Optical Retail Chain Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 162.86 Billion |

| Market Size (2031) | USD 185.95 Billion |

| Growth Rate (2026 - 2031) | 2.69% CAGR |

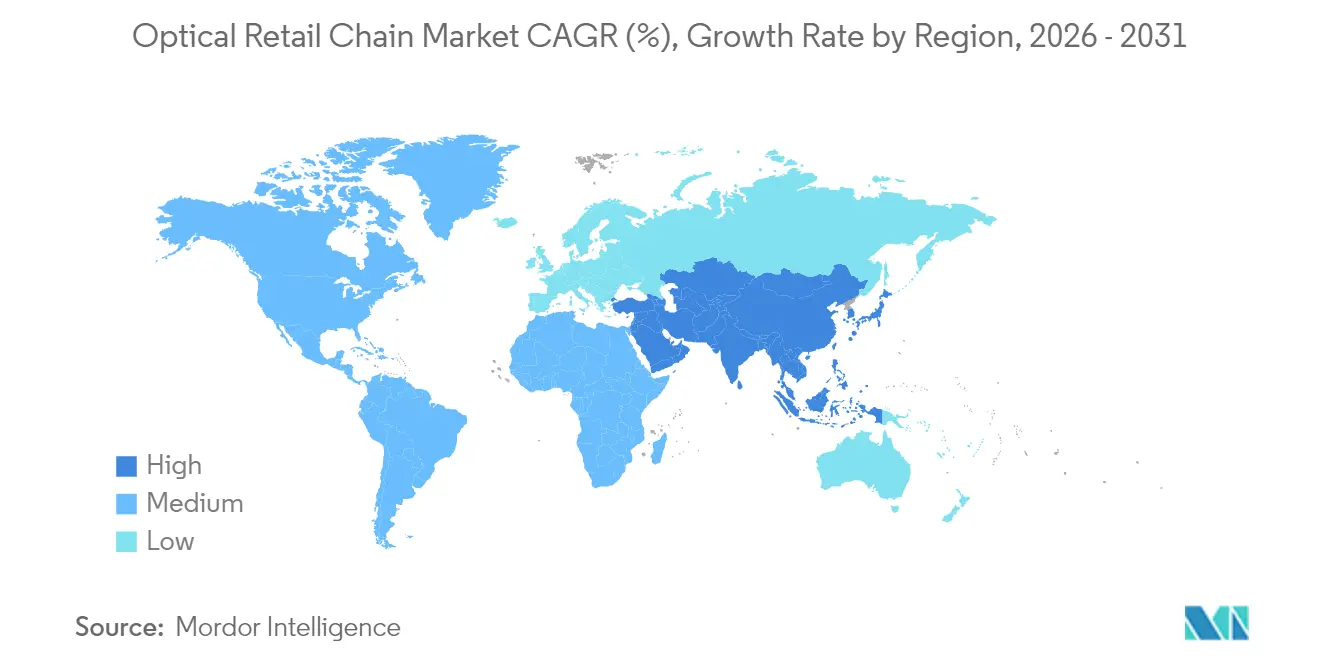

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Retail Chain Market Analysis by Mordor Intelligence

The Optical Retail Chain market size was USD 158.59 billion in 2025, is projected at USD 162.86 billion in 2026, and is forecast to reach USD 185.95 billion by 2031 at a 2.69% CAGR. Demand and delivery models are shifting as myopia becomes a global public health issue, while tariffs and online disruptors compress margins for incumbents. Chains are investing in AI-enabled diagnostics, smart eyewear attachments, and omnichannel logistics to protect traffic and capture higher-value prescriptions. Premiumization holds even as unit volumes soften, as the United States' spending reached USD 69.5 billion in 2025 despite volume declines, reflecting trade-up behavior toward progressive lenses and specialty solutions. Leading platforms that link retail, lens technology, and services are scaling faster than mid-tier independents that face greater tariff exposure and weaker negotiating leverage with suppliers.[1]Source: The Vision Council, “United States Optical Industry Reaches USD 69.5 Billion Despite Declines in Product Volume and Eye Exams,” The Vision Council, thevisioncouncil.org. Hardware and software integration is now a core differentiator, as shown by double-digit growth and strong cash generation at vertically integrated leaders that monetize AI glasses, myopia management, and subscription services tied to in-store expertise.

Key Report Takeaways

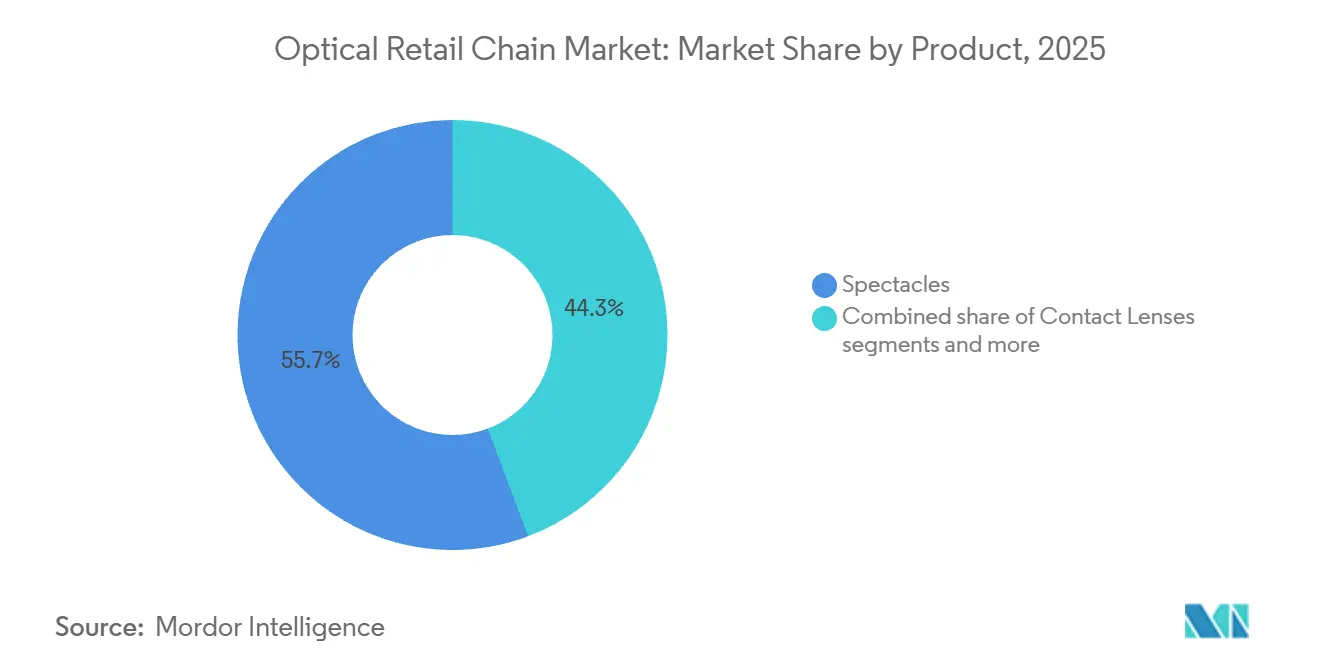

- By product, spectacles led with 55.72% of the Optical Retail Chain market size in 2025, while contact lenses are projected to expand at an 8.01% CAGR through 2031.

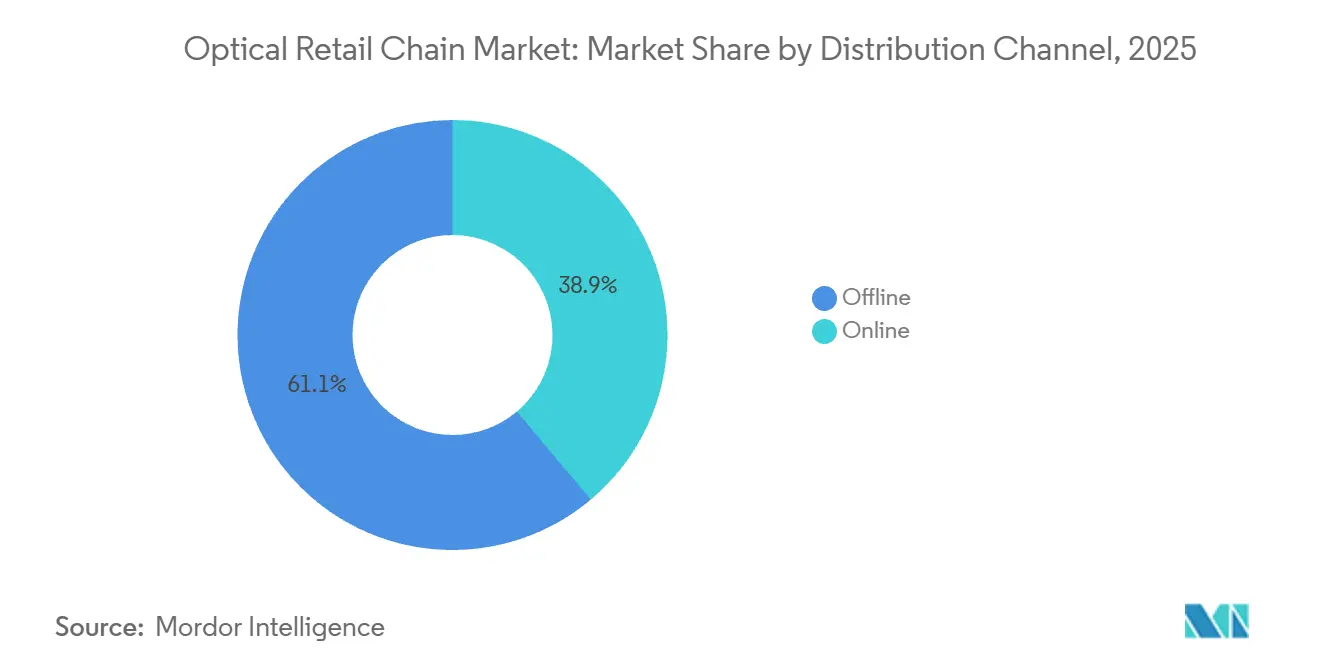

- By distribution channel, offline accounted for 61.12% of the Optical Retail Chain market size in 2025, while online is set to post a 7.44% CAGR to 2031.

- By geography, Asia-Pacific accounted for 42.31% of the Optical Retail Chain market size in 2025 and is forecast to grow at a 6.86% CAGR through 2031.

- By gender, women accounted for 49.01% of the Optical Retail Chain market size in 2025, while unisex frames are set to grow at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optical Retail Chain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Myopia Among Gen-Z Consumers | +0.85% | Global, concentrated in East Asia & urban centers | Medium term (2-4 years) |

| Growing Elderly Demographic Driving Presbyopia Demand | +0.40% | North America, Europe, Japan | Long term (≥ 4 years) |

| Strategic Omnichannel Investments by Optical Retail Chains | +0.55% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Expanding Consumer Spending Power Across APAC | +0.50% | Asia-Pacific, spillover to the Middle East | Medium term (2-4 years) |

| Untapped Growth Potential in Tier-Three Cities of India and China | +0.35% | Asia-Pacific, India & China tier-3/4 cities | Medium term (2-4 years) |

| Deployment of AI-Enabled Vision Screening Kiosks in Retail Stores | +0.25% | North America piloting, global scalability emerging | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Myopia Among Gen-Z Consumers

Global myopia prevalence has accelerated, with 2025 levels reaching 34% of the population and long-range projections indicating near half of the world population could be myopic by 2050, with East Asia as the epicenter of growth. China’s urban teens already post very high prevalence, which sustains recurring demand for more frequent prescription updates and higher-complexity lenses. This demand shift has elevated myopia management to a core growth vector for chains that can support clinical fitting and follow-up across large store networks. Recent research shows a substantial rise in myopia prevalence among children and adolescents, with data from China indicating over half of urban school-aged youth are affected, and projections suggesting that myopia will continue rising sharply through mid-century. Myopia rates have increased markedly over the past decades across global youth, with systematic reviews estimating that roughly one-third of children and teens are now nearsighted, and prevalence is expected to approach 40% by 2050. These trends reflect lifestyle and environmental factors driving the early onset and progression of myopia among younger generations, including Gen-Z. The growing burden of myopia is driving demand for corrective solutions, such as prescription eyewear and optical care services.[2]Source: Zhe Pan et al., “Myopia and High Myopia Trends in Chinese Children and Adolescents Over 25 Years: A Nationwide Study With Projections to 2050,” Lancet Regional Health Western Pacific, pmc.ncbi.nlm.nih.gov. The combination of rising prevalence and an expanding portfolio of regulated solutions now supports a durable uplift in the Optical Retail Chain market, where clinical programs can be delivered consistently at scale.

Growing Elderly Demographic Driving Presbyopia Demand

Presbyopia remains a near-universal condition by middle age and is driving steady demand for progressive, multifocal, and photochromic lenses within the Optical Retail Chain market. Product mix upgrades are visible in retailer disclosures, including premium progressives that lifted revenue per customer and supported resilience against macro softness. EssilorLuxottica’s lens portfolio momentum in 2025 featured advanced progressives and next-generation photochromics across EMEA, reinforcing the shift toward higher value prescriptions within chain retail. Adjacent opportunities are emerging at the intersection of audiology and vision, supported by the company’s Nuance Audio hearing aid glasses, which received United States and EU clearances in 2025 and reached broad retail distribution by year-end. [3]Source: EssilorLuxottica, “Essilor Stellest, First Myopia Control Spectacle Lens to Obtain FDA Market Authorization,” EssilorLuxottica, essilorluxottica.com. Retailers that couple progressive lenses with integrated care journeys and cross-category add-ons are positioned to capture more lifetime value per patient encounter and create recurring upgrade cycles. Disclosures from leading United States eyewear retailers also show sustained customer adoption of premium lens tiers, validating the presbyopia-led mix shift in 2025.

Strategic Omnichannel Investments by Optical Retail Chains

Omnichannel capabilities have become a core competitive differentiator in the Optical Retail Chain market, connecting online browsing and purchasing with in-store eye exams, fittings, and rapid fulfillment options. Leading players such as EssilorLuxottica have reported strong growth in direct-to-consumer channels while simultaneously expanding physical store networks, enabling efficient attachment of prescription lenses and premium add-ons to frames and smart eyewear. Programs like Ray-Ban Meta and Oakley Meta have gained substantial traction, supported by customized lens solutions that are difficult to replicate through online-only platforms. Digitally native brands are also expanding brick-and-mortar footprints to increase exam capacity, enhance try-on conversion, and optimize buy-online-pickup-in-store models that reduce last-mile delivery costs. The integration of tele-optometry, remote diagnostic tools, and app-based prescription management further broadens access to care, while retailers with unified logistics, in-store labs, and seamless digital workflows convert more customer traffic into personalized orders and recurring revenue relationships than single-channel competitors.

Expanding Consumer Spending Power Across APAC

Automated vision testing kiosks and remote validation workflows have begun to compress time and cost for basic prescription updates, offering short tests at accessible price points in mass retail settings. As these solutions enter large retailers and malls, they can reduce barriers to entry for under served patients and relieve local capacity constraints in markets with long wait times. The Optical Retail Chain market could benefit from kiosks that triage demand, route complex cases into comprehensive exams, and capture eyeglass and contact lens sales following rapid prescription refreshes. The availability of devices seeking regulatory clearance has increased confidence among retail partners, even as professional bodies emphasize that technology should not replace comprehensive eye exams. Operators that integrate kiosk-based journeys with in-store clinical capacity, lens personalization, and warranty programs can protect high-value services while welcoming cost-sensitive customers. The strategic balance lies in democratizing access to prescriptions while avoiding price-only competition on exams that historically anchored traffic for full-service optical chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Compression From Online-Only Competitors | -0.40% | Global, most acute in North America & Europe | Short term (≤ 2 years) |

| Supply Chain Disruptions in Acetate and Metal Inputs | -0.30% | Global, concentrated impact on China-sourced frames | Short term (≤ 2 years) |

| Reimbursement Limitations Under European Regulations | -0.15% | Europe, primarily DACH and Southern Europe | Long term (≥ 4 years) |

| Proliferation of Counterfeit Lenses in Emerging Markets | -0.10% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Compression From Online-Only Competitors

Direct-to-consumer operators sustain low entry prices and lean supply chains, pressuring legacy chains on headline price points and shipping costs. Warby Parker’s reporting showed gross margin variability in 2025 driven by tariffs, category mix, and logistics, underscoring how input costs and channel shifts feed into pricing decisions.[4]Source: Warby Parker Inc., “Form 10 Q for the Quarterly Period Ended June 30, 2025,” SEC, sec.gov. Subscription models, including omnichannel formats in which members receive exchanges and bundled services, expanded in 2025 and lifted average order values for operators that aligned store services with digital replenishment[5]Source: Mister Spex SE, “Q3 2025 Performance Update,” Mister Spex Corporate, misterspex.com. Competitive dynamics remain intense, as United States peers highlighted industry rivalry and structural cost pressures in their risk disclosures while targeting mix upgrades into premium lens categories to stabilize margins. The net effect is a bifurcating Optical Retail Chain market, where scale, vertical integration, and service bundling help offset pressures squeezing mid-tier, price-only propositions.

Supply Chain Disruptions in Acetate and Metal Inputs

Sourcing exposure to China and single supplier dependencies have created concentration risk for key materials, including acetate and metal components, with implications for lead times, working capital, and markdowns. Warby Parker outlined manufacturing and supplier concentration in its filings and also recorded inventory write-downs in 2025 tied to assortment changes, illustrating how volatility can spill into margins. Verticalized leaders pursued resilience by bringing critical inputs closer to demand centers and securing upstream capacity in high-index monomers and Rx manufacturing, reducing reliance on distant nodes. EssilorLuxottica also invested in advanced Rx lab capacity in France to support made-to-measure lenses, powered by renewable energy and designed for high-service markets in Europe. In the regulatory arena, the EU continued to refine medical device frameworks and traceability, expanding compliance workloads that favor operators with stronger systems and clinical governance. Retailers that combine supplier diversification with automation and tighter demand planning are less likely to absorb sharp margin hits from component shortages or rulemaking transitions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Spectacles Dominance Persists as Contact Lenses Surge via DTC Innovation

Spectacles accounted for 55.72% of the Optical Retail Chain market in 2025, and contact lenses are projected to grow at an 8.01% CAGR through 2031, driven by the adoption of daily disposables and subscription models. Retailers continue to report lens mix upgrades to premium progressives and advanced coatings that support resilient ticket values, even as traffic normalizes. Warby Parker disclosed a rising mix of contact lenses as part of its broader assortment, which supported top-line momentum while adding cost complexity that management closely monitored. EssilorLuxottica’s direct channels have become important for sunglasses and smart eyewear journeys, with store staff enabling prescription attachment and photochromic conversions at scale. Myopia management lenses posted strong growth in 2025 across the company’s Stellest portfolio, reflecting greater clinician training and parent awareness in markets with high pediatric prevalence.

The Optical Retail Chain market is also seeing targeted private-label innovation that enhances margins and control over lead times. Mister Spex reported higher margins from its SpexPro private-label lenses and continued to grow its share of prescription glasses in Germany in 2025, aided by omnichannel service programs that encourage in-store fitting and follow-up. Sunglasses remain an important gateway into the category, with premium banners like Sunglass Hut leveraging both online and store-based curation and seasonal drops to maintain flow. The Vision Council’s 2025 report confirms consumer trade-up dynamics in the United States, where spending rose even as volumes softened, reinforcing the shift toward higher-quality frames and lenses. Operators that combine differentiated assortment with clinical programs for myopia and presbyopia are capturing a larger share of the category’s durable value pools. As more retailers refine inventory depth around hero SKUs and tie customization to store labs, conversion into premium lenses is likely to remain a central lever for growth in the Optical Retail Chain market.

By Gender: Women Lead Market Share as Unisex Designs Reshape Brand Positioning

Women held 49.01% of the Optical Retail Chain market share in 2025, while unisex frames are forecast to grow at a 6.05% CAGR through 2031 as brands limit gendered labeling and focus on fit and universal shapes. Retailers are investing in adaptive sizing and modular designs that map across face shapes and age cohorts, reducing SKU complexity and increasing sell-through across channels. Several luxury houses have leaned into unisex silhouettes and neutral colorways to standardize creative direction while retaining seasonal novelty. Kering’s 2025 disclosures reflect ongoing product introductions across key Maisons, underscoring a broader industry move toward versatile design systems that translate across geographies and demographics. The Optical Retail Chain market is also consolidating fit technology advances, including in-store 3D scanning and parametric design, to deliver frames that prioritize comfort and aesthetics regardless of gender.

Mass and premium players are adjusting navigation and merchandising to reflect this shift. Mister Spex’s custom 3D-printed Eyed solutions emphasize individualized fit over gender identity and are positioned as a service-led upgrade that drives attachment of higher-margin lenses. Digital natives organize assortments by shape, width, and fit profile rather than by gender labels, which streamlines findability and supports higher mobile conversion rates. Unisex positioning also supports faster cross-season carryover of bestselling SKUs, lowering risk of markdowns while strengthening replenishment forecasting. The Vision Council’s 2025 market view indicates that United States spending rose even as volumes moderated, suggesting that practical benefits like fit, durability, and lens performance outweighed legacy style segmentation in many purchases. As brands and retailers continue to consolidate catalogs around universal frames and size-inclusive fits, unisex growth is set to be a durable contributor to the Optical Retail Chain market.

By Distribution Channel: Offline Dominates as Online Accelerates with Subscription Innovations

Offline channels accounted for 61.12% of the Optical Retail Chain market size in 2025, while online channels are expected to grow at a 7.44% CAGR through 2031, driven by virtual try-on, teleoptometry, and curated subscriptions. Hybrid models are now the norm at scale, with large platforms reporting growth in both e-commerce and store-based sales as consumers seek quick access to exams, professional fitting, and same-day fulfillment. Store networks also serve as production and service hubs for personalized lenses, adjustments, and repairs, which stabilize traffic against online-only price competition. In the United States, the Vision Council documented higher spending in 2025 even as total volumes declined, underscoring the role of brick-and-mortar in complex prescription journeys and insurance-linked care. Digital pioneers expanded store counts in 2025 and invested in app-based vision tests and virtual try-on to connect discovery to exam booking and local pickup. The Optical Retail Chain market is also seeing greater use of store labs to deliver fast turnaround prescriptions, raising customer satisfaction and reducing returns.

Subscriptions have become an important lever for loyalty and mix improvement. Mister Spex’s Switch program, which bundles multiple frames with exchanges and in-store services, delivered average order values that far exceeded those of non-members and scaled within months of its 2025 launch. Large European platforms reported subscription contributions to optical revenue across many countries, highlighting consumer appetite for predictable cost and care touchpoints tied to local stores. United States chains such as National Vision are retooling technology stacks, including EHR and payor API integrations, to improve claim accuracy and lower friction for insured customers, which is a key influence on channel choice for prescription eyewear. As omnichannel execution matures, the edge goes to operators who can route demand from mobile to store, keep delivery windows short, and anchor customer relationships in services that online only models cannot match at scale. This balance of digital convenience and in-store care continues to define growth trajectories in the Optical Retail Chain market.

Geography Analysis

Asia-Pacific led with 42.31% of the Optical Retail Chain market share in 2025 and is projected to expand at a 6.86% CAGR through 2031, powered by underpenetrated city tiers in India and China, fast-rising disposable incomes, and aggressive omnichannel rollouts. Myopia management is a structural tailwind in Greater China, where EssilorLuxottica’s Stellest portfolio grew strongly and where new iterations of the lens family and related smart eyewear are expanding addressable pediatric segments. Japan’s aging population supports premium lens and audiology convergence, reflected in large national chains that have broadened their formats and invested in technology-led shopping experiences. JINS opened a flagship in Tokyo’s Ginza with a digital-first journey and continues to scale across Asia with standardized processes that compress exam-to-delivery times. Regional champions are also expanding across Southeast Asia and the Middle East through owned stores and partnerships, creating a multi-country platform layer that can support faster product diffusion and unified service standards. The Optical Retail Chain market in APAC will likely remain the primary growth engine as clinical capacity, mobile commerce, and in-store technology penetrate beyond tier 1 cities.

North America remained the second-largest region by value, with the United States optical sector reaching USD 69.5 billion in 2025 despite volume declines, pointing to consumers trading up to premium prescriptions and lens technologies. Average exam costs rose year over year, reflecting greater diagnostic complexity and screening for age-related conditions, including presbyopia and glaucoma. EssilorLuxottica reported growth in North America, with smart eyewear programs and premium banners delivering peak sales days and strong comps in late 2025. Warby Parker expanded to 313 stores by Q3 2025 and announced a partnership with Google to develop AI-powered glasses, backed by substantial product development funding, signaling deeper convergence of optical retail and wearables. National Vision ended a legacy partnership, rebalanced its footprint, and outlined a transformation plan to 2030 that targets mix shifts into premium lenses and managed care segments while aiming for margin expansion.

Europe demonstrated resilience through localized sourcing, premium positioning, and disciplined omnichannel models in the Optical Retail Chain market. EssilorLuxottica’s EMEA operations delivered strong results in 2025, with double-digit growth in both professional solutions and direct-to-consumer activity, aided by continued integration of former GrandVision banners and higher penetration of EssilorLuxottica's frames and lenses. Mister Spex consolidated its German core market in 2025, closed non-core international stores, and improved store-level margins while expanding service-linked products that support repeat traffic. The EU advanced proposals in late 2025 to simplify medical device rules and promote innovation, which should, over time, reduce compliance friction for chains with strong regulatory systems. Aging demographics in several European countries continue to support presbyopia segments, favoring retailers that can deliver advanced progressives and hearing-vision hybrids tied to clinical screening. The region’s pathway shows steady mid-single-digit growth rather than outsized surges, anchored by service-led differentiation and subscription models that drive loyalty in mature markets.

Competitive Landscape

A concentrated group of global leaders anchors the Optical Retail Chain market alongside a growing base of regional and digital challengers. EssilorLuxottica continues to expand its retail footprint worldwide, generating strong revenue growth and cash flows that support acquisitions across materials, automation, and data capabilities. Its success in scaling smart eyewear and accelerating myopia management demonstrates the advantages of integrating medical technology with retail distribution. United States-based digital-native brands are expanding their physical store networks to increase capacity and improve fulfillment speed, underscoring the importance of omnichannel models. Meanwhile, European operators are refining portfolios, closing weaker locations, and investing in private-label lenses and bundled services to strengthen margins and customer attachment.

Technology investment and mergers and acquisitions are central to competitive positioning. EssilorLuxottica has pursued vertical integration by acquiring lens material operations, automation capabilities, and health-technology assets to enhance quality control and data-driven care initiatives. Regulatory approvals for advanced myopia-control lenses have created new service categories within retail chains, supported by widespread staff training. Warby Parker has advanced partnerships in AI-enabled eyewear, underscoring the growing convergence between optical retail and consumer electronics. Regional players are also leveraging tele-optometry, app-based testing, and subscription services to generate recurring revenue and deepen customer relationships.

Pricing discipline and margin management continue to separate market leaders from smaller competitors. Trade-related cost pressures have prompted selective pricing adjustments and sourcing diversification among large integrated platforms. Direct-to-consumer challengers maintain transparent entry pricing strategies while scaling laboratory capacity and improving turnaround times to sustain brand equity. Traditional chains differentiate through in-store diagnostics, complex fittings, and repair services that build trust and encourage repeat visits. As competition intensifies, the Optical Retail Chain market increasingly rewards operators that combine service bundles and technology-driven personalization rather than relying solely on store expansion for growth.

Optical Retail Chain Industry Leaders

EssilorLuxottica

GrandVision (incl. FYidoctors, Pearle)

Specsavers

Visionworks (VSP)

Fielmann

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: EssilorLuxottica announced a share buyback program and released Q4/Full Year 2025 results, showing revenue growth of +11.2% at constant currency, a 16.0% adjusted operating margin, and record free cash flow of EUR 2.8 billion. The company sold over 7 million AI glasses units in FY2025 and expanded Nuance Audio to 15,000 doors across 12 markets, while myopia management portfolio revenue grew 22% worldwide.

- October 2025: EssilorLuxottica announced it acquired RetinAI (Ikerian AG), a health-tech company specializing in AI and data management for eyecare. The purchase enhances the company’s med-tech strategy by integrating advanced machine-learning software for retinal imaging and disease monitoring, empowering clinicians with faster, data-driven diagnostic insights and supporting research and pharmaceutical workflows.

- September 2025: EssilorLuxottica announced that its Essilor Stellest spectacle lens received market authorization from the United States Food and Drug Administration via the De Novo pathway, making it the first clinically proven spectacle lens approved to slow myopia progression in children. The authorization follows prior FDA Breakthrough Device designation and is supported by clinical data showing a significant reduction in myopia progression with Stellest lenses.

- August 2025: EssilorLuxottica acquired Automation & Robotics in Belgium, which specializes in automated systems for optical lens quality control, to enhance manufacturing efficiency and scalability.

Global Optical Retail Chain Market Report Scope

Optical retail chains are businesses primarily selling prescription and non-prescription eyewear, including lenses, eyeglasses, and contact lenses. They typically operate numerous outlets across various locations, providing consumers with multiple eyewear options. The optical retail chain market forecast is segmented by product (spectacles, sunglasses, and contact lenses), gender (men, women, and unisex), distribution channel (offline online), and geography (Asia-Pacific, North America, Europe, South America, and the Middle East & Africa). The report offers the market size in value terms in USD for all the abovementioned segments. The report offers the market size in value terms in USD for all the abovementioned segments.

| Spectacles |

| Sunglasses |

| Contact Lenses |

| Men |

| Women |

| Unisex |

| Offline |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product | Spectacles | |

| Sunglasses | ||

| Contact Lenses | ||

| By Gender | Men | |

| Women | ||

| Unisex | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Optical Retail Chain market?

The Optical Retail Chain market size was USD 158.59 billion in 2025 and is forecast to reach USD 185.95 billion by 2031 at a 2.69% CAGR, reflecting steady demand and ongoing premiumization.

Which region is expected to contribute most to growth through 2031?

Asia-Pacific leads the Optical Retail Chain market with a 42.31% share in 2025 and a projected 6.86% CAGR through 2031, as underpenetrated city tiers, rising incomes, and myopia management expand the addressable demand.

How are leading players defending margins amid tariffs and online competition?

Leaders are diversifying sourcing, investing in AI-enabled fitting and diagnostics, scaling smart eyewear with prescription attachments, and expanding subscriptions that bundle in-store services with digital convenience.

What product categories are driving mix upgrades in the Optical Retail Chain market?

Premium progressives, photochromics, and myopia management lenses are lifting average tickets, supported by omnichannel journeys that tie virtual try-on and remote testing to in-store customization.

How is omnichannel reshaping consumer pathways from exam to fulfillment?

Chains use teleoptometry, app-based prescription updates, BOPIS, and store labs to compress delivery time, convert virtual discovery into store traffic, and increase attachment rates for coatings and premium lenses.

Page last updated on: