North America Integrated Workplace Management System (IWMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

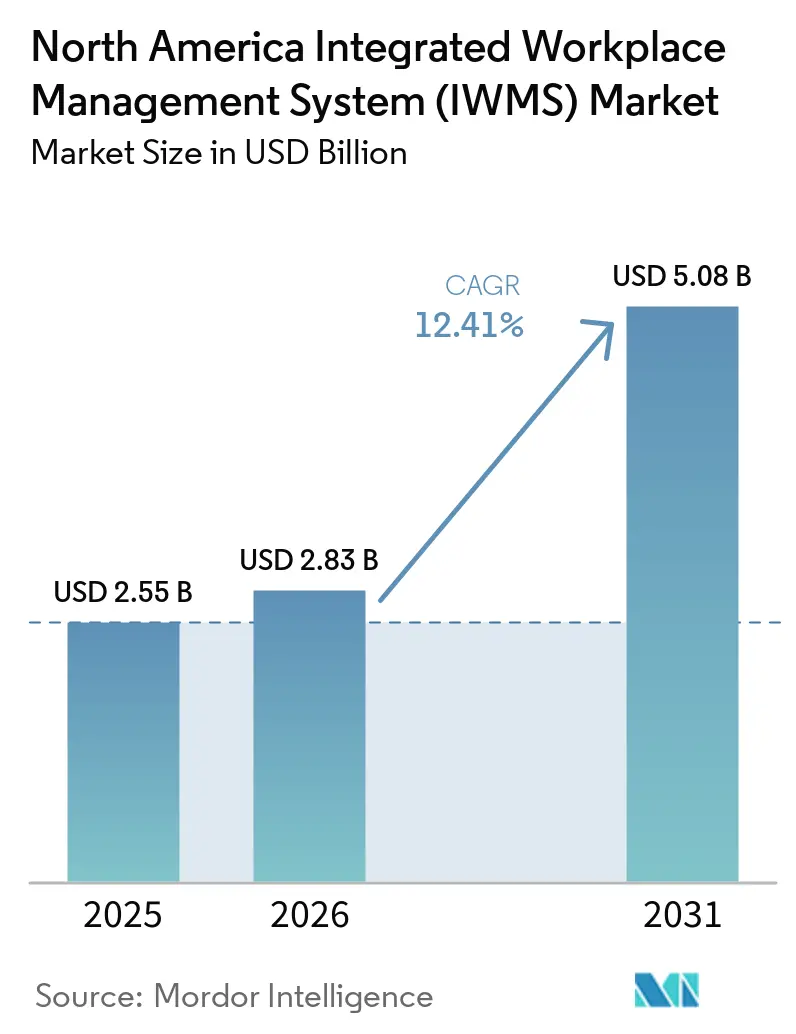

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 12.41% CAGR |

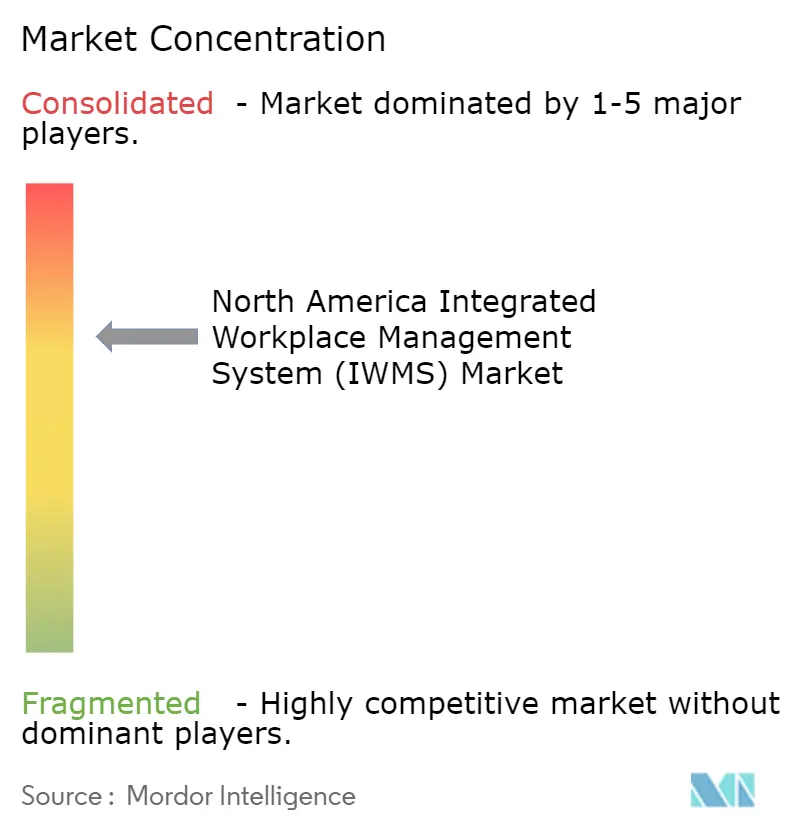

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Integrated Workplace Management System (IWMS) Market Analysis by Mordor Intelligence

The North America Integrated Workplace Management System (IWMS) market size was valued at USD 2.55 billion in 2025, USD 2.83 billion in 2026, and is forecast to reach USD 5.08 billion by 2031, growing at a CAGR of 12.41% over 2026-2031. The North America Integrated Workplace Management System market remains the largest regional revenue pool because vendor depth, cloud readiness, and enterprise buying maturity are stronger here than in most other regions. Demand in the North America Integrated Workplace Management System (IWMS) market is being shaped by hybrid work becoming a fixed operating model and by tighter climate and lease reporting obligations that require auditable building data rather than spreadsheet-based processes. Competitive conditions in the North America IWMS market are defined by platform breadth, AI-backed analytics, and connector ecosystems, as buyers now place more value on unified systems than on isolated tools. The same shift is expanding room for service-led growth, since implementation, integration, and managed support have become more important as deployments span more systems and business teams. Even with long rollout cycles and budgetary competition from other workplace technologies, the North America Integrated Workplace Management System market continues to benefit from a structural pull driven by occupancy analytics, ESG reporting timelines, and standardized lease accounting requirements.

Key Report Takeaways

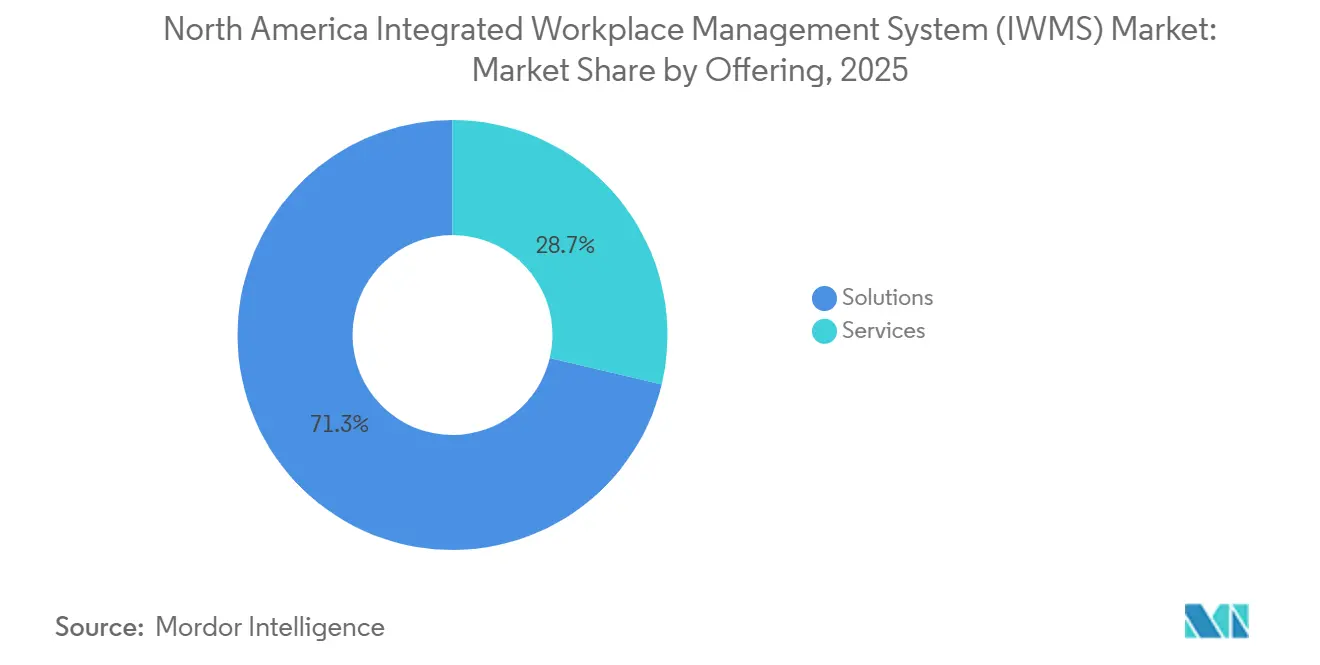

- By offering solutions, held 71.30% of revenue in 2025, while services are projected to expand at a 16.84% CAGR through 2031 in the North America Integrated Workplace Management System (IWMS) market.

- By deployment, cloud accounted for 66.80% share of the North America Integrated Workplace Management System market in 2025, while on-premises is projected to record the fastest 15.27% CAGR through 2031.

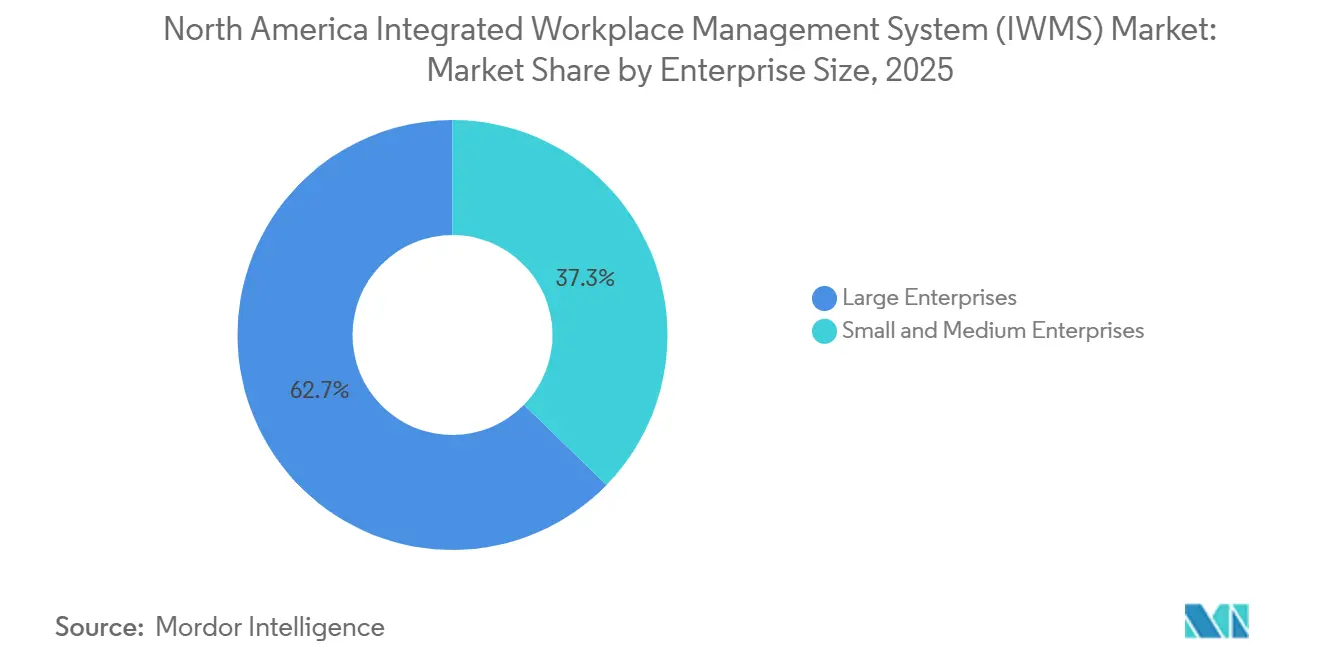

- By enterprise size, large enterprises held 62.70% share of the North America IWMS market in 2025, while SMEs are expected to expand at a 17.41% CAGR through 2031.

- By end-user industry, information technology and telecom were the largest segments in 2025, while healthcare and life sciences are projected to advance at a 19.12% CAGR through 2031 in the North America Integrated Workplace Management System market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Integrated Workplace Management System (IWMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid Work and Desk Optimization Across Large Portfolios | +3.2% | North America-wide, concentrated in US gateway markets and Canada's urban cores | Short term (≤ 2 years) |

| Cloud Migration of Workplace and Facilities Software | +2.5% | Global, with North America as a primary adopter region | Medium term (2-4 years) |

| Sustainability Reporting and Building Decarbonization Requirements | +2.0% | US, especially California SB 253 and SB 261, and Canada, with spillover to Mexico | Medium term (2-4 years) |

| Integration with ERP, HRIS, BIM, and Building Systems | +1.6% | Global, concentrated in large enterprise corridors of the US and Canada | Long term (≥ 4 years) |

| Portfolio Rationalization and Real Estate Cost Reduction | +1.2% | US gateway markets, including New York, Chicago, San Francisco, and Washington, D.C. | Short term (≤ 2 years) |

| Public Sector and Higher Education Modernization Spending | +0.8% | US federal and state agencies, and Canadian provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work And Desk Optimization Across Large Portfolios

Structured hybrid work has become the operating baseline across large employers, creating a clearer use case for the North America Integrated Workplace Management System (IWMS) market. The 2026 benchmark, which covered 84 organizations and 716 million square feet, shows that North America still has the widest actual-to-target utilization gap globally, with actual utilization at 41% against a 77% target.[1]JLL, “Global Occupancy Planning Benchmark Report 2026,” JLL, jll.com The same benchmark shows that the share of employees attending 3-4 in-office days a week rose to 55% in 2026 from 36% in 2025, while fully remote work fell to 10% from 18%, pushing more demand into a narrower part of the workweek. That pattern makes older space-allocation methods less dependable, because peak-day pressure now matters more than average attendance. It also shifts the buying case away from simple cost control and toward avoiding capacity failures that weaken mandated return-to-office programs. As a result, space analytics, reservation management, and occupancy forecasting are moving closer to core buying priorities across the regional market.

Cloud Migration Of Workplace And Facilities Software

Cloud migration continues to reshape software buying in the North America Integrated Workplace Management System (IWMS) market, as enterprises now prefer recurring SaaS deployments over capital-intensive on-premises rollouts. Planon listed its IWMS on AWS Marketplace in April 2026, allowing customers to apply existing AWS Enterprise Discount Program credits to procurement and lowering a common budget barrier. That move reflects a broader pattern in which vendors align with hyperscaler purchasing channels to shorten approvals and reduce IT resistance. Cloud held 66.80% share in 2025, yet the continued growth of on-premises deployments in regulated sectors shows that buyers are not choosing one model in isolation. Instead, more organizations are adopting mixed deployment structures in which sensitive workloads remain on private infrastructure while administrative modules move to the cloud. SAP's December 31, 2027, maintenance deadline for HCM On-Premise also supports adjacent application changes that create additional pull for cloud-ready IWMS platforms with strong SAP connectors.

Sustainability Reporting And Building Decarbonization Requirements

Sustainability reporting is now a direct buying driver for the North America IWMS market because building-level data has become central to compliance preparation. California SB 253 moved into implementation with regulations approved by the California Air Resources Board on February 26, 2026, and the rule requires covered companies doing business in California to file first Scope 1 and Scope 2 emissions reports by August 10, 2026. That timetable makes it harder to defer sustainability modules, especially when facility teams need normalized energy and emissions data at the asset level. The Institute for Market Transformation reported that more than 50 US cities and counties had enacted Building Performance Standards by 2025, increasing financial exposure for organizations that still lack monitoring and benchmarking capabilities. This is changing purchase timing because facilities teams often need a system response before broader enterprise transformation programs are finalized. It also makes the value of ESG overlays more immediate, since reporting deadlines now create fixed schedules that standard IT governance processes cannot easily delay.[2]Institute for Market Transformation, “2025 Building Policies Outlook, More and Smaller Cities Still Passing Building Performance Standards,” Institute for Market Transformation, imt.org

Integration With ERP, HRIS, BIM, And Building Systems

Integration has become one of the most important structural drivers in the North America Integrated Workplace Management System (IWMS) market because buyers no longer view real estate and facilities tools as isolated applications. A 2025 study found that 88% of IT leaders are directly involved in real estate and facilities software decisions, and 77% of their organizations already run smart building programs. That means an IWMS decision often involves IT, OT, HR, finance, and workplace operations simultaneously. Planon's move to SAP Solution Extension status in January 2026 signaled that certified platform-level integration is becoming a purchasing requirement rather than an optional post-sale project. IBM's 2026 consolidation of TRIRIGA capabilities into the Maximo Application Suite also points to a model where fewer integration seams separate capital projects, maintenance workflows, and corporate real estate operations.[3]IBM, “IBM Reports First-Quarter 2025 Financial Results,” IBM Newsroom, ibm.com The market effect is clear: vendors with certified connectors and strong ecosystem ties are better placed than those that still depend on heavy custom API work for each deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Implementation Cycles and Change-Management Friction | -1.8% | North America-wide, strongest drag in mid-market US and Canadian enterprise segments | Medium term (2-4 years) |

| High Integration Complexity With Legacy Enterprise Systems | -1.4% | US industrial and government sectors, and other legacy-heavy verticals | Long term (≥ 4 years) |

| Data Security, Privacy, and Governance Concerns | -1.0% | North America, especially US healthcare and government, and Canada under PIPEDA | Medium term (2-4 years) |

| Budget Pressure From Competing Workplace Technology Priorities | -0.7% | US and Canada mid-market enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long Implementation Cycles And Change-Management Friction

Implementation length remains a practical drag on the North America Integrated Workplace Management System market because enterprise programs often take 12-24 months to reach full operating scope. That time frame reflects process redesign, data migration, and cross-functional alignment needs, not just software setup. The 2026 benchmark showed that organizations running formal change-management programs fell to 31% in 2026 from 40% in 2025, even as hybrid work planning became more complex. Mid-market buyers feel this more sharply because they usually do not have the governance structures that large enterprises use to coordinate project teams and ongoing operations. Vendors are trying to reduce the burden with pre-built templates and vertical accelerators, but those methods often narrow the first deployment phase and leave some capabilities for later investment. This keeps time-to-value under pressure and can slow reference building for vendors when customers do not move quickly from initial rollout to full usage.

High Integration Complexity With Legacy Enterprise Systems

Legacy fragmentation is another durable restraint on the North America Integrated Workplace Management System (IWMS) market, especially in industrial, government, and other environments with older system estates. Planon's IDC-backed study found that 71% of organizations still use spreadsheets for real estate and facilities management, which shows how much workflow activity remains outside formal integrated systems. In government settings, the challenge is even more pronounced because real property, asset, and facility lifecycle requirements can depart sharply from commercial software reference models. As organizations add IoT sensors, BIM feeds, digital twins, and AI tools to existing environments, each extra layer introduces new dependencies that raise cost and delay returns. Middleware and open API strategies have improved interoperability, but they have not eliminated the problem across mixed-vintage building portfolios. The result is that many buyers still face a heavier transformation task than the software label alone suggests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Consolidation Keeps Solutions In The Lead

Solutions held 71.30% of the North America Integrated Workplace Management System (IWMS) market in 2025, indicating that large buyers still favor unified platforms over multiple point tools. This part of the North America Integrated Workplace Management System (IWMS) industry covers real estate and lease management, space and facilities management, asset and maintenance management, capital project management, workplace experience and analytics, and sustainability and ESG intelligence under one data model. The appeal is practical because disconnected tools need custom data handling before enterprises can generate portfolio-wide reporting. JLL reported that 69% of corporate real estate teams identified a single source of truth for space data as a 2026 priority, which supports the continued dominance of integrated solutions. Within the solutions stack, workplace experience and analytics have become among the most active areas, as companies need better visibility into peak-day demand under structured hybrid work.

Capital project management and sustainability modules are also gaining weight within the North America IWMS market as deferred renewal needs and reporting deadlines become harder to postpone. Gordian said in April 2026 that the higher education capital renewal backlog reached USD 156 per gross square foot in 2025, up 8% year over year, which supports stronger demand for project and lifecycle tools.[4]Gordian, “Capital Renewal Backlog Rises 8% In Gordian's 13th Annual State Of Facilities In Higher Education Report,” Gordian, gordian.com Services are projected to grow at a 16.84% CAGR through 2031, as implementation, integration, and managed support typically follow large platform deployments. The boundary between solutions and services is also becoming less clear as subscription models increasingly bundle rollout support, updates, and customer success into recurring contracts. That trend raises switching costs for incumbents, while also making long-term ownership costs more visible for buyers.

By Deployment: Sensitive Workloads Keep On-Premises Relevant

On-premises is projected to expand at a 15.27% CAGR through 2031, even though cloud held 66.80% of the North America Integrated Workplace Management System (IWMS) market share in 2025. This pattern does not signal a reversal of cloud preference. Instead, it reflects how government agencies, defense contractors, healthcare providers, and financial institutions continue to hold some building and occupancy data on controlled infrastructure. In these segments, buyers are increasingly selecting hybrid deployment models so that compliance-sensitive workloads remain private while less-sensitive workloads move to public cloud environments. That creates room for vendors that can support cloud, on-premises, and hosted private-cloud options without splitting the user experience.

Johnson Controls reported in 2026 that 63% of US university leaders planned to implement generative AI for operations and maintenance over the next year, adding another layer of architectural complexity, as building data often requires low-latency access. SAP's scheduled end of maintenance for HCM On-Premise at the end of 2027 is also pushing adjacent workload reviews that benefit IWMS vendors with stronger SAP cloud integration paths. Buyers in the North America Integrated Workplace Management System market are therefore not deciding between flexibility and control as separate goals. They are asking for both at the same time. Vendor differentiation increasingly depends on how well platforms can meet security and residency needs without giving up scalability or easier upgrades.

By Enterprise Size: SME Demand Strengthens As Entry Models Improve

SMEs are forecast to grow at a 17.41% CAGR through 2031, making them the fastest-growing size band in the North America Integrated Workplace Management System (IWMS) market. Large enterprises still held 62.70% share in 2025 because they have longer deployment histories, larger portfolios, and broader module usage. The growth is driven by improved pricing and packaging rather than by reduced demand among larger buyers. Vendors are increasingly using modular SaaS structures that let smaller customers start with space or maintenance management and add more capabilities over time. AI-assisted setup and pre-built connectors are also lowering the level of internal technical expertise needed for basic deployment.

This matters because many mid-sized operators still manage significant square footage, especially in multi-tenant properties, coworking facilities, and regional healthcare systems. Some of these organizations also face the same disclosure and audit requirements as larger companies, which reduces the value of waiting. In the North America Integrated Workplace Management System (IWMS) industry, SMEs are becoming a more active source of new customer additions than in earlier buying cycles. Services demand is often front-loaded in this segment because smaller firms rely on vendor-led rollout from the start. That pattern helps explain why services are growing faster than the core solutions layer, even while integrated platforms remain the main revenue base.

By End-User Industry: Healthcare And Life Sciences Sets The Fastest Pace

Healthcare and life sciences are projected to grow at a 19.12% CAGR through 2031, making it the fastest-growing end-user group in the North America Integrated Workplace Management System (IWMS) market. Information technology and telecom remained the largest vertical in 2025 because the sector operates dense, distributed office portfolios that benefit from centralized space and asset intelligence. Healthcare's faster expansion is tied to a more urgent mix of compliance, maintenance, and operational requirements. Hospital networks and pharmaceutical campuses need auditable records for safety and maintenance, controlled access to spaces, and coordinated facility oversight across broad physical footprints. Those needs make integrated systems more valuable as facility networks more complex.

BFSI remains a steady source of demand because lease accounting and physical security documentation continue to support real estate and asset management use cases. Government and public sector spending is also strengthening as modernization programs and deferred capital needs support larger facility system investments. Industrial manufacturing, retail, and e-commerce add another growth layer, since distribution and warehouse activity increases the importance of asset and maintenance workflows. The North America IWMS market is seeing higher service intensity in healthcare and government than in most commercial verticals, as those customers typically require more customization for audit trails, accreditation requirements, and identity management. That difference in deployment complexity is one of the clearest reasons services are outpacing solutions in CAGR terms.

Geography Analysis

The United States accounted for 78.20% of the North America Integrated Workplace Management System (IWMS) market in 2025 and remains the primary demand center for the region. This lead reflects the scale of the commercial real estate base, a mature enterprise software ecosystem, and stronger pressure to replace manual workflows with auditable platforms. Corporate headquarters density in the New York metro area and Silicon Valley supports faster replacement cycles as employers recalibrate office footprints for hybrid work. JLL reported that North America's actual-to-target utilization gap remained 18 percentage points in 2026, underscoring the need for investment in occupancy intelligence and space optimization tools. California's climate disclosure schedule is also making the United States the main commercialization zone for sustainability and ESG intelligence modules.

Canada is projected to grow at a 15.94% CAGR through 2031, the fastest rate in the region. Budget 2025 introduced the Build Communities Strong Fund, allocating CAD 51 billion (USD 37.4 billion) over 10 years for community infrastructure, including major building retrofits and climate adaptation work at postsecondary institutions. Gordian's 2026 higher education report adds another layer of support, as campus renewal backlogs remain large and continue to encourage investment in capital projects and asset lifecycle systems. Canadian technology occupiers in Toronto, Vancouver, and Montreal are also expanding structured hybrid programs, which support workplace experience and analytics demand.

Mexico remains the smallest of the 3 country markets, but it offers a longer-term growth path for the North America Integrated Workplace Management System market. Near-shoring is supporting industrial expansion in the Bajío corridor and in northern states tied closely to US supply chains. Demand is still led mainly by US and Canadian multinationals that need consistent asset and maintenance workflows across cross-border portfolios. That means Mexico's current opportunity is less about deep domestic IWMS penetration and more about greenfield facilities being equipped with modern cloud-based operating systems from the

Competitive Landscape

The North America Integrated Workplace Management System (IWMS) market has high competitive intensity, with a moderately concentrated top tier and a more fragmented mid-market. IBM, Planon Group B.V., MRI Software, Trimble Inc., and Eptura, Inc. compete across many of the same functional areas, but they differ in channel strategy, deployment flexibility, and ecosystem reach. IBM and Trimble benefit from broader enterprise software relationships, while Planon has leaned into co-sell and integration pathways through AWS Marketplace and SAP Solution Extension status. Eptura strengthened its position in April 2026 when it announced new AI workflows, real-time analytics, and a shared data foundation across workplace and facilities use cases. The same month, Eptura was named a Leader in the 2026 Gartner Magic Quadrant for Workplace Experience Applications, which supported its shift toward a broader worktech position.

Nuvolo is pushing a different route by building on the ServiceNow platform and using IT service management adjacency to expand into workplace and facilities workflows. That approach is especially relevant in healthcare and federal accounts where ServiceNow already has internal legitimacy and deployment history. Facilio is approaching the North America Integrated Workplace Management System (IWMS) market from a different angle, with AI agent layers that sit on top of incumbent systems rather than requiring a full migration. Its Atom Autonomous AI Agent Suite, launched in February 2026, was positioned to automate up to 40% of repetitive back-office facilities work across existing platforms. These strategies show that competition is widening beyond classic suite replacement and into augmentation, automation, and platform adjacency.

The launch of a dedicated platform for data center operators in March 2026 is another example of how vendors are targeting specialized operating environments rather than relying solely on broad, horizontal positioning. Continued Maximo positioning and AI expansion also support the view that predictive maintenance and energy management are becoming more central to vendor differentiation. Q1 2025 results showing USD 841 million in revenue and organic annualized recurring revenue growth of 17% point to sustained momentum in enterprise software activity that supports IWMS relevance. Across the North America Integrated Workplace Management System (IWMS) market, white-space opportunity remains strongest in the SME tier, where modular SaaS packaging and faster implementation paths are opening accounts that were previously priced out of full-scale adoption.

North America Integrated Workplace Management System (IWMS) Industry Leaders

Planon Group B.V.

MRI Software LLC

Trimble Inc.

Eptura, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nuvolo introduced Nuvolo AI, a connected data foundation for AI-driven automation spanning facilities operations and workplace management, directly embedded within its ServiceNow-native IWMS platform and targeting enterprise healthcare, government, and life sciences accounts.

- April 2026: Eptura, Inc. announced enhanced platform capabilities across workplace experience, asset management, and space planning, including AI workflows, real-time analytics, and a shared data foundation linking workplace and facilities information, the company will roll out the features through July 2026.

- April 2026: Eptura, Inc. was named a Leader in the 2026 Gartner Magic Quadrant for Workplace Experience Applications, a formal recognition of the company's shift from traditional IWMS positioning to a broader AI-backed worktech platform serving 25 million users in 115 countries.

- April 2026: Planon Group B.V. listed its Integrated Workplace Management Solution on the Amazon Web Services Marketplace, enabling organizations to apply existing AWS Enterprise Discount Program credits to Planon purchases and streamlining enterprise procurement through centralized cloud billing infrastructure.

North America Integrated Workplace Management System (IWMS) Market Report Scope

The North America Integrated Workplace Management System (IWMS) market refers to technology platforms that unify and optimize workplace operations by integrating core functions such as real estate and lease management, facilities and space management, asset and maintenance management, capital project management, workplace experience and analytics, and sustainability/ESG intelligence. These systems are delivered through cloud, on-premises, and hybrid deployment models, serving both large enterprises and SMEs across industries, including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The primary objective of this market is to enable organizations in the United States, Canada, and Mexico to improve operational efficiency, reduce costs, enhance employee and workplace experiences, ensure compliance, and leverage data-driven insights for strategic decision-making.

The North America Integrated Workplace Management System (IWMS) market report is segmented by Offering (Solutions, [Real Estate and Lease Management, Facilities and Space Management, Asset and Maintenance Management, Capital Project Management, Workplace Experience and Analytics, and Sustainability and ESG Intelligence] and Services), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (United States, Canada, and Mexico0. The Market Forecasts are Provided in Terms of Value (USD).

| Solution | Real Estate and Lease Management |

| Facilities and Space Management | |

| Asset and Maintenance Management | |

| Capital Project Management | |

| Workplace Experience and Analytics | |

| Sustainability and ESG Intelligence (embedded/overlay layer) | |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Offering | Solution | Real Estate and Lease Management |

| Facilities and Space Management | ||

| Asset and Maintenance Management | ||

| Capital Project Management | ||

| Workplace Experience and Analytics | ||

| Sustainability and ESG Intelligence (embedded/overlay layer) | ||

| Services | ||

| By Deployment | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

What is the size outlook for the North America integrated workplace management system (IWMS) space?

The North America Integrated Workplace Management System (IWMS) market was valued at USD 2.55 billion in 2025 and is forecast to reach USD 5.08 billion by 2031 at a 12.41% CAGR over 2026-2031.

Which segment leads spending by offering in North America?

Solutions led spending with a 71.30% revenue share in 2025, showing that buyers still prefer unified platforms over multiple point solutions.

Why is hybrid work still a major demand driver for IWMS platforms?

Structured hybrid work has created a wide gap between target and actual office utilization, which increases demand for occupancy analytics, reservation tools, and better space planning.

Which deployment model is growing fastest in the region?

On-premises is projected to grow at a 15.27% CAGR through 2031, mainly because regulated sectors still want tighter control over sensitive facility and occupancy data.

Which end-user group is expanding the fastest?

Healthcare and life sciences is projected to grow at a 19.12% CAGR through 2031 because hospital and pharma sites need stronger compliance, maintenance, and space controls.

Which country offers the strongest growth opportunity after the United States?

Canada is the fastest-growing geography with a projected 15.94% CAGR through 2031, supported by infrastructure investment, hybrid workplace adoption, and stricter data governance needs.

Page last updated on: