Train Lighting Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 0.92 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

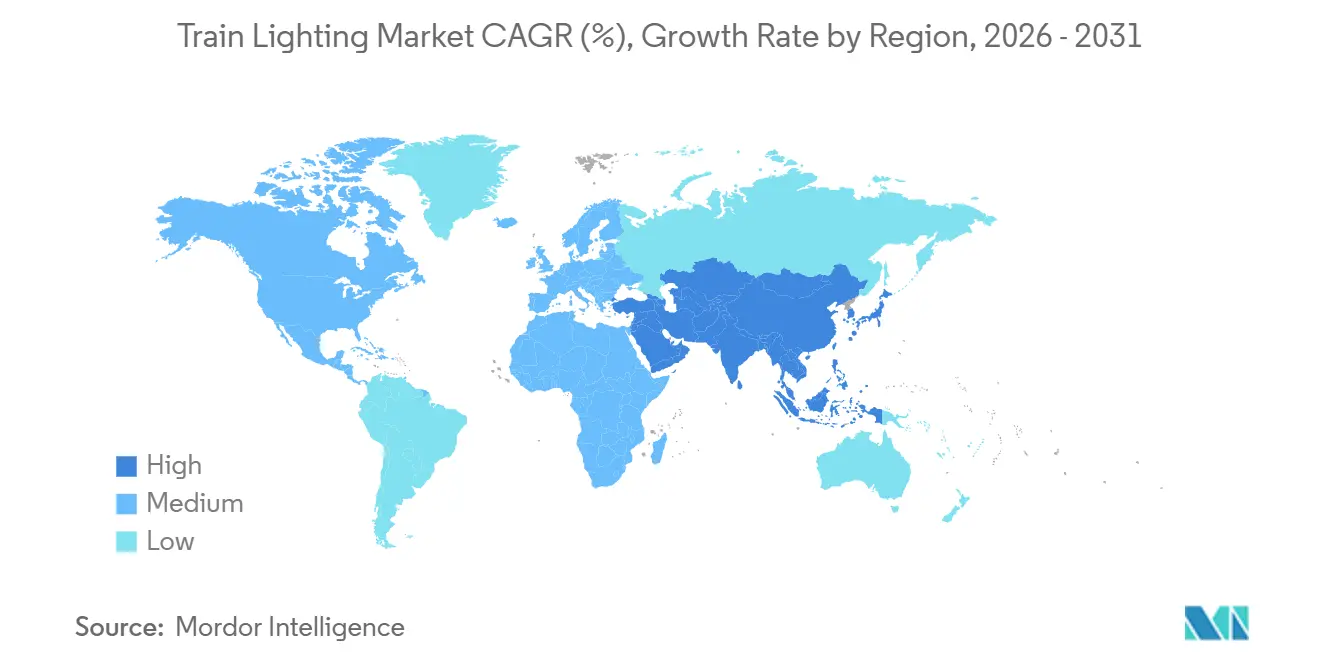

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Train Lighting Market Analysis by Mordor Intelligence

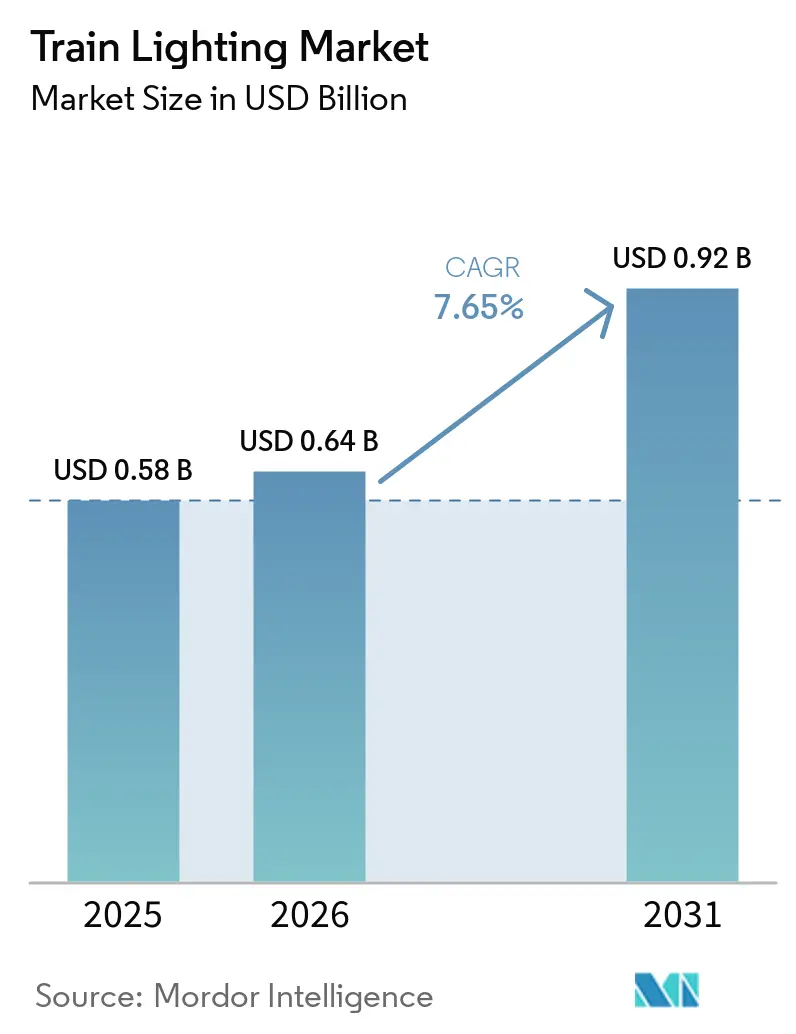

The train lighting market size is expected to increase from USD 0.58 billion in 2025 to USD 0.64 billion in 2026 and reach USD 0.92 billion by 2031, growing at a CAGR of 7.65% over 2026-2031. Robust retrofit activity, safety-driven exterior upgrades and the shift toward smart, connected solutions keep demand on a steady upswing. LED technology, already the dominant light source, benefits from long service life, lower energy use and falling unit prices, while urban rail expansion in Asia-Pacific bolsters new-build volumes. Digital diagnostics embedded in smart luminaires reduce unscheduled downtime, creating a strong value proposition for operators seeking leaner maintenance budgets. Competitive positioning favors suppliers capable of bundling hardware with fleet-management software and that are compliant with EN 45545, APTA, and similar regional standards.

Key Report Takeaways

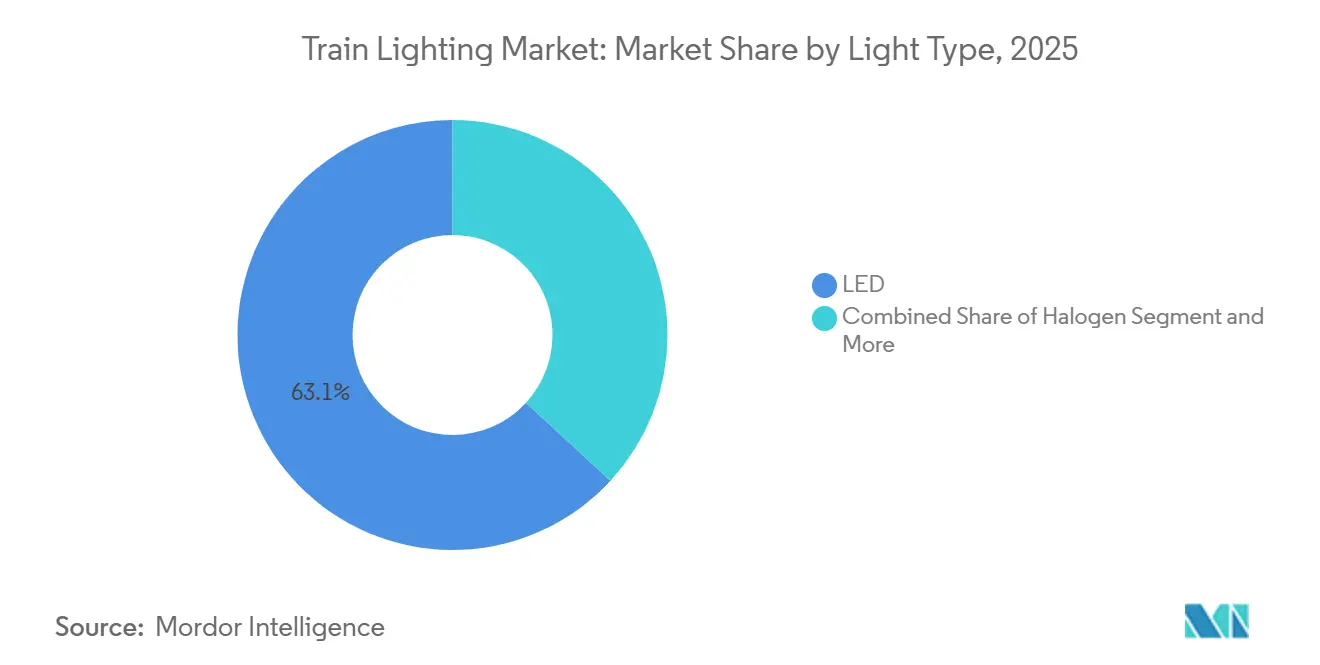

- By light type, LED captured 63.15% of the train lighting market share in 2025 and posts the highest projected CAGR at 8.95% through 2031.

- By position, interior lighting accounted for 53.18% of the train lighting market share in 2025, while exterior applications are set to advance at an 8.63% CAGR through 2031.

- By rolling stock, passenger coaches led with 25.33% of the train lighting market share in 2025; metros are the fastest-growing sub-segment, growing at a 9.79% CAGR to 2031.

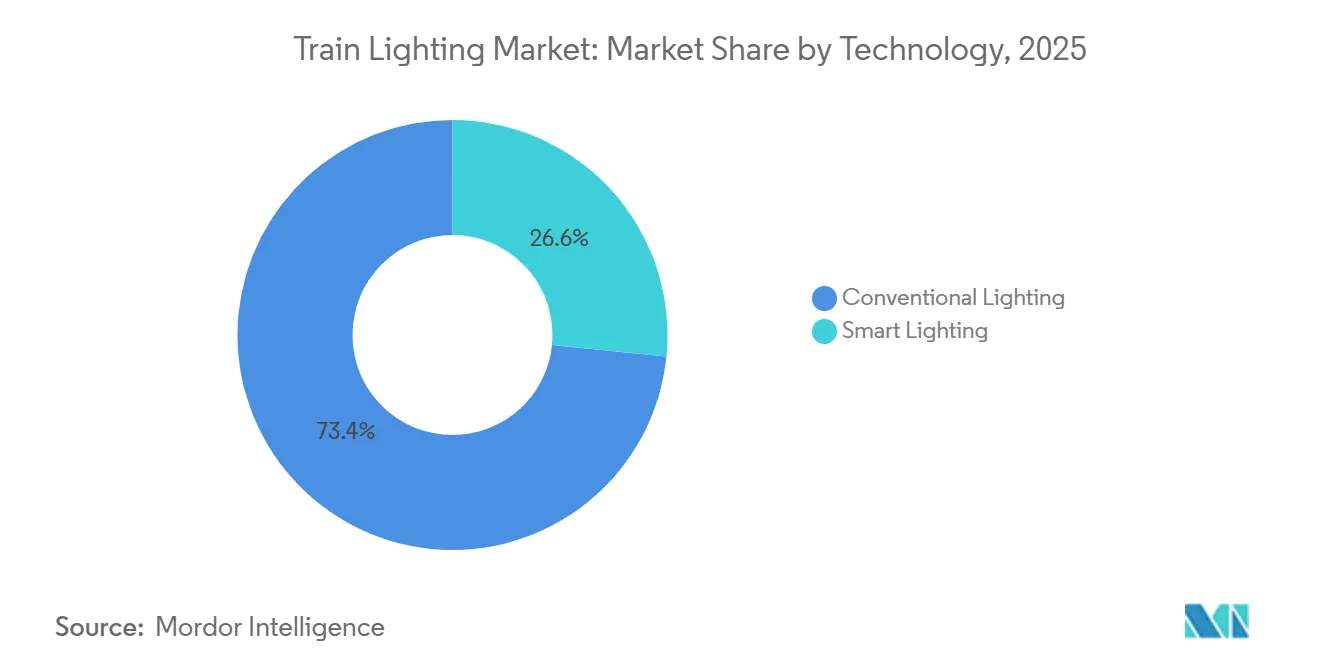

- By technology, conventional solutions retained a 73.41% of the train lighting market share in 2025, yet smart lighting is forecast to expand at a 11.99% CAGR through 2031.

- By end user, public operators accounted for 68.14% of the train lighting market share in 2025, whereas private fleets recorded the fastest growth at a 9.17% CAGR through 2031.

- By geography, Asia-Pacific accounted for 38.55% of the train lighting market share in 2025 and is projected to grow at an 8.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Train Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficient LED Retrofits Lower Costs | +2.1% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Compliance with Safety Lighting Standards | +1.8% | Europe, North America, expanding globally | Short term (≤ 2 years) |

| Rapid Asia-Pacific Metro Expansion | +1.7% | APAC, particularly China and India | Long term (≥ 4 years) |

| Smart IoT Lighting for Monitoring | +1.4% | APAC core, spill-over to Europe and North America | Medium term (2-4 years) |

| European Programs Demand LED Kits | +1.2% | Europe, technology transfer to other regions | Short term (≤ 2 years) |

| Adaptive Tunnel Lighting Mitigates Pollution | +0.9% | Europe and developed APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient LED Retrofits Lowering Total Lifecycle Cost

Operators gravitate to LEDs because service life regularly exceeds 60,000 hours, stretching replacement intervals and trimming inventory burdens[1]"LED Lighting challenges," Grah Lighting, www.grahlighting.com. Payback periods of 2 to 3 years remain common where rolling stock accumulates high daily mileage. The business case strengthens further as turnkey retrofit kits eliminate the need for rewiring, dramatically reducing installation labor. Historic budget hesitation among freight fleets is waning as supply of fluorescent tubes diminishes. As standard-gauge networks harmonize headlight intensity rules, LEDs emerge as a low-risk compliance route that future-proofs fleets against looming efficiency mandates.

Compliance with EN 45545, APTA and Other Safety Lighting Standards

Fire-smoke criteria under EN 45545 and photometric thresholds in APTA rules drive material selection and photometric testing[2]Kimmo Kaukanen, "Guide to EN 45545-2 fire testing requirements for railway materials," Measurlabs, measurlabs.com. Suppliers invest in flame-retardant polymers and accredited labs to maintain approval status. Certified product lines simplify cross-border tendering, giving incumbents first-mover advantage. At the operator level, documented compliance streamlines fleet certification for cross-regional service. The incremental cost, while notable, is viewed as a necessary hedge against retrofit rework.

Rapid Metro and Light-Rail Expansion in Asia-Pacific Driving New Lighting Installations

Large-scale projects in India, Indonesia and Vietnam replicate the template, embedding LED interiors as baseline specification. The growing adoption of driverless metros is driving demand for exterior marker lights tied to automated control systems. Local content clauses prompt domestic suppliers to broaden their product portfolios, yet international vendors hold an edge in certification expertise. As passenger comfort rises on the policy agenda, full-spectrum LEDs with higher color-rendering indices are gaining traction across new lines.

IoT-Enabled Smart Lighting Improving Fleet-Wide Asset Monitoring

Smart luminaires send real-time operational data to maintenance dashboards, flagging anomalies before faults occur. Predictive alerts shrink unplanned downtime and help operators optimize spare-part holdings. Functionality extends to adaptive dimming modes triggered by ambient light or carriage occupancy, unlocking additional energy savings without sacrificing safety. Integration with train management systems supports centralized updates, ensuring configuration consistency across multi-depot fleets. Cybersecurity remains a parallel focus, with operators ring-fencing lighting networks inside secure sub-domains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Cost vs Fixtures | -1.3% | Global, cost-sensitive operators | Short term (≤ 2 years) |

| Volatile LED Chip Supply Chains | -1.1% | Global, impact on North America and Europe | Medium term (2-4 years) |

| Limited ROI for Freight Operators | -0.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Cyber-Security Risk in Networks | -0.6% | APAC and Europe leading smart adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Retrofit CAPEX Versus Legacy Fluorescent Fixtures

Purchase prices for rail-grade LED assemblies still outstrip fluorescent units, challenging operators with tight capital envelopes. Financing instruments from multilateral lenders ease the hurdle, but approval timelines slow rollouts. Some fleets adopt phased conversion, focusing first on high-failure or safety-critical areas. As legislation targets mercury disposal, fluorescent options will continue to fade, pointing to LED inevitability. Suppliers counter cost objections with service-life warranties that rebalance the total-cost calculus.

LED Chip Supply-Chain Volatility Amid Geo-Political Trade Tensions

Concentrated wafer production heightens exposure to export controls and tariff swings, occasionally stretching delivery cycles. To buffer risk, lighting vendors dual-source critical emitters and pre-qualify alternative binning. Qualification loops, however, add months to project timelines and tie up engineering capacity. Greater traceability across the semiconductor supply chain is gradually emerging as buyers request origin documentation. Strategic stockpiling remains a stopgap as the ecosystem seeks longer-term resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Light Type: LED Gains Further Ground

LED retains clear leadership with 63.15% of the train lighting market share in 2025, while its nearest rivals ceded ground as maintenance economics shifted decisively in favor of solid-state sources. Operators favor LEDs for their durability and regulatory headroom, qualities underscored in prominent locomotive retrofit programs. Standardization of footprints and optics smooths fleet conversions, and suppliers increasingly market drop-in modules to minimize downtime. The declining availability of legacy halogen or fluorescent spares hastens switchover timelines. With color-tuning and smart-bus compatibility now standard on premium models, LED incumbency looks secure.

Growth momentum aligns with an 8.95% CAGR, the fastest among light types. New-build rolling stock now specifies LED as the default, eliminating the need for debate over specifications. Refurbishment tenders routinely bundle lighting into broader energy-efficiency packages, thereby amplifying the addressable volumes. Freight locomotives, once a holdout, are moving to LED headlights for better lumen maintenance and lower amperage draw. Niche xenon fixtures disappear from catalogs as equivalent LED packages hit mandated candela thresholds. Over the forecast horizon, halogen and fluorescent lamps transition almost entirely to aftermarket niches.

By Position: Interior Leads, Exterior Gathers Pace

Interior luminaires accounted for 53.18% of the train lighting market share in 2025, owing to abundant fixture points within coaches and multiple ambiance layers. Passenger comfort, color consistency, and vandal-resistant frame are the most common procurement checklists. Modular ceiling panels facilitate factory installation and simplify progressive refits in existing cars. Reading lights, corridor strips, and restroom fixtures converge on a single set of integrated drivers to save space. Enhancements in lens design spread illumination evenly without glare.

Exterior units advance at the segment-leading 8.63% CAGR as safety regulations tighten luminous-intensity thresholds. Headlights, marker lights, and tail lamps rank high for immediate payback because reduced current draw translates into smaller alternator load and lower fuel use. All-in-one exterior modules with quick-swap fronts address harsh operating conditions and enable line-side replacement at high speed. Enhanced ingress-protection ratings sustain performance during washdowns and ballast strikes. Thermal architecture optimized for wide ambient swings improves perceived reliability among operators operating in extreme climates.

By Train Type: Passenger Coaches Dominate, Metros Accelerate

Passenger coaches hold 25.33% of the train lighting market share in 2025 on account of their large installed base across intercity corridors. Upgrade cycles often synchronize lighting with HVAC and seat refurbishment, maximizing workshop uptime. Uniform fixture geometry across coach series helps suppliers standardize components. Certification documentation, once secured, can cover decades of production, reinforcing vendor lock-in. Retrofit programs financed with recovery funds create sizable, but predictable, order blocks.

Metros book the quickest trajectory at a 9.79% CAGR through 2031, powered by driverless-train rollouts in Asia-Pacific’s mega-cities. Platform-screen doors, advanced CCTV, and smart lighting increasingly form integrated bid packages. Metro operators value fail-safe battery-backup luminaires that support rapid evacuation protocols. Lightweight assemblies help maintain energy budgets where regeneration and onboard storage interplay tightly. The uplift extends beyond rolling stock, spilling into depot and tunnel lighting to ensure maintenance visibility.

By Technology: Smart Lighting Outpaces Conventional

Conventional solutions are expected to account for 73.41% of the train lighting market share in 2025, as many fleets prioritize straightforward LED replacements over adopting connectivity features. Simplicity, proven reliability, and low upfront expense sustain this preference, particularly among freight and regional operators. Platform synergy with existing wiring looms keeps disruption minimal. Replacement cycles mirror scheduled heavy-maintenance intervals, aligning capital outlay with routine service windows. As supply stabilizes, conventional LEDs drop in price, preserving their baseline appeal.

Smart lighting is growing at a 11.99% CAGR as predictive maintenance gains executive endorsement. Diagnostics embedded in each luminaire pinpoint voltage anomalies or temperature excursions before lumens sag. Ethernet-over-twisted-pair backbones piggyback on train control networks, limiting new cabling. Firmware upgrades over the air preserve asset value. Operators trial adaptive brightness models that dim aisles when occupancy sensors detect empty cars, lowering consumption without breaching safety codes. Future network extensions envisage data hand-off to wayside systems for holistic energy orchestration.

By End User: Public Sector Leads, Private Concessions Grow Fast

Public rail agencies accounted for 68.14% of the train lighting market share in 2025, owing to their stewardship of national and commuter operations. Multi-year capital plans embed lighting within broader decarbonization strategies, providing suppliers with visibility on procurement pipelines. Grant funding and international loans soften initial cost burdens, yet bidding remains price-sensitive. Framework agreements streamline call-off orders across diverse rolling-stock classes, creating economies of scale. Technical specifications frequently cite established reference projects to de-risk selections.

Private operators chart the higher 9.17% CAGR as concession contracts proliferate in emerging metros and regional corridors. These companies often pursue aggressive lifecycle-cost targets to satisfy shareholder expectations, making connected lighting a logical fit. Performance-based maintenance contracts incentivize uptime guarantees and shift reliability risk to suppliers. Financing models tied to ridership revenue can unlock earlier adoption of smart features. As branding gains marketing weight, private fleets experiment with dynamic color schemes, pushing luminaire manufacturers to broaden aesthetic options.

Geography Analysis

Asia-Pacific anchors demand, accounting for 38.55% of the train lighting market share in 2025 and an 8.23% CAGR outlook. Rapid urbanization drives elevated coach orders, and local standards mandating higher tunnel luminance accelerate LED penetration. Suppliers collaborate with domestic car builders to navigate certification and localization rules. The growing emphasis on automated operations is driving investment in connected lighting as a cornerstone of intelligent trains. Cross-border export ambitions of regional vendors intensify competition in the global train lighting market.

Europe’s mature network shows steady renewal activity under green-mobility funding programs. Operators tap EU grants to refurbish aging fleets, and strict fire-smoke and recyclability laws sustain premium product uptake. Incumbent suppliers leverage deep compliance portfolios to secure repeat orders. Smart-bus architectures gain traction in long-distance services as part of digital-train demonstrators. Sustainability reporting requirements propel disclosure of luminaire recyclability and embodied carbon.

The Americas combine retrofit momentum in legacy diesel fleets with select new-build metro schemes. North American safety standards enforce high candela values for exterior fixtures, guiding niche specialization among domestic suppliers. South American metros are increasingly specifying LED from day one to curtail operational costs. Cross-border supply logistics, particularly lead-time sensitivity, influence sourcing decisions. Growing scrutiny of cybersecurity in public procurement is driving the inclusion of secure-boot and encrypted-communication clauses in lighting packages.

Competitive Landscape

The top five train lighting vendors share space with agile regional specialists, fostering fragmentation. Established players bank on decades of rolling-stock OEM alliances, using broad certification libraries as competitive moats. Incremental product updates, such as self-diagnosing drivers, refresh value propositions without altering mechanical interfaces. Regional firms differentiate through quick-turn custom orders, especially for niche exterior modules or heritage-fleet spares.

Digital integration shapes recent strategy shifts. Teknoware’s Traintelligence suite exemplifies the vendor's pivot toward software-assisted maintenance, offering dashboards that visualize fixture health in real time. LPA Group’s contract haul across multiple European refurbishments underscores the reward for multi-platform adaptability. Semiconductor vendors partner with lighting OEMs to co-develop rail-grade emitters, reinforcing vertical collaboration loops.

Consolidation at the system-integrator level creates both opportunities and threats. Large conglomerates extend portfolios into subsystems adjacent to lighting, bundling offers around complete electrical architectures. Independent lighting suppliers counter by forming technology alliances, pooling R&D on secure data protocols. Sustainability narratives deliver added positioning leverage, as operators factor recyclability and material sourcing into award criteria. Overall, competition balances heritage credibility with innovation agility.

Train Lighting Industry Leaders

-

LPA Group plc

-

Teknoware Oy

-

SBF Spezialleuchten GmbH

-

LECIP Holdings Corporation

-

ams-OSRAM AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: INPS unveiled its latest innovation in illuminated technology: precision-engineered backlit control panels. These panels, crafted from high-impact acrylic and custom laser-cut, boast embedded LED lighting, seamlessly merging functionality with a contemporary aesthetic.

- June 2025: INPS unveiled a modular LED lighting solution for autorack railcars, enhancing loading visibility and operational safety.

Global Train Lighting Market Report Scope

The Train Lighting Market is analyzed based on light type, position, train type, technology, end-user, and geography.

By Light Type, the market is segmented into LED, Halogen, Fluorescent, and Xenon. By Position, the market is segmented into Interior Lighting (Cabin, Corridor, Restroom, and Reading Lights) and Exterior Lighting (Headlights, Tail Lights, and Marker Lights). By Train Type / Rolling Stock, the market is segmented into Diesel Locomotives, Electric Locomotives, DMUs, EMUs, Metros, Light Rail, Passenger Coaches, and Freight Wagons. By Technology, the market is segmented into Conventional Lighting and Smart Lighting (IoT-enabled and Adaptive Systems). By End User, the market is segmented into Public Rail Operators and Private Rail Operators. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

| LED |

| Halogen |

| Fluorescent |

| Xenon |

| Interior Lighting | Cabin |

| Corridor | |

| Restroom | |

| Reading Lights | |

| Exterior Lighting | Headlights |

| Tail Lights | |

| Marker Lights |

| Diesel Locomotives |

| Electric Locomotives |

| DMUs |

| EMUs |

| Metros |

| Light Rail |

| Passenger Coaches |

| Freight Wagons |

| Conventional Lighting | |

| Smart Lighting | IoT-enabled |

| Adaptive Systems |

| Public Rail Operators |

| Private Rail Operators |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Light Type | LED | |

| Halogen | ||

| Fluorescent | ||

| Xenon | ||

| By Position | Interior Lighting | Cabin |

| Corridor | ||

| Restroom | ||

| Reading Lights | ||

| Exterior Lighting | Headlights | |

| Tail Lights | ||

| Marker Lights | ||

| By Train Type / Rolling Stock | Diesel Locomotives | |

| Electric Locomotives | ||

| DMUs | ||

| EMUs | ||

| Metros | ||

| Light Rail | ||

| Passenger Coaches | ||

| Freight Wagons | ||

| By Technology | Conventional Lighting | |

| Smart Lighting | IoT-enabled | |

| Adaptive Systems | ||

| By End User | Public Rail Operators | |

| Private Rail Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the train lighting market be by 2031?

The train lighting market size is projected to reach USD 0.92 billion by 2031, supported by a 7.65% CAGR from 2026-2031.

Which light source holds the biggest share in railway applications?

LED technology led the category with a 63.15% share in 2025, reflecting its durability, energy efficiency and regulatory alignment.

What is the fastest-growing application area for train lighting?

Exterior lighting, especially headlights and marker units, is expected to expand at an 8.63% CAGR through 2031.

Which rolling-stock segment shows the most rapid growth in lighting demand?

Metro trains are forecast to log a 9.79% CAGR as urban transit networks extend and adopt driverless operations.

Page last updated on: