Tissue Engineered Skin Substitute Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

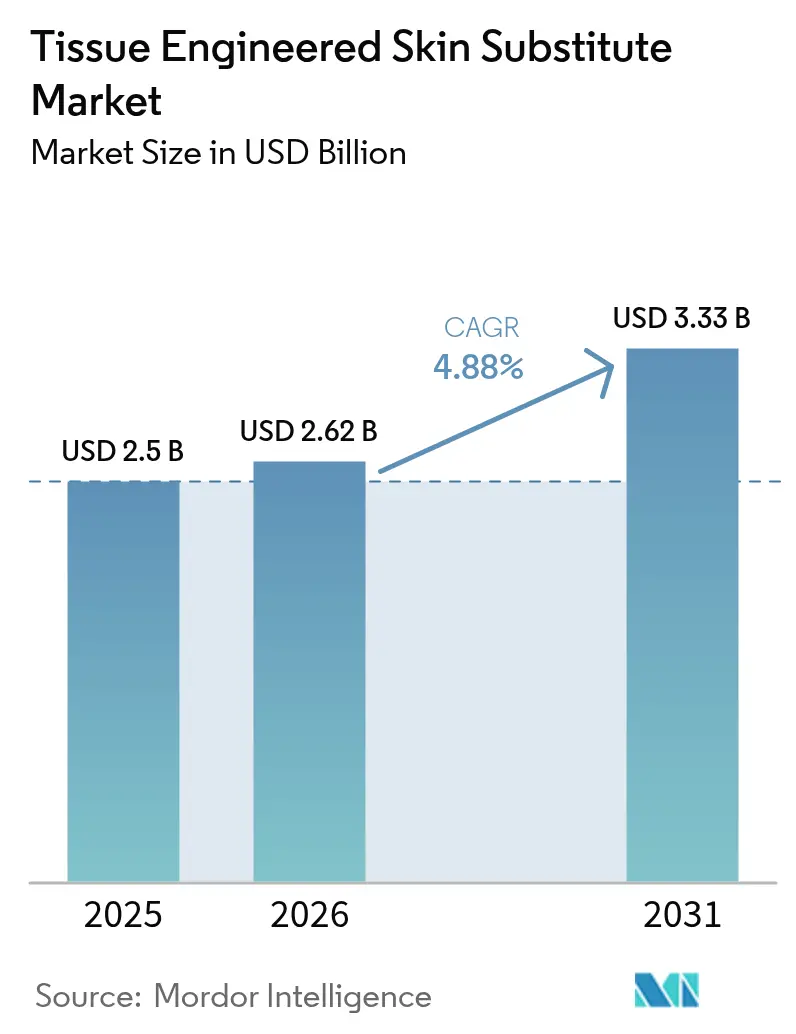

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Engineered Skin Substitute Market Analysis by Mordor Intelligence

tissue-engineered skin substitutes market size in 2026 is estimated at USD 2.62 billion, growing from 2025 value of USD 2.5 billion with 2031 projections showing USD 3.33 billion, growing at 4.88% CAGR over 2026-2031. Adoption has moved beyond pilot studies into routine care as reimbursement becomes predictable and clinical guidelines mature. Integrating 3D bioprinting with traditional tissue-engineering expands therapeutic scope yet forces manufacturers to modernize quality-control systems. Biosynthetic scaffolds gain momentum because they unite biologic compatibility with the consistency of synthetic chemistry, addressing batch-to-batch variability. Investors fund automated, closed-loop manufacturing lines that promise lower contamination risk and faster release times, anchoring long-run cost advantages. Across regions, North America keeps volume leadership through robust insurance coverage, while Asia Pacific records the steepest unit gains on the back of government hospital upgrades and demographic shifts that elevate chronic-wound incidence.

Key Report Takeaways

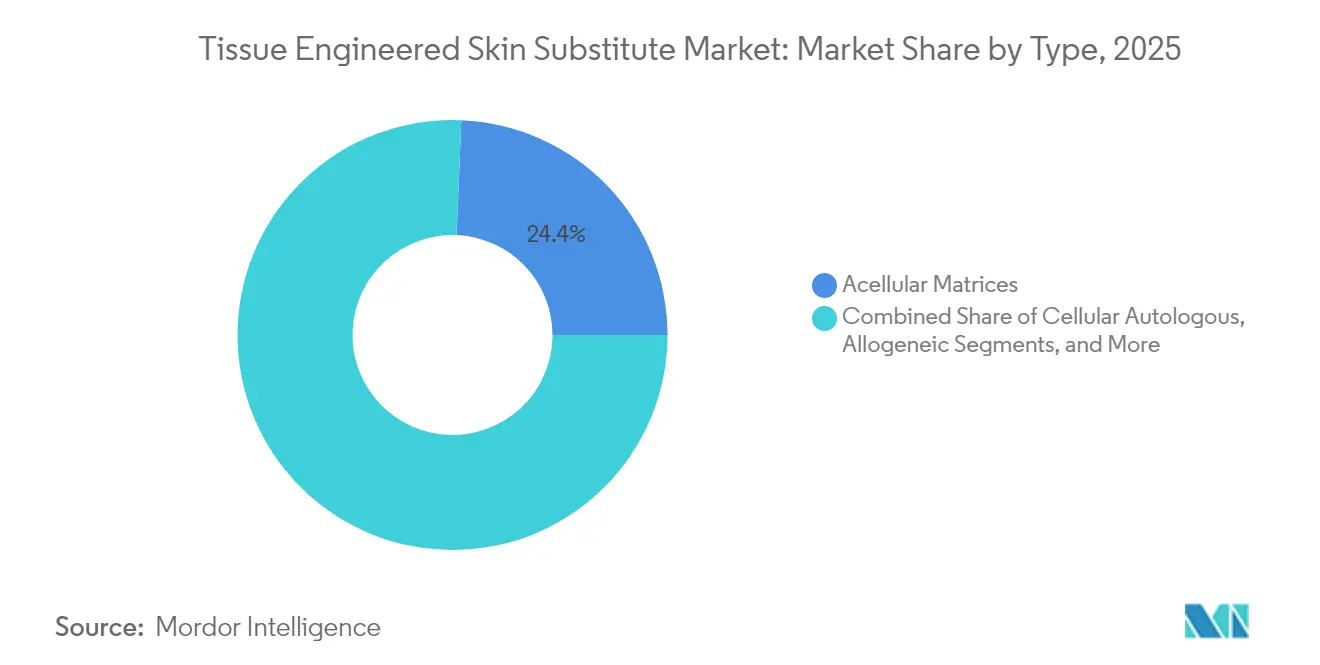

- By construct type, acellular matrices led with a 24.35% market share of tissue-engineered skin substitutes in 2025; cellular autologous constructs are forecast to post the fastest 13.10% CAGR through 2031.

- By product material, natural and biological substances captured 32.85% revenue in 2025, whereas biosynthetic variants are expanding at an 11.05% CAGR.

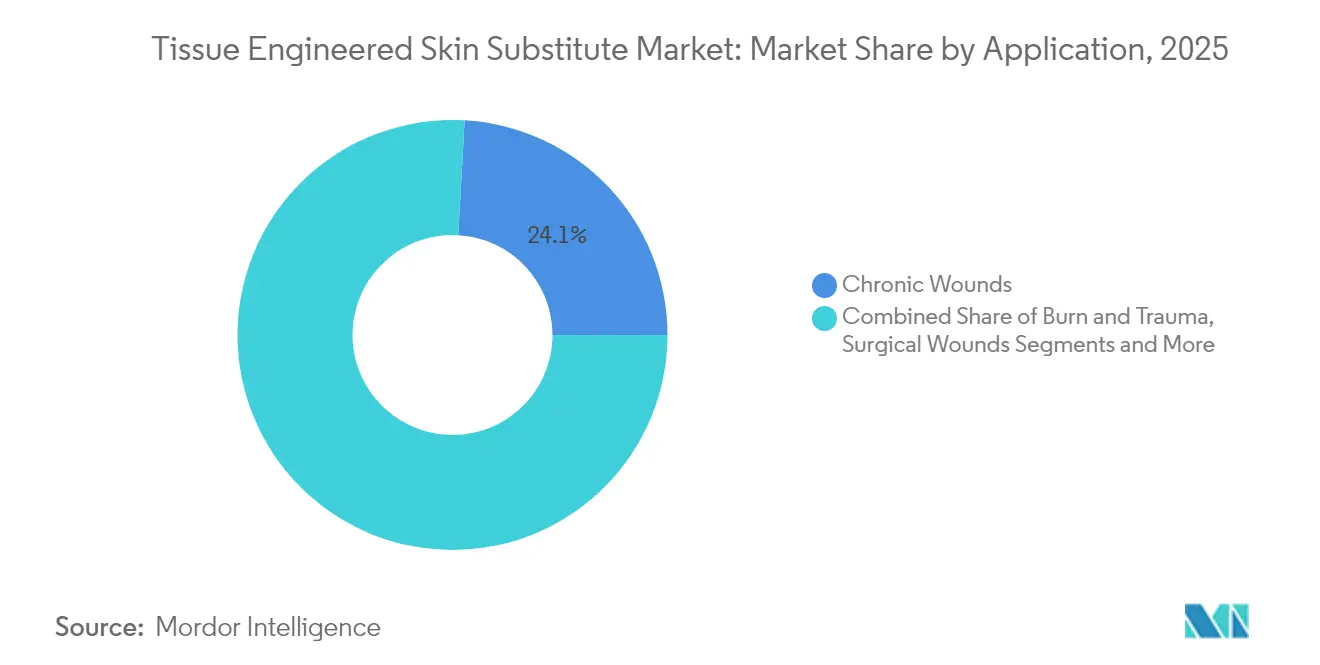

- By application, chronic wounds comprised 24.10% of the tissue-engineered skin substitutes market size in 2025, and diabetic foot ulcers are on track for a 10.98% CAGR.

- By end-user, hospitals commanded 23.10% revenues in 2025, yet home healthcare is climbing at a 8.85% CAGR as point-of-care tools mature.

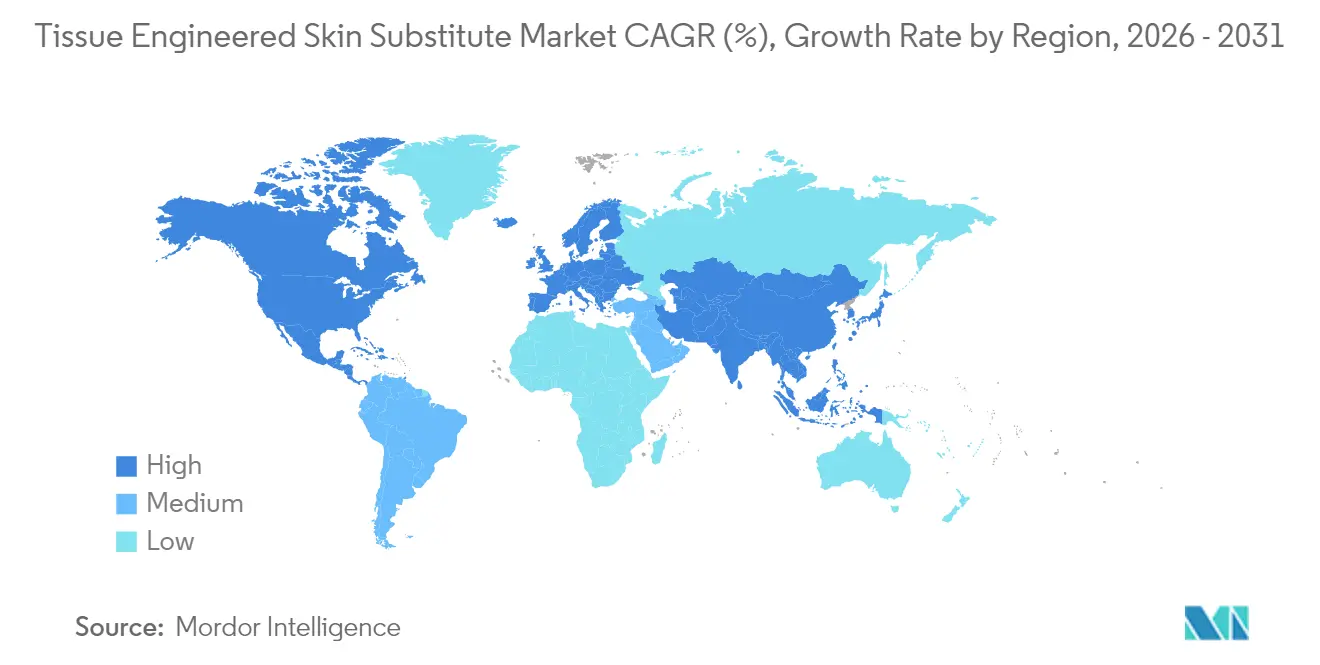

- By geography, North America secured a 29.60% market share in 2025 for tissue-engineered skin substitutes, while Asia Pacific is projected to deliver a 9.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tissue Engineered Skin Substitute Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic wounds increasing | +1.20% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Higher burn & trauma incidence | +0.80% | Stronger impact in developing economies | Medium term (2-4 years) |

| Adoption of 3D‐bioprinting | +0.70% | Starts in North America & EU, spreading to APAC | Medium term (2-4 years) |

| Aging population with fragile skin | +0.90% | Developed economies | Long term (≥ 4 years) |

| Growth in regenerative-medicine funding | +0.50% | Primarily North America & EU | Short term (≤ 2 years) |

| Veterinary crossover demand | +0.30% | Early uptake in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence Of Chronic Wounds

Roughly 6.7 million people in the United States live with chronic wounds, generating treatment outlays exceeding USD 50 billion each year. As 21% of Americans are expected to be 65 or older by 2040, comorbidities such as diabetes and vascular disease further complicate care. Hospitals, therefore, invest in advanced substitutes that shorten healing time and prevent costly infections. Real-world databases documenting reduced readmissions strengthen payer confidence, encouraging broader formulary inclusion.

Rising Burn & Trauma Incidence

Thermal, chemical, and electrical burns create an immediate need for biologic coverage. FDA clearance of AVITA Medical’s RECELL GO system in 2024 provided an autologous spray-on therapy that lessens donor-site morbidity and matches pigmentation. Defense and industrial-safety budgets fund similar platforms, driving procurement beyond specialized burn units into regional trauma centers.

Rapid Adoption Of 3D-Bioprinting Workflows

Bioprinting converts manual graft assembly into automated, layer-by-layer deposition of living cells, hydrogels, and growth factors. Embedded printing now forms perfusable channels inside thick constructs, resolving diffusion limits that once capped graft thickness.[1]ScienceDirect Editors, “Embedded 3D Bioprinting Techniques,” sciencedirect.comAutomation also improves batch-to-batch reproducibility, a quality attribute embraced by regulators validating manufacturing consistency.

Aging Population with Fragile Skin & Comorbidities

Senescent cells accumulate in aged skin, secreting inflammatory molecules that stall epithelial migration and angiogenesis.[2]Frontiers Editors, “Senescent Cells in Aged Skin,” frontiersin.org As older patients require longer healing times, clinicians turn to substitutes enriched with vascularization cues. Public insurers incentivize use because faster closure curbs hospital stay length and reduces antibiotic use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement in emerging markets | -0.60% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Inability to recreate skin appendages | -0.50% | Developed markets | Long term (≥ 4 years) |

| Donor‐tissue supply bottlenecks | -0.40% | North America & Europe | Medium term (2-4 years) |

| Regulatory ambiguity for point-of-care printing | -0.40% | Highest in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement in Emerging Markets

Many developing economies prioritize primary care over premium wound treatments, delaying uptake despite high clinical need. Absence of formal health-technology assessment limits systematic value analysis, and public hospitals often default to gauze and saline. Manufacturers now design cost-controlled variants specifically for these regions, though lower margins threaten reinvestment in R&D.

Regulatory Uncertainty For Autologous Point-Of-Care Printing

Autologous grafts produced inside hospitals blur boundaries among devices, biologics, and medical practice. When processing exceeds minimal manipulation, the FDA regulates the output as a drug, triggering expensive trials.[3]Journal of Translational Medicine Editors, “Regulatory Issues in Autologous Therapies,” translational-medicine.biomedcentral.com Many institutions lack GMP suites, restricting accessibility and discouraging venture capital for mobile bioprinters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cellular Innovation Challenges Matrix Dominance

Acellular matrices commanded 24.35% tissue-engineered skin substitutes market share in 2025 due to easier sterilization and off-the-shelf logistics. Cellular autologous grafts, however, are registering a 13.10% CAGR, driven by personalized medicine trends and reduced immunogenicity. Hospitals with dedicated tissue labs deploy these solutions for ulcers unresponsive to medicines. RECELL GO mini, approved in December 2024, treats wounds up to 480 cm² with limited donor harvest, spotlighting how automation lowers resource needs. As volumes grow, economies of scale are expected to narrow cost gaps, nudging market preference toward bespoke constructs.

Composite dermo-epidermal products remain technically sophisticated but capacity-constrained because multilayer fabrication demands strict environmental control. Cellular allogeneic options occupy a midpoint, balancing shelf-readiness with biologic signaling, yet donors must match pathogen-screening regulations that complicate logistics. Industry investment, therefore, favors bio-printed cellular autologous platforms that pair point-of-care speed with immune compatibility.

By Product Material: Biosynthetic Innovation Disrupts Natural Dominance

Natural biological scaffolds, including bovine and porcine dermis, captured 32.85% revenues in 2025. Their track record and known safety profiles smooth hospital committee approvals. Supply limitations and animal-origin sensitivities, though, stimulate an 11.05% CAGR in biosynthetic substitutes that combine recombinant human collagen with robust polymers. Hospitals appreciate consistent mechanical strength and predictable degradation curves, which ease surgeon training.

Marine collagen innovations extend material diversity. Kerecis leveraged fish-skin matrices rich in omega-3 lipids and gained quick Medicare coding in 2025, illustrating payer openness to sustainable biomaterials. Meanwhile, purely synthetic meshes retain cost advantages for high-volume burns and emergent use in field hospitals. Hybrid biosynthetic platforms now dominate R&D pipelines, aiming to mirror biologic cues while ensuring industrial scalability.

By Application: Diabetic Complications Drive Chronic-Wound Innovation

Chronic wounds formed 24.10% of the tissue-engineered skin substitutes market size in 2025, yet diabetic foot ulcers are on an 10.98% CAGR trajectory through 2031. Hyperglycemia impairs leukocyte function and angiogenesis, prompting integration of antimicrobial peptides and vasodilators into graft design. The FDA issued 2024 guidance easing diabetic-foot infection drug trials, indirectly encouraging combination products.

Burns and acute trauma remain revenue heavyweights in tertiary centers because immediate skin coverage mitigates fluid loss and scarring. Surgical wounds constitute a growth pocket as elective orthopedic and cardiovascular procedures rise globally. Cosmetic reconstruction, while niche, commands premium pricing, driving aesthetic-focused formulations that modulate scar architecture and pigment fidelity.

By End-User: Home Healthcare Disrupts Hospital-Centric Models

Hospitals retained a 23.10% revenue share in 2025 owing to established operating theaters and burn units. Home healthcare, however, is advancing at a 8.85% CAGR. Compact, pre-hydrated dressings allow trained nurses to manage changes in patient residences, supported by tele-monitoring apps that flag infection early. U.S. Medicare Administrative Contractors postponed restrictive Local Coverage Determinations in March 2025, granting interim reimbursement stability to home-bound care pathways.

Ambulatory surgical centers (ASCs) also benefit as payers redirect routine grafting away from high-cost inpatient beds. ASCs deploy standardized protocols, reducing turnaround times and lowering per-procedure expense. Specialized burn centers provide leadership for full-thickness injuries that demand multidisciplinary support. Overall, payer efforts to shift care to lower-cost sites underpin long-run demand for easily applied, portable tissue-engineered skin substitutes.

By Manufacturing Technology: Bioprinting Challenges Conventional Methods

Manual assembly dominates 2024 unit output because infrastructure is widespread and regulatory filings are familiar. Still, 3D-printed grafts log the highest growth as programmable deposition customizes thickness, cell density, and vascular architecture. Global 3D bioprinting revenue is forecast to jump from USD 2.24 billion in 2024 to USD 6.82 billion by 2034, underscoring strategic capital flows.

Electrospun nanofibers offer a high surface area that promotes keratinocyte migration, while decellularized matrices preserve natural chemokines without immunologic baggage. Suppliers with closed-cartridge printers now run validation batches under ISO 13485 rules, reducing contamination risk and meeting traceability mandates. The race centers on marrying automated process control with scalable clean-room footprints that fit hospital budgets.

Geography Analysis

North America secured a 29.60% market share in tissue-engineered skin substitutes in 2025, anchored by Medicare codes Q4100–Q4180 and robust private insurance uptake. Venture capital remains plentiful: the U.S. regenerative medicine segment is projected to reach USD 80.74 billion by 2033. The recent postponement of Local Coverage Determinations in 2025 eased near-term reimbursement pressure, letting suppliers focus on outcome-data generation rather than code lobbying. Academic burn units in Boston, San Antonio, and Los Angeles pilot AI-directed dosing schedules, positioning the region at the forefront of evidence-based wound care.

Asia Pacific delivers the fastest rise with a 9.02% CAGR to 2031. China’s wound-care facilities grew from 16 in 2010 to 357 in 2019, showcasing the state's commitment to specialty care. Urban hospitals in Shanghai and Guangzhou test biosynthetic sheets for diabetic ulcers, while provincial clinics deploy cost-trimmed porcine matrices. Japan’s PMDA has published draft guidance clarifying cell-therapy dossiers, accelerating dual approvals for U.S. developers. South Korea funnels Defense Ministry grants into combat wound bioprinting, further enlarging the regional innovation base.

Europe registers moderate expansion as tight health-technology assessments enforce price discipline. Germany’s statutory insurers demand conclusive cost-utility data before listing new grafts, prompting pilot registries to collect real-world evidence. France and the Nordics reimburse biosynthetic matrices that cut nursing time, recognizing long-term savings. The Middle East & Africa feature pockets of rapid uptake in medical tourism hubs such as Dubai, where private hospitals target affluent burn patients. South America’s growth is tied to macro-economic stabilization in Brazil and Colombia, where public insurers gradually allocate budgets for chronic-wound management.

Competitive Landscape

Industry concentration is moderate. Top players command robust distribution yet face agile newcomers exploiting niche science. Smith & Nephew posted 3.8% underlying revenue growth in Q1 2025, driven by GRAFIX PLUS momentum. Geistlich Pharma expanded U.S. exposure via a StimLabs distribution pact, pairing Swiss collagen expertise with domestic sales bandwidth.

Product differentiation defines positioning. Kerecis’ fish-skin grafts leverage intrinsic omega-3 lipids for anti-inflammatory benefits, while AVITA Medical’s spray-on epidermal cells deliver pigment match for cosmetic zones. SolasCure’s enzymatic Aurase Gel earned FDA Fast Track in June 2025 because it targets calciphylaxis ulcers, a small yet high-severity cohort. Automation capacity emerges as a bargaining chip in payer negotiations since it underwrites steady supply and uniform quality.

White-space opportunities span infection-control hybrid dressings and cost-efficient emerging-market lines, though regulatory complexity tempers aggressive scale-outs.

Tissue Engineered Skin Substitute Industry Leaders

Amarantus BioScience Holdings

Organogenesis Inc.

3M Company

Smith & Nephew plc

Tissue Regenix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kerecis obtained rapid Medicare contractor approval for its new fish-skin matrix, increasing clinical accessibility.

- April 2025: AVITA Medical launched Cohealyx, a collagen-based dermal matrix designed to enhance cell migration and vascularization.

- March 2025: Convatec welcomed the postponement of Local Coverage Determinations on tissue-engineered skin substitutes in the United States.

- January 2025: SolasCure received FDA Fast Track Designation for Aurase Wound Gel, addressing calciphylaxis ulcers.

Global Tissue Engineered Skin Substitute Market Report Scope

Skin substitutes are the most straightforward of the tissue-engineered organ constructs, and have been developed over many years for the testing of commercial products, therapeutics, and as models of skin biology and pathology. They are based on the ability of fibroblasts and keratinocytes to form a skin-like structure spontaneously, but have been extended by the inclusion of other cell types to provide models of the very wide range of properties displayed by intact skin. The tissue engineered skin substitute market encompasses the production of these constructs on a commercial scale, particularly for therapeutic purposes.

| Cellular Autologous |

| Cellular Allogeneic |

| Acellular Matrices |

| Composite (Dermo-epidermal) |

| Natural/Biological |

| Synthetic |

| Biosynthetic |

| Collagen |

| Chitosan |

| Hyaluronic Acid |

| PEG & Other Polymers |

| Conventional Manual |

| 3-D Bioprinted |

| Electrospun Nanofiber |

| Decellularized ECM |

| Chronic Wounds | Diabetic Foot Ulcers |

| Venous Leg Ulcers | |

| Pressure Ulcers | |

| Burn & Trauma | Thermal Burns |

| Chemical/Radiation Burns | |

| Surgical Wounds | |

| Cosmetic Reconstruction |

| Hospitals |

| Specialised Burn Centres |

| Ambulatory Surgical Centres |

| Home Healthcare |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Construct Type | Cellular Autologous | |

| Cellular Allogeneic | ||

| Acellular Matrices | ||

| Composite (Dermo-epidermal) | ||

| By Product Material | Natural/Biological | |

| Synthetic | ||

| Biosynthetic | ||

| By Biomaterial Source | Collagen | |

| Chitosan | ||

| Hyaluronic Acid | ||

| PEG & Other Polymers | ||

| By Manufacturing Technology | Conventional Manual | |

| 3-D Bioprinted | ||

| Electrospun Nanofiber | ||

| Decellularized ECM | ||

| By Application | Chronic Wounds | Diabetic Foot Ulcers |

| Venous Leg Ulcers | ||

| Pressure Ulcers | ||

| Burn & Trauma | Thermal Burns | |

| Chemical/Radiation Burns | ||

| Surgical Wounds | ||

| Cosmetic Reconstruction | ||

| By End-User | Hospitals | |

| Specialised Burn Centres | ||

| Ambulatory Surgical Centres | ||

| Home Healthcare | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the tissue-engineered skin substitutes market?

The tissue engineered skin substitutes market stands at USD 2.62 billion in 2026 and is projected to reach USD 3.33 billion by 2031.

Which construct type grows the fastest?

Cellular autologous products record a 13.10% CAGR through 2031, reflecting strong demand for personalized grafts.

Why are biosynthetic materials gaining traction?

Biosynthetic scaffolds marry biologic functionality with manufacturing consistency, driving an 11.05% CAGR over 2026-2031.

Which region offers the highest growth opportunity?

Asia Pacific shows the quickest pace with a 9.02% CAGR due to healthcare infrastructure upgrades and demographic shifts.

How is home healthcare influencing market dynamics?

Home-based wound care rises at a 8.85% CAGR as portable, easy-to-apply substitutes reduce inpatient reliance and cut costs.

Page last updated on: