Vendor-Neutral Archive And PACS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.92 Billion |

| Market Size (2031) | USD 6.94 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vendor-Neutral Archive And PACS Market Analysis by Mordor Intelligence

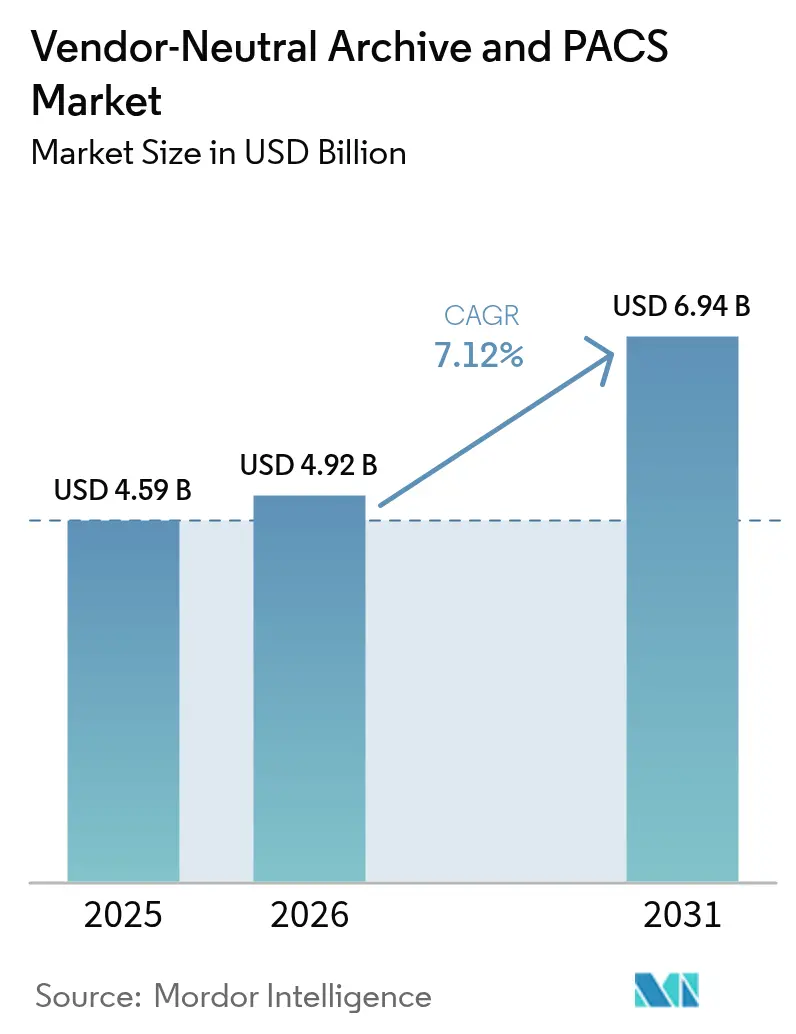

The Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market size was valued at USD 4.59 billion in 2025 and estimated to grow from USD 4.92 billion in 2026 to reach USD 6.94 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Strong momentum arises from accelerating imaging volumes, stricter privacy regulations, and a decisive shift toward interoperable, cloud-enabled imaging ecosystems. Providers are retiring departmental silos in favor of enterprise platforms that serve radiology, cardiology, pathology, and orthopedics, thereby unifying image management and analytics. Competitive intensity is reinforced by consolidation plays such as RadNet’s USD 103 million purchase of iCAD and GE HealthCare’s long-term imaging partnership with Sutter Health across 300+ sites, underscoring an industry pivot toward end-to-end enterprise imaging suites rather than point products. Continued adoption of cloud deployments that promise 30% cost savings, the rise of zero-trust cybersecurity mandates, and over 1,000 FDA-cleared AI tools embedded in imaging workflows collectively sustain future growth for the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.[1]Health Imaging, “FDA has approved over 1,000 clinical AI applications, with most aimed at radiology,” healthimaging.com

Key Report Takeaways

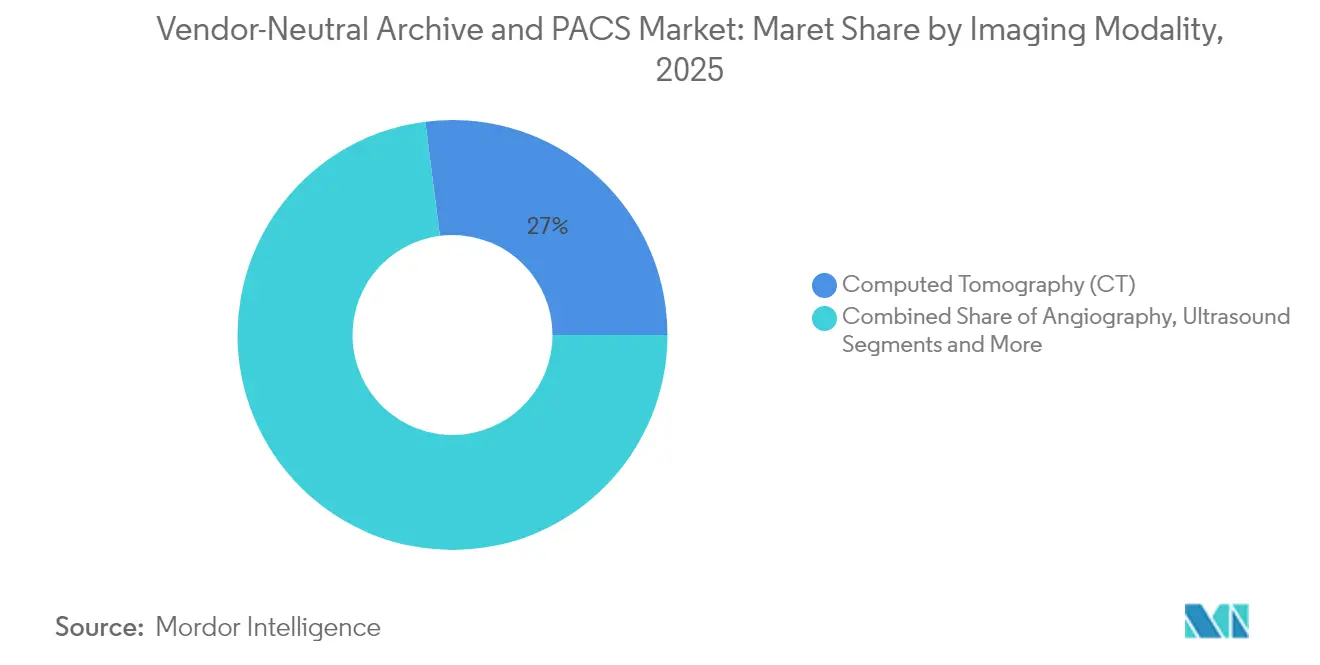

- By imaging modality, CT led with 27.02% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market share in 2025, while ultrasound is forecast to expand at a 9.74% CAGR through 2031.

- By component, software accounted for 39.08% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market size in 2025; services register the fastest growth at 9.21% CAGR to 2031.

- By type, PACS systems held 63.41% share of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market size in 2025, whereas VNA software is projected to rise at an 10.72% CAGR.

- By mode of delivery, on-site deployments controlled 50.34% share in 2025, but cloud models exhibit an 11.02% CAGR to 2031.

- By usage model, single-department setups represented 42.58% revenue in 2025; multi-site health-system rollouts advance at 10.12% CAGR.

- By end-user, hospitals captured 41.76% share in 2025, while diagnostic imaging centers grow quickest at 9.34% CAGR.

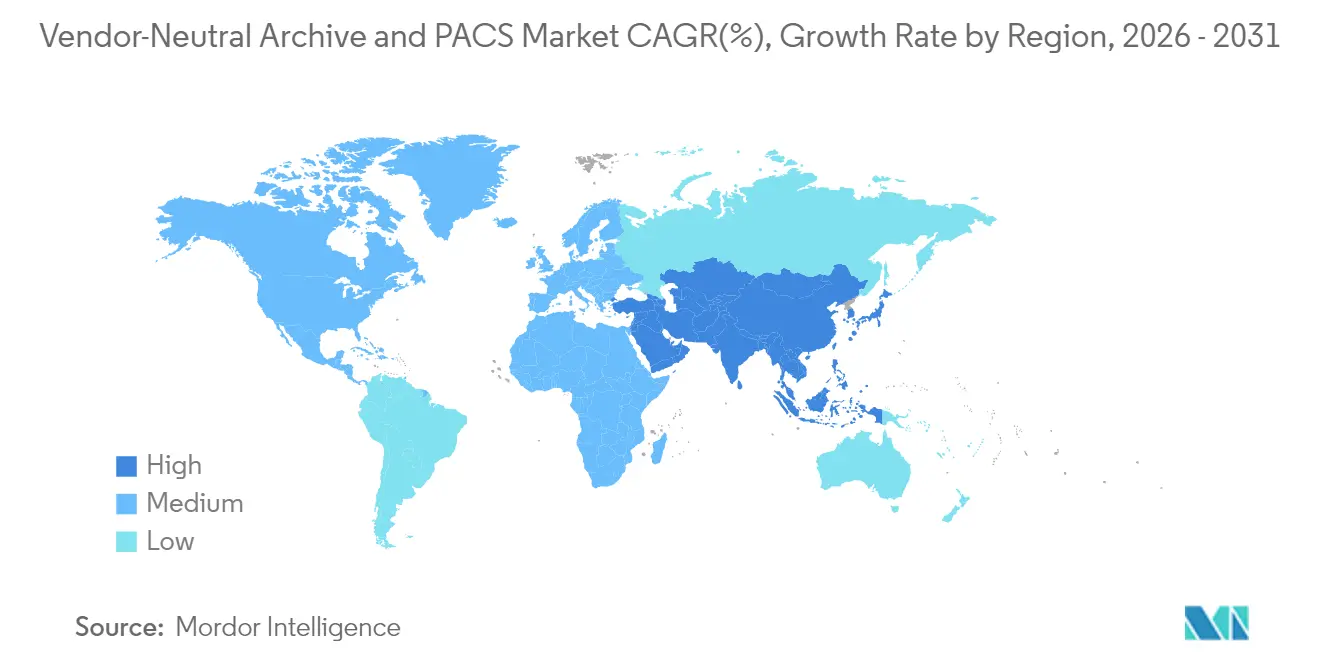

- By geography, North America commanded 43.21% share in 2025, whereas Asia-Pacific posts the highest 8.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vendor-Neutral Archive And PACS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Universal medical-image archiving | +1.8% | Global (strongest in North America & EU) | Medium term (2-4 years) |

| Declining cloud & on-prem storage cost | +1.5% | Global (fastest in APAC) | Short term (≤ 2 years) |

| Deep integration with electronic health records | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Climbing imaging volumes & higher-resolution modalities | +1.0% | Global (highest in APAC) | Long term (≥ 4 years) |

| AI/ML demand for longitudinal image repositories | +0.8% | North America & EU, spreading globally | Long term (≥ 4 years) |

| Cyber-insurance push for immutable, zero-trust VNAs | +0.7% | Global (strongest in North America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand For Universal Medical-Image Archiving

Health systems are replacing departmental silos with enterprise archives that house radiology, cardiology, pathology, and orthopedic images on a single backbone. The migration enables clinicians to review complete longitudinal imaging histories inside their workflow, eliminating diagnostic blind spots and improving care coordination. Vendors such as Sectra and Hyland market their VNA suites as “pixel EMRs” because they align images with clinical data in real time. Value-based reimbursement further rewards this consolidation, making the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market a linchpin for data-driven precision care.

Declining Data-Storage Cost (Cloud & On-Prem)

Cloud economics let providers lower imaging TCO by 30% while gaining elastic capacity for ever-larger studies. Automated lifecycle policies move older exams into cheaper cold tiers without harming retrieval speed, helping community hospitals and rural clinics adopt enterprise capabilities once limited to academic centers. Emerging markets leapfrog legacy hardware altogether, reinforcing cloud momentum within the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

High-Level Integration With Electronic Health Records

Modern VNAs exchange data via HL7 FHIR, letting images, reports, and AI insights surface directly inside the EHR interface. The 2025 HIPAA Security Rule increases pressure for interoperable yet secure designs, and CMS payment models favor coordinated care that depends on seamless data flow. These forces amplify EHR-VNA convergence, keeping the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market on an upward trajectory.

AI/ML Training Datasets Require Large Longitudinal Image Repositories

Hospitals view their archives as strategic AI assets. Comprehensive historical images enable proprietary algorithms that boost diagnostic accuracy and operational efficiency.[2]Vishwanatha M. Rao, Michael Hla, “Multimodal generative AI for medical image interpretation,” nature.com VNAs now bundle de-identification, federated learning, and dataset curation tools, making them the backbone for health-care AI development and reinforcing growth of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront migration & integration costs | −1.2% | Global (hardest for mid-size providers) | Short term (≤ 2 years) |

| Long product life cycle slows replacement sales | −0.8% | North America & EU | Medium term (2-4 years) |

| Proprietary metadata mapping raises vendor-lock-in risk | −0.6% | Global, multi-vendor sites | Medium term (2-4 years) |

| Unpredictable cloud-egress fees inhibit cloud VNA adoption | −0.4% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Migration & Integration Costs

Transitioning from legacy PACS to a fully cloud-native VNA can require multi-year, multi-million-dollar programs. Organizations must run dual systems, retrain staff, and redesign workflows, stretching IT budgets. Yet documented cases show five-year savings of USD 3 million for large children’s hospitals and immediate reductions of USD 700,000 in adult networks after go-live. While initial expense slows orders, the long-term payback sustains participation in the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

Long Product Life Cycle Slows Replacement Sales

Hospitals often run imaging systems for 10–15 years, delaying new purchases even as AI and cloud offerings advance rapidly. Vendors now promote subscription pricing and phased migration paths that allow incremental upgrades without a disruptive rip-and-replace approach, partially easing the drag on the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Imaging Modality: CT Dominance Amid Ultrasound Surge

CT captured 27.02% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market in 2025, driven by its versatile role in stroke triage, trauma evaluation, and oncology staging. The modality’s high throughput translates into steady archive growth, reinforcing overall Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market expansion. Ultrasound, benefiting from handheld devices and AI-assisted guidance, posts a 9.74% CAGR that opens new opportunities in primary care and remote settings.

Demand for MRI and PET data—rich in multi-sequence reconstructions—poses stringent storage and retrieval needs best met by scalable VNAs. Mammography workloads also intensify as risk prediction AI gains FDA clearance, pushing more facilities to adopt longitudinal breast-imaging repositories. Angiography contributes stable volumes linked to interventional cardiology growth, rounding out modality diversity.

By Component: Software Leadership With Services Acceleration

Software owned 39.08% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market size in 2025 thanks to agile, cloud-native codebases that add AI and cybersecurity features via push updates. Services rise quickest at 9.21% CAGR as migrations, managed hosting, and 24/7 monitoring become mandatory for compliance and uptime. Hardware demand persists for edge caches in latency-sensitive cath-lab or OR settings, yet its share gradually tapers.

Implementation consultancies charge premium rates because they orchestrate data extraction, validation, and downtime-free cutovers. Managed services appeal to resource-strained community hospitals that prefer predictable OPEX rather than capital outlays, solidifying the service footprint within the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

By Type: PACS Incumbency Challenged By VNA Innovation

PACS still controls 63.41% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market size, reflecting entrenched workflows and vendor relationships. Nonetheless, VNA applications climb at 10.72% CAGR, propelled by enterprises seeking interoperability, elimination of proprietary fees, and AI-ready data lakes. Migration playbooks that de-risk cutovers and pre-built cloud connectors accelerate the swing toward neutral archives.

Healthcare networks no longer view VNA as an optional back-end; they treat it as an engine for cross-specialty imaging, revenue-cycle analytics, and multi-institutional data exchange. As a result, new procurements almost always consider VNA functionality, even when framed initially as a PACS upgrade.

By Mode of Delivery: Cloud Transformation Accelerating

On-site installations retained 50.34% share in 2025 as large IDNs favored direct control. Cloud, however, posts an 11.02% CAGR because elastic pricing, disaster recovery, and hyperscale-grade security outweigh sovereignty concerns. Many providers adopt hybrid models that keep recent studies on-prem and archive historical images in the cloud, striking a balance that furthers Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market adoption.

Regional gateways enable AI vendors to process datasets without transferring PHI outside jurisdictional boundaries, easing regulators’ worries and broadening cloud uptake among early-stage APAC digitizers.

By Usage Model: Enterprise Expansion Beyond Single Departments

Single-department deployments made up 42.58% revenue in 2025, but expanding health systems want unified imaging across acute, ambulatory, and outpatient footprints. Multi-site rollouts advancing at 10.12% CAGR illustrate consolidation pressures that mandate common imaging policy, security, and analytics across locations. The Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market thus shifts from departmental to enterprise budgeting cycles.

Multi-department use rises as cardiology, pathology, and wound care imaging integrate into the same archive, eliminating redundant systems and enabling holistic AI algorithms that merge data streams for richer insights.

By End-User: Hospital Dominance With Imaging Center Growth

Hospitals held 41.76% share in 2025 because they deliver wide-ranging services, operate 24/7, and manage emergency care imaging at scale. However, diagnostic imaging centers, fueled by patient preference for low-cost outpatient exams, grow at 9.34% CAGR. Their lean operations spur demand for turnkey, subscription-priced archives that plug directly into referring physician portals, adding dynamism to the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

Ambulatory surgical centers and specialized orthopedics clinics increasingly adopt mobile imaging paired with cloud VNAs, widening end-user diversity and stimulating vendor innovation in lightweight, API-driven solutions.

Geography Analysis

North America, holding 43.21% of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market in 2025, benefits from robust HIPAA frameworks, large enterprise health systems, and sizeable capital budgets that support multi-hospital imaging transformations. GE HealthCare’s partnership with Sutter Health covering 300+ facilities exemplifies regional scale and sophistication.Providers adopt immutable archives and AI analytics in anticipation of evolving payer models emphasizing quality metrics tied to imaging efficiency.

Asia-Pacific leads growth at 8.97% CAGR through 2031 as governments in China, India, and ASEAN channel stimulus into digital health infrastructure. National health-information exchanges require standards-based imaging, driving cloud-native VNA deployments that sidestep legacy lock-in. Private hospital chains and teleradiology firms further accelerate adoption to meet soaring imaging demand from aging populations and expanded cancer screening.

Europe records steady momentum supported by GDPR data-governance rules and cross-border care initiatives. Providers prioritize data sovereignty, favoring local cloud regions or hybrid models. In the Middle East, Africa, and Latin America, greenfield hospitals build digital-first imaging stacks, leveraging subscription VNAs to conserve upfront capital. Collectively these regions add incremental volume that broadens the global footprint of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market.

Regulatory Landscape

Regulation for VNA and PACS spans medical-device software oversight, privacy/security, and health-data interoperability mandates that directly shape product design and procurement. In the United States, FDA oversight applies when PACS-related functions perform medical image management and processing, while basic storage and display can fall outside the device definition; imaging IT vendors increasingly pair regulated viewing/processing modules with enterprise archives. A recent example of the FDA posture on AI lifecycle controls is Siemens Healthineers use of a Predetermined Change Control Plan (PCCP) for AI-enabled software functions in syngo Dynamics (VA41F), cleared under 510(k) K253689 in March 2026.

Interoperability requirements are tightening as the US Office of the National Coordinator for Health Information Technology (ONC) advances a faster cadence of standards updates and explores imaging exchange requirements for certified health IT. ONC published its 2026 Standards Version Advancement Process (SVAP) cycle in June 2026, supporting newer versions of standards including USCDI v6 and updated HL7 FHIR artifacts, and in January 2026 issued an RFI on diagnostic imaging interoperability standards (DICOM, DICOMweb, FHIR, IHE) that has prompted stakeholders such as RSNA to push for DICOM-based requirements in 45 CFR Part 170. In Europe, GDPR-driven governance and the EU Medical Device Regulation (MDR) framework continue to influence how imaging platforms manage data sovereignty, security controls, and device-software responsibilities across member states.

Value Chain Analysis

The VNA and PACS value chain begins with modality image generation and DICOM tagging, then moves into acquisition gateways, normalization and routing (including metadata harmonization and patient identity matching), core archive and index services (VNA), clinical workflow and interpretation (PACS, diagnostic viewers), and distribution to downstream consumers such as EHRs, specialty systems, and external exchange networks. Standards and integration layers are pivotal inputs: the industry is shifting from legacy DIMSE-based DICOM connectivity toward RESTful DICOMweb and HL7 FHIR-enabled exchange using common web infrastructure (HTTP, OAuth, API gateways), which increases the importance of interface engines, integration consultants, and interoperability middleware alongside the core archive.

Deployment and operations form the second half of the chain, where cloud infrastructure providers, cybersecurity tooling, and managed-service partners support storage tiering, immutable retention, backup/disaster recovery, and continuous compliance monitoring. Policy activity also influences how images move across organizations: the ONC finalized the HTI-2 rule in December 2024, advancing interoperability and implementing provisions supporting TEFCA, which raises the bar for cross-entity information sharing and elevates demand for standards-based image exchange capabilities. Key bottlenecks for buyers remain multi-year migration programs, dual-running legacy and new systems, and ongoing costs tied to cloud egress and integration maintenance, pushing vendors to package migration utilities, hybrid architectures, and service-led implementations.

Competitive Landscape

Market consolidation continues as full-line OEMs—Siemens Healthineers, GE HealthCare, and Philips—bundle imaging modalities, AI, and enterprise software into unified platforms. GE HealthCare’s Genesis cloud suite, developed with AWS, expands its product roadmap threefold by 2028 and embeds edge storage plus automated migration utilities. Siemens Healthineers is spending USD 150 million on new U.S. facilities to scale next-gen imaging hardware that feeds seamlessly into its Syngo Carbon VNA.

Specialists such as RamSoft, Sectra, and Hyland differentiate through cloud-native architectures, open APIs, and integrated zero-trust controls. AI-centric players including DeepHealth and See-Mode—recently acquired by RadNet—target modality-specific niches, bringing AI value propositions that mesh tightly with VNAs for longitudinal learning. Competitive edge increasingly revolves around time-to-value, proven cybersecurity posture, and the breadth of embedded AI algorithms rather than core DICOM storage features alone. Consequently, the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market displays balanced rivalry where innovators coexist with established multinationals.

Vendor-Neutral Archive And PACS Industry Leaders

Agfa Healthcare NV

GE Healthcare

FUJIFILM Holdings Corporation

Sectra AB

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace area is standards-based imaging exchange beyond single enterprises, as US policy signals move toward formalized technical requirements for image interoperability. In January 2026, ASTP/ONC published an RFI on diagnostic imaging interoperability standards and certification, and both RSNA and the American Hospital Association responded in March 2026 highlighting the cost and workflow burden created by vendor-specific interoperability barriers. This policy direction elevates opportunities for VNAs, PACS vendors, and specialist middleware providers that can operationalize DICOMweb, IHE profiles, and HL7 FHIR to support cross-organization image access aligned with TEFCA-era exchange patterns.

Another opportunity sits in enterprise workflow orchestration and routing that connects imaging archives to AI pipelines and multi-site operations, including metadata normalization, automated DICOM and non-DICOM routing, and governance controls that reduce lock-in risk. Industry activity in 2026 supports this shift toward interoperability and routing layers: DataFirst, Inc. and Konica Minolta Healthcare announced a partnership in June 2026 to integrate DataFirst Silverback Workflow Engine with Exa PACS|RIS and Exa Teleradiology for enhanced DICOM routing and enterprise interoperability, and Merge released a cloud-native VNA platform update (Merge Imaging Suite VNA v26.0) on Microsoft Azure in July 2026 to support hybrid cloud deployments and standards-based workflow routing. These actions underscore buyer attention on hybrid architectures, enterprise routing, and exchange-readiness as core selection criteria alongside archive scalability and security.

Recent Industry Developments

- July 2026: Merge released Merge Imaging Suite VNA v26.0 as a cloud-native platform on Microsoft Azure, positioning the product for hybrid cloud deployment and workflow routing aligned with standards-based integration. The update strengthens cloud delivery options for enterprise imaging programs that need scalable archives and consistent access across sites. It also intensifies competition among VNAs and PACS suites that are being packaged as broader enterprise imaging platforms.

- November 2025: Agfa HealthCare signed Enterprise Imaging Cloud SaaS agreements with EFW Radiology in Canada and UI Health in the United States, expanding its cloud footprint in two North American care settings with different scale and workflow needs. These agreements reinforce a shift toward subscription delivery and managed operations for imaging archives and viewers. They also provide reference deployments that can influence procurement for other multi-site providers prioritizing faster go-live and standardized deployments.

- November 2024: Groupe sante CHC in Belgium chose Agfa HealthCare Enterprise Imaging under a 10-year contract to implement an enterprise imaging platform spanning VNA and PACS across its medical imaging department. The long-duration award highlights the importance of lifecycle support, migration services, and roadmap commitments in enterprise imaging selection. It also signals continued replacement of siloed archives with consolidated platforms in European health systems operating under stringent data governance requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from vendor-neutral archive (VNA) and PACS platforms used to store, manage, and retrieve medical images and related records across healthcare settings, including software licensing or subscriptions plus supporting services.

Scope exclusions: We exclude radiology information systems sold without an imaging archive layer, standalone analytics modules, and generic data-lake platforms that are not sold as VNA or PACS for clinical imaging workflows.

Segmentation Overview

- By Imaging Modality

- Angiography

- Mammography

- Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- Ultrasound

- Nuclear Medicine/PET

- Other Modalities

- By Component

- Hardware

- Software

- Services (Implementation, Migration, Managed)

- By Type

- PACS

- Vendor-Neutral Archive (VNA) Software

- By Mode of Delivery

- On-site (Premise)

- Hybrid

- Cloud-Hosted

- By Usage Model

- Single Department

- Multiple Departments (Enterprise Imaging)

- Multiple Sites / Health-system

- By End-User

- Hospitals (Large, Mid-size, Small)

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers & Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to set the boundaries and build the first demand map for VNA and PACS adoption by region and care setting. We rely on public sources such as the WHO and OECD health statistics, CDC and national health ministry publications, FDA device and software communications where applicable, and standards bodies like DICOM and HL7 for interoperability cues that influence buying cycles. In parallel, we review peer-reviewed clinical imaging informatics literature to understand image growth, storage patterns, and typical deployment choices.

To translate those signals into a usable market model, we also screen company filings, annual reports, investor decks, hospital procurement releases, and reputable press coverage of multi-year imaging IT programs. Select paid subscriptions are used only for company financials and news tracking, plus patent databases to sanity-check where product development and image management workflows are moving. The desk sources listed here are illustrative, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what is actually being purchased and deployed, and how budgets are split between VNA, PACS, migration, and managed services. We speak with a mix of hospital IT and imaging leaders, diagnostic imaging operators, and solution-side product and delivery experts across APAC, EMEA, and the Americas, and then we use these inputs to tune adoption rates, replacement cycles, and realistic price ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 40% |

| Mid tier: 60% | Functional/Unit leaders: 43% | EMEA: 34% |

| Smaller Players: 15% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build, where imaging procedure growth, hospital digitization rates, and the installed base of imaging archives are used to reconstruct how much VNA and PACS spend is likely to occur in each region. The model is then corroborated through selective bottom-up checks, mainly by sampling vendor and channel price ranges, mapping typical contract bundles (software plus migration or managed services), and testing the totals against plausible deal volumes in key countries.

Inputs are kept practical and traceable, so we lean on indicators such as diagnostic imaging volumes, average image data growth and retention requirements, cloud versus on-prem deployment preference, replacement and upgrade cycles of legacy PACS, and enterprise viewer rollouts that pull demand toward unified archives. When information is thin for a country or care setting, we fill gaps using proxy adoption curves from similar health systems and then re-check those proxies through expert feedback.

For forecasting, scenario analysis is used around the main swing factors that buyers highlighted, including cloud migration timing, cybersecurity and privacy compliance spending, and multi-department enterprise imaging expansion beyond radiology. The scenarios are converted into an annual outlook by applying a smoothed trend line to validated drivers, and assumptions are revisited whenever primary inputs show a shift in budgets or procurement cadence.

Data Validation & Update Cycle

Validation happens through multiple passes, starting with basic consistency checks across regions, currencies, and year-on-year growth so outliers can be flagged early. We then compare the modeled totals against independent signals, such as hospital IT spending trends and reported imaging platform investments, and any large variance is investigated until the driver or the data point is explained.

Before sign-off, the numbers and assumptions are reviewed by another analyst, and follow-up calls are triggered when a key variable moves beyond an expected band (for example, a step change in cloud adoption or a visible change in pricing behavior). Reports are refreshed annually, and interim updates are added when material events occur, followed by a final pre-delivery check to ensure clients receive the latest view.

Mordor Intelligence's Global Vendor Neutral Archive Vna and Pacs Market Market Size Versus Other Published Estimates

Published market sizes for VNA and PACS can look far apart even when the topic sounds the same, because each estimate picks its own boundaries and timing. The most common differences come from what is counted as part of the platform spend, how cloud subscriptions are annualized, and whether services like migration and managed operations are included.

The spread usually shows up when one study bundles adjacent enterprise imaging items that are not always bought with VNA or PACS, or when aggressive cloud adoption assumptions are applied without grounding them in procurement behavior. Hospital imaging procedure growth, upgrade cycle feedback from IT teams, and observed deal bundling patterns are the checks that keep Mordor Intelligence's estimate tied to recurring and one-time revenues that are specific to VNA and PACS deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.92 B (2026) | |

| Trade Journal A | USD 5.09 B (2025) | Uses a different base year and a longer horizon, and the public summary does not clarify whether services and hardware are separated from adjacent imaging IT items, which can lift the reported total. |

| Global Consultancy B | USD 5.62 B (2026) | Appears to apply broader segmentation and may include a wider enterprise imaging stack beyond core VNA and PACS, and the higher growth path can be driven by faster cloud mix shift assumptions. |

Looking across the table, most of the gap is explained by year selection and what is counted inside the spend boundary, rather than a disagreement on the direction of demand. By keeping the inputs tied to imaging volumes, upgrade cycles, and contract structures, we are able to provide a number that is easy to reconcile back to real buying activity.

Key Questions Answered in the Report

What is the current value of the Vendor-Neutral Archive (VNA) & Picture Archiving and Communication System (PACS) market?

The market stands at USD 4.92 billion in 2026 and is projected to reach USD 6.94 billion by 2031.

Which segment records the highest share within this market?

PACS systems retain 63.41% of overall revenue, reflecting longstanding adoption across radiology departments.

Why are cloud deployments gaining ground in enterprise imaging?

Providers realize up to 30% cost reductions and benefit from elastic capacity, disaster recovery, and advanced security unavailable in many on-premise data centers.

Which geographic region grows the fastest and why?

Asia-Pacific leads with a 8.97% CAGR thanks to government-funded health IT programs, cloud-friendly policies, and rapid hospital expansion.

Which region has the biggest share in Vendor-Neutral Archive And PACS Market?

In 2025, the North America accounts for the largest market share in Vendor-Neutral Archive And PACS Market.

What years does this Vendor-Neutral Archive And PACS Market cover, and what was the market size in 2025?

In 2025, the Vendor-Neutral Archive And PACS Market size was estimated at USD 4.59 billion. The report covers the Vendor-Neutral Archive And PACS Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Vendor-Neutral Archive And PACS Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: