Multi-Country Payroll (MCP) Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

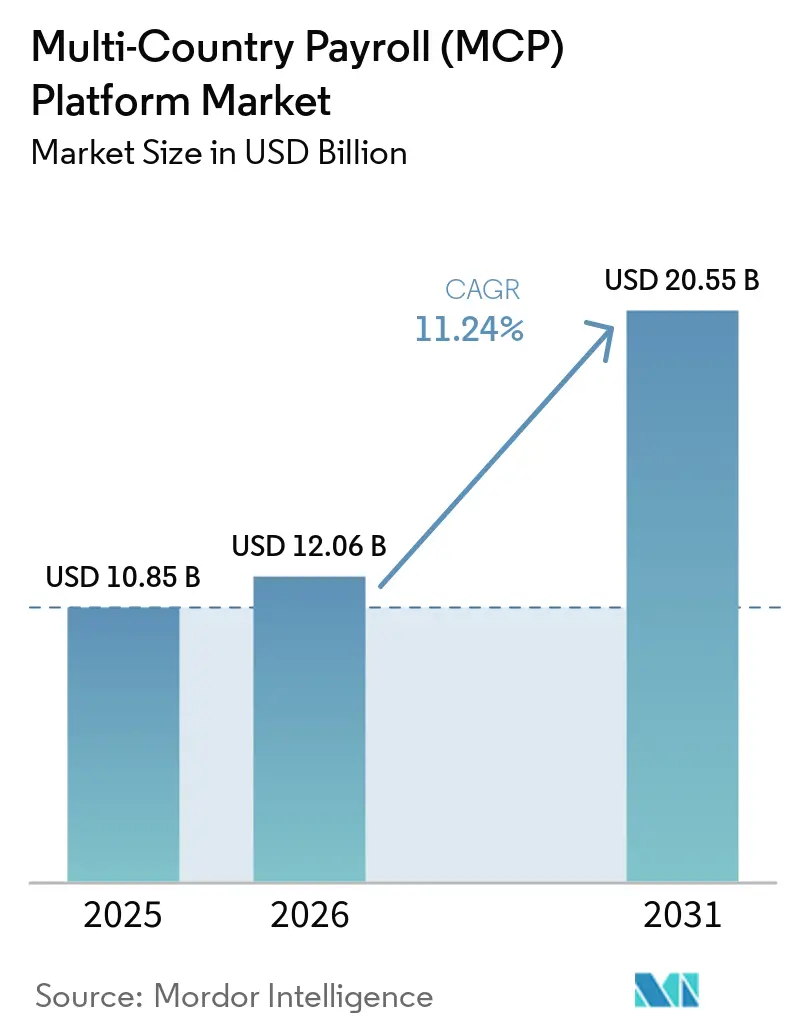

| Market Size (2026) | USD 12.06 Billion |

| Market Size (2031) | USD 20.55 Billion |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Country Payroll (MCP) Platform Market Analysis by Mordor Intelligence

The Multi-Country Payroll (MCP) Platform market size is projected to expand from USD 10.85 billion in 2025 and USD 12.06 billion in 2026 to USD 20.55 billion by 2031, registering a CAGR of 11.24% between 2026 to 2031. Demand is accelerating as enterprises retire on-premises payroll stacks that cannot meet real-time tax-reporting mandates already active in 44 jurisdictions. Cloud-native engines now synchronize statutory updates within hours, eliminating costly middleware and reducing penalty risk. Adoption is further propelled by hybrid and remote work models that fragment payroll obligations across multiple tax authorities, as well as by venture capital backing for AI-native platforms that promise zero-touch compliance. Platform consolidators are responding with an acquisition spree that fills geographic gaps and broadens compliance coverage while data-residency rules in Europe and Asia continue to shape deployment choices.

Key Report Takeaways

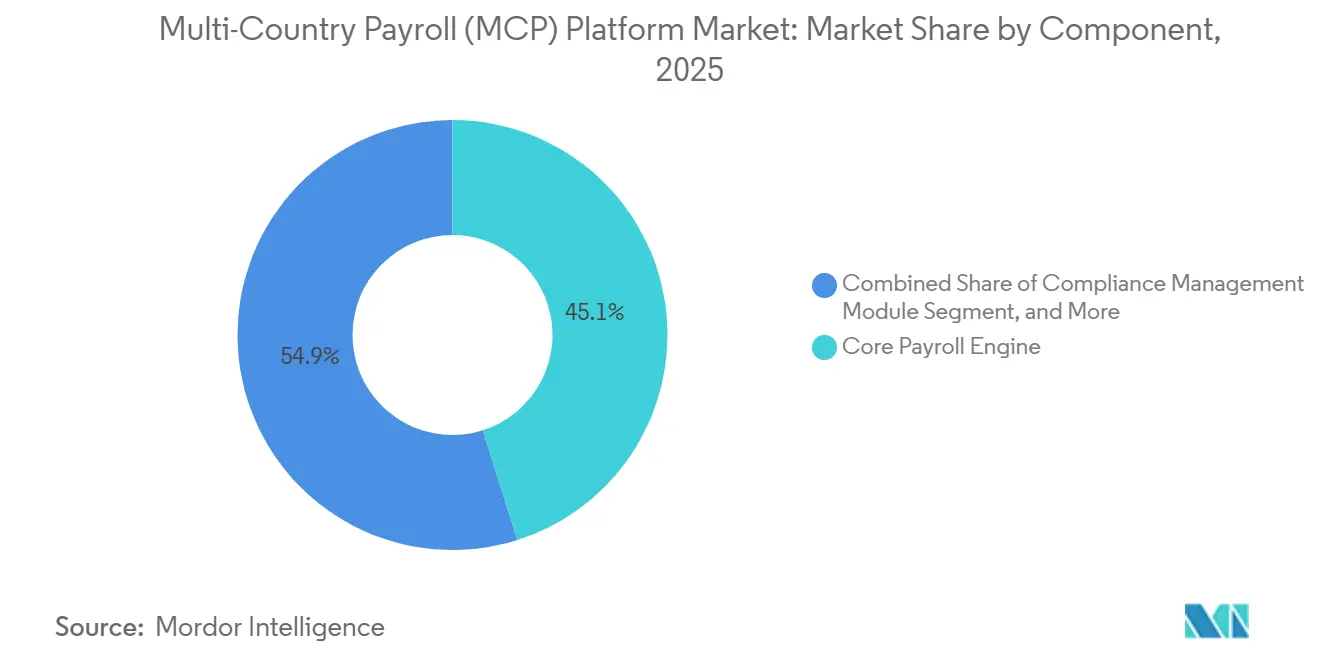

- By component, the Core Payroll Engine segment held 45.11% revenue share in 2025, while the Compliance Management Module is advancing at a 12.67% CAGR through 2031.

- By deployment model, Cloud-Based configurations accounted for 60.14% of 2025 revenue, whereas Hybrid deployment is on track for a 13.05% CAGR to 2031.

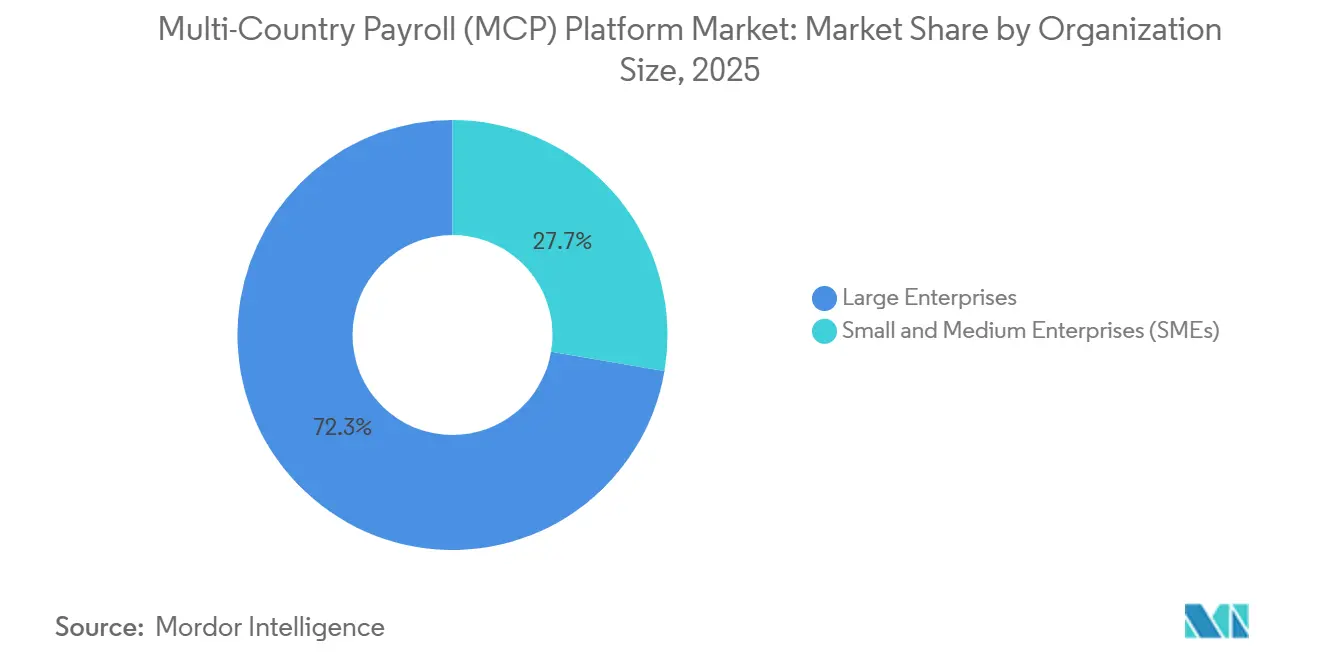

- By organization size, Large Enterprises commanded 72.33% of 2025 revenue, yet Small and Medium Enterprises are expanding at a 13.56% CAGR on the back of Employer of Record adoption.

- By end-user industry, IT and Telecommunication led with 33.61% revenue share in 2025, but Healthcare is forecast to post the fastest growth at an 11.98% CAGR through 2031.

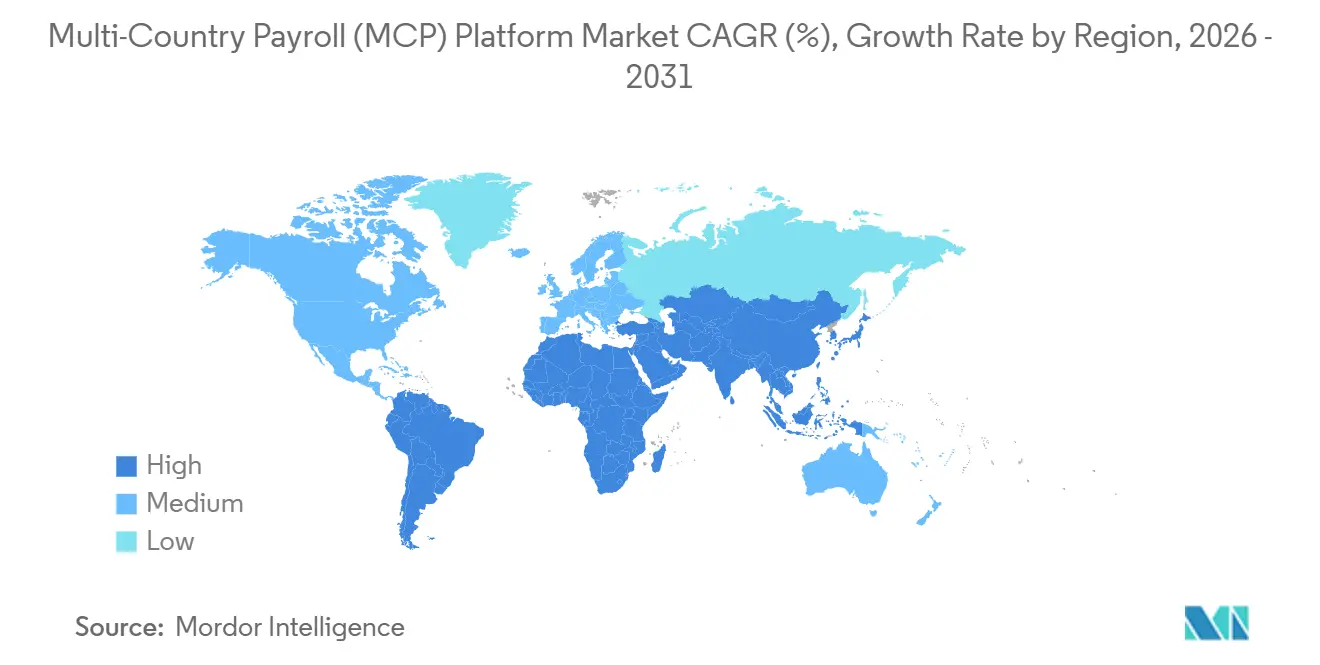

- By geography, North America captured 37.24% of global revenue in 2025, while Asia-Pacific is projected to register a 12.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-Country Payroll (MCP) Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift to Cloud-Native Global Payroll Engines | +2.8% | Global, with concentrated adoption in North America, Europe, and APAC tier-1 cities | Medium term (2-4 years) |

| Growing Compliance Complexity from Real-Time Tax Reporting Mandates | +3.1% | Europe, South America, APAC, Middle East | Short term (≤ 2 years) |

| Expansion of Global Hybrid and Remote Workforces | +2.4% | Global, highest in advanced knowledge hubs | Medium term (2-4 years) |

| Digitization of Employer of Record Models Among SMEs | +1.9% | North America, Europe, APAC, spillover to Middle East and Africa | Medium term (2-4 years) |

| Integration of Payroll Data with Workforce Analytics Platforms | +1.2% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Venture Capital Funding Spree into Payroll-as-a-Service Startups | +0.9% | Global funding centered in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift To Cloud-Native Global Payroll Engines

Cloud-native payroll separates compute from storage, allowing companies to burst capacity during peak pay cycles without hardware upgrades. Early movers report 60% cuts in processing time after adopting API-first architectures that link payroll directly with general-ledger and workforce-management modules.[1]ADP, “ADP and SAP Announce Strategic Partnership,” ADP.com Single-tenant designs host country-specific logic as micro-services, trimming total cost of ownership by up to 40% relative to legacy suites. Continuous delivery lets vendors push tax-rule updates without client downtime, while zero-trust security frameworks meet strict data-sovereignty mandates. Financial institutions and healthcare providers, however, must weigh interoperability clauses in the EU Data Act that may erode switching costs and intensify price competition.

Growing Compliance Complexity From Real-Time Tax Reporting Mandates

Real-time reporting has turned payroll into a continuous compliance stream. The OECD framework effective January 2025 obliges employers to transmit pay data within 48 hours, exposing gaps in systems that rely on batch validation. Poland’s KSeF and France’s forthcoming e-invoicing rollout extend structured XML and digital-signature demands to payroll-related documents. Brazil’s eSocial now cross-checks employer filings against individual tax returns in real time, flagging errors within days. These shifts fuel demand for Compliance Management Modules that ingest updates via government APIs and auto-adjust gross-to-net logic without human touch.

Expansion Of Global Hybrid And Remote Workforces

Roughly 23.4% of the U.S. workforce was fully remote in 2025, and 37% of global employees expressed readiness to work from another country if policies allowed. Digital-nomad visas introduced by 65 nations have different income floors and residency triggers, forcing employers to apportion salary across multiple tax codes. Modern platforms reconcile time-tracking feeds with jurisdiction-specific engines, ensuring accurate withholding even when staff rotate between Portugal, Spain, and the United States within one fiscal year. The demand is most visible in IT and Telecommunication, where distributed teams are the norm and payroll must integrate with project-level cost accounting.

Digitization Of Employer Of Record Models Among SMEs

Employer of Record arrangements let SMEs hire abroad without opening entities, boosting the service’s global value to USD 7.45 billion in 2026. Venture-backed providers like Deel and Globalization Partners bundle EoR with cloud payroll, enabling a 53% SME adoption share. AI-first challengers such as Niural and Central automate statutory ingestion for zero-touch processing, compressing onboarding from weeks to days. Regulatory ambiguity still clouds markets like India and China, but the model’s variable-cost structure remains attractive for fast-growing SaaS and professional-services firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Data Residency and Cross-Border Privacy Concerns | -1.8% | Europe, China, India, Russia, Brazil | Short term (≤ 2 years) |

| High Switching Costs From Legacy Enterprise Resource Planning Payroll | -1.4% | North America, Europe | Medium term (2-4 years) |

| Scarcity of Localized Banking Rails in Emerging Economies | -0.7% | Sub-Saharan Africa, parts of South America, Southeast Asia | Long term (≥ 4 years) |

| Limited Awareness Outside Tier-1 Multinationals | -0.5% | Middle East and Africa, secondary APAC cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Residency And Cross-Border Privacy Concerns

GDPR fines reached EUR 2.92 billion (USd 3.44 billion) in 2024, underscoring enforcement intensity. India’s DPDPA restricts outbound data flows unless destination countries clear adequacy checks, prompting vendors to add local data centers. China’s PIPL tags payroll processors for state-owned companies as critical operators, mandating annual security audits. Russia’s Federal Law 152-FZ led some Western vendors to exit, while Brazil’s LGPD enforces GDPR-like consent terms. These fragmentary regimes inflate infrastructure costs and slow rollouts of new country coverage.

High Switching Costs From Legacy Enterprise Resource Planning Payroll

Migration from SAP, Oracle, or Workday payroll can exceed USD 5 million for a 10,000-employee firm, including dual-run periods that double administrative effort. Integrated data models linking payroll with benefits, talent, and finance modules raise reconciliation risks when decoupled. Change-management burdens, from training to remapping journals, delay return on investment, causing large enterprises to adopt a wait-and-see stance even as SMEs leapfrog to pure-cloud stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Compliance Modules Outpace Core Engines

In 2025, core engines generated the largest slice of the Multi-Country Payroll (MCP) Platform market share at 45.11%, affirming their central role in gross-to-net calculations. Real-time mandates now elevate compliance modules, which are recording a 12.67% CAGR through 2031 as clients demand automatic ingestion of statutory changes. The MCP Platform market size for compliance software is swelling because tax agencies across Europe, South America, and APAC post updates through APIs that can shift deduction tables overnight. Vendors that catalog legislative feeds and push updates without downtime shield enterprises from fines and auditing headaches. Reporting and analytics add further value, surfacing labor-cost anomalies that finance teams use for scenario planning.

Continuous compliance is reshaping purchasing criteria. Deel’s acquisition of Safeguard Global’s database gives clients near-immediate country coverage, while startups such as Warp offer machine-learning models that flag U.S. state-level rule changes within hours. As such, future growth will hinge less on core calculation engines and more on agility in absorbing regulatory flux, positioning compliance modules as the new battleground for differentiation.

By Deployment Model: Hybrid Configurations Bridge Security and Scalability

Cloud solutions captured 60.14% of 2025 revenue, benefiting from consumption-based pricing and vendor-managed upgrades. Yet hybrid models are forecast to grow at 13.05% CAGR, mirroring the tug-of-war between scale and sovereignty requirements under the EU Data Act and China’s PIPL.[2]European Commission, “GDPR Fine Statistics,” EC.europa.eu The Multi-Country Payroll (MCP) Platform market size allocated to hybrid deployments is climbing as banks and hospitals retain employee master data on-premises while offloading calculation workloads to encrypted cloud clusters.

Hybrid adoption is also pronounced in APAC, where Japan’s electronic payroll register deadline in 2027 encourages phased cloud migration. Vendors respond with partitioned architectures that keep audit logs local, satisfy zero-trust guidelines, and still deliver elastic compute. As lock-in risk falls because of mandated interoperability, enterprises gain confidence to operate core engines locally and tap cloud modules for analytics and compliance.

By Organization Size: SMEs Embrace EoR-Bundled Payroll

Large Enterprises held 72.33% of 2025 revenue, reflecting entrenched global footprints and complex payroll matrices. However, SMEs are expanding fastest at 13.56% CAGR thanks to Employer of Record bundles that combine hiring, compliance, and payroll in a single invoice. The Multi-Country Payroll (MCP) Platform market size for SMEs is thus expanding even without heavyweight HRIS integrations. VC-backed disruptors pitch zero-touch onboarding, multi-currency wallets, and pay-as-you-go contracts that resonate with startups lacking internal payroll teams.

Enterprise buyers still prioritize vendor stability, illustrated by the UK NHS awarding Infosys a 15-year payroll contract covering 1.9 million staff. Integration depth with SAP or Workday continues to tip decisions toward incumbents. Yet if AI-native platforms prove they can manage compliance at scale, the switching calculus for large enterprises could shift, especially as hybrid architectures lower migration hurdles.

By End User Industry: Healthcare Gains Momentum

IT and Telecommunication retained 33.61% market share in 2025, leveraging early cloud adoption and distributed engineering teams. Healthcare, though smaller, is projected to grow at 11.98% CAGR on the back of mega-contracts like the NHS deal, which showcased reliable third-party processing of GBP 55 billion (USD 74.8 billion) in annual pay. The MCP Platform market share in Healthcare is poised to rise as shift-based staffing, complex overtime rules, and cross-border clinical trials strain legacy systems.

Banking and financial services emphasize encrypted hybrid deployment to satisfy stringent data-localization edicts, while manufacturing companies use analytics modules to apportion labor costs by product line. Retail and e-commerce value rapid onboarding for seasonal peaks; logistics and hospitality lean on mobile self-service because frontline staff often lack desktop access. Consequently, vendors increasingly differentiate through verticalized compliance libraries that cover industry-specific collective agreements and incentive schemes.

Geography Analysis

North America generated 37.24% of 2025 revenue in the MCP platform amrket, buoyed by early cloud adoption and multi-state payroll complexity. Venture capital clusters in the United States funnel resources into Payroll-as-a-Service platforms that promise automated state-tax apportionment, and 67% of U.S. employers intend to switch vendors within 12 months due to dissatisfaction with outdated tables. Canada’s electronic remittance push further backs demand for cloud-native compliance engines. Growth is moderating, however, as penetration levels near saturation, directing vendor attention toward mid-market firms and cross-border U.S.-Mexico manufacturing corridors.

Asia-Pacific is the fastest-growing region at a projected 12.45% CAGR. India’s DPDPA forces providers to provision local data centers; Japan’s electronic payroll rule effective April 2027 compels businesses to abandon paper-based processes.[3]Ministry of Electronics and Information Technology, “Digital Personal Data Protection Act,” Meity.gov.in China’s PIPL imposes critical-infrastructure audits, raising the bar for security documentation. Mature markets such as Australia and New Zealand already operate real-time Single Touch Payroll, serving as case studies for emerging Southeast Asian economies. Fragmented regulations across Thailand, Vietnam, and Indonesia favor regional specialists that offer in-country support and localized banking integrations.

Europe remains pivotal, driven by SAF-T and impending e-invoicing requirements. France’s phased rollout from September 2026 creates an 18-month compliance window that payroll vendors must meet. Germany, the United Kingdom, Italy, and Spain together make up over 60% of European payroll spending, with Schrems II complicating transatlantic data flows and accelerating the establishment of EU-based data centers. In South America, Brazil’s eSocial and Argentina’s AFIP real-time checks demand granular reporting, making compliance modules indispensable. The Middle East and Africa trail in adoption, hampered by unbanked populations, 57% in Sub-Saharan Africa, but mobile-money integrations such as M-Pesa are beginning to unlock payroll digitalization.

Competitive Landscape

The Multi-Country Payroll (MCP) Platform market features moderate fragmentation: the top five vendors, ADP, Ceridian, Deel, Globalization Partners, and CloudPay, command roughly 40-45% of global revenue in 2025. Consolidation is brisk; Deel’s March 2025 purchase of Safeguard Global’s payroll division added 140 countries and strengthened its compliance database. Vistra’s May 2025 acquisition of iiPay delivered 10 million additional payslips and deepened Middle East and Africa reach. Strategic alliances also shape competition: ADP’s partnership with SAP migrated 50 enterprise clients to S/4HANA Cloud in under a year, signaling that incumbents can defend share through ecosystem integration.

Technology differentiation hinges on the latency of compliance updates. Startups like Niural and Warp ingest legislative feeds via APIs and refresh rules within hours, whereas some incumbents still batch changes quarterly. Agentic AI is emerging as a battleground feature; Globalization Partners’ G-P Gia assistant answers payroll queries in natural language and resolves exceptions autonomously. Certifications such as ISO/IEC 27001 and SOC 2 Type II remain table stakes, but the ability to layer workforce analytics and forecasting on top of payroll now dictates premium pricing.

Looking ahead, vendors that marry jurisdiction-specific compliance engines with predictive analytics are poised to shift perception from transactional processors to strategic workforce-planning partners in the MCP platform market. Those lagging on AI, analytics, or compliance breadth may become acquisition targets or risk relegation to commodity status as interoperability rules remove switching friction.

Multi-Country Payroll (MCP) Platform Industry Leaders

Automatic Data Processing, Inc.

CloudPay Inc.

Safeguard Global LLC

Papaya Global Ltd.

Neeyamo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vistra and Globalization Partners unveiled a pathway that lets clients graduate from EoR contracts to full entity formation without changing payroll infrastructure.

- February 2026: Barcelona-based Valeria raised EUR 2 million (USD 2.13 million) to build mobile-first payroll for frontline industries.

- January 2026: Payoneer bought Boundless to fuse EoR services with cross-border payments, targeting European SMEs.

- January 2026: Globalization Partners introduced G-P Gia, an AI assistant that resolves payroll exceptions and delivers labor-cost insights.

Global Multi-Country Payroll (MCP) Platform Market Report Scope

The Multi-Country Payroll (MCP) Platform Market features cloud-based systems that streamline payroll processing, tax compliance, and payments across borders. These platforms harmonize global payroll operations, automate adherence to local statutory requirements, and offer consolidated reporting for multinationals. The MCP market solutions seamlessly integrate with HR, finance, and time-tracking systems, ensuring accuracy and minimizing compliance risks. The market's growth is spurred by an expanding global workforce, the intricacies of payroll management, and the quest for cohesive governance amidst varied regulatory landscapes.

The Multi-Country Payroll Platform Market Report is Segmented by Component (Core Payroll Engine, HRIS Integration Module, Compliance Management Module, Reporting and Analytics Module, and Other Components), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), End User Industry (IT and Telecommunication, BFSI, Manufacturing, Retail and E-Commerce, Healthcare, Professional Services, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Core Payroll Engine |

| HRIS Integration Module |

| Compliance Management Module |

| Reporting and Analytics Module |

| Other Components |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecommunication |

| Banking, Financial Services, and Insurance |

| Manufacturing |

| Retail and E-Commerce |

| Healthcare |

| Professional Services |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Core Payroll Engine | |

| HRIS Integration Module | ||

| Compliance Management Module | ||

| Reporting and Analytics Module | ||

| Other Components | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End User Industry | IT and Telecommunication | |

| Banking, Financial Services, and Insurance | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Healthcare | ||

| Professional Services | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current market size of the Multi-Country Payroll (MCP) Platform market?

The market reached USD 12.06 billion in 2026 and is projected to hit USD 20.55 billion by 2031.

Which region is forecast to grow the fastest through 2031?

Asia-Pacific is expected to register the highest CAGR at 12.45% during 2026-2031, driven by data-privacy laws and electronic payroll mandates.

Why are compliance management modules outpacing core payroll engines?

Real-time tax-reporting rules demand automated ingestion of statutory updates, causing the compliance segment to grow at 12.67% CAGR, faster than the overall platform.

What deployment model is gaining traction in regulated industries?

Hybrid deployment is expanding at 13.05% CAGR because it balances cloud scalability with on-premises data storage required by data-residency laws.

How are SMEs approaching cross-border payroll?

Many SMEs adopt Employer of Record bundles, enabling 13.56% CAGR in the SME segment as they leverage variable-cost contracts to avoid setting up legal entities.

Page last updated on: