Cartilage Repair/Regeneration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

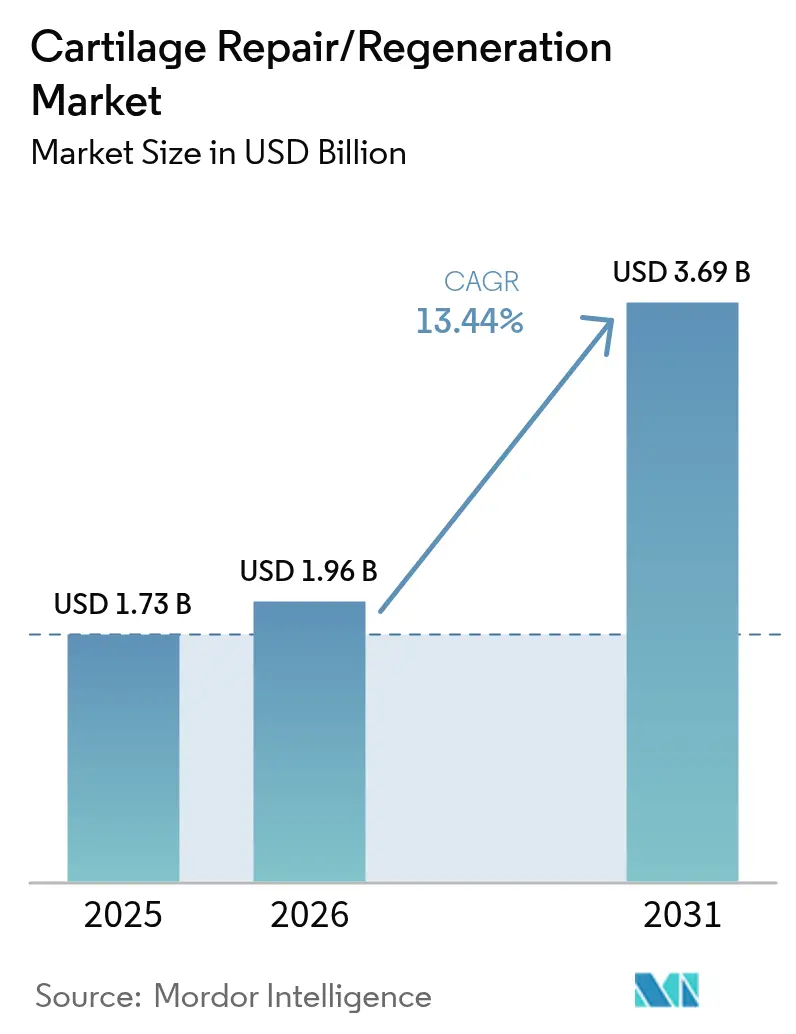

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 13.44% CAGR |

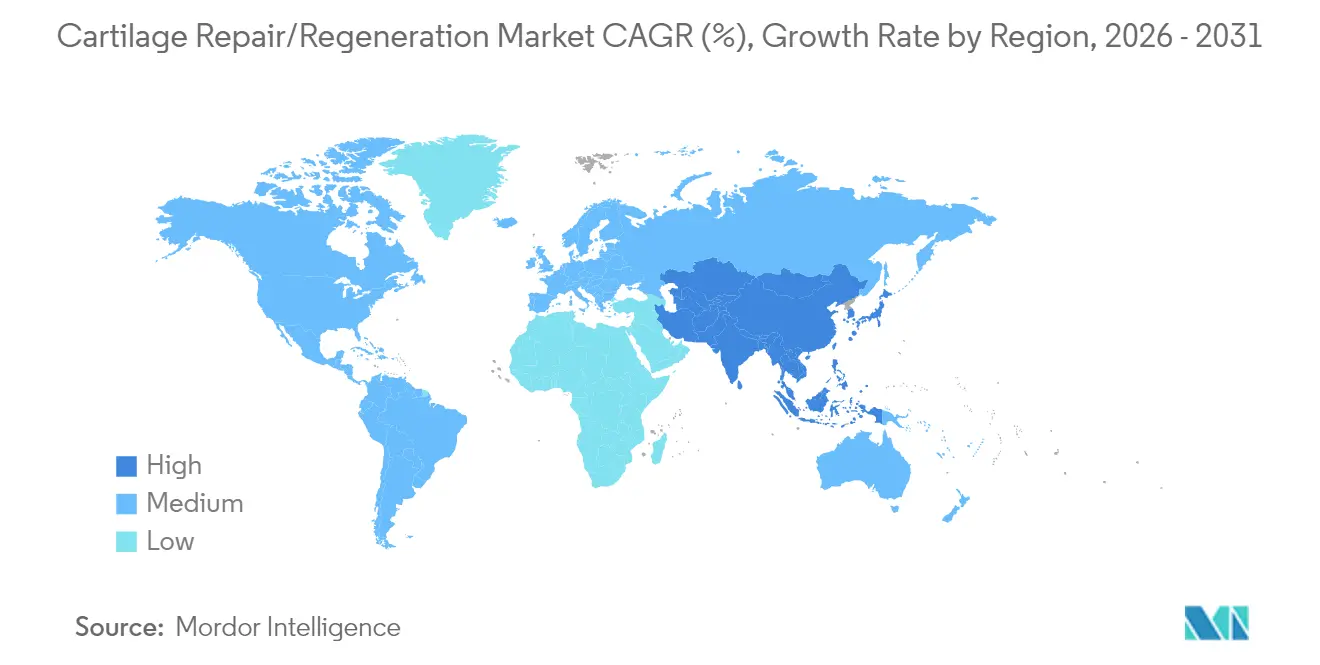

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cartilage Repair/Regeneration Market Analysis by Mordor Intelligence

Cartilage repair/regeneration market size in 2026 is estimated at USD 1.96 billion, growing from 2025 value of USD 1.73 billion with 2031 projections showing USD 3.69 billion, growing at 13.44% CAGR over 2026-2031. Demographic aging, rising obesity, and sports injury volumes expand the patient pool, while technological advances in cell-based implants and tissue-engineered scaffolds improve clinical outcomes. Outpatient arthroscopic procedures shorten recovery times and lower costs, reinforcing payer and provider adoption. North America leads revenue generation, but Asia-Pacific posts the fastest expansion as healthcare infrastructure and disposable incomes climb. Competitive activity is steady, with large device firms acquiring niche innovators to secure next-generation technologies.

Key Report Takeaways

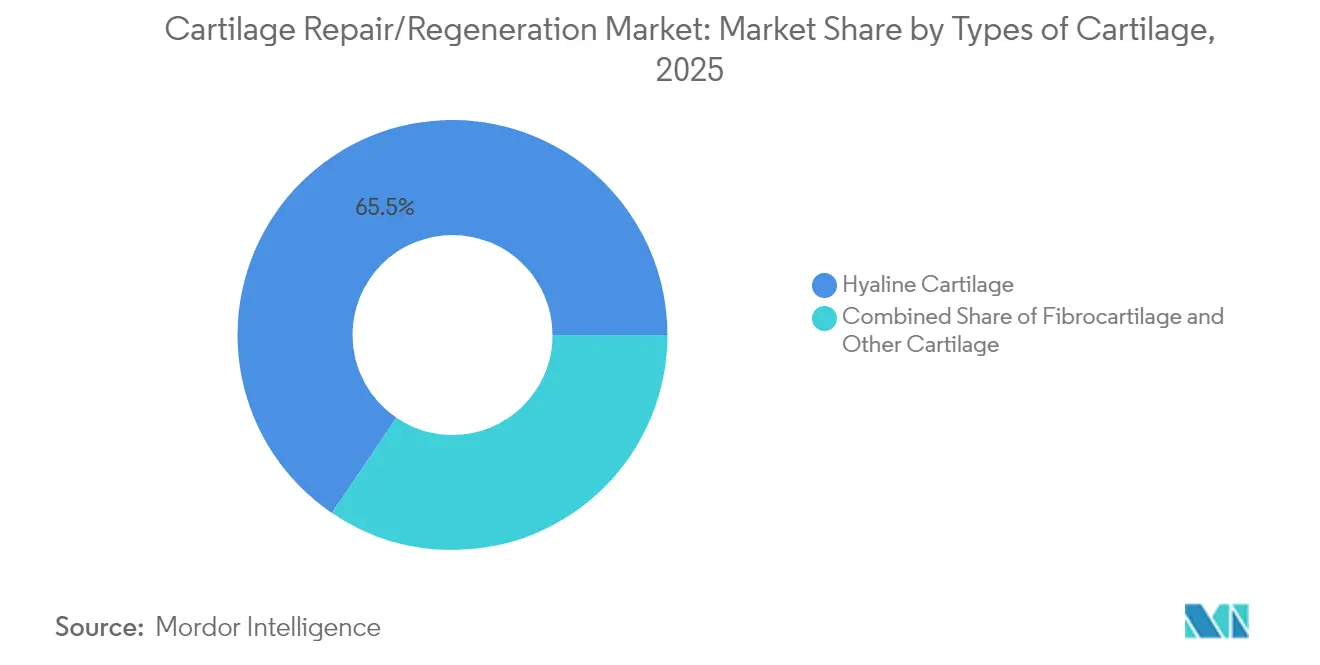

- By cartilage type, hyaline tissue dominated with 65.52% cartilage repair/regeneration market share in 2025, whereas fibrocartilage is projected to grow at a 14.02% CAGR through 2031.

- By treatment modality, cell-based approaches captured 61.72% of the cartilage repair/regeneration market size in 2025; non-cell-based options record the highest forecast growth at 14.21% CAGR.

- By treatment type, palliative procedures held 54.66% of revenue in 2025, while intrinsic repair stimulus methods are expected to accelerate at 13.98% CAGR.

- By surgical technique, chondroplasty and microfracture accounted for 27.74% of the cartilage repair/regeneration market size in 2025; matrix-induced ACI is set to lead growth at 14.55% CAGR.

- By application site, knee interventions commanded 49.62% of 2025 revenue, yet ankle repairs should advance fastest with 14.83% CAGR.

- By end user, hospitals and clinics controlled 61.85% of spending in 2025; ambulatory surgical centers are forecast to expand at 14.56% CAGR.

- By geography, North America contributed 44.72% of 2025 sales, while Asia-Pacific is projected to post a 15.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cartilage Repair/Regeneration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Heart Failure & Other Cardiac Disorders | +1.5% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapidly Expanding Geriatric Population And Sedentary Lifestyles | +0.8% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Break-Through Product Innovations | +0.6% | North America & Europe first, then Asia-Pacific | Medium term (2-4 years) |

| Favourable Reimbursement & HF Disease-Management Mandates In OECD Nations | +0.4% | OECD countries, spillover to emerging markets | Medium term (2-4 years) |

| AI-Driven CRT Optimisation & Predictive Analytics Platforms | +0.3% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Commercialisation Of Leadless & Modular CRT Systems In Emerging Markets | +0.2% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence of Osteoarthritis and Traumatic Cartilage Lesions

Surging osteoarthritis prevalence, which climbed 132.2% between 1990 and 2022, now affects 7.96% of the global population and drives sustained demand for restorative surgery. Adult cases aged 30-44 exceeded 32.97 million in 2022, underscoring a shift toward younger patients seeking durable repair solutions. Chondral defects afflict 36% of athletes’ knees, creating a sizable cohort that prefers definitive intervention over symptom management [1]Litchfield R et al., “Athlete Knee Chondral Defects,” journals.lww.com. The widening patient base ensures that the cartilage repair/regeneration market remains on an expanding trajectory through the decade.

Surge in Outpatient Minimally Invasive Orthopedic Procedures

Same-day discharge for joint surgeries in the United States rose from less than 1% in 2017 to 30.5% in 2023, demonstrating payer and provider confidence in ambulatory pathways. FDA clearance of MACI Arthro in August 2024 validated arthroscopic delivery of autologous chondrocyte implants, further normalizing outpatient treatment. Ambulatory surgical centers benefit most, displaying a 15.07% CAGR through 2030 as they combine cost savings with better patient convenience. This procedural migration underpins broader adoption across the cartilage repair/regeneration market.

Breakthroughs in Tissue-Engineered Scaffolds and Cell-Based Implants

Nanofiber “dancing molecule” technology from Northwestern University stimulates cartilage formation within hours, signaling future one-step biologic repairs. EU-funded ENCANTO is advancing nasal-septum chondrocyte constructs for knee defects, illustrating public investment in translational science. Clinical trials pairing allogeneic mesenchymal stromal cells with autologous chondrons show superior results to legacy techniques. These innovations collectively raise treatment efficacy and underpin premium pricing within the cartilage repair/regeneration market.

Increasing Participation in High-Impact and Recreational Sports

Soccer alone generated 843,063 lower-extremity injuries between 2014 and 2023, with 47% classified as strains or sprains that often involve cartilage damage. Track and field recorded 128,761 such injuries over the same period, with female athletes facing 58% higher risk. Rising female sports participation broadens demand for ligament and cartilage repair solutions. This youthful, active demographic values rapid return to play, boosting acceptance of advanced regenerative therapies across the cartilage repair/regeneration market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Region Regulatory Requirements And Lengthy Approval Cycles | -0.7% | Global, particularly impacting new market entries | Medium term (2-4 years) |

| High Procedure/Device Cost & Limited Implanter Skill Base | -0.5% | Emerging markets, rural areas in developed countries | Long term (≥ 4 years) |

| Supply-Chain Vulnerability For Rare-Earth Magnets And Semiconductor ICs | -0.4% | Global, with highest impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Rising Clinical Scrutiny Of Non-Responder Rates Spurring CSP Substitutes | -0.3% | North America & Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Implant Costs Limiting Uptake

Stem-cell knee therapy costs range between USD 5,000 and USD 15,000 in South Korea, restricting adoption beyond affluent or insured patients. China’s volume-based procurement cut total hip arthroplasty prices by 50.1%, highlighting intense cost pressure that could spill over to cartilage technologies. Blue Cross payers in the United States mandate stringent criteria for autologous chondrocyte implantation, illustrating reimbursement hurdles. These economic constraints slow penetration in price-sensitive regions, tempering cartilage repair/regeneration market growth.

Lengthy and Complex Regulatory Approval Pathways

The European Medicines Agency requires extensive additional monitoring for 88% of cell and gene therapy products, extending time to market [2]European Medicines Agency, “Additional Monitoring for ATMPs,” ema.europa.eu . In the United States, combination products blending biologics and devices face dual-center review, prolonging timelines and increasing capital needs. Smaller innovators often lack resources for multipronged submissions, postponing commercialization and limiting competitive intensity in the cartilage repair industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Types of Cartilage: Hyaline Dominance Reflects Weight-Bearing Demands

Hyaline tissue held 65.52% of revenue in 2025, confirming its central role in load-bearing joints most vulnerable to degeneration. Bilayer atelocollagen scaffolds now replicate hyaline morphology more reliably, improving long-term outlook for patients. Fibrocartilage, driven by meniscal repair needs, is projected to expand at 14.02% CAGR, supported by advances in collagen-based hydrogels that recruit endogenous stem cells.

The cartilage repair/regeneration market size for hyaline applications is projected to widen further as surgeons prioritize tissue-specific products that enhance integration. Meanwhile, niche elastic-cartilage reconstruction for ear and nasal defects creates incremental volume, diversifying revenue streams across smaller sub-segments.

By Treatment Modality: Cell-Based Therapies Lead Regenerative Revolution

Cell-based solutions captured 61.72% revenue in 2025 through clinical superiority in pain reduction and tissue restoration, as evidenced by meta-analysis reporting standardized mean differences of –1.27 in pain scores . However, cell-free implants should post 14.21% CAGR through 2031 on the strength of off-the-shelf availability and lower cost.

Premium products such as MACI generated USD 46.3 million in Q1 2025 sales, reflecting commercial traction in the United States. Conversely, CARTIHEAL Agili-C offers a cell-free scaffold that reduced total knee arthroplasty risk by 87% at four years. Healthy rivalry between personalized and ready-to-use solutions ensures a balanced growth outlook across the cartilage repair/regeneration market.

By Treatment Type: Palliative Procedures Dominate Current Practice

Palliative options—debridement, lavage, viscosupplementation—accounted for 54.66% of sales in 2025 because they impose minimal procedural complexity and allow rapid symptom relief. Yet intrinsic repair stimulus techniques such as microfracture, autologous chondrocyte implantation, and micro-fragmented adipose injections should climb at 13.98% CAGR.

Ten-year MACI outcomes show durable improvements in function and MRI morphology, spurring clinician confidence. This evidence nudges payers toward reimbursing curative approaches, progressively shifting revenue mix within the cartilage repair/regeneration market.

By Surgical Technique: Microfracture Leads Despite Limitations

Chondroplasty and microfracture retained 27.74% share in 2025 because they require no specialized infrastructure. Matrix-induced ACI, however, is forecast to expand 14.55% CAGR as larger lesion indications and arthroscopic delivery gain traction. FDA-cleared arthroscopic MACI simplifies operating-room workflow, aligning with outpatient migration.

Robotic assistance further refines precision; the global orthopedic robot pool is set to double by 2030. These enablers lay groundwork for scalability, broadening the cartilage repair/regeneration market size among complex cases previously judged inoperable.

By Application Site: Knee Dominance Drives Market Concentration

Knee interventions held 49.62% revenue in 2025, mirroring 364.58 million global knee-osteoarthritis cases. Ankle repairs, buoyed by talar autograft innovations, are poised for 14.83% CAGR as clinical outcomes improve.

The cartilage repair/regeneration market share of knee procedures may dilute slightly as ankle, hip, and shoulder indications mature, yet knees will remain the anchor of procedural volume. Site-specific instruments from Arthrex and others reinforce adoption across multiple joints.

By End User: Hospital Dominance Faces Outpatient Challenge

Hospitals and clinics controlled 61.85% of revenue in 2025 thanks to their capacity for complex, multiphase treatments. Ambulatory surgical centers should grow 14.56% CAGR as arthroscopic techniques shorten stay length.

The cartilage repair industry sees office-based biologic injections emerging as the next frontier, enabling physicians to capture more value and widening access in rural regions with limited surgical capacity.

Geography Analysis

North America produced 44.72% of 2025 revenue, underpinned by FDA clearances and consistent private‐payer reimbursement. Vericel, Arthrex, and Stryker dominate surgeon preference, while Johnson & Johnson’s VELYS unicompartmental knee robot received clearance in June 2024, spotlighting ongoing innovation. Growth remains steady as baby-boomer activity levels sustain procedure volumes.

Asia-Pacific is projected to deliver a 15.02% CAGR, buoyed by infrastructure investment and rising disposable incomes. China’s procurement reforms, which halved implant prices, improve affordability even as regulatory pathways tighten. Japan leverages universal coverage for advanced therapies, whereas South Korea attracts inbound medical tourists for stem-cell knee repairs priced at USD 5,000-15,000. India’s expanding middle class gradually lifts procedure counts despite reimbursement gaps.

Europe sustains innovation momentum through EMA’s advanced therapy framework and EUR 11.3 million ENCANTO funding. Middle East & Africa and South America remain nascent yet compelling as economic development enlarges insured populations, positioning them as long-range demand reservoirs for the cartilage repair/regeneration market.

Regulatory Landscape

Cartilage repair and regeneration offerings span medical devices, biologics, and combination products, so developers typically manage multi-track evidence and quality requirements across regions. In the United States, the FDA Office of Combination Products assigns lead-center jurisdiction based on the principal mode of action, and sponsors may need coordinated IDE and IND pathways for products intended to repair or replace knee cartilage under FDA guidance.

In Europe, many regenerative cartilage solutions fall under the Advanced Therapy Medicinal Product (ATMP) framework (including tissue-engineered medicines) under Regulation (EC) No 1394/2007. Combined ATMPs that include a device component also need to satisfy EU Medical Devices Regulation (EU) 2017/745 conformity requirements, including Article 117 expectations for device evidence in the medicinal dossier. Standards activity continues to shape testing programs, including ISO 10993-6:2026 for local effects after implantation and ISO/TS 21560:2020 (confirmed in 2024) for safety, manufacturing, and quality control expectations for tissue-engineered medical products.

Value Chain Analysis

The value chain begins with biomaterial and biologic inputs, such as collagen matrices, hyaluronic acid, and cell-processing reagents. It then moves through scaffold fabrication, cell sourcing and expansion (autologous or allogeneic where applicable), and sterile packaging under GMP-grade controls. For cell-based cartilage repair products, chain-of-identity and chain-of-custody controls, along with cold-chain logistics, connect centralized manufacturing with time-sensitive distribution to hospitals or ambulatory surgical centers.

Demand is driven by orthopedic surgeons, hospital systems, and ambulatory surgical centers, with distributors and specialized sales teams supporting instrumentation and implant pull-through. Partnership activity highlights how companies rely on regional collaborators to manage commercialization and operational complexity, including Rokit Healthcare partnering with WEGO Group for China and signing a UAE-focused memorandum to validate and commercialize AI cartilage regeneration technology, Cellcolabs aligning with Hong Kong-based CNRM to support a Phase I/II knee osteoarthritis trial, and Regentis Biomaterials collaborating with Humanitas Research Hospital in Italy to build European Centers of Excellence for GelrinC deployment.

Competitive Landscape

The cartilage repair/regeneration market is moderately fragmented. Arthrex, Stryker, and Zimmer Biomet command established portfolios in microfracture and fixation devices. Cell-therapy specialists such as Vericel hold proprietary manufacturing know-how, while CartiHeal brought a first-in-class osteochondral scaffold to market prior to its USD 180 million sale to Smith & Nephew in 2023.

Competition centers on technology and evidence generation. Vericel’s arthroscopic MACI launch creates a short-term edge, whereas Smith & Nephew integrates CartiHeal with its robotics suite for comprehensive knee solutions.

Robotic platforms from Johnson & Johnson and Stryker sharpen surgical precision, fostering hospital loyalty. Off-the-shelf peptides, exosome products, and bioprinted grafts from emerging biotech firms could reset cost structures, intensifying rivalry and quickening product cycles across the cartilage repair/regeneration market.

Cartilage Repair/Regeneration Industry Leaders

Zimmer Biomet

Stryker Corporation

Arthrex, Inc.

Smith & Nephew plc

Vericel Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is expanding as payers and providers look for therapies that show durable joint function improvements and structural cartilage repair, especially for knee lesions that often move from palliative care toward eventual arthroplasty. Clinical differentiation is becoming more evidence-led as longer follow-up datasets mature. Smith+Nephew, for example, released five-year randomized controlled trial data for CARTIHEAL AGILI-C (reported in April 2026), showing higher overall KOOS scores versus surgical standard of care through 60 months, which supports greater surgeon confidence in osteochondral scaffold approaches.

Commercial infrastructure also creates opportunity in the United States as newer restorative implants gain clearer reimbursement paths. Smith+Nephew announced a Category I CPT code for AGILI-C, effective January 1, 2027. In parallel, late-stage cell therapy pipelines broaden the set of potential regenerative options beyond autologous chondrocyte implants, including MEDIPOST reporting Japan Phase 3 success for CARTISTEM (May 2026) and initiating a pivotal US Phase 3 study with first participant treated (July 2026). Scaffold programs such as Regentis Biomaterials GelrinC also advanced site expansion and trial enrollment in 2026, reinforcing opportunities to integrate cartilage restoration into outpatient orthopedic pathways alongside enabling technologies such as arthroscopic delivery workflows and adjacent perioperative solutions.

Recent Industry Developments

- July 2026: MEDIPOST treated the first US participant in a Phase 3 clinical trial of its umbilical cord-derived MSC therapy (CARTISTEM) for knee osteoarthritis. The FDA-approved single pivotal study design positions the program around a defined pathway toward a future biologics license application and raises competitive pressure on established surgical and scaffold-based repair options.

- October 2025: Zimmer Biomet completed its acquisition of Monogram Technologies, adding AI-driven, semi-autonomous orthopedic robotics capabilities with CT-based total knee arthroplasty navigation. The deal strengthens integrated surgical ecosystems that can support cartilage preservation and joint reconstruction workflows across hospitals and ambulatory settings.

- August 2024: The FDA cleared MACI Arthro, validating arthroscopic delivery for autologous chondrocyte implantation procedures. This clearance supports outpatient migration by simplifying operating-room workflow and aligning advanced cartilage restoration with same-day orthopedic care pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from procedures and solutions used to repair or regenerate damaged articular cartilage, including cell-based and non-cell-based approaches used across major joints.

Scope exclusions: We exclude rehabilitation services, general pain management drugs, and non-cartilage orthopedic implants that do not directly restore cartilage tissue.

Segmentation Overview

- By Types of Cartilage

- Hyaline Cartilage

- Fibrocartilage

- Elastic / Other Cartilage

- By Treatment Modality

- Cell-based Therapies

- Non-cell-based / Cell-free Therapies

- By Treatment Type

- Palliative (Debridement, Viscosupplementation)

- Intrinsic Repair Stimulus (ACI, MACI, Micro-fracture)

- By Surgical Technique

- Chondroplasty & Micro-fracture

- Autologous Chondrocyte Implantation (ACI)

- Matrix-induced ACI (MACI)

- Osteochondral Allograft / Juvenile Allograft

- By Application Site

- Knee

- Hip

- Ankle

- Spine

- Other Joints (Shoulder, Elbow, Wrist)

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public healthcare and epidemiology baselines, since cartilage damage demand usually follows osteoarthritis burden and sports injury volumes. We used inputs such as the World Health Organization, the US CDC, the OECD health statistics portal, and national health ministries to capture patient and procedure context.

To connect disease burden to procedure adoption, we also reviewed open clinical guidance and evidence summaries from bodies such as the US National Library of Medicine (PubMed), the FDA device and biologics databases, and orthopedic society publications where accessible. Pricing direction and company positioning were cross-checked using annual reports, investor decks, reputable medical press, and a paid subscription that compiles company financials, patent activity, and news. These sources are not exhaustive, and additional public references were used during analysis to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured questionnaires with orthopedic surgeons, sports medicine specialists, hospital procurement staff, distributors, and product or clinical leaders. Because this is a global market, we ensured views were balanced across mature and developing healthcare systems so the procedure mix, reimbursement direction, and adoption timelines could be normalized, and then checked back against desk assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 14% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where treated patient pools were reconstructed by major joint sites and aligned to procedure rates, and then translated into value using typical per procedure therapy mix and average selling price ranges. Once the first pass totals were formed, they were corroborated using selective bottom-up checks like sampled supplier revenue splits by region, channel feedback on unit volumes, and ASP x volume sanity checks for common techniques.

Key inputs used in the model included osteoarthritis prevalence, sports injury incidence trends, arthroscopy volumes, adoption of cell-based versus non-cell-based techniques, reimbursement coverage signals, and outpatient shift indicators that affect procedure counts and pricing. Forecasts were developed using scenario analysis supported by expert views on regulatory momentum, surgeon training curves, and expected ASP progression for implants and biologics. Where direct procedure data was thin for some countries, we applied proxy indicators such as orthopedic surgery capacity, health spending trends, and regional penetration benchmarks, then re-checked them with interview feedback.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final totals align with real world signals, not just model math. We compared derived values against independent indicators like procedure volumes, device approvals, and pricing direction, and then reviewed outliers by region and by therapy type to confirm they were explainable.

Before sign-off, assumptions and calculations go through stepwise analyst reviews, and follow-up calls are triggered when responses conflict with observed demand or clinical practice patterns. Reports are refreshed annually, and interim updates are made when material events occur (for example, major approvals, reimbursement changes, or sharp pricing moves). Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Cartilage Repairregeneration Market Estimate Compared With Other Published Estimates

Published market values for cartilage repair and regeneration do not always match, even when they are framed as the same topic. Differences usually come from what gets counted as a cartilage therapy, how procedure volumes are estimated, and which year is treated as the starting point.

The main gap comes from scope expansion into broad orthopedic and arthritis treatment revenues, where Mordor Intelligence counts value only when it is tied to cartilage repair or regeneration procedures and their related implant or biologic therapy components, which reduces inflation from adjacent care categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.96 B (2026) | |

| Global Consultancy A | USD 6.28 B (2025) | Uses a wider cartilage repair definition that can fold in broader arthritis and joint disorder treatment revenues, and it anchors sizing to a 2024 base year which lifts the near-term total versus a procedure-linked pool. |

| Industry Publisher B | USD 5.82 B (2024) | Starts from a broad 2024 revenue base and applies a lower growth path that appears to mix repair and general orthopedic care, with limited clarity on how cell-based versus non-cell-based procedure volumes and ASPs are validated by region. |

Taken together, the spread is mainly explained by scope and the way procedure-linked demand is translated into dollars. When the counted revenue is kept tied to cartilage-specific procedures, and key inputs like adoption, pricing, and regional uptake are cross-checked in the field, the resulting market size becomes easier to trace and repeat year over year.

Key Questions Answered in the Report

What is the current size of the cartilage repair/regeneration market and how fast is it growing?

The cartilage repair/regeneration market is valued at USD 1.96 billion in 2026 and is projected to reach USD 3.69 billion by 2031.

Which region leads the cartilage repair/regeneration market?

North America accounts for 44.72% of 2025 revenue owing to early technology adoption and favorable reimbursement.

What segment holds the largest cartilage repair market share by treatment modality?

Cell-based therapies command 61.72% of global revenue due to their demonstrated regenerative benefits.

Why are ambulatory surgical centers growing faster than hospitals?

Outpatient arthroscopic techniques allow same-day discharge, lowering facility costs and driving a 14.56% CAGR for ASCs

Page last updated on: