Mixed Reality In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 5.84 Billion |

| Growth Rate (2026 - 2031) | 20.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

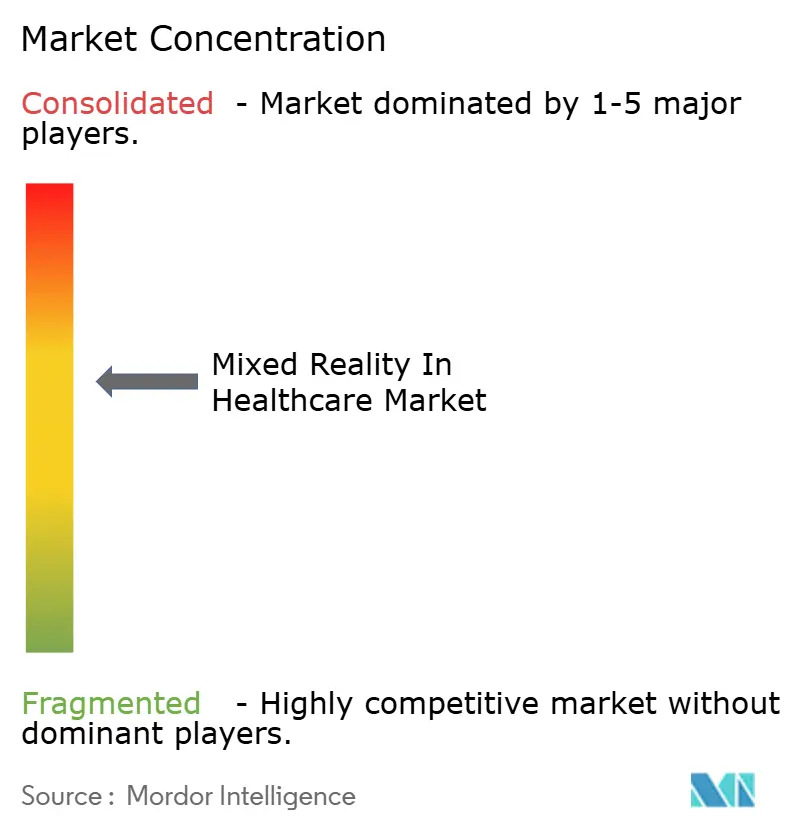

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mixed Reality In Healthcare Market Analysis by Mordor Intelligence

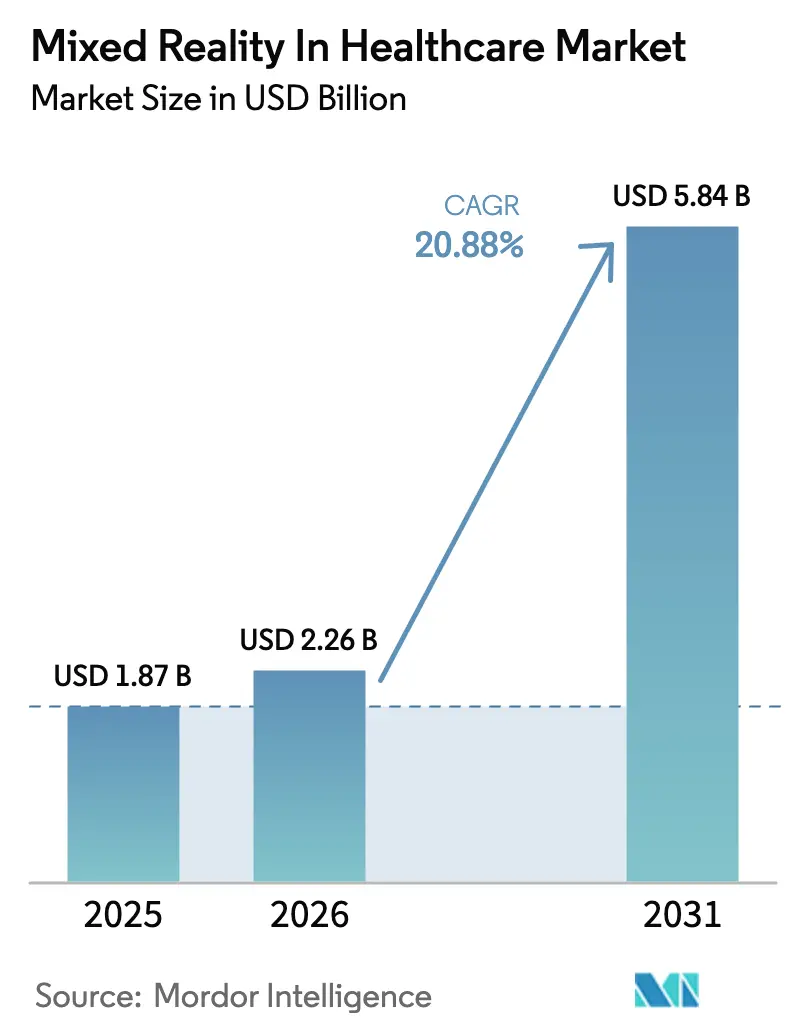

The Mixed Reality In Healthcare Market size was valued at USD 1.87 billion in 2025 and estimated to grow from USD 2.26 billion in 2026 to reach USD 5.84 billion by 2031, at a CAGR of 20.88% during the forecast period (2026-2031).

Accelerated FDA approvals for augmented-reality surgical navigation systems, rapid roll-out of 5G medical networks, and the fusion of AI-driven adaptive simulation platforms are collectively amplifying adoption across surgical, training and telepresence use cases. North America continues to anchor early-stage demand owing to established reimbursement pathways and mature XR-ready hospital infrastructure, while Asia Pacific’s sweeping 5G upgrades and sizeable public-sector digital health budgets are propelling the region to become the fastest-growing arena. Equipment vendors are shifting from pure hardware sales to ecosystem playbooks that bundle cloud rendering, managed services and privacy-preserving AI, thereby unlocking recurring revenue streams. Meanwhile, privacy‐centric edge-AI models and ergonomic improvements in head-mounted displays are actively softening the impact of data-residency rules and surgeon interface fatigue.

Key Report Takeaways

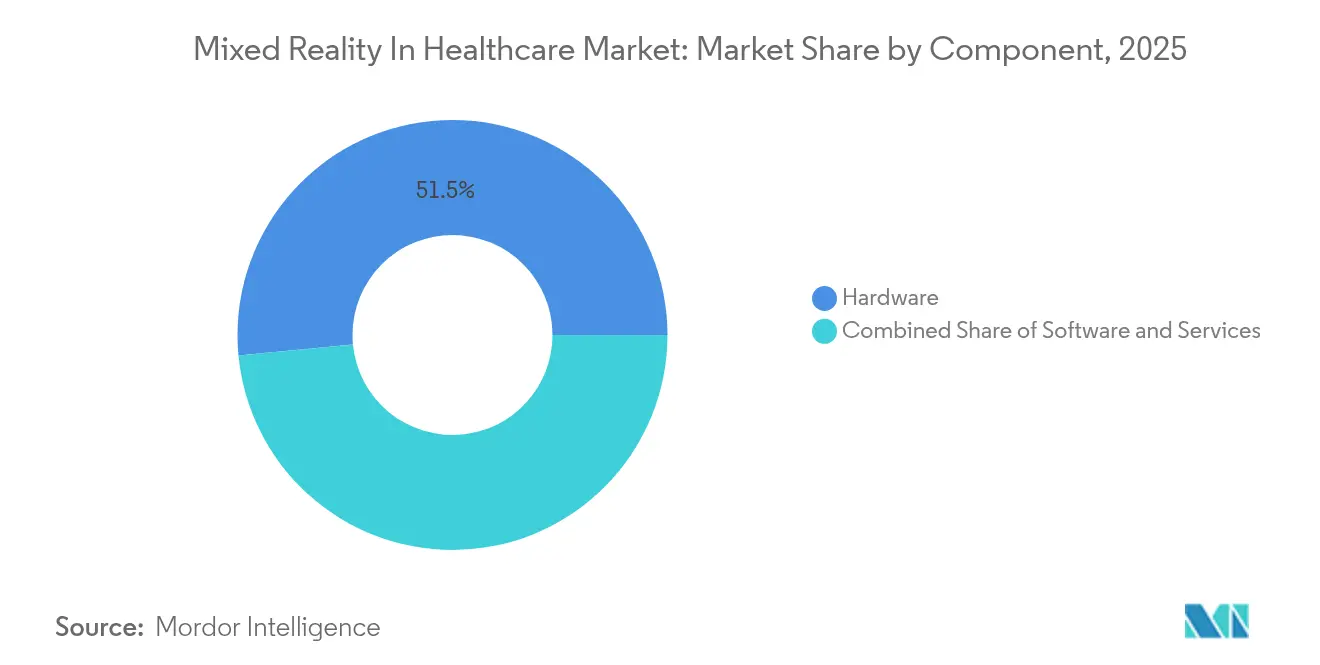

- By component, hardware led with 51.52% revenue share in 2025; services are projected to expand at a 25.19% CAGR through 2031.

- By application, surgery and intra-operative guidance accounted for 37.25% of the mixed reality in healthcare market share in 2025, whereas rehabilitation and physical therapy are advancing at a 21.96% CAGR to 2031.

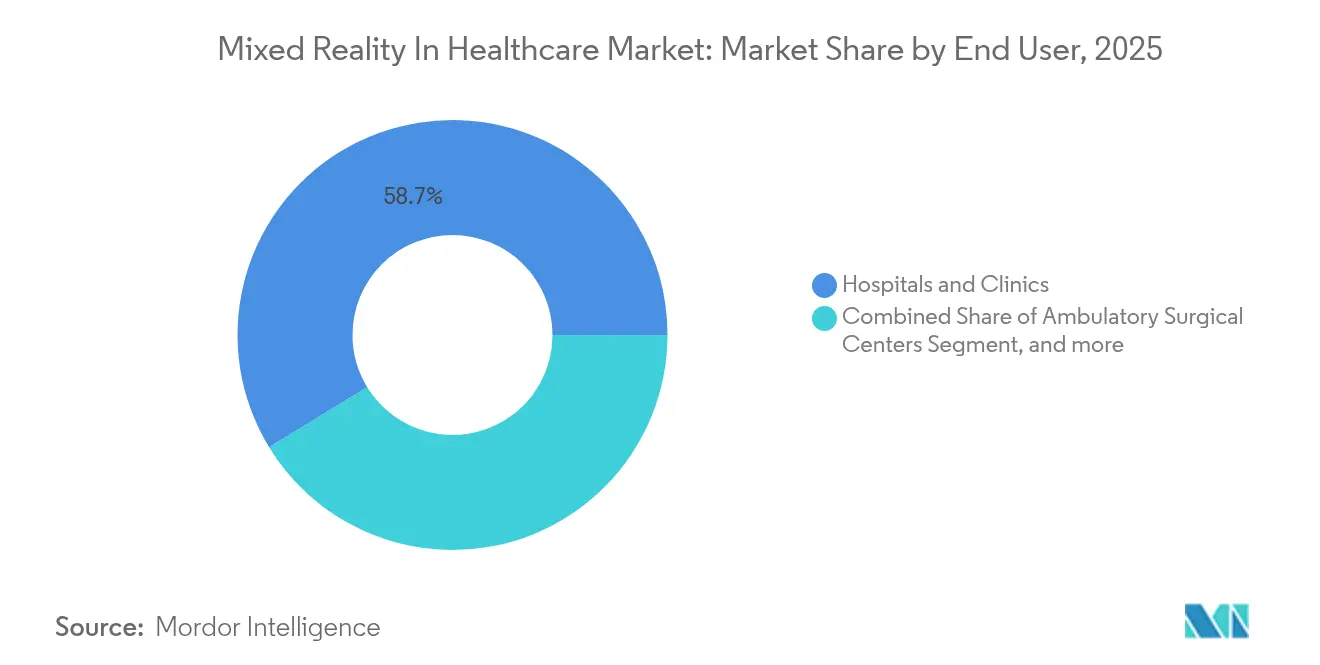

- By end user, hospitals and clinics captured 58.74% of the mixed reality in healthcare market size in 2025, while fitness and rehabilitation centers are poised for a 22.71% CAGR between 2026-2031.

- By geography, North America commanded 43.62% market share in 2025; Asia Pacific is forecast to record the fastest 23.91% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mixed Reality In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of XR-Ready Surgical Navigation Platforms | +4.2% | Global, with North America & EU leading | Medium term (2-4 years) |

| Government-Funded Immersive Training Programs | +3.8% | North America, EU, APAC core markets | Long term (≥ 4 years) |

| Surge in Telepresence Demand for Rural Healthcare Access | +3.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Fast-Track Approvals for Patient-Specific Holographic Planning Tools | +2.9% | North America, EU regulatory zones | Medium term (2-4 years) |

| Roll-Out of 5G-Enabled Ultra-Low-Latency Cloud Rendering | +4.5% | APAC core, spill-over to global markets | Medium term (2-4 years) |

| Integration of AI for Adaptive Simulation & Predictive Modeling | +3.7% | Global, with tech-advanced regions leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of XR-Ready Surgical Navigation Platforms

Early surgical adopters report measurable productivity and safety gains once head-mounted 3D visualisation replaces traditional 2D screens. Stryker’s Blueprint Mixed Reality Guidance System used with HoloLens 2 completed its first shoulder arthroplasties at Mayo Clinic, reducing implant-placement error and trimming operating-room time.[1]Stryker, “Blueprint Mixed Reality Guidance System Performs First Clinical Shoulder Arthroplasty,” stryker.com Microsoft’s field data shows up to 30% shorter ward-round durations when teams collaborate through holographic overlays . Clinical trials by MediView confirmed sub-3 mm registration accuracy, satisfying thresholds for minimally invasive work . The momentum underscores a shift toward spatial computing that compresses cognitive load and bolsters procedural confidence.

Government-Funded Immersive Training Programs

Public agencies are underwriting extended-reality curricula to address clinician shortages. The US National Science Foundation awarded USD 2.8 million for a VR simulator that drills frontline responders on respiratory pandemics, allowing universities to reuse assets for broader medical education.[2]National Science Foundation, “Award Abstract #2148954 – XR Simulation for Pandemic Response,” nsf.gov In parallel, the Department of Defense backs Design Interactive’s Asclepius, an AI-guided combat casualty interpreter on HoloLens 2, to sharpen remote triage accuracy. Such grants seed intellectual property that commercial firms later license, fast-tracking standardised XR protocols across trauma, oncology and cardiology specialties.

Surge in Telepresence Demand for Rural Healthcare Access

Low-density regions are embracing holographic consultation to counter clinician shortages. Vodafone’s 5G-linked ambulances stream 360-degree imagery to hospital specialists, letting paramedics perform AI-prompted interventions en route and elevating survival odds in acute stroke scenarios. Texas-based Crescent Regional Hospital deployed Holoconnects’ life-size Holobox for remote doctor-patient dialogues, slashing specialist wait-times during night shifts. These deployments demonstrate the mixed reality in healthcare market’s ability to equalise access without costly brick-and-mortar expansion.

Fast-Track Approvals for Patient-Specific Holographic Planning Tools

Regulators now fast-track mixed-reality devices that demonstrably cut complication rates. The FDA cleared Novarad’s OpenSight system, which lets surgeons overlay CT data on patients during pre-op walk-throughs, improving trajectory planning.[3]Novarad, “OpenSight Augmented Reality System Receives FDA Clearance,” fda.gov Zeta Surgical secured a Special 510(k) for a mixed-reality navigation upgrade that reduces time-to-incision in neuro cases. Speedier approvals are compressing go-to-market cycles and intensifying competitive iteration around patient-tailored holography.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Hardware & Integration Costs | -2.8% | Global, particularly cost-sensitive markets | Short term (≤ 2 years) |

| Shortage of AR/MR-Skilled Clinical Workforce | -3.2% | Global, with acute shortages in emerging markets | Medium term (2-4 years) |

| Cyber-Skeuomorphic Interface Fatigue Among Surgeons | -1.9% | Developed markets with high XR adoption | Medium term (2-4 years) |

| Data-Sovereignty Barriers to Cross-Border Holographic Libraries | -2.1% | EU, APAC regions with strict data laws | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Integration Costs

Premium spatial-computing headsets exceed many hospitals’ capital thresholds. Apple Vision Pro’s introductory price tier, while clinically capable, competes against multiple operating-suite upgrades when budgets tighten. Smaller ambulatory centres instead trial low-cost EmdoorVR units priced near USD 280, forfeiting retina-level resolution for affordability. Added expenses around sterilisation sleeves, workflow redesign and cloud bandwidth intensify scrutiny. Managed-service subscriptions that convert capex into opex are emerging to soften adoption hurdles and widen the mixed reality in healthcare market.

Shortage of AR/MR-Skilled Clinical Workforce

Spatial computing demands new cognitive and motor proficiencies not taught in conventional medical curricula. A multicentre review found that clinicians required five to eight supervised sessions to reach baseline XR proficiency, delaying programme rollout. Universities are piloting micro-credential pathways, yet graduation pipelines lag institutional demand. Until training capacity scales, deployment pace will hinge on in-house champion surgeons and vendor-provided bootcamps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Amid Services Acceleration

Hardware retained 51.52% of mixed reality in healthcare market share during 2025, underscoring the pivotal role of head-mounted displays and holographic light-field panels in clinical performance. Investments continue to chase lighter optics and sealed-for-sterile enclosures, as evidenced by Princeton University’s prototype that renders high-definition holograms through conventional spectacles. Hospitals justify spending because surgical accuracy correlates with display fidelity, reducing revision surgeries. Services, however, log the steepest 25.19% CAGR as providers pivot to subscription-based cloud rendering, uptime monitoring and user-analytics dashboards. This transition dilutes capex spikes and fosters continuous feature upgrades, creating annuity-style revenue that attracts software integrators. Cloud pipelines further enable privacy-preserving multimodal AI transcription, edging data-sovereignty fears without on-premise silicon.

The software tier sits between hardware heft and service agility. On-premise deployments remain vital where national statutes demand local storage, but hybrid clouds gain ground as zero-trust security frameworks mature. Application programming interfaces now plug PACS radiology images into 3D engines in seconds, cutting typical set-up times by half. As real-time holography demands burst compute, autoscaling GPU instances take precedence, heralding a broader shift toward graphics-as-a-service that will reshape procurement conversations over the forecast horizon.

By Application: Surgery Leadership Challenged by Rehabilitation Growth

Surgery and intra-operative guidance applications commanded 37.25% of the mixed reality in healthcare market size in 2025, anchored by high-acuity cases where centimetre-level precision outweighs headset costs. The landmark shoulder replacement performed with Apple Vision Pro demonstrated surgeon appetite for retina-grade micro-OLED clarity, accelerating vendor pipelines for orthopaedic and cardiovascular templates. High-value reimbursement schedules further lock in utilisation, strengthening the segment’s near-term hold.

Rehabilitation and physical therapy are scaling fastest, tracking a 21.96% CAGR through 2031. Meta-analysis on 36 controlled trials revealed that immersive VR improved post-stroke upper-limb function by an additional 8 Fugl-Meyer points over conventional therapy, fuelled by gamified adherence. Pay-for-performance insurers increasingly reimburse XR sessions conducted in fitness facilities, democratising access outside tertiary centres. Patient-centric design, including eye-tracked fatigue gauges, bolsters compliance, positioning rehabilitation as the breakout frontier for the mixed reality in healthcare market.

By End User: Hospital Dominance Faces Rehabilitation-Center Disruption

Hospitals and clinics owned 58.74% of mixed reality in healthcare market share in 2025, leveraging bundled procurement budgets and in-house IT support. GE Healthcare and MediView launched the first augmented-reality interventional suite, integrating holographic fluoroscopy overlays that cut radiation exposure by 29% in pilot cath labs. Academic medical centres, by virtue of research grants, trail-blaze multi-specialty use cases that migrate to community hospitals once validated.

Fitness and rehabilitation centres record the sharpest 22.71% CAGR as they harness XR for musculoskeletal recovery and chronic-pain desensitisation. Lean operating models let these venues pivot rapidly, bundling virtual coach subscriptions with wearables that stream kinematic data into therapist dashboards. Ambulatory surgical centres widen the user mix as insurers steer low-complexity procedures away from inpatient wards. Meanwhile, university labs nurture proof-of-concepts on paediatric phobia treatment and geriatric fall-risk assessment, feeding a pipeline of evidence that reinforces end-user diversification.

Geography Analysis

North America preserved its 43.62% revenue hold in 2025, driven by FDA rapid-path clearances and enterprise deals between ecosystem leaders such as Microsoft and Mass General Brigham that embed AI models into surgical holography workflows. Canadian institutions like St. Joseph’s Health Care London mirror US momentum, leveraging provincial grants to scale reconstructive-surgery XR pilots. Mexico’s flourishing medical tourism sector now markets mixed-reality-guided orthopaedics as a premium differentiator, swelling cross-border patient inflows.

Asia Pacific tops the growth chart with a 23.91% CAGR outlook. China blends state-owned telecom investments and domestic headset manufacturing to compress device costs, reinforcing rural telepresence ambitions. Japan’s Health 2025 showcase underlines governmental resolve to export XR-enabled eldercare paradigms. India’s 1.4 billion population, coupled with National Digital Health Mission incentives, fosters fertile ground for cloud-rendered simulation labs in tier-2 cities. Australia and South Korea capitalise on near-universal 5G coverage to pilot latency-sensitive telesurgery tests, cementing APAC’s stature in the mixed reality in healthcare market.

Europe progresses steadily on the back of harmonised e-health frameworks and GDPR-compatible data fabrics. Germany’s newly enacted Digital Act widens reimbursement for mixed-reality rehabilitation, while the UK executed its first Apple Vision Pro-assisted hepatobiliary surgery at Guy’s & St Thomas’ NHS Trust. France and Spain pool Horizon Europe funds into open-source holographic anatomy atlases, reducing language barriers for cross-border clinical training. The Middle East allocates sovereign-wealth capital to build XR-enabled centres of excellence in Dubai and Riyadh, whereas South Africa positions itself as a sub-Saharan pilot bed after upgrading academic hospitals with 5G fixed-wireless links. Latin America, led by Brazil, experiments with rental-based headset models to soften currency volatility, marking incremental yet meaningful penetration.

Competitive Landscape

Competition remains moderate as no single vendor controls an end-to-end stack, yet incumbents retain scale advantages. Microsoft continues to cross-sell HoloLens 2 into Epic-integrated electronic health record ecosystems, curating a walled garden of validated surgical apps. Apple’s Vision Pro intensified premium-tier rivalry, bringing eye-tracked foveated rendering that raised clinician expectations for visual acuity. Google maintains a research foothold through Project Starline volumetric video, eyeing remote oncology follow-ups as a first revenue beachhead.

Specialised device makers, meanwhile, carve niches. Augmedics achieved first-in-class FDA clearance for diegetic spinal navigation, catalysing venture inflows aimed at orthopaedic sub-segments. Stryker exploits its implanted-device customer base to bundle planning software, whereas Philips experiments with holographic echo-cardiography overlays to complement its imaging franchise. Start-ups such as XRHealth and HoloAnatomy Labs leverage pay-per-session SaaS to sprint ahead in rehabilitation and med-ed verticals.

M&A picked up pace as capital markets reward synergistic pipelines. HealthpointCapital’s July 2025 acquisition of ImmersiveTouch underscored hunger for turnkey planning engines that dovetail with implant design workflows, while Qualcomm’s minority stake in Proto Hologram hints at silicon houses pushing towards healthcare differentiation. Long-run success will belong to vendors who harmonise hardware lifecycles with cloud micro-services, keep data governance airtight and show prospective buyers peer-reviewed outcome deltas.

Mixed Reality In Healthcare Industry Leaders

EchoPixel

Microsoft

Firsthand Technology

Osso VR

Surgical Theater

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Mercy Medical Center, a US-based orthopedic surgery center, reported the utilization of Blueprint Mixed Reality (MR) Guidance, developed by Stryker, to offer shoulder arthroplasty. The Blueprint Mixed Reality system overlays 3D holographic images with real life, allowing the surgeon to view the surgical site directly.

- January 2024: GigXR Inc., a provider of mixed reality solutions for healthcare training, and CAE Healthcare reported the partnership to enhance the efficiency and effectiveness of clinical simulation. The collaboration between GigXR and CAE Healthcare streamlines the ability to implement and manage multimodal simulation for medical schools, nursing schools, and hospital systems.

Global Mixed Reality In Healthcare Market Report Scope

As per the scope of the report, mixed reality (MR) is an emergent technology that blends virtual reality (VR) and augmented reality (AR). This technology is used for medical teaching and surgery planning to improve patient care. The mixed reality in the healthcare market is segmented into components, applications, end users, and geography. By component, the market is segmented into software, hardware, and services. By application, the market is segmented into surgery and surgery simulation, patient care management, fitness management, medical training and education, and other applications. The market is segmented by end user into hospitals and clinics, surgical centers, and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for the above segments.

| Hardware | Head-Mounted Displays (HMD) |

| Holographic Displays | |

| Software | On-Premise |

| Cloud-Based | |

| Services |

| Surgery & Intra-operative Guidance |

| Patient Care Management |

| Rehabilitation & Physical Therapy |

| Fitness & Wellness Management |

| Medical Training & Education |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Research & Academic Institutes |

| Fitness & Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | Head-Mounted Displays (HMD) |

| Holographic Displays | ||

| Software | On-Premise | |

| Cloud-Based | ||

| Services | ||

| By Application | Surgery & Intra-operative Guidance | |

| Patient Care Management | ||

| Rehabilitation & Physical Therapy | ||

| Fitness & Wellness Management | ||

| Medical Training & Education | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Research & Academic Institutes | ||

| Fitness & Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current mixed reality in healthcare market size?

The mixed reality in healthcare market size stands at USD 2.26 billion in 2026 and is projected to reach USD 5.84 billion by 2031.

How fast is the mixed reality in healthcare market growing?

The market is forecast to grow at a 20.88% CAGR between 2026 and 2031, driven by regulatory fast-tracking, 5G roll-outs and AI-enhanced simulation.

Which region is expanding fastest in mixed-reality healthcare adoption?

Asia Pacific is set to register a 23.91% CAGR through 2031 as 5G networks, public funding and affordable headset manufacturing converge.

Which application segment shows the highest growth momentum?

Rehabilitation and physical therapy lead future expansion with a 21.96% CAGR, fuelled by clinical evidence of improved stroke recovery.

Why are services growing faster than hardware?

Managed XR services convert capital expense into subscription models, delivering cloud rendering, analytics and continuous updates that healthcare providers prefer over large upfront hardware outlays.

What is the biggest barrier to wider XR adoption in healthcare?

The acute shortage of AR/MR-skilled clinicians combined with high initial device costs remains the leading constraint, though expanded training programs and lower-priced headsets are gradually easing the hurdle.

Page last updated on: