Automotive Fog Lights Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 1.28 Billion |

| Growth Rate (2025 - 2030) | 2.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

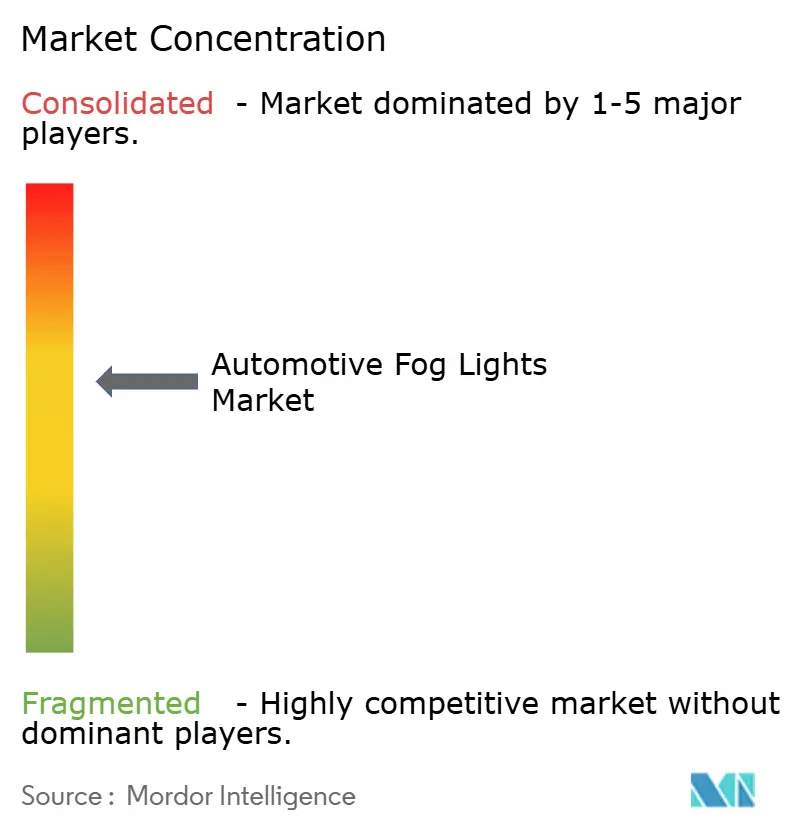

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fog Lights Market Analysis by Mordor Intelligence

The automotive fog lights market size stood at USD 1.12 billion in 2025 and is forecast to reach USD 1.28 billion by 2030, expanding at a 2.65% CAGR. Moderately paced growth mirrors the shift toward energy-efficient lighting, rising fitment mandates, and integration with advanced driver assistance systems. LED fog lamps already hold clear dominance, while adaptive beam software and sensor fusion technologies shape product differentiation. Supply-chain localization across Asia-Pacific is strengthening cost competitiveness, and software-defined lighting is turning fog lamps into upgradeable safety assets. Competitive intensity now centers on control of thermal management know-how, patent portfolios for pixelated LED arrays, and the ability to meet multi-jurisdiction compliance.

Key Report Takeaways

- By light type, LEDs captured a 51.96% share in the automotive fog light market in 2024 and are projected to grow at a 3.63% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars led with a 59.81% share in the automotive fog light market in 2024, and are expected to record the fastest CAGR of 9.24% during the forecast period (2025-2030).

- By application, front fog lights hold a 70.59% share of the automotive fog light market in 2024 and are expected to advance at a 3.82% CAGR during the forecast period (2025-2030).

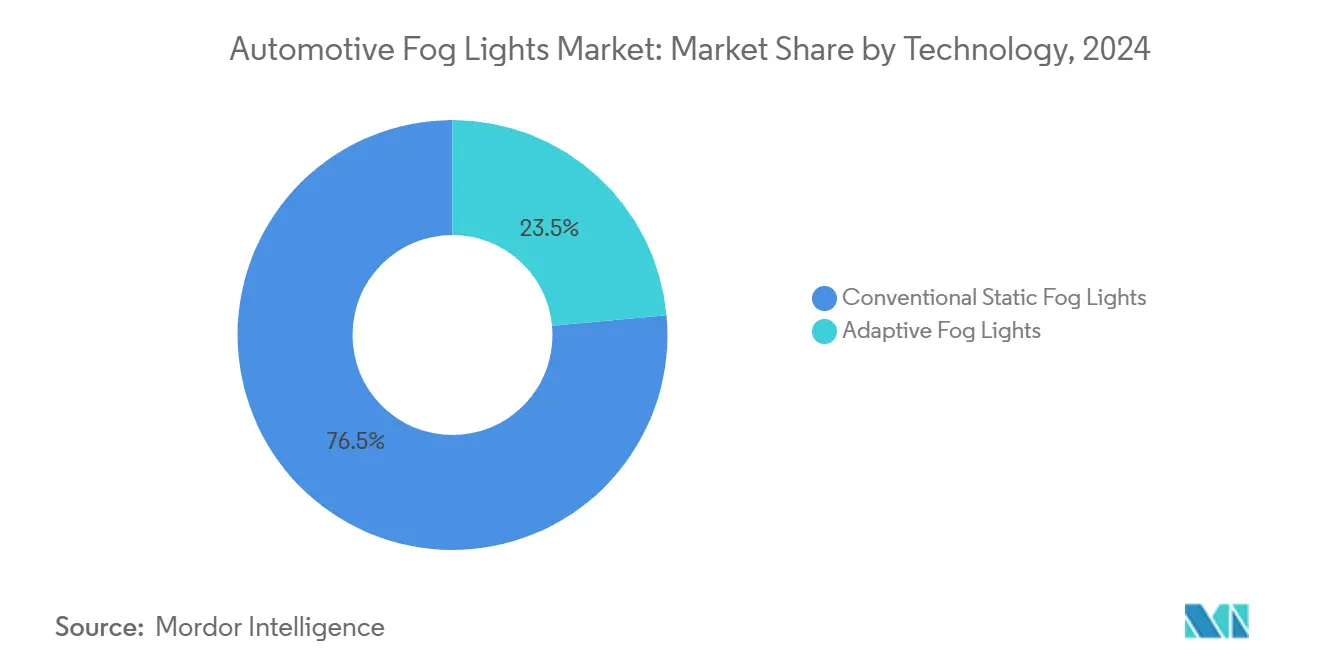

- By technology, conventional static systems retained a 76.47% share in the automotive fog light market in 2024; adaptive systems are projected to post a 3.92% CAGR during the forecast period (2025-2030).

- By distribution channel, OEMs commanded 54.91% share in the automotive fog light market in 2024, whereas the aftermarket grow at 3.06% CAGR during the forecast period (2025-2030).

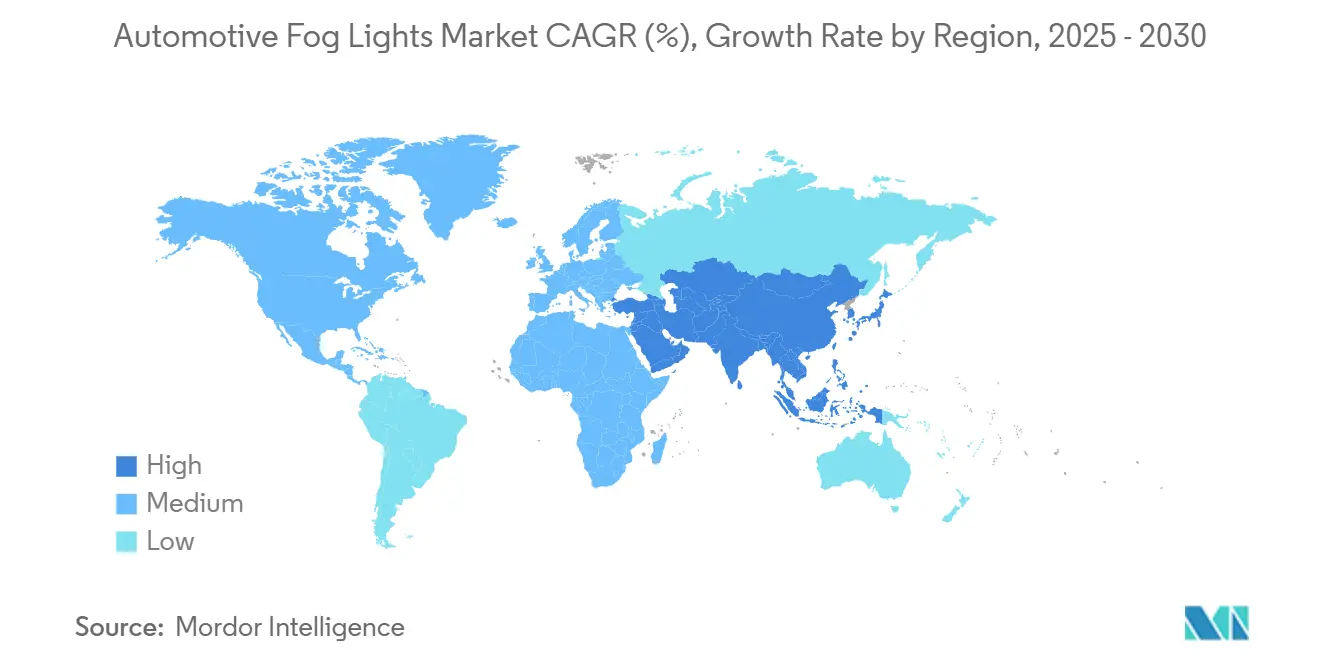

- By geography, Asia-Pacific captured a 37.25% share in the automotive fog light market in 2024 and is forecasted to be the fastest-growing region, with a 2.75% CAGR during the forecast period (2025-2030).

Global Automotive Fog Lights Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Sensor Integration | +1.1% | Global, Led By North America & Europe | Medium Term (2-4 Years) |

| Shift Toward LED Lamps | +0.9% | Global, Accelerated In Asia-Pacific | Short Term (≤ 2 Years) |

| Stringent Safety Regulations | +0.8% | Emerging Markets, India & China Focus | Medium Term (2-4 Years) |

| OTA Adaptive Beam Software | +0.7% | North America & Europe Premium Segments | Long Term (≥ 4 Years) |

| Low-Voltage Lighting Demand | +0.5% | Global Urban Centers, EU Leading | Short Term (≤ 2 Years) |

| Passenger-Vehicle Production Growth | +0.4% | Asia-Pacific, South America | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Integration of Fog Lamps with ADAS Sensor Housings

Manufacturers these days embed LiDAR, radar, and cameras inside fog lamp assemblies to create multipurpose safety units[1]“Koito Showcases LiDAR-Integrated Lighting,” MarkLines, marklines.com. Sensor fusion allows beam patterns to adjust in real time, maintaining visibility in fog, rain, and snow. Infineon’s 16 000-pixel micro-LED array, showed how the approach improves object detection at low speeds. The architecture supports styling freedom because sensors hide within existing lighting envelopes. Cost and thermal hurdles remain but tier-one suppliers expect platform adoption on 2026 model lines.

Shift Toward LED Fog Lamps for Energy-Efficiency

LED fog lamps consume about 75% less power than halogen units, extending electric-vehicle range and curbing CO₂. ams OSRAM’s 2024 NIGHT BREAKER SMART series combines intelligent thermal control with adaptive brightness. Component prices fell by around 20% in 2024 as Chinese back-end packaging lines ramped up, shrinking the premium gap. EU and California rules that phase out halogen by 2027 accelerate OEM conversion. Customizable color temperature and programmable patterns further raise demand among design-oriented brands.

Stringent Safety Regulations Mandating Front/Rear Fog Lamps

Regulators in India and China introduced new photometric and color norms that take effect in 2024-2025, lifting global demand. The NHTSA amendment to FMVSS 108 in 2022 cleared the path for adaptive driving beams in the United States[2]“NHTSA Updates FMVSS 108,” InterRegs, interregs.com. China's GB 4785 standard updates, mandate improved fog lamp photometric performance and introduce color temperature restrictions that favor LED technology over traditional halogen systems. Such mandates reward suppliers with certified global platforms and create early aftermarket opportunities for compliant retrofit kits.

Over-the-Air Up-gradable Adaptive Beam Software

Software-defined lighting makes fog lamps updatable throughout the vehicle life cycle. Tesla's introduction of adaptive headlight functionality via over-the-air updates in 2024 demonstrates the potential for software-driven lighting enhancements that can be deployed to existing vehicle fleets. Valeo and ams OSRAM are developing RGB driver ecosystems compatible with open vehicle networks, enabling hazard communication through color-coded beams. Pixel LED matrices add granularity but remain costly for mass segments until 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -0.7% | Global, Most Acute In Price-Sensitive Markets | Short Term (≤ 2 Years) |

| Raw-Material Price Volatility | -0.5% | Global Manufacturing Hubs | Medium Term (2-4 Years) |

| Thermal Issues | -0.4% | Premium Vehicle Segments Globally | Long Term (≥ 4 Years) |

| Regional Color-Temperature Bans | -0.3% | Europe, Select Asian Markets | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of LED/Adaptive Fog Lights

The high cost of LED and adaptive fog lights remains a major barrier to adoption, especially in cost-sensitive markets and commercial vehicle segments. LED fog lamps are typically 3–4 times more expensive than halogen units, while adaptive systems can cost up to 10 times more due to sensor integration. Rising tariffs and labor costs in 2024 further strained manufacturers, particularly smaller players lacking scale. Specialized equipment and quality control requirements also add to production complexity. However, ongoing improvements in manufacturing efficiency are expected to bring LED fog light costs closer to halogen levels by 2027–2028.

Raw-Material Price Volatility for Lenses and Housings

Volatile prices of key materials like aluminum, polycarbonate, and rare earth elements are creating cost and supply chain challenges for fog lamp manufacturers. Aluminum prices spiked in 2024, while polycarbonate faces regulatory pressure due to environmental concerns, pushing companies toward costlier alternatives. The heavy reliance on China for rare earth elements adds geopolitical risk, potentially disrupting LED phosphor supply. Rising freight costs from Asia further compound these issues, especially for smaller manufacturers with limited inventory flexibility. As a result, the market may see increased consolidation favoring larger players with stronger supply chain resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Light Type: LED Technology Drives Market Evolution

LED fog lamps captured 51.96% share in the automotive fog light market in 2024, and are advancing at a 3.63% CAGR during the forecast period (2025-2030). Their dominance stems from more extended service life, lower power draw, and tight alignment with electric-vehicle efficiency goals. Halogen solutions still serve budget-minded drivers in the replacement market, but OEM adoption is fading as regulatory pressure favors lower energy consumption. Xenon/HID systems now occupy a shrinking niche in legacy premium trims, limited by ballast complexity and cost. Replacement cycles are lengthening, too, as many newer LEDs last the vehicle's lifetime.

Laser fog lamps, championed by BMW prototypes, produce highly focused beams yet continue to battle heat-dissipation constraints. Tier-one suppliers are patenting hybrid LED–laser modules that combine intensity with lower thermal load, laying the groundwork for next-gen adaptive arrays. Thermal breakthroughs and component cost reductions could unlock broader adoption after 2028, especially in high-performance cars. In parallel, start-ups are experimenting with graphene heat sinks to push laser packages below current size limits. If successful, lasers could redefine premium fog-lighting design in the following product cycle.

By Vehicle Type: Commercial Segments Accelerate Adoption

The passenger cars segment led with 59.81% share in the automotive fog light market in 2024 and is projected to post the highest CAGR of 9.24% during the forecast period (2025-2030), benefiting from steady LED penetration across compact and mid-size models. Durable LEDs cut maintenance intervals and downtime, an attractive proposition for delivery services that operate in harsh urban weather. Low-voltage architectures in electric vans further magnify efficiency rewards, making LED fog lamps standard in many 2025 fleet-procurement tenders. Regulatory incentives for safety upgrades raise demand by tying insurance discounts to modern lighting fitment.

In passenger cars, adaptive functions once limited to luxury lines are now cascading into volume segments as controller prices fall. Insurance studies linking modern fog lighting to lower collision rates bolster consumer willingness to pay for upgrades. Government rebate schemes for advanced safety content in China and India also funnel volume toward LED and adaptive units. Consequently, the automotive fog lights market share gap between passenger and commercial classes is expected to be addressed by 2030. E-commerce growth acts as a tailwind, keeping unit volumes brisk in both categories.

By Application: Front Fog Dominance With Adaptive Innovation

Front fog lights accounted for a 70.59% share in the automotive fog light market in 2024 and remain the primary contributor to the overall automotive fog light market size. Their central safety role during heavy rain and fog cements OEM fitment, while logging a healthy 3.82% CAGR during the forecast period (2025-2030). Rear fog lights retain importance in EU and Chinese regulations, yet growth is slower because rear lamps are single-function components. Even so, color-balanced LED rear fog modules are gaining favor for better conspicuity without glare. Premium brands have started integrating rear fog functions into continuous light bars, raising design value.

Adaptive front fog systems rely on matrix LEDs and multiple sensors to steer the beam cut-off with surgical precision. Forvia Hella’s 2024 rear wing lighting for LYNK & CO proved that adaptive concepts can spread beyond the front fascia to side and rear applications. UNECE Regulation R149 now provides a clear certification path, accelerating global rollout plans for 2026 model lines. Over-the-air firmware keeps these lamps current, allowing new beam patterns or weather modes to be downloaded post-sale. Such software-driven flexibility strengthens the long-term revenue outlook for OEMs and suppliers alike.

By Technology: Conventional Systems Face Adaptive Disruption

Conventional static fog lights still capture 76.47% share in the automotive fog light market in 2024, owing to low tooling costs and broad regulatory familiarity. Their straightforward circuitry suits budget models and some emerging-market vehicles with high price sensitivity. Nonetheless, adaptive systems turn heads by growing at a 3.92% CAGR during the forecast period (2025-2030), mirroring OEM ambitions for smarter, data-driven lighting. Drivers appreciate how matrix arrays cut glare for oncoming traffic while widening the illuminated field in bends. Insurance agencies are beginning to recognize adaptive lamps in risk scoring, which could quicken adoption.

Stanley Electric and Mitsubishi Electric Mobility’s 2025 joint venture aims to bring pixel-controlled adaptive modules below traditional cost thresholds. The automotive fog lights market size allocated to adaptive technology is projected to double its slice by 2030 as economies of scale build. Software-upgrade pathways create new aftermarket revenue, letting owners unlock premium beam patterns later. Regulators are also drafting glare-control metrics for these adaptive designs. Collectively, these shifts hint at a tipping point where static lamps will no longer dominate the value mix.

By Distribution Channel: OEM Leadership With Aftermarket Innovation

OEM channels captured 54.91% share in the automotive fog light market in 2024, because automakers bundle fog lights with cohesive styling, electrical integration, and global homologation services. In-house validation ensures lamps meet photometric standards across regions, a critical factor for worldwide platforms. Meanwhile, the aftermarket posts a solid 3.06% CAGR during the forecast period (2025-2030), as LED retrofit kits allow older vehicles to gain modern performance. Replacement demand spikes after severe weather seasons when drivers realize the benefits of better visibility. Retailers now offer vehicle-specific harnesses that simplify do-it-yourself installation, shrinking labor time.

Specialized firms supply Bluetooth-controlled RGB fog lamps, tri-color projectors, and laser-inspired spot modules that cater to enthusiasts. Europe’s component certification programs grant street-legal status to many upgrades, legitimizing sales channels and reducing regulatory risk. Online tutorials and real-time beam-pattern simulators further boost consumer confidence in self-installation. As more fleets adopt retrofit LED kits to hit sustainability targets, the automotive fog lights market share gap between OEM and aftermarket is expected to narrow. Suppliers capable of fast product refresh cycles will seize this incremental growth.

Geography Analysis

Asia-Pacific retained 37.25% share in 2024 and leads growth at 2.75% CAGR. China’s lighting component ecosystem drives scale economies, while India’s new rear fog mandate adds OEM and retrofit volumes. Local suppliers benefit from proximity to automakers, reducing logistics costs and enabling joint design cycles. Countries such as Thailand and Indonesia double down on supplier parks that bundle die-casting, LED packaging, and final assembly lines, cementing regional dominance.

Europe’s market remains technologically influential with stringent UNECE standards and sustainability policy. Circular-economy pilots, including Stellantis-Valeo’s remanufactured LED headlamps, lower CO₂ by 70% and open secondary revenue streams. EU directives on halogen phase-outs by 2027 spur LED adoption across both OEM and aftermarket. Economic softness tempers unit expansion, but high value per unit sustains regional revenue.

North America posts steady gains on the back of FMVSS 108 revisions that legalized adaptive driving beams. Consumer appetite for LED upgrades drives a robust aftermarket, and commercial fleet electrification amplifies low-voltage lighting demand. Mexico’s growing role as near-shore manufacturing hub aids supply resilience. Latin America and the Middle East & Africa start from smaller bases but pick up speed as safety rules tighten and vehicle production rises in Brazil, Turkey, and South Africa.

Competitive Landscape

The automotive fog lights market exhibits moderate concentration, creating opportunities for both established suppliers and emerging technology specialists to capture growth through innovation and strategic positioning. Koito leads by leveraging early adoption of sensor-ready fog lamps and deep OEM ties. Valeo follows with strong adaptive beam IP and global footprint. Forvia Hella excels in modular matrix LED platforms. These firms pour resources into software teams, reflecting the transition toward digital lighting ecosystems.

Strategic deals reshaped the landscape in 2024-2025. Lumileds divested its lamps and accessories arm to First Brands Group for USD 238 million in August 2024, sharpening focus on LED dies and phosphors. Stanley Electric and Mitsubishi Electric Mobility formed a venture aimed at next-generation adaptive modules, pooling optoelectronics and control-software competencies. Start-ups specializing in thermal materials and over-the-air firmware forge partnerships with tier-ones, providing agile innovation.

Competitive axes now hinge on patent depth in pixelated LED arrays, ability to pass multi-site COP (Conformity of Production) audits, a growing requirement as OEMs demand consistent quality across global manufacturing footprints. In-house thermal simulation capabilities are becoming critical for optimizing LED performance and longevity, especially under varying environmental conditions. Mid-size suppliers seek differentiation through fast-to-market retrofit lines and circular-economy credentials. Market entry barriers rise as compliance testing expands to glare-control metrics and cybersecurity standards for software-defined lighting.

Automotive Fog Lights Industry Leaders

Koito Manufacturing Co., Ltd.

Valeo SA

Forvia Hella

Magneti Marelli S.p.A.

Stanley Electric Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mahindra introduced the XUV 3XO SUV with LED front fog lights, panoramic roof, and 17-inch alloys.

- March 2025: Maruti Suzuki unveiled its eVitara EV featuring matrix LED DRL and LED fog lights.

- February 2025: ams OSRAM released the LR6 LED source for slim signal lamps, suited for rear fog lights.

- October 2024: Hyundai revealed the 2025 i30 facelift with updated fog lights and refreshed bumper design.

Global Automotive Fog Lights Market Report Scope

| Halogen |

| LED |

| Xenon/HID |

| Laser |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Front Fog Lights |

| Rear Fog Lights |

| Conventional Static Fog Lights |

| Adaptive Fog Lights |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Light Type | Halogen | |

| LED | ||

| Xenon/HID | ||

| Laser | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| By Application | Front Fog Lights | |

| Rear Fog Lights | ||

| By Technology | Conventional Static Fog Lights | |

| Adaptive Fog Lights | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2025 value of the automotive fog lights market?

The automotive fog lights market size reached USD 1.12 billion in 2025.

How fast is the market expected to grow?

It is projected to expand at a 2.65% CAGR between 2025 and 2030.

Which light type leads global demand?

LED fog lamps dominate with a 51.96% share.

Which vehicle class is growing the quickest?

Passenger Cars post the fastest CAGR at 9.24% through 2030.

Why are adaptive fog lights gaining traction?

They align with ADAS integration, offer beam control, and can receive over-the-air updates.

Which region contributes the most revenue?

Asia-Pacific holds the largest regional share at 37.25% in 2024.

Page last updated on: