HCM Software In Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

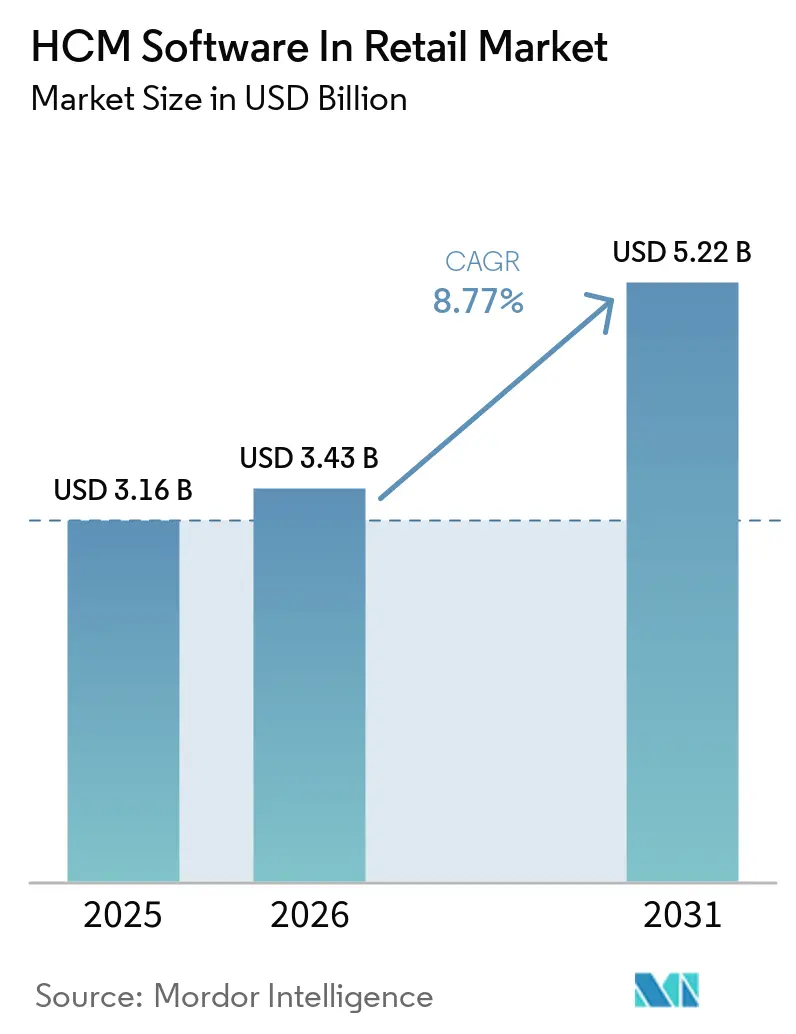

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 5.22 Billion |

| Growth Rate (2026 - 2031) | 8.77% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In Retail Market Analysis by Mordor Intelligence

The HCM software in retail market size is expected to increase from USD 3.16 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.22 billion by 2031, growing at a CAGR of 8.77% over 2026-2031. Cloud-first rollouts, AI-embedded scheduling and unified compliance dashboards are moving retailers away from stand-alone payroll engines and toward platform-based ecosystems. Vendors now bundle real-time labor analytics with point-of-sale data so that store managers can fine-tune staffing in half-hour windows, a capability increasingly critical for micro-fulfillment formats. Implementation partners are playing a larger role because multi-country wage, tax and privacy mandates require continuous configuration rather than one-time installs. Finally, headline risks around algorithmic bias and data breaches are forcing board-level scrutiny of HCM road maps, nudging buyers toward providers with transparent AI governance and tier-one cybersecurity postures.

Key Report Takeaways

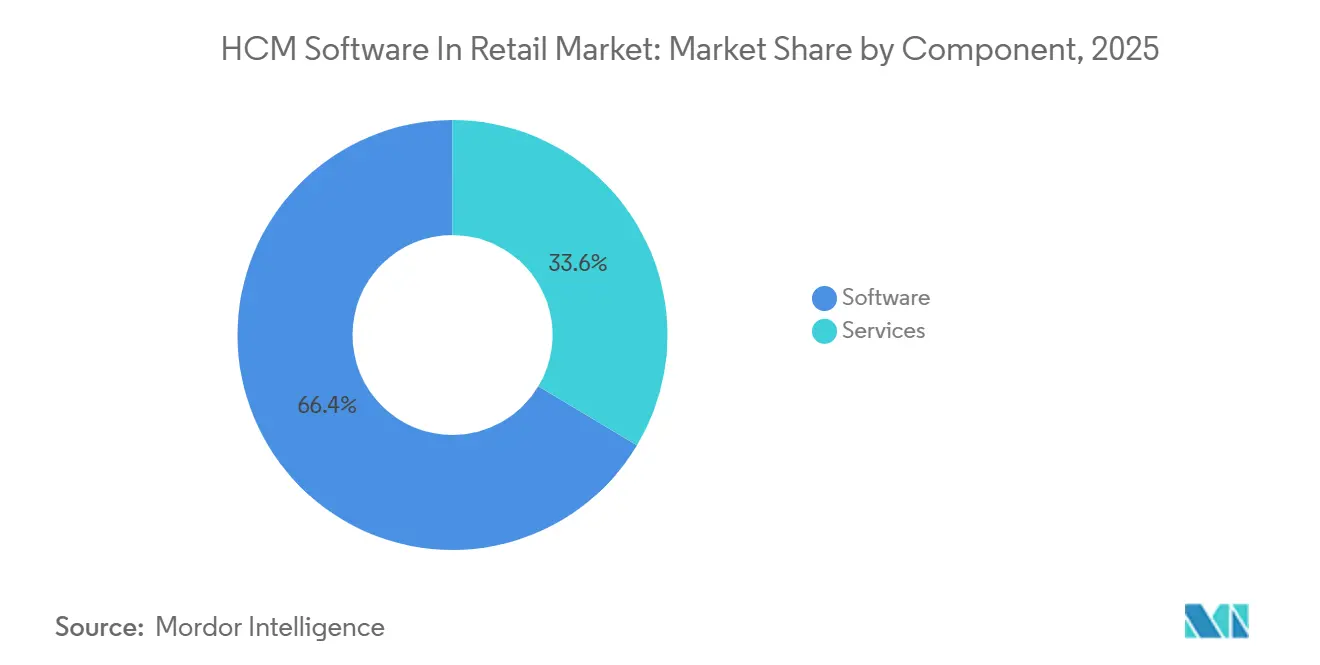

- By component, software led with 66.42% of the HCM software in retail market share in 2025, while services are advancing at an 11.01% CAGR through 2031.

- By deployment model, cloud held 54.11% revenue share in 2025, yet hybrid architectures are expanding at a 10.67% CAGR to 2031.

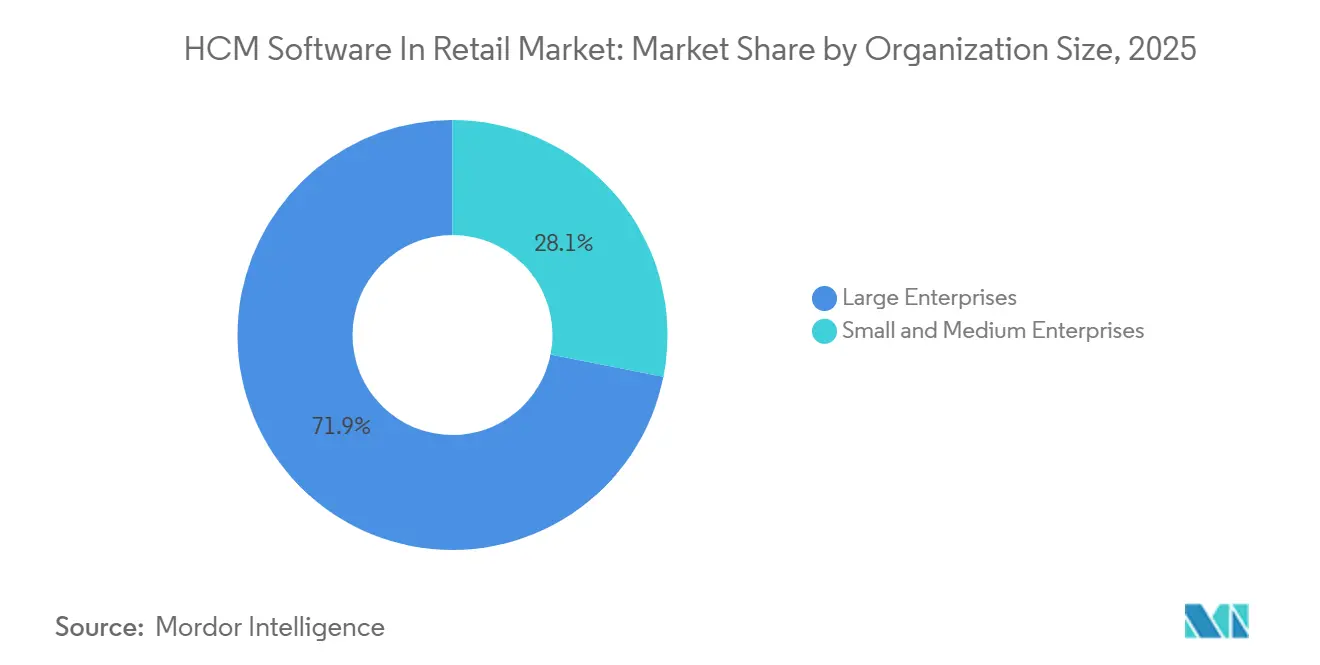

- By organization size, large enterprises captured 71.89% of 2025 revenue, whereas small and medium enterprises are forecast to grow at an 11.49% CAGR between 2026-2031.

- By function, payroll management accounted for 36.51% of the HCM software in retail market size in 2025, while learning and development is projected to accelerate at a 9.91% CAGR to 2031.

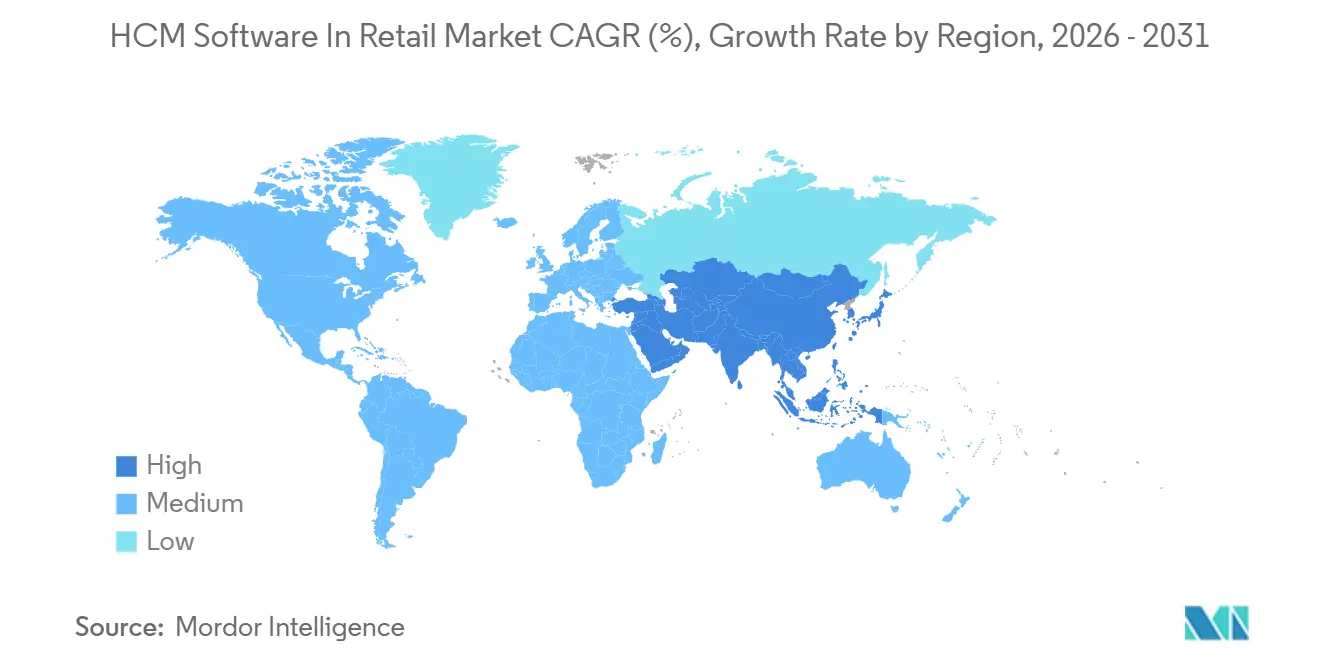

- By geography, North America dominated with 38.22% share in 2025, though Asia-Pacific is poised to post the fastest regional CAGR of 10.45% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Cloud-Based HCM Suites | +2.1% | Global, especially North America and Western Europe | Medium term (2-4 years) |

| Growing Focus on Mobile-First Self-Service HR Applications | +1.8% | Global, strongest in Asia-Pacific and urban North America | Short term (≤ 2 years) |

| Increasing Use of AI-Driven Workforce Analytics | +1.6% | North America and Europe core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Escalating Compliance Complexity Across Multi-State Retail Jurisdictions | +1.3% | North America and EU, emerging in Middle East and select Asia-Pacific markets | Long term (≥ 4 years) |

| Surge in Micro-Fulfillment Retail Formats Requiring Agile Labor Scheduling | +0.9% | Urban clusters in North America, Europe and Asia-Pacific | Short term (≤ 2 years) |

| Integration of HCM with Point-of-Sale Platforms Enhancing Store Productivity | +0.7% | Global, faster uptake in large-format retail and QSR chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-Based HCM Suites

Retailers are shifting capex-heavy on-premises systems to subscription-based cloud suites to access quarterly feature drops, embedded analytics and automatic legislative updates. Workday cited faster retail deal cycles in its January 2026 commentary, attributing momentum to chains seeking mobile time tracking and compliance dashboards without onsite IT overhead.[1]Workday Investor Relations, “Fiscal 2026 Third-Quarter Results,” workday.com Private equity’s USD 12.3 billion Dayforce take-private underscores investor conviction that multi-tenant SaaS economics outperform perpetual-license models. Mid-market adopters such as Belk unified payroll, benefits and scheduling across 300 stores after moving to Workday, eliminating legacy upgrade backlogs. Cloud vendors also shoulder liability for overtime and data-residency rules, an advantage as Hong Kong’s “468” overtime regime and the EU Pay Transparency Directive come online in 2026.

Growing Focus on Mobile-First Self-Service HR Applications

Smartphone apps are shrinking manager-mediated workflows by letting associates swap shifts, update availability and view pay slips on demand. Sona’s 2025 rollouts saved between 0.8%-4.0% of total payroll and returned 40 manager hours per week previously lost to manual schedule changes. Legion recorded 88% weekly active usage among frontline staff, cutting attrition by one-third thanks to real-time transparency. Geofenced clock-ins and biometric validation in isolved and Darwinbox apps curb time theft and support audit-ready attendance logs. Adoption trends skew toward Asia-Pacific, where CARSOME deployed Darwinbox’s mobile payroll across 3,000 staff in four countries by February 2026.

Increasing Use of AI-Driven Workforce Analytics

AI models are moving from pilots to production, informing attrition forecasts, shift optimization and skills gap analysis. An ETHRWorld Southeast Asia poll of 100 HR chiefs showed 75% already embedded AI in HR processes, with 65% budgeting higher 2026 spends for learning and recruitment modules. Checkr’s 2026 CHRO survey found 85% of retailers plan to infuse AI in hiring within 12 months, seeking faster screen-to-hire cycles. Workday’s pending USD 1.1 billion Sana acquisition will bake skills intelligence into its suite, turning static job profiles into dynamic capability maps. Still, the U.S. EEOC’s May 2023 guidance reminds employers they remain liable for discriminatory algorithms, keeping bias-testing on the C-suite agenda.

Escalating Compliance Complexity Across Multi-State Retail Jurisdictions

From U.S. predictive scheduling ordinances to Europe’s pay-equity audits, labor rules now change quarterly and differ city by city. TogetHR’s March 2026 review logged 50 unique overtime regimes that multi-state retailers must track, with six-figure fines for errors in California and New York. GDPR’s extra-territorial scope forces non-EU retailers to host staff data inside European borders and maintain consent trails for every cross-border transfer, complicating vendor selection VISTRA. Retail legal teams liken today’s environment to compliance whack-a-mole, elevating HCM configuration to a continuous risk-mitigation function rather than a set-and-forget module.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Risks in Employee Information Systems | -1.2% | Global, higher scrutiny in EU and North America | Short term (≤ 2 years) |

| High Cost and Complexity of Migrating Legacy HR Systems | -1.0% | North America and Europe where on-premises ERP depth is high | Medium term (2-4 years) |

| Algorithmic Bias Litigation Risk in AI Recruiting Tools for Retail | -0.6% | North America and EU, emerging case law in Asia-Pacific | Long term (≥ 4 years) |

| Seasonal Workforce Volatility Undermining ROI on Full-Suite HCM Investments | -0.5% | Global, acute in fashion, grocery and consumer electronics retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Risks in Employee Information Systems

Employee records house social security numbers, pay data and health details prized by cybercriminals. Workday’s August 2025 breach forced emergency patches across retail clients and reminded boards that HCM platforms sit on some of the most regulated personal data. GDPR fines can reach 4% of global turnover, so retailers operating in Europe now require vendors to store data within EU borders and document every transfer. The American Bar Association warns that adversarial inputs can manipulate AI screening bots, exposing companies to both hacking events and civil-rights suits in one incident.

High Cost and Complexity of Migrating Legacy HR Systems

Shifting payroll and benefits from on-premises ERPs to cloud suites can cost millions and disrupt wage runs if data cleansing, field mapping and parallel testing falter. Home Bargains’ 2025 migration spanned multiple fiscal years and required phased go-lives to protect bi-weekly pay cycles. SAP offers bridge options like H4S4 to let clients postpone a full cloud leap, but each path demands fresh licenses, HANA upgrades and interface rewiring.[2]SAP Community, “Hybrid SAP ERP HCM Options,” community.sap.com Many retailers therefore adopt hybrid strategies, cloud talent atop on-prem payroll, to spread risk and preserve sunk costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Speed as Execution Rules the Agenda

Services are expanding at an 11.01% CAGR through 2031, outpacing software’s dominant 66.42% share in 2025. The HCM software in retail market size for services reflects the reality that platform subscriptions only launch the journey; localization, testing and ongoing regulatory tuning now drive spend. Consulting majors such as Accenture, Deloitte and PwC integrate HCM rollouts into wider digital transformations, while boutique integrators specialize in statutory payroll for markets like Indonesia and Mexico. Software remains sticky because payroll engines are the system of record, yet functionality converges fast, pushing value creation into advisory and optimization layers. Rolling Arrays’ April 2026 commentary stressed that Southeast Asian clients judge providers on post-go-live discipline, not feature parity.

For retailers spanning 10-plus countries, services partners juggle localized tax tables, union rules and language packs, evolving into managed-service models that outsource payroll closing and compliance audits. IDC data show 60% of Asia-Pacific enterprises face operational disruption whenever regulators tweak labor codes, making SLA-backed support indispensable. Consequently, the HCM software in retail market increasingly values vendors able to package technology with regional service benches, a trend expected to deepen as EU pay-equity reports and U.S. fair-workweek laws proliferate.

By Deployment Model: Hybrid Paths Balance Ambition and Risk

Hybrid deployments are projected to grow at a 10.67% CAGR, eclipsing pure-cloud’s early glamour by reconciling modern talent tools with entrenched payroll databases. Many chains keep SAP or Lawson payroll on-prem but layer Oracle Recruiting, SuccessFactors Learning or Workday Skills Cloud on top, routing data via integration hubs that demand rigorous end-to-end testing. The HCM software in retail market share for cloud still leads at 54.11% in 2025 because SaaS eliminates patching and eases store roll-outs, yet ROI can erode when deeply customized overtime logic must be rebuilt on a vanilla SaaS stack.

Retailers weighing their journey assess whether workforce management is a differentiator or utility. If differentiator, they accept change costs for best-of-breed suites. If utility, they opt for core-hybrid bridges like SAP’s H4S4 that preserve payroll DNA while adding modern UX. Accenture cautions that hybrids require twice the test effort, as workflows cross system boundaries in every pay cycle. Still, this path lets risk-averse CFOs stage spend and upskill HR teams gradually, sustaining momentum without payroll failure headlines.

By Organization Size: SME Momentum Picks Up Pace

Small and medium enterprises are tracking an 11.49% CAGR, narrowing the functionality gap once reserved for big-box chains. Modular SaaS licensing and pre-configured compliance rules mean a 50-store apparel chain can now adopt scheduling AI once viable only for 1,000-store giants. Around 60% of European retail employment sits inside SMEs, highlighting untapped headroom. The HCM software in retail market size for SMEs remains below large-enterprise spend, yet growth velocity is higher because digitization starts from a lower base.

Asia-Pacific showcases this shift. GaiaWorks runs 1,800 retail brands on standardized templates, letting franchisees onboard in days. TeamLease helped a mid-tier Indian appliance retailer hire 25 frontline staff per month and automate leave and attendance, proof that out-of-the-box flows meet SME budgets. Vendors must therefore design upgrade paths so clients can add analytics, learning and talent modules as store counts rise, avoiding costly rip-and-replace cycles.

By Function: Learning and Development Climbs the Priority Ladder

Payroll still secured 36.51% of 2025 spend, reflecting non-negotiable statutory demands, but learning and development is accelerating at a 9.91% CAGR as retail pivots from cost control to capability building. The HCM software in retail market share for learning modules climbs because better-trained frontline associates convert browsers into buyers. YOOBIC cut onboarding time by 50% and lifted conversion by 22% for a specialty retailer, while Continu saved GoPro USD 1 million across 20 countries by unifying disparate LMS assets.[3]YOOBIC, “Retail Learning Platform Impact,” yoobic.com The growing adoption of learning modules underscores the retail sector's commitment to enhancing workforce efficiency and customer engagement.

Asian giants highlight this evolution. UNIQLO Singapore’s one-year Management Candidate program feeds store-manager pipelines, blending mentorship and skills frameworks tracked in the HCM suite. Litmos reports 40% higher engagement when micro-learning is mobile-first, aligning with a workforce that often skips desktop logins. As omnichannel fulfillment blurs store and warehouse roles, continuous learning helps staff flex between pick-and-pack, clienteling and social-commerce streaming, securing future-ready labor agility.

Geography Analysis

North America retained 38.22% of global revenue in 2025 due to sophisticated labor codes and early AI adoption. U.S. retailers grapple with 50 state wage laws plus city-level predictive scheduling, making compliance automation a board concern. Vendors respond with geo-coded rules engines and wage-theft alerts, features now standard in the HCM software in retail market. Algorithmic bias lawsuits also germinate here, injecting demand for explainable AI and fairness dashboards.

Asia-Pacific is the fastest riser at a 10.45% CAGR. India’s organized retail booms alongside Southeast Asia’s mobile-first workforce, while Chinese chains weave HCM directly into social-commerce and instant-delivery apps. ETHRWorld data show 65% of HR leaders in the region will boost AI budgets in 2026, yet only 11% feel fully prepared, opening doors for services partners. Government digitization pushes, such as Singapore’s Digital Workforce initiative, further accelerate cloud HCM uptake.

Europe’s growth rides on rule changes instead of store count expansion. The EU Pay Transparency Directive effective June 2026 forces every retailer above 100 employees to publish wage structures and justify gender pay gaps, a catalyst pushing the HCM software in retail market size upward as firms upgrade reporting pipelines. GDPR’s data-residency demands splinter vendor choices, favoring platforms with EU-hosted data centers. South America, the Middle East and Africa contribute smaller shares but show spotty high growth in urban corridors where international franchises replicate North American compliance playbooks.

Competitive Landscape

Competition is moderately fragmented. ERP stalwarts such as Workday, Oracle and SAP cross-sell HCM modules into their retail install bases, bundling payroll, skills clouds and analytics to lock in wallet share. Specialist players like Legion, GaiaWorks and Darwinbox carve niches with mobile-first scheduling, Asia-centric payroll and AI engines tailored for shift labor. Consulting majors wrap platform deployments inside larger digital agendas, capturing recurring optimization fees and raising switching costs.

Technology road maps converge on three battlegrounds. First, skills intelligence: Workday’s USD 1.1 billion Sana deal and SAP’s Joule AI announcement bet on dynamic capability maps over static job codes. Second, hybrid architecture: retailers want cloud talent atop on-prem payroll, yet only a few vendors offer certified integration kits with real-time sync. Third, bias governance: the Mobley v. Workday class action and EEOC guidance make algorithmic fairness tooling a must-have, steering buying toward vendors with transparent audit logs.

Disruptors unbundle suites with API-first niche tools, bias scanners, gig-shift exchanges, attrition predictors, that plug into incumbents. Incumbents counter by opening marketplaces, as ADP showed by migrating 50 SAP clients via joint templates in 12 months. Consolidation likely continues, but functional specialists will survive where they deliver clear ROI or regulatory shield. Overall, vendor scale plus tailored compliance capabilities define success in the HCM software in retail market.

HCM Software In Retail Industry Leaders

Automatic Data Processing, Inc.

Workday, Inc.

SAP SE

Oracle Corporation

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Workday closed its USD 1.1 billion Sana acquisition to embed AI-based skills graphs into its HCM suite, expanding personalized learning pathways for retail clients.

- November 2025: Thoma Bravo finalized the USD 12.3 billion Dayforce take-private, freeing the firm to accelerate product road maps outside quarterly earnings cycles.

- November 2025: Workday broadened Workday GO, a pre-configured package aimed at mid-market retailers seeking 90-day deployments and tiered pricing.

- October 2025: CARSOME rolled out Darwinbox across 3,000 Southeast Asian employees, winning a gold award for HCM innovation on go-live.

Global HCM Software In Retail Market Report Scope

HCM Software in the Retail Market encompasses digital platforms that oversee workforce scheduling, payroll, labor forecasting, compliance, and employee engagement across a network of stores. Retailers leverage these systems to manage high-volume, variable-hour staffing, optimize labor costs, and enhance operational efficiency. Today's solutions offer features such as AI-driven scheduling, mobile self-service, and real-time workforce analytics. The market's growth is propelled by the expansion of omnichannel retail, heightened compliance mandates, and a demand for agile labor management.

The HCM Software in Retail Market Report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Function (Payroll Management, Workforce Management, Talent Management, Core HR, Learning and Development, and Other Functions), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Payroll Management |

| Workforce Management |

| Talent Management |

| Core HR |

| Learning and Development |

| Other Functions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Function | Payroll Management | |

| Workforce Management | ||

| Talent Management | ||

| Core HR | ||

| Learning and Development | ||

| Other Functions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current HCM software in retail market size and its projected value by 2031?

The market stands at USD 3.43 billion in 2026 and is forecast to reach USD 5.22 billion by 2031, expanding at an 8.77% CAGR.

Which deployment model is growing fastest among retailers adopting HCM platforms?

Hybrid architectures are the fastest, projected to grow at a 10.67% CAGR as chains layer cloud talent modules over legacy payroll.

Why are learning and development modules gaining traction in retail HCM suites?

Retailers link frontline capability to sales conversion, with platforms like YOOBIC cutting onboarding time by 50% and lifting conversion by 22%.

What major regulation in 2026 is driving European retailers to upgrade HCM systems?

The EU Pay Transparency Directive effective June 2026 forces companies with 100-plus staff to publish and explain gender pay gaps.

How are small and medium retailers justifying HCM investments?

Modular SaaS pricing and pre-built compliance templates let SMEs digitize payroll and scheduling without large-enterprise budgets, supporting 11.49% CAGR growth.

Page last updated on: