Market Overview

| Study Period | 2020 - 2031 |

|---|---|

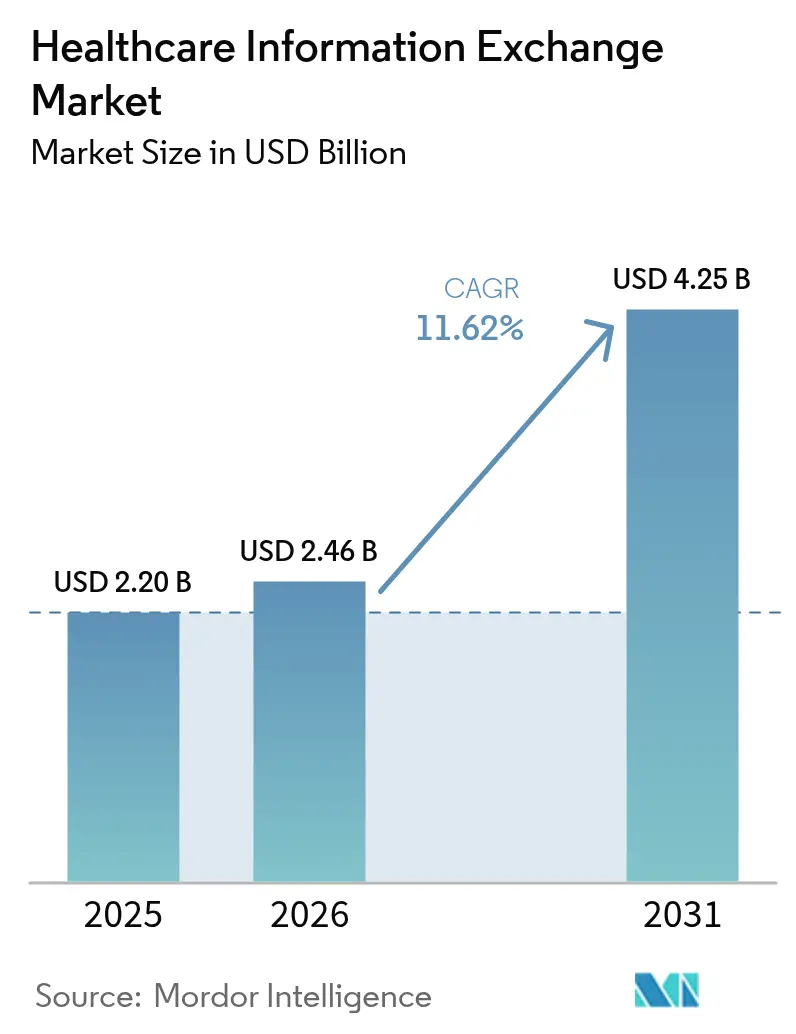

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 4.25 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

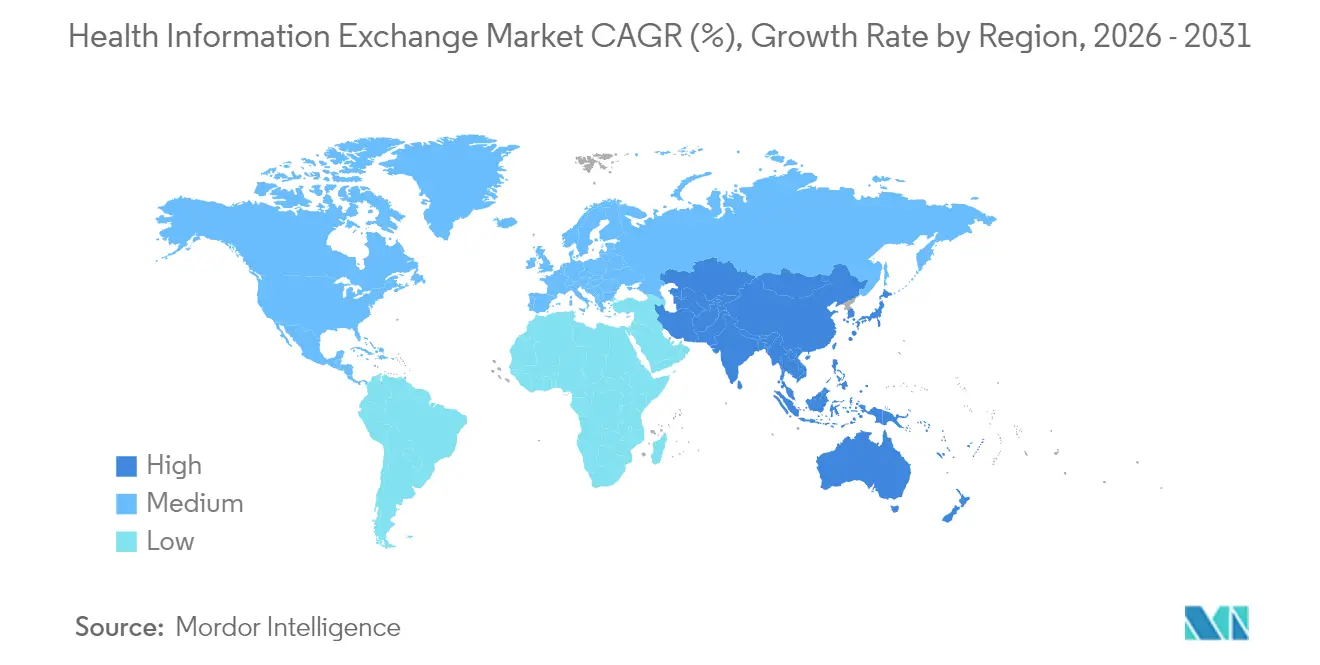

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Information Exchange Market Analysis by Mordor Intelligence

The health information exchange market size was valued at USD 2.20 billion in 2025 and estimated to grow from USD 2.46 billion in 2026 to reach USD 4.25 billion by 2031, at a CAGR of 11.62% during the forecast period (2026-2031). This rapid expansion mirrors global digital‐health priorities, including stricter interoperability rules, growing cybersecurity vigilance, and the shift to value-based care models. National frameworks such as the Trusted Exchange Framework and Common Agreement (TEFCA) are reinforcing interoperability expectations, while providers invest in hybrid cloud architectures to balance local control with scalability. Centralized deployments still dominate, yet the hybrid approach’s strong growth signals a gradual redesign of data governance strategies. Meanwhile, Epic Systems’ nationwide TEFCA roll-out is redefining competitive dynamics, prompting rivals to accelerate platform upgrades and security enhancements.

Key Report Takeaways

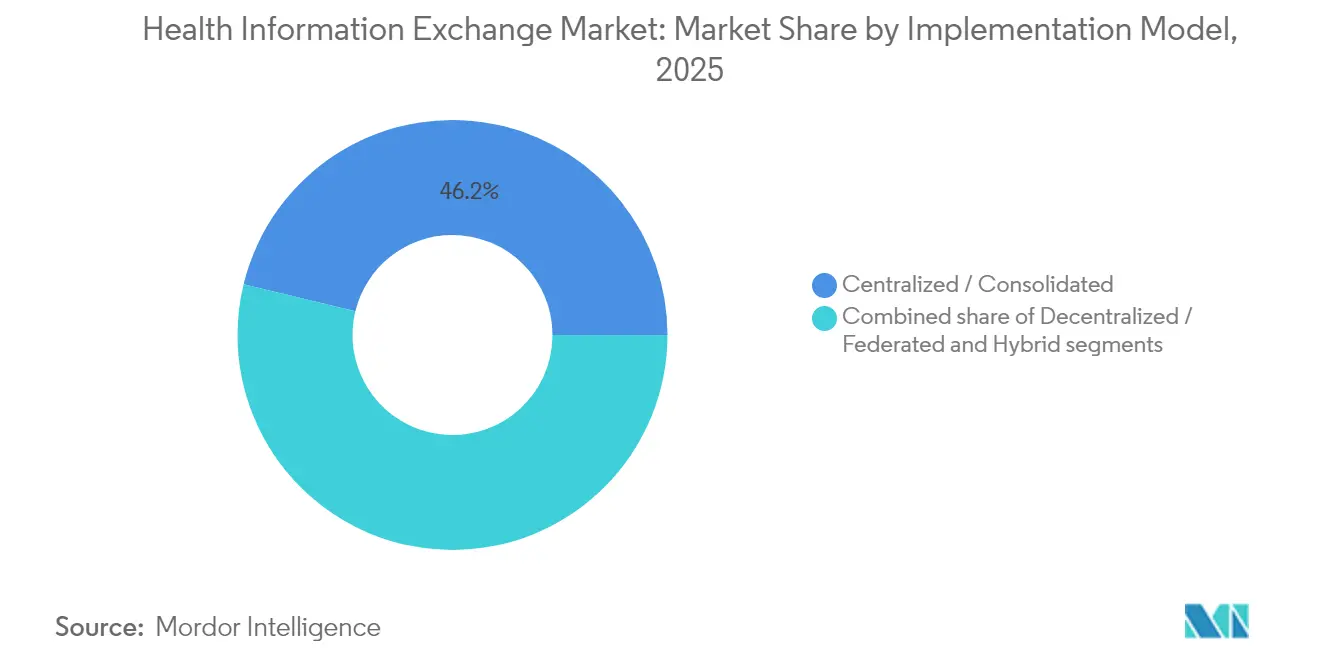

- By implementation model, centralized/consolidated deployments held 46.20% of health information exchange market share in 2025; hybrid approaches are expanding at 13.12% CAGR through 2031.

- By application, workflow management accounted for 34.20% of the health information exchange market size in 2025, whereas the “other applications” category is growing at 13.55% CAGR on the back of AI decision-support use cases.

- By component, Enterprise Master Person Index systems led with 29.40% health information exchange market share in 2025, while clinical data repository solutions are growing fastest at 14.39% CAGR.

- By end user, healthcare providers dominated with 56.85% share in 2025, but payers are forecast to grow at 14.30% CAGR through 2031.

- By geographic region, North America captured 47.10% of health information exchange market share in 2025, while Asia-Pacific is advancing at a 12.21% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Healthcare Information Exchange Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital transformation of healthcare systems | +2.8% | Global, led by North America and EU | Medium term (2-4 years) |

| Expanding government funding for nationwide interoperability | +2.1% | North America core, spill-over to APAC | Long term (≥ 4 years) |

| Shift toward value-based care and population health management | +1.9% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Rapid growth of cloud-based health IT deployments | +1.6% | Global, fastest in Asia-Pacific | Medium term (2-4 years) |

| Emergence of consumer-driven health-data ownership models | +1.2% | North America & EU | Medium term (2-4 years) |

| Integration of artificial intelligence for real-time clinical decision support | +1.8% | Tech-advanced markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation of Healthcare Systems

Digital transformation has moved past basic EHR roll-outs into enterprise-wide interoperability platforms that enable real-time data exchange across care settings. Hospital groups are prioritizing patient-experience metrics alongside operational efficiency, prompting greater investment in standards-based data-sharing frameworks. In Asia-Pacific, government grants for digital-health infrastructure amplify adoption as providers respond to aging populations and rural access challenges. Interoperability tools now function as the central nervous system of connected care, linking clinicians, payers, and public-health agencies. The outcome is a measurable uptick in cross-facility data liquidity, which improves care coordination and reduces redundant testing.

Expanding Government Funding for Nationwide Interoperability

Public-sector investment is reaching unprecedented levels. The U.S. Centers for Disease Control and Prevention earmarked USD 255 million for public-health data exchange through 2026[1]Centers for Disease Control and Prevention, “Data Modernization Initiative,” cdc.gov. Across the Atlantic, the European Health Data Space regulation set aside EUR 810 million for cross-border exchange readiness by 2031[2]European Commission, “European Health Data Space: Regulation (EU) 2025/651,” ec.europa.eu. Australia is financing vendor connections to My Health Record, while Japan and South Korea have placed interoperability at the heart of national digital-health agendas. Government funds are widening the user base beyond hospitals, enabling community clinics and research bodies to join secure exchange networks.

Shift Toward Value-Based Care and Population Health Management

The Centers for Medicare & Medicaid Services intends to move every beneficiary into an accountable-care relationship by 2030. Providers entering risk-sharing contracts require timely access to multi-source patient data to close care gaps, stratify risk, and track quality metrics. Integrated payer-provider organizations—so-called payviders—are now major adopters of exchange platforms as they align financial risk with clinical outcomes. Robust data-sharing capabilities are proving integral to hitting shared-savings targets and preventing avoidable readmissions.

Rapid Growth of Cloud-Based Health IT Deployments

Cloud adoption offers elastic scaling, automated updates, and resilient disaster recovery, making software-as-a-service HIE models attractive. In Asia-Pacific, many systems leapfrog legacy hardware by opting directly for cloud-native deployments, shaving months off implementation timelines. Vendors are consolidating around cloud-first architectures, standardizing on HL7 FHIR APIs that simplify third-party integrations. Hospitals report smoother upgrades, tighter security patch cycles, and improved uptime compared with on-premise predecessors.

Emergence of Consumer-Driven Health-Data Ownership Models

Patients increasingly expect seamless access to and control over their own records. U.S. rules now compel providers to furnish electronic data through API-enabled apps. As mobile health adoption rises, patient-led data exchange is transforming the traditional provider-centric model. Healthcare organizations respond with enhanced portal functionalities and digital front doors that allow individuals to authorize data sharing with specialists, researchers, or fitness apps.

Restraints Impact Analysis of Healthcare Information Exchange Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment for interoperability infrastructure | -1.4% | Global, especially smaller providers | Medium term (2-4 years) |

| Persistent data privacy and cybersecurity threats | -2.2% | Worldwide, heightened in North America & EU | Short term (≤ 2 years) |

| Fragmented standards and vendor information-blocking practices | -1.5% | Global | Medium term (2-4 years) |

| Limited technical expertise in small and rural provider settings | -1.0% | Rural and underserved areas worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment for Interoperability Infrastructure

Joining an exchange often demands substantial upfront fees, staff training, and multi-vendor interface development. Rural hospitals with thin margins struggle to justify large expenditures without clear reimbursement incentives. Even when funding is available, project complexity can delay tangible benefits, leading some organizations to stagger roll-outs or limit participation. Hybrid models reduce—but do not eliminate—capital pressure, as local hardware is still required for edge processing and business-continuity planning.

Persistent Data Privacy and Cybersecurity Threats

Healthcare remains a lucrative target for cybercriminals. The Change Healthcare ransomware incident exposed 190 million records and cost an estimated USD 3.1 billion to remediate. Such breaches intensify provider hesitation to share data widely, fearing reputational harm and regulatory fines. Regulators respond with tougher penalty regimes, pushing organizations to invest in zero-trust frameworks and continuous-monitoring services. These added security obligations slow onboarding and inflate total cost of ownership for exchange platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Healthcare Information Exchange Market Segment Analysis

By Implementation Model:

Hybrid Deployments Drive Future GrowthCentralized architectures retained 46.20% of health information exchange market share in 2025, favored for straightforward governance and simpler vendor management. Yet hybrid frameworks are pacing at a 13.12% CAGR, reflecting mounting concern over single points of failure. The health information exchange market size for hybrid deployments is projected to expand sharply as hospitals keep sensitive data on-site while using cloud nodes for national connectivity. Change Healthcare’s outage illustrated the risks of over-centralization, prompting board-level discussions on resiliency. Hybrid adopters also value the ability to migrate incrementally, avoiding major downtime. Vendors are releasing modular toolkits that allow local data residency alongside FHIR-based cloud services. This dual-layer model supports disaster recovery, reduces latency for bedside applications, and meets data-localization mandates in Europe and Asia.

Growth momentum indicates hospitals will favor flexible topologies that evolve with regulatory requirements. As TEFCA connectivity matures, hybrid participants can peer with nationwide networks without relinquishing local database control. Meanwhile, federated implementations persist among institutions operating in jurisdictions with stringent sovereignty rules, such as Germany and India. Collectively, these dynamics position the hybrid configuration as a bridge between traditional on-premise systems and fully hosted solutions, ensuring the health information exchange market retains deployment-model diversity through 2031.

By Setup Type:

Public Sector AccelerationPrivate exchanges accounted for 61.90% of the health information exchange market size in 2025, largely driven by hospital networks seeking bespoke workflows. Public HIE programs, however, are forecast for a 14.15% CAGR, buoyed by federal and state grants that lower barriers for safety-net clinics. CDC’s Data Modernization Initiative exemplifies this shift, underwriting cloud migration costs for public-health nodes. The European Health Data Space takes a similar stance, assigning national authorities to spearhead infrastructure build-out. Public platforms increasingly facilitate syndromic surveillance and chronic-disease registries, functions often overlooked in private systems.

As a result, governments are setting architectural baselines that private stakeholders must match, thereby lifting overall interoperability maturity. Smaller physician groups benefit from no-cost onboarding, gaining access to wider referral networks and decision-support assets. These factors collectively raise the profile of public exchanges, gradually rebalancing market composition while reinforcing the societal value of open data sharing.

By Application:

Workflow Management Leads, AI Applications SurgeWorkflow-management tools dominated with 34.20% of health information exchange market share in 2025 as providers fought staffing shortages and administrative overhead. Secure messaging, order reconciliation, and discharge summaries remain daily necessities, anchoring budget allocations. Nevertheless, AI-driven clinical-decision modules within the “other applications” bucket are registering a 13.55% CAGR. Epic’s addition of more than 100 AI features underscores the pivot toward intelligent automation. These capabilities mine longitudinal patient data to suggest medication adjustments, predict deterioration, and reduce manual chart review.

Investment in advanced analytics signals a broader intent to turn raw data into actionable insight. As predictive models prove clinical value, stakeholders expect reimbursement mechanisms to recognize decision-support outcomes, further stimulating adoption. Consequently, the health information exchange market is expanding from a transactional data-bus concept into a strategic intelligence layer, embedding analytics at the point of care.

By Exchange Type:

Consumer-Mediated Growth AcceleratesQuery-based exchange remained largest at 41.10% of health information exchange market share in 2025, critical for emergency departments needing instant patient histories. Direct-trust protocols still facilitate routine referrals, but consumer-mediated exchange is projected to climb 13.08% CAGR through 2031. Application-programming-interface access lets patients aggregate records from multiple portals into smartphone apps, reflecting rising consumer expectations. U.S. rulemaking now penalizes information blocking, forcing hospitals to deliver data to any app chosen by the patient.

Payers see an opportunity to embed member engagement solutions that integrate claims and clinical data, improving chronic-disease management. Device makers also plan to sync wearable data with exchange networks, creating a feedback loop between home monitoring and clinical decision-making. This patient-centric movement promises to widen the data mix flowing through platforms, elevating privacy and consent management to core competencies.

By Component:

Clinical Data Repositories Drive InnovationEnterprise Master Person Index modules led components with 29.40% market share in 2025, underscoring the non-negotiable need for accurate patient matching. Yet clinical data repositories show the fastest expansion at 14.39% CAGR, as organizations aggregate longitudinal histories to support population-health dashboards. Health plans leverage repositories to stratify risk, while research consortia mine de-identified cohorts for precision-medicine studies. Vendors now bundle high-speed analytics engines with repository licenses, enabling real-time quality-measure reporting.

Record locator services and provider directories continue to underpin care coordination, but they are now integrated into broader suites rather than sold as stand-alone modules. Emerging add-ons—blockchain security layers, homomorphic-encryption toolkits, and federated-learning hubs—signal how the health information exchange market will extend component architecture to meet specialized security and research demands.

By End User:

Payers Drive Fastest ExpansionProviders generated 56.85% of 2025 revenue, given their frontline role in data generation. Public-health agencies remain steady participants thanks to pandemic-era reporting mandates. Payers, however, are forecast to grow at 14.30% CAGR as they deepen involvement in risk-bearing arrangements. Integrated health systems use shared platforms to align care-coordination workflows with claims adjudication, reducing discord between clinical and financial processes. Payers also seek to harness real-time data to trigger member outreach, detect fraud, and support value-based contracts.

This acceleration alters vendor roadmaps, prompting feature sets tailored to actuarial analytics, prior-authorization automation, and secure bidirectional data feeds. The health information exchange industry thereby becomes a linchpin for payer-provider convergence strategies, positioning exchange vendors at the nexus of clinical and financial transformation.

Geography Analysis

North America Healthcare Information Exchange Market

North America retained 47.10% of 2025 revenue, driven by comprehensive regulatory mandates and robust federal funding. TEFCA adoption is expanding quickly as Epic Systems connects more than 1,000 hospitals through standardized APIs. Canada and Mexico add further growth, supported by national telehealth investments. The USD 3.1 billion fallout from the Change Healthcare breach spurred hospital boards to increase cybersecurity budgets, reinforcing exchange subscriptions viewed as essential infrastructure.

Europe Healthcare Information Exchange Market

Europe is reshaping its data-sharing landscape under the European Health Data Space regulation, which earmarked EUR 810 million for cross-border exchange readiness through 2031. Countries such as Finland already demonstrate mature nationwide services through the Kanta platform, acting as blueprints for other member states. The EHDS framework introduces standardized consent mechanisms that balance innovation with privacy, prompting vendors to enhance data-protection modules for the regional market.

APAC Healthcare Information Exchange Market

Asia-Pacific, the fastest-growing region at 12.21% CAGR, benefits from heavy public investment and demographic pressures. Japan’s national platform build-out, Australia’s My Health Record enhancements, and India’s flagship Ayushman Bharat Digital Mission illustrate government commitment. Cloud-native deployments allow emerging markets to skip legacy hardware phases, creating fertile ground for new entrants. Venture capital flows to telehealth and hospital-at-home models also stimulate demand for real-time data orchestration, bolstering the region’s contribution to overall health information exchange market growth.

Competitive Landscape

The market exhibits moderate consolidation, with Epic Systems expanding its lead through TEFCA connectivity and consistent customer-satisfaction scores. Epic added 176 U.S. hospitals in 2024 while Oracle Health lost 74 sites as upgrades stalled. InterSystems and Health Catalyst pursue a best-of-breed strategy, focusing on specialized analytics and data-repository performance. M&A activity is accelerating: HEALWELL AI’s April 2025 acquisition of Orion Health formed a global interoperability and AI powerhouse, and Centauri Health Solutions acquired MedAllies to strengthen direct-messaging capabilities.

Competitive differentiation now hinges on vendor partnership models, security credentials, and multi-cloud resiliency rather than mere interface counts. Emerging opportunities include consumer-mediated exchange apps, blockchain-secured networks, and AI-native decision-support platforms. Vendors that pair robust cybersecurity with rapid innovation are best positioned to capture the next wave of health information exchange market demand.

Healthcare Information Exchange Industry Leaders

Epic Systems Corporation

Oracle Cerner Corporation

Veradigm, Inc.

InterSystems Corporation

Orion Health

- *Disclaimer: Major Players sorted in no particular order

Healthcare Information Exchange Market Companies Covered in this Report

- Epic Systems

- Oracle Cerner Corporation

- Veradigm, Inc.

- Intersystems

- Orion Health

- Meditech

- eClinicalWorks

- Optum Insight

- Change Healthcare

- NextGen Healthcare

- OpenText

- Infor

- Koninklijke Philips

- Axway

- Health Catalyst

- 4medica

- Verato

- Konica Minolta Healthcare

- CliniComp

- Orchestrate Healthcare

Recent Industry Developments in Healthcare Information Exchange Market

- April 2025: HEALWELL AI completed acquisition of Orion Health, creating an interoperability and AI leader Healwell AI.

- April 2025: Centauri Health Solutions acquired MedAllies, adding messaging and record-location services across 1,000+ hospitals FinSMEs.

- March 2025: The European Union published the European Health Data Space regulation, allocating EUR 810 million for implementation through 2031 Arnold & Porter.

- January 2025: U.S. HHS finalized HTI-2 and HTI-3 rules establishing TEFCA governance and reproductive-health data protections Ropes & Gray.

- December 2024: Epic Systems reported 625 hospitals connected to TEFCA and targeted full-community transition by end-2025 Epic.

Healthcare Information Exchange Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global Healthcare Information Exchange (HIE) market as every cloud-hosted or on-premise platform, integration middleware, and managed service that moves structured clinical or administrative data among unaffiliated providers, payers, public health agencies, and patients in near-real time. Transfers cover directed referrals, query-based record pulls, and consumer-mediated sharing.

Scope Exclusions: stand-alone EHR modules kept inside one enterprise, analytics dashboards that never export data, and networking hardware.

Segments Covered in This Report

- By Implementation Model

- Centralized / Consolidated

- Decentralized / Federated

- Hybrid

- By Setup Type

- Private

- Public

- By Application

- Internal Interfacing

- Secure Messaging

- Workflow Management

- Web Portal Development

- Other Applications

- By Exchange Type

- Direct Exchange

- Query-Based Exchange

- Consumer-Mediated Exchange

- By Component

- Enterprise Master Person Index (EMPI)

- Healthcare Provider Directory (HPD)

- Record Locator Service (RLS)

- Clinical Data Repository

- Other Components

- By End User

- Public Health Agencies

- Healthcare Providers

- Payers & Health Plans

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with hospital CIOs, payer IT leads, state HIE officers, and regional integrators across North America, Europe, and Asia-Pacific. Their insight on license fees, hybrid uptake rates, and policy timelines replaced uncertain desk inputs with firsthand detail and helped us fine-tune assumptions.

Desk Research

We began with open government sets such as the ONC interoperability dashboard, Eurostat eHealth tables, and Japan-MHLW facility surveys because they anchor HIE adoption ratios for our baseline. Peer-reviewed articles in JAMIA and HIMSS briefs clarified workflow bottlenecks that shape upgrade timing, while company 10-Ks and respected media revealed contract sizes.

Our team then tapped paid resources, D&B Hoovers for private revenue splits and Dow Jones Factiva for deal flow, and matched them against customs filings where software exports appear. The sources named are illustrative; many additional repositories strengthened data checks.

Market-Sizing & Forecasting

A top-down demand pool built from provider counts, EHR penetration, and HIE adoption ratios fixed the 2025 baseline, and one selective bottom-up roll-up of average connection fees multiplied by active nodes served as a sense check. Key drivers in our model include acute-care beds, payer enrollment, TEFCA rollout milestones, cloud migration share, and average per-node license price. Multivariate regression, supplemented by scenario analysis, projects 2025-2030 values.

Data Validation & Update Cycle

Outputs face a second analyst audit; variance above three percentage points triggers rework before team lead sign-off. We refresh numbers annually and issue interim updates whenever major policy or M&A events reshape fundamentals.

How Mordor Intelligence's Healthcare Information Exchange Market Size Compares to Other Published Estimates

Published totals often diverge, and Mordor Intelligence recognizes that scope width, currency timing, and treatment of publicly funded exchanges drive most gaps.

Because our model counts payer spend, hybrid deployments, and year-specific exchange rates, it narrows variance and raises confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.20 billion (2025) | Mordor Intelligence | - |

| USD 1.70 billion (2024) | Global Consultancy A | Hybrid setups omitted; constant 2023 FX |

| USD 1.60 billion (2024) | Industry Analytics B | Payer spend excluded |

| USD 4.23 billion (2024) | Trade Journal C | Includes hardware and broader tools |

The comparison shows that our balanced scope, timely currency calibration, and dual-path validation give decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is driving the rapid growth of the health information exchange market?

Strong regulatory mandates, rising cybersecurity investments, and the shift to value-based care are expanding adoption, resulting in an 11.62% CAGR through 2031.

Which implementation model is growing fastest?

Hybrid deployments, which balance local data control with cloud scalability, are expanding at a 13.12% CAGR.

How big is the health information exchange market size today?

The market stands at USD 2.46 billion in 2026 and is forecast to reach USD 4.25 billion by 2031.

Which region leads the health information exchange market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Healthcare Information Exchange Market?

North America holds 47.10% of 2025 revenue thanks to TEFCA roll-outs and federal funding.

What role do payers play in future growth?

Payers are the fastest-growing end-user group at 14.30% CAGR as they require comprehensive patient data for risk-sharing and care-management programs.

What is the biggest restraint to market expansion?

Persistent cybersecurity threats, exemplified by the Change Healthcare breach, remain the primary barrier, reducing forecast CAGR by an estimated 2.2%.

Page last updated on: