Headlight Control Module Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

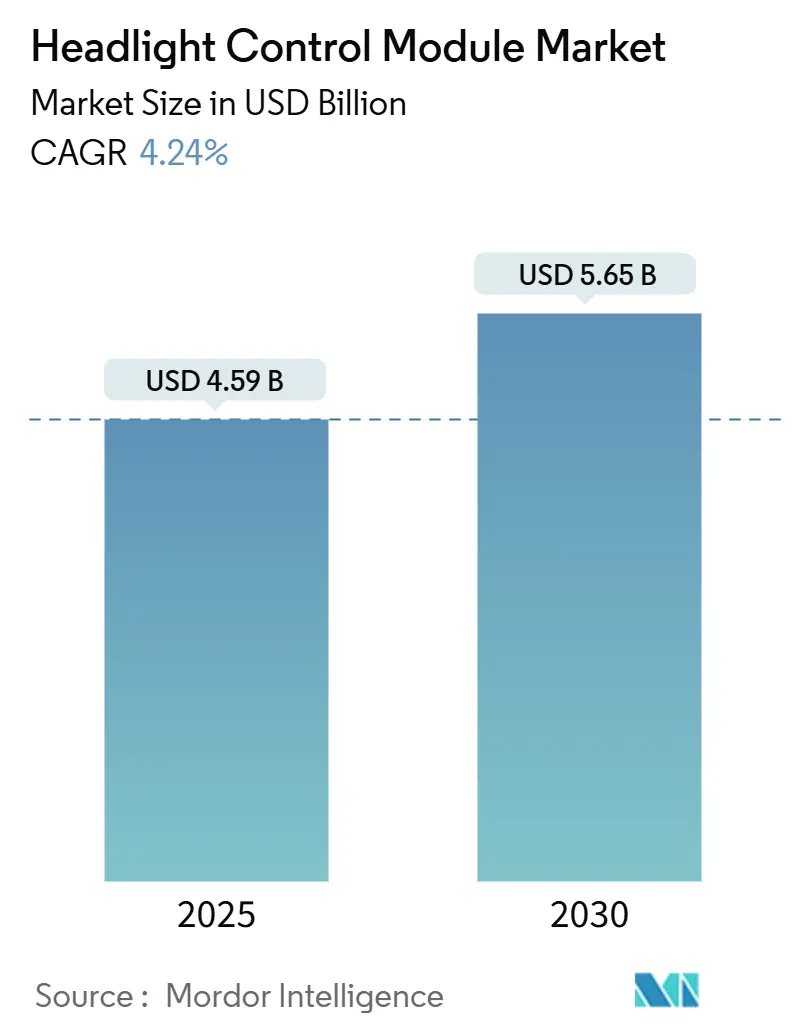

| Market Size (2025) | USD 4.59 Billion |

| Market Size (2030) | USD 5.65 Billion |

| Growth Rate (2025 - 2030) | 4.24% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Headlight Control Module Market Analysis by Mordor Intelligence

The headlight control module market size stood at USD 4.59 billion in 2025 and is forecast to reach USD 5.65 billion by 2030, advancing at a 4.24% CAGR during the forecast period. Regulatory mandates that curb glare, falling LED costs, and electrification-led 48 V architectures underpin this steady expansion, while moderate competitive intensity allows suppliers to balance price and innovation. Stricter UNECE and FMVSS rules have triggered a pivot from static halogen systems to adaptive LED matrices, and price erosion now lets mid-segment models specify modules once reserved for flagships. Asia-Pacific remains the volume anchor, yet the Middle East and Africa accelerate fastest as luxury purchases persist despite harsh climates that demand robust thermal management. Semiconductor shortages and heat-dissipation limits create near-term friction, but V2X-ready beam forming and gaze-tracking ADAS integration open premium revenue streams as regulations evolve to endorse connected-lighting coordination.

Key Report Takeaways

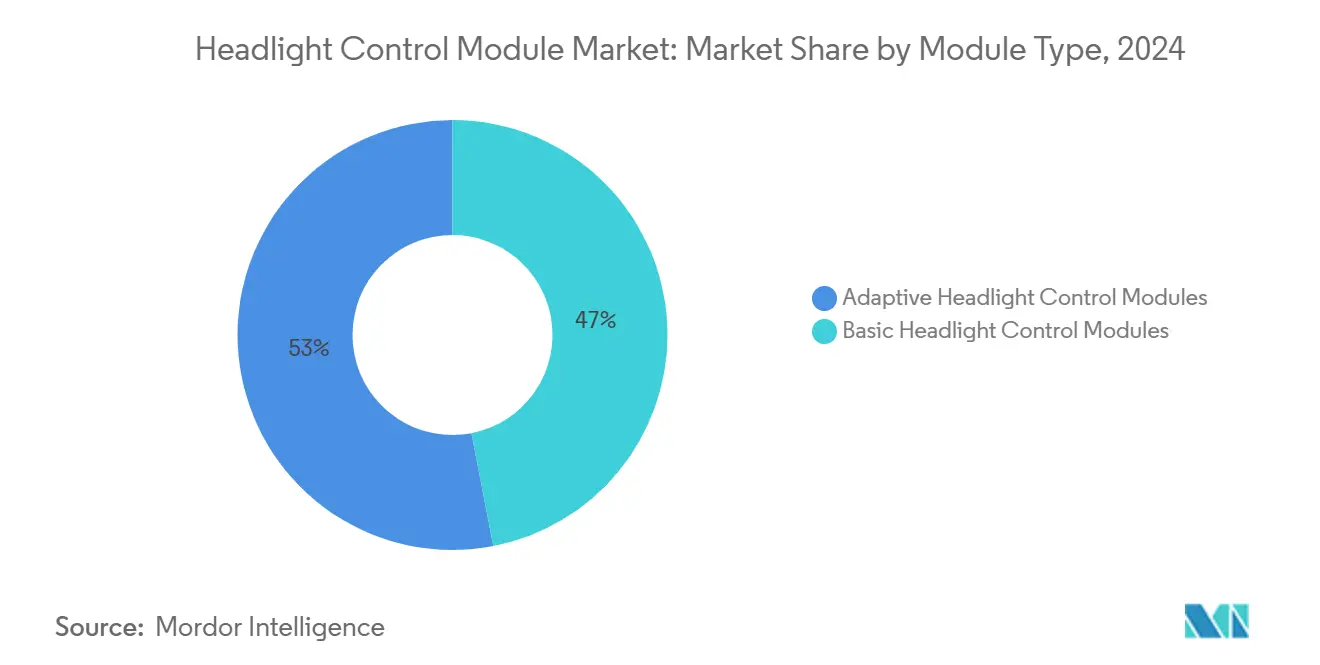

- By module type, adaptive headlight control modules held 53.04% share of the headlight control module market in 2024, and are projected to grow at a 7.92% CAGR through 2030.

- By technology, LED platforms commanded 52.27% share of the headlight control module market in 2024, whereas Xenon solutions are forecast to post the fastest 6.13% CAGR through 2030.

- By functionality, High Beam Assist led the market with a 28.73% share of the headlight control module market in 2024; Cornering Control is expected to expand at the swiftest 6.81% CAGR through 2030.

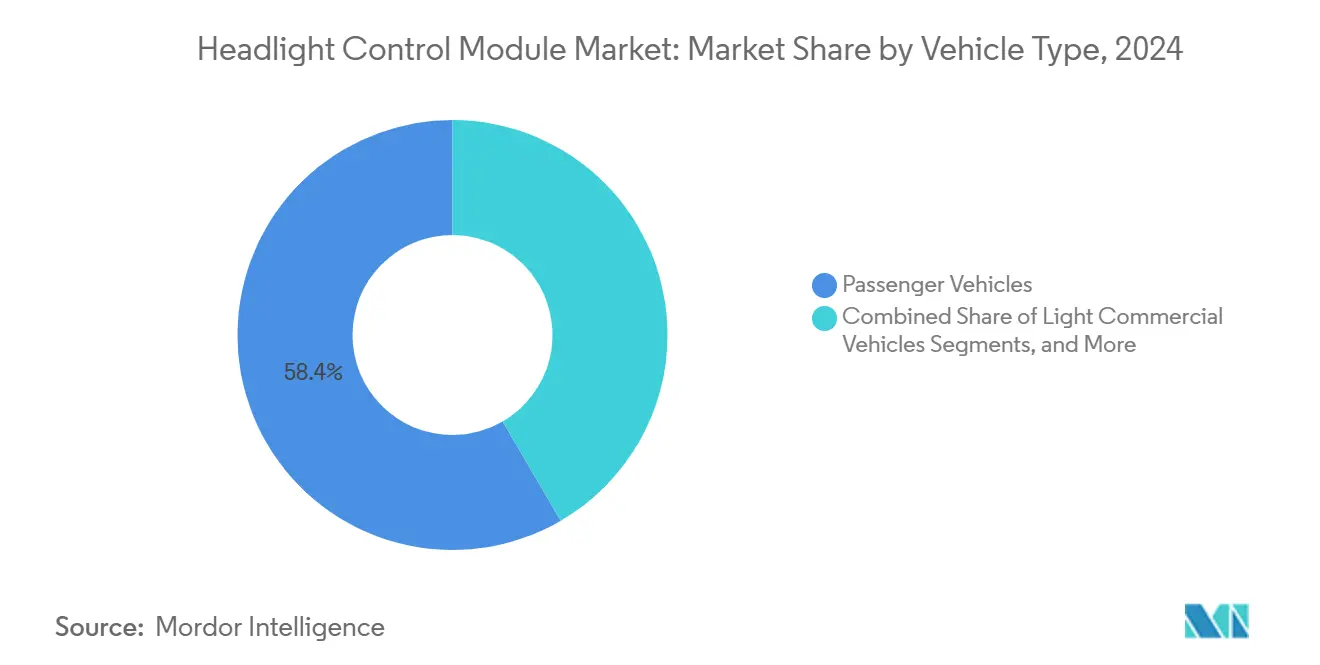

- By vehicle type, passenger vehicles accounted for a 58.39% share of the headlight control module market in 2024 and are set to grow at a 5.88% CAGR through 2030.

- By distribution channel, the original equipment manufacturer (OEM) dominated the market with 91.06% share of the headlight control module market in 2024, while the aftermarket is projected to advance at a 9.23% CAGR to 2030.

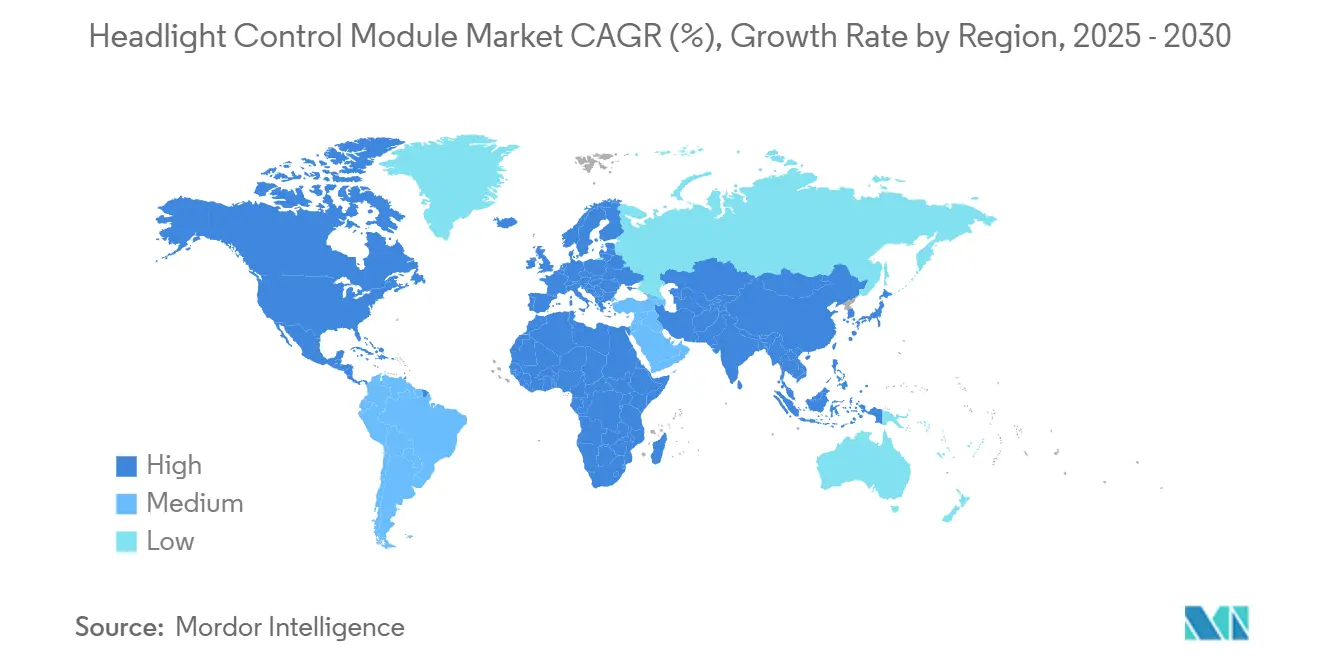

- By geography, Asia-Pacific captured 41.96% of the headlight control module market in 2024, while the Middle East and Africa are anticipated to record the strongest 8.37% CAGR through 2030.

Global Headlight Control Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter UNECE and FMVSS Glare-Reduction Mandates | +1.2% | Global, with EU leading implementation | Medium term (2-4 years) |

| LED Price Erosion Enabling Mid-Segment Adoption | +0.8% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Premium-Vehicle Growth in Emerging Asia-Pacific Economies | +0.6% | Asia-Pacific, selective MEA markets | Long term (≥ 4 years) |

| Electrification Raising 48-V Electrical-Architecture Demand | +0.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| V2X-Based Predictive Beam-Forming Pilots | +0.3% | EU pilot regions, selective US markets | Long term (≥ 4 years) |

| Gaze-Tracking High-Beam ADAS Integration | +0.2% | Premium segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter UNECE and FMVSS Glare-Reduction Mandates

Regulatory enforcement of glare-reduction standards fundamentally reshapes headlight control module specifications, with UNECE Regulation 48 and FMVSS 108 now requiring precise beam pattern control to minimize oncoming driver discomfort. The regulatory shift has created a technical inflection point where traditional static beam patterns can no longer satisfy compliance requirements, forcing OEMs to adopt adaptive control systems with real-time beam shaping capabilities. Matrix LED systems with individual element control have emerged as the preferred solution, requiring sophisticated control algorithms to process camera input and adjust beam patterns within milliseconds[1]"New business sedan car equipped with HELLA lighting technology," Forvia Hella, hella.com. This regulatory pressure has effectively eliminated the viability of basic halogen systems in premium segments, accelerating the transition to electronically controlled LED arrays. The compliance framework varies significantly across regions, with European markets leading implementation timelines and creating first-mover advantages for suppliers with proven adaptive beam technologies. UNECE's technical requirements for glare measurement and beam pattern validation have established new testing protocols that favor suppliers with extensive R&D capabilities in optical simulation and control system integration.

LED Price Erosion Enabling Mid-Segment Adoption

The dramatic reduction in LED component costs has democratized access to advanced headlight control technologies previously reserved for luxury vehicles, with automotive-grade LED prices declining sufficiently to enable widespread mid-segment adoption. This cost erosion stems from manufacturing scale economies and improved semiconductor fabrication yields, making LED-based control modules economically viable for volume production vehicles. The price trajectory has reached a tipping point where LED systems now offer superior total cost of ownership compared to halogen alternatives when factoring in energy consumption, lifespan, and maintenance requirements. The cost reduction extends beyond LED emitters to include control electronics, with power management ICs and thermal management solutions becoming more affordable through volume production. This pricing dynamic has created a competitive advantage for early adopters who can offer LED-based control modules at price points previously dominated by halogen systems.

Premium-Vehicle Growth in Emerging Asia-Pacific Economies

Expanding premium vehicle sales in emerging Asia-Pacific markets is driving sophisticated headlight control module adoption, with luxury vehicle penetration creating demand for advanced lighting technologies that differentiate brand positioning. Economic growth in markets like India, Southeast Asia, and secondary Chinese cities has generated a new demographic of affluent consumers who prioritize vehicle technology features, including adaptive lighting systems. This trend has prompted luxury OEMs to standardize advanced headlight control modules across regional model variants, creating volume opportunities for Tier-1 suppliers with localized production capabilities.

The premium segment growth is particularly pronounced in markets with challenging driving conditions, where adaptive beam control provides tangible safety benefits that justify premium pricing. Local regulatory frameworks in these markets are evolving to accommodate advanced lighting technologies, creating regulatory tailwinds for sophisticated control module adoption. The geographic expansion of premium brands has also driven technology transfer, with features previously exclusive to European or North American markets now becoming standard in Asia-Pacific luxury vehicles.

Electrification Raising 48-V Electrical-Architecture Demand

The automotive industry's electrification trajectory catalyzes the adoption of 48V electrical architectures that enable more powerful and responsive headlight control systems, fundamentally changing the power budget available for lighting applications. The transition from traditional 12V systems to 48V architectures provides approximately 4x the power capacity while maintaining similar current levels, enabling high-intensity LED arrays and rapid actuator response times required for matrix beam control[2]Sang Wook Lee, "Implementation and Experimental Verification of Smart Junction Box for Low-Voltage Automotive Electronics in Electric Vehicles," Applied Sciences, mdpi-res.com . This architectural evolution simplifies power conversion requirements for LED drivers, reducing component count and improving thermal efficiency in compact module designs. The 48V infrastructure also supports advanced thermal management systems with active cooling fans and heat pumps, addressing a critical constraint in high-power LED applications. OEMs report that 48V systems enable more sophisticated control algorithms with faster processing capabilities, supporting real-time beam pattern optimization based on vehicle dynamics and environmental conditions. The electrification trend has created a technology convergence where headlight control modules can leverage the same power infrastructure used for mild-hybrid systems, creating economies of scale in component sourcing and system integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost and Design Complexity of Adaptive Modules | -0.7% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Semiconductor Supply-Chain Volatility | -0.5% | Global, with Asia-Pacific manufacturing concentration | Medium term (2-4 years) |

| Patchwork Homologation Rules Across Regions | -0.4% | Europe, North America, and Asia-Pacific regulatory frameworks | Medium term (2-4 years) |

| Thermal Management Limits for Compact LED Drivers | -0.3% | Global, acute in high-temperature climates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost and Design Complexity of Adaptive Modules

The inherent complexity of adaptive headlight control modules presents significant cost and engineering challenges that constrain market penetration, particularly in price-sensitive vehicle segments where advanced lighting features compete with other technology priorities. Adaptive systems require sophisticated integration of sensors, actuators, control algorithms, and thermal management components, creating a system-level complexity that multiplies potential failure modes and warranty exposure for OEMs. The design complexity extends to software development, where control algorithms must process real-time input from multiple sensors while maintaining fail-safe operation and regulatory compliance across diverse operating conditions[3]A.J. Sairam, "Optimal Control Logic for a Cost-effective Light Intensity Dependent Headlamp Enhanced by Internet of Things," IEEE, ieeexplore.ieee.org. Manufacturing complexity increases exponentially with the number of individually controllable LED elements, requiring precise optical alignment and thermal management that drives production costs and quality control requirements. The integration challenge is compounded by the need for seamless communication with vehicle ADAS systems, requiring additional validation and testing protocols that extend development timelines and increase engineering costs. This complexity barrier has created a market bifurcation where premium segments adopt advanced adaptive systems while volume segments remain constrained by cost considerations.

Semiconductor Supply-Chain Volatility

Ongoing semiconductor supply chain disruptions continue to impact headlight control module production, with automotive-grade MCUs and LED driver ICs experiencing extended lead times that constrain production scalability and increase procurement costs. The automotive semiconductor market faces persistent allocation challenges, with headlight control modules competing for the same MCU and analog IC components used in other vehicle systems, creating internal prioritization conflicts for OEMs. According to industry reports, lead times for automotive-qualified MCUs have extended to 20-54 weeks, forcing suppliers to maintain higher inventory levels and accept longer production planning cycles that increase working capital requirements. The supply constraint is particularly acute for specialized LED driver ICs with automotive qualification, where limited supplier options create single-source dependencies that amplify supply risk. Geopolitical tensions and export controls on semiconductor manufacturing equipment have further complicated supply chain planning, with suppliers increasingly pursuing dual-sourcing strategies that add complexity and cost to module designs. The volatility has prompted some OEMs to simplify headlight control module specifications to reduce component count and supplier dependencies, potentially slowing the adoption of advanced features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Adaptive Systems Drive Premium Integration

Adaptive units held a 53.04% of the headlight control module market share in 2024 and will log a 7.92% CAGR to 2030 as glare-free high-beam legislation spreads and ADAS fusion deepens. Adaptive modules already anchor premium trims; cost parity with basic units narrows each production cycle, aided by integrated thermal pads and common-footprint PCB designs. The headlight control module market size for adaptive variants is slated to widen further as over-the-air (OTA) software updates let OEMs monetize lighting features post-sale.

Basic modules linger in cost-sensitive fleet and aftermarket spheres, but their share erodes as regulators sunset halogen allowances. Suppliers pivot basic product lines into vertically integrated service parts to protect volume while funneling R&D toward adaptive algorithm libraries that harvest camera imagery for predictive beam sculpting.

By Technology: LED Dominance with Xenon Resurgence

LED platforms accounted for 52.27% of the headlight control module market share in 2024, thanks to efficiency, package flexibility, and the ability to segment beams at pixel scale. The headlight control module market size tied to LED is projected to grow steadily, yet faces thermal ceiling pressures that spur research in liquid micro-channels and graphite heat spreaders.

Xenon modules, though energy-dense, reclaimed momentum with a 6.13% CAGR outlook because some luxury brands prize their color temperature and long-range penetration in fog. A hybrid approach, LED low beam plus Xenon high beam, emerges in SUVs where designers chase both styling freedom and lumen punch. Halogen continues a sunset trajectory, kept alive mainly by cost and ease of replacement.

By Functionality: High Beam Assist Leads Market Evolution

High Beam Assist holds a 28.73% share of the headlight control module market in 2024 by automating glare mitigation via camera feedback and rapid LED dimming, a functionality now expected even in upper-mid trims. The headlight control module market grows as software improvements smooth beam transitions that once annoyed drivers.

Cornering/Bending Light Control heads the growth chart at 6.81% CAGR through 2030, as urban crash data pushes regulators to favor lateral beam drag that illuminates pedestrian zones. Future releases blend steering-angle, yaw rate, and map-based curve prediction, merging once-discrete functions into holistic scene-aware lighting.

By Vehicle Type: Passenger Vehicles Maintain Leadership

Passenger cars held a 58.39% share of the headlight control module market in 2024 and are set to expand at a 5.88% CAGR through 2030, owing to global light-vehicle recovery and consumer appetite for higher-spec tiers. Thus, the headlight control module market share within passenger lines remains the prime battleground for volume and innovation.

Light Commercial Vehicles increasingly specify adaptive modules to cut driver fatigue on night deliveries. At the same time, heavy trucks are selectively adopted for long-haul safety. Suppliers tailor PCB conformal coatings and heatsink materials to withstand diesel-engine vibration and extended duty cycles, carving a niche margin layer absent in passenger segments.

By Distribution Channel: OEM Dominance with Aftermarket Growth

Original equipment manufacturers (OEMs) hold a 91.06% share of the headlight control module market in 2024 because calibration to ADAS and diagnostic networks occurs best during line build. Yet the aftermarket will post a 9.23% CAGR through 2030, as do-it-yourself enthusiasts seek LED retrofit kits with plug-and-play controllers certified for regulatory compliance.

Module makers respond with universal harness adapters and smartphone calibration apps, though legislative divergence still constrains addressable volume. The headlight control module industry maintains two-tier logistics, tight OEM integration, and fragmented aftermarket channels, each with unique margin structures.

Geography Analysis

In 2024, Asia-Pacific dominates the global headlight control module market with a 41.96% share, driven by strong automotive production in China, Japan, and South Korea. The region benefits from established Tier-1 supplier networks and rising premium vehicle adoption in markets like India and Southeast Asia. Chinese OEMs increasingly standardize advanced modules to enhance brand competitiveness, while Japanese suppliers like Koito and Stanley Electric lead in adaptive beam algorithms and thermal management. Integrated supply chains reduce costs and enable rapid technology deployment across platforms.

The Middle East and Africa are the fastest-growing regions, with an 8.37% CAGR through 2030, supported by GCC countries' luxury vehicle demand and aftermarket OEM-grade components growth. Extreme temperatures and dusty conditions drive demand for robust thermal management and sealed designs. Europe sees steady demand due to UNECE regulations requiring advanced glare control systems, while North America grows with ADAS integration and premium feature adoption. Regional priorities vary: Asia-Pacific focuses on cost efficiency, Europe on regulatory compliance, North America on ADAS and connectivity, and Middle East and Africa on durability under harsh conditions.

South America shows selective growth in Brazil and Argentina, driven by automotive production recovery and premium vehicle imports. Regulatory frameworks vary, with some markets adopting UNECE standards while others maintain unique requirements, influencing module specifications and supplier strategies. Geographic supply chain considerations are critical, with suppliers establishing regional production to reduce costs and improve responsiveness. Geopolitical factors further drive supply chain diversification, shaping regional market trends.

Competitive Landscape

The headlight control module market exhibits moderate concentration with established Tier-1 automotive suppliers maintaining technological leadership through extensive patent portfolios and integrated manufacturing capabilities. Market leaders like Koito, HELLA, Valeo, and Continental leverage their scale advantages to invest in R&D for next-generation adaptive beam technologies while maintaining cost competitiveness through vertical integration and global production networks. Competition intensifies around thermal management innovations and software-defined lighting functions, where suppliers differentiate through proprietary algorithms for beam pattern optimization and integration capabilities with vehicle ADAS systems. White-space opportunities exist in V2X-enabled lighting coordination and machine learning-based predictive beam control, where traditional automotive suppliers compete with technology companies bringing software expertise to hardware-centric markets.

Emerging disruptors include semiconductor companies like Texas Instruments and Renesas that provide integrated control solutions. These companies potentially bypass traditional Tier-1 suppliers by offering direct-to-OEM platforms with embedded intelligence and connectivity features. The competitive landscape reveals strategic partnerships between lighting suppliers and technology companies to combine hardware manufacturing expertise with software development capabilities, as seen in recent collaborations around adaptive beam algorithms and thermal management solutions.

Headlight Control Module Industry Leaders

-

Hella GmbH and Co. KGaA

-

Valeo SA

-

Marelli Holdings

-

Denso Corporation

-

Koito Manufacturing Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hella, a subsidiary of Forvia, equipped NIO's Onvo L90 SUV with its advanced interactive pixel headlight system. Building upon Onvo's iconic light cluster design, this system elevates the L90's intelligent features and harmonizes with the SUV's distinctive style and front trunk configuration.

- June 2024: FORVIA HELLA announced a strategic realignment of its lighting production at the Lippstadt facility to enhance competitiveness amid evolving European market conditions. The plant is set to specialize exclusively in producing cutting-edge headlamp technologies, while existing and upcoming production of rear combination lamps, interior lighting, and car body lighting will be relocated to other sites.

Global Headlight Control Module Market Report Scope

| Basic Headlight Control Modules |

| Adaptive Headlight Control Modules |

| Halogen |

| LED |

| Xenon |

| Automatic Headlight Control |

| Manual Headlight Control |

| Daytime Running Light Control |

| High Beam Assist |

| Cornering/Bending Light Control |

| Headlight Levelling |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Module Type | Basic Headlight Control Modules | |

| Adaptive Headlight Control Modules | ||

| By Technology | Halogen | |

| LED | ||

| Xenon | ||

| By Functionality | Automatic Headlight Control | |

| Manual Headlight Control | ||

| Daytime Running Light Control | ||

| High Beam Assist | ||

| Cornering/Bending Light Control | ||

| Headlight Levelling | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2025 valuation of the global headlight control module market?

The market is valued at USD 4.59 billion in 2025.

Which region commands the largest revenue share?

Asia-Pacific leads with 41.96% share in 2024.

Which module type is growing fastest?

Adaptive headlight control modules are expanding at 7.92% CAGR through 2030.

Why are 48 V architectures important for lighting?

They quadruple available power, enabling dense LED arrays and rapid beam adjustment without bulky cabling.

Which distribution channel is projected to grow fastest?

The aftermarket is forecast to rise 9.23% CAGR due to retrofit LED demand.

What regulatory frameworks drive adaptive lighting adoption?

UNECE Regulation 48 and FMVSS 108 mandate glare reduction, pushing OEMs toward adaptive beam technologies.

Page last updated on: