Biosimulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

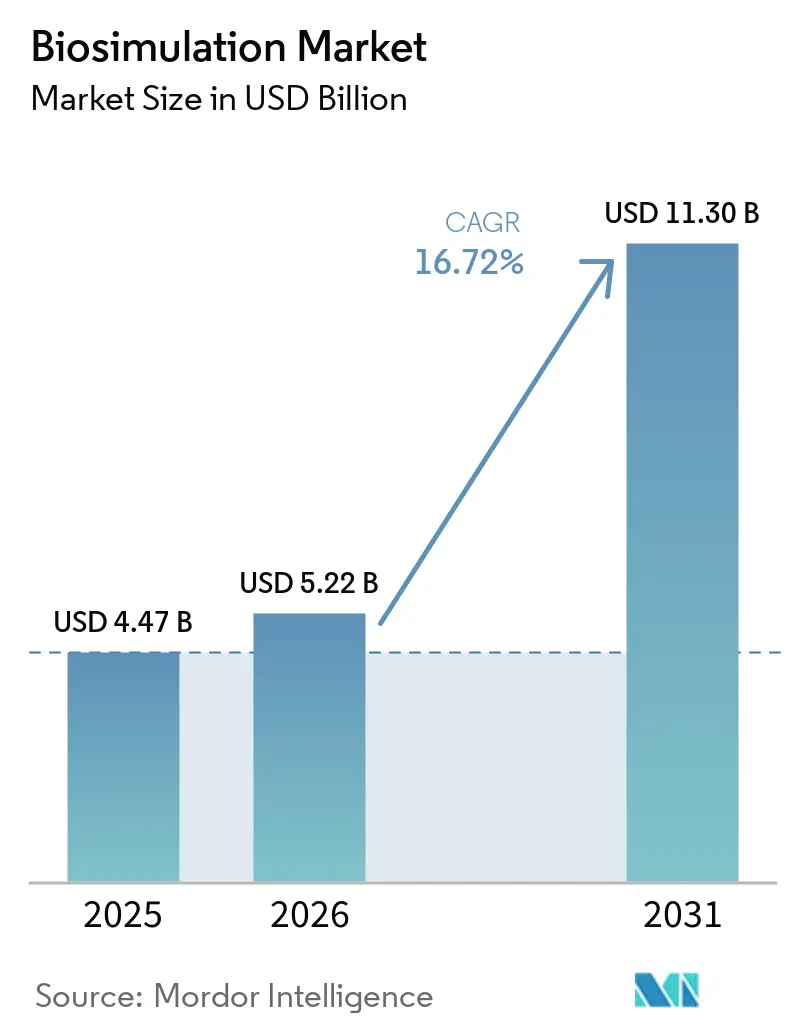

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 11.30 Billion |

| Growth Rate (2026 - 2031) | 16.72% CAGR |

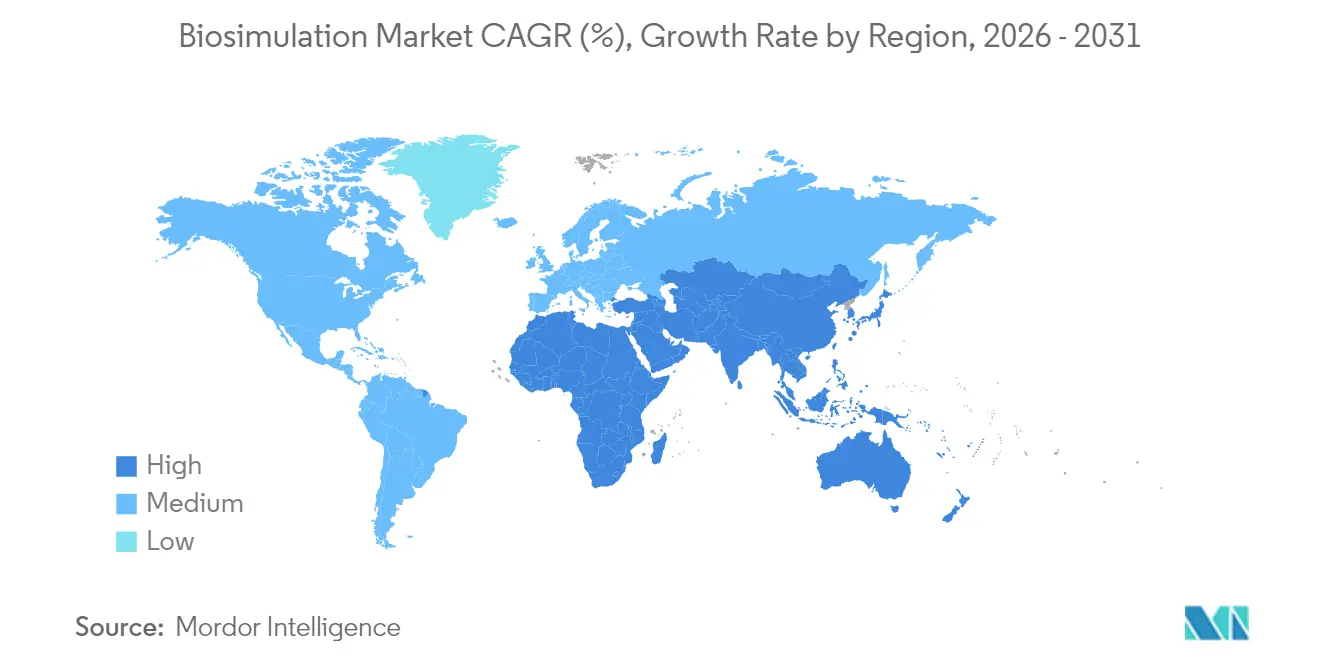

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

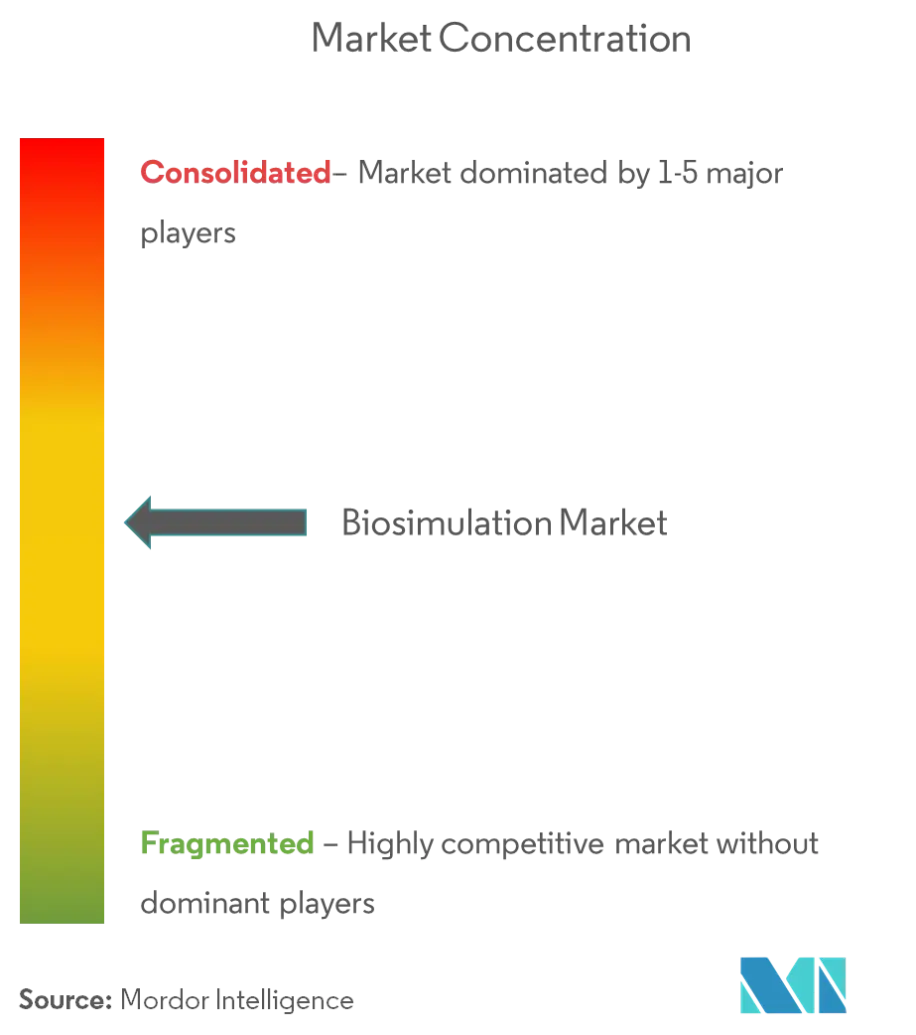

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biosimulation Market Analysis by Mordor Intelligence

Biosimulation market size in 2026 is estimated at USD 5.22 billion, growing from 2025 value of USD 4.47 billion with 2031 projections showing USD 11.3 billion, growing at 16.72% CAGR over 2026-2031.

Strong growth stems from the pharmaceutical sector’s rising use of in-silico modeling to curb escalating R&D expenses, from regulators’ formal endorsement of model-informed drug development, and from rapid progress in cloud-delivered high-performance computing. Adoption also receives momentum from the FDA’s Quantitative Medicine Center of Excellence, the finalized ICH M15 guideline, and the broadening use of virtual twin studies to reduce animal testing requirements fda.gov. Wider corporate IT budgets, artificial intelligence integration, and expanding precision-medicine pipelines further reinforce demand, while moderate fragmentation allows vendors to differentiate on analytics depth, therapeutic‐area expertise, and regulatory familiarity.

Key Report Takeaways

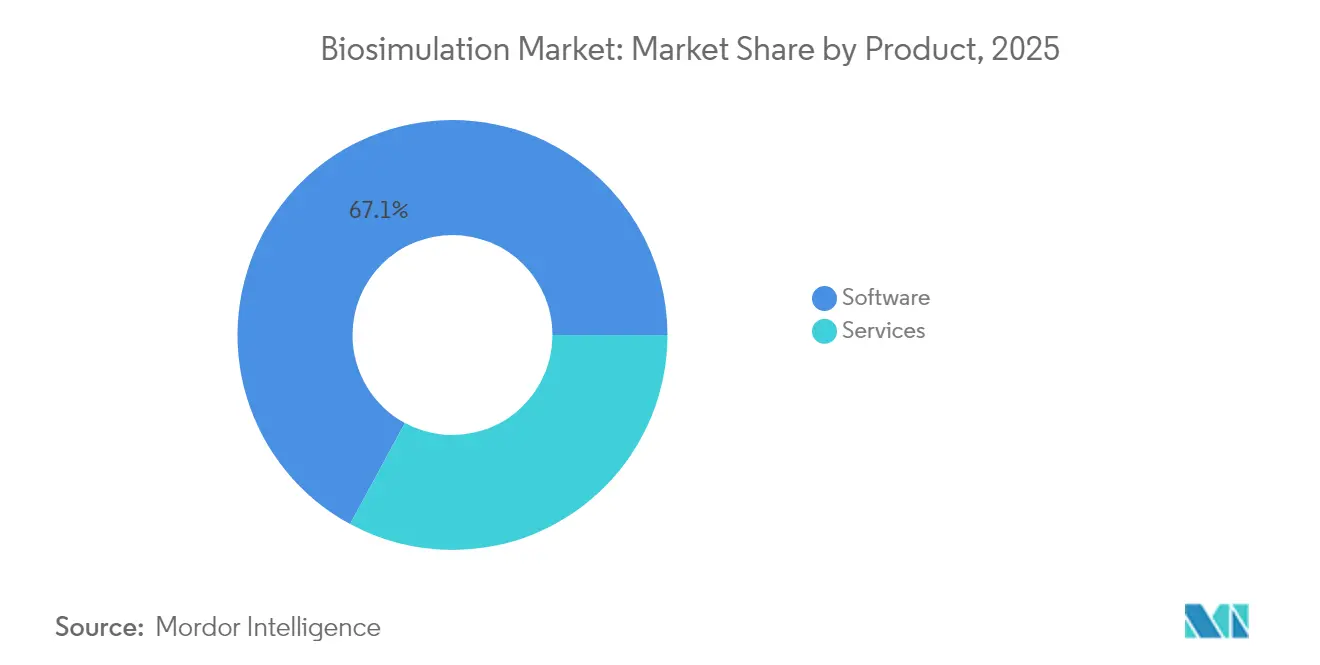

- By product, software platforms led with 67.10% revenue share in 2025; seervice solutions are poised to grow at an 18.05% CAGR through 2031.

- By delivery model, ownership/on-premise held 46.90% of the biosimulation market share in 2025, while subscription-based solutions are set to accelerate at 18.70% CAGR to 2031.

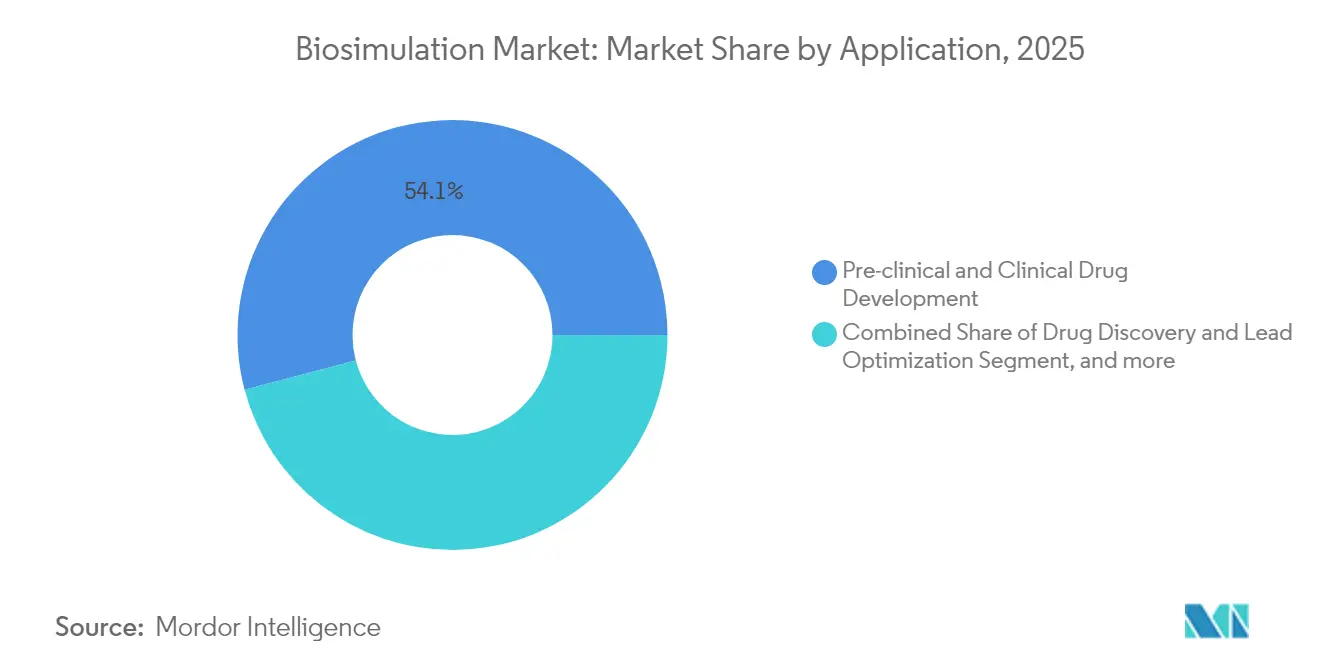

- By application, drug discovery and lead optimization commanded 54.10% of the biosimulation market size in 2025; precision medicine and companion diagnostics are forecast to expand at a 19.50% CAGR through 2031.

- By end user, pharmaceutical and biotechnology firms accounted for 62.50% revenue share in 2025; contract research organizations represent the fastest-growing group at 20.95% CAGR.

- By geography, North America retained 44.10% revenue share in 2025; Asia-Pacific is projected to climb at 22.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biosimulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing healthcare-sector IT budgets | +3.2% | Global (North America & Europe highest) | Medium term (2-4 years) |

| Growing adoption of biosimulation platforms by regulators | +4.1% | Global (FDA, EMA, PMDA leadership) | Long term (≥ 4 years) |

| Escalating drug-development costs | +3.8% | Global (strongest in developed markets) | Short term (≤ 2 years) |

| Cloud-based high-performance computing cuts simulation TCO | +2.9% | Global (earlier in North America & APAC) | Medium term (2-4 years) |

| FDA MIDD program mainstreams model-based submissions | +2.4% | North America with global spillover | Long term (≥ 4 years) |

| Expansion of real-world-data-driven “virtual-twin” studies | +1.8% | US, EU, Japan early movers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Healthcare-Sector IT Budgets

Life-sciences CIO surveys show that a majority of firms raised technology allocations in 2024, with one quarter prioritizing artificial-intelligence projects. Larger budgets translate into stronger demand for integrated biosimulation platforms that merge PBPK, QSP, and AI algorithms. Pfizer and Novo Nordisk publicly report measurable cost savings tied to cloud-native modeling investments, reinforcing the business case for broader rollouts across the biosimulation market. Elevated spending also accelerates cloud infrastructure upgrades that permit extensive virtual twin studies and real-time collaboration among globally dispersed teams. The trend supports sustained double-digit growth for the biosimulation market over the medium term.

Growing Adoption of Biosimulation Platforms by Regulators

Regulatory momentum has reached a critical threshold. The FDA notes that QSP-based submissions now double every 1.4 years, while its permanent MIDD-paired-meeting program offers structured advice on quantitative models.[1]U.S. Food and Drug Administration, “Quantitative Medicine Center of Excellence,” fda.gov The ICH M15 guideline, finalized in 2024, harmonizes international expectations for model-informed drug development and reduces uncertainty for sponsors.[2]European Medicines Agency, “ICH M15: Model-Informed Drug Development Guideline,” ema.europa.eu The EMA and PMDA publish detailed PBPK guidance, and agencies increasingly accept simulation data in lieu of animal studies for monoclonal antibodies. This official endorsement creates a feedback loop: each successful filing builds confidence, prompting still more sponsors to embed biosimulation into development plans.

Escalating Drug-Development Costs

Return on R&D for large biopharma improved slightly to 5.9% in 2024 but remains below historical norms. Cost pressure pushes firms toward digital approaches that shorten cycle times, raise success probabilities, and allow earlier termination of non-viable candidates. Biosimulation platforms support these aims by predicting human pharmacokinetics before first-in-human dosing, optimizing dosing regimens for complex biologics, and informing adaptive trial designs. Smaller biotech companies, which operate under tighter capital constraints, increasingly rely on subscription-based biosimulation to conserve cash and show data-driven credibility to investors, contributing to expansion in the biosimulation market.

Cloud-Based High-Performance Computing Cuts Simulation TCO

Cloud partnerships with major providers allow GSK, Bayer, and Pfizer to run large-scale simulations without maintaining on-premise supercomputers. Pay-as-you-go compute makes advanced PBPK or QSP modeling financially feasible for mid-tier firms as well. Cloud architectures also support automatic algorithm updates, access to specialized GPUs for machine-learning workloads, and secure collaboration across business units. As regulatory authorities clarify data-integrity expectations for cloud submissions, more sponsors migrate critical workloads, reinforcing the structural shift away from perpetual licenses toward flexible subscriptions within the biosimulation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Awareness Among Clinicians & Trial Teams | -2.1% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled PBPK/QSP Modelers | -2.8% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Lack of Global Data-Format & Model-Validation Standards | -1.9% | Global, with fragmentation across regulatory jurisdictions | Long term (≥ 4 years) |

| Regulatory Uncertainty Around AI-Generated Models | -2.3% | Global, most pronounced in US and EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Awareness Among Clinicians & Trial Teams

Many trial investigators remain unfamiliar with quantitative modeling outputs, hindering full integration of virtual insights into protocol design and decision making. Educational curricula often lack advanced pharmacometrics modules, and operational staff face tight timelines that favor traditional practices. Companies respond with internal academies and e-learning modules, yet adoption still varies by therapeutic area and geography. The gap is widest in emerging markets where digital infrastructure lags and local regulators are only beginning to reference ICH M15. Until practical know-how spreads, some sponsors will under-utilize biosimulation’s potential.

Shortage of Skilled PBPK/QSP Modelers

Global demand for modeling talent outpaces supply, particularly for professionals with coding fluency in Python or R and hands-on regulatory submission experience. Academia is expanding cross-disciplinary programs, but time-to-competence remains long because QSP requires mathematics, systems biology, and clinical insight. Competition from technology companies further shrinks the available pool. Industry mitigates the bottleneck through automated workflows, user-friendly interfaces, and strategic alliances with universities. Nonetheless, persistent scarcity slows project throughput and influences some firms to outsource modeling to specialized CROs, impacting scalability within the biosimulation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Software Platforms Drive Innovation

Software solutions held 67.10% revenue in 2025, reflecting the preference for integrated modeling environments that streamline visualization, verification, and regulatory reporting. Certara’s Phoenix release and Dassault Systèmes’ BIOVIA upgrades underscore a race to embed AI modules that speed compound screening. The biosimulation market continues to reward vendors that couple PBPK and QSP engines with intuitive dashboards and extensive compound libraries. Services, while smaller in absolute value, grow steadily as sponsors seek consulting expertise to customize workflows and interpret complex outputs reinforcing growth in the biosimulation market.

Services, though niche today, are projected to post an 18.05% CAGR by 2031 as real-time biosensor data feed directly into digital twins for chronic-disease management. This expansion broadens the biosimulation market beyond drug development into clinical decision support. Services providers benefit from the complexity of integrating sensor streams with QSP models, a task that demands both domain knowledge and data-engineering skills. Vendors that combine platform software with wraparound advisory offerings are positioned to capture higher share of wallet in late-stage projects.

By Delivery Model: Cloud Transformation Accelerates

Ownership-based deployments still account for 46.90% revenue because large pharmaceutical companies maintain sophisticated internal data centers. However, subscription services grow at 18.70% CAGR as firms value elastic compute and lower capital outlay. The biosimulation market reflects a larger life-sciences trend in which regulated workloads shift to validated cloud environments certified for Good Practice guidelines. Continuous algorithm updates and embedded compliance features appeal to small and mid-sized sponsors that lack specialist IT staff.

Security and data-sovereignty remain reasons for some enterprises to remain on-premise, especially when handling proprietary monoclonal-antibody sequences or trial data subject to regional privacy rules. Hybrid models therefore persist, with sensitive workloads staying behind the firewall and burst compute sent to the cloud. Platform providers respond with containerized deployments that move seamlessly between environments, ensuring identical validation documentation in either setting. Increased clarity from regulators regarding electronic-records controls will further unlock cloud use for pivotal-study models.

By Application: Precision Medicine Leads Growth

Drug discovery and lead-optimization workflows accounted for 54.10% revenue in 2025, highlighting the value of in-silico screens in selecting better candidates earlier. Yet precision medicine and companion-diagnostic design outpaces all other uses with a 19.50% CAGR. Growing availability of next-generation sequencing and real-world data enables digital twins that capture patient heterogeneity with unprecedented detail. SandboxAQ’s alliance with Sanofi exemplifies how machine learning parses deep knowledge graphs to pinpoint actionable biomarkers.

In oncology, QSP models now explore bispecific antibodies and antibody-drug conjugates to optimize dose schedules, while immune-oncology platforms simulate checkpoint-inhibitor combinations before clinical deployment. The biosimulation market’s expansion into personalized regimens underpins the transition from one-size-fits-all therapy toward tailored dosing informed by patient genetics, physiology, and comorbidities. Regulatory encouragement of biomarker-driven submissions accelerates this trajectory, making precision applications the most dynamic revenue contributor over the forecast horizon.

By End User: CROs Embrace Advanced Modeling

Pharmaceutical and biotechnology firms generated 62.50% of 2025 revenue by licensing or purchasing modeling platforms to streamline in-house R&D. Contract research organizations show the fastest velocity, expanding at 20.95% CAGR as they embed biosimulation into full-service offerings that include protocol design, site selection, and adaptive trial monitoring. Charles River Laboratories’ use of virtual control groups to reduce animal cohorts illustrates how CROs turn modeling capabilities into a strategic differentiator.

Academic centers and research institutes leverage open-source frameworks to explore disease mechanisms and validate novel targets. Public-private consortia fund community models that accelerate knowledge sharing, but many institutions still rely on commercial tools for regulatory-grade outputs. As payers and regulators push for evidence of real-world effectiveness, CROs that combine decentralized-trial operations with predictive analytics gain a competitive edge, and their rapid adoption further enlarges the biosimulation market.

Geography Analysis

North America dominated with 44.10% revenue share in 2025, supported by the FDA’s proactive stance on model-informed development and deep local venture funding. Europe follows, fueled by the EMA’s extensive PBPK guidance, robust data-privacy laws that encourage secure cloud adoption, and strong industrial ties between software vendors and research hospitals. Both regions host many early adopters of QSP for complex biologics.

Asia-Pacific registers the fastest 22.60% CAGR, benefiting from regulatory harmonization and an expanding biosimilar pipeline. Japan’s PMDA approved 35 biosimilar products by early 2024, several of which leveraged modeling to justify abbreviated clinical datasets. China’s multi-year plan for pharmaceutical innovation has attracted global platform providers to establish regional centers, while India’s emerging biotech corridor adds capacity for cost-efficient model building. Lower labor costs and a growing pool of data scientists enable local firms to operate dedicated biosimulation centers, reinforcing regional independence.

Latin America, the Middle East, and Africa contribute smaller shares today but display accelerating interest as multinational sponsors extend virtual-study methodology to diverse populations. Technology-transfer programs seed local know-how, and cloud infrastructure rollouts lower entry barriers. Over time, broader real-world-data availability will unlock the full potential of biosimulation in these underserved markets.

Competitive Landscape

The biosimulation market remains moderately fragmented. Certara, Dassault Systèmes, Simulations Plus, and Schrödinger hold significant share, yet no single supplier controls more than one-third of global revenue. Competition focuses on breadth of mechanistic models, AI integration, regulatory-consulting capacity, and therapeutic-area depth rather than on pricing alone. Recent moves cement this orientation: Certara’s purchase of cheminformatics specialist Chemaxon expands structure-activity coverage, while Schrödinger’s USD 150 million upfront deal with Novartis broadens multiyear access to its discovery platform.

Strategic alliances gain prominence as vendors integrate electronic-lab-notebook data, high-content screening outputs, and genomic insights. Dassault Systèmes’ Medidata platform underscores how virtual twins converge with clinical-trial management to create a single digital thread from molecule to patient. New entrants exploit cloud-native microservices and large-language models to automate sensitivity analyses, offering pay-per-use pricing that appeals to seed-stage biotech.

White-space opportunities cluster in predictive toxicology, rare-disease modeling, and seamless real-world-evidence ingestion. Gates Foundation funding for Schrödinger’s toxicology tool illustrates how philanthropic capital accelerates innovation in areas aligned with public-health goals. The outlook therefore points to ongoing acquisitions, consortia formation, and co-development pacts that collectively sustain high competitive intensity without tipping into commoditization.

Biosimulation Industry Leaders

In Silico Biosciences, Inc.

Pharmaceutical Product Development, LLC

Schrödinger, LLC

Simulations Plus, Inc.

Certara

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Dassault Systèmes’ Medidata brand added more than 300 new customers in 2024 and unveiled AI-driven patient-engagement alliances to strengthen virtual-trial execution.

- January 2025: Schrödinger announced support for the FDA plan to phase out animal testing for monoclonal antibodies and confirmed a late-2025 launch of its predictive-toxicology module, backed by a USD 10 million Gates Foundation grant.

- January 2025: SandboxAQ was selected by Sanofi to apply quantitative AI models for biomarker discovery during clinical development.

- December 2024: Schrödinger expanded a multi-target collaboration with Novartis that includes USD 150 million upfront and up to USD 2.3 billion in milestones.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global biosimulation market as all licensed software platforms and associated professional services that deploy mechanistic, stochastic, or hybrid in-silico models (PBPK, QSP, PK/PD and allied approaches) to simulate biological processes for drug, device, or diagnostic R&D. Revenues are booked at the point of sale to end users and converted to USD using the average annual rate, ensuring comparability across regions.

Scope Exclusions: Pure bioinformatics data-curation tools, general-purpose HPC hardware sales, and one-off consulting assignments unrelated to model-informed drug development are excluded.

Segmentation Overview

- By Product

- Software

- Services

- By Delivery Model

- Subscription

- Ownership / On-premise

- By Application

- Pre-clinical & Clinical Drug Development

- Drug Discovery & Lead Optimization

- Precision-medicine & Companion-diagnostics Design

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed clinical pharmacologists, PK/PD modeling leads, cloud-HPC product managers, and regulatory reviewers across North America, Europe, and Asia-Pacific. Their insights refined price corridors, typical seat counts, and regional uptake rates, bridging the gaps left by desk research and strengthening our assumptions.

Desk Research

We first mapped demand and supply using publicly available, tier-1 sources such as the US FDA's MIDD pilot reports, EMA qualification opinions, NIH RePORTER grant files, ICH-M15 drafts, SEC-filed 10-Ks, and presentations from the Drug Information Association and International Society of Pharmacometrics. These clarify user cohorts, regulatory milestones, and spending pools. Paid repositories, including D&B Hoovers and Dow Jones Factiva, were tapped to validate company bookings and track press releases. The sources above are illustrative; many other references supported data collection and cross-checks.

Market-Sizing & Forecasting

A top-down model begins with global R&D outlays and then allocates the share spent on model-informed workflows. Selective bottom-up roll-ups of key vendors plus sampled ASP × user volumes validate totals. Core drivers include active clinical-trial counts, IND submissions, average computational hours per project, biosimulation penetration in Phase II studies, and regional cloud-HPC cost indices. A multivariate regression links these variables to historical revenue, while scenario analysis adjusts for regulatory endorsements and AI-enabled productivity gains. When vendor disclosures are partial, analog peer cohorts and weighted imputation bridge gaps before final reconciliation.

Data Validation & Update Cycle

Outputs face variance screening against independent indicators, peer review, and senior analyst sign-off. We refresh every twelve months and trigger interim updates for events such as landmark FDA guidance or major platform price shifts. A final validation pass precedes delivery so clients receive the latest view.

Why Our Biosimulation Baseline Commands Reliability

Published estimates often diverge because firms choose different base years, bundle or omit services, or anchor forecasts to contrasting R&D scenarios. Our disciplined scope, driver-based modeling, and annual refresh curb those variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.47 B (2025) | Mordor Intelligence | - |

| USD 4.24 B (2024) | Global Consultancy A | Services counted separately; earlier base year; static FX rates |

| USD 3.91 B (2024) | Trade Journal B | Excludes cloud-hosted licenses; assumes flat penetration across trial phases |

The comparison shows that Mordor's scope alignment, variable-driven forecasting, and frequent updates give decision-makers a balanced, transparent baseline they can depend on.

Key Questions Answered in the Report

What is the current value of the biosimulation market?

The biosimulation market size reached USD 5.22 billion in 2026 and is projected to more than double to USD 11.3 billion by 2031.

Which product category leads the biosimulation market?

Integrated software platforms dominate with 67.10% revenue share in 2025, driven by demand for comprehensive PBPK and QSP modeling environments.

Why is Asia-Pacific the fastest-growing region?

Regulatory harmonization, a surge in biosimilar development, and expanding local talent pools push Asia-Pacific to a 22.60% CAGR through 2031.

How are cloud deployments influencing adoption?

Subscription-based, cloud-hosted solutions grow at 18.70% CAGR because they provide elastic compute, lower upfront costs, and seamless AI integration.

What is the biggest challenge for biosimulation vendors?

An acute shortage of skilled PBPK and QSP modelers constrains project throughput and elevates the importance of training, automation, and academic partnerships.

Which application segment is expanding the fastest?

Precision medicine and companion-diagnostic modeling lead growth at a 19.50% CAGR thanks to genomic data integration and virtual twin adoption.

Page last updated on: