Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 27.67 Billion |

| Market Size (2031) | USD 36.56 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Adaptive Lighting System Market Analysis by Mordor Intelligence

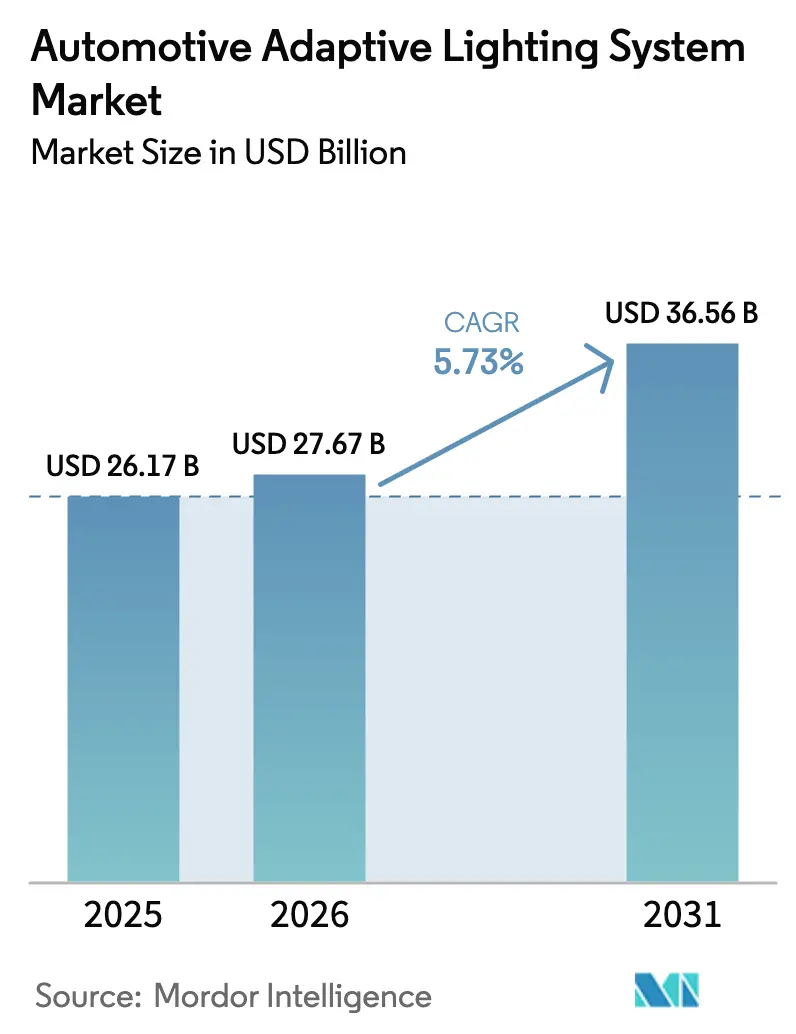

The automotive adaptive lighting market size is expected to increase from USD 26.17 billion in 2025 to USD 27.67 billion in 2026 and reach USD 36.56 billion by 2031, growing at a CAGR of 5.73% over 2026-2031. Near-synchronous regulatory changes in Europe and North America are erasing the split‐engineering costs that once slowed the rollout of advanced beams, enabling global platforms to scale faster[1]"National Highway Traffic Safety Administration", Adaptive Driving Beam Headlamps Final Rule, NHTSA, nhtsa.gov. Automakers are pairing high-resolution headlamps with over-the-air functionality so that feature upgrades can be sold long after the initial vehicle purchase, supporting new recurring-revenue streams. Suppliers are racing to localize production of LED, laser, and micro-LED modules in Mexico, Poland, Türkiye, and Thailand to blunt currency risk and shipping delays. Software-defined lighting is moving from luxury branding to mainstream safety, with embedded sensors and AI algorithms constantly adjusting beam shape in real time based on traffic, terrain, and weather.

Key Report Takeaways

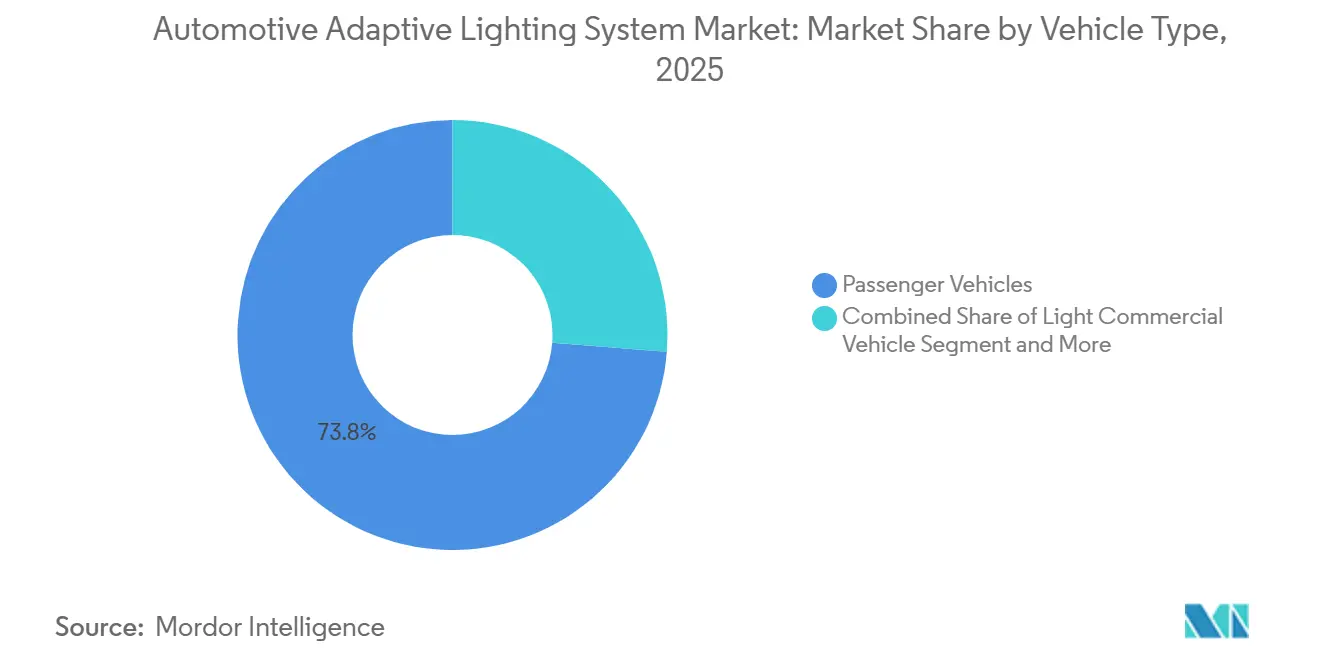

- By vehicle type, passenger vehicles commanded 73.76% of the automotive adaptive lighting market share in 2025, while medium and heavy commercial vehicles are projected to expand at a 9.62% CAGR through 2031.

- By application, exterior lighting accounted for 93.22% of the automotive adaptive lighting market in 2025, and interior adaptive lighting is forecast to grow at an 8.27% CAGR through 2031.

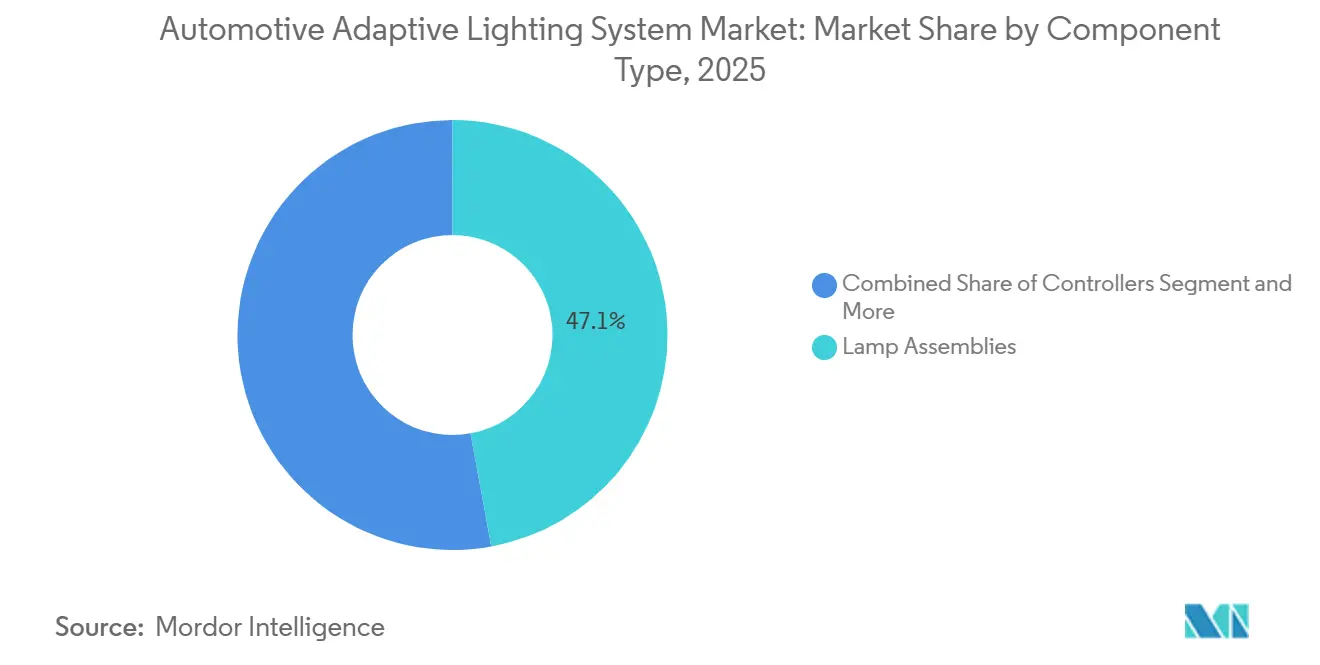

- By component, lamp assemblies accounted for 47.12% of the automotive adaptive lighting market size in 2025, whereas sensors and cameras are advancing at a 10.89% CAGR over 2026-2031.

- By technology, LEDs secured 65.56% of the automotive adaptive lighting market share in 2025, yet laser lighting is projected to rise at a 14.55% CAGR through 2031.

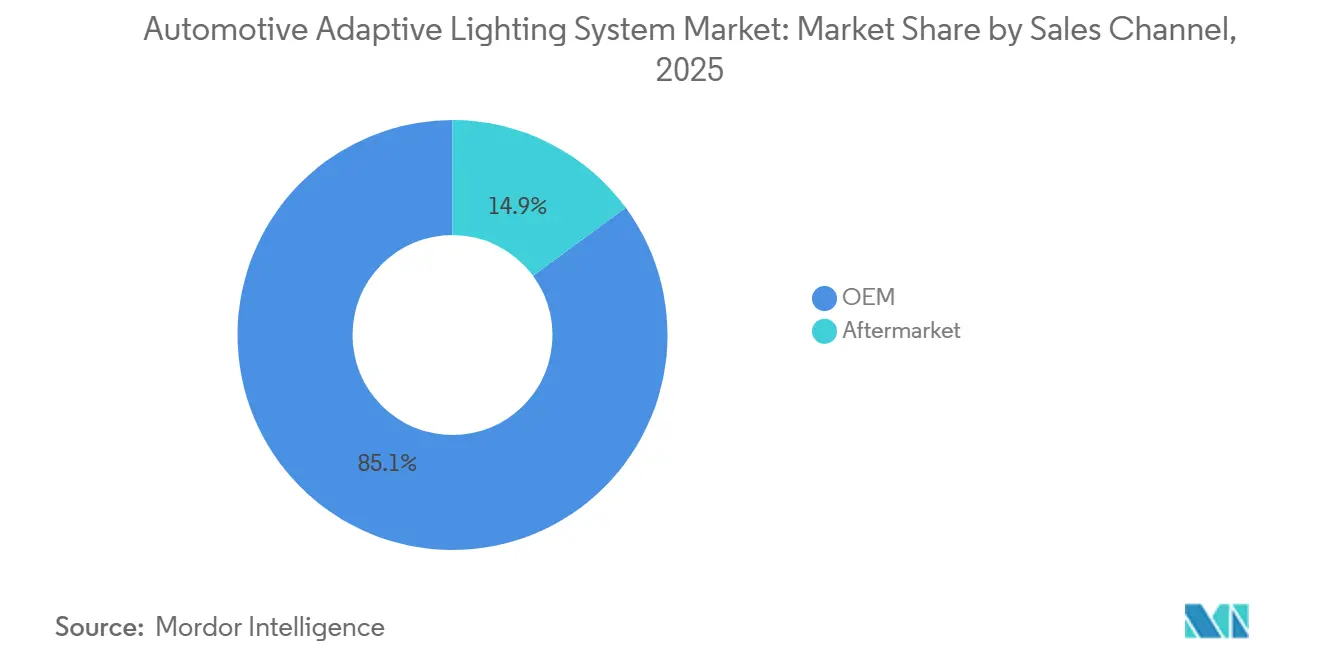

- By sales channel, the OEM channel accounted for 85.10% of the automotive adaptive lighting market in 2025, and the aftermarket is poised to grow at a 7.87% CAGR through 2031.

- By functionality, automatic high beam held 39.95% of the automotive adaptive lighting market share in 2025, whereas adaptive front lighting is set to expand at an 11.77% CAGR through 2031.

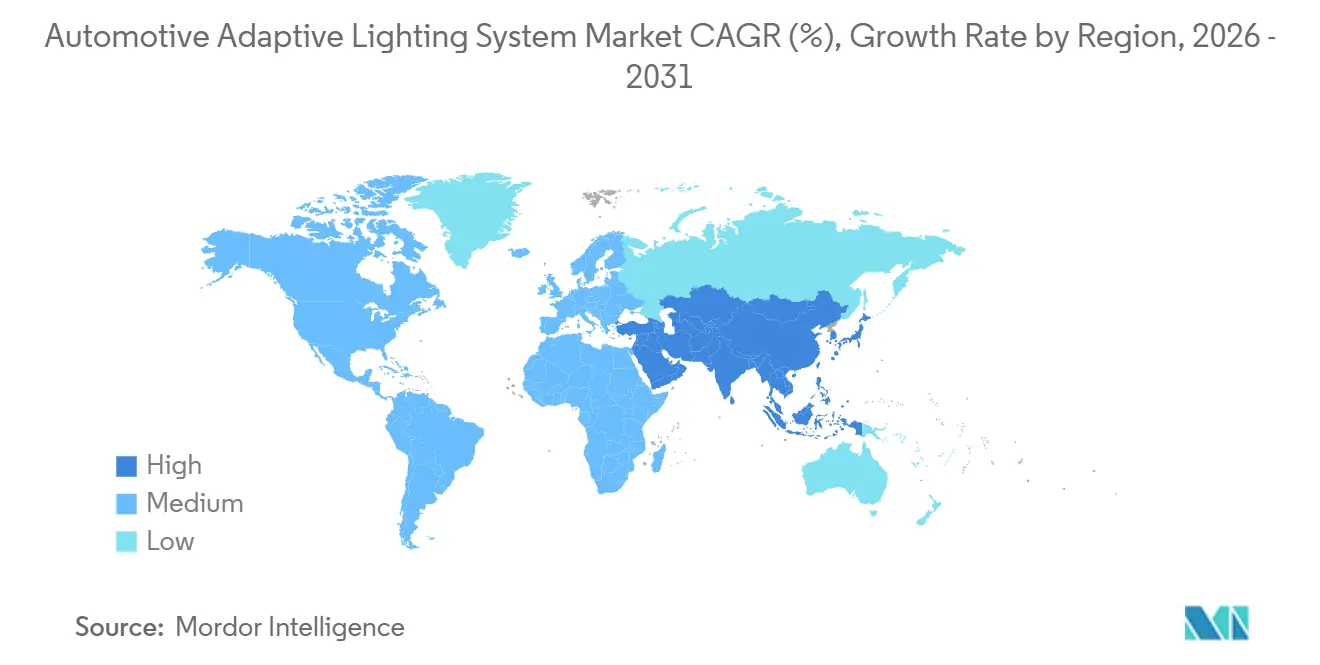

- By geography, Asia-Pacific commanded 45.55% share in 2025 and is projected to post the fastest CAGR of 8.91% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Adaptive Lighting System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Lighting Regulations | +1.4% | Global, with peak impact in North America and Europe | Medium term (2-4 years) |

| Advanced Safety Systems and ADAS | +1.3% | Global, led by Asia Pacific and Europe | Long term (≥ 4 years) |

| Rising Feature-Take Rates | +1.1% | Global, concentrated in China, North America, Middle East | Medium term (2-4 years) |

| LED Cost Reduction | +0.8% | Global, with accelerated adoption in Asia Pacific | Short term (≤ 2 years) |

| Post-Sale Beam-Pattern Upgrades | +0.5% | North America, Europe, China (premium segments) | Long term (≥ 4 years) |

| V2X-Triggered Pedestrian-Communication Lighting | +0.3% | Europe, China (pilot cities), limited North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Lighting Regulations (ADB, ECE R123)

The United States legalized adaptive driving beams in 2022, aligning with Europe’s ECE R123 and ending decades of suppression of the feature. This convergence lets automakers certify one hardware stack for multiple regions while fine-tuning beam patterns in software to satisfy each local photometric clause. China’s GB 4599-2024 and companion rules came into force in 2025 with explicit approval for road-projection symbols, opening the door for lane guidance and pedestrian alerts. India validated a home-grown adaptive front lighting design that mirrors European optics, signaling an intent to mandate the feature on trucks by 2027[2]"Adaptive Front Lighting System (AFLS)", ARAI, araiindia.com. Together, these moves increase the addressable volume for suppliers, spur economies of scale, and accelerate investments in pixelated LEDs and laser-on-chip arrays.

Growing Demand for Advanced Safety Systems and ADAS

Automotive lighting now serves as an outward-facing sensor, not just illumination. Mercedes-Benz embedded adaptive beams into Active Brake Assist so the lamps actively highlight vulnerable road users when radar or camera flags a threat. Bosch pairs its Gen3 multi-purpose camera with headlamps on heavy trucks to shrink nighttime crash rates, a big win for fleet insurers. As OEMs deeply couple lighting with braking, steering, and perception ECUs, buyers are effectively locked into the tier-1 supplier that owns the entire stack. That establishment, and the prospect of subscription-based light upgrades delivered over-the-air, make adaptive lighting a priority line item on future product plans.

Rising Premium and SUV Sales Lifting Feature-Take Rates

SUVs and premium sedans show adaptive-lighting fitment rates up to four times those of compact cars, because buyers willingly pay extra for technology-laden cabins. In China, adaptive driving beam configuration rate exceeded 50% among vehicles priced above CNY 500,000 (~USD 72,602.15) during early 2025[3]"How much do you know about car lights: Adaptive high beam ADB is the current mainstream smart headlight solution", EEWORLD.com.cn, Inc., en.eeworld.com.cn. Audi has already pushed micro-LED matrix lights from flagships down to the Q3, illustrating a clear trickle-down playbook. Certified-pre-owned data also shows higher resale speed and value for cars equipped with adaptive ambient lighting, reinforcing customer willingness to pay.

Rapid LED Cost Reduction and Performance Gains

Continuous gains in chip efficiency and the mass production of micro-LED wafers have reduced component costs enough that mainstream crossovers can adopt adaptive arrays with little margin erosion. Samsung’s PixCell micro-LED package debuted at scale in 2025 EV launches, beating halogen on output while consuming less power. Patented thermal barriers stabilize junction temperature, allowing designers to throttle current for bright beams without bulky heat sinks. Research published in 2025 confirmed that optimized fin geometry can cut junction temperatures by more than 6 °C, directly extending LED lifetime.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Adaptive Modules | -0.8% | Global, most acute in price-sensitive Asia Pacific and South America | Short term (≤ 2 years) |

| Thermal Management Limits | -0.5% | Global, particularly compact-class vehicles in hot climates | Medium term (2-4 years) |

| ECU Cybersecurity Risks | -0.2% | Global, regulatory scrutiny rising in Europe and China | Long term (≥ 4 years) |

| GaN Substrate Supply Bottlenecks | -0.2% | Global, concentrated in premium segments using laser lighting | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Adaptive Modules vs. Fixed Lamps

Adaptive headlamps still cost 2-4 times as much as fixed LEDs, so OEMs usually bundle them with premium trim lines or paid software unlocks. On the 2026 BMW 3 Series, an adaptive ambient option adds nearly EUR 1,850 (~USD 2,135.15) to the sticker, limiting uptake in cost-sensitive markets. Dealership retrofits are scarce because extra harnesses void electrical warranties, cutting off a quick aftermarket path. Some suppliers now offer tiered packages that separate the expensive MEMS mirrors from basic auto-high-beam logic so that entry cars can at least comply with emerging regulations without big price jumps.

Thermal Management Limits in High-Lumen LED/Laser Units

Laser and high-power micro-LED arrays dump more than 50 W cm-2 into slim headlamp housings. BMW concluded in 2024 that the cooling gear required for standalone laser lighting added weight and cost, prompting a pivot to matrix LEDs with broader spread patterns. Peer-reviewed tests in 2025 showed that 20% of the laser input power was lost as heat, reinforcing the need for better substrates and phase-change materials. These thermal ceilings slow adoption in compact cars, which are governed by strict pedestrian-impact styling rules that demand wafer-thin lamp profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Adaptive Uptake

Passenger vehicles retained the largest 73.76% share of the automotive adaptive lighting market in 2025, helped by steady model-year refreshes that make matrix and pixel LEDs standard on mid-trim crossovers. Carmakers bundle the lamps with infotainment upgrades so buyers view them as part of a single comfort-and-safety package rather than a costly stand-alone option. Styling freedom in SUVs also gives designers more space for heatsinks and sensors, which further encourages rapid rollout. As volume rises, tier-1 suppliers gain scale economies that lower per-module costs and improve reliability through shared electronics platforms.

Medium and heavy commercial vehicles are expected to post the fastest 9.62% CAGR through 2031, driven by regulations that pair adaptive beams with collision-mitigation braking on long-haul rigs. Fleet operators accept the added expense because better nighttime visibility cuts accident downtime and insurance premiums. Lamp makers now offer modular housings that slide into existing apertures, letting trucks upgrade during scheduled maintenance without repainting surrounding panels. The resulting retrofit path accelerates adoption and provides suppliers with a second revenue cycle once factory warranties expire.

By Application: Exterior Dominance Masks Interior Surge

Exterior systems held a commanding 93.22% share in 2025, reflecting global laws that require glare-free beams and daytime running lamps on every new vehicle. Automakers migrate to single global lamp architectures that can be recalibrated in software, limiting tooling changes across regions. That strategy shortens development cycles and lets design teams focus on signature graphics that reinforce brand identity. Suppliers, in turn, compete on thermal management and optical efficiency rather than on basic compliance.

Interior adaptive lighting is rising fastest at an 8.27% CAGR, largely because electric and autonomous models use color and intensity shifts to substitute for engine sound as feedback to occupants. Cabin-centric systems integrate with voice assistants and biometric sensors so light scenes match the driver's mood or route conditions. Software updates can add new themes just like smartphone wallpapers, giving OEMs an ongoing revenue stream. As screens proliferate inside vehicles, ambient LEDs also cut eye strain by balancing overall luminance.

By Component: Sensors Outpace Lamps

Lamp assemblies accounted for the largest 47.12% of 2025 spend, as they remain the visual and regulatory focal point of every lighting package. Most automakers still specify bespoke housings to underline brand DNA, so tooling stays a high-margin niche for tier-1 vendors. Vertical integration into optics, coatings, and seals helps suppliers keep durability in harsh environments while protecting intellectual property. Continued consolidation around global platforms now allows one base design to serve multiple nameplates with only bezel or reflector tweaks.

Sensors and cameras are set to record the fastest 10.89% CAGR as adaptive lighting shifts from reactive to predictive beam shaping. Lidar and radar feeds train algorithms to widen or narrow light cones before the driver even steers, raising the value of perception hardware embedded inside or near the lamp. Module makers, therefore, buy or partner with sensor start-ups to safeguard channel control. As the share of electronics rises, supply chains move closer to semiconductor fabs rather than to legacy plastics hubs.

By Technology: LEDs Dominate, Lasers Climb

LED technology accounted for 65.56% of installations in 2025 because it balances cost, efficiency, and design flexibility across all vehicle classes. Continuous improvements in chip efficiency let engineers shrink housings without sacrificing output, supporting sleeker front-end styling. Pixel counts keep rising, so software can mask oncoming traffic while retaining full high-beam reach elsewhere. That functionality is now a prerequisite for top safety ratings in multiple regions.

Laser lighting is set for the fastest 14.55% CAGR, concentrated in ultra-luxury badges where extended range still resonates with buyers. Suppliers increasingly pair a small central laser booster with a wide LED matrix for close-field coverage, smoothing the handoff between the two sources. Hybrid setups mitigate past thermal worries and comply with stricter glare caps under ECE R123. A steady trickle of patents on gallium nitride substrates hints at lower future costs that could broaden the addressable market beyond flagships.

By Sales Channel: Aftermarket Gains on Aging Fleets

OEM lines accounted for 85.10% of 2025 revenue because factory-installed lights integrate deeply with body control modules, steering sensors, and camera calibration. Even so, the aftermarket is set to grow at a 7.87% CAGR as vehicle age in India, Brazil, and Türkiye pushes owners toward safer, brighter replacements. New plants in Pune and São Paulo now stamp headlamps that slide into legacy housings yet carry CAN-FD-ready controllers, easing do-it-yourself installation.

For automakers, bundling adaptive lights with advanced driver-assistance suites remains a profitable upsell. BMW’s multi-tiered packages prove that consumers are willing to pay for style and safety combined. Yet warranty constraints mean many aftermarket kits stop at plug-and-play LED bulbs, leaving full matrix functions to authorized service centers, a dynamic likely to persist until open standards simplify ECU re-flashing.

By Functionality: Adaptive Front Lighting Leads Innovation

Automatic high beam ruled with 39.95% penetration in 2025 because a single camera and basic software meet regulations in most countries. Adaptive front lighting, however, is clocking an 11.77% CAGR as lane-linked and GPS-linked beam shaping becomes the norm. Pixel counts beyond 20,000 are now common, letting lamps carve out glare-free pockets for oncoming cars while pumping full brightness into empty road zones.

Cornering and dynamic-bending modules still serve useful roles at lower price points, but their mechanical parts add weight. Software-only solutions that read steering angle and radar data can achieve similar results in microseconds. Regulatory acceptance of projected warning symbols in Europe and China will accelerate the shift from mere illumination to active communication, embedding the lamps more deeply into the V2X ecosystem.

Geography Analysis

Asia-Pacific captured 45.55% of the automotive adaptive lighting market revenue in 2025 and is growing at an 8.91% CAGR through 2031, driven by China’s rapidly evolving rules that allow road-projection features. Domestic brands deploy adaptive beams as a status symbol in electric models competing head-to-head with German luxury imports. Japanese suppliers such as Koito and Stanley are expanding factories across ASEAN and Latin America to hedge against currency shifts while staying close to global vehicle platforms. India is shaping up as the next inflection market; an indigenous lighting standard mirroring Europe’s optics clears the path for a mandate covering trucks from 2027 onward.

Europe maintains technology leadership and will advance at a measured 4.49% CAGR to 2031. ECE R123 sets a high bar for glare-free performance, nudging all new platforms toward matrix LEDs or lasers. German premium OEMs continue to trickle down high-resolution lamps into sub-EUR 40,000 (~USD 46,178.20) models, forcing volume brands to adopt similar tech or risk market share erosion. Production costs are being squeezed as suppliers shift assembly to Poland, Hungary, and Morocco, where wages are lower, but logistics still favor on-time delivery to EU plants.

North America is finally unlocking pent-up demand now that the NHTSA green-lit adaptive beams. Growth of 4.78% CAGR through 2031 may seem modest, yet the base is small after decades of prohibition. Over-the-air activations on existing vehicles, led by Tesla, prove that a latent install base already waits in the driveway. Suppliers are localizing micro-LED lines in Mexico to capitalize on the United States-Mexico-Canada Agreement’s rules-of-origin credits, all while trimming shipping lead times. South America and the Middle East follow in tandem; revenue lifts come from SUV-heavy lineups where buyers accept feature premiums, but the lack of stringent lighting rules still limits full matrix rollouts.

Competitive Landscape

Koito, Valeo, Hella, Stanley Electric, and Marelli headline a moderately concentrated field where the top tier secures long-term programs by combining lamps with sensors and software. Koito’s acquisition of lidar specialist Cepton illustrates the trend: by owning perception hardware, the company can offer a single warranty covering both light and object detection. Valeo countered by partnering with laser-projection expert Appotronics to turn headlamps into communication surfaces that can project warnings onto asphalt. Hella, now under Forvia, is relocating selected assembly lines to Eastern Europe, reducing cost pressure while keeping engineering in Germany to maintain premium relationships.

Stanley Electric deepened its portfolio through the purchase of Iwasaki Electric, gaining phosphor and ultraviolet know-how that supports new cabin-sanitization lamps. Marelli, fresh from refinancing, showcased an OLED-TFT rear module that blends stop, turn, and welcome animations in one paper-thin panel, appealing to designers who want seamless bodywork. Chinese challengers, such as ams OSRAM’s local joint ventures, pitch micro-LED boards at aggressive prices, leveraging government incentives and vast domestic demand to undercut incumbents in bidding rounds. To defend share, legacy suppliers highlight decades of field data and global homologation expertise, assuring automakers of smooth certification across regions. The result is brisk innovation but also heightened collaboration, as OEMs push for shared development costs on optics, heat sinks, and cybersecurity.

A new competitive front is software. Over-the-air licensing lets car brands sell dynamic beam patterns or holiday-themed light shows long after purchase, and whoever controls the firmware platform gains recurring margin. Suppliers embed secure bootloaders and encryption keys inside lamp controllers, making it hard to swap modules without authorized software. Regulators now audit these systems for cyber-resilience, so established players lean on their track record to pass compliance gates quickly. Smaller entrants must meet the same bar, stretching engineering budgets and encouraging alliances with chipset vendors that already possess hardened security libraries.

Automotive Adaptive Lighting System Industry Leaders

-

Stanley Electric Co. Ltd.

-

Koito Manufacturing Co., Ltd.

-

Valeo SA

-

Hella GmbH & Co. KGaA

-

Marelli Automotive Lighting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Opel debuted Intelli-Lux HD on the new Astra range, packing over 50,000 pixels per headlamp for glare-free high beam that self-adapts in milliseconds.

- April 2025: Valeo teamed with Appotronics to commercialize laser video-projection front lights that merge entertainment and safety overlays.

- April 2025: Marelli revealed the first OLED-TFT pixel rear lamp and a near-field ground-projection module at Auto Shanghai, pushing design boundaries for brand signatures.

Global Automotive Adaptive Lighting System Market Report Scope

The automotive lighting market is analyzed across vehicle type, application, component type, technology, sales channel, functionality, and geography. By vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, and medium and heavy commercial vehicles. By application, the market is segmented into exterior lighting and interior lighting. By component type, the market is segmented into controllers, sensors/cameras, lamp assemblies, actuators, and others. By technology, the market is segmented into LED, Xenon / HID, halogen, and laser lighting. By sales channel, the market is segmented into OEM and aftermarket. By functionality, the market is segmented into automatic high beam, dynamic bending lights, cornering lights, and adaptive front lighting. By geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Turkey, and Rest of Middle East and Africa).

Market forecasts are provided in terms of value (USD) and volume (Units).

By Vehicle Type

| Passenger Vehicles |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (MHCV) |

By Application

| Exterior Lighting |

| Interior Lighting |

By Component Type

| Controllers |

| Sensors / Cameras |

| Lamp Assemblies |

| Actuators |

| Others |

By Technology

| LED |

| Xenon / HID |

| Halogen |

| Laser Lighting |

By Sales Channel

| OEM |

| Aftermarket |

By Functionality

| Automatic High Beam |

| Dynamic Bending Light |

| Cornering Lights |

| Adaptive Front Lighting |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles (LCV) | ||

| Medium and Heavy Commercial Vehicles (MHCV) | ||

| By Application | Exterior Lighting | |

| Interior Lighting | ||

| By Component Type | Controllers | |

| Sensors / Cameras | ||

| Lamp Assemblies | ||

| Actuators | ||

| Others | ||

| By Technology | LED | |

| Xenon / HID | ||

| Halogen | ||

| Laser Lighting | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Functionality | Automatic High Beam | |

| Dynamic Bending Light | ||

| Cornering Lights | ||

| Adaptive Front Lighting | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global spending on adaptive headlights be by 2031?

The automotive adaptive lighting market size is projected to reach about USD 36.56 billion by 2031.

Which vehicle class is adopting the technology fastest?

Medium and heavy commercial trucks lead with a forecasted 9.62% CAGR as safety mandates tighten.

Why are micro-LED headlamps replacing lasers?

Micro-LED arrays spread heat across a larger surface, meet glare-free rules, and deliver finer resolution without heavy cooling hardware.

What keeps aftermarket growth below OEM levels?

Deep integration of lamps with body control modules makes warranty-safe retrofits difficult, limiting the aftermarket to simpler bulb swaps.

Which region currently dominates sales?

Asia-Pacific holds the largest share, driven by China’s early regulatory approval of road-projection functions and high new-energy-vehicle penetration.

Page last updated on: