Biosurgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

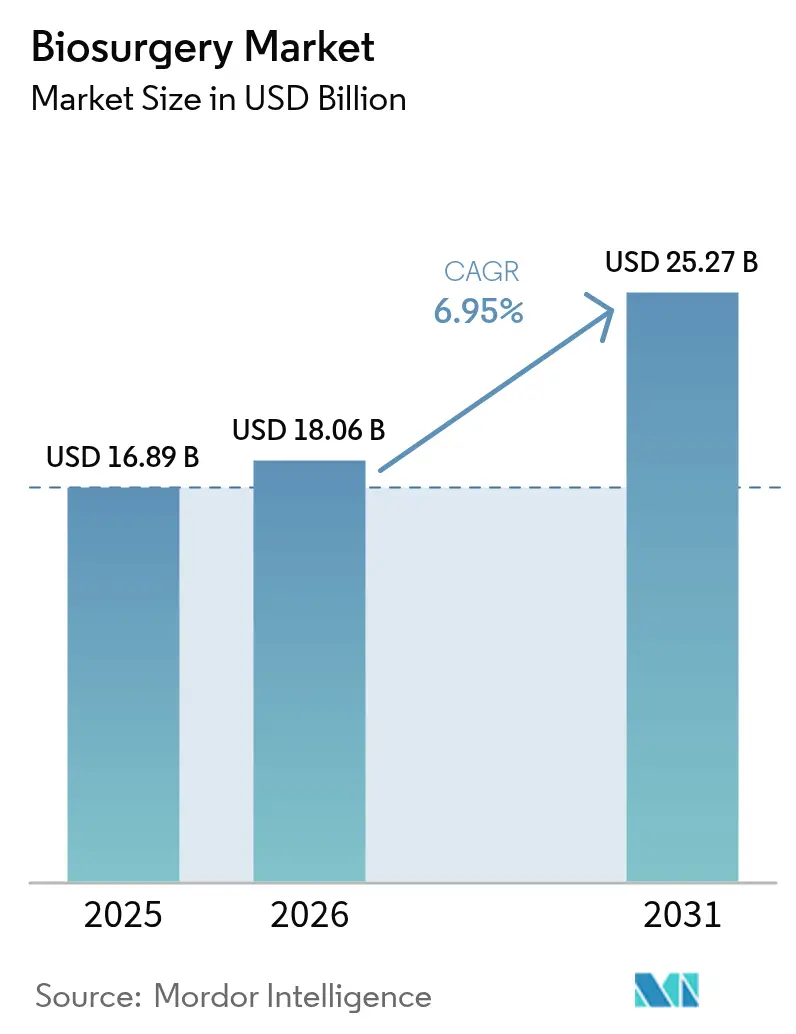

| Market Size (2026) | USD 18.06 Billion |

| Market Size (2031) | USD 25.27 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

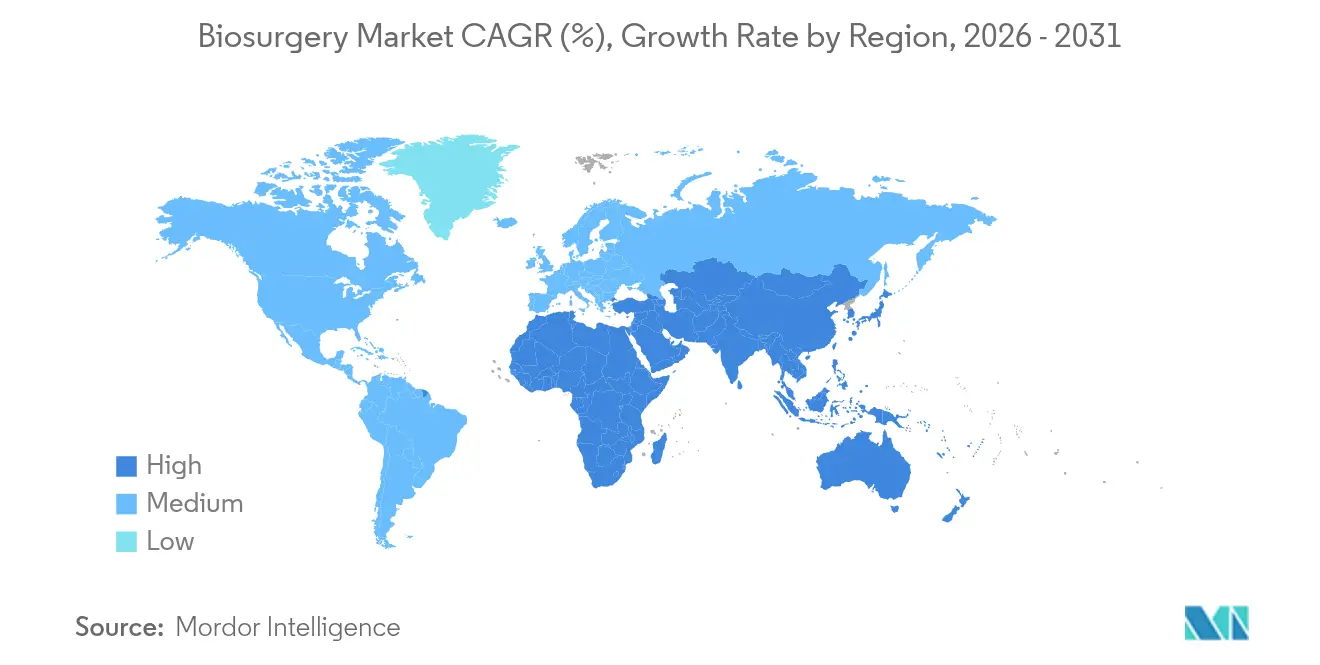

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

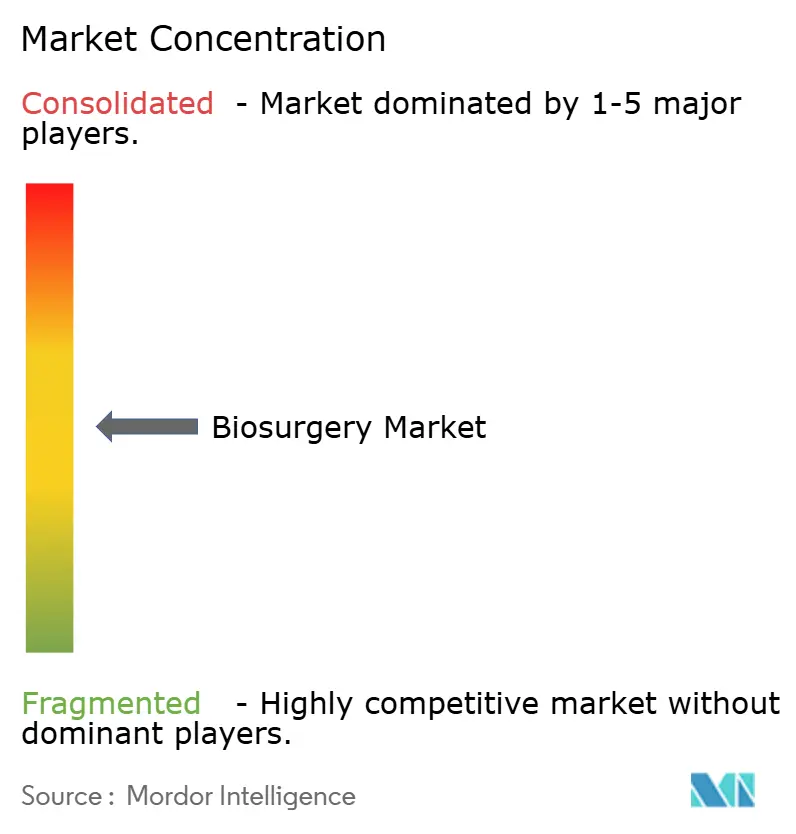

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biosurgery Market Analysis by Mordor Intelligence

Biosurgery Market size in 2026 is estimated at USD 18.06 billion, growing from 2025 value of USD 16.89 billion with 2031 projections showing USD 25.27 billion, growing at 6.95% CAGR over 2026-2031.

This expansion reflects the combined impact of population aging, higher surgical complexity, and widespread adoption of minimally invasive techniques that demand refined solutions for hemostasis, tissue repair, and wound closure. Hospitals are intensifying their focus on rapid‐recovery protocols, which elevates demand for next-generation biomaterials that shorten operating times and curb transfusions. Meanwhile, real-time 3-D-printed, bioresorbable scaffolds are making patient-specific implants economically viable, strengthening the biosurgery market’s momentum. The rise of hospital-at-home models, supported by new Medicare coding for caregiver wound-care training, is shifting a portion of postoperative care into residential settings, creating fresh opportunities for portable sealing and adhesive kits. North America leads in reimbursement sophistication, yet Asia-Pacific’s accelerating surgical volumes position it as the fastest-growing region through 2030. Competitive pressure is moderate but mounting as specialized innovators challenge long-standing incumbents with smart biomaterials and digital-enabled surgical platforms.

Key Report Takeaways

- By product type, bone-graft substitutes held 32.97% of the biosurgery market share in 2025, while surgical sealants and adhesives are forecast to expand at a 7.55% CAGR to 2031.

- By source, biologic products commanded 61.24% revenue in 2025; synthetic and semi-synthetic alternatives are advancing at an 8.29% CAGR through 2031.

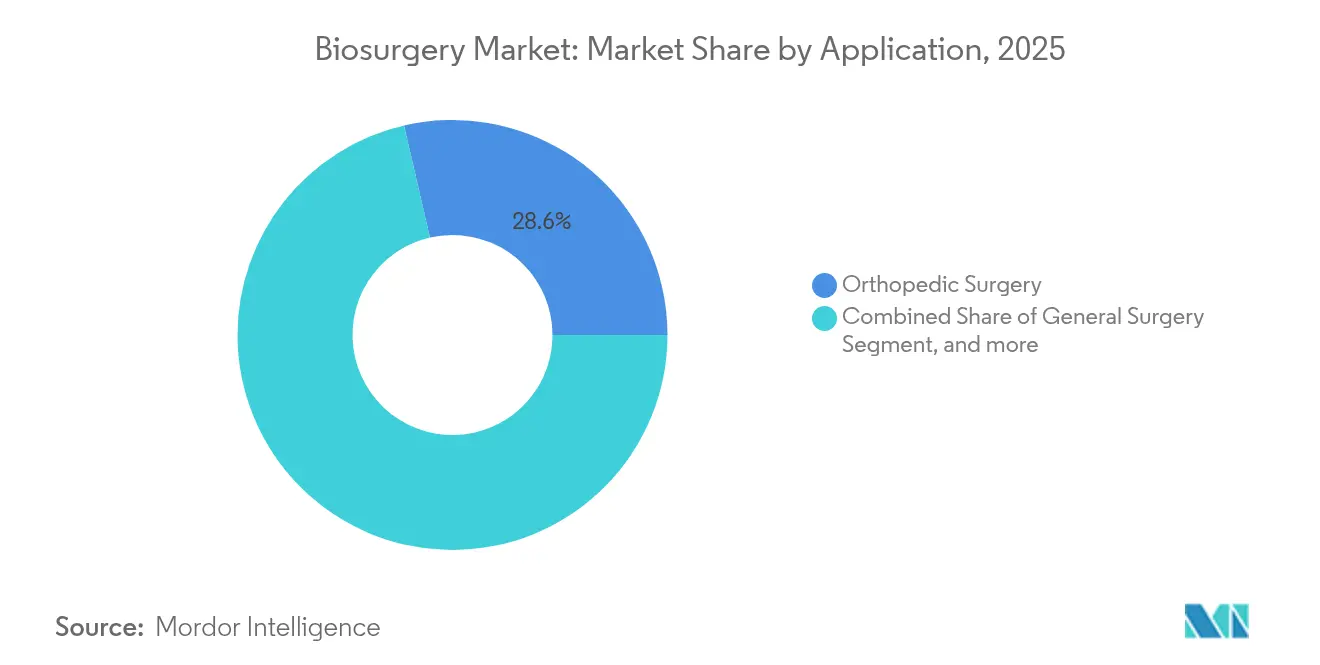

- By application, orthopedic surgery accounted for 28.62% of the biosurgery market size in 2025, whereas cardiovascular surgery is growing fastest at a 8.82% CAGR through 2031.

- By end user, hospitals controlled 67.47% of 2025 revenue; ambulatory surgical centers are projected to grow at an 8.35% CAGR to 2031.

- By geography, North America led with 41.34% share in 2025; Asia-Pacific is set to rise at an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biosurgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging geriatric & co-morbid patient pool | +1.8% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Rise in complex & minimally invasive surgical volumes | +1.5% | Global; led by North America & Asia-Pacific | Medium term (2–4 years) |

| Pipeline of next-gen biomaterials & combination products | +1.2% | North America & Europe; expanding in Asia-Pacific | Medium term (2–4 years) |

| Hospital-at-home reimbursement for rapid wound-closure kits | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Point-of-care 3-D-printed, bioresorbable scaffolds | +0.6% | North America & Europe; early Asia-Pacific uptake | Medium term (2–4 years) |

| Supplier localisation of plasma-derived sealants | +0.4% | Asia-Pacific & emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Geriatric & Co-Morbid Patient Pool

The median age of surgical patients climbed from 56 to 59 years between 2008 and 2020 and is projected to reach 61.5 years by 2030, amplifying demand for products that safely control bleeding in fragile tissue.[1]E. Bergeron et al., “Global Surgical Patient Demographics to 2030,” sciencedirect.com Concurrently, obesity prevalence among surgical candidates is increasing, with 80% expected to present above-normal BMI by 2030, further complicating hemostasis. A Geneva tertiary center documented a 48.3% rise in high-risk elderly anesthesia cases over the past decade, underscoring healthcare systems’ willingness to operate on complex geriatric profiles. Complication rates exceed 32% in patients over 90 years when general anesthesia is applied, compared with 19.4% under regional techniques, highlighting the need for advanced, minimally traumatic biosurgical options. These demographic shifts secure long-horizon growth for the biosurgery market.

Rise in Complex & Minimally Invasive Surgical Volumes

Robotic hernia repairs, though under 5% of all repairs in Nordic countries, are climbing steadily, reflecting global adoption of robotic platforms that work within confined anatomical spaces. Laparoscopic and robotic lumbar fusion surgeries show lower complication rates and reduced recovery times than open procedures, but they depend on sealants and adhesives that perform reliably in limited fields.[2]A. Valli et al., “Robotic Hernia Repair in Nordic Countries,” springer.com Cardiovascular settings echo this trend: pulsed-field ablation products yielded nearly 30% revenue growth for a leading manufacturer in 2025, signalling robust uptake of advanced devices that must integrate seamlessly with bioactive adjuncts. As emerging markets invest in robotics and high-definition imaging, the biosurgery market receives another tailwind.

Pipeline of Next-Gen Biomaterials & Combination Products

Programmable 3-D-printed scaffolds that deform at 48 °C to fill defects and modulate macrophage responses at 42 °C illustrate the shift toward dynamic biomaterials. Recombinant human collagen eliminates zoonotic risk while delivering consistent mechanical strength. The FDA cleared multiple platelet-rich-plasma devices in 2024, confirming regulatory openness to autologous products that shorten healing timelines.[3]U.S. FDA, “Premarket Approvals for Platelet-Rich Plasma Devices,” fda.gov Injectable hydrogel platforms now emulate extracellular matrices yet remain deliverable via minimally invasive techniques. Artificial-intelligence tools fine-tune scaffold architecture to individual biomechanics, pushing the biosurgery market from generic to patient-specific solutions.

Hospital-At-Home Reimbursement Accelerating Demand for Rapid Wound-Closure Kits

CMS introduced caregiver-training codes in the 2025 Physician Fee Schedule, validating remote wound-care models. Chronic wounds impact 10.5 million Medicare beneficiaries and cost USD 28 billion annually, driving providers to favor early closure solutions that avoid readmissions. Digital telehealth platforms such as WoundConnect demonstrate that remote monitoring can cut costs and improve outcomes. Venture funding is flowing into apps that guide caregivers through dressing changes and track healing progress in real time. The convergence of reimbursement incentives and digital oversight accelerates uptake of portable sealants and adhesives, bolstering the biosurgery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing & limited reimbursement | -1.1% | Global; sharpest in emerging markets | Medium term (2–4 years) |

| Stringent multi-jurisdiction biologic approval pathways | -0.7% | Worldwide; variable by region | Long term (≥ 4 years) |

| Cold-chain fragility of biologic sealants | -0.5% | Asia-Pacific, MEA & South America | Medium term (2–4 years) |

| Collagen-derived graft contamination & AMR scrutiny | -0.3% | Global; heightened in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing & Limited Reimbursement

CMS plans a 2.93% cut to average wound-care payments in 2025, tightening hospital budgets and pressuring procurement of premium biosurgery products. Autologous platelet-rich plasma lacks consistent reimbursement despite favorable outcomes in diabetic ulcers, prompting clinicians to weigh cost against efficacy. Emerging markets magnify the challenge; Brazil’s import tariffs elevate prices and restrict access to high-end biomaterials. As reimbursement lags innovation, uptake of the newest offerings is uneven, tempering the biosurgery market’s full potential.

Stringent Multi-Jurisdiction Biologic Approval Pathways

The FDA–EMA Parallel Scientific Advice program streamlines some filings, but divergent data requirements mean companies still navigate lengthy, costly paths before launch. Biologics License Applications demand extensive manufacturing validation versus simpler chemical drug filings, stretching development timelines and budgets. Although a 2024 FDA final rule forecasts USD 2.8 million in annual regulatory cost reductions, complexity persists for gene-therapy-adjacent biosurgical innovations. Where regulatory convergence is slow, the biosurgery market faces staggered rollouts and patchy global availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bone-Graft Substitutes Lead Innovation

Bone-graft substitutes captured 32.97% of the biosurgery market share in 2025, owing to escalating orthopedic and dental surgery volumes. The segment benefits from tri-element-doped hydroxyapatite–polycaprolactone scaffolds that inhibit tumor recurrence, foster osteogenesis, and provide inherent antibacterial action. Hemostatic agents remain core staples across specialties, as 54 FDA-approved formulations offer varied formats for open and minimally invasive procedures. Adhesion barriers, typified by SEPRAFILM, decrease repeat operations by limiting fibrous scar formation. While niche, staple-line reinforcement products gain traction alongside robotic surgeries that amplify staple use.

Surgical sealants and adhesives, the fastest-growing product set at 7.55% CAGR, benefit from innovations such as a fibrin sealant that cut transfusions 35% and trimmed operating time by 25 minutes. A room-temperature patch launched in 2025 eliminates refrigeration, easing logistics and broadening reach. LIQUIFIX liquid adhesive, the only FDA-cleared internal hernia sealant, exemplifies device specialization in complex repairs. These breakthroughs highlight how materials science, ease-of-use, and procedure-time savings propel the biosurgery market.

By Source: Biologic Dominance Faces Synthetic Challenge

Biologic offerings commanded 61.24% of 2025 revenue, buoyed by fibrin and collagen matrices that integrate naturally into healing pathways. Demand for plasma-derived medicinal products is projected to climb 30% by 2030, yet collection shortfalls linger, prompting governments to localize plasma supply. Clinical trials such as Grifols’ ADFIRST fibrinogen study underline ongoing biologic innovation.

Synthetic and semi-synthetic materials, however, are outpacing the market at an 8.29% CAGR. Polymer constructs like a fully absorbable P4HB scaffold now in breast revision trials promise durable support without foreign-body permanence. Injectable alginate–collagen hydrogels loaded with antibiotics demonstrated single-dose efficacy equal to multi-dose systemic regimens, mitigating infection risk while curbing overall antibiotic exposure. Rising pharmaceutical cold-chain investment (USD 9.6 billion expected by 2035) underscores biologic distribution hurdles that synthetics circumvent. The biosurgery market thus bifurcates, with biologics prevailing in high-performance indications and synthetics thriving where cost and logistics matter most.

By Application: Orthopedic Surgery Leads, Cardiovascular Accelerates

Orthopedic surgery contributed 28.62% to biosurgery market size in 2025 on the strength of joint replacements and sports-medicine repairs. Customized lattice implants that mirror bone anisotropy are enhancing load distribution and long-term fixation. Platelet-rich-fibrin-coated scaffolds achieved 100% union rates in complex hindfoot procedures, cutting average healing to 20.2 weeks. General surgical applications sustain steady demand for universal hemostatic agents, while neurosurgical matrices such as DuraGen resorb within 34 days, reducing the need for secondary interventions.

Cardiovascular surgery, forecast to grow 8.82% annually, benefits from demographic urgency and advanced energy sources like pulsed-field ablation. Surgical aortic-valve cases are projected to climb annually through 2041 in tertiary centers, adding incremental volume and sealing demand. Gynecologic and thoracic specialties adopt tailored adhesion barriers that cut postoperative adhesions up to 85% in trials. The precision-medicine ethos across these indications deepens reliance on bespoke, outcome-driven biosurgical solutions.

By End User: Hospitals Dominate, ASCs Gain Momentum

Hospitals held 67.47% of 2025 revenue, reflecting their role in high-acuity, multi-disciplinary care. Elderly patients above 90 years experience ICU admissions in 44.6% of general-anesthesia cases, amplifying the need for dependable hemostatic management. July 2024 Outpatient Payment updates added pass-through codes for new skin substitutes, confirming continued hospital alignment with advanced biosurgery technologies.

Ambulatory surgical centers, expanding at an 8.35% CAGR, benefit from lower overhead and a surge in outpatient minimally invasive procedures. Robotics accelerates this migration, while ASCs leverage streamlined inventories that favor versatile, easy-to-use adhesives and patches. Hospital-at-home programs further blur boundaries, allowing ASC clinicians to extend postoperative surveillance via telehealth and remote wound-monitoring systems.

Geography Analysis

North America represented 41.34% of the biosurgery market in 2025, underpinned by robust reimbursement, high procedure volumes, and steady regulatory throughput. Multiple platelet-rich-plasma devices cleared by the FDA in 2024 spotlight the region’s rapid technology adoption. Canada accelerates public-hospital modernization, while Mexico leverages cross-border device supply chains, though regulatory harmonization continues to evolve.

Europe sustains strong uptake of room-temperature sealing patches that bypass cold logistics, widening access especially in midsize hospitals. EMA-FDA cooperative frameworks support simultaneous submissions, yet subtle documentation differences prolong some approvals. Investments in manufacturing automation and sustainability align with the region’s stringent environmental standards, steadily shaping procurement criteria.

Asia-Pacific, forecast at an 8.01% CAGR, is propelled by demographic momentum and infrastructure spend, with the local production initiatives, such as a USD 15 million plasma-collection facility in China, aim to secure supply and meet viral-safety norms. The region confronts fragile cold chains, spurring AI-driven monitoring tools that maintain product integrity in tropical climates. Middle East & Africa and South America trail but show rising procedure rates as public and private insurers broaden surgical coverage; regulatory overhauls in Brazil signal growing regional standardization.

Competitive Landscape

The biosurgery market is moderately competitive and consists of several major players. Market leadership concentrates among diversified multinationals, yet space remains for agile innovators. Johnson & Johnson integrated its med-tech franchises under a single banner and earmarked USD 148.07 billion for technology advancement, reinforcing scale advantages. Medtronic generated USD 33.5 billion in 2025 and plans a diabetes spin-off to sharpen focus on high-growth cardiovascular and surgical segments.

Acquisitions remain pivotal: Stryker’s USD 4.9 billion purchase of Inari Medical opens the peripheral-vascular channel, while BD’s USD 4.2 billion bid for a critical-care portfolio expands its smart-connected-care footprint. Small-cap disruptors such as TELA Bio capitalize on narrow but meaningful gaps, with the only FDA-approved liquid adhesive for internal hernia repairs. The FDA’s acceptance of autologous platelet-rich products reduces entry barriers for niche players.

Platform convergence defines the next competitive stage: firms combining AI-guided planning, on-site 3-D printing, and responsive biomaterials can outmaneuver product-centric rivals. Sustainability is an emerging differentiator, as health systems rank suppliers on carbon and cold-chain footprints. Moderate consolidation paired with rising specialist entrants underpins a dynamic yet balanced biosurgery market.

Biosurgery Industry Leaders

Baxter International Inc.

Johnson & Johnson

Becton, Dickinson and Company

B. Braun Melsungen AG

CryoLife (Artivion)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stryker Corporation announced definitive agreement to acquire Inari Medical for USD 4.9 billion, providing entry into the high-growth peripheral vascular segment and expanding capabilities in venous thromboembolism treatment, which affects up to 900,000 lives annually in the U.S.

- May 2025: Medtronic reported strong fiscal year 2025 results with USD 33.5 billion total revenue and announced plans to separate its Diabetes business into a standalone public company, while achieving nearly 30% revenue increase in Cardiac Ablation Solutions driven by pulsed field ablation products

- May 2025: BD reported second quarter fiscal 2025 revenue increase of 4.5% with significant contributions from its Interventional segment, launching the Phasix ST Umbilical Hernia Patch as the first bioabsorbable mesh for umbilical hernia repair and announcing USD 2.5 billion investment in U.S. manufacturing capacity over five years.

- April 2025: Baxter International launched room-temperature Hemopatch Sealing Hemostat in Europe, eliminating refrigeration requirements and enhancing surgical accessibility for rapid hemostasis applications across open and minimally invasive procedures.

Global Biosurgery Market Report Scope

As per the scope of the report, biosurgery products are used in various surgeries and repair weakened and damaged tissues and bones. Biosurgery has opened a new paradigm in surgical care, wound and tissue management, and regenerative healing. It has even unlocked new potential in regenerative healing with the right mix of biologics and synthetics. The Biosurgery Market is Segmented by Product (Bone and Graft Substitutes, Soft-Tissue Attachments, Hemostatic Agents, Surgical Sealants and Adhesives, Adhesion Barriers and Staple Line Reinforcement) Application (Orthopedic Surgery, General Surgery, Neurological Surgery, Cardiovascular Surgery, Gynecological Surgery, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers value (in USD millions) for the above segments.

| Bone-Graft Substitutes |

| Hemostatic Agents |

| Surgical Sealants & Adhesives |

| Adhesion Barriers |

| Soft-Tissue Attachments |

| Staple-Line Reinforcement |

| Biologic |

| Synthetic / Semi-synthetic |

| Orthopedic Surgery |

| General Surgery |

| Neurological Surgery |

| Cardiovascular Surgery |

| Gynecological Surgery |

| Thoracic & Reconstructive Surgery |

| Hospitals |

| Ambulatory Surgical Centres |

| Speciality Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Bone-Graft Substitutes | |

| Hemostatic Agents | ||

| Surgical Sealants & Adhesives | ||

| Adhesion Barriers | ||

| Soft-Tissue Attachments | ||

| Staple-Line Reinforcement | ||

| By Source | Biologic | |

| Synthetic / Semi-synthetic | ||

| By Application | Orthopedic Surgery | |

| General Surgery | ||

| Neurological Surgery | ||

| Cardiovascular Surgery | ||

| Gynecological Surgery | ||

| Thoracic & Reconstructive Surgery | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Speciality Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the biosurgery market?

The biosurgery market was valued at USD 18.06 billion in 2026 and is forecast to reach USD 25.27 billion by 2031.

Which product category holds the highest biosurgery market share?

Bone-graft substitutes led with 32.97% revenue in 2025.

Which region is expanding fastest in the biosurgery market?

Asia-Pacific is projected to grow at an 8.01% CAGR through 2031.

What is driving adoption of surgical sealants and adhesives?

Breakthroughs in biomaterial science and evidence of reduced transfusions and operating times are propelling a 7.55% CAGR in this segment.

Why are ambulatory surgical centers important to biosurgery growth?

ASCs perform a rising volume of minimally invasive procedures, supporting an 8.35% CAGR for biosurgical products suited to outpatient settings.

Page last updated on: