Automotive Ambiance Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

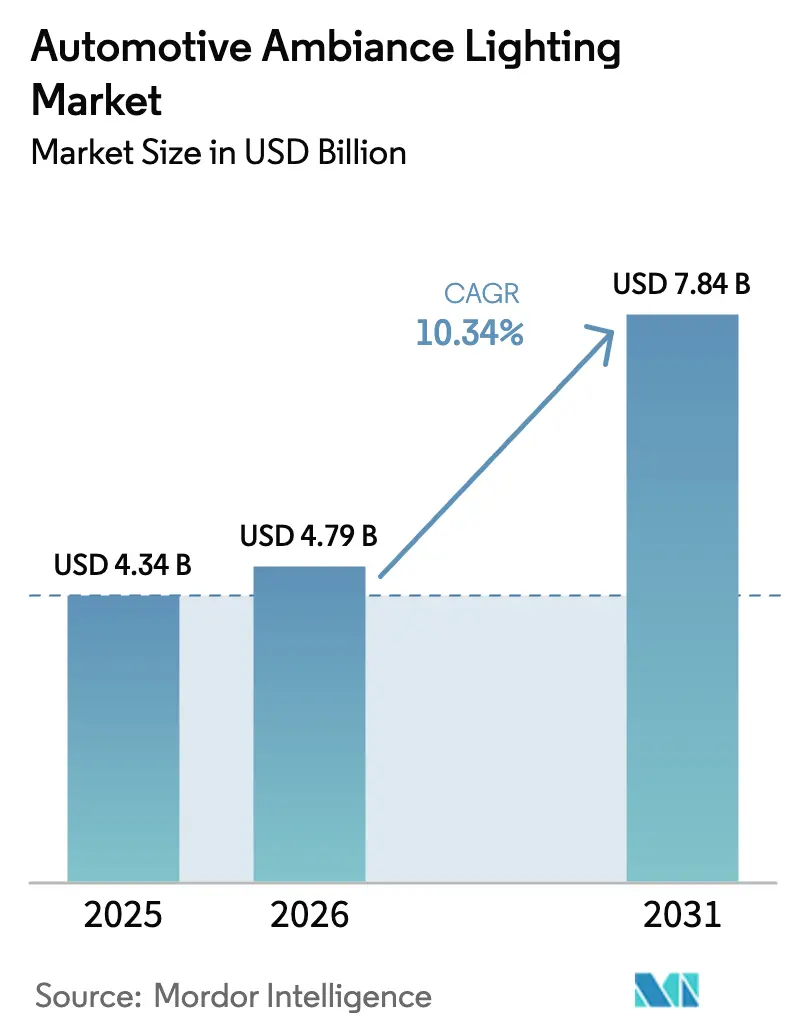

| Market Size (2026) | USD 4.79 Billion |

| Market Size (2031) | USD 7.84 Billion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Ambiance Lighting Market Analysis by Mordor Intelligence

The automotive ambient lighting market size is expected to grow from USD 4.34 billion in 2025 to USD 4.79 billion in 2026 and is forecast to reach USD 7.84 billion by 2031 at 10.34% CAGR over 2026-2031. This momentum reflects how vehicle makers now rely on lighting to build brand identity, shape user experience, and reinforce perceived quality. Lower LED prices, improved thermal management, and AI-driven personalization platforms have shifted ambient lighting from a luxury option to a mainstream feature in compact cars, electric vehicles, and premium SUVs alike. Passenger vehicles remain the prime growth engine, yet rising adoption by long-haul trucks signals a broader wellness-oriented design agenda for commercial fleets. Asia-Pacific leads demand on the back of China’s electric-vehicle boom, while North America and Europe stress safety, cybersecurity, and subscription-ready over-the-air (OTA) upgrades that monetize lighting features. Meanwhile, aftermarket retrofit kits thrive as buyers seek to refresh existing cabins, pushing the segment’s beyond the overall automotive ambient lighting market trajectory.

Key Report Takeaways

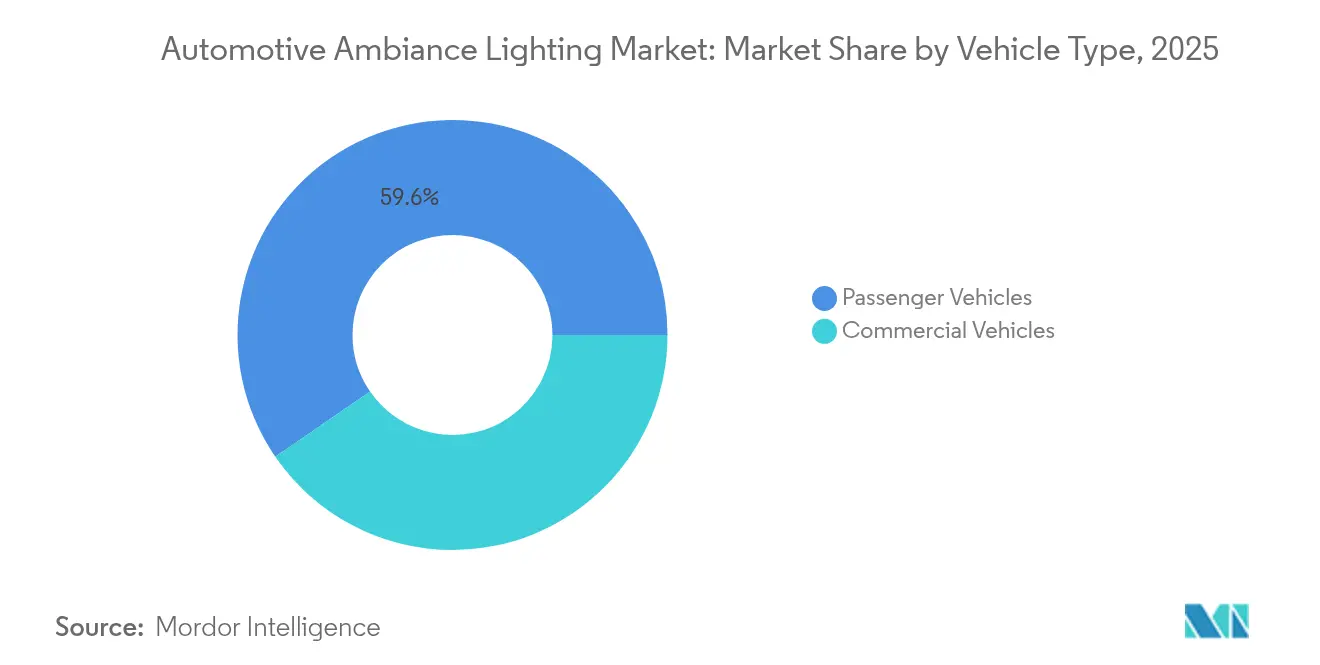

- By vehicle type, passenger vehicles led with 59.58% of the automotive ambiance lighting market share in 2025, and will expand at an 11.12% CAGR through 2031.

- By application, footwell lighting captured 33.45% of the automotive ambiance lighting market size in 2025, while center-console lighting accelerates at a 16.21% CAGR to 2031.

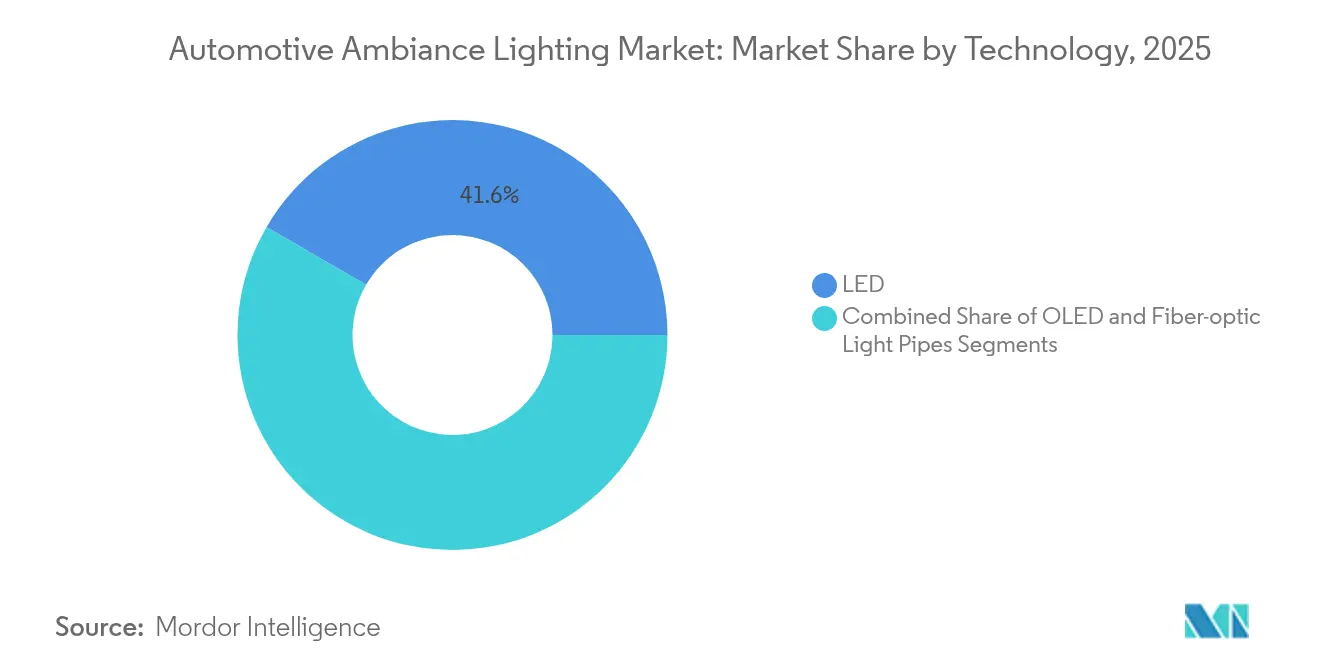

- By technology, LEDs held 41.62% revenue share in 2025; OLED solutions post the fastest 12.44% CAGR.

- By sales channel, OEM installations accounted for 78.15% of the automotive ambiance lighting market size in 2025, but the aftermarket recorded the strongest 13.62% CAGR.

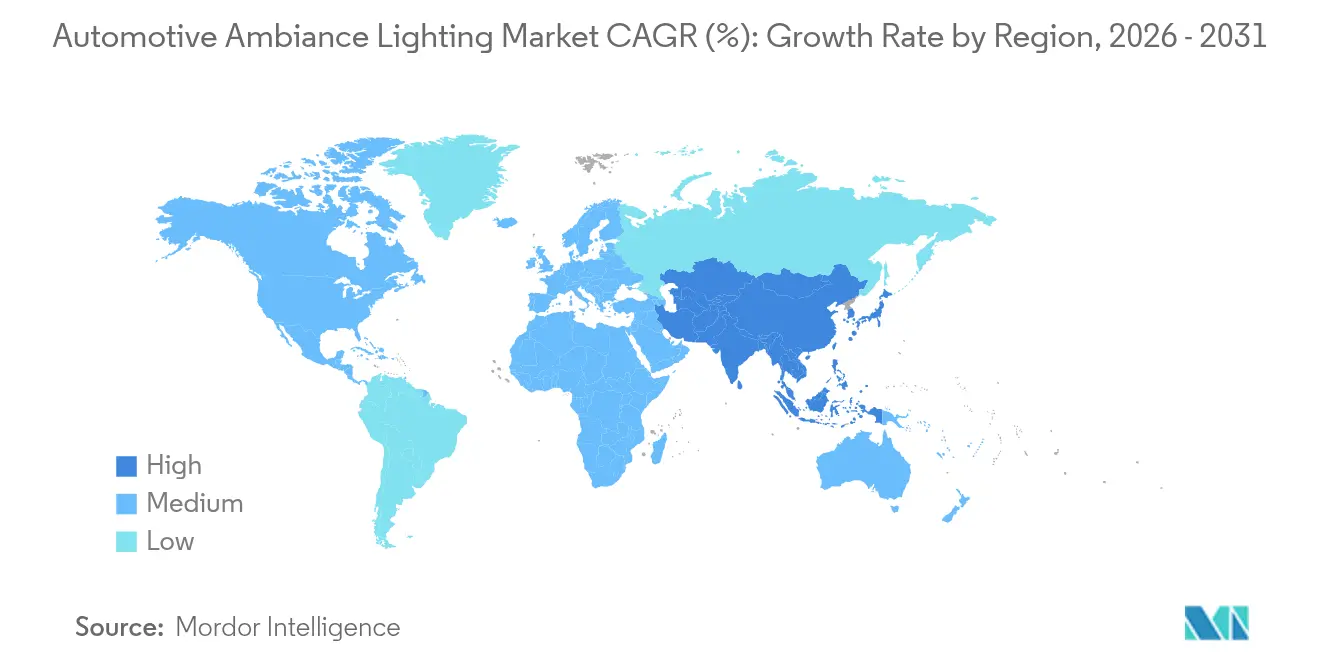

- By geography, Asia-Pacific commanded 41.83% revenue in 2025 and is growing at a 12.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Ambiance Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Demand for Luxury & Premium vehicles | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| OEM Differentiation Via in-Cabin Personalization | +2.1% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Declining LED Cost & Efficiency Gains | +1.9% | Global | Long term (≥ 4 years) |

| Ambient-Lighting-Enabled HMI & Driver-Monitor Alerts | +1.6% | North America & EU, early adoption in APAC | Medium term (2-4 years) |

| OTA-Configurable Lighting Creating Subscription Revenue | +1.2% | North America & Europe, pilot programs in China | Long term (≥ 4 years) |

| AI-driven Infotainment & Wellness Features Integration | +0.9% | Premium segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for luxury & premium vehicles

Luxury brands now embed as many as 4,096 individually addressable RGB LEDs, producing multicolor cabin scenes that helped several 2025 Wards 10 Best Interiors & UX winners secure top honors. Such systems let automakers weave unique color sequences into start-up rituals or drive modes, reinforcing brand signatures. Psychological studies show ambient lighting elevates perceived material quality and mood, bolstering premium positioning. As component costs fall, this feature is migrating into mid-tier trims, sustaining volume expansion across the automotive ambiance lighting market.

OEM differentiation via in-cabin personalization

Concepts like Yanfeng’s XiM25 smart cabin display floating light bars that change hue by user profile, route scenario, or biometric input, illustrating how lighting becomes the visual layer of personalization ecosystems. HARMAN’s Luna avatar fuses voice, AI, and ambient illumination to deliver contextual cues, making lighting part of an emotionally intelligent HMI. In shared-mobility settings, instant color shifts help riders feel the cabin is uniquely theirs, boosting satisfaction and differentiating fleet brands within the automotive ambiance lighting market.

Declining LED cost & efficiency gains

200 mm silicon-carbide platforms reduce die costs while raising efficiency, evidenced by Wolfspeed’s automotive revenue tripling during 2024-2025. Advanced 16.16 fixed-point algorithms now predict junction temperature and chromaticity with 5 °C accuracy, allowing stable color even at −40 °C to 120 °C duty cycles. These improvements enable high-pixel LED arrays in cost-sensitive models, widening the automotive ambiance lighting market addressable base.

Ambient-lighting-enabled HMI & driver-monitor alerts

Display-like LED rows serve as silent informers; a ring of light can shift from green to red as driver-monitoring cameras detect distraction, reducing cognitive load compared with warning chimes. As automated-driving features scale, lighting transitions visually confirm handover states. Biometric integration further adjusts color temperature to combat drowsiness, transforming ambient lighting into a safety system within the automotive ambiance lighting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Thermal/EMI Management Raises Design Cost | -1.8% | Global, particularly in compact vehicle segments | Short term (≤ 2 years) |

| Cyber-Security Risk in CAN-Controlled Lighting | -1.2% | North America & Europe, regulatory focus | Medium term (2-4 years) |

| Non-Uniform Global Luminance Standards | -0.9% | Global, trade barriers between regions | Long term (≥ 4 years) |

| Semiconductor Shortages Constrain LED Driver Supply | -0.7% | Global, supply chain concentration in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex thermal/EMI management raises design cost

LED junction temperatures above 85 °C can halve lifespan, forcing automakers to use aluminum heat sinks, vapor-chamber foils, and coupled heat-pipe loops. Simultaneously, high-frequency drivers must achieve CISPR 25 Class 5 EMC targets; Texas Instruments reference boards incorporate spread-spectrum clocks and multi-layer PCBs to pass stringent tests. These countermeasures lift bill-of-material costs, especially tough for entry-level trims, thereby tempering expansion of the automotive ambiance lighting market.

Cyber-security risk in CAN-controlled lighting

Ambient lighting nodes connected to the Controller Area Network can expose vehicles to spoofing or malicious firmware if encryption is weak. Secure-boot schemes based on AES-128 CMAC slow down initialization and add flash memory overhead, but regulators in North America and Europe increasingly treat them as mandatory. Over-the-air updates heighten attack surfaces, compelling OEMs and aftermarket kit makers to invest in penetration testing and compliance audits, which can lengthen development cycles and raise entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Vehicles Drive Market Expansion

Passenger cars commanded 59.58% of the automotive ambiance lighting market share in 2025, and their 11.12% CAGR outpaces the overall automotive ambiance lighting market through 2031. Electric sedans and crossovers routinely position multizone RGB lighting as a value-added justification for higher sticker prices, and premium brands market mood-responsive color scripts as core to the digital cockpit identity. In addition, EV drivetrain silence heightens occupants’ sensory focus on visual cues, making lighting more salient in brand storytelling across the automotive ambiance lighting market.

Commercial vehicles remain smaller but attractive. Long-haul truck cabins increasingly install circadian-tuned LEDs that fade to amber at night to reduce melatonin suppression and lessen fatigue. Fleet managers link interior lighting states with telematics to encourage rest-break compliance, building a return-on-investment narrative around lower driver turnover. Adoption, however, is tempered by tight cost controls and slower replacement cycles typical of heavy-duty platforms, moderating commercial demand within the broader automotive ambiance lighting market.

By Application: Center Console Emerges as Growth Leader

Footwell lighting, though mature, retained 33.45% of the automotive ambiance lighting market size in 2025 through its proven ability to enhance perceived space and resale appeal. Door-panel and headliner use cases are evolving toward safety-linked “welcome” sequences and seat-integrated wellness cues. Overall, the application mix shows a shift from static decorative placements to functional interaction zones, sustaining differentiation within the automotive ambiance lighting industry.

Center-console systems post a 16.21% CAGR, the fastest within the automotive ambiance lighting market, as screens morph into tactile surfaces, integrating self-illuminated feedback keys. MicroLED tiles embedded under thin plastic create flat panels that rise into mechanical buttons on demand, and perimeter lamps alter hue in sync with HVAC or drive mode selections. Such dynamic effects convert the console from passive storage to active user-interface real estate, explaining outsized growth.

By Technology: LED Dominance Faces OLED Challenge

LED arrays delivered 41.62% revenue share in 2025 and remain the cost king. Efforts such as Marelli’s h-Digi microLED headlamp demonstrate pixel densities allowing animated turn signals that double as branding signatures. Continuous efficiency gains keep LEDs the default for volume models, anchoring the mass side of the automotive ambiance lighting market.

OLED solutions clock a 12.44% CAGR and appeal to premium interiors where ultra-thin, bendable panels wrap curved trim. BMW’s 2025 concept doors hide see-through OLED blades that glow only when occupants approach, delivering “surprise-and-delight” theatrics. Yet higher cost per lumen, temperature sensitivity, and shorter life slow mainstream use, confining OLED to premium subsets of the automotive ambiance lighting industry.

By Sales Channel: Aftermarket Acceleration Signals Retrofit Demand

OEM fitment represented 78.15% of the automotive ambiance lighting market size in 2025, thanks to system integration advantages. Factory modules talk natively to gateway ECUs, enabling predictive pre-conditioning and OTA feature unlocks tied to subscription plans. Still, the aftermarket’s 13.62% CAGR highlights pent-up demand across the installed vehicle parc.

Do-it-yourself LED kits with smartphone apps replicate multicolor effects for under USD 120, and plug-and-play CAN bridges now emulate factory lighting signals without voiding warranties. As component costs compress, retrofit suppliers may steal incremental share within the automotive ambiance lighting market, especially in regions where average vehicle age exceeds 10 years.

Geography Analysis

Asia-Pacific held 41.83% of global revenue in 2025 and is forecast to expand at 12.97% CAGR, making it the largest and fastest-growing regional slice of the automotive ambient lighting market. China’s domestic OEMs embrace Generation Z aesthetics that pair neon-like strips with AI avatars, as seen in Yanfeng’s XiM25 concept, and accelerated EV output scales volume for local lighting suppliers. Domestic champions such as Xingyu and Shanghai Koito have ramped up smart-lighting lines, narrowing technology gaps with global peers and pushing export ambitions.

North America follows anchored by luxury SUVs and pickup trucks that bundle ambient lighting with ADAS suites. UNECE-aligned cybersecurity frameworks and Federal Motor Vehicle Safety Standards emphasize EMI robustness, inflating engineering effort but ensuring system reliability.

Europe records a moderate growth rate as stringent Regulation No. 48 and eco-design norms shape system specifications. German and French OEMs prioritize seamless light-guide integration and low-emission materials, with FORVIA-HELLA leveraging combined optics and electronics know-how to win platform awards. Partnerships such as ams OSRAM–Valeo develop full interior ecosystems linking instrument-panel surfaces, door trims and seatbacks, underscoring Europe’s role in premium innovation for the automotive ambient lighting market.

Competitive Landscape

The automotive ambiance lighting market exhibits moderate fragmentation. This reflects the technical complexity and capital requirements that favor established suppliers with comprehensive automotive experience. The competitive intensity has increased following strategic consolidations. Market leaders leverage integrated approaches that combine lighting hardware, control systems, and software capabilities, creating barriers for pure-play component suppliers.

Technology remains the primary competitive arena. Marelli’s h-Digi microLED matrix headlamp offers 40-µm pixels and merges lidar in one housing, signaling convergence between exterior projection and interior ambience. Patent filings on integrated light-display panels that sense hand gestures underscore a rush to secure intellectual property around multifunctional cabin surfaces. Cost-effective disruptors from China and India court regional mass-market contracts with vertically integrated LED back-ends and flexible printed-circuit assemblies.

Automotive Ambiance Lighting Industry Leaders

Valeo S.A.

ams OSRAM

Grupo Antolin

Koito Manufacturing Co., Ltd.

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AUO showcased its Smart Cockpit 2025 at CES, integrating the world’s first transparent Micro LED roof panel that morphs from skylight to ambient glow, hinting at display-lighting convergence.

- December 2024: ams OSRAM and Valeo launched a cooperation to transform vehicle interiors into dynamic environments using synchronized lighting ecosystems.

- October 2024: Yanfeng released the XiM25 smart cabin for Generation Z, featuring floating LED films that adapt color to passengers’ social-media profiles.

- October 2024: Yanfeng and Loomia formed a partnership to embed e-textile circuits into seat upholstery, advancing seamless ambient lighting and haptic feedback.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive ambiance lighting market as every factory-installed or retrofitted interior illumination module, primarily LED and emerging OLED packages, designed to bathe dashboards, doors, consoles, footwells, and headliners in customizable colors that enhance brand identity, safety cues, and occupant comfort.

Scope Exclusions: Exterior headlamps, taillights, instrument-cluster back-lighting, and non-passenger-vehicle installations sit outside this scope.

Segmentation Overview

- By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- By Application

- Dashboard

- Center Console

- Doors

- Footwell

- Others

- By Technology

- LED

- OLED

- Fiber-optic Light Pipes

- By Sales Channel

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cabin-lighting engineers at global OEMs, LED package vendors, and regional aftermarket installers across Asia-Pacific, Europe, and North America. Their insights validated penetration swings between trim lines, ASP dispersion across channels, and the march toward dynamic RGB features.

Desk Research

We pulled multi-year light-vehicle output and luxury-trim ratios from sources such as the International Organization of Motor Vehicle Manufacturers, ACEA, and NHTSA to anchor the potential install base. Customs data from Volza and Asia Metal flagged LED package trade flows, while Questel patent counts signaled OLED commercialization timing. Company filings, investor decks, and press releases of leading Tier-1 lighting suppliers refined average selling prices, which we benchmarked against news captured through Dow Jones Factiva. These public and paid inputs give us a broad yet current baseline; many additional references informed the process.

Market-Sizing & Forecasting

A top-down build links 2024 global light-vehicle production to factory-fit penetration, then layers aftermarket retrofits. Selective supplier roll-ups check the totals. Key variables include premium-car share, LED cost per lumen, EV production, regional luxury sales, and average lighting points per vehicle. We forecast through multivariate regression, with ARIMA smoothing for near-term volatility. Bottom-up gaps in retrofit volumes are bridged using installer panel inputs before final sign-off.

Data Validation & Update Cycle

Outputs pass variance checks against customs codes and peer models, followed by senior analyst review. The dataset refreshes yearly, with interim updates triggered by regulation, major M&A, or step-change technology costs to keep clients current.

Why Mordor's Automotive Ambiance Lighting Baseline Commands Reliability

Published estimates differ because firms mix product types, vehicle classes, geographies, and refresh cadences. Gaps widen whenever aftermarket volumes or OLED premiums are ignored.

Key gap drivers include narrow "interior-only" scopes, bundling of dome or dashboard lamps, static ASP inflation, and currency-conversion cut-offs. Mordor updates penetration and ASP annually, captures global retrofits, and rolls currencies at twelve-month averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.34 B (2025) | Mordor Intelligence | - |

| USD 1.78 B (2024) | Regional Consultancy A | excludes aftermarket and commercial vehicles; static ASPs |

| USD 1.70 B (2024) | Trade Journal B | limited geography sample; older production baseline |

| USD 4.60 B (2025) | Global Consultancy C | bundles dome and dashboard lamps, inflating scope |

External point estimates therefore stretch from USD 1.70 billion to USD 4.60 billion for 2024-2025, underscoring how scope choices shift baselines. Our balanced top-down model, selectively checked bottom-up, delivers a transparent, repeatable mid-case that decision-makers can trust.

Key Questions Answered in the Report

What is the size of the automotive ambiance lighting market today and what is its 2031 outlook?

The market stands at USD 4.79 billion in 2026 and is projected to climb to USD 7.84 billion by 2031, supported by a 10.34% CAGR over 2026-2031.

Which region currently leads demand and how quickly is it expanding?

Asia-Pacific holds 41.83% of global revenue in 2025 and is advancing at a 12.97% CAGR through 2031.

Which application area is growing the fastest?

Center-console lighting shows the highest momentum with a 16.21% CAGR, reflecting its integration with interactive infotainment surfaces.

How fast is the aftermarket segment expanding?

Aftermarket retrofit kits are posting a 13.62% CAGR, outpacing OEM fitment on the strength of consumer upgrades to existing vehicles.

Why is LED cost decline such an important growth driver?

Ongoing efficiency gains and larger silicon-carbide wafers keep slashing LED prices, enabling multizone lighting even in mid-market vehicles and broadening adoption.

What are the main technical hurdles that could slow growth?

Complex thermal and EMI management requirements raise design costs, while cybersecurity risks in CAN-controlled lighting demand extra safeguards that can lengthen development cycles.

Page last updated on: