Cloud HCM Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

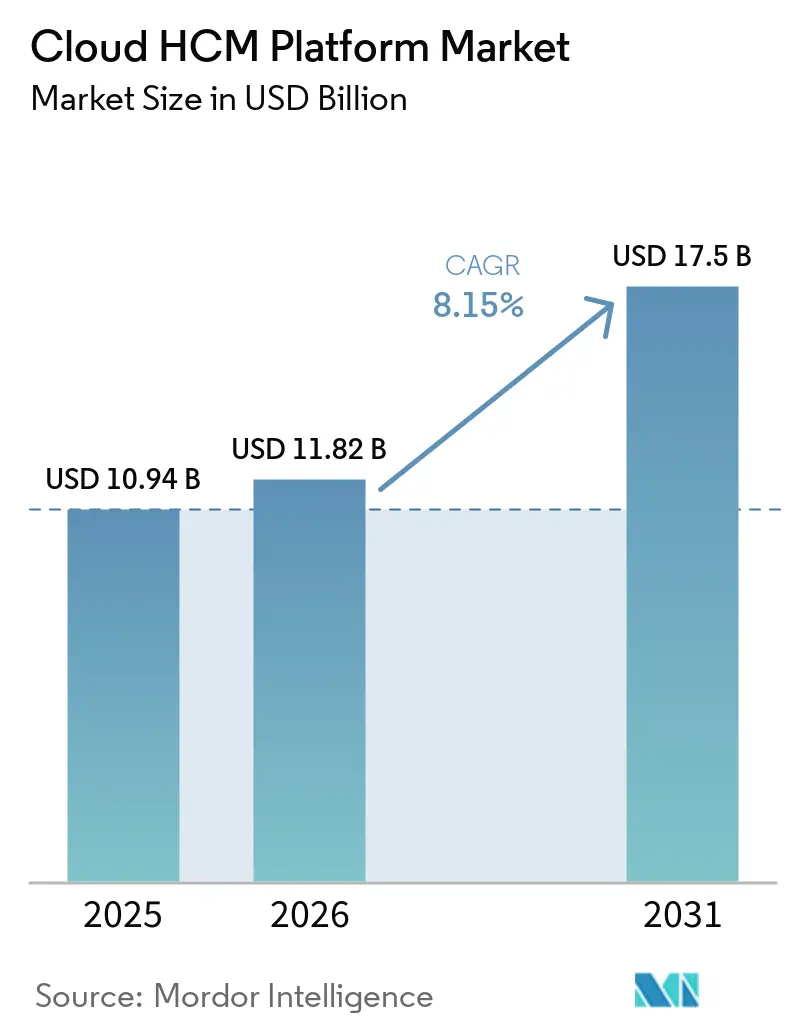

| Market Size (2026) | USD 11.82 Billion |

| Market Size (2031) | USD 17.5 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

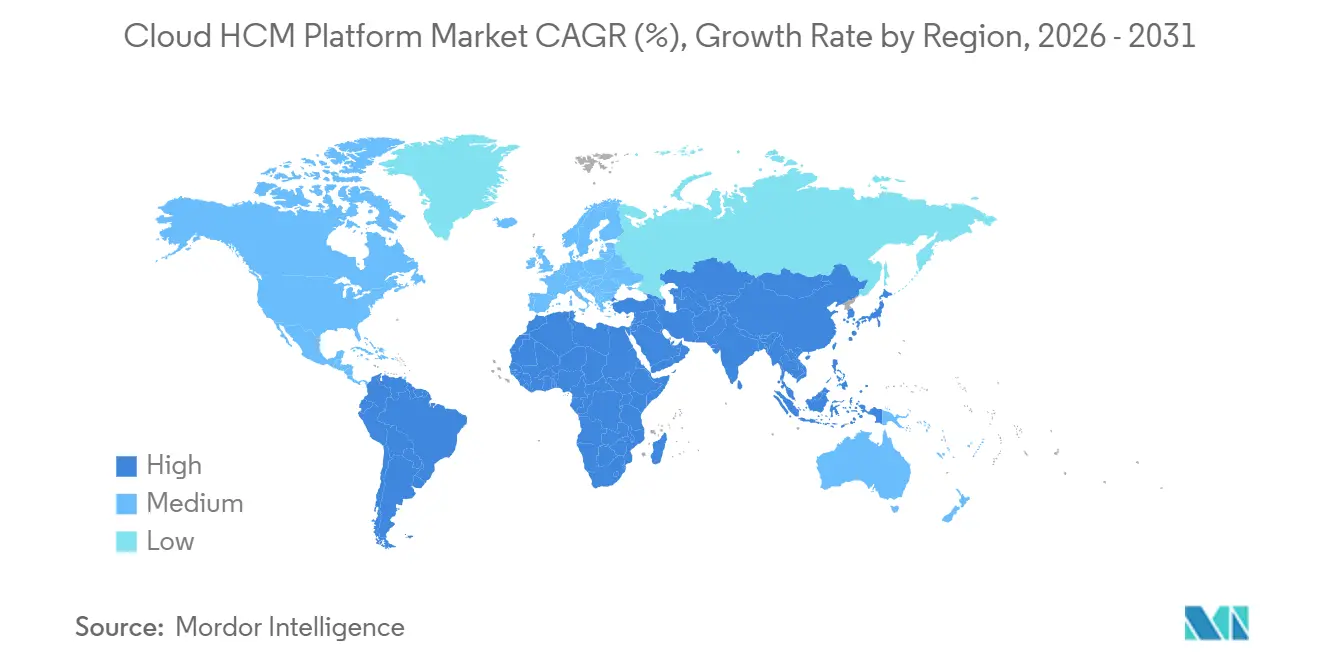

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud HCM Platform Market Analysis by Mordor Intelligence

The cloud HCM platform market size is expected to increase from USD 10.94 billion in 2025 to USD 11.82 billion in 2026 and reach USD 17.50 billion by 2031, growing at an 8.15% CAGR over 2026-2031. Enterprises are moving beyond basic HR record-keeping toward artificial-intelligence-driven talent platforms that surface real-time skills insights, automate workflows, and unify multi-country payroll. Government cloud-migration mandates, rapid adoption of generative AI copilots that cut HR workload by half, and intensifying payroll-compliance complexity are accelerating platform demand. Vendors that combine global payroll coverage, AI-powered skills intelligence, and low-code extensibility are capturing disproportionate share as buyers consolidate disparate HR tools into unified suites. Competitive strategies now hinge on embedding embedded analytics, pre-built industry accelerators, and partnerships that shorten deployment timelines while addressing data-residency rules.

Key Report Takeaways

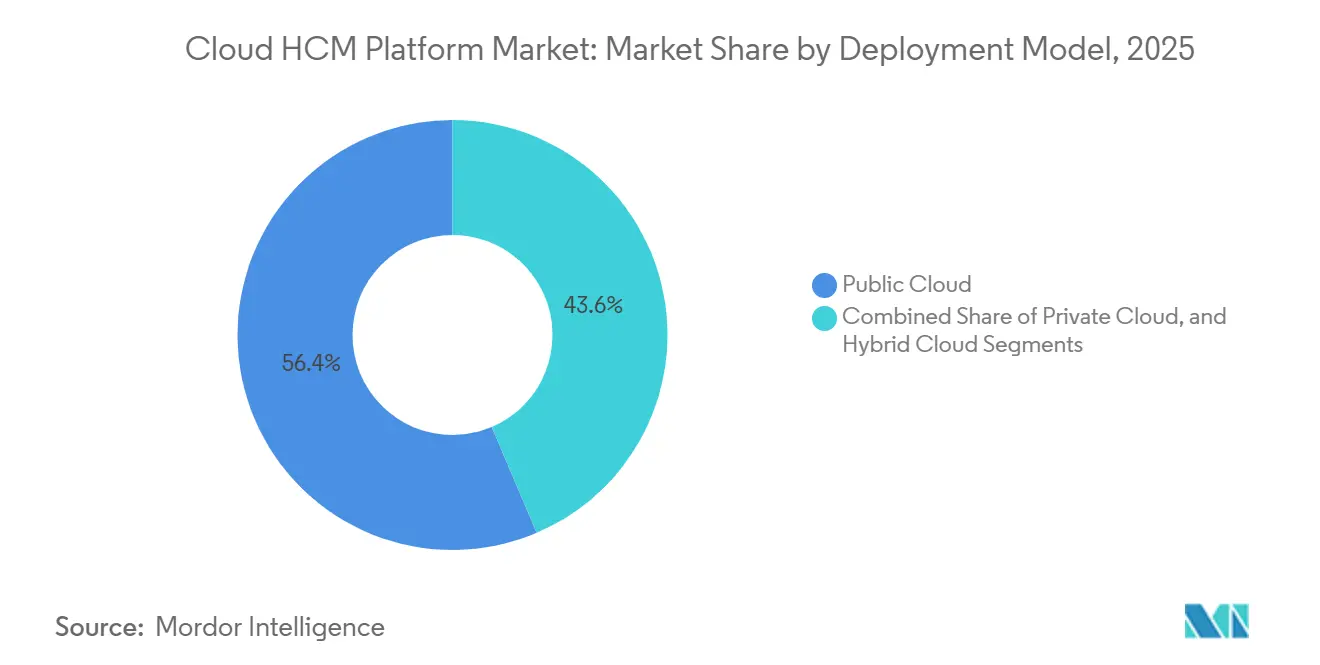

- By deployment model, public cloud held 56.41% of the cloud HCM platform market share in 2025, while hybrid cloud is expanding at a 10.64% CAGR through 2031.

- By organization size, large enterprises contributed 68.04% of 2025 revenue, whereas small and medium enterprises represent the fastest-growing cohort at an 11.02% CAGR.

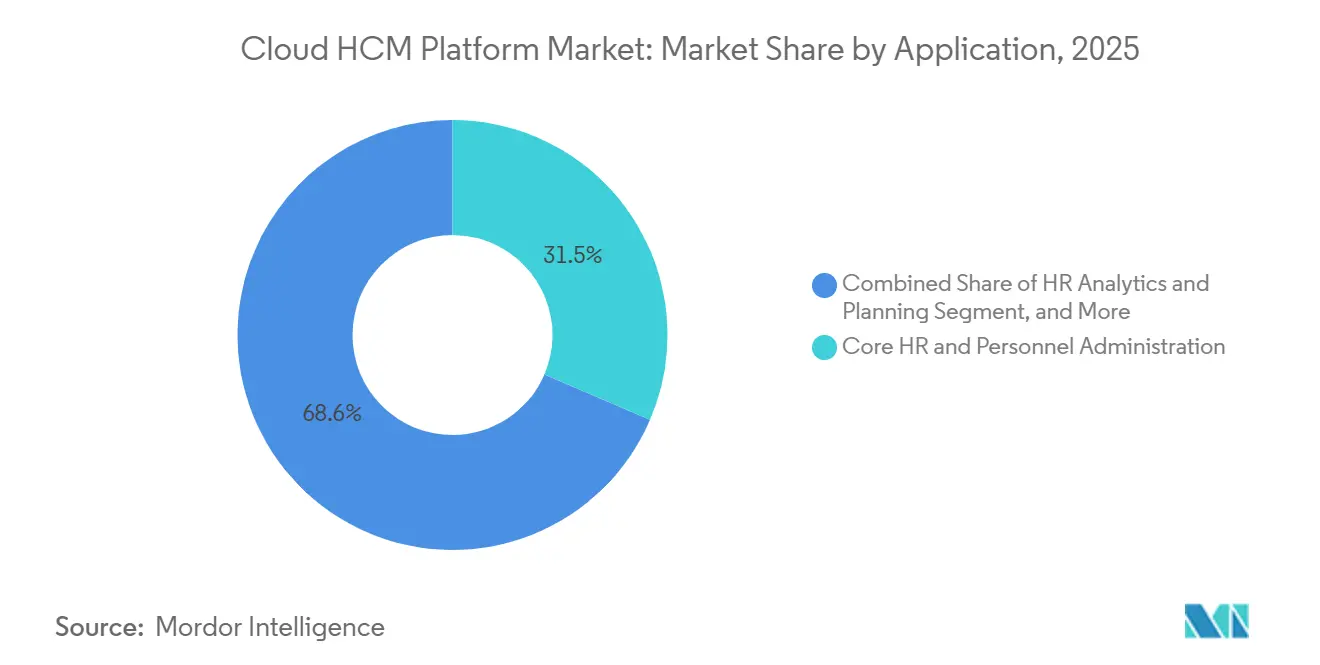

- By application, core HR and personnel administration led with 31.45% of 2025 revenue, and HR analytics and planning is projected to advance at a 9.81% CAGR through 2031.

- By industry vertical, IT and telecommunications captured 22.34% of 2025 revenue, while healthcare and life sciences is poised to expand at a 9.33% CAGR.

- By geography, North America accounted for 37.44% of 2025 revenue, and Asia-Pacific is forecast to grow at a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud HCM Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI-Driven Skill Mapping and Talent Intelligence | +2.1% | Global, early traction in North America and Western Europe | Medium term (2-4 years) |

| Rise of Skills-Based Workforce Planning in Large Enterprises | +1.8% | Global, concentrated in technology hubs across three regions | Medium term (2-4 years) |

| Integration of Generative AI Copilots Into HCM User Interfaces | +1.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Surge in Global Payroll Compliance Complexity | +1.4% | Global, acute in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Government Incentives for Cloud Migration of HR Systems | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of Industry-Specific Cloud HCM Accelerators | +1.0% | Global, vertical focus in four regulated sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI-Driven Skill Mapping and Talent Intelligence

Skill inference engines embedded in leading platforms now process billions of transactional datapoints to auto-tag employee capabilities, surface internal mobility paths, and shorten hiring cycles. Workday Skills Cloud alone analyzes more than 800 billion transactions annually, while SAP SuccessFactors Dynamic Skills framework lets organizations integrate third-party ontologies for niche roles.[1]Product Page, “Workday Skills Cloud,” Workday, workday.com Specialized partners such as Censia and Phenom claim 40% faster passive-candidate discovery versus keyword search, enabling employers to redeploy existing staff into skill-adjacent roles and cut recruiting costs by one-quarter. The effect is felt most in technology, professional-services, and financial-services companies where average skill half-life has dropped to 2.5 years, making dynamic talent intelligence a board-level priority.

Rise of Skills-Based Workforce Planning in Large Enterprises

Cisco’s 30 000-employee shift to skills-based planning and Merck’s enterprise-wide skills taxonomy show how competencies are replacing static jobs as the unit of workforce design. Research indicates skills-based organizations realize 98% higher high-performer retention and 52% faster ramp-up for new hires. Platforms respond by embedding skills ontologies and AI-driven gap analytics directly into core HR. SAP’s 2025 launch of Joule Studio enables HR teams to build custom agents that pinpoint skill gaps and recommend training without IT intervention. Manufacturing and healthcare firms that cross-train production or clinical staff report lower overtime and vacancy rates, although success depends on cleansing legacy data and validating taxonomies before go-live.

Integration of Generative AI Copilots Into HCM User Interfaces

Natural-language copilots are transforming employee self-service. SAP Joule now answers pay-statement queries in Germany, Netherlands, and Mexico, reducing HR tickets by 50%. Oracle auto-generates job descriptions and interview questions, Workday drafts performance reviews, and Microsoft Copilot for HR screens candidates and sequences onboarding tasks. Domain-specific fine-tuning on proprietary HR datasets improves accuracy over generic models. With 76% of North American HR teams planning AI adoption by 2027, vendors embedding secure, context-aware copilots gain a first-mover advantage.

Surge in Global Payroll Compliance Complexity

HCM suites now issue thousands of statutory updates annually to keep pace with divergent tax, labor, and social-insurance rules. SAP SuccessFactors delivered 2,000 legal changes across 104 countries in 2025 alone. Penalties for errors remain steep: payroll mistakes cost USD 291 per remediation and expose firms to litigation, driving demand for unified global payroll engines. Partnerships such as SAP and ADP’s 2025 alliance bundle localized templates covering 140 countries and shorten migrations to under 12 months. Asia-Pacific complexity, exemplified by China’s Personal Information Protection Law and India’s forthcoming data-protection bill, amplifies demand for compliant multi-country payroll.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency Legislation Increasing Localization Costs | -1.3% | Europe, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Persistent Integration Bottlenecks With Legacy ERP Stacks | -1.1% | Global, highest in mature ERP bases | Medium term (2-4 years) |

| High Total Cost of Ownership for Mid-Market Buyers | -0.9% | Global, 1 000-5 000-employee segment | Medium term (2-4 years) |

| Vendor Lock-In Concerns Limiting Long-Term Commitments | -0.7% | Global, pronounced in two mature regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Residency Legislation Increasing Localization Costs

GDPR and a patchwork of national sovereignty rules require in-country hosting, forcing vendors to duplicate infrastructure and support teams. China’s cybersecurity laws demand separate Chinese instances, while India and Indonesia contemplate similar mandates. Hybrid architectures, on-premises payroll with cloud talent modules, are emerging as cost-effective workarounds, yet dual licenses and complex data synchronization erode anticipated savings.

Persistent Integration Bottlenecks With Legacy ERP Stacks

Seventy-seven percent of large employers run HR data across multiple databases, with custom ERP configurations prolonging implementations. Middleware such as MuleSoft or SAP Integration Suite is often required, and compensation write-back errors can trigger costly payroll fixes. Organizations must budget up to 150% of first-year license fees for integration and testing, making coexistence architectures an attractive interim strategy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Reconcile Sovereignty and Scale

Public cloud accounted for 56.41% of the cloud HCM platform market in 2025, reflecting Workday’s multi-tenant SaaS model that delivers quarterly updates without on-premises hardware. Hybrid models hold growing appeal, expanding at a 10.64% CAGR as enterprises pair public-cloud talent modules with on-premises payroll to satisfy data-sovereignty statutes. Dual-license economics remain delicate, yet coexistence avoids the USD 6-12 million migration costs typical of large global rollouts.

Hybrid deployments increasingly rely on real-time connectors such as Oracle Human Data Loader and SAP Integration Suite, enabling daily synchronization while mitigating payroll-error risk. Third-party support firms offering discounted maintenance for legacy payroll further shift the cost-benefit calculus. Gartner expects 85% of enterprises to operate cloud-centered HR infrastructure by 2028, but regulated sectors will keep hybrid models for the long term. The cloud HCM platform market size for hybrid setups is therefore positioned to outpace overall growth as privacy mandates tighten.

By Organization Size: SMEs Accelerate Through Rapid, Low-Cost Adoption

Large enterprises held 68.04% revenue share in 2025, purchasing end-to-end suites spanning global payroll, analytics, and workforce management. SMEs, however, are growing at 11.02% CAGR, attracted to per-employee pricing that starts at USD 6 monthly and promises go-lives inside 90 days. The cloud HCM platform market size for SMEs is still small, yet rising quickly as lightweight suites bundle payroll, benefits, and time tracking to displace spreadsheets.

Vendors such as HiBob, Rippling, and Deel differentiate via intuitive mobile interfaces, IT-HR convergence, and embedded multi-country compliance. Despite tight budgets, 68% of SMEs prefer cloud deployments to avoid infrastructure costs, with 46% still citing implementation expense as a barrier. Freemium entry tiers and template-driven onboarding lower those hurdles, suggesting sustained double-digit SME adoption even as enterprise penetration plateaus.

By Application: Analytics Becomes the Fastest-Growing Workstream

Core HR led 2025 revenue at 31.45%, cementing its role as the employee-data backbone. HR analytics and planning is forecast to grow at 9.81% CAGR as leadership teams demand predictive attrition models and workforce-scenario planning. Platforms like Visier, Eightfold AI, and Workday Peakon embed no-code dashboards that surface KPIs without data-science skills. Use of the phrase cloud HCM platform market size beside granular application figures is limited to preserve accurate context.

Continuous-feedback performance modules, AI-curated learning paths, and automated onboarding workflows are folding into integrated suites, eliminating the swivel-chair experience of separate point solutions. Regulatory frameworks such as GDPR require explainability for algorithmic recommendations, driving vendors to publish transparency features that let employees review inputs used in talent decisions.

By Industry Vertical: Healthcare Surges on Compliance-Driven Scheduling Needs

IT and telecommunications captured the largest 22.34% stake in 2025, fueled by fast hiring cycles and skill-adjacent redeployments. Healthcare and life sciences is the fastest-growing vertical at 9.33% CAGR thanks to HIPAA-compliant shift management, clinical credentialing, and GxP-validated learning requirements. UKG’s nurse-scheduling engine, Oracle’s license-tracking workflows, and Workday’s labor-productivity analytics exemplify verticalized functionality.[2]Case Study, “Oracle Fusion Analytics,” Oracle, oracle.com The cloud HCM platform market share across regulated healthcare environments is therefore set to rise steadily through 2031.

Banking, manufacturing, retail, and government each apply unique labor rules, seasonal demand curves, or union constraints that off-the-shelf suites address through industry accelerators. Vendors that ship pre-configured compliance packs reduce implementation time and differentiate in crowded RFPs, underscoring the strategic value of vertical expertise.

Geography Analysis

North America generated 37.44% of 2025 revenue, anchored by high-value federal contracts such as the U.S. Office of Personnel Management’s USD 100 million Workday award and the Department of Energy’s USD 38 million Technology Modernization Fund-backed rollout. Canada and Mexico show steady uptake, supported by SAP Joule’s 2025 Spanish-language payroll explanations. Vendor dominance is stark: Workday, SAP, and Oracle influence over 95% of enterprise decisions at firms with more than 5 000 employees, with Workday leading new-buyer consideration surveys.

Asia-Pacific is the fastest-growing territory at a 10.27% CAGR. Darwinbox’s 9-times international revenue surge and Ramco Systems’ 150-country payroll reach illustrate home-grown vendors scaling beyond regional borders. Japan’s SmartHR leads domestic share with 70 000 tenants, while global providers must operate separate Chinese instances to comply with cybersecurity protocols, inflating localization costs. India’s impending data-protection law and Indonesia’s Regulation 71/2019 add to compliance complexity, steering buyers toward vendors with country-specific payroll modules.

Europe remains material despite slower expansion. GDPR and national sovereignty statutes compel in-country data centers, prompting Workday to commit EUR 175 million (USD 197 million) to an AI center in Dublin tailored for European customers. SAP’s deep integration with S/4HANA and localized payroll spanning 50-plus countries sustains traction in Germany and France, while Oracle’s E.ON win underlines growing acceptance in regulated utilities. South America, the Middle East, and Africa trail in absolute value yet gain momentum through government digitization mandates and mobile-first workforce management.

Competitive Landscape

Market concentration is moderate. Workday, SAP SuccessFactors, and Oracle Cloud HCM still dominate enterprise awards, but SME specialists such as BambooHR, Gusto, and Rippling gain ground through low-cost, rapid-deployment offerings. Workday’s USD 1.1 billion Sana acquisition folds knowledge-management search into its suite, easing employee self-service. SAP’s ADP alliance bundles global payroll templates across 140 countries, slashing migration roadmaps for multinational clients.

Oracle solidifies European reach with utilities wins and a Gartner Leader nod. Meanwhile, Darwinbox’s USD 140 million Series D and Challenger status highlight regional disruptors capturing emerging-market share with localized compliance engines.[3]Press Release, “Oracle Named Gartner Leader,” Oracle, oracle.com These developments highlight the dynamic nature of the market, where established players and emerging disruptors continue to shape the competitive landscape.

Strategic themes coalesce around AI-first product roadmaps, industry accelerators, and ecosystem partnerships that compress time-to-value. UKG’s Google Cloud pact embeds agentic AI in workforce management, Sage’s Criterion buy targets mid-market cross-sell, and Rippling’s IT-HR convergence appeals to remote-first firms. Vendors able to couple predictive analytics with transparent AI governance and global-payroll compliance will outperform laggards as buyers consolidate fragmented toolsets.

Cloud HCM Platform Industry Leaders

Workday, Inc.

SAP SE

Oracle Corporation

Automatic Data Processing, Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP released its 1H2026 Employee Central Payroll update, adding four AI-powered payroll agents that promise an 80% cut in payroll inquiries.

- November 2025: Workday expanded Workday GO for the mid-market and committed EUR 175 million (approximately USD 205 million) to an AI center in Dublin to meet European data-sovereignty needs.

- November 2025: Workday completed its USD 1.1 billion Sana acquisition, integrating generative search and knowledge management into Workday HCM.

- October 2025: Sage acquired Criterion, bolstering mid-market HCM capabilities in North America and Europe.

Global Cloud HCM Platform Market Report Scope

Cloud-native Human Capital Management (HCM) platforms are revolutionizing the HR landscape by consolidating functions like HR, talent management, payroll, workforce analytics, and employee experience into a single digital interface. Leveraging Software as a Service (SaaS) architectures, these platforms offer organizations of all sizes benefits such as continuous updates, reduced infrastructure costs, and effortless scalability. Many Cloud HCM solutions now come equipped with AI-driven insights, mobile accessibility, and self-service tools, all aimed at boosting workforce productivity and enhancing decision-making. The market's expansion is largely driven by modernization efforts, the rising demand for remote work solutions, and a notable pivot from traditional on-premise HR technologies.

The Cloud HCM Platform Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR and Personnel Administration, Payroll and Compensation Management, Talent Acquisition and Onboarding, Workforce Management and Time Tracking, Learning and Development, Performance and Succession Management, and HR Analytics and Planning), Industry Vertical (Banking Financial Services and Insurance, Healthcare and Life Sciences, IT and Telecommunications, Manufacturing, Retail and E-Commerce, Government and Public Sector, Education, Hospitality and Travel, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Core HR and Personnel Administration |

| Payroll and Compensation Management |

| Talent Acquisition and Onboarding |

| Workforce Management and Time Tracking |

| Learning and Development |

| Performance and Succession Management |

| HR Analytics and Planning |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| IT and Telecommunications |

| Manufacturing |

| Retail and E-Commerce |

| Government and Public Sector |

| Education |

| Hospitality and Travel |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Application | Core HR and Personnel Administration | |

| Payroll and Compensation Management | ||

| Talent Acquisition and Onboarding | ||

| Workforce Management and Time Tracking | ||

| Learning and Development | ||

| Performance and Succession Management | ||

| HR Analytics and Planning | ||

| By Industry Vertical | Banking, Financial Services and Insurance | |

| Healthcare and Life Sciences | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Government and Public Sector | ||

| Education | ||

| Hospitality and Travel | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the cloud HCM platform market size in 2026?

The market is valued at USD 11.82 billion in 2026, rising toward USD 17.50 billion by 2031, according to Mordor Intelligence.

Which deployment model is growing the fastest?

Hybrid cloud is advancing at a 10.64% CAGR through 2031 as firms balance data-sovereignty mandates with public-cloud scale.

Who are the leading vendors for large-enterprise buyers?

Workday, SAP SuccessFactors, and Oracle Cloud HCM dominate enterprise decisions, together influencing more than 95% of selections.

Why is Asia-Pacific the fastest-growing region?

Local vendors such as Darwinbox and Ramco, combined with expanding payroll compliance needs across diverse regulations, are propelling a 10.27% regional CAGR.

What role does generative AI play in cloud HCM platforms?

Copilots now draft job descriptions, explain pay statements, and summarize reviews, cutting HR inquiry volume by up to 50% and speeding self-service adoption.

Page last updated on: