Composable HCM Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.79 Billion |

| Market Size (2031) | USD 27.37 Billion |

| Growth Rate (2026 - 2031) | 20.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composable HCM Platform Market Analysis by Mordor Intelligence

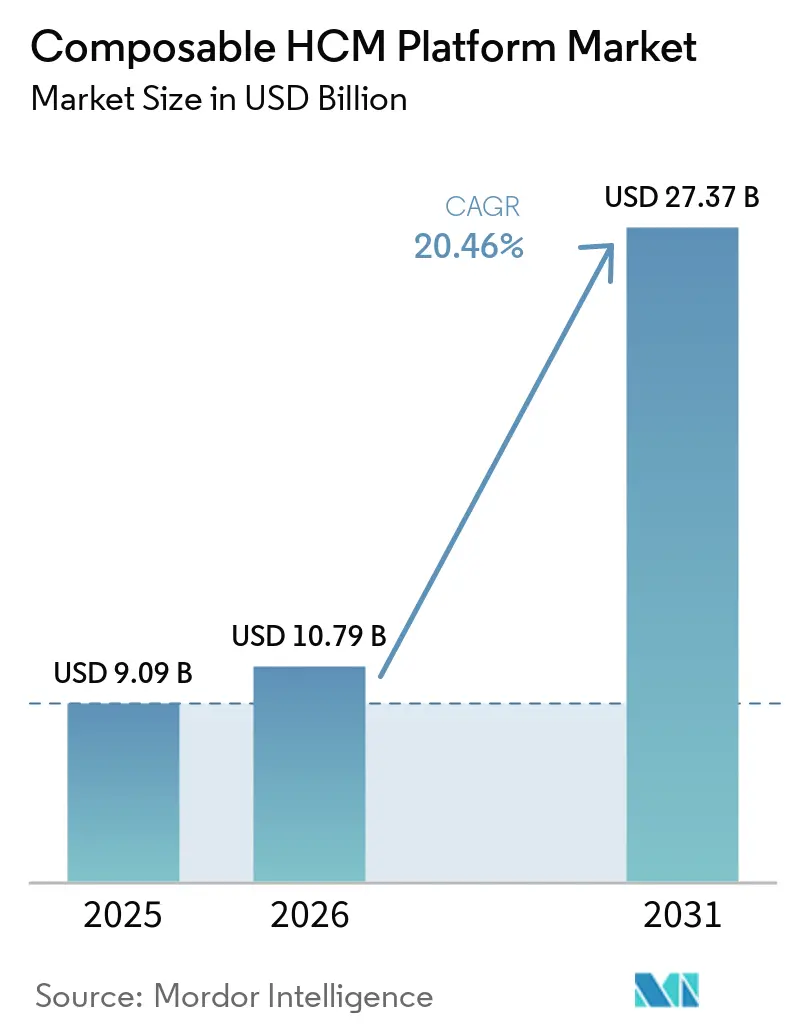

The composable HCM platform market size is projected to be USD 9.09 billion in 2025, USD 10.79 billion in 2026, and reach USD 27.37 billion by 2031, growing at a CAGR of 20.46% from 2026 to 2031. The composable HCM platform market is expanding as enterprises seek workforce systems that can be updated in parts, rather than replacing entire HR stacks when regulations, business models, or operating structures shift. Demand is also supported by the need to connect HR, payroll, finance, and workforce planning data in a governed environment that enables faster decision-making and fewer process gaps. Competitive activity is moving toward a three-tier structure in which established HR platforms protect their installed base, cloud-native vendors compete on extensibility, and payroll infrastructure providers move up into analytics and talent workflows. Regional data residency requirements in Europe and Asia-Pacific are increasing the value of localized cloud infrastructure, giving vendors with stronger regional delivery capabilities a clearer path into regulated accounts. The market is also gaining support from rising service demand, as implementation, integration, and ongoing configuration work are growing alongside platform adoption as organizations extend composable design across more HR processes.

Key Report Takeaways

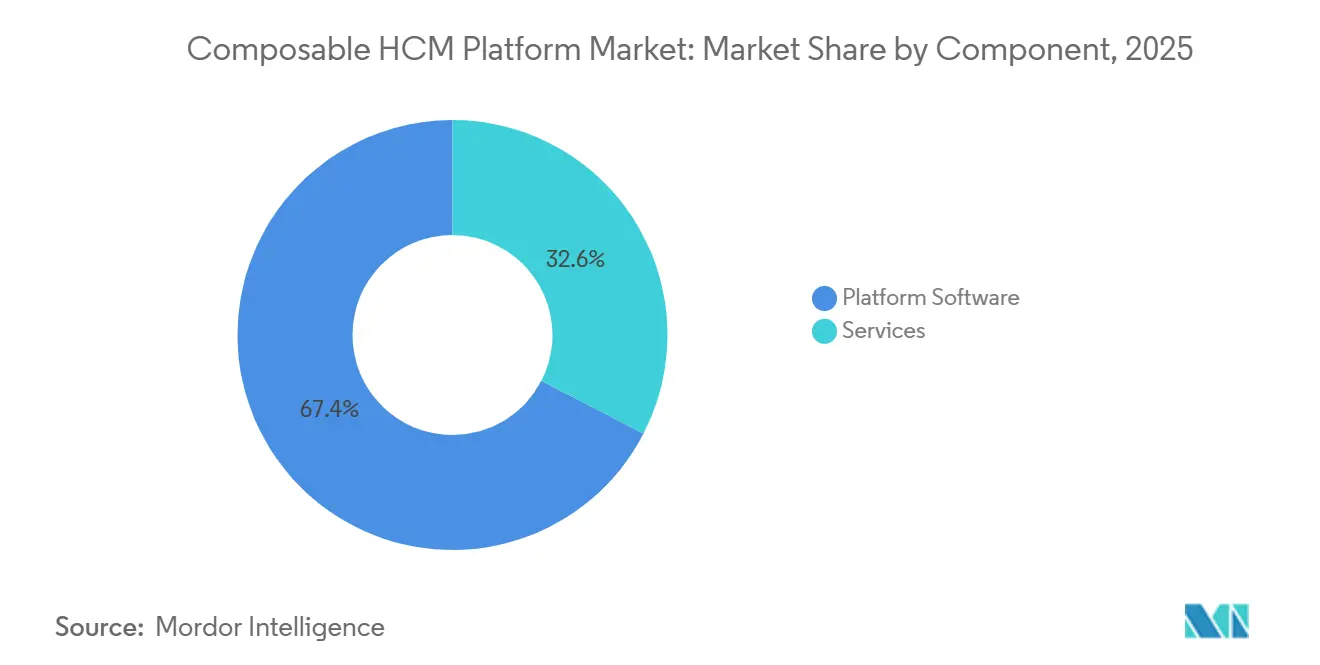

- By component, platform software accounted for 67.42% share of the composable HCM platform market in 2025, while services are projected to expand at a 20.66% CAGR through 2031.

- By deployment model, cloud-based deployment captured 72.18% of market revenue in 2025, while hybrid deployment is projected to grow at a 21.47% CAGR through 2031.

- By end-user enterprise size, large enterprises accounted for 60.83% of revenue in 2025, while SMEs are expected to expand at a 22.14% CAGR through 2031 in the composable HCM platform market.

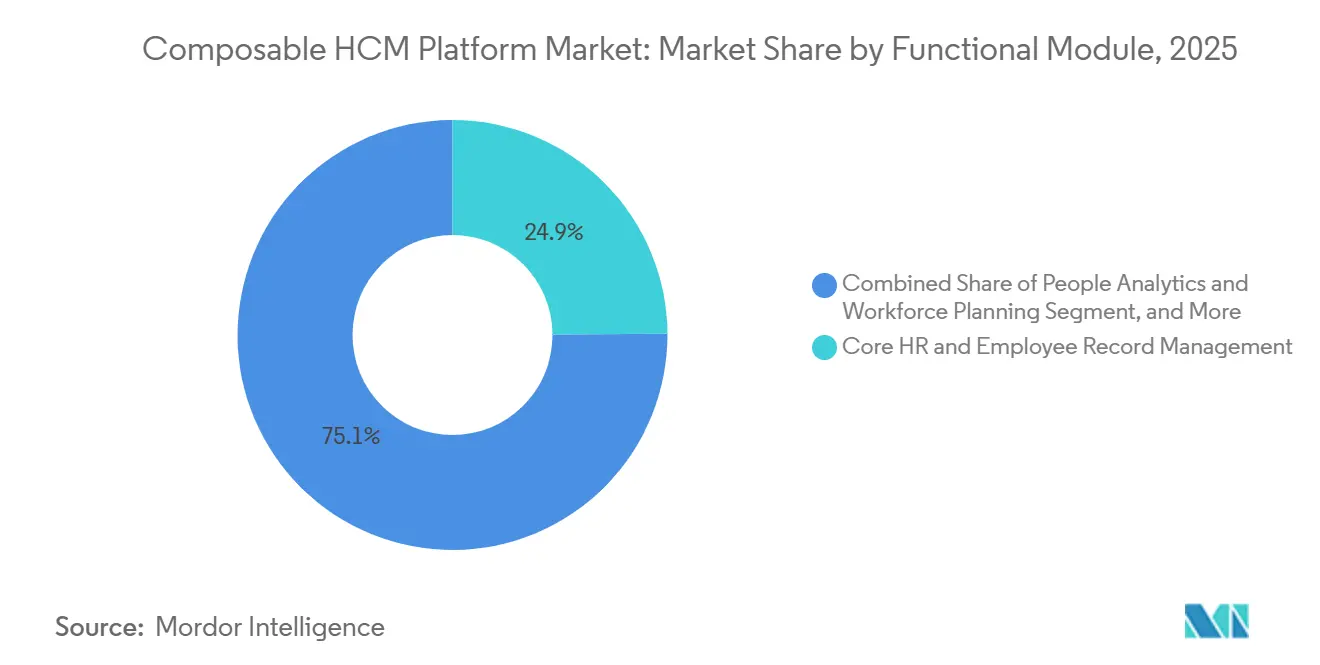

- By functional module, core HR and employee record management accounted for 24.91% of revenue in 2025, while workforce intelligence, analytics, and planning are projected to advance at a 23.68% CAGR through 2031.

- By end user industry vertical, information technology and telecom led with a 26.74% revenue share in 2025, while healthcare and life sciences are projected to expand at a 24.11% CAGR through 2031.

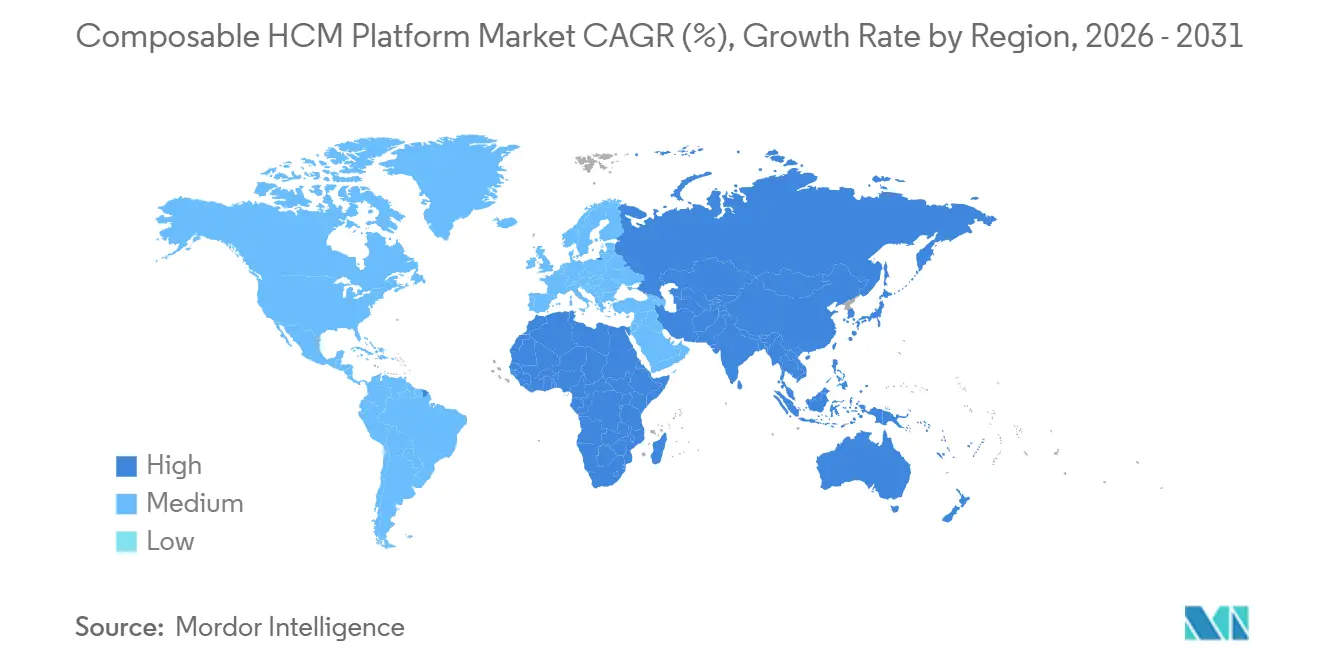

- By geography, North America held 39.86% of the composable HCM platform market share in 2025, while Asia-Pacific is projected to grow at a 24.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Composable HCM Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Cloud-Native Modular HR Architecture | +3.8% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Rising Demand for AI-Driven Workforce Planning and People Analytics | +3.4% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Multi-Country Payroll and Compliance Automation Needs | +2.9% | Global, with APAC and Europe as primary adoption zones | Medium term (2-4 years) |

| Frontline and Distributed Workforce Digitization | +2.3% | North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| EU Pay Transparency Readiness and Pay Equity Reporting | +1.9% | Europe, with spill-over to North America | Short term (≤ 2 years) |

| Low-Code Marketplace Extensions and Packaged HR Capabilities | +1.6% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Cloud-Native Modular HR Architecture

The composable HCM platform market is gaining traction because many enterprises no longer want HR systems that require full platform upgrades whenever one process changes. Older HR stacks often make each policy revision, compliance update, or analytics request more costly because every change touches multiple tightly linked systems. The composable HCM platform market benefits from the spread of microservices, API-first design, cloud-native delivery, and headless application architectures, enabling organizations to replace a single module without disrupting adjacent workflows. Workday moved in this direction in September 2025, when it launched Workday Build, which opened the company’s applications, data, and AI infrastructure to customer- and partner-built extensions directly on the platform. SAP SuccessFactors reinforced this direction in its 1H 2026 release by linking AI agents across recruiting, payroll, learning, and workforce administration through a more loosely coupled service model. As more enterprises modernize one module at a time, the cost and disruption of later HR changes tend to decline, strengthening the case for the composable HCM platform market over a longer adoption cycle.[1]Workday, “Workday Unveils Workday Build, Giving Developers the Tools to Build the Future of Work,” Workday Newsroom, newsroom.workday.com

Rising Demand for AI-Driven Workforce Planning And People Analytics

The composable HCM platform market is also being driven by a clear shift from static HR reporting to active workforce decision support. Organizations now want planning tools that can connect labor costs, headcount, skills, and operating outcomes in a single, governed environment rather than across disconnected systems. Workday’s general availability launch of Sana in March 2026 showed how leading vendors are building policy-aware AI agents that can complete multi-step HR and finance tasks from a single interface. SAP reported in May 2026 that 62% of C-suite executives were dissatisfied with how people data connects to business performance, indicating a real gap in current enterprise operating models.[2]SAP, “SAP SuccessFactors 1H 2026 Release,” SAP News Center, news.sap.com Demand is rising fastest in scenario planning and labor cost modeling, where companies want to test workforce options before making staffing decisions. Once this planning layer is adopted, the value of unified employee data rises quickly, which keeps the composable HCM platform market closely tied to advances in workforce intelligence.

Expansion of Multi-Country Payroll and Compliance Automation Needs

The composable HCM platform market is increasingly shaped by payroll complexity, as multi-country compliance has become harder to manage across fragmented systems. Enterprises are dealing with real-time tax enforcement, changing worker classification rules, and broader pay transparency obligations across multiple jurisdictions simultaneously. PayrollOrg reported in 2025 that 57% of global payroll professionals viewed local compliance as their biggest challenge, ahead of vendor management and process automation.[3]PayrollOrg, “Global Payroll Challenges and Compliance Priorities,” PayrollOrg, payroll.org Deel’s USD 300 million Series E round in October 2025, at a USD 17.3 billion valuation, reflected how much value investors now place on native payroll infrastructure that can scale across more countries. UKG added to this shift in May 2026 with Pro Pay and Workforce AI, which were designed to identify, analyze, and resolve payroll issues before they reach employees. The composable HCM platform market is therefore moving toward platforms where payroll accuracy and compliance automation are part of the core architecture rather than optional add-ons.

Frontline and Distributed Workforce Digitization

The composable HCM platform market is expanding beyond office-based workforces, as employers now need HR systems that can handle scheduling, attendance, onboarding, and payroll for distributed labor models. This need is particularly strong in sectors where work shifts change often, and managers need timely operational visibility. Vendors are responding with mobile-first and workflow-driven tools that connect time data more directly to payroll engines and manager approvals. Paychex expanded its workforce management offer in February 2026 with AI-enhanced scheduling capabilities, including automated approval of conforming timecards and exception-based review for managers. These product moves show that frontline digitization is no longer a side feature, because it often determines whether labor-intensive employers can turn HR data into usable operating control. As that data becomes part of the same system architecture, the composable HCM platform market gains a stronger foothold in sectors that previously relied on separate scheduling and payroll tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, AI Governance, and Algorithm Audit Burdens | -1.9% | Europe and North America | Short term (≤ 2 years) |

| Legacy HR and Payroll Migration Complexity | -1.5% | Global | Medium term (2-4 years) |

| Suite Vendor Marketplace Lock-In Risk | -1.2% | North America and Europe | Medium term (2-4 years) |

| Country-Level Payroll and Benefits Rule Fragmentation | -0.9% | Asia-Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, AI Governance, and Algorithm Audit Burdens

The composable HCM platform market faces a real constraint due to the governance burden associated with AI-based hiring, performance, and planning tools. Companies now have to document model logic, preserve audit trails, and maintain clear human oversight when automated systems influence employment decisions. This burden is especially strong in Europe, where the EU AI Act classified employment-related AI tools as high-risk applications and set documentation and conformity obligations before market placement.[4]European Union, “Regulation (EU) 2024/1689 Laying Down Harmonised Rules on Artificial Intelligence,” Official Journal of the European Union, eur-lex.europa.eu The composable HCM platform market, therefore, moves faster for vendors with mature compliance controls, as they can progress through procurement and legal review with less friction. Newer entrants may still offer strong AI functionality, but many face longer review cycles when buyers test security, governance, and explainability requirements. In regulated industries, governance readiness is becoming an early screening factor, which reduces the number of vendors that reach a detailed functional evaluation.

Legacy HR and Payroll Migration Complexity

The composable HCM platform market also slows when enterprises confront the practical difficulty of moving away from long-standing HR and payroll systems. Many large organizations still operate multiple platforms across payroll, benefits, time and attendance, talent management, and compliance, each with its own data model and embedded rules. Migration becomes harder when country-specific payroll logic was custom-coded years earlier and never fully documented. The result is that companies often underestimate project scope, which can delay go-lives, narrow implementation phases, or leave old systems running beside new ones for longer than planned. That outcome weakens the architectural value of the new platform because fragmentation continues at the integration layer. The composable HCM platform market will therefore continue to grow, but the pace of conversion from legacy estates will depend heavily on governance discipline and migration sequencing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Software Anchors Revenue As Services Scale Faster

Platform software accounted for 67.42% of revenue in 2025, keeping this part of the composable HCM platform market at the center of buyer spending. Enterprises prioritized the core layer first because API orchestration, low-code configuration, workflow control, and workforce data management determine how well the rest of the system can connect. Spending in this area also reflected a clear preference for integration-capable HR foundations rather than stand-alone point tools that add more interfaces. Within the software layer, core composable HCM platforms and API and integration orchestration platforms remained the most valuable sub-tiers because they set the interoperability ceiling for the full architecture. Marketplace and extensibility platforms also gained more attention as large employers sought pre-built business capabilities that shortened time-to-value across specific HR use cases.

Services remained smaller in 2025, but they are projected to grow at a 20.66% CAGR through 2031, indicating that the composable HCM platform industry is expanding beyond license revenue alone. The composable HCM platform market tends to drive greater service demand as implementations expand into a broader set of workflows and require more configuration support than internal HR teams can sustain. This pattern matters because implementation, advisory, and managed services often continue long after the initial software deployment. Workflow automation and process orchestration are helping expand this need since organizations increasingly want approval chains, compliance actions, and data flows configured without constant developer involvement. Over time, the revenue balance may still favor platform software, but service income should remain an important part of how vendors and partners participate in the composable HCM platform market.

By Deployment Model: Hybrid Deployments Narrow Cloud’s Lead

Cloud-based deployment accounted for 72.18% of revenue in 2025, making it the leading model in the composable HCM platform market. Buyers favored subscription-based infrastructure because it reduces capital spending and aligns upgrade cycles with vendor release schedules. Cloud adoption also aligned well with the market's modular design logic, since new components are easier to connect when vendors maintain a more consistent update rhythm. At the same time, on-premises deployment still has relevance in government, defense, and critical infrastructure environments where employee data and payroll processing are tightly controlled. These exceptions kept deployment choice tied to regulatory context rather than to architecture preference alone.

Hybrid deployment is projected to expand at a 21.47% CAGR through 2031, which makes it the fastest-growing model in the composable HCM platform market. Many enterprises prefer a phased approach in which regulated data remains on-premises while analytics, collaboration, and extensibility layers move to the cloud first. This pattern is especially relevant in Europe and the Asia-Pacific region, where country-specific residency rules can slow a full shift to public cloud. The composable HCM platform market is therefore not moving in a straight line from on-premises to the cloud, because hybrid structures offer a practical bridge for organizations dealing with migration risk and compliance constraints. As regional cloud infrastructure deepens, some hybrid users will move further toward cloud-only delivery, but hybrid should remain a durable choice through the forecast period.

By End User Enterprise Size: Large Enterprise Scale Anchors Revenue While SMEs Drive Faster Expansion

Large enterprises accounted for 60.83% of revenue in 2025, making them the largest players in shaping the composable HCM platform market. Their lead came from multi-country payroll demands, multi-entity employee record management, and the need to coordinate complex talent and compliance workflows through a single composable layer. In many cases, these buyers approached adoption as a multi-year architecture program that replaced siloed systems accumulated through growth and M&A activity. This spending concentration was not simply a budget effect, because organizational complexity itself increased the value of unified data governance and cross-module integration. Large enterprises, therefore, remained the highest-value customers, even though they also faced the most difficult implementations.

SMEs are projected to grow at a 22.14% CAGR through 2031, making them the most dynamic end-user cohort in the composable HCM platform market. Cloud-native vendors have lowered adoption barriers by packaging implementation templates, reducing the need for custom code, and allowing buyers to add modules in stages rather than all at once. Platforms such as HiBob, Personio, and Factorial HR helped move this model forward by making it easier for smaller organizations to begin with core HR and payroll, then extend into analytics or talent management later. This change matters because it broadens the addressable market for the composable HCM platform beyond enterprises with dedicated transformation teams. The composable HCM platform market is also seeing this acceleration below the 1,000-employee threshold, especially in APAC, where cloud-native deployment and preconfigured workflows are supporting faster adoption.

By Functional Module: Workforce Intelligence Moves Ahead Of Record-Keeping Priorities

Core HR and employee record management accounted for 24.91% of the composable HCM platform market in 2025, making it the largest functional module. This position served as the required data foundation for payroll, analytics, learning, and talent processes across the broader architecture. Without a governed employee master record, downstream modules cannot operate reliably, which is why buyers usually start here before expanding elsewhere. Payroll, compensation, and benefits remained the next-largest area because payroll accuracy and statutory obligations still carry direct operational and financial consequences. Talent acquisition and recruiting, along with talent management and internal mobility, formed the next tier as employers continued to prioritize hiring support and internal skills movement.

Workforce intelligence, analytics, and planning are projected to expand at a 23.68% CAGR through 2031, making it the fastest-growing functional area in the composable HCM platform market. Demand is rising because workforce data is now being used more directly in budget planning, staffing choices, and performance management rather than being stored mainly for reporting. Workday’s March 2026 launch of Sana showed how the category is shifting toward agentic workflows that connect business context, policy logic, and employee data in a more active decision layer. Workforce management and labor optimization, learning and workforce development, and employee experience and service delivery are also expanding as companies seek stronger coordination across scheduling, skills, and internal support processes. A smaller but structurally important area is workforce data fabric and employee identity management, because it determines how securely and accurately AI agents can operate across the composable stack.

By End User Industry Vertical: Healthcare And Life Sciences Outpaces Technology On Growth

Information technology and telecom led with a 26.74% revenue share in 2025, which gave the segment the largest position in the composable HCM platform market. This vertical benefited from high workforce complexity, stronger API governance maturity, and a larger installed base of remote and hybrid operating models that fit modular HR design. BFSI is another major user group because audit requirements, distributed sales structures, and variable compensation models create strong demand for connected workforce systems. Industrial manufacturing, along with retail and e-commerce, formed the next tier where frontline workforce control and compliance automation were the most practical adoption drivers. These patterns kept industry demand tied closely to where workforce coordination is both operationally difficult and financially material.

Healthcare and life sciences are projected to grow at a 24.11% CAGR through 2031, which makes it the fastest-growing vertical in the composable HCM platform market. The segment is being pushed forward by clinical staffing shortages, credential-based scheduling requirements, and tighter labor-cost oversight. In 2026, IHH Healthcare decided to unify HR, finance, and supply chain systems on Oracle Fusion Cloud across its multi-country operations, which reflects the scale of platform investment now moving into healthcare environments. Government and public sector adoption is also increasing, but at a more measured pace because data sovereignty rules, civil service compensation structures, and negotiated benefit frameworks require high levels of configurability. Other end-user industries, including logistics, hospitality, and utilities, are also moving into the composable HCM platform market as frontline productivity and retention become more visible management priorities.

Geography Analysis

North America accounted for 39.86% of the composable HCM platform market in 2025, making it the largest regional segment. The United States accounted for most of that demand because enterprises there were early adopters of API-first HR architecture and had a dense vendor ecosystem to support multi-module deployment. Large organizations in technology, financial services, and healthcare continued to connect core HR, payroll, analytics, and talent management within unified data structures, keeping the composable HCM platform market firmly anchored in the region. Canada gained momentum from growing interest in multi-provincial compliance automation, while Mexico saw demand driven by workforce digitization in manufacturing and distribution environments. This regional lead also reflected stronger cloud infrastructure penetration and greater willingness among enterprises to move away from legacy HR cores.

Asia-Pacific is projected to expand at a 24.89% CAGR through 2031, which makes it the fastest-growing geography in the composable HCM platform market. Growth is coming from rapid SME digitization in India and Southeast Asia, multi-country payroll modernization in Japan, South Korea, and Australia, and rising healthcare platform investment across the region. China remains important, but its path is shaped by localization rules that favor architectures with regional cloud deployment options. India is also seeing demand from technology services exporters and global capability centers that manage distributed workforces, while labor-intensive sectors are moving toward more connected HR operations. Tech Mahindra’s May 2026 partnership with UKG showed how APAC-based service and technology capabilities are increasingly influencing deployment patterns well beyond the region.

Europe is moving through a more compliance-driven expansion in the composable HCM platform market, with the June 7, 2026, transposition deadline under the EU Pay Transparency Directive pushing employers toward better job architecture and pay data infrastructure. Germany, the United Kingdom, France, the Netherlands, and the Nordic countries remain the main demand centers because they combine enterprise scale with stricter expectations around governed workforce data. South America is still an emerging geography, but Brazil stands out because its large enterprise base and complex payroll obligations create strong demand for compliance-linked payroll automation. The Middle East is also expanding, led by Saudi Arabia and the United Arab Emirates, where workforce nationalization programs are increasing the need for detailed workforce composition reporting. Africa remains at an earlier stage, but South Africa and Nigeria are moving faster as payroll complexity and multi-jurisdiction compliance needs create clearer use cases for modular HR infrastructure.

Competitive Landscape

The composable HCM platform market has a fairly concentrated top layer, led by vendors such as Workday, ADP, UKG, SAP SuccessFactors, and Dayforce, while the broader field remains fragmented across regional specialists, vertical platforms, and payroll infrastructure providers. Competition is increasingly centered on who can combine modular architecture with governed data, extensibility, and practical AI execution across real HR workflows. The composable HCM platform market is therefore not being shaped only by software breadth, because buyers are also evaluating API openness, marketplace maturity, payroll depth, and deployment flexibility. This has created visible separation between vendors defending large installed bases and challengers trying to win through faster configuration and stronger developer tools. It has also raised the importance of partnerships, local infrastructure, and post-deployment support as selection criteria.

Agentic AI became a defining point of competition across the composable HCM platform market in 2025 and 2026. Workday expanded this direction with Sana and its Microsoft 365 Copilot integration, which allows employees and managers to complete HR and finance tasks without leaving the Microsoft environment. SAP moved in parallel with 14 Joule Assistants and 42 specialized HR agents that connected payroll, recruiting, onboarding, and workforce planning in a more autonomous model. UKG also pushed the category forward with Pro Pay and Workforce AI, targeting payroll issue detection and resolution before errors affect employees. These moves show that the composable HCM platform market is shifting from simple workflow automation toward guided and goal-based task execution.

A second area of separation comes from data advantage and ecosystem reach across the composable HCM platform market. ADP’s position is strengthened by its access to a data estate of more than 41 million employee records through ADP Assist, which supports model training and operational refinement at a scale that newer challengers may struggle to match. Consolidation pressure is also rising, as shown by ADP’s integration of WorkForce Software capabilities into Workforce Now, Lyric HCM, and Global Payroll in late 2025. At the same time, white space remains in SME-focused deployments, country-specific compliance depth outside core Western markets, and workforce data fabric and identity management layers that still lack a single clear leader. Vendors that can combine modular deployment, compliance readiness, and durable partner ecosystems are likely to hold the strongest position as the composable HCM platform market matures.

Composable HCM Platform Industry Leaders

Workday, Inc.

UKG Inc.

Automatic Data Processing, Inc.

Dayforce, Inc.

Paycom Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP launched 14 Joule Assistants and 42 HR agents at Sapphire, introducing “Autonomous HCM” with AI-native payroll, recruiting, onboarding, and workforce planning.

- May 2026: Workday integrated its Sana agent into Microsoft 365 Copilot, enabling HR and finance tasks directly in Microsoft apps for 11,500+ organizations, including most of the Fortune 500.

- May 2026: Paychex unveiled its WISE AI platform, combining context-aware intelligence and autonomous execution across Flex, Paycor, and SurePayroll for workflows like scheduling and timesheet approvals.

- May 2026: UKG introduced Pro Pay with Workforce AI, featuring Payroll Analyst and Auditing agents to detect and resolve payroll errors in real time, targeting 2–4% payroll leakage.

Global Composable HCM Platform Market Report Scope

The Composable HCM Platform market refers to modular and API-driven human capital management solutions that allow organizations to flexibly assemble, integrate, and extend HR functionalities such as core HR, payroll, talent management, workforce optimization, learning, analytics, and employee experience. These platforms leverage workflow orchestration, low-code/no-code configuration, and workforce data fabric to deliver scalable, customizable, and intelligent HR ecosystems. Offered through cloud-based, on-premise, and hybrid models, they serve both large enterprises and SMEs across industries, including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The core purpose of this market is to provide adaptable, data-driven, and extensible HR systems that improve efficiency, compliance, and employee engagement while supporting organizational agility and digital transformation.

The Composable HCM Platform market report is segmented by Component (Platform Software, [Core Composable HCM Platforms, API and Integration Orchestration Platforms, Workflow Automation and Process Orchestration Engines, Low-code/No-code HR Configuration Platforms, Workforce Data Fabric and Intelligence Platforms, and Marketplace and Extensibility Platforms] and Services), Deployment Model (Cloud-based, On-premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functional Module (Core HR and Employee Record Management; Payroll, Compensation and Benefits; Talent Acquisition and Recruiting; Talent Management and Internal Mobility; Workforce Management and Labor Optimization; Learning and Workforce Development; Workforce Intelligence, Analytics and Planning; Employee Experience, HR Service Delivery and Workflow Automation; Integration and Workflow Orchestration and Workforce Data Fabric and Employee Identity Management), End-user Industry Vertical (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform Software | Core Composable HCM Platforms |

| API and Integration Orchestration Platforms | |

| Workflow Automation and Process Orchestration Engines | |

| Low-code/No-code HR Configuration Platforms | |

| Workforce Data Fabric and Intelligence Platforms | |

| Marketplace and Extensibility Platforms | |

| Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR and Employee Record Management |

| Payroll, Compensation and Benefits |

| Talent Acquisition and Recruiting |

| Talent Management and Internal Mobility |

| Workforce Management and Labor Optimization |

| Learning and Workforce Development |

| Workforce Intelligence, Analytics and Planning |

| Employee Experience, HR Service Delivery and Workflow Automation |

| Integration and Workflow Orchestration |

| Workforce Data Fabric and Employee Identity Management |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platform Software | Core Composable HCM Platforms |

| API and Integration Orchestration Platforms | ||

| Workflow Automation and Process Orchestration Engines | ||

| Low-code/No-code HR Configuration Platforms | ||

| Workforce Data Fabric and Intelligence Platforms | ||

| Marketplace and Extensibility Platforms | ||

| Services | ||

| By Deployment Model | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Functional Module | Core HR and Employee Record Management | |

| Payroll, Compensation and Benefits | ||

| Talent Acquisition and Recruiting | ||

| Talent Management and Internal Mobility | ||

| Workforce Management and Labor Optimization | ||

| Learning and Workforce Development | ||

| Workforce Intelligence, Analytics and Planning | ||

| Employee Experience, HR Service Delivery and Workflow Automation | ||

| Integration and Workflow Orchestration | ||

| Workforce Data Fabric and Employee Identity Management | ||

| By End user Industry Vertical | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the composable HCM platform space?

The composable HCM platform market was valued at USD 9.09 billion in 2025, stands at USD 10.79 billion in 2026, and is forecast to reach USD 27.37 billion by 2031 at a 20.46% CAGR.

Which deployment model leads today and which one is growing fastest?

Cloud-based deployment led with a 72.18% share in 2025, while hybrid deployment is projected to grow fastest at a 21.47% CAGR through 2031.

Why are enterprises moving toward composable HCM platforms?

Enterprises want modular systems that can adapt faster to payroll, compliance, analytics, and workflow changes without a full platform replacement.

Which company size group is driving the most demand?

Large enterprises led revenue with 60.83% in 2025 because they face greater cross-border payroll, multi-entity record, and workflow coordination complexity, while SMEs are growing fastest at 22.14% CAGR.

What functional area is seeing the fastest expansion?

Workforce intelligence, analytics and planning is expected to grow at a 23.68% CAGR through 2031 as organizations move from static reporting to real-time workforce decision support.

Which regions and verticals offer the strongest growth outlook?

Asia-Pacific is the fastest-growing region at a 24.89% CAGR, and healthcare and life sciences is the fastest-growing vertical at a 24.11% CAGR through 2031.

Page last updated on: