Laser Headlight Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 18.81 Billion |

| Market Size (2030) | USD 66.01 Billion |

| Growth Rate (2025 - 2030) | 28.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Headlight Market Analysis by Mordor Intelligence

The Laser Headlight Market size is estimated at USD 18.81 billion in 2025, and is expected to reach USD 66.01 billion by 2030, at a CAGR of 28.56% during the forecast period (2025-2030). This expansion reflects rising global visibility rules, the quest for energy-efficient electric vehicles, and demand for lighting systems that work seamlessly with advanced driver assistance platforms. United States safety regulations impose strict limits on vehicle headlights' brightness and projection distance, presenting a challenging shift for automakers, while European UNECE R149 allows higher-luminance adaptive beams. Tier-1 suppliers respond by combining laser power with fine-grained LED matrix control, aiming to balance performance, cost, and compliance. Supply constraints for high-power blue laser diodes push manufacturers toward a hybrid architecture that reduces dependence on scarce components. Commercial fleet operators have begun to favor laser-assisted systems that cut driver fatigue on long routes and lower accident-related costs.

Key Report Takeaways

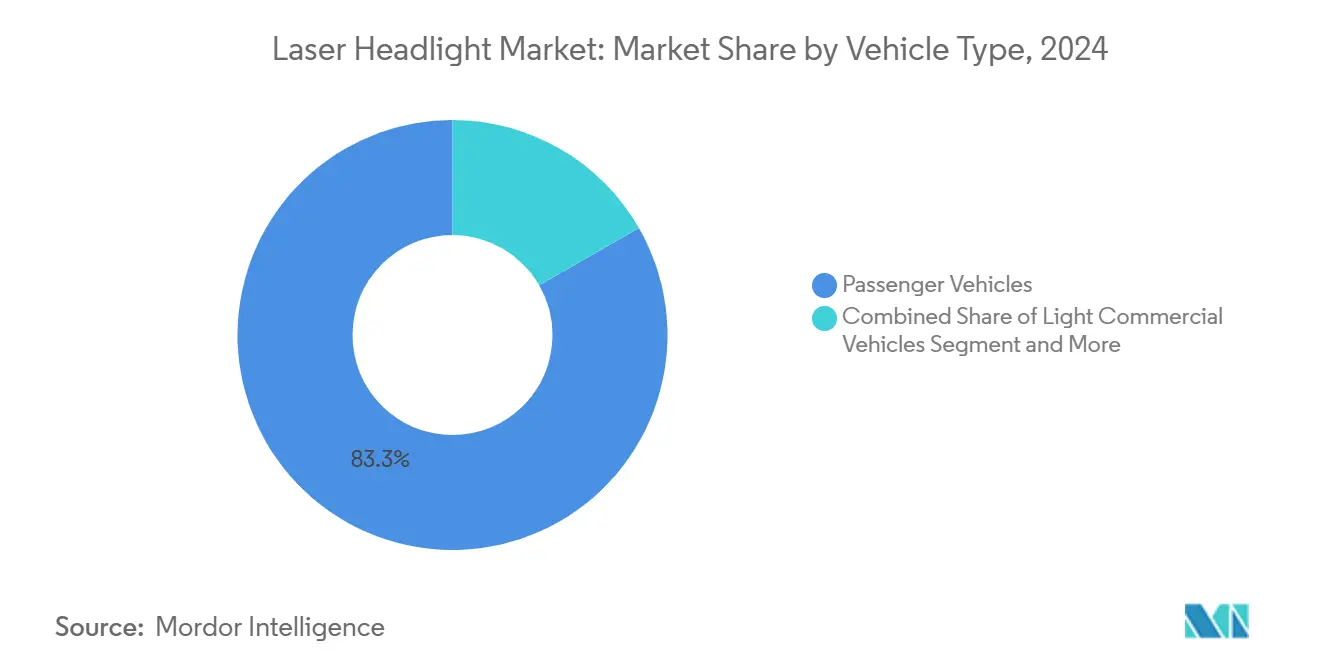

- By vehicle type, passenger cars held 83.27% of the laser headlight market share in 2024, whereas medium and heavy commercial vehicles are expected to record the fastest 28.59% CAGR during the forecast period (2025-2030).

- By technology, conventional laser systems accounted for 67.56% revenue share in 2024, yet intelligent variants are expected to grow at 28.65% CAGR during the forecast period (2025-2030).

- By sales channel, the OEM segment captured an 86.13% share of the laser headlight market in 2024, while aftermarket installations are expected to grow at a 28.66% CAGR during the forecast period (2025-2030).

- By application, high-beam units led with 47.28% market share in 2024; cornering-light modules are expected to expand at a 28.61% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific led with 37.83% revenue share in 2024, while the region is forecast to expand at a 28.63% CAGR during the forecast period (2025-2030).

Global Laser Headlight Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter UNECE and NHTSA Visibility Regulations | +6.2% | Europe and North America, spillover to Asia Pacific | Medium term (2-4 years) |

| EV Energy-Efficiency Push | +4.8% | Global, with early adoption in Europe and China | Long term (≥ 4 years) |

| Premium OEM Differentiation | +3.1% | North America and Europe, premium segments in Asia Pacific | Short term (≤ 2 years) |

| Rapid ADAS & Lidar Fusion | +2.9% | Global, led by autonomous vehicle development hubs | Long term (≥ 4 years) |

| V2X-Ready Projection Of Symbols/Patterns | +1.7% | Europe and North America, regulatory pilot programs | Medium term (2-4 years) |

| Thin Laser-Phosphor Modules Freeing Battery Packaging Space | +1.2% | Global EV markets, particularly China and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter UNECE & NHTSA Visibility Regulations

Uneven regulatory landscapes shape the laser headlight market. European regulations offer greater flexibility, allowing high-end vehicles to use advanced headlight systems that adapt to driving conditions and illuminate significantly farther than typical standards. In contrast, FMVSS 108 keeps U.S. systems within tighter limits, steering many brands toward hybrid LED-laser arrangements. Automakers invest in glare-prevention algorithms that dim specific pixels in milliseconds to satisfy real-time compliance. Tier-1 suppliers channel R&D budgets into photometric test benches to validate shifting beam patterns under diverse road conditions. The result is rapid iteration of firmware and optical designs that favor modular lamps usable in multiple jurisdictions without costly redesign. Supplier roadmaps increasingly highlight micro-optics that blend laser intensity with LED precision to sidestep future rule changes [1]“Regulation No. 149: Adaptive Front-Lighting Systems,” UNECE, unece.org .

EV Energy-Efficiency Push For Ultra-High-Luminance Lamps

Electric vehicles gain tangible range benefits when headlights deliver more lumens per watt. Laser-phosphor modules can cut consumption by up to one-third compared with legacy LED arrays when operating in high-beam mode, supporting smaller batteries or longer drive cycles. Heat generated by blue laser diodes can be redirected to warm the cabin in cold climates, allowing additional battery savings that resonate with consumers in northern regions. Automakers experiment with integrating lamp cooling loops into existing thermal circuits to avoid standalone fans that draw extra power. While technology raises upfront costs, the total cost of ownership improves for fleets that log high annual mileage. Energy regulators in Europe and China encourage efficient lighting through incentive programs that stimulate adoption.

Premium OEM Differentiation Via Long-Range Adaptive Beams

Luxury brands exploit laser lighting as a marketing beacon for technological leadership. With advanced headlight systems, BMW's production vehicles have outshone standard LEDs in long-range highway illumination, enhancing driver confidence at elevated speeds[2]“LaserLight Technology Explained,” BMW Group, bmwgroup.com . Adaptive algorithms tie beam length to vehicle speed and navigation data, so drivers enjoy optimal visibility without manual switching. Yet escalating bills of material and the United States regulatory ceilings temper rollout plans, prompting many nameplates to pivot toward dense microLED arrays that promise similar clarity at lower cost. Even so, laser systems remain a tangible status symbol in select flagship models, reinforcing brand narratives focused on advanced engineering.

Rapid ADAS & LiDAR Fusion Demanding Pixel-Level Lighting

Autonomous-ready platforms require headlights to sculpt light around other road users while highlighting lane markers or obstacles. MEMS mirrors inside laser units tilt beams in microseconds, enabling angular resolution below 0.1 degrees, which aligns with camera pixel grids for coordinated perception. Selective illumination simplifies computer-vision workloads by boosting contrast on items the software must classify. Integration teams confront new cybersecurity vectors because compromised lighting code could dazzle oncoming drivers; therefore, secure boot processes and over-the-air update encryption form part of design checklists. Shared sourcing of blue laser diodes for lidar and headlights reduces inventory complexity and encourages holistic thermal strategies across the front fascia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM & Production Cost | -3.4% | Global, particularly cost-sensitive markets in Asia Pacific | Short term (≤ 2 years) |

| Thermal-Management and Reliability Challenges | -2.1% | Global, critical in high-temperature regions | Medium term (2-4 years) |

| Upcoming IEC Eye-Safety Re-Classification Of Blue Lasers | -1.8% | Global, with immediate impact in Europe and North America | Short term (≤ 2 years) |

| Supply-Chain Constraints | -1.5% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High BOM & Production Cost Vs. Matrix-LED Solutions

High price points pose a significant hurdle to adoption. For example, swapping out a laser headlamp on a luxury European sports sedan can be several times pricier than upgrading to advanced LED matrix units. Blue laser diodes, which meet automotive-grade standards, are sold at a premium, primarily due to their lower production yields than LEDs.

Consequently, fleet operators, who prioritize total cost of ownership, often lean towards advanced LED arrays. These arrays offer most performance benefits but at a fraction of the cost. Suppliers, such as ams OSRAM, champion microLED solutions like the EVIYOS™ platform, positioning them as a cost-effective route to high-resolution adaptive lighting. However, until laser components achieve better economies of scale, their aggressive pricing will remain elusive, hindering widespread adoption.

Thermal-Management & Reliability Challenges

High-power diodes generate localized heat spikes that can degrade phosphor efficiency and shift color over time, threatening warranty metrics. Components in automotive duty cycles must function reliably, whether in frigid cold or sweltering heat. Inadequate thermal management can push junction temperatures past safe limits, underscoring the importance of robust cooling solutions for ensuring long-term performance and safety. Engineering teams add heat sinks, vapor chambers, or active liquid loops, but each addition raises mass and cost. Validation regimens include thermal shock, vibration, and photon flux stability tests tuned to laser-specific failure modes. Field data from early deployments in Southern Europe revealed elevated warranty claims tied to phosphor browning, prompting design revisions that delay volume rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Adoption

Passenger cars still dominate the laser headlight market with an 83.27% share in 2024 due to early deployments by German premium brands, but regulatory ceilings dull incremental gains. Light commercial vans occupy a middle ground, where budget pressures steer many fleet managers toward hybrid LED-lasers or pure LED alternatives. The medium and heavy commercial segment is on track for the fastest 28.59% CAGR during the forecast period (2025-2030), reflecting strong interest among logistics firms in improving night-time accident records.

Fleet operators see measurable savings when long-range beams cut collision rates and related downtime. European insurance providers have begun offering premium discounts for trucks with adaptive laser systems that integrate with lane-keeping cameras. The commercial trend has prompted Stanley Electric and Mitsubishi Electric to co-develop modules tailored to tall cab designs that improve forward visibility angles. On the passenger side, consumer enthusiasm wanes when owners realize that U.S.-spec units deliver shorter range than European counterparts, nudging buyers toward microLED matrices at lower price points. Consequently, manufacturers segment their offerings carefully, reserving laser optics for halo trims or regions with permissive laws.

By Technology Type: Intelligence Integration Accelerates

The conventional cohort retains 67.56% of 2024 revenue because early BMW and Audi systems have not yet cycled out of production, but momentum is shifting rapidly. Intelligent laser headlights accounted for a minority share in 2024, yet are rising at a 28.65% CAGR during the forecast period (2025-2030) as pixel-level control becomes a baseline expectation among premium OEMs.

Software-defined vehicles treat the lamp as another edge node that receives over-the-air updates, learns user preferences, and coordinates with cloud navigation services. MEMS-based scanners direct beams to label road hazards or draw temporary pedestrian crossings, turning illumination into a communication channel. Cost differentials shrink as integrated control ASICs replace discrete electronics in first-generation designs. Patent filings indicate growing supplier activity around neural-network-based glare detection that dynamically remaps intensity zones in response to camera feedback. In parallel, regulatory bodies explore test protocols that certify photometry and software integrity, reinforcing the need for intelligent architecture.

By Sales Channel: Aftermarket Retrofit Demand

OEM factories account for an 86.13% share of the laser headlight market in 2024 because integration complexity favors line-side installation. Even so, the aftermarket is expected to be the fastest-growing, with a 28.66% CAGR during the forecast period (2025-2030), as retrofit kits target commercial fleets and high-end enthusiasts who seek performance gains without buying new vehicles.

Regulatory hurdles slow independent installers in the United States, where parts must comply with FMVSS 108 and often require individual state inspections. Europe offers a more streamlined path: UNECE regulations allow kits if installers can document photometric compliance. To sidestep heat issues, retrofit providers package pre-calibrated modules with dedicated aluminum heat sinks and CAN bus adapters. Commercial carriers operating at night on rural highways form the most attractive customer base because the risk-reduction payback period is clear. However, universal designs remain elusive due to the need for model-specific brackets and aerodynamic trims.

By Application: Cornering Light Innovation

High-beam functions maintained a 47.28% share in the laser headlight market in 2024 because they exploit the primary advantage of laser luminance on straight roads. Cornering lights, however, are projected to expand at 28.61% CAGR during the forecast period (2025-2030), as autonomous-vehicle programs prioritize 360-degree visibility for low-speed urban maneuvers.

Dynamic cornering beams pivot in concert with steering and yaw sensors, lighting side streets before the driver commits to a turn. Laser modules enhance this capability by maintaining brightness even at sharp angles; LEDs often lose efficacy when optical paths lengthen. V2X integration lets lamps project pedestrian warnings when vehicles execute right turns across bike lanes, a function already piloted on delivery vans in Germany. Low-beam and daytime-running roles broaden adoption by amortizing costs over several lighting modes, yet thermal limits remain tighter in enclosed housings. Suppliers now study phosphor materials that retain color balance at elevated temperatures to unlock broader use cases.

Geography Analysis

Asia-Pacific commands a 37.83% share in the laser headlight market in 2024. It is expected to grow at a 28.63% CAGR as Chinese and Japanese automakers race to install premium lighting that differentiates brand portfolios. Domestic Chinese diode makers shorten supply chains, lowering lead times and easing price pressure. Japanese firms like Koito and Stanley leverage long-standing optics know-how to refine laser-phosphor modules that meet stringent durability tests. Despite this momentum, local regulators study glare complaints, prompting consideration of adaptive algorithms similar to European rules.

Europe sustains robust demand thanks to UNECE R149, which supports adaptive high beams that showcase laser reach. German marques once spearheaded laser adoption, but spiraling costs and the rapid rise of dense LED matrices have rebalanced technology strategies. Suppliers, including Valeo and Hella, hedge bets by developing microLED solutions while keeping laser expertise for niche sports cars alive. Scandinavian markets provide fertile ground because long winter nights magnify the safety benefits of extended illumination.

North America trails partly because FMVSS 108 restricts peak intensity, curbing laser performance advantages. Nevertheless, commercial-fleet retrofits gain traction for long-haul trucks that run fixed routes across the Plains, where deer strikes and low-light incidents are common. Canada mirrors the United States regulations, while Mexico hosts assembly plants that supply the region with hybrid lighting modules. Autonomous-vehicle test beds in California and Arizona demand pixel-level lighting to complement sensor suites, spurring small-batch laser prototypes despite regulatory uncertainty.

Competitive Landscape

The laser headlight market shows moderate concentration, with Koito, Valeo, Hella, and ams OSRAM holding lead positions through deep OEM ties and vertically integrated production. These firms are increasingly pivoting toward microLED matrices while preserving laser competencies for flagship models and commercial packages. AMS OSRAM’s 25,600-pixel EVIYOS™ illustrates a strategy to deliver high resolution without reliance on scarce laser diodes [3]“Investor Presentation FY 2025,” ams OSRAM, ams-osram.com . Koito’s patents on thermal-aware driver ICs enable efficient power distribution that scales across both LED and laser platforms, preserving optionality for automakers hedging technology bets.

Start-ups seek to disrupt with software-centric approaches that treat the lamp as a projector for informational graphics. Their agility appeals to emerging electric-only brands eager to differentiate dashboards and lighting simultaneously. Yet achieving automotive-grade reliability and gaining OEM validation cycles pose steep barriers. Established suppliers leverage decades of quality data, global service networks, and economies of scale to defend their share.

White-space opportunities open in medium-duty trucks, where safety regulators tighten nighttime visibility standards. Suppliers craft ruggedized housing and redundant cooling paths to withstand high engine-bay temperatures. Partnerships between thermal-management specialists and optics companies accelerate progress toward lighter heat sinks and more stable phosphor composites. Collaboration with lidar vendors is rising because shared laser components yield cost synergies and simplify module packaging.

Laser Headlight Industry Leaders

Robert Bosch GmbH

Continental AG

Valeo S.A.

Hella GmbH & Co. KGaA

Koito Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ams OSRAM issued EUR 500 million in senior notes due 2029 to pre-finance potential OSRAM minority put options and fund convertible-bond repurchases, underscoring its commitment to automotive lighting innovation.

- December 2024: ams OSRAM showcased EVIYOS™ HD 25 micro-LED headlights at CES 2025. These headlights deliver 25,600 individually controllable pixels for glare-free road projection.

- September 2024: ams OSRAM unveiled ALIYOS™ LED-on-foil technology with LEONHARD KURZ, enabling ultra-thin flexible lighting films for novel exterior designs.

Global Laser Headlight Market Report Scope

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Intelligent Laser Headlights |

| Conventional Laser Headlights |

| OEM |

| Aftermarket |

| High Beam |

| Low Beam |

| Cornering Light |

| Daytime Running Light |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Technology Type | Intelligent Laser Headlights | |

| Conventional Laser Headlights | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Application | High Beam | |

| Low Beam | ||

| Cornering Light | ||

| Daytime Running Light | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the laser headlight market in 2030?

Based on current projections, the laser headlight market is expected to reach USD 66.01 billion by 2030.

Which vehicle segment is growing fastest for laser headlights?

As fleets invest in long-range visibility, medium and heavy commercial vehicles register the quickest expansion at a 28.59% CAGR.

How do regulations influence laser headlight adoption in North America?

FMVSS 108 caps headlight intensity, reducing performance advantages and pushing OEMs toward hybrid or microLED solutions.

Why are intelligent laser headlights gaining traction?

Pixel-level control enables advanced driver assistance functions such as selective glare avoidance and road symbol projection.

Which region holds the largest share today?

Asia-Pacific leads with 37.83% of 2024 revenue, driven by premium adoption in China and Japan, plus supportive regulations.

What is the main cost barrier for laser headlights?

High-power blue laser diodes and specialized phosphor materials keep bill-of-materials costs roughly three times higher than LED matrices.

Page last updated on: