HCM For Deskless And Frontline Workers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.34 Billion |

| Market Size (2031) | USD 30.74 Billion |

| Growth Rate (2026 - 2031) | 14.92% CAGR |

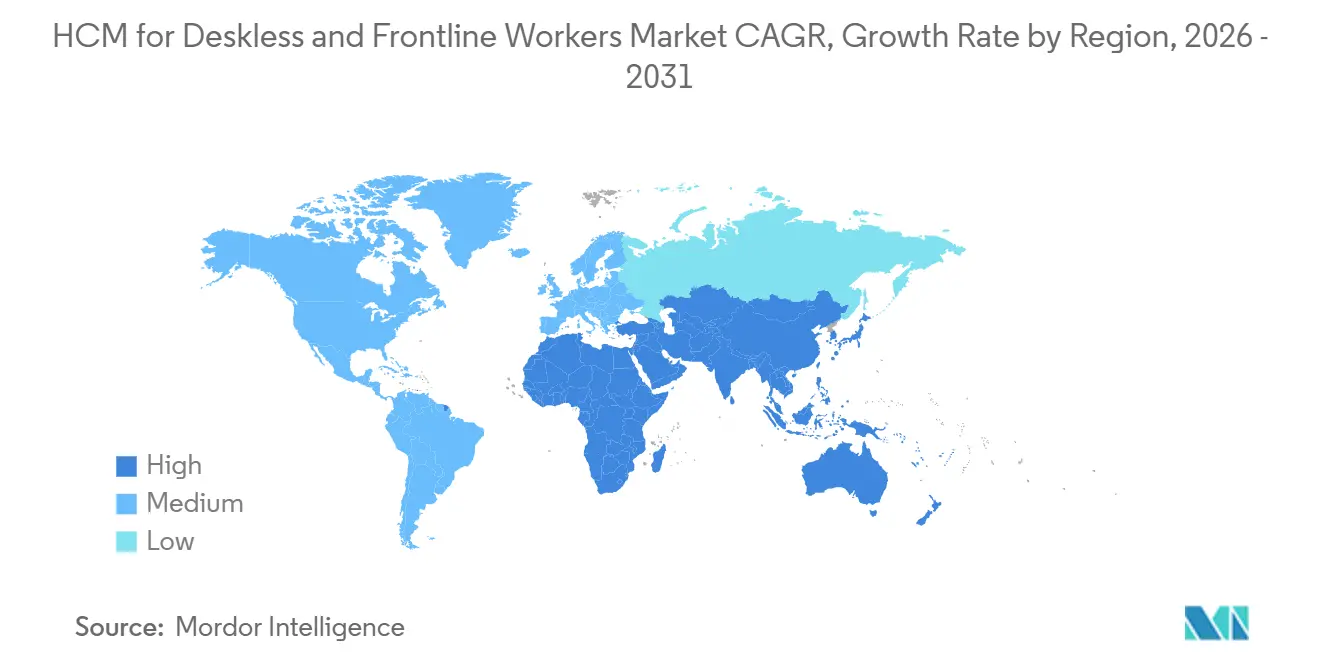

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM For Deskless And Frontline Workers Market Analysis by Mordor Intelligence

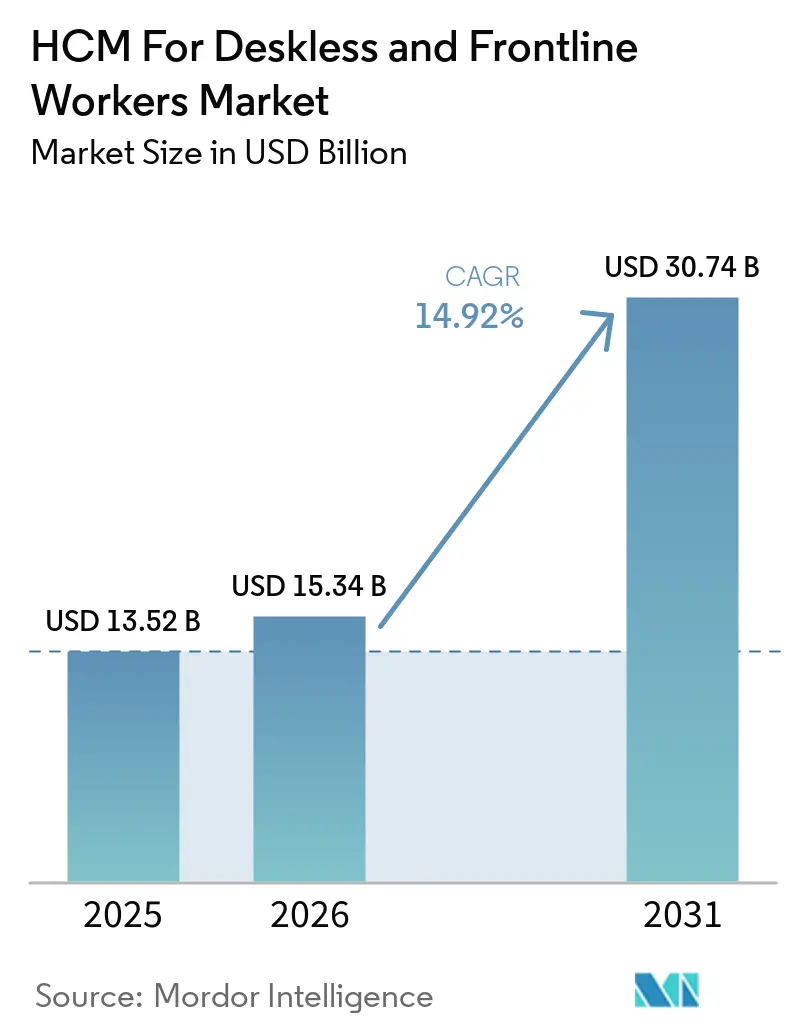

The HCM for deskless and frontline workers market size reached USD 13.52 billion in 2025 and is forecast to reach USD 30.74 billion by 2031, advancing at a CAGR of 14.92% during 2026-2031. This pace reflects a broader shift in HR technology, because employers are now redesigning systems for workers who spend their time in stores, hospitals, warehouses, transit networks, and job sites rather than at desks. The HCM for deskless and frontline workers market is moving beyond isolated pilots, as multi-site employers replace manual rosters, disconnected payroll portals, and desktop-first tools with mobile applications that combine scheduling, compliance, communication, and pay access. Labor regulation is also pushing this shift, because predictive scheduling, earned-wage access, and AI transparency rules are harder to manage with spreadsheets or fragmented systems. The HCM for deskless and frontline workers market remains moderately fragmented, with specialist vendors, suite providers, and vertical-focused entrants all competing for enterprise and mid-market accounts. Growth is still moderated by legacy system fragmentation, because employers with incompatible payroll, POS, EHR, and ERP environments face slower deployments and longer integration cycles.

Key Report Takeaways

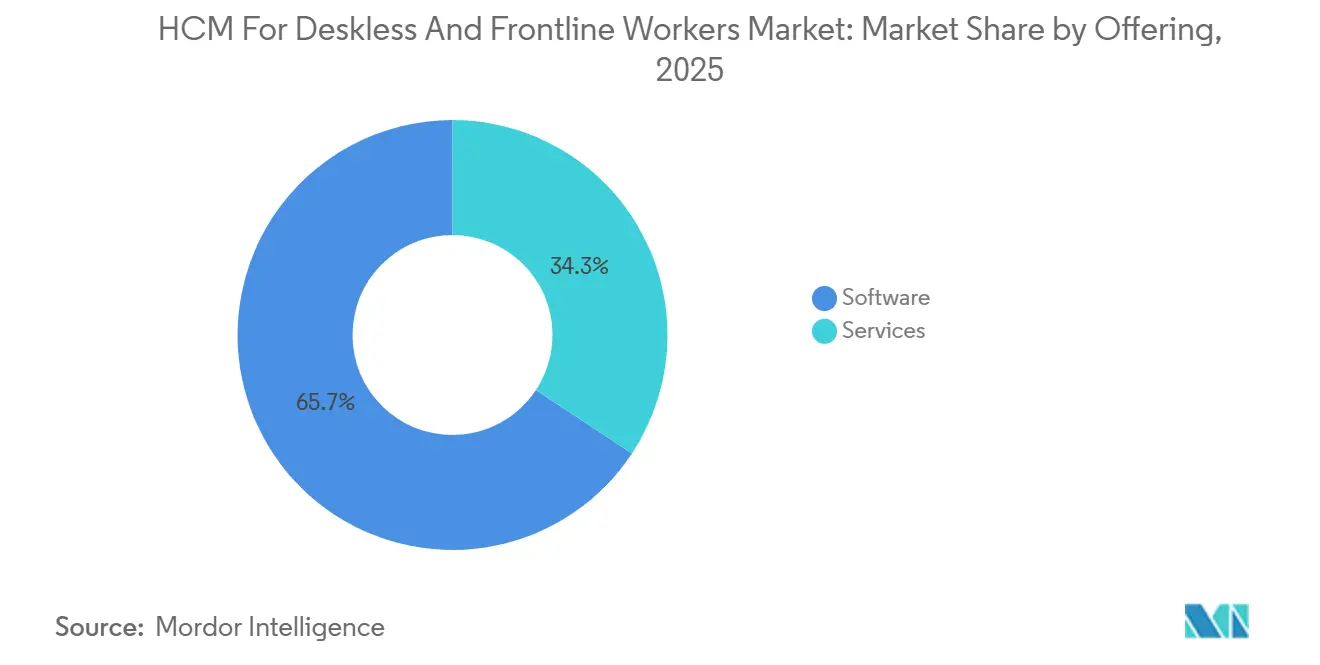

- By offering software solutions, held 65.72% of revenue in the HCM for Deskless and Frontline Workers Market 2025, while services are projected to expand at a 16.42% CAGR through 2031.

- By deployment mode, cloud-based deployment held 72.19% share in 2025, while hybrid deployment is projected to expand at a 17.36% CAGR through 2031.

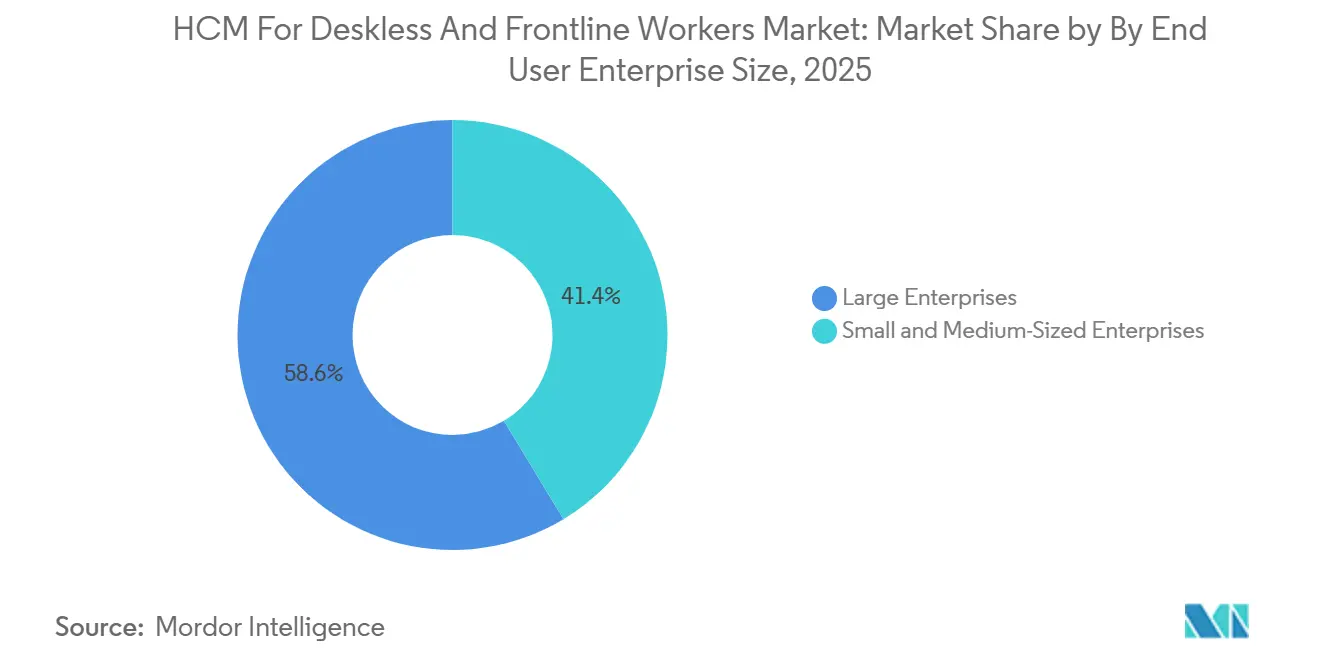

- By end-use enterprise size, large enterprises held a 58.63% share in 2025, while SMEs are projected to record the highest CAGR of 18.11% through 2031.

- By end-user industry, retail and e-commerce accounted for 24.81% of the market share in 2025, while healthcare and life sciences are projected to expand at a 15.94% CAGR through 2031.

- By geography, North America held 39.42% share of the HCM for deskless and frontline workers market in 2025, while Asia-Pacific is projected to record the fastest CAGR of 19.00% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM For Deskless And Frontline Workers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-Rule Complexity Across Multi-Site Shift Operations | +3.8% | Global | Medium term (2-4 years) |

| Mobile-First Digitization of Deskless Workflows | +3.2% | APAC core, spill-over to South America and MEA | Short term (≤ 2 years) |

| AI-Led Labor Forecasting and Schedule Optimization | +2.9% | North America and Europe | Short term (≤ 2 years) |

| Unified HR, Payroll, Scheduling, and Communication Stacks | +2.1% | North America and Europe | Medium term (2-4 years) |

| Explainable AI and Audit-Ready Scheduling Demand | +1.5% | North America and Europe | Medium term (2-4 years) |

| Worker-Control Expectations Around Shifts, Pay, and Flexibility | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Rule Complexity Across Multi-Site Shift Operations

The HCM for deskless and frontline workers market is gaining from the rising complexity of labor rules across multi-site shift environments. Predictive scheduling ordinances in cities such as San Francisco, New York City, Chicago, and Seattle require advance notice, rest-period protection, and compliance with premium pay requirements, making manual roster control harder to sustain. The burden rises further when a single employer operates across multiple jurisdictions, because wage-and-hour rules, break requirements, overtime thresholds, and minor-work restrictions do not align neatly. Illinois HB 3773, which took effect in January 2026, added algorithm restriction requirements for AI-driven employment decisions, showing how quickly compliance obligations are layering across the United States. In this setting, vendors that embed rule-aware engines and update them as regulations change are turning compliance from a support feature into a clear buying factor.[1]State of Illinois, “House Bill 3773, Artificial Intelligence Video Interview Act Amendment,” Illinois General Assembly, ilga.gov

Mobile-First Digitization of Deskless Workflows

The HCM for deskless and frontline workers market is also being driven by the shift of smartphones to the primary HR access point for non-desk workers. Employers increasingly want one mobile app to handle schedules, payslips, tasks, training, and team communication, because workers on shop floors and hospital wards do not have reliable access to desktop systems. Vendors such as Connecteam, Beekeeper, and Flip have helped set that expectation by showing that frontline engagement improves when these functions are brought together in one simple interface. A June 2025 study in JMIR Formative Research found that 76% of surveyed healthcare shift workers ranked scheduling flexibility and autonomous shift-swap capability among their top work-condition preferences, which supports the demand for mobile-native scheduling tools. This is making interface quality and offline performance more important than raw feature count, especially in the SME tier, where buyers move quickly if the user experience is weak.[2]Aubert Anne-Laure et al., “Integrating Nurse Preferences Into AI-Based Scheduling Systems, Qualitative Study,” JMIR Formative Research, formative.jmir.org

AI-Led Labor Forecasting and Schedule Optimization

The HCM for deskless and frontline workers market is seeing AI-led labor forecasting move from a differentiator to a baseline expectation in frontline-heavy sectors. Legion stated in January 2026 that analysis of more than 2 million frontline workers on its platform showed a 33% average improvement in retention and a 66% improvement in on-time punches when AI-led schedule optimization was activated.[3]Legion Technologies, “Legion Launches 90+ AI Workforce Innovations,” Legion Press Releases, legion.co Humanforce stated in May 2026 that its Smart Scheduling launch reduced roster-management time by up to 70% and lowered labor costs by up to 15% through demand-aligned shift generation. These claims matter because buyers are now judging platforms by their ability to detect demand signals that manual planners often miss. The value is not limited to automation, since the software can connect weather, booking patterns, promotions, and patient volumes to future staffing needs before shortfalls appear.

Unified HR, Payroll, Scheduling, and Communication Stacks

The HCM for deskless and frontline workers market is also benefiting from a clear preference for unified platforms over disconnected point tools. When scheduling, payroll, time tracking, and messaging are in separate systems, workers switch between apps, managers manually reconcile records, and payroll errors become more likely. WorkJam’s January 2026 release reflected this direction by placing AI-powered workflow automation directly into retail and manufacturing execution tasks, rather than leaving it as a separate toolset. Deputy’s U.S. Payroll launch through Paycor integration showed the same pattern, with the company stating that payroll processing time could be reduced by up to 50% for shift-based businesses. This favors vendors that can enter through one use case, usually scheduling or time tracking, and then expand across adjacent HR workflows over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity Across HR, Payroll, POS, And EHR | -1.8% | Global | Medium term (2-4 years) |

| Workforce Data Privacy and Mobile Cybersecurity Exposure | -1.3% | North America and Europe | Medium term (2-4 years) |

| Shared-Device Identity and Digital Access Gaps | -0.9% | APAC core, South America, and MEA | Long term (≥ 4 years) |

| Manager And Worker Distrust of Opaque Scheduling AI | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity Across HR, Payroll, POS, And EHR

The HCM market for deskless and frontline workers still faces its most serious barrier: legacy integration complexity. Large employers in retail, healthcare, and manufacturing often run payroll, POS, EHR, and ERP systems on separate architectures, and those systems do not integrate easily with cloud-native workforce tools. That slows implementation, because data models, identity structures, and reporting logic often need to be rebuilt before scheduling or payroll modules can run reliably across sites. In multi-site healthcare systems, deployment timelines can stretch to 9-18 months, delaying payback and weakening internal support for broader suite rollouts. The problem becomes even harder after M&A activity, when acquired locations operate different HR and payroll systems and require an additional layer of integration work before standardization becomes possible.

Workforce Data Privacy And Mobile Cybersecurity Exposure

The HCM market for deskless and frontline workers also faces a significant drag from data privacy and mobile security risks. These platforms handle sensitive records such as biometric punches, shift preferences, earned-wage balances, and health-related scheduling accommodations, and much of that data moves across personal smartphones and public mobile networks. The risk profile differs from that of office HR systems because device patching is inconsistent, shared devices are common in warehouses and clinics, and access rights must be revoked frequently in high-turnover settings. Europe’s tightening scrutiny of employment-related AI systems, including the high-risk requirements under the EU AI Act set to take effect in August 2026, is adding to the control burden that vendors must address through logging, oversight, and governance features.[4]European Parliament and Council of the European Union, “Regulation (EU) 2024/1689 Laying Down Harmonised Rules on Artificial Intelligence,” Official Journal of the European Union, eur-lex.europa.eu Vendors that build phishing-resistant authentication, strong role-based access controls, and better mobile session control into their products are in a stronger position, but the cost and operational effort still slow some buying decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offeriing: Software Platforms Anchor Revenue While Services Scale

Software solutions accounted for 65.72% of the HCM market share for deskless and frontline workers in 2025, making software the clear revenue anchor across frontline deployments. Demand centered on workforce management and payroll-and-pay-management modules, because they sit closest to labor cost control and labor-law compliance in multi-site operating models. For many employers, workforce management remains the first product they buy, since scheduling and time capture deliver visible operational value quickly. At the same time, analytics and compliance tools are becoming higher-value add-ons because audit-ready scheduling and rule validation now support legal defensibility as much as internal reporting.

Services are projected to expand at the fastest CAGR of 16.42% from 2026 to 2031, reflecting the growing need for integration work, vertical configuration, and ongoing compliance support. The HCM for deskless and frontline workers market is therefore shifting from stand-alone module sales toward broader contracts that bundle core HR, employee records, learning, and communication functions into a single platform relationship. That change narrows the stand-alone opportunity for pure-play learning or communication vendors, especially when enterprise buyers prefer one vendor to manage deployment and change management. Axonify’s May 2026 platform update showed how product lines are converging, as the company linked frontline learning more closely to operational execution metrics and reported that customers experienced a 47% reduction in lost sales and a 23% decrease in call-handling time after AI-enabled training interventions.

By Deployment Mode: Hybrid Architecture Emerges As The Practical Bridge

Cloud-based deployment accounted for 72.19% of the HCM market for deskless and frontline workers in 2025, reflecting the preference for subscription delivery and the need to onboard distributed sites quickly. That leadership is supported by mid-market buying behavior, because cloud products reduce infrastructure burden and make updates easier across many locations. Even so, the HCM for deskless and frontline workers market is not moving in a straight line toward full cloud replacement. Hybrid deployment is projected to expand at a 17.36% CAGR from 2026 to 2031, because large employers often need to keep EHR, POS, or MES systems on-premises while adding cloud HCM modules around them.

This dynamic is especially evident in healthcare and manufacturing, where continuity, regulations, and capital budget constraints make full-system replacement difficult within normal planning cycles. For these buyers, hybrid architecture is not a temporary compromise; it is the most realistic way to connect cloud scheduling, payroll, and engagement tools with entrenched operational systems. On-premises deployment is gradually shrinking, but its installed base remains important in regulated industries and some government environments where data residency or security rules limit hosting options. Vendors with stronger hybrid API layers and real-time synchronization are better placed to win enterprise renewals, because they meet buyers where their infrastructure already stands rather than forcing a complete migration first.

By End Use Enterprise Size: Large Enterprises Lead While SMEs Gain Speed

Large enterprises accounted for 58.63% of revenue in 2025, indicating that the HCM for deskless and frontline workers market continues to draw most of its spending from employers with broad site networks and complex labor exposure. National retailers, hospital systems, and global logistics groups use these platforms to manage multi-jurisdiction scheduling, staffing visibility, and payroll consistency at scale. Their buying cycles are longer, since pilots often begin across 20-50 sites before a wider rollout is approved. Even with that slower path, large accounts remain attractive because they support broad module adoption and stronger long-term contract values.

SMEs are projected to expand at the fastest CAGR of 18.11% from 2026 to 2031, as lower-cost mobile applications reduce the barrier to entry for shift-based businesses. Vendors such as Homebase, Teambridge, Connecteam, and Workforce.com are helping smaller operators move away from paper schedules and basic calendar tools without taking on enterprise-level implementation work. This is widening the addressable base of the HCM for deskless and frontline workers market, especially among foodservice businesses, independent retailers, and smaller construction firms with 50-250 workers. The tradeoff is margin pressure, because rapid user growth in this tier often comes with lower per-seat pricing and fewer service attachments, which can limit profitability even when adoption is strong.

By End-User Industry: Retail Leads While Healthcare Builds Momentum

Retail and e-commerce held the largest share of the HCM for deskless and frontline workers market in 2025 at 24.81%, maintaining the segment's lead. Labor remains one of the largest controllable operating costs in this sector, and omni-channel operations add scheduling complexity across stores, fulfillment points, and last-mile delivery. Hospitality and foodservice, manufacturing, and transportation and logistics form the next tier of demand, since all three operate with high shift frequency, significant compliance exposure, and persistent turnover pressure. These industries also increasingly value employee communication and engagement tools, because service continuity depends on keeping shift-based staff informed and available.

The healthcare and life sciences sector is projected to expand at the fastest CAGR of 15.94% from 2026 to 2031, driven by nursing shortages and the growing need to balance fairness, workload, and continuity of care. In this segment, scheduling is no longer seen solely as a labor-cost issue, because staffing quality directly affects retention and patient outcomes. A February 2026 study published in Systems found that AI-mediated hospital scheduling could balance fairness, workload distribution, and individual preferences simultaneously, something manual approaches struggle to achieve at scale. Construction and field services, energy and utilities, and public sector and education remain smaller in share, but they represent sticky demand areas because time accuracy, project labor costing, certification tracking, and compliance reporting all support renewal.

Geography Analysis

North America led the HCM for deskless and frontline workers market in 2025 with a 39.42% share, reflecting the scale of U.S. retail and healthcare, mature cloud infrastructure, and a compliance-heavy regulatory environment that accelerates the adoption of automated scheduling and workforce platforms. The U.S. continues to benefit from compliance-led procurement cycles, while Canada advances through healthcare digitization and logistics flexibility, and Mexico sees stronger uptake in northern manufacturing-export zones shaped by multinational standards.

Asia-Pacific is projected to grow fastest, with a 19.00% CAGR from 2026 to 2031. Manufacturing digitization in China, India, and Southeast Asia, along with the rapid expansion of organized retail and QSR chains, are key driver. Gig-adjacent labor models further boost demand for mobile-native scheduling and pay coordination. Large healthcare groups like IHH Healthcare and Health Management International are adopting enterprise-grade platforms to unify operations, while Japan’s convenience and QSR sectors and Australia/New Zealand’s regional vendors add depth to the opportunity.

Europe remains the third-largest demand block, with Germany, the UK, and France at the center. Germany’s complex labor framework sustains demand for audit-ready scheduling, while ATOSS reported EUR 189.3 million in 2025 revenue and strong cloud growth in 2026. The UK’s blended workforce model supports unified HR and payroll adoption. South America, the Middle East, and Africa are earlier-stage but maturing, with Brazil’s retail digitization, Saudi Arabia’s labor formalization agenda, and Shoprite Group’s rollout of YOOBIC across 3,600+ South African stores pointing to broader enterprise adoption.

Competitive Landscape

The HCM for deskless and frontline workers market remains fragmented, with no single provider holding a dominant share across all regions and end-user categories. Competition is split between established suite vendors that compete on integration depth and compliance breadth, and mobile-first entrants that compete on speed, ease of deployment, and scheduling intelligence. This leaves room for specialists in healthcare rostering, construction compliance, and flexible labor orchestration, especially where broad-suite vendors have a weaker workflow fit. The HCM for deskless and frontline workers market, therefore, rewards vendors that can solve specific operational problems first and then widen the relationship across payroll, communication, and engagement functions.

Several recent moves show how vendors are trying to broaden that reach. Humanforce launched Humanforce Connect in April 2026, building on the capabilities acquired from Emprevo and ShiftMatch to create a single environment for roster creation, private labor marketplaces, and agency vendor management. Deputy expanded closer to core payroll workflows through its Paycor-linked U.S. Payroll launch, which reflects a wider push among suppliers to remove friction between time tracking and pay execution. Legion also pushed the field forward in January 2026 with more than 90 AI workforce management innovations that moved beyond assisted recommendations toward more autonomous decision execution across forecasting, scheduling, and labor optimization. These moves suggest that the next phase of competition will center less on basic scheduling and more on how many adjacent workflows a vendor can automate in the same operating environment.

Product architecture is also being shaped by explainability and governance needs. ATOSS stated that it planned to launch its agentic ATC assistant in Q2 2026, allowing workers to describe scheduling needs by voice while the system autonomously validates applicable rules. Vendors are increasingly investing in predictive forecasting methods and explainable scheduling logic as they prepare for stricter oversight of employment-related AI. The August 2026 implementation phase of the EU AI Act is raising the importance of quality management, event logging, and human oversight in workforce applications that influence hiring and scheduling decisions. As a result, competition is likely to favor companies that can combine mobile usability, compliance controls, and deeper integration with enterprise systems within a single platform.

HCM For Deskless And Frontline Workers Industry Leaders

WorkForce Software, LLC

Deputy Corporation

Mobilesson Ltd. d/b/a Connecteam

Humanforce Holdings Pty Ltd

Quinyx AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Humanforce Holdings Pty Ltd launched AI-powered Smart Scheduling, an advanced rostering engine that reduces roster management time by up to 70% and can lower labor costs by up to 15% through demand-aligned shift generation. The product analyzes historical sales, weather, and bookings data to generate compliance-embedded shift patterns for frontline employers in healthcare, hospitality, and retail.

- May 2026: UKG unveiled agentic-powered UKG Pro Pay with Workforce AI at Payroll Congress 2026, extending the company's AI-led workforce operating platform into payroll execution with autonomous processing capabilities designed for large-scale frontline workforces.

- May 2026: Deputy Corporation launched Deputy Analytics+ globally, an enterprise-grade business intelligence and reporting solution built specifically for shift-based businesses, providing interactive dashboards, dynamic filters, and drill-down reports without requiring dedicated data teams.

- May 2026: Axonify Inc. unveiled significant AI enhancements at the Association for Talent Development Annual Conference in Los Angeles, including an AI Insights engine for frontline readiness reporting and an AI-powered Rollout tool for structured operational initiative execution. Customers reported a 47% reduction in lost sales and a 23% decrease in call-handling time following platform adoption.

Global HCM For Deskless And Frontline Workers Market Report Scope

The HCM for Deskless and Frontline Workers market comprises software and services that manage human capital functions for non-office-based employees, including workforce scheduling, payroll, compliance, communication, engagement, and learning. These solutions enable enterprises to streamline HR operations, improve productivity, and enhance employee experience for distributed, mobile, and frontline workforces across industries.

The HCM for Deskless and Frontline Workers market report is segmented by Offering (Software [Core HR and Employee Records, Workforce Management, Payroll and Pay Management, Talent Acquisition and Onboarding, Learning and Enablement, Employee Communication and Engagement, and Analytics and Compliance], and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-user Industry (Retail and E-commerce, Healthcare and Life Sciences, Manufacturing, Hospitality and Foodservice, Transportation and Logistics, Construction and Field Services, Energy and Utilities, Public Sector and Education), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Core HR and Employee Records |

| Workforce Management | |

| Payroll and Pay Management | |

| Talent Acquisition and Onboarding | |

| Learning and Enablement | |

| Employee Communication and Engagement | |

| Analytics and Compliance | |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Hospitality and Foodservice |

| Transportation and Logistics |

| Construction and Field Services |

| Energy and Utilities |

| Public Sector and Education |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Software | Core HR and Employee Records |

| Workforce Management | ||

| Payroll and Pay Management | ||

| Talent Acquisition and Onboarding | ||

| Learning and Enablement | ||

| Employee Communication and Engagement | ||

| Analytics and Compliance | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End Use Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | Retail and E-commerce | |

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Hospitality and Foodservice | ||

| Transportation and Logistics | ||

| Construction and Field Services | ||

| Energy and Utilities | ||

| Public Sector and Education | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the HCM for deskless and frontline workers market in 2025, and what is the 2031 outlook?

The HCM for deskless and frontline workers market reached USD 13.52 billion in 2025 and is forecast to reach USD 30.74 billion by 2031, at a 14.92% CAGR over 2026-2031.

Why are employers shifting toward mobile-first HCM platforms for frontline teams?

Employers want one simple app for scheduling, pay access, communication, and task management because deskless workers rely on phones, not desktops, during the workday.

Which offering category leads revenue, and which one is growing faster?

Software led with a 65.72% share in 2025, while services are projected to grow faster at a 16.42% CAGR through 2031 due to integration and compliance support needs.

Why is hybrid deployment gaining traction if cloud already dominates?

Cloud held 72.19% share in 2025, but hybrid is growing faster at 17.36% CAGR because many employers still need to connect cloud HCM modules with on-premises EHR, POS, or MES systems.

Which end-user sector is currently the largest, and which one is expanding the fastest?

Retail and e-commerce led with 24.81% share in 2025, while healthcare and life sciences is projected to grow fastest at a 15.94% CAGR because staffing quality now affects both retention and service outcomes.

Which region offers the strongest growth opportunity through 2031?

North America remained the largest region in 2025 with 39.42% share, but Asia-Pacific is projected to post the fastest growth at a 19.00% CAGR through 2031.

Page last updated on: