Small-scale Bioreactors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.34 Billion |

| Market Size (2030) | USD 3.25 Billion |

| Growth Rate (2025 - 2030) | 7.04% CAGR |

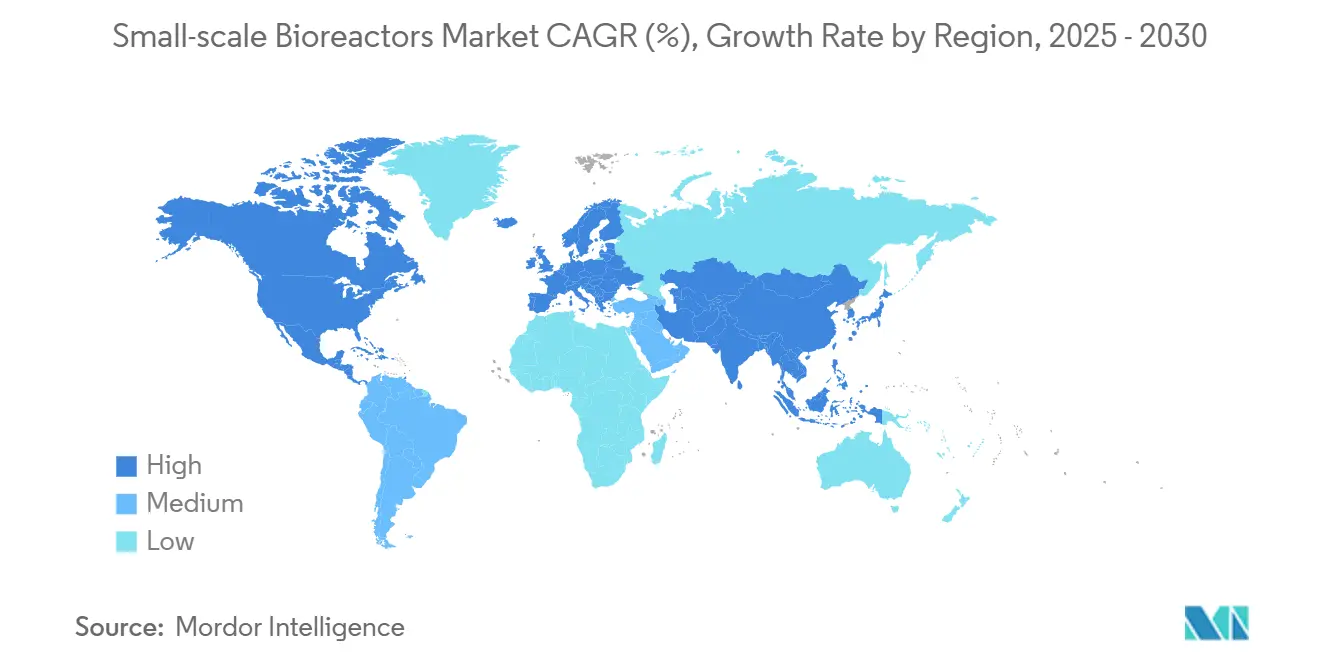

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

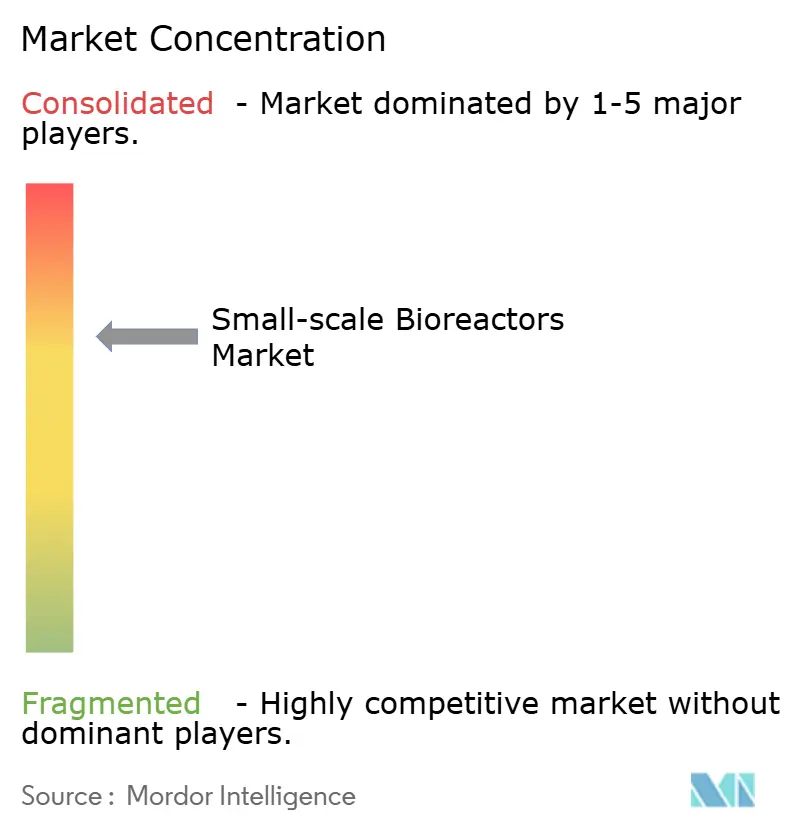

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small-scale Bioreactors Market Analysis by Mordor Intelligence

The small-scale bioreactors’ market size stands at USD 2.34 billion in 2025 and is forecast to reach USD 3.25 billion by 2030, advancing at a 7.04% CAGR. Growth rests on three pillars: faster biologics pipelines, wider use of single-use components, and new cultured-meat applications. North American manufacturers benefit from favorable U.S. regulatory programs, while Asia Pacific suppliers ride large government investment waves. Continuous processing and AI-driven digital twins shorten development cycles, pushing demand for well-instrumented bench systems. Consolidation among equipment vendors is reshaping the supply of power and accelerating innovation.

Key Report Takeaways

- By technology, single-use systems held a 66.9% small-scale bioreactors market share in 2024 and are expanding at an 8.5% CAGR through 2030.

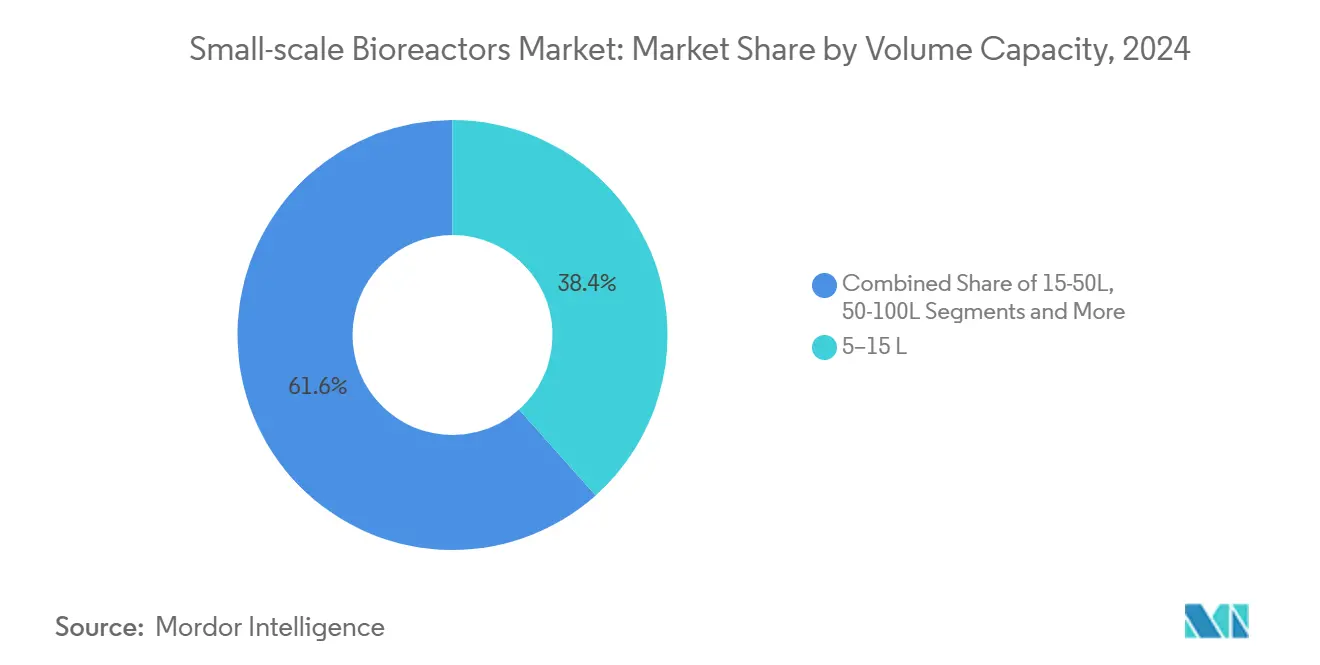

- By volume capacity, the 5–15 L class captured 38.4% of the small-scale bioreactors market share in 2024, whereas sub-5 L units are set to advance at a 6.7% CAGR to 2030.

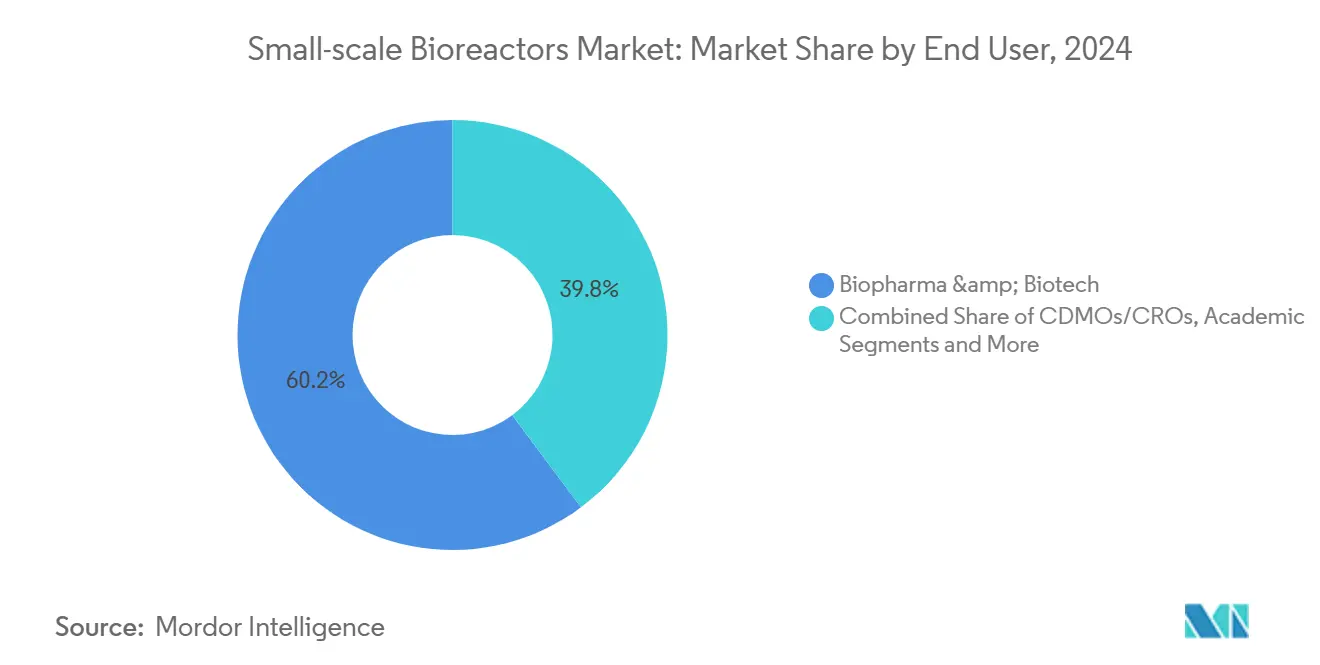

- By end user, biopharma and biotech firms accounted for 60.2% of demand in 2024, yet food and agri-biotech users are heading for a 7.2% CAGR up to 2030.

- By geography, North America led with 38.1% revenue share in 2024, while Asia Pacific is projected to grow at a 9.1% CAGR during 2025-2030.

Global Small-scale Bioreactors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of Single-Use Bench & Mini Bioreactors | +2.10% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Rising Biologics & Cell-Therapy R&D Spend | +1.80% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Need For High-Throughput Parallel Screening | +1.20% | Global, concentrated in pharma hubs | Short term (≤ 2 years) |

| Shift Toward Continuous & Intensified Bioprocessing | +0.90% | North America & EU, selective APAC adoption | Medium term (2-4 years) |

| Integration Of AI-Driven Digital-Twin Control | +0.80% | Advanced markets: US, Germany, Japan | Long term (≥ 4 years) |

| Cultured-Meat And Cellular-Ag Start-Up Demand | +0.60% | Global, with Singapore and Netherlands leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Single-Use Bench & Mini Bioreactors

Pharmaceutical developers are replacing stainless-steel rigs with fully disposable vessels to eliminate cross-contamination risk and compress changeover time to under one hour. The approach also removes the cost and delay of cleaning validation, freeing capacity in multi-product plants. Regulators back this shift; the U.S. FDA’s 2025 guidance calls out advanced manufacturing technologies that improve uniformity and patient safety.[1]ECA Academy, “New FDA Guidelines: Batch Uniformity and Drug Product Integrity,” gmp-compliance.org Lower facility footprints further strengthen the financial case, especially for CMOs juggling many low-volume biologics. Together, these factors propel the small-scale bioreactors market toward more flexible, disposable architectures.

Rising Biologics & Cell-Therapy R&D Spend

Capital continues to flow into biologics pipelines as firms chase complex diseases beyond small-molecule reach. German biotech financing surged 78% in 2024, a signal echoed across mature markets.[2]BIO Deutschland Staff, “Biotechnologie auf Erfolgskurs: Deutlicher Anstieg der Finanzierungen in Deutschland,” BIO Deutschland, biodeutschland.org Small-scale systems bridge the gap between discovery labs and commercial plants by enabling rapid process-parameter mapping. Cell-therapy workflows depend on these bench reactors because each batch is patient-specific and requires tight control. Long product cycles mean developers revisit bench equipment throughout clinical phases, sustaining replacement demand and service revenue.

Need for High-Throughput Parallel Screening

Twenty-four-vessel micro-bioreactor arrays, such as Ambr 250 Perfusion, let scientists explore dozens of variables in days, cutting development timelines by up to 50%. Larger datasets yield more predictive design spaces, satisfying regulators who expect robust statistical evidence. Although initial capital is higher, the time savings outweigh the cost for blockbuster programs. Adoption accelerates as companies race to be first-in-class in crowded antibody and gene-therapy fields, supporting a virtuous cycle for ever-smaller, smarter reactors.

Shift Toward Continuous & Intensified Bioprocessing

Continuous culture reduces facility footprint and work-in-progress inventories, aligning with FDA initiatives that reward real-time quality monitoring.[3]BioProcess Online Staff, “What FDA Draft Guidance Tells Us About In-Process Control Strategies,” BioProcess Online, bioprocessonline.comTo qualify, producers run extensive benchtop studies that de-risk perfusion, high-cell-density, and advanced feeding strategies. Bench reactors with integrated sensors validate control loops long before pilot scale, locking in room for iterative improvement. Intensification also benefits biosimilar producers under price pressure, accelerating uptake in both mature and emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced micro-sensors & controllers | -1.10% | Global, acute for small firms | Short term (≤ 2 years) |

| Scale-up predictive-accuracy limitations | -0.70% | Worldwide, worse for complex biologics | Medium term (2-4 years) |

| Stringent plastic-waste regulations on disposables | -0.50% | Europe first, global follow-on | Long term (≥ 4 years) |

| Polymer-film supply-chain bottlenecks | -0.40% | Global, Asia Pacific manufacturing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Micro-Sensors & Controllers

Fully integrated sensor suites can add USD 10,000-50,000 per bench vessel, pushing budgets beyond many start-ups. Parallel configurations multiply that expense, straining cash in the discovery stage. Maintenance and calibration bring ongoing charges, forcing smaller labs to settle for less-granular monitoring. This cost gap creates a two-tier landscape where cash-rich pharma gains data advantages, while academic groups and small firms risk slower progress, tempering overall market velocity.

Scale-Up Predictive-Accuracy Limitations

Fundamental differences in mixing and oxygen transfer between 2 L and 2,000 L reactors mean benchtop data do not always translate, leading to costly pilot reruns. Shear-sensitive gene-therapy cultures are especially vulnerable. Developers hedge by running extra-scale steps, which dilute the time savings promised by small-scale bioreactors. Although CFD modeling and digital twins improve projections, these tools remain expensive and skill-intensive, prolonging adoption among resource-constrained teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Volume Capacity: Miniaturization Drives Innovation

Sub-5 L units logged the fastest 6.7% CAGR, propelled by high-throughput screening for antibodies and gene vectors. In contrast, 5–15 L formats captured 38.4% of the small-scale bioreactors market size in 2024 due to their balance of throughput and scale relevance. Pharmaceutical teams appreciate the space efficiency of micro-reactors that pack dozens of experiments in a single hood. Yet when the tech-transfer stage approaches, scientists still gravitate to the 10 L sweet spot that mirrors full-scale geometry more closely. Smaller capacity growth also reflects rising cellular-ag experiments that seldom exceed grams-per-day outputs during proof-of-concept phases.

Larger brackets—15-50 L, 50-100 L, and 100-250 L—serve niche pilot and personalized medicine campaigns. A 3D cell expansion system capable of 500 million cells per run illustrates how design innovations compress hardware footprints. Automation layers, such as robotic sampling, lower staffing needs, and sharpen batch-to-batch reproducibility. Collectively, miniaturization and automation encourage iterative cycles, driving sustained upgrades across the small-scale bioreactors market.

By Technology: Single-Use Systems Reshape Manufacturing

In 2024, single-use rigs controlled 66.9% of the small-scale bioreactors market and posted an 8.5% growth trajectory as facilities chase speed and sterility gains. The value proposition intensifies in multi-product suites, where washing stainless lines can idle capacity for days. Glass remains relevant for optical monitoring tasks, whereas stainless steel wins at very high titers, where bag costs rise sharply.

Hybrid and 3D-printed vessels are carving footholds among start-ups that need custom geometries or rapid iterations. Regulators signal support; the FDA’s 2025 cGMP update highlights disposables that cut operator exposure and batch variability. Consequently, procurement teams embed single-use compatibility into all new plant specifications, cementing dominance across the small-scale bioreactors market.

By End User: Food Tech Emerges as Growth Engine

Biopharma and biotech players consumed 60.2% of units in 2024, particularly for monoclonal antibody screening and cell-therapy characterization. Yet food and agri-biotech firms top the growth table with a 7.2% CAGR, spurred by precision fermentation proteins and lipid fermentation for cocoa and coffee substitutes.

Contract development and manufacturing organizations (CDMOs) attract customers who lack in-house reactors. The U.S. Biosecure Act’s limits on Chinese suppliers push Western sponsors toward Indian CRDMOs, whose revenues could reach USD 26.73 billion by 2028. Academia remains a steady buyer, although grant cycles constrain premium sensor adoption. This multipronged demand sustains healthy order pipelines for both entry-level and feature-rich models across the small-scale bioreactors industry.

Geography Analysis

North America retained 38.1% revenue in 2024, underpinned by the U.S. FDA’s Advanced Manufacturing Technologies Designation Program, which shortens review queues for companies employing innovative equipment. American venture capital channels cash into cell-therapy start-ups, while Canada promotes biomanufacturing grants to diversify supply away from China. Mexico benefits from cost-competitive contract production aligned to U.S. quality standards.

Asia Pacific delivers the fastest 9.1% CAGR to 2030, driven by China’s USD 4.17 billion state investment in 2024 and follow-up allocations slated for 2025. India leverages the BioE3 framework and the Biosecure Act tailwinds to market itself as a scaling hub for Western sponsors. Japan, South Korea, and Australia invest in mRNA vaccine capacity, crystallizing regional demand for advanced benchtop vessels.

Europe holds steady through robust German financing, hitting EUR 1.917 billion in 2024, and an EU biotech roadmap advocating smoother regulatory pathways. Scandinavian governments fund sustainable food-tech pilots, adopting small-scale disposables to validate alternative protein recipes quickly. Middle East & Africa and South America expand more modestly due to limited cold-chain networks and scarce specialist talent, yet greenfield vaccine initiatives in Saudi Arabia and Brazil could unlock pockets of accelerated orders later this decade.

Competitive Landscape

The small-scale bioreactors market is moderately consolidated, with the top five suppliers holding significant global revenue in 2024. Danaher fused Cytiva and Pall in a USD 7.5 billion transaction that created the sector’s most extensive integrated portfolio from cell-line development tools to downstream filters. Ecolab entered upstream equipment through a USD 3.7 billion Purolite purchase, highlighting purification synergies that anchor turnkey offerings. Agilent’s USD 925 million BIOVECTRA acquisition adds lipid nanoparticle and sterile fill capabilities that mesh with mRNA workflows.

Competition tilts toward automation depth, software openness, and sensor embeddedness. Vendors bundle inline Raman probes, self-cleaning sampling robots, and AI dashboards that predict titer drift. Benchtop digital twins cut process-transfer errors, giving early adopters faster IND submissions and improved facility utilization. As customers pursue continuous processing, suppliers integrate perfusion-ready connectors and low-shear impellers that mimic factory tanks. Players also localize component molding to mitigate polymer-film shortages, investing in U.S. and European extrusion lines to bypass geopolitical risk.

Disruptive entrants emerge from academia; German start-up BioThrust adapts artificial lung design to boost oxygen transfer while reducing foaming. Indian engineering firms co-develop modular skid packages that align with Biosecure Act sourcing rules, winning pilot projects from U.S. vaccine makers. Strategic partnerships proliferate; SciY folded Optimal Industrial Technologies into a lab digitalization suite that aggregates multi-vendor data and feeds AI models. Together, these moves elevate technology baselines and maintain brisk upgrade cycles across the small-scale bioreactors market.

Small-scale Bioreactors Industry Leaders

Sartorius Stedim Biotech

Thermo Fisher Scientific

Danaher

Eppendorf AG

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Danaher Corporation (Cytiv) launched the Xcellerex X-platform bioreactor, which is designed for regulated manufacturing processes.

- March 2025: Danaher took a significant step by merging the Cytiva and Pall portfolios under the Cytiva brand. This move created a USD 7.5 billion bioprocess entity with the most comprehensive bioreactor portfolio in the industry, covering everything from bench-scale to commercial production systems.

- March 2024: Sartorius introduced the Ambr 250 High Throughput Perfusion system, which supports up to 24 parallel single-use bioreactors with 100-250 mL working volumes. This innovation enables faster development of scalable perfusion processes.

- February 2024: Sartorius launched the Univessel SU stirred tank single-use bioreactor, offering a working volume range of 0.6-2L. With fully single-use components, it allows turnaround times of less than an hour.

Global Small-scale Bioreactors Market Report Scope

| Less Than 5 L |

| 5 -15 L |

| 15- 50 L |

| 50 - 100 L |

| 100 - 250 L |

| Single-use (polymer) |

| Glass |

| Stainless steel |

| Hybrid / 3-D-printed |

| Others |

| Biopharma & Biotech Companies |

| CDMOs / CROs |

| Academic & Research Institutes |

| Food & Agri-biotech Firms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Volume Capacity | Less Than 5 L | |

| 5 -15 L | ||

| 15- 50 L | ||

| 50 - 100 L | ||

| 100 - 250 L | ||

| By Technology | Single-use (polymer) | |

| Glass | ||

| Stainless steel | ||

| Hybrid / 3-D-printed | ||

| Others | ||

| By End User | Biopharma & Biotech Companies | |

| CDMOs / CROs | ||

| Academic & Research Institutes | ||

| Food & Agri-biotech Firms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the small-scale bioreactors market?

The small-scale bioreactors market size is USD 2.34 billion in 2025 with a forecast value of USD 3.25 billion by 2030.

Which technology segment leads revenue in small-scale bioreactors?

Single-use systems dominate with 66.9% market share in 2024 and retain the fastest CAGR at 8.5%.

Which region is expanding fastest in small-scale bioreactors?

Asia Pacific is projected to grow at a 9.1% CAGR through 2030, driven by Chinese and Indian biomanufacturing investments.

Why are sub-5 L reactors gaining popularity?

They support high-throughput screening that cuts biologics development timelines by up to 50%, pushing a 6.7% CAGR for the segment.

How is regulation shaping bioreactor demand?

FDA and EU guidance endorses continuous processing and advanced sensors, motivating firms to upgrade to more instrumented small-scale rigs.

Who are the key consolidators in the market?

Danaher, Ecolab, and Agilent are leading consolidation with multibillion-dollar acquisitions that broaden end-to-end bioprocess portfolios.

Page last updated on: