North America HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

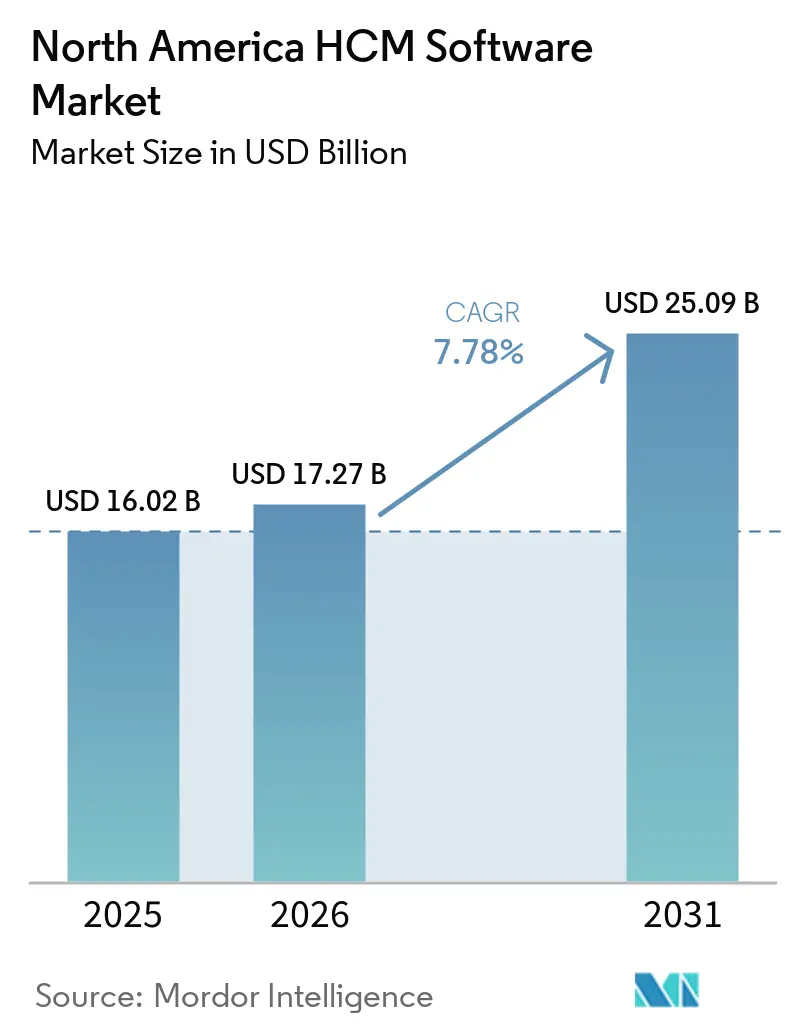

| Base Year Market Size (2025) | USD 16.02 Billion |

| Market Size (2026) | USD 17.27 Billion |

| Market Size (2031) | USD 25.09 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America HCM Software Market Analysis by Mordor Intelligence

The North America HCM software market size is projected to expand from USD 16.02 billion in 2025 to USD 17.27 billion in 2026 and USD 25.09 billion by 2031, registering a CAGR of 7.78% between 2026 and 2031. Strong demand for compliance automation, AI-driven talent analytics, and hybrid work orchestration continues to anchor growth. Software still dominates spending, yet services revenue is accelerating as enterprises seek integration expertise and algorithmic audit support. Cloud deployment remains the preferred model, although hybrid adoption is rising because regulated industries retain payroll data on-premises. Large enterprises generate the most revenue, but small and medium enterprises are closing the gap as modular pricing lowers barriers to entry. Competitive intensity is heightening as incumbents embed generative AI while venture-backed challengers bundle HR, IT, and finance workflows to win share.

Key Report Takeaways

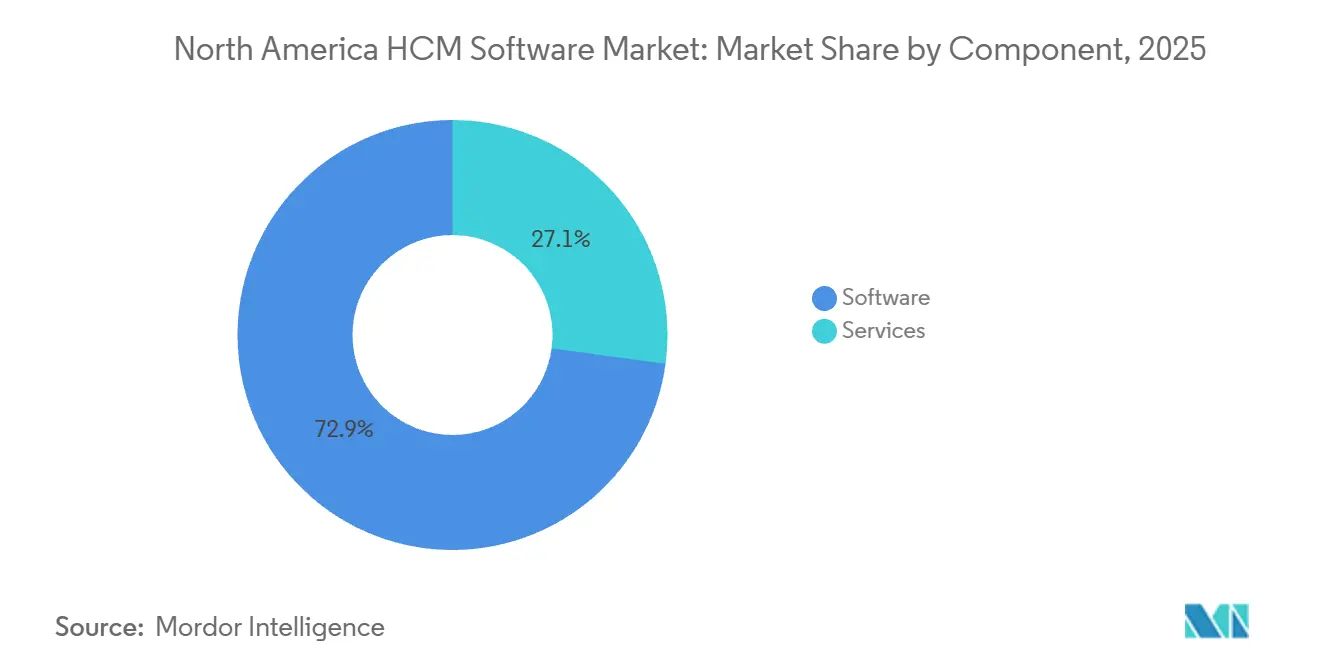

- By component, software held 72.86% of the North America HCM software market share in 2025, while services expanded at an 8.94% CAGR through 2031.

- By deployment mode, cloud captured 63.42% of the North America HCM software market size in 2025, yet hybrid configurations recorded the fastest 9.21% CAGR to 2031.

- By organization size, large enterprises accounted for 69.91% of spending in 2025, whereas small and medium enterprises grew at an 8.87% CAGR.

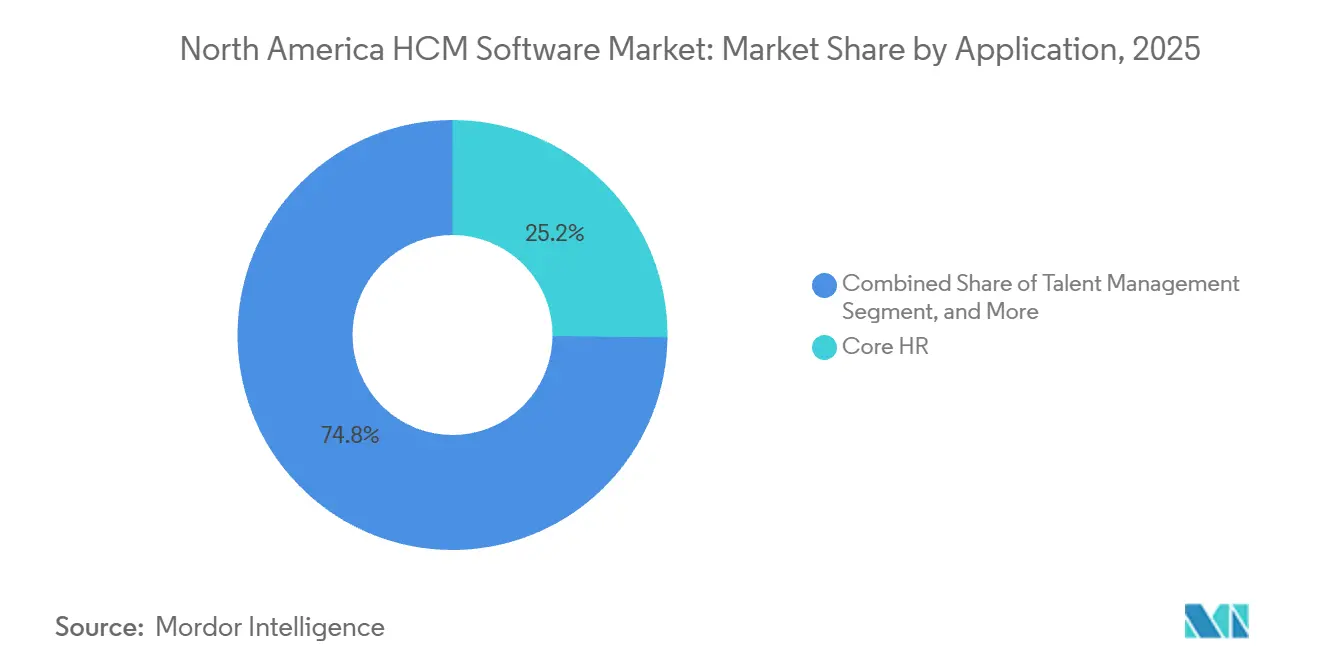

- By application, core HR led with 25.18% of 2025 revenue, while talent management advanced at a 9.48% CAGR to 2031.

- By end-user industry, BFSI contributed 22.63% in 2025, but healthcare and life sciences posted the highest 9.32% CAGR.

- By geography, the United States held 81.11% of 2025 revenue, with Mexico emerging as the fastest-growing country at an 8.69% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Migration of HR Systems | +1.8% | United States, Canada; early Mexico border adoption | Medium term (2-4 years) |

| Rise of AI-Driven Talent Analytics | +2.1% | United States, Canada; pilot Mexico rollouts | Short term (≤ 2 years) |

| Compliance Mandates on Payroll and Tax | +1.5% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Skills-Based Hiring Framework Adoption | +1.2% | United States, Canada, Mexico IT hubs | Medium term (2-4 years) |

| Generative AI Copilots for HR Workflows | +1.6% | United States, Canada; limited Mexico use | Short term (≤ 2 years) |

| Expansion of Total Workforce Management for Gig Labor | +0.9% | United States, Canada, Mexico corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration of HR Systems

Enterprises continue to replace on-premises infrastructure with cloud platforms to gain real-time analytics, mobile self-service, and continuous feature releases. Hybrid adoption grows faster than pure cloud adoption because banking and healthcare firms keep payroll processing in private environments to meet data residency mandates. The U.S. HR 2.0 program is migrating 2.2 million civilian employees to shared cloud service centers, while Canada’s federal rollout of Dayforce confirms the complexity of converting union pay rules to standardized workflows. These marquee projects validate the economics of the cloud and encourage state and provincial agencies to follow suit.

Rise of AI-Driven Talent Analytics

A 2026 SHRM survey showed 39% of organizations using AI for recruiting or performance management, up sharply in three years.[1]Society for Human Resource Management, “AI in the Workplace,” shrm.org Predictive attrition models now flag flight risks six to nine months in advance, and skills-inference engines surface internal candidates who would otherwise stay invisible. Yet change management is critical; 64% of frontline staff fear displacement, forcing vendors to supply transparency and reskilling pathways. Workday’s 2025 purchase of Paradox embedded conversational assistants that book interviews without recruiter input, demonstrating how AI can remove low-value tasks while enhancing candidate experience.

Compliance Mandates on Payroll and Tax

California’s Automated Decision Systems rules, effective October 2025, require annual impact assessments, while the EEOC’s 2024-2028 plan prioritizes algorithmic fairness.[2]Equal Employment Opportunity Commission, “Strategic Enforcement Plan 2024-2028,” eeoc.gov Mexico’s CFDI 4.0 standard and REPSE certification impose criminal liability for errors, driving rapid platform adoption. Canada’s pay transparency laws mandate gender pay gap disclosure, compelling HCM suites to generate audit-ready compensation analytics. Collectively, these regulations punish manual processes and reward automated tax logic, lifting demand across the region.

Skills-Based Hiring Framework Adoption

Workday research found 60% of manufacturers are struggling to fill roles, with 1.9 million vacancies projected by 2035 if degree requirements persist. Skills ontologies deconstruct roles into discrete capabilities, enabling internal mobility and broader talent pools. Competency-based screening also lowers algorithmic bias risk by moving away from proxies like university prestige. Vendors now embed skills graphs that map workforce capabilities to strategic projects, allowing proactive reskilling before new market entries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cyber-Security Concerns | -1.1% | United States, Canada, Mexico | Short term (≤ 2 years) |

| High Implementation Costs for SMEs | -0.7% | United States, Canada, Mexico | Medium term (2-4 years) |

| Algorithmic Bias and AI-Audit Exposure | -0.9% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Legacy ERP-HCM Integration Complexity | -0.6% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

Recent breaches at Paychex and Workday, plus Oracle’s critical CVE-2024-21287 patch, highlight how centralized employee data attracts threat actors. State privacy laws grant workers broad rights to access and delete data, while Mexico’s LFPDPPP levies fines up to 2% of revenue. Enterprises, therefore, delay cloud migrations until vendors demonstrate encryption, access controls, and rapid incident response. Providers now publish SOC 2 reports and zero-trust roadmaps to rebuild confidence.

Algorithmic Bias and AI-Audit Exposure

Mobley v. Workday advanced to class notice in February 2026, alleging racially disparate outcomes in applicant screening.[3]PACER, “Mobley v. Workday Docket,” pacer.gov Eightfold AI faces FCRA litigation for adverse-action notice failures. The EEOC’s first AI discrimination settlement with iTutorGroup in 2023 set a precedent, and California now mandates annual algorithm audits. Vendors that supply fairness dashboards and third-party certifications gain an advantage, while customers demand explainability before signing multi-year deals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software as Integration Complexity Rises

Software held a 72.86% share in 2025, reflecting the dominance of licensing revenue from core HR, payroll, and talent management modules, yet services are expanding at 8.94% through 2031 as enterprises require specialized expertise to integrate HCM platforms with legacy ERP systems, configure algorithmic audit trails, and train managers on AI-assisted decision tools. Services revenue is rising faster than software revenue as enterprises seek support for migrating data, configuring AI governance, and integrating legacy ERP systems. Implementation projects often span 12-24 months and involve multi-country payroll harmonization. Managed services adoption is also increasing among small employers that prefer to outsource payroll and benefits administration.

Software sales remain robust because cloud architectures enable incremental module purchases. Vendors monetize innovation through subscription tiers, yet services capture greater wallet share when compliance mandates or skills frameworks require customized workflows. The interplay of product and consulting revenue underscores why the North America HCM software market size continues to expand even as license growth moderates.

By Deployment Mode: Hybrid Gains as Regulated Industries Retain On-Premises Cores

Cloud deployments commanded a 63.42% share in 2025, driven by lower upfront capital expenditure, automatic updates, and mobile-first employee experiences that on-premises systems cannot match, yet hybrid configurations are growing fastest at 9.21% as enterprises balance agility with data residency and audit requirements. Cloud remains the primary choice for talent and learning modules, but hybrid deployments grow fastest as banks and hospitals keep sensitive payroll data on private infrastructure. This split configuration allows rapid innovation without breaching data sovereignty rules.

On-premises adoption in the North America HCM software market is gradually shrinking, though defense contractors and some Canadian ministries still maintain standalone environments. Small businesses gravitate toward pure cloud for cost predictability, whereas global enterprises choose hybrid to meet divergent jurisdictional mandates, reinforcing hybrid as the pivotal growth engine in the North America HCM software market.

By Organization Size: SMEs Accelerate as Modular Pricing Lowers Barriers

Large enterprises held a 69.91% share in 2025, reflecting their complex needs for multi-country payroll, union pay rules, and workforce analytics that justify enterprise-grade HCM suites, yet small and medium enterprises are adopting at 8.87% as vendors introduce modular pricing, embedded AI, and self-service onboarding that eliminate the need for dedicated HR teams. Large enterprises dominate absolute spending, driven by global payroll complexity and union pay rules that necessitate enterprise-grade suites.

However, SME uptake is accelerating and narrowing the feature gap. Vendors like Gusto and Rippling bundle HR, IT, and compliance in one interface and offer transparent per-employee pricing. Regulatory pressure, such as California’s AI notification rules and Mexico’s CFDI 4.0 mandates, forces even micro-firms to abandon spreadsheets. Consequently, SME adoption supports broader penetration for the North America HCM software market, while large enterprises continue to negotiate volume discounts and access premium support.

By Application: Talent Management Surges on Skills-Based Hiring Demand

Core HR captured a 25.18% share in 2025, encompassing employee records, organizational charts, and self-service portals that form the foundational layer of HCM systems, yet talent management is expanding fastest at 9.48% as enterprises shift from reactive hiring to proactive skills development and internal mobility. Competency graphs match adjacent skills to open roles, shrinking external hiring costs.

Workforce management applications, which include scheduling, time tracking, and labor forecasting, are growing steadily as retailers, healthcare systems, and manufacturers seek to optimize labor costs and reduce premium spend on external agencies. Payroll remains a steady anchor, enhanced with real-time tax engines. Learning and development solutions benefit from reskilling initiatives, further widening the functional footprint of the North America HCM software market.

By End-User Industry: Healthcare Leads Growth Amid Nursing Shortages

Banking, financial services, and insurance held a 22.63% share in 2025, driven by complex compensation structures, stringent regulatory reporting, and high employee counts that justify enterprise HCM investments, yet healthcare and life sciences are growing fastest at 9.32% as acute nursing shortages and premium labor costs demand predictive staffing and retention analytics. Nursing shortages push hospitals to deploy predictive staffing analytics that lower burnout.

IT and telecommunications, industrial manufacturing, retail and e-commerce, government and public sector, and other end-user industries each contribute significant revenue. Government agencies are modernizing legacy systems through initiatives such as the U.S. federal HR 2.0 program, which consolidates 2.2 million civilian employees onto shared service centers, and Canada's multi-year Dayforce deployment across ministries. Together, these verticals diversify revenue streams and fortify resilience across the North America HCM software market.

Geography Analysis

The United States provides 81.11% of regional revenue, bolstered by fragmented state regulations and the federal HR 2.0 modernization. State-specific mandates on pay transparency and algorithmic impact assessments increase reliance on platforms. Robust merger activity, such as Paychex-Paycor and Workday-Paradox, confirms long-term confidence. Strada Global reported a 17% increase in U.S. compliance complexity in 2025, driven by divergent state mandates on paid leave, predictive scheduling, and data privacy that require HCM platforms to maintain jurisdiction-specific logic for all 50 states.[4]Strada Global, “U.S. Compliance Complexity Report 2025,” stradaglobal.com

Canada’s trajectory is molded by pay transparency laws, bilingual payroll requirements, and public-sector modernization. The Canadian federal government's multi-year Dayforce implementation aims to consolidate legacy systems across ministries, a program that underscores the complexity of migrating decades of customizations and union-negotiated pay rules into standardized workflows. Different provincial payroll taxes and Quebec’s bilingual requirements make compliance more complex, forcing vendors to build localized features, something that can be challenging for platforms without strong Canada-specific expertise.

Mexico exhibits the fastest growth at 8.69%. U.S. companies are setting up engineering hubs in cities like Guadalajara, Monterrey, and Mexico City to tap into nearby talent without offshore challenges, driving demand for HCM platforms that meet local requirements such as CFDI 4.0 payroll standards and REPSE certification. Employer-of-record services that automate SAT, IMSS, and INFONAVIT filings reduce compliance risk and enable foreign firms to scale teams quickly. Collectively, these dynamics reinforce the continental breadth of the North America HCM software market.

Competitive Landscape

The market remains moderately consolidated. Workday, ADP, and UKG lead large-enterprise accounts by embedding generative AI and expanding partner ecosystems. Incumbents such as Workday, ADP, and UKG defend their positions through continuous AI integration, strategic acquisitions, and partner ecosystems that extend functionality into adjacent domains such as benefits administration and learning management. Workday’s USD 1.0 billion Paradox acquisition introduced conversational recruiting, while ADP’s new copilot features automate payroll troubleshooting. UKG added Inova Payroll to deepen mid-market reach.

High-growth disruptors such as Deel and Rippling raise multi-hundred-million-dollar rounds to fund global payroll and IT provisioning across unified stacks, winning share among growth-stage firms that value speed over depth. White-space opportunities exist in AI fairness and audit capabilities, as clients seek assurance against EEOC and California regulations. Approximately 90% of large employers now use automated screening, yet most require third-party validation, creating a service niche.

Price competition is heating up in the SME segment, where Gusto’s 75 AI features, launched in April 2026, are designed to solve everyday HR challenges for businesses without dedicated HR teams. This puts pressure on other vendors to stay competitive, leading incumbents to offer bundled solutions and flexible, usage-based pricing. As a result, competition remains strong, continuously pushing innovation and better value across the North America HCM software market.

North America HCM Software Industry Leaders

Workday, Inc.

Automatic Data Processing, Inc.

Ultimate Kronos Group

Paycom Software, Inc.

Dayforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Gusto launched 75 AI features covering compliance alerts, conversational onboarding, and benefits guidance, targeting SME adoption.

- February 2026: A federal court authorized class notice in Mobley v. Workday, advancing claims of racial bias in applicant screening.

- January 2026: Eightfold AI faced a class action alleging FCRA violations tied to algorithmic screening practices.

- October 2025: Deel raised USD 300 million Series E at a USD 17.3 billion valuation to fund product expansion.

North America HCM Software Market Report Scope

The North America HCM Software Market refers to the market for software solutions and associated services that enable organizations across the United States, Canada, and Mexico to manage and optimize human resources functions across the employee lifecycle. It includes platforms covering core HR, payroll, talent management, workforce management, and learning and development, along with related services such as implementation, integration, consulting, and support, delivered through cloud, on-premises, and hybrid deployment models. The market encompasses revenues from software licensing, subscriptions, and services, driven by increasing adoption of AI-enabled analytics, automation, and compliance capabilities, while excluding standalone HR outsourcing and staffing services.

The North America HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| United States |

| Canada |

| Mexico |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Core HR |

| Talent Management | |

| Workforce Management | |

| Payroll Management | |

| Learning and Development | |

| By End-User Industry | IT and Telecommunications |

| BFSI | |

| Industrial Manufacturing | |

| Healthcare and Lifesciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America HCM software market by 2031?

The market is forecast to reach USD 25.09 billion by 2031, growing at a 7.78% CAGR over 2026-2031.

Which component is growing faster, software or services?

Services record the stronger 8.94% CAGR through 2031 as firms seek integration and AI audit expertise .

Why are hybrid deployments gaining traction?

Enterprises in regulated sectors keep sensitive payroll data on-premises to meet residency rules while leveraging cloud agility for talent and learning modules.

Which application segment shows the highest growth?

Talent management posts the quickest 9.48% CAGR, driven by skills-based hiring and internal mobility tools.

What drives rapid adoption in Mexico?

Nearshoring investment and strict CFDI 4.0 payroll receipt mandates boost demand for compliant HCM platforms.

Page last updated on: