billion by 2031 at a 6.83% CAGR.

Which product category leads the surgical glue market?

Natural formulations such as fibrin and collagen glues held 58.90% market share in 2025, but synthetic alternatives are growing the fastest at a 12.62% CAGR.

Why are cosmetic surgery adhesives growing rapidly?

Cosmetic procedures prioritise minimal scarring and quick recovery. Advanced cyanoacrylate films meet these needs, driving a 11.54% CAGR in the cosmetic segment.

How does robotic surgery influence adhesive design?

Robotic platforms require low-viscosity, precisely metered adhesives that can be applied through narrow trocars, prompting manufacturers to develop formulations compatible with automated dispensers.

Which region offers the highest growth potential for surgical glue suppliers?

Asia-Pacific shows the fastest regional CAGR at 9.09% through 2031 due to expanding hospital infrastructure, rising trauma volumes, and streamlined regulatory pathways in Japan and China.

Page last updated on: