EConsent In Healthcare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

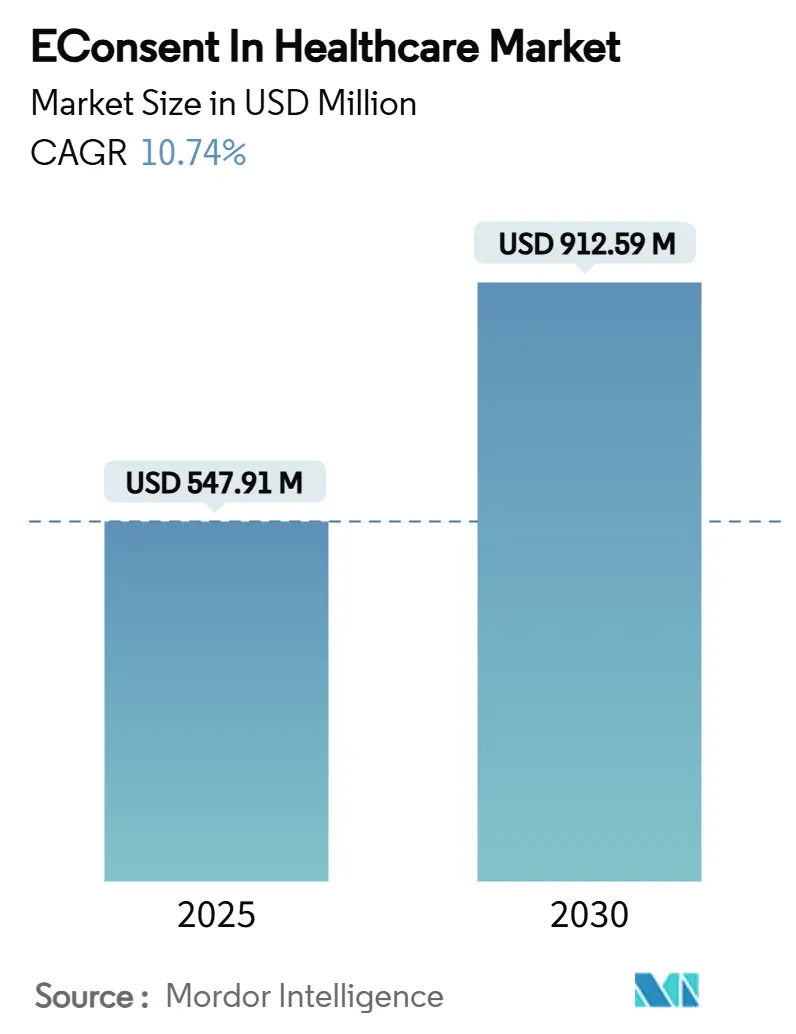

| Market Size (2025) | USD 547.91 Million |

| Market Size (2030) | USD 912.59 Million |

| Growth Rate (2025 - 2030) | 10.74% CAGR |

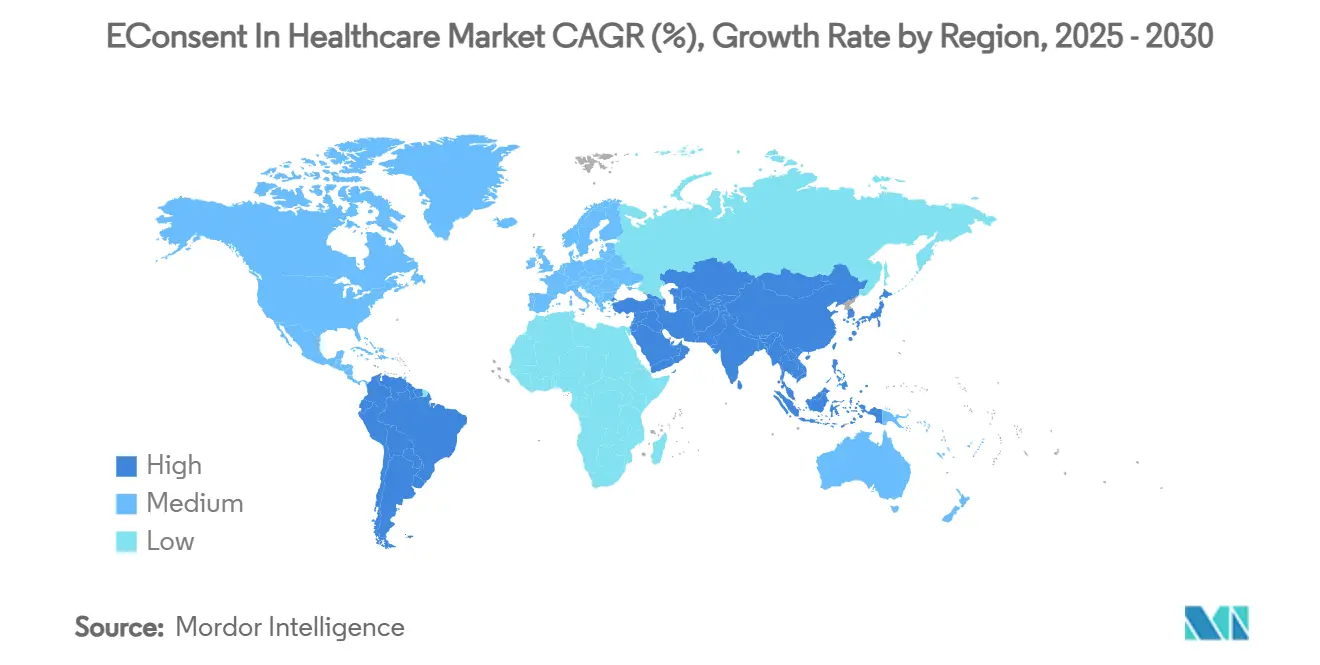

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EConsent In Healthcare Market Analysis by Mordor Intelligence

The eConsent in healthcare market size stands at USD 547.91 million in 2025 and is projected to expand to USD 912.59 million by 2030, reflecting a robust 10.74% CAGR over the forecast period. This expansion mirrors the accelerating digital overhaul of consent workflows across clinical research, routine care, and telehealth operations. Regulatory endorsements on both sides of the Atlantic, growing familiarity with hybrid and fully decentralized clinical trials, and tangible gains in enrollment speed and patient comprehension all reinforce the shift from paper to electronic processes. Cloud-native software architectures lower infrastructure burdens, while artificial-intelligence (AI) modules that draft, translate, and customize forms almost instantly further tilt the cost-benefit equation in favor of electronic consent. Meanwhile, blockchain-backed audit functionality satisfies stringent data-governance mandates, especially in the European Union, and multilingual video content helps sponsors reach historically under-represented communities.

Key Report Takeaways

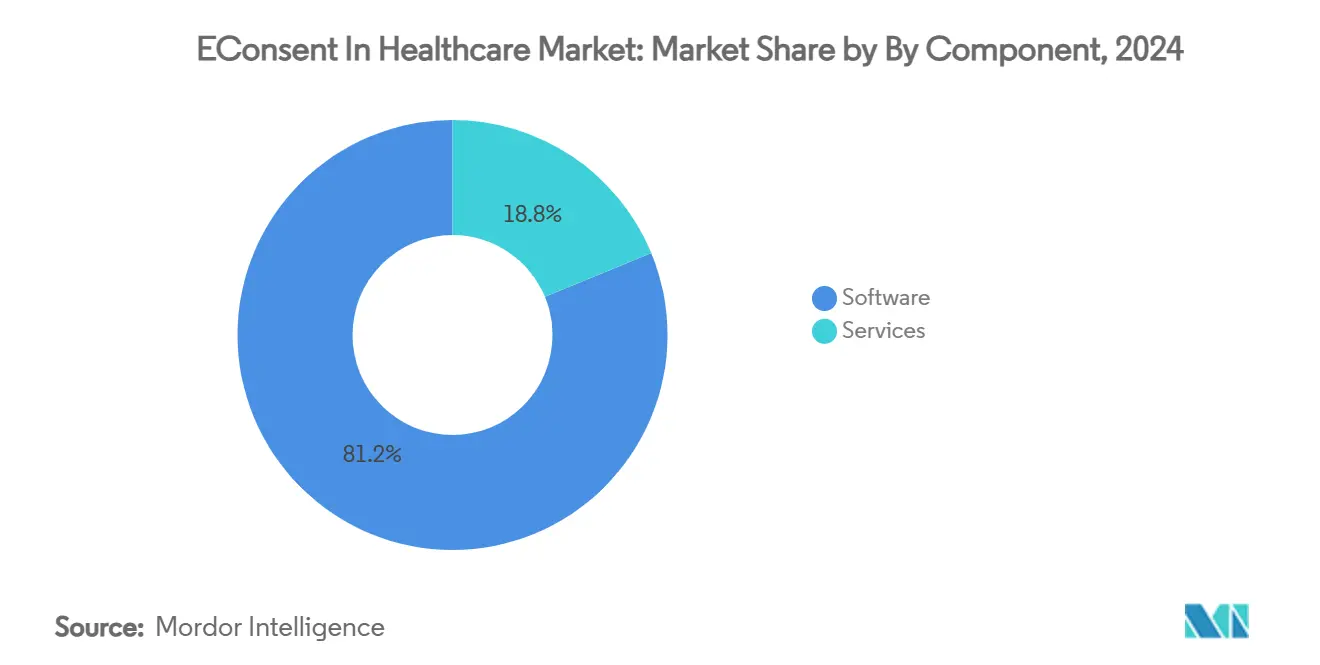

- By component, software held 81.23% of the eConsent in healthcare market share in 2024, whereas services are forecast to register a 14.66% CAGR through 2030.

- By delivery mode, cloud-based platforms commanded 89.34% share of the eConsent in healthcare market size in 2024, with hybrid deployments on track to grow at 13.56% CAGR between 2025-2030.

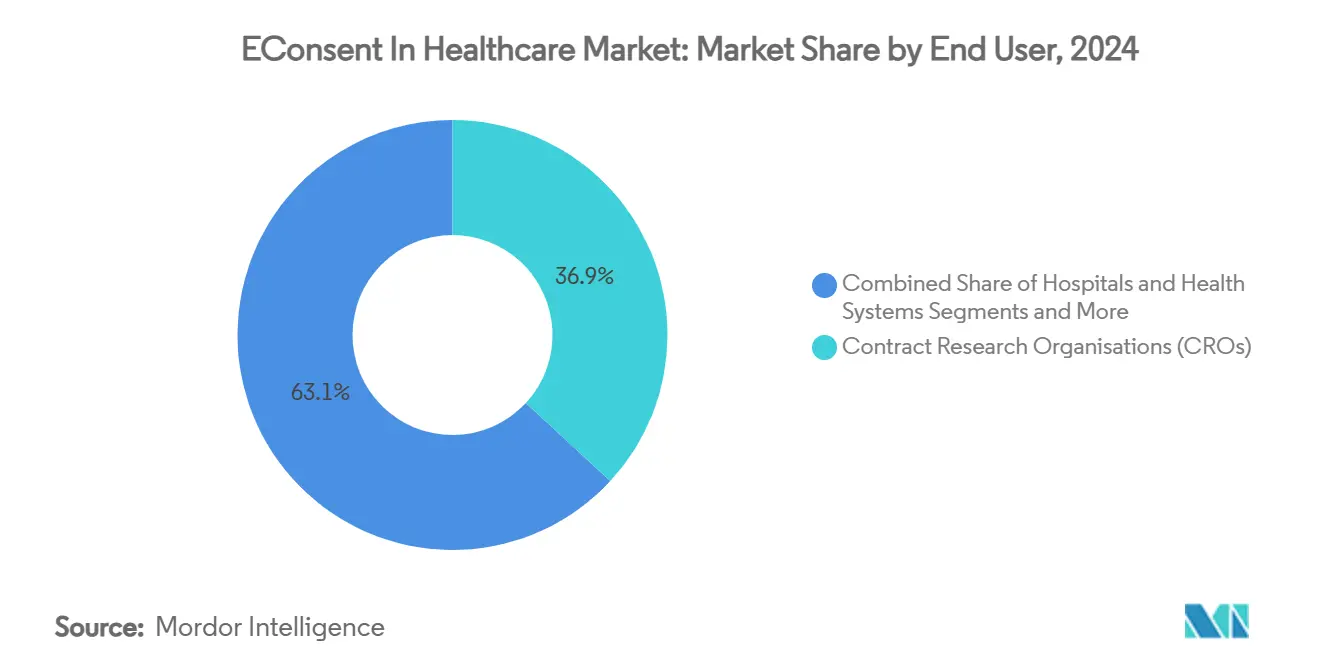

- By end user, contract research organizations accounted for 36.88% share of the eConsent in healthcare market size in 2024, while academic research institutes are advancing at a 12.88% CAGR through 2030.

- By application, clinical trials captured 62.34% of the eConsent in healthcare market share in 2024; telemedicine and remote-care consent is projected to expand at 14.46% CAGR to 2030.

- North America retained 42.34% of the eConsent in healthcare market share in 2024, whereas Asia-Pacific is set to log a 12.35% CAGR during the forecast horizon.

Global EConsent In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decentralized-trial adoption surge post-COVID | +2.1% | Global, especially North America & EU | Medium term (2-4 years) |

| FDA & EMA eConsent guidance fuels uptake | +1.8% | North America & EU, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Better patient comprehension lowers dropout | +1.4% | Global | Long term (≥ 4 years) |

| Gen-AI personalized consent speeds enrollment | +1.6% | North America & EU early adopters | Short term (≤ 2 years) |

| Blockchain audit trails for EU Digital Health Act | +1.2% | EU core, aligned jurisdictions | Medium term (2-4 years) |

| Multilingual adaptive video consent for diversity | +0.9% | Global, high-diversity regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decentralized-trial adoption surge post-COVID

Permanent integration of remote and site-less elements into trial design drives steady demand for platforms that support geographically dispersed participants. The FDA’s September 2024 guidance removed lingering compliance doubts, letting sponsors treat remote consent as a default rather than an exception.[1]Food and Drug Administration, “Electronic Systems, Electronic Records, and Electronic Signatures in Clinical Investigations: Questions and Answers,” FDA.gov Comparative data from multi-country pilots show that decentralized trials outpace traditional studies in enrollment speed while achieving broader demographic reach. Investments already poured into telemedicine infrastructure make a return to paper impractical, cementing the eConsent in healthcare market as a critical enabler.

FDA & EMA eConsent guidance fuels uptake

Clear rules from the FDA (October 2024) and the EMA, coupled with the January 2025 finalization of ICH E6(R3), establish that properly validated electronic signatures carry identical legal weight to ink-on-paper equivalents. These positions harmonize record-keeping expectations across jurisdictions, freeing global sponsors from having to maintain parallel processes. The unified compliance framework also clarifies cross-border data-transfer obligations, opening the door to multi-region protocols without repetitive local re-engineering.[2]Kieran Kenny, “ICH GCP E6 (R3): Transformative Updates Make Good Clinical Practice Better,” ICONplc.com

Better patient comprehension lowers dropout

Interactive explanations, comprehension “check-ins,” and on-demand translations elevate understanding, tackling a long-standing industry pain point. Surveys of phase II-IV study volunteers show 83% prefer digital over paper consent, and 95% would recommend the experience to peers.[3]Michelle Longmire, “New Medable AI Capabilities Simplify Digital Clinical Trial Launch,” Medable.com Adaptive learning algorithms further tailor the density and format of information, reducing mid-study attrition and protocol deviations that inflate timelines.

Gen-AI personalized consent speeds enrollment

Generative-AI modules now draft initial consent language and auto-select relevant regulatory clauses in minutes. Sponsors report that drafting cycles fall from several days to under an hour, compressing overall study start-up windows. The same algorithms localize, translate, and adjust readability to patient literacy levels, delivering personalization at scale and enlarging the addressable patient pool for complex therapies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration cost & legacy IT friction | -1.9% | Global, acute in long-established systems | Medium term (2-4 years) |

| Cyber-security & cross-border data concerns | -1.5% | Global, data-sensitive jurisdictions | Long term (≥ 4 years) |

| Low digital literacy among older patients | -1.2% | Global, aging populations | Long term (≥ 4 years) |

| Proprietary vendor lock-in risks | -0.8% | Global, multi-vendor settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High integration cost & legacy IT friction

Large health systems face expenditures ranging from USD 30,000 for small practices to USD 650,000 for enterprise-scale rollouts, primarily due to complex electronic-health-record (EHR) interfaces and validation work. These capital outlays, compounded by ongoing patching, staff retraining, and incremental cyber-security reinforcements, can delay break-even timelines and deter fast-follower adopters.

Cyber-security & cross-border data concerns

High-profile ransomware events intensify stakeholder anxiety, prompting boards to seek additional assurances on encryption, key management, and data-at-rest protections. Divergent data-localization rules, especially in China, India, and certain Gulf states, further complicate multi-country rollouts, forcing sponsors to maintain segregated data stores and duplicate monitoring protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services gain ground amid complex deployments

Services are on track to record a 14.66% CAGR through 2030 as sponsors shift focus from simple software acquisition to holistic consent optimization. The eConsent in healthcare market size attributed to software remains dominant, yet multi-country pilots reveal that post-deployment services—configuration, language localization, and staff training—consume an expanding share of total spend. Vendors now position professional services as key differentiators, bundling change-management workshops and outcome analytics that quantify comprehension gains. Consultancy teams also walk sites through ever-evolving 21 CFR Part 11 interpretations, GDPR nuances, and local health-authority audits. This advisory layer has become indispensable, especially for academic networks lacking dedicated regulatory-affairs staff. In turn, software roadmaps increasingly integrate customer-feedback loops provided by service consultants, tightening the cycle between user need and product evolution.

The eConsent in healthcare market continues to view software as the engine of scalability, but buyers no longer regard licences as plug-and-play assets. End users ask vendors to shoulder more of the validation burden and to supply reusable training content mapped to each therapeutic area. Implementation specialists now coordinate cross-platform data harmonization—merging consent metadata with electronic case-report-form (eCRF) fields, serious adverse event logs, and patient-reported outcome measures. As regulators press for enriched audit trails, service partners step in to update workflows, refresh document templates, and run quarterly simulation audits. The shift from static deployment to continuous optimization underpins the sustained outperformance of the services segment.

By Delivery Mode: Cloud models eclipse on-premise holdouts

Cloud offerings claimed 89.34% of the eConsent in healthcare market share in 2024, buoyed by immediate scalability, automatic upgrades, and global reach. Multi-tenant architectures let sponsors open studies in new jurisdictions without spinning up local server racks, accelerating first-patient-in milestones by weeks. Cost structures, now largely converted to consumption-based fees, appeal to small and mid-size biotechs that prize budget predictability. Cloud providers also embed disaster-recovery playbooks across redundant zones, assuaging board-level risk committees. As a result, investors view cloud maturity as a leading indicator of vendor viability.

Hybrid deployments remain relevant where data-localization laws restrict storage of personally identifiable information outside national borders. These configurations keep protected health information in a private subnet while routing metadata, translation engines, and analytics dashboards through regional clouds. On-premise solutions persist only in tightly regulated defense-related studies and within a handful of government-run academic medical centers that operate legacy mainframes. Even these users increasingly pilot “cloud-adjacent” connectors that prepare them for eventual migration. Therefore, the eConsent in healthcare market size tied to pure on-premise licences is expected to shrink each successive year, while cloud-led revenue expands at 13.56% CAGR.

By End User: Academia accelerates under diversity mandates

Academic research institutes, motivated by the U.S. National Institutes of Health diversity targets and similar European initiatives, are forecast to post a 12.88% CAGR through 2030. Many universities now bundle eConsent licences into central-grant overheads, ensuring all internal investigators use harmonized templates. This practice streamlines IRB review cycles and allows metrics on inclusion, comprehension, and withdrawal rates to be benchmarked across departments. Consortium-wide procurement also unlocks volume discounts and shared multilingual video libraries, elevating return on investment.

Contract research organizations, with 36.88% of the eConsent in healthcare market share in 2024, retain pole position. CROs embed consent configurations into turnkey trial-master-file (TMF) services, enabling sponsors to outsource both operational execution and compliance reporting. Hospitals and integrated health systems increasingly piggyback on enterprise research networks, deploying unified workflows that cover treatment consent in the morning clinic and trial enrollment in the afternoon. Pharmaceutical and biotech firms continue to adopt eConsent at steady pace, especially in oncology, cell-and-gene, and rare disease studies where patient scarcity justifies elevated technology spend.

By Application: Telemedicine consent outpaces all segments

Telemedicine and remote-care consent is projected to soar at 14.46% CAGR, mirroring the mainstreaming of virtual visits, at-home diagnostics, and digital therapeutics. Payers in the United States and Germany now reimburse remote consultations at parity with in-person care, locking in demand for friction-less digital consent paths. The eConsent in healthcare market size tied to virtual-care programs expands as providers negotiate umbrella contracts that cover multiple chronic-care pathways under a single licence. Consent artifacts generated during televisits feed directly into EHRs, reducing documentation errors and facilitating downstream analytics on care-plan adherence.

Clinical trials, while already accounting for 62.34% of the eConsent in healthcare market share in 2024, sustain mid-single-digit growth as industry moves from pilot to global-scale decentralized protocols. Patient-treatment consent digitization within hospitals adds incremental volume; although revenue per consent is lower than in trials, aggregate transaction count is substantial. Data-privacy consent modules, tailored to GDPR and HIPAA, round out vendor portfolios by commoditizing templated language that can be invoked across any workflow whenever data leaves the source system.

Geography Analysis

North America held 42.34% of eConsent in healthcare market share in 2024 on the strength of clear FDA guidance, robust venture funding, and a mature clinical-research ecosystem. Flagship U.S. health systems—such as Mayo Clinic and Mass General Brigham—run enterprise licence agreements that span academic trials and community-based telehealth initiatives. CROs headquartered in Raleigh-Durham and Philadelphia push standardized electronic workflows to a global network of partner sites, reinforcing vendor adoption even in smaller therapeutic niches. Canada’s federal digital-health roadmap channels grants toward indigenous-population outreach, prompting provincial health authorities to mandate bilingual consent interfaces in English and French. Mexico’s regulatory agency COFEPRIS, aiming to attract phase II oncology studies, released draft rules in 2025 that mirror 21 CFR Part 11, further widening the continent’s adoption footprint.

Europe advances on a twin policy axis of GDPR enforcement and the EU Digital Health Act. Germany leads with extensive study activity across oncology and neurology, helped by the country’s telematics-infrastructure program that certifies cloud-hosted modules. The United Kingdom, notwithstanding Brexit, continues to collaborate with the EMA on technical-pilot exchanges, granting reciprocal recognition of validated eConsent platforms. France, Italy, and Spain accelerate adoption through national recovery-fund grants earmarked for hospital digitization. Estonia showcases a blockchain-based national consent registry that slashes administrative turnaround, serving as a blueprint for other EU states. This collective momentum supports mid-single-digit growth for the eConsent in healthcare market across the bloc.

Asia-Pacific promises the highest regional CAGR of 12.35% through 2030. Japan’s Pharmaceuticals and Medical Devices Agency fast-tracks digital-therapeutic prescriptions for Parkinson’s disease, demanding agile consent flows aligned with home-use devices. China’s National Medical Products Administration introduced a standardized eConsent technical specification in late 2024, pairing it with subsidies for contract sites that adopt compliant software. Large public hospitals in Shanghai and Beijing now pilot AI-generated Mandarin and Cantonese video explanations to bridge regional dialect gaps. India, buoyed by new academic-industry partnerships, integrates eConsent modules into its Ayushman Bharat digital-health stack, although internet-bandwidth variability necessitates offline-capable designs. Australia and South Korea, already leaders in real-world-evidence generation, update Good Clinical Practice handbooks to cite electronic consent as a preferred option, cementing their role as early adopters in the region.

Competitive Landscape

Competitive intensity remains moderate but rising as incumbents, specialists, and AI-first newcomers jostle for differentiation. Veeva Systems leverages its Vault Clinical Suite to bundle eConsent with eTMF and EDC, delivering an integrated data pipeline that appeals to global pharmas. Signant Health pivots toward unified patient-engagement hubs, evidenced by its October 2024 alignment with IQVIA’s One Home for Sites that stitches together eCOA, RTSM, and telemedicine modules. Medable, meanwhile, positions generative-AI tooling as a productivity lever, boasting reductions in consent-form drafting times from days to mere minutes.

Suvoda’s pending merger with Greenphire, announced January 2025, underlines a market-consolidation trend aimed at owning more of the patient journey—from consent through supply management to reimbursement. Smaller players focus on white-space opportunities such as pediatric assent, multilingual rare-disease outreach, or blockchain-based immutable registries. Most vendors adopt a partner-rather-than-build approach for specialized capabilities, leading to an ecosystem of modular APIs. Price competition is muted because buyers prioritize regulatory pedigree and user-experience metrics over licence cost alone, but as AI commoditizes drafting, downward pricing pressure on basic software is expected.

Barriers to entry hinge on 21 CFR Part 11 validation, GDPR compliance, and ISO 27001 certification. Consequently, new entrants often rope in an academic medical center to co-author white papers documenting usability gains—a tactic that speeds trust building. Despite such activity, no supplier holds a double-digit individual share, indicating ample headroom for both organic expansion and mergers.

EConsent In Healthcare Industry Leaders

Medable

Signant Health

Veeva Systems

Oracle Life Sciences

IQVIA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Suvoda and Greenphire announced a merger to combine eConsent, randomization, trial-supply management, and payments solutions, with closing expected in Q2 2025 pending regulatory approval.

- October 2024: Medable partnered with Google Cloud to list its digital and decentralized clinical-trial platform on Google Cloud Marketplace, leveraging AI and global cloud infrastructure to streamline study design.

- September 2024: Signant Health joined IQVIA’s One Home for Sites initiative, integrating eConsent with eCOA, EDC, RTSM, and telemedicine within a single site-facing workspace.

Global EConsent In Healthcare Market Report Scope

| Software |

| Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Pharmaceutical & Biotechnology Cos. |

| Contract Research Organisations (CROs) |

| Hospitals & Health Systems |

| Academic Research Institutes |

| Clinical Trials |

| Patient Treatment Consent |

| Telemedicine & Remote Care |

| Data-privacy / GDPR / HIPAA Consents |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Delivery Mode | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By End User | Pharmaceutical & Biotechnology Cos. | |

| Contract Research Organisations (CROs) | ||

| Hospitals & Health Systems | ||

| Academic Research Institutes | ||

| By Application | Clinical Trials | |

| Patient Treatment Consent | ||

| Telemedicine & Remote Care | ||

| Data-privacy / GDPR / HIPAA Consents | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the eConsent in healthcare market?

The eConsent in healthcare market size is USD 547.91 million in 2025.

How fast is the market expected to grow by 2030?

It is forecast to reach USD 912.59 million by 2030, reflecting a 10.74% CAGR.

Which component segment is expanding the quickest?

Services, registering a 14.66% CAGR as sponsors seek expertise beyond software licences.

Why are cloud-based deployments so dominant?

They account for 89.34% share because centralized hosting reduces infrastructure overhead and accelerates trial start-up timelines.

Which region shows the strongest growth potential?

Asia-Pacific, driven by Japan’s digital-therapeutics policies and China’s large-scale hospital digitization, is slated for a 12.35% CAGR.

Page last updated on: