Convenience Food Retail Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 1.27 Trillion |

| Market Size (2031) | USD 1.81 Trillion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

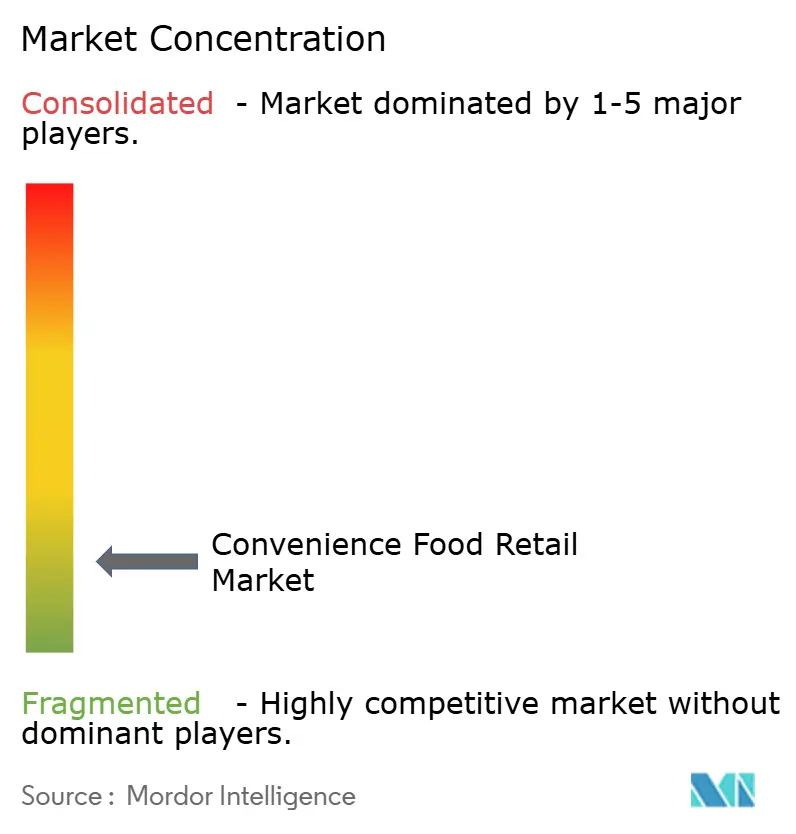

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Convenience Food Retail Market Analysis by Mordor Intelligence

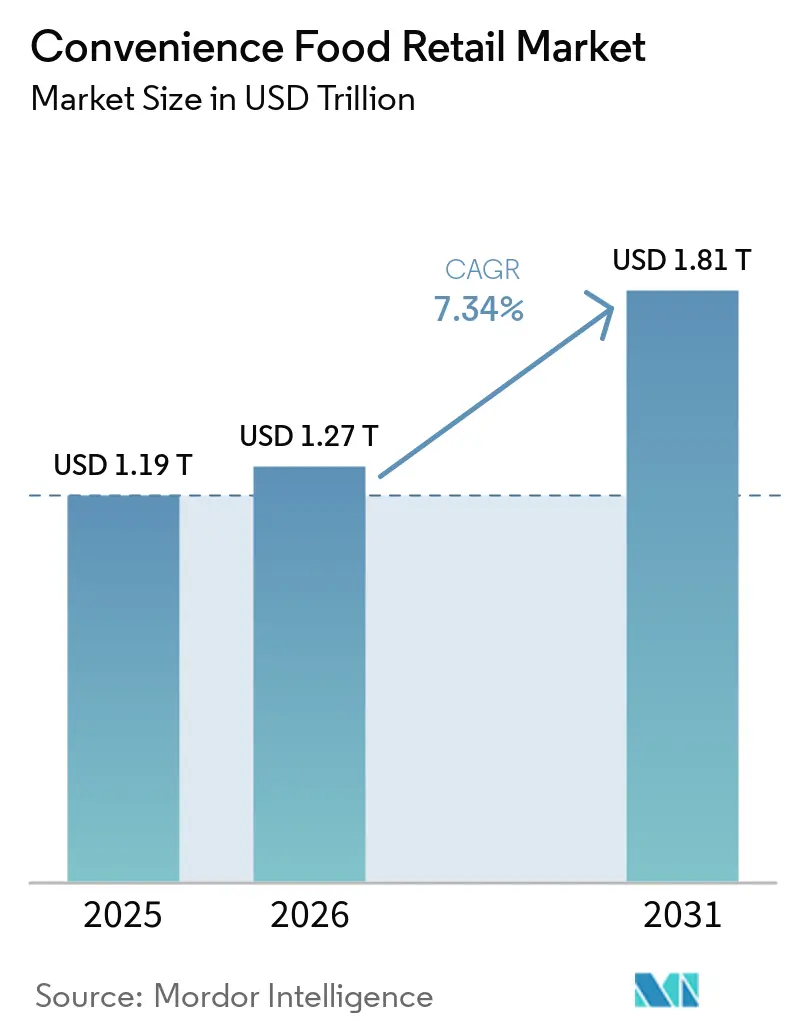

The Convenience Food Retail Market size was valued at USD 1.19 trillion in 2025 and is estimated to grow from USD 1.27 trillion in 2026 to reach USD 1.81 trillion by 2031, at a CAGR of 7.34% during the forecast period (2026-2031).

The convenience food retail market is being reshaped by a steady shift away from tobacco and packaged beverages toward fresh prepared food, which now plays a much larger role in store profits. In 2025, U.S. in-store foodservice accounted for 28.5% of total in-store sales and 38.9% of gross profit, underscoring why operators across the convenience food retail market are directing more capital toward kitchens, hot food, bakery programs, and meal solutions[1]CONVENIENCE.ORG https://www.convenience.org/Media/Daily/2026/April/15/1-US-Convenience-Store-Sales-340-Billion_Research. The convenience food retail market is also benefiting from broader use of loyalty systems, order-ahead functions, and private-label expansion, because these tools help chains lift repeat visits and protect margin on everyday items. At the same time, the convenience food retail market is seeing a wider strategic split between franchise-led network expansion and corporate-owned expansion through acquisitions, especially as large operators buy foodservice-capable assets to speed format upgrades. Growth opportunities remain strongest where dense urban demand, strong food attachment, EV-related dwell time, and forecourt redevelopment are all pulling consumers toward a more food-led and service-led convenience model.

Key Report Takeaways

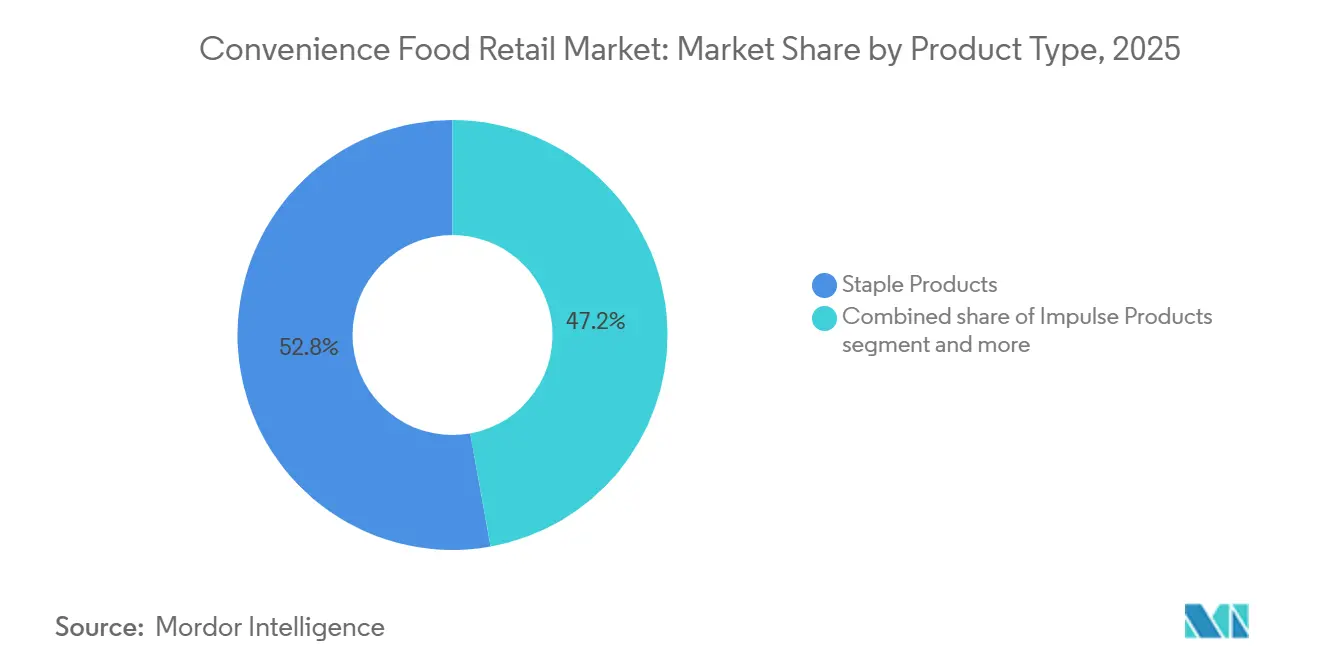

- By product type, staple products held 52.83% of the global convenience food retail market share in 2025, while impulse products are forecast to expand at a CAGR of 7.98% through 2031.

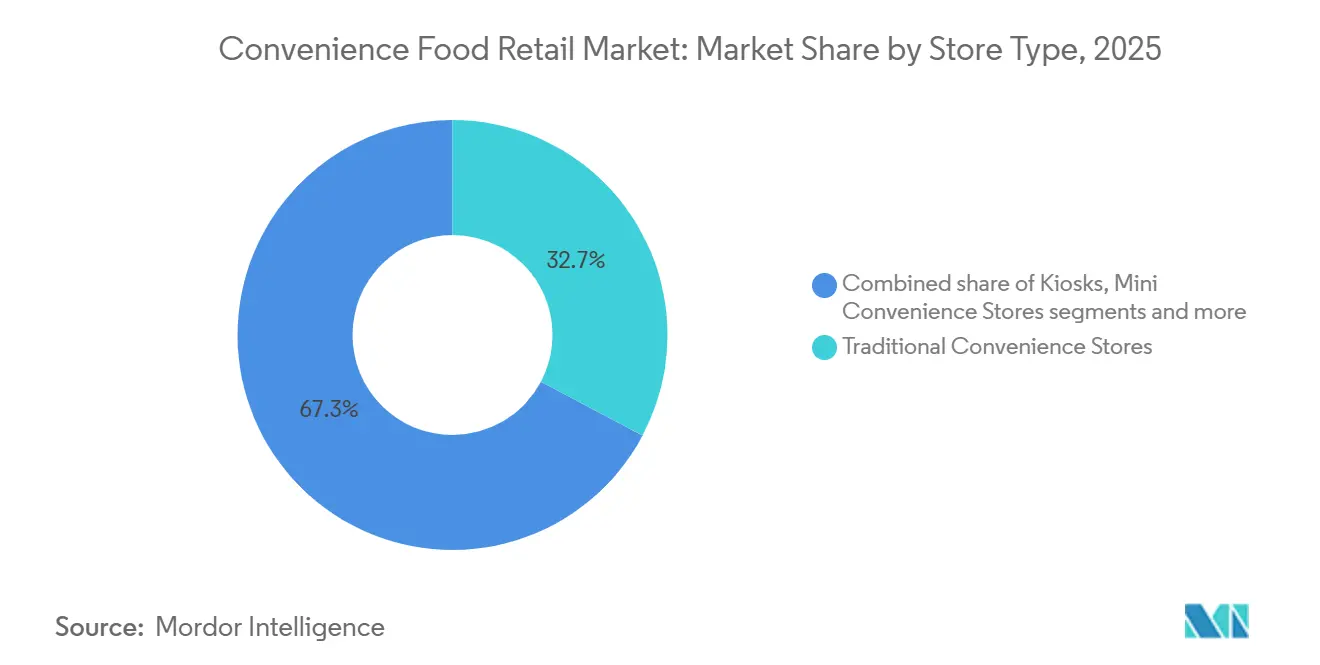

- By store type, traditional convenience stores accounted for 32.74% of the global convenience food retail market share in 2025, while hyper convenience stores are projected to grow at a CAGR of 8.34% through 2031.

- By ownership model, franchise stores held 44.85% of the global convenience food retail market share in 2025, while corporate-owned chains are forecast to grow at a CAGR of 8.81% through 2031.

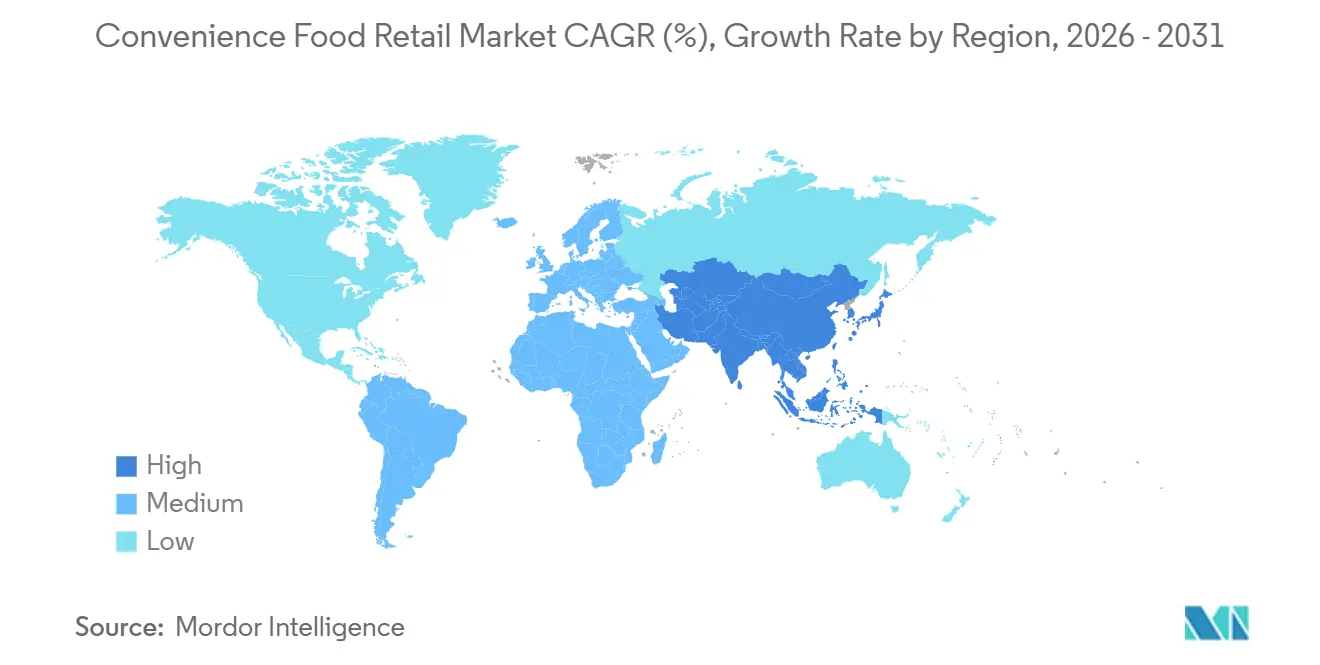

- By geography, Asia-Pacific held 35.98% of the global convenience food retail market share in 2025, while the Middle East and Africa are forecast to expand at a CAGR of 7.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Convenience Food Retail Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| On-The-Go and Top-Up Shopping Demand | +2.3% | Global | Short term (≤ 2 years) |

| Fresh Foodservice Margin Expansion | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Loyalty, Order-Ahead, And Omnichannel Engagement | +0.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Private-Label Value Architecture | +0.7% | North America, Europe | Medium term (2-4 years) |

| Micro-Fulfillment and Pickup-Node Monetization | +0.5% | Asia-Pacific, North America | Long term (≥ 4 years) |

| EV-Charging Dwell-Time Food Attachment | +0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

On-The-Go and Top-Up Shopping Demand

The convenience food retail market continues to benefit from food and refill occasions that are decided at the last minute and fulfilled close to the point of need. The convenience food retail market is structurally suited to these missions because stores are located on commuting routes, at fuel forecourts, and in dense residential corridors where speed matters more than a large basket assortment. This pattern is consistent with NACS's 23rd straight year of inside-sales growth for U.S. convenience retail in 2025, signaling that shoppers are still making more food and merchandise trips to small-format stores. As visits become more mission-based, operators in the convenience food retail market can build larger baskets by pairing ready-to-eat foods with immediate household or beverage needs at a single stop. The operating effect is clear: stores no longer rely on a single category to define the trip, which improves the value of each visit. This also supports continued investment in locations and layouts that reduce friction and make proximity the main reason to choose the store.

Fresh Foodservice Margin Expansion

Fresh proprietary food has become one of the clearest earnings levers in the convenience food retail market, and the spread between sales contribution and profit contribution is large enough to keep investment rising. NACS reported that foodservice accounted for 38.9% of gross profit in 2025, even though it represented 28.5% of in-store sales, underscoring why prepared food remains central to store economics across the convenience food retail market. Seven & i said average purchase per store per day for just-made counter merchandise rose 8.3% in FY2025, supported by SEVEN CAFÉ Bakery rollout across roughly 8,000 Japanese stores and a planned Live-Meal launch in FY2026[2]7ANDI.COM https://www.7andi.com/en/ir/file/library/ks/pdf/2026_0409kse_02.pdf. Caseys reported a 57.8% prepared food and dispensed beverage gross margin in fiscal 2025, compared with 34.8% for grocery and general merchandise, underscoring how fresh food can reshape the profit mix in the convenience food retail market[3]SEC.GOV https://www.sec.gov/Archives/edgar/data/726958/000072695825000032/ex991q42025pressrelease.htm. Once chains build kitchen capability and proprietary menu systems, the convenience food retail market becomes less exposed to pure price competition from discounters because freshness and speed are harder to match. That is why food-led investment is moving from a growth option to a core requirement for leading operators.

Loyalty, Order-Ahead, and Omnichannel Engagement

Digital engagement is becoming a more practical operating tool in the convenience food retail market rather than a secondary brand feature. The convenience food retail market benefits from loyalty and order-ahead systems, which make repeat purchases easier and help chains steer customers toward higher-margin offerings such as coffee, bakery items, meal deals, and proprietary snacks. Seven & i linked its private-brand expansion and 7NOW delivery growth to a larger digital ecosystem, with 7NOW revenue reaching nearly USD 979 million in FY2025 and supporting more frequent consumer touchpoints beyond the physical store visit. As these systems improve, operators can use transaction data to refine promotion timing, product placement, and menu range without widening discount depth. That is important in the convenience food retail market because visit frequency is high, and even small gains in repeat conversion can lift store-level productivity. Over time, digital engagement also strengthens the chain’s ability to defend immediate-need missions that might otherwise migrate to app-based ordering platforms.

Private-Label Value Architecture

Private labels are moving from a margin support tool to a broader assortment strategy in the convenience food retail market. U.S. private-label sales across retail reached USD 282.8 billion in 2025, up 3.3%, compared with 1.2% growth for national brands, confirming that value pressure and improved quality are strengthening acceptance of own-brand offers[4]PLMA.COM https://www.plma.com/article/us-private-label-industry-reached-2828-billion-sales-2025. Seven & i added 175 new private-brand items in FY2025, which shows that scale operators in the convenience food retail market are expanding the program across a wider range of everyday needs rather than limiting it to a few entry categories. The convenience food retail market benefits from this shift because private label helps chains control price points while also improving unit economics in categories where national-brand loyalty is not absolute. It also gives operators greater freedom to reformulate, resize, or bundle items based on local demand and regulatory requirements. That dual role, protecting traffic and protecting gross margin, is why own-brand development is becoming more deliberate across food, beverages, and impulse lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Competition from Discounters and Rapid Delivery | -1.0% | Global, high in APAC and North America | Short term (≤ 2 years) |

| Labor, Lease, And Foodservice Cost Inflation | -0.8% | North America, Europe, Oceania | Medium term (2-4 years) |

| HFSS And Healthier-Promotion Restrictions | -0.6% | Europe (UK, Scotland, Wales) | Medium term (2-4 years) |

| Cybersecurity And Systems-Integration Exposure | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Competition from Discounters and Rapid Delivery

Price pressure remains one of the clearest constraints on expansion in the convenience food retail market, especially in mature urban areas where consumers can quickly compare options. The convenience food retail market faces competition from hard discounters on value and from rapid-delivery models on speed, meaning store operators must defend both price perception and convenience simultaneously. This pressure matters most where store networks are already dense, because the fight is then over mission capture rather than pure market creation. It also explains why larger chains in the convenience food retail market are investing more in proprietary food, digital ordering, and stronger store formats that are harder to substitute. Couche-Tard’s GetGo acquisition and Casey’s ongoing site additions both reflect a push toward better foodservice assets rather than a simple increase in store count. As a result, operators that lack scale, differentiated food, or reliable digital access remain more exposed to share loss on urgent-need trips.

Labor, Lease, And Foodservice Cost Inflation

The convenience food retail market is also constrained by rising costs as stores add more labor-intensive foodservice operations. NACS said direct store operating expenses rose 4.2% in 2025, while hourly wages averaged USD 15.04 and card fees reached a record USD 21.3 billion, indicating that several cost lines are moving against store profitability at once. These pressures weigh more heavily on the convenience food retail market when operators extend service hours, introduce made-to-order food, or enter higher-rent urban and forecourt locations. The challenge is not limited to payroll because fresh-food programs also need better inventory control, more prep discipline, and more waste management than packaged categories. That means the convenience food retail market must fund kitchens, labor scheduling, and spoilage control simultaneously. Chains that can automate ordering, sharpen assortment, and spread fixed costs across a larger estate will be better positioned to protect margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Staple Demand Anchors Scale While Impulse Lines Lift Growth

Staple products accounted for 52.83% of the convenience food retail market in 2025, making them the largest product category and the main driver of routine top-up shopping. These items keep stores relevant to everyday household needs by covering repeat purchases in beverages, perishables, packaged foods, and basic grocery items. Impulse products are projected to grow at 7.98% through 2031, the fastest rate among product types, as operators upgrade food-to-go ranges, sharpen merchandising, and use proprietary launches to encourage unplanned add-on purchases. This growth matters because impulse lines often sit close to checkout, entry, and meal occasions, where the convenience food retail market can raise basket value without changing the mission of the trip. The category is also becoming more regulated in some developed markets, which changes how chains design both promotions and assortment. In England, the Food Promotion and Placement Regulations restricted certain HFSS location and volume-price promotions from October 2025, which directly affects how larger chains merchandise high-turn impulse items.

Emergency products remained the smallest product segment, but they still play an important role in the convenience food retail market because they are built around urgent, non-deferrable trips. These items support the format’s core promise of immediacy, especially when shoppers need medicine, travel basics, or household items outside a planned grocery trip. As operators strengthen private-label programs, the convenience food retail industry is beginning to apply the same own-brand logic to emergency lines where brand attachment is often weaker, and price comparison is direct. That matters because the convenience food retail market can protect unit margin without asking shoppers to compromise on speed or availability. Couche-Tard stated that food and beverage accounted for 49% of FY2025 gross profit, reinforcing the broader push toward a more controlled, differentiated product mix across stores.

By Store Type: Traditional Stores Hold Scale While Hyper Formats Push the Upper Limit

Traditional convenience stores accounted for 32.74% of global revenue in 2025. They remained the base format for the convenience food retail market because they combine network reach, manageable capital intensity, and broad mission coverage. Their position reflects the fact that the convenience food retail market still relies on dense store grids that can serve daily top-ups, meals, beverages, and urgent-need occasions with a small footprint. Kiosks and mini convenience formats remain important in transit-heavy or high-rent environments because they protect convenience access where larger stores are not practical. Limited-selection and expanded formats sit between those poles and allow operators to adjust assortment depth to local demand, labor availability, and real estate economics. This layered format mix keeps the convenience food retail market flexible, but it also makes the role of destination stores more visible as chains look for stronger differentiation.

ADNOC Distribution’s The Hub by ADNOC illustrates why the upper end of the format spectrum is gaining attention in the convenience food retail market. The first site opened in Abu Dhabi in November 2025, with a retail footprint 3 times that of a traditional service station, and the company said it targeted 30 locations by 2030, following the first 6 sites achieving 90% retail-unit lease occupancy at opening. Circle K’s EV-only hub in Gothenburg offers another version of the same logic, combining ultra-fast charging with a fresh-food convenience store on a high-traffic motorway corridor. These examples show that the convenience food retail market is no longer defining format value only through square footage or assortment count. It is defined as the number of missions a single location can capture during a single visit. That is why destination stores can support better unit economics even when they require more upfront investment.

By Ownership Model: Franchise Breadth Leads Today While Corporate Ownership Gains Speed

Franchise stores accounted for 44.85% of global revenue in 2025, making them the largest ownership model in the convenience food retail market and confirming the efficiency of asset-light network growth. The convenience food retail market has long relied on franchising to accelerate footprint build-out, especially when operators want local execution and faster market coverage without bearing the full capital burden at every site. This model remains attractive because it can scale brand presence quickly and adapt to local trading conditions with less centralized balance-sheet strain. At the same time, the convenience food retail market is seeing faster growth in corporate-owned chains, which are projected to expand at 8.81% through 2031. That rate is significant because it shows that direct ownership is gaining favor in areas where foodservice consistency, digital rollout, and systems integration matter more than pure store count.

Recent corporate activity shows why direct ownership is gaining momentum within the convenience food retail market. Couche-Tard completed its acquisition of GetGo Café + Markets in 2025, adding 270 foodservice-capable sites across 5 U.S. states and explicitly tying the deal to fresh-food capability. Caseys has also raised its fiscal 2026 EBITDA growth guidance to 18% to 20% after absorbing 198 CEFCO stores, while prepared food and dispensed beverage sales reached USD 1.61 billion in fiscal 2025. These moves suggest that the convenience food retail market is placing a premium on acquisition targets that already have the right kitchen, site quality, and traffic profile. The larger implication is that high-quality regional assets may become scarcer as consolidation moves forward. That can keep valuations firm for foodservice-capable chains and push leading operators toward more new-to-industry construction.

Geography Analysis

Asia-Pacific accounted for 35.98% of the convenience food retail market in 2025. It remained the largest regional contributor, driven by dense urban demand, strong food attachment, and high store accessibility, which support frequent use. Japan is central to that position because leading chains there treat convenience stores as daily food destinations, not only as packaged-goods outlets. Seven & i’s FY2025 update showed an 8.3% rise in just-made counter merchandise purchase per store per day and a bakery rollout to roughly 8,000 Japanese stores, which supports the region’s food-led operating model. South Korea and parts of Southeast Asia add a digital and small-format expansion layer that keeps the convenience food retail market tied closely to mobile ordering, local neighborhood demand, and high-frequency visits. With a forecast CAGR of 7.6% through 2031, Asia-Pacific remains the scale center of the convenience food retail market and one of its most food-intensive regions.

North America held the second-largest regional position in 2025, and the convenience food retail market in the region is growing at a more moderate 4.0% through 2031 because the network is mature and competition is now centered on margin quality. NACS reported that U.S. in-store merchandise and foodservice sales reached USD 341.2 billion in 2025, with foodservice accounting for 38.9% of gross profit, underscoring the extent to which the convenience food retail market in North America depends on prepared food to sustain in-store earnings. Europe is projected to grow at 5.8% through 2031, and the convenience food retail market there is increasingly shaped by forecourt foodservice upgrades, EV-related store redesign, and tighter promotion rules. Circle K’s EV-only convenience hub in Gothenburg shows how European operators are using longer dwell time to attach fresh food and beverages to the charging visit. At the same time, HFSS rules in England and Scotland are forcing large chains to adjust impulse placement, promotions, and product reformulation.

The Middle East and Africa are the fastest-growing regional blocks in the convenience food retail market, with a projected CAGR of 7.89% through 2031, as operators use forecourt redevelopment to build broader destination retail. ADNOC’s destination-format rollout clearly shows this direction, with larger roadside sites designed around foodservice, family amenities, and non-fuel retail. The convenience food retail market in these geographies benefits from lower existing proximity penetration across several catchments, giving new formats more room to establish local trip habits. South America also remains an important growth arena for the convenience food retail market because chain-led rollout and urban proximity demand continue to support network expansion, even though the eligible primary sources supplied for this draft were stronger for North America, Europe, Asia-Pacific, and the Gulf. Together, these regions show that the convenience food retail market is expanding through 2 distinct paths: deeper monetization in mature networks and new convenience adoption in underpenetrated corridors.

Competitive Landscape

The convenience food retail market remained highly fragmented in 2025, with a large base of independent and regional operators, even though global leaders held stronger food, data, and capital capabilities. The main international names continue to include 7-Eleven and Seven & i Holdings, FamilyMart, Alimentation Couche-Tard, FEMSA and OXXO, and Lawson, but the convenience food retail market does not concentrate enough store ownership in this group to behave like a tightly controlled oligopoly. That is why scale advantages are more evident in menu innovation, private-label rollout, digital engagement, and acquisition capacity than in simple store-count dominance. Seven & i and Couche-Tard disclosures both show steady investment in food-led assortment and network quality, which reinforces the operating gap between global leaders and smaller chains. In the convenience food retail market, the best-capitalized operators are not winning by offering the lowest price on every item. They are winning by making the store visit more useful, more frequent, and more profitable.

A recent strategy by leading chains shows 3 recurring priorities across the convenience food retail market. First, operators are buying or building better foodservice assets, as seen in Couche-Tard’s GetGo acquisition and Casey’s continued food-led expansion. Second, they are using destination formats to expand the trip, as seen in Circle K’s EV-only hub and ADNOC’s larger roadside concept. Third, they are improving their proprietary food and private-brand control, as shown by Seven & i’s bakery rollout, new Live-Meal plans, and expansion of their private-brand offerings. These moves are important because the convenience food retail market now rewards chains that can combine speed with a differentiated food proposition. They also show that strategic competition is moving away from tobacco dependence and toward a broader daily-needs platform.

White-space opportunities in the convenience food retail market are strongest where EV dwell time, fresh food attachment, and data-led repeat purchasing can be combined within a single operating model. The convenience food retail market also has room for more disciplined private-label expansion, especially where regulation and value pressure make controlled assortment more attractive. At the same time, heavier reliance on loyalty platforms, ordering systems, and connected store technology means cybersecurity and systems integration are becoming more material to execution quality. For the convenience food retail market, this creates a clear divide between operators that can scale modern retail infrastructure and those that remain tied to narrower legacy economics.

Convenience Food Retail Industry Leaders

7-Eleven Inc.

FamilyMart Co., Ltd.

Alimentation Couche-Tard Inc.

FEMSA / OXXO

Lawson, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cumberland Farms agreed to acquire Coen Markets (54 operating sites and 3 new-to-industry locations in development across Pennsylvania, Ohio, and West Virginia), accelerating EG Group's food-forward convenience footprint in the US Northeast.

- March 2026: Alimentation Couche-Tard completed 80 new-to-industry openings through Q3 of fiscal 2026, with 58 stores under construction, and outlined a 5-year plan to add at least 750 stores through new construction and single-site acquisitions.

- March 2026: Casey's General Stores revised fiscal 2026 EBITDA growth guidance upward to 18-20%, guided inside same-store sales growth of 3.5-4.5%, confirmed at least 80 new store openings during fiscal 2026, and reported nicotine pouch sales up 31% and vapor products up 12% year-on-year, diversifying beyond its food-led core.

- November 2025: ADNOC Distribution opened the first "The Hub by ADNOC" destination-format convenience location in Abu Dhabi, with 6 sites planned by end-2025 and 30 by 2030; initial sites achieved 90% retail-unit lease occupancy at opening, and the format targets USD 30 million annual EBITDA by 2030.

Global Convenience Food Retail Market Report Scope

| Staple Products |

| Impulse Products |

| Emergency Products |

| Kiosks |

| Mini Convenience Stores |

| Limited Selection Convenience Stores |

| Traditional Convenience Stores |

| Expanded Convenience Stores |

| Hyper Convenience Stores |

| Independent Stores |

| Franchise Stores |

| Corporate-Owned Chains |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Staple Products | |

| Impulse Products | ||

| Emergency Products | ||

| By Store Type | Kiosks | |

| Mini Convenience Stores | ||

| Limited Selection Convenience Stores | ||

| Traditional Convenience Stores | ||

| Expanded Convenience Stores | ||

| Hyper Convenience Stores | ||

| By Ownership Model | Independent Stores | |

| Franchise Stores | ||

| Corporate-Owned Chains | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is driving growth in convenience food retail through 2031?

A shift toward fresh-prepared food, stronger private-label programs, loyalty integration, and investment in destination-format stores is supporting growth. The category is projected to rise from USD 1.27 trillion in 2026 to USD 1.81 trillion by 2031 at a 7.3% CAGR.

Which product type is growing fastest in this space?

Impulse products are forecast to grow at 7.98% through 2031, helped by better food-to-go ranges, stronger merchandising, and more proprietary product launches.

Which store format is expanding the quickest?

Hyper convenience stores are projected to grow at 8.34% through 2031 because they combine food service, EV charging, loyalty tools, and larger destination-style layouts.

Why is food service so important for convenience operators?

Food service plays a larger role in profit than its sales share suggests. In the United States, it represented 28.5% of in-store sales in 2025 but contributed 38.9% of gross profit.

Which ownership model leads globally today?

Franchise stores led the global revenue mix in 2025 with a 44.85% share, while corporate-owned chains are expected to grow faster at 8.81% through 2031.

Which region is the largest and which is growing fastest?

Asia-Pacific held the largest share in 2025 at 35.98%, while the Middle East and Africa are forecast to post the fastest growth at 7.89% through 2031.

Page last updated on: