Ozempic Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

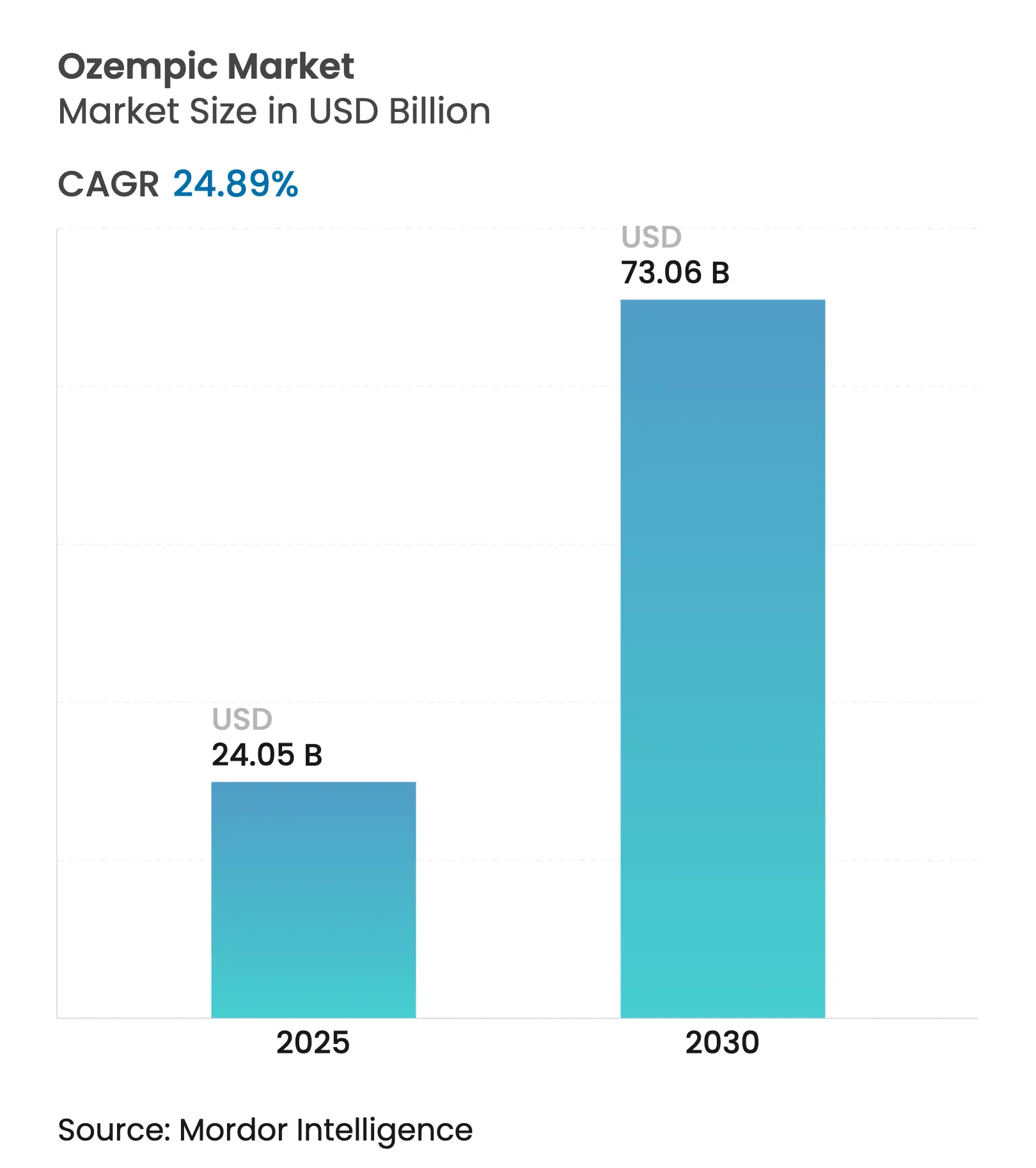

| Market Size (2025) | USD 24.05 Billion |

| Market Size (2030) | USD 73.06 Billion |

| Growth Rate (2025 - 2030) | 24.89 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

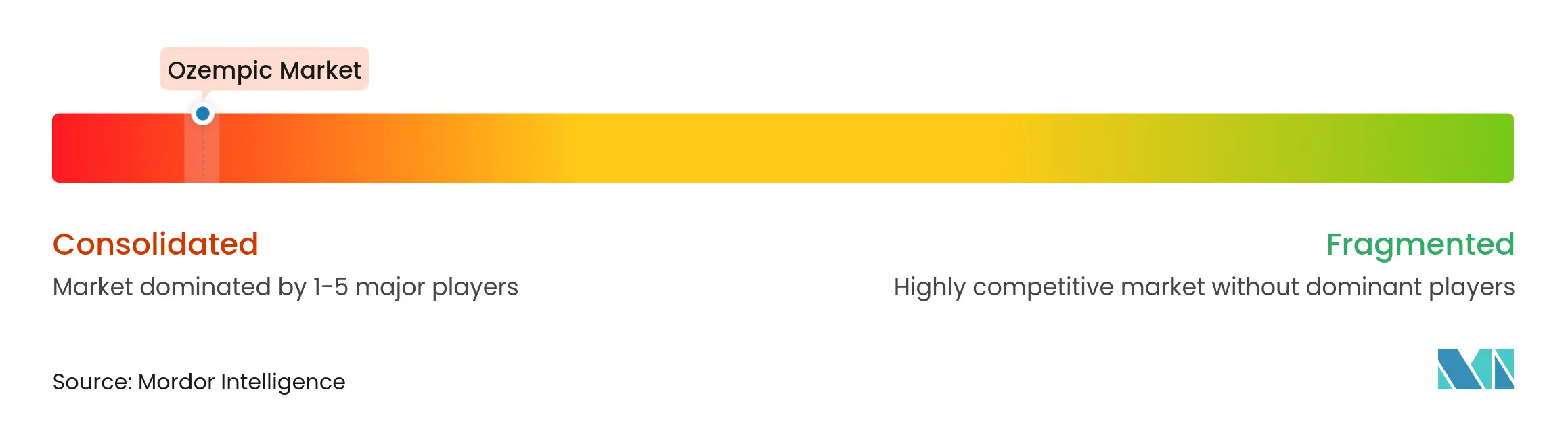

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ozempic Market Analysis by Mordor Intelligence

This sharp trajectory mirrors supply stabilization, aggressive manufacturing scale-up, and expanding clinical indications that are redefining metabolic care worldwide. Novo Nordisk’s USD 9 billion global capacity build-out, the FDA’s February 2025 shortage resolution, and broadening payer acceptance collectively accelerate therapeutic uptake, while duopoly dynamics intensify competitive positioning. Rising obesity prevalence, digital prescription pathways, and an expanding evidence base for cardiovascular and renal benefits further reinforce demand. At the same time, looming Medicare price negotiations and patent expirations introduce pricing uncertainty that could reshape value capture.

Key Report Takeaways

- By geography, North America led with a 69.97% market share in 2024; Asia-Pacific is projected to grow at a 5.01% CAGR through 2030.

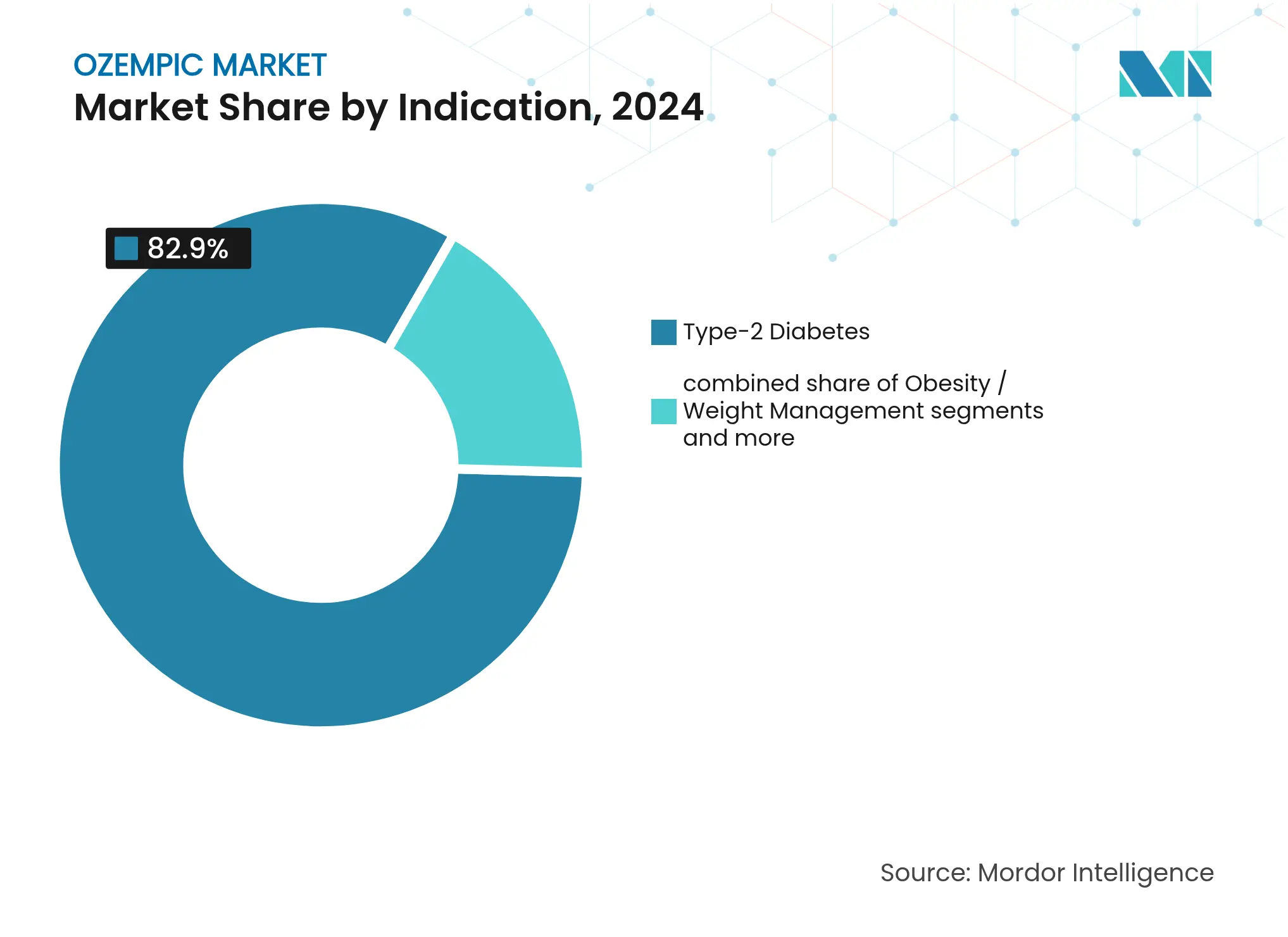

- By indication, Type 2 diabetes accounted for 82.90% of the Ozempic market size in 2024, while obesity and weight management is expanding at a 4.82% CAGR to 2030.

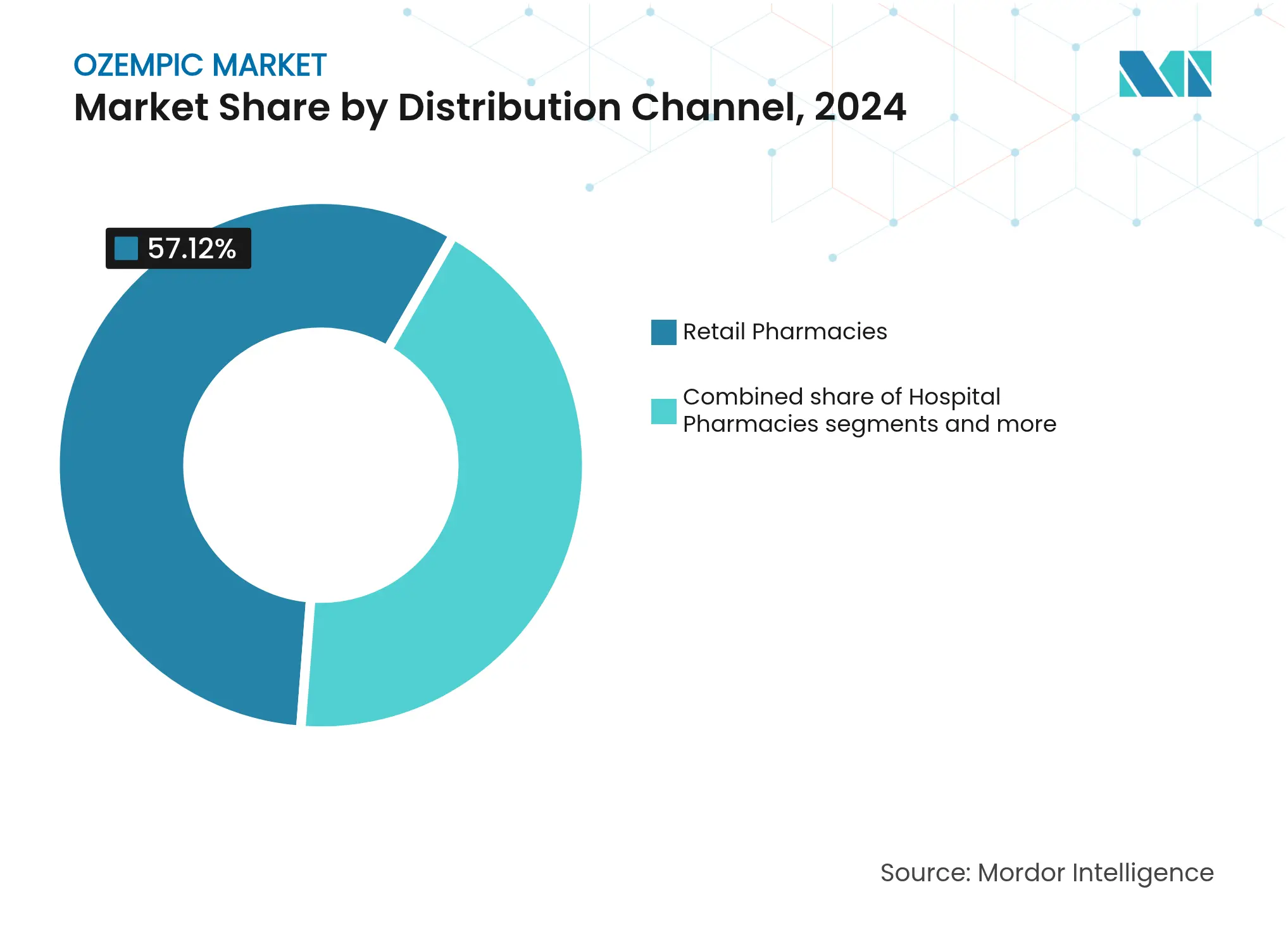

- By distribution channel, retail pharmacies held 57.12% of the Ozempic market in 2024; tele-health platforms record the fastest growth at a 4.80% CAGR through 2030.

Global Ozempic Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High list price & variable reimbursement hurdles High list price & variable reimbursement hurdles | -4.8% | Global, most acute in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-4.8% | Geographic Relevance:Global, most acute in emerging markets | Impact Timeline:Medium term (2-4 years) |

Injectable delivery deters needle-averse patients Injectable delivery deters needle-averse patients | -2.1% | Global, cultural variations in acceptance | Long term (≥ 4 years) | |||

Global supply shortages due to device-fill capacity limits Global supply shortages due to device-fill capacity limits | -1.9% | Global, resolved but capacity constraints remain | Short term (≤ 2 years) | |||

Emerging safety-signal scrutiny (gastroparesis lawsuits) Emerging safety-signal scrutiny (gastroparesis lawsuits) | -1.6% | North America primarily, regulatory spillover risk | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Global Prevalence of Type-2 Diabetes

More than 700 million adults are projected to live with diabetes by 2030, enlarging the eligible patient base that anchors long-run demand for the market[1]Source: U.S. Food and Drug Administration, “FDA Ends Shortage Listing for Semaglutide,” fda.gov . An aging demographic in developed economies aligns with rising obesity in emerging regions, creating a dual-vector growth engine. China alone is expected to surpass 500 million overweight or obese adults by 2033, a figure that eclipses the entire North American population. Regulatory agencies increasingly endorse GLP-1 receptor agonists as first-line therapy, broadening access across payers. Expanded labeling for renal protection, secured in January 2025, now positions Ozempic as a multifaceted metabolic intervention[2]Source: U.S. Food and Drug Administration, “Ozempic Secures Renal-Protection Indication,” fda.gov . These converging trends establish a resilient demand floor that supports continued double-digit volume growth.

Superior HbA1c and Weight-Loss Efficacy versus Legacy GLP-1s

Semaglutide’s clinical profile consistently outperforms earlier-generation GLP-1 analogs, with high-dose regimens achieving 20.7% weight loss in the STEP UP trial, far ahead of historical benchmarks. The combined glycemic and weight-reduction benefit simplifies treatment regimens that previously required multiple agents, thereby enhancing adherence and healthcare efficiency. Cardiovascular outcome data reveal risk-reduction advantages that extend therapeutic value beyond glucose control, strengthening the product’s positioning in evidence-based guidelines. Health-economic models show that reduced hospitalization and complication rates offset higher acquisition costs over time, a finding that resonates with payers seeking long-term cost containment. Competitive follow-on molecules now require significant differentiation to match these outcomes.

Expanding Obesity Prescriptions via Tele-Health Platforms

Digital health firms report a seven-fold rise in non-diabetic patients initiating GLP-1 therapy between 2021 and 2025, reflecting new demand unlocked by virtual care convenience. Platforms such as LillyDirect integrate diagnostics, prescription, and home delivery, reducing friction that traditionally impeded obesity pharmacotherapy. Privacy and stigma concerns are mitigated by remote consultations, thereby engaging patient segments historically under-treated in brick-and-mortar settings. The FDA’s April 2025 guidance clarifying compounding policies fostered a shift from unregulated channels to compliant tele-health providers. As wearable-linked monitoring and automated refill programs mature, tele-health’s share of the Ozempic market is set to expand in both developed and select emerging economies.

Employer-Sponsored Insurance Adding GLP-1 Coverage

In 2024, 96% of large U.S. employers covered GLP-1s for diabetes, and a growing subgroup now adds weight-management indications, reflecting an awareness of productivity gains from healthier workforces. Benefit design innovations such as lifetime caps, body mass index thresholds, and step-therapy protocols help employers manage near-term spending while still granting access. Expanded coverage directly lifts prescription volumes, particularly for commercially insured adults aged 35-54 who display high responsiveness to employer benefit changes. Multinational corporations adopting harmonized policies across North America and Europe further amplify demand. As long-term data continue to validate reductions in absenteeism and comorbidity costs, employer plans represent an enduring incremental driver.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High list price & variable reimbursement hurdles High list price & variable reimbursement hurdles | -4.8% | Global, most acute in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-4.8% | Geographic Relevance:Global, most acute in emerging markets | Impact Timeline:Medium term (2-4 years) |

Injectable delivery deters needle-averse patients Injectable delivery deters needle-averse patients | -2.1% | Global, cultural variations in acceptance | Long term (≥ 4 years) | |||

Global supply shortages due to device-fill capacity limits Global supply shortages due to device-fill capacity limits | -1.9% | Global, resolved but capacity constraints remain | Short term (≤ 2 years) | |||

Emerging safety-signal scrutiny (gastroparesis lawsuits) Emerging safety-signal scrutiny (gastroparesis lawsuits) | -1.6% | North America primarily, regulatory spillover risk | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High List Price and Variable Reimbursement Hurdles

Annual therapy costs nearing USD 15,000 per patient challenge affordability in both public and private systems, prompting price negotiations that target 33% discounts for Medicare starting 2027. Medicaid programs have tightened formularies, while some state employee plans removed coverage for weight-management indications, reducing short-term uptake. International reference pricing exerts downward pressure in Europe and Latin America, and out-of-pocket exposure restricts penetration in much of Asia-Pacific. Manufacturers respond with patient-assistance programs and value-based agreements that tie reimbursement to real-world outcomes. Despite these mitigations, pricing frictions remain a headwind, especially in lower-income countries where co-payment burdens limit adherence.

Emerging Safety-Signal Scrutiny

Rising litigation over gastroparesis and gastrointestinal events has heightened regulatory surveillance, with over 455 adverse reports linked to compounded semaglutide formulations as of 2025. While the branded product maintains a favorable benefit-risk profile, intensified monitoring could lead to additional label language or mandatory risk-evaluation programs. Physicians may adopt more stringent patient-selection criteria and counseling protocols, potentially slowing initiation rates in borderline cases. Media coverage amplifies consumer concerns, though real-world evidence continues to show low absolute incidence of severe events. Sustained pharmacovigilance and transparent communication will be pivotal in maintaining prescriber confidence.

Segment Analysis

By Indication: Diabetes Dominance with Obesity Acceleration

Type 2 diabetes commanded 82.90% of the Ozempic market in 2024, reflecting entrenched reimbursement pathways and clinical familiarity among endocrinologists. The segment’s absolute revenue growth remains solid, yet its proportional share will decline as obesity prescriptions rise. Obesity and weight management is projected to post a 4.82% CAGR through 2030 as payers expand coverage and tele-health platforms ease access barriers. Cardiovascular risk-reduction use, pending regulatory review, could accelerate adoption across cardiology practices, opening new referral pathways.

Clinical research signals potential entry into Type 1 diabetes, where early studies show insulin-sparing effects with improved glycemic stability, suggesting a long-term opportunity once confirmatory trials mature. Investigations into metabolic dysfunction-associated steatohepatitis and neurodegenerative disorders hint at future horizons that could transform Ozempic into a platform therapy. Such diversification lowers dependence on a single disease state and buffers revenue against competition from next-generation molecules.

By Distribution Channel: Retail Leadership with Digital Disruption

Retail pharmacies held 57.12% of global volume in 2024, leveraging insurance connectivity and pharmacist counseling to reinforce adherence. Their omnichannel evolution, including drive-thru pickups and automated text refill reminders, sustains relevance even as digital models grow. Tele-health platforms, though starting from a smaller base, are the fastest-growing outlet with a 4.80% CAGR forecast to 2030, driven by direct-to-consumer marketing and seamless supply logistics. The Ozempic market size channeled through virtual care could top USD 9 billion by the end of the decade if current adoption curves persist. Hospital pharmacies retain importance for complex cases requiring close monitoring, particularly those with multi-organ complications. Online and mail-order services appeal to cost-sensitive segments, but regulatory crackdowns on unauthorized compounding have shifted volumes back toward licensed dispensers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated the largest revenue share at 69.97% in 2024, underpinned by high insurance penetration, early regulatory approvals, and strong clinical guideline support. Medicare price negotiations, set to take effect in 2027, will temper revenue expansion but could widen patient access. Tele-health uptake is especially pronounced in the United States, where digital literacy and employer health benefits converge. Canada follows similar patterns, although formulary differences produce varied provincial adoption rates.

Asia-Pacific registers the fastest growth at a 5.01% CAGR through 2030. China leads regional demand, buoyed by rapid urbanization, growing disposable income, and escalating obesity prevalence. Patent expiry in 2026 will invite generic entrants, likely suppressing price points yet expanding overall treatment access. Japan and South Korea exhibit high per-capita spending and favor innovative therapies, while India’s gradual reimbursement reforms signal medium-term upside. Australia remains supply constrained even after global shortage resolution, highlighting persistent demand-supply imbalance.

Europe shows steady uptake anchored by evidence-based national health systems. The European Medicines Agency’s favorable opinion for renal-protection use extends reimbursement across member states. Germany, France, and the United Kingdom dominate volumes due to established obesity management frameworks. South America presents nascent yet rising consumption, led by Brazil where Novo Nordisk’s USD 1 billion manufacturing expansion supports local availability. The Middle East and Africa trail in absolute volumes but offer long-run potential as non-communicable disease burdens rise and healthcare infrastructure strengthens.

Competitive Landscape

Market Concentration

Novo Nordisk controlled 2024 revenue, reflecting high manufacturing complexity, extensive clinical data requirements, and entrenched brand loyalty. Novo Nordisk’s USD 9 billion capacity investment program along with its USD 11 billion Catalent acquisition enlarges injectable pen and active pharmaceutical ingredient output, targeting both shortage mitigation and margin optimization. Eli Lilly counters with tirzepatide franchise expansion and the launch of LillyDirect, a vertically integrated digital channel aimed at reinforcing patient retention.

Pipeline activity intensifies as competitors pursue dual-agonist mechanisms, oral formulations, and alternative delivery devices. Viking Therapeutics advanced VK2735 into Phase 2 trials, reporting 14.7% weight loss that signals credible late-stage competition. Generic manufacturers prepare to enter the Chinese market post-2026, potentially introducing price competition and accelerating volume growth. Strategic alliances between biotech innovators and contract development organizations aim to overcome scale-up hurdles. Meanwhile, regulatory scrutiny on compounding pharmacies protects branded incumbents by eliminating gray-market leakage.

Sustainability commitments also shape competitive narratives, with leading firms investing in renewable energy for manufacturing and eco-friendly device materials to align with emerging payer sustainability criteria. Marketing efforts increasingly emphasize long-term health-economic benefits to regulators and payers, while direct-to-consumer campaigns reinforce brand recognition amid growing molecule-class parity.

Ozempic Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Novo Nordisk announced FDA acceptance of its filing for oral semaglutide 25 mg for chronic weight management, positioning the company to address needle-averse segments with a once-daily tablet format

- January 2025: Ozempic received FDA approval for kidney-protection in adults with Type 2 diabetes, reducing the risk of kidney failure

Table of Contents for Ozempic Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising global prevalence of type-2 diabetes

- 4.2.2Superior HbA1c & weight-loss efficacy vs. legacy GLP-1s

- 4.2.3Expanding obesity prescriptions via tele-health platforms

- 4.2.4Employer-sponsored insurance adding GLP-1 coverage

- 4.2.5Social-media–driven consumer demand spill-over

- 4.2.6Planned cardiovascular-risk-reduction label expansion

- 4.3Market Restraints

- 4.3.1High list price & variable reimbursement hurdles

- 4.3.2Injectable delivery deters needle-averse patients

- 4.3.3Global supply shortages due to device-fill capacity limits

- 4.3.4Emerging safety-signal scrutiny (gastroparesis lawsuits)

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Industry Rivalry

5. Market Size & Growth Forecasts (Value, USD Mn)

- 5.1By Indication

- 5.1.1Type-2 Diabetes

- 5.1.2Obesity / Weight Management

- 5.1.3Cardiovascular-Risk-Reduction (anticipated)

- 5.1.4Other Emerging Uses

- 5.2By Distribution Channel

- 5.2.1Hospital Pharmacies

- 5.2.2Retail Pharmacies

- 5.2.3Online / Mail-Order Pharmacies

- 5.2.4Tele-health Platforms

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2Japan

- 5.3.3.3India

- 5.3.3.4South Korea

- 5.3.3.5Australia

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4South America

- 5.3.4.1Brazil

- 5.3.4.2Argentina

- 5.3.4.3Rest of South Ameroca

- 5.3.5Middle East and Africa

- 5.3.5.1GCC

- 5.3.5.2Saudi Arabia

- 5.3.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.2.1Novo Nordisk

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ozempic Market Report Scope

Ozempic is a weekly injection that helps lower blood sugar by helping the pancreas make more insulin. The Ozempic market is segmented by Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America).

The report offers the value (in USD) and volume (in units) for the above segments.