Global Halitosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

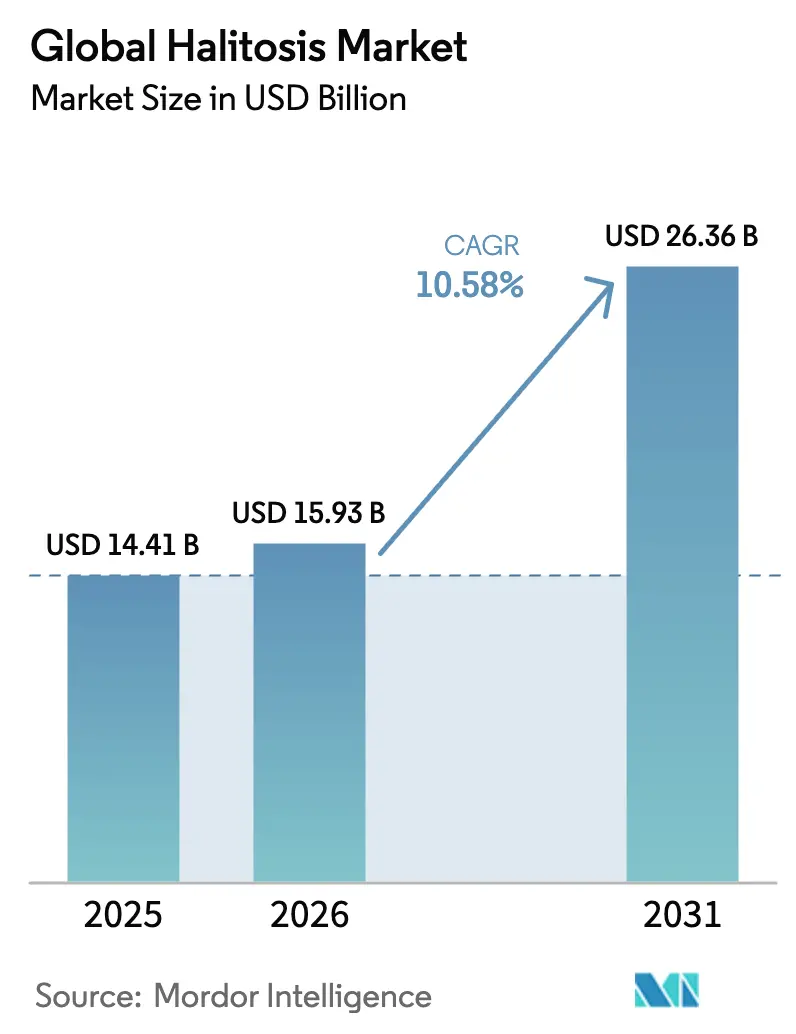

| Market Size (2026) | USD 15.93 Billion |

| Market Size (2031) | USD 26.36 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Halitosis Market Analysis by Mordor Intelligence

The halitosis market size is expected to grow from USD 14.41 billion in 2025 to USD 15.93 billion in 2026 and is forecast to reach USD 26.36 billion by 2031 at 10.58% CAGR over 2026-2031. Rising consumer awareness of the oral-systemic health connection, accelerating geriatric demographics affected by xerostomia, and a steady flow of microbiome-friendly product launches underpin this growth trajectory. At the same time, AI-enabled breath-analysis devices facilitate early detection, moving therapy initiation from the clinic to the home. Incumbent brands are acquiring science-backed challengers rather than developing technology from scratch, exemplified by Church & Dwight’s high-profile TheraBreath purchase. Nevertheless, social stigma, an absence of reimbursement codes, and chlorhexidine-linked taste alteration curb faster treatment adoption, leaving substantial headroom for innovation.

Key Report Takeaways

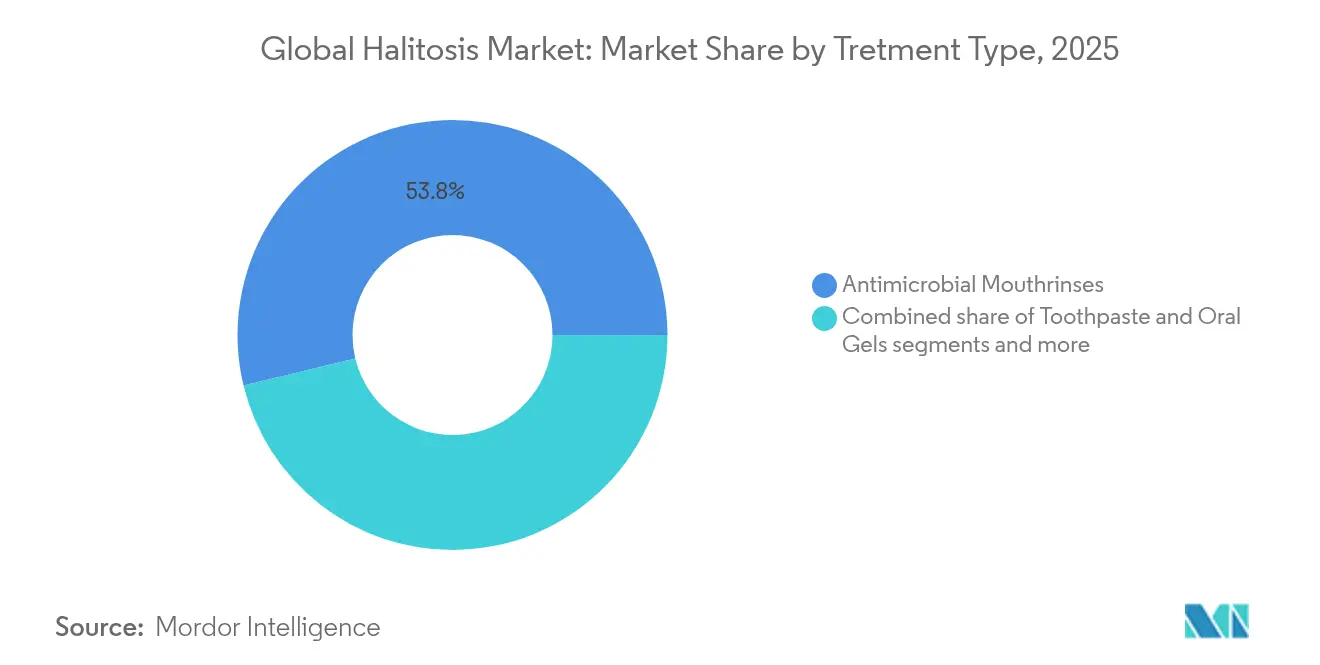

- By product type, antimicrobial mouthrinses commanded 53.78% of the halitosis market share in 2025.

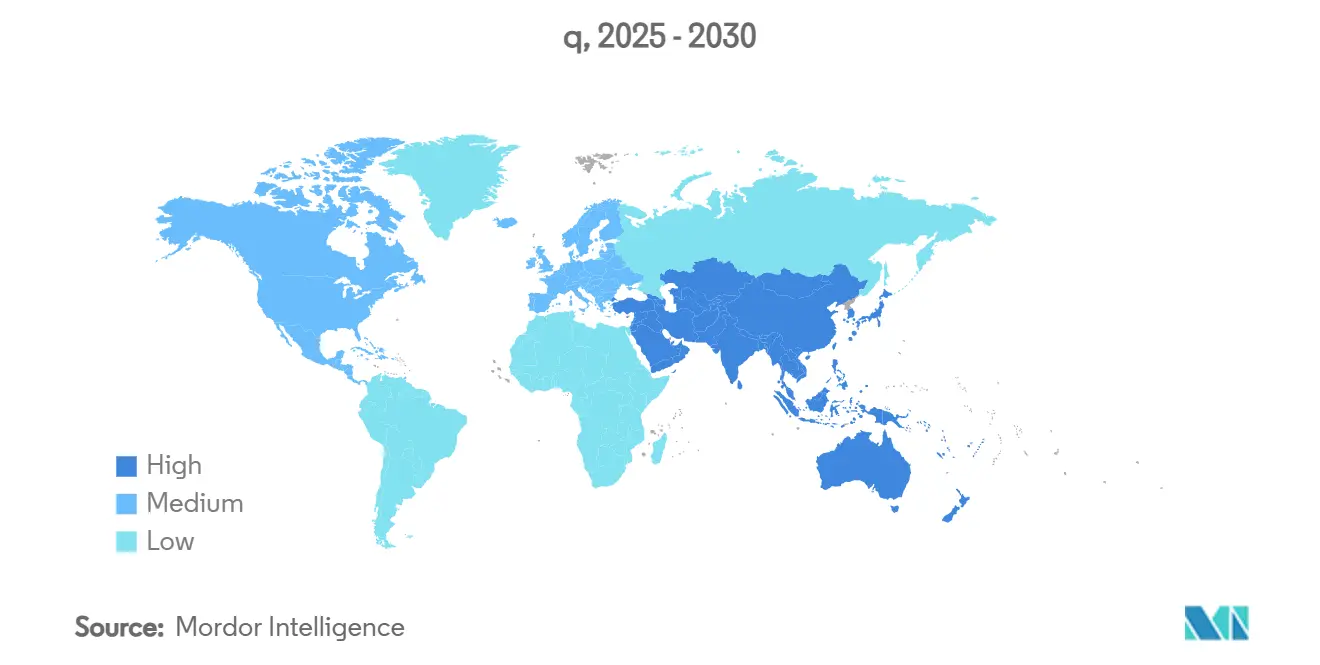

- Asia-Pacific is projected to log the fastest 12.67% CAGR through 2031, outpacing every other region.

- Chlorhexidine-based antiseptics retained a 40.42% portion of the halitosis market size in 2025, though zinc formulations are accelerating at 13.02% CAGR.

- Homecare captured 46.35% of global revenue in 2025, reflecting a decisive pivot toward preventive self-care.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Halitosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of periodontal disease & poor oral hygiene | +2.1% | Global, with highest impact in APAC and MEA | Medium term (2-4 years) |

| Growing geriatric population with xerostomia-linked halitosis | +1.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Proliferation of OTC oral-care SKUs via e-commerce platforms | +1.4% | Global, led by North America and China | Short term (≤ 2 years) |

| Breakthrough oral-microbiome probiotics & synbiotics | +1.6% | North America & EU regulatory approval, APAC adoption | Medium term (2-4 years) |

| Smartphone-connected halitosis sensors enabling self-diagnosis | +0.9% | Tech-forward markets: US, Japan, South Korea | Medium term (2-4 years) |

| Employer dental-wellness programs mandating breath screening | +0.7% | Corporate-heavy regions: North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of periodontal disease & poor oral hygiene

Severe periodontitis affected more than 1 billion people in 2024 and could reach 1.56 billion by 2050, enlarging the addressable base for the halitosis market. Western sub-Saharan Africa and Qatar post the world’s highest incidence among young adults, underscoring unmet therapy needs in emerging economies. Laboratory work reveals how Fusobacterium nucleatum and Streptococcus gordonii synergistically boost methyl-mercaptan, a principal malodor culprit. Social determinants—low income and limited dental access—strongly influence disease burden, directing demand toward affordable zinc rinses and probiotic tablets.

Growing geriatric population with xerostomia-linked halitosis

Thirty percent of adults aged 65 plus report chronic dry mouth, a problem worsened by more than 400 xerogenic medications. Oral frailty now affects one quarter of seniors worldwide, and the WHO lists 280 million older adults living with untreated oral disorders. Diabetes compounds risk; diabetic seniors show 20.4% caries prevalence versus 18.6% in non-diabetics. Assisted-living centers in the United States, Canada, and Germany have started routine breath screening, boosting institutional sales of moisturizing mouth-sprays.

Proliferation of OTC oral-care SKUs via e-commerce platforms

Post-pandemic consumers draw a strong link between oral care and overall wellness; 92% of US adults express this belief. Niche halitosis startups exploit social-commerce channels to bypass tight retail shelf space, accelerating penetration of probiotic sprays. Malaysia illustrates how digital channels fill access gaps: 94% of adults cite gum issues, and premium zinc rinses are now shipped nationwide within 48 hours. Younger buyers insist on clean labels, discouraging alcohol and demanding proof-of-efficacy links embedded in QR codes.

Breakthrough oral microbiome probiotics & synbiotics

Randomized studies prove that targeted probiotics can halve malodor scores when paired with routine brushing. BLIS K12 and M18 strains demonstrated durable mucosal colonization, prompting a 2025 China rollout. Probiotic toothpastes carry live Streptococcus salivarius M18 and maintain fluoride compatibility. ASEAN harmonization of nutraceutical rules streamlines product registrations, encouraging multi-country launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chlorhexidine-related taste alteration & staining | -1.2% | Global, long-term users | Short term (≤ 2 years) |

| Consumer substitution with home remedies & sugar-free gum | -0.8% | Developing markets | Medium term (2-4 years) |

| Absence of reimbursement or clinical guidelines | -1.1% | US, Canada, EU | Long term (≥ 4 years) |

| Social stigma delays diagnosis | -0.9% | Cultures with oral-health taboos | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chlorhexidine-related taste alteration & tooth-staining

Chlorhexidine rinses increase buccal-cell micronuclei and trigger bitter aftertaste plus brown staining, undermining adherence. Black tea or red wine worsen discoloration, though adding milk halves stain persistence. Hyperpure chlorine dioxide and zinc-ion rinses show comparable antimicrobial efficacy without sensory drawbacks. Honey mouthwash trials confirm equivalent plaque reduction but much lower adverse-effect incidence, steering dentists toward natural alternatives.

Absence of reimbursement / clinical guidelines for halitosis

Medicare still categorizes halitosis management as cosmetic and excludes it from coverage. The FDA’s dental-device code lacks a distinct halitosis sub-category, complicating filings for breath-analysis startups. Without standardized diagnostic grades, practitioners hesitate to adopt pay-for-outcome models. The WHO pegs global oral-disease costs at USD 387 billion annually, yet halitosis remains off universal-coverage agendas

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Antimicrobials Retain the Lion’s Share

Antimicrobial mouthrinses delivered 53.78% of the halitosis market size in 2025, benefiting from instant volatile-sulfur suppression and dentist endorsements. Listerine Clinical Solutions supplies 67% more zinc than leading peers, promising 24-hour freshness in double-blind trials. Toothpastes and gels rank second, as daily habit loops drive volume; probiotic SKUs add a premium tier. Probiotic sprays and lozenges post the fastest 15.12% CAGR; clinical data show 50% odor reduction over eight weeks. Chewing gum and mints maintain steady demand thanks to portability. Collectively, diversified portfolios cushion the halitosis market against single-category volatility.

By Drug Class: Antiseptics Rule, but Metal Ions Rise

Chlorhexidine antiseptics still comprise 40.42% of 2025 sales value but face headwinds on safety perception. Zinc-ion formulations cut malodor without staining, adding share swiftly. Hyperpure chlorine dioxide demonstrated non-inferiority to 0.12% chlorhexidine in 2024 clinical work. Enzyme-activated rinses and peptide antimicrobials such as ε-poly-L-lysine achieved 50.3% volatile-compound reduction versus 32.1% for standard rinses. Expect metal-ion and oxygenating classes to outgrow the overall halitosis market by roughly 250 basis points through 2031.

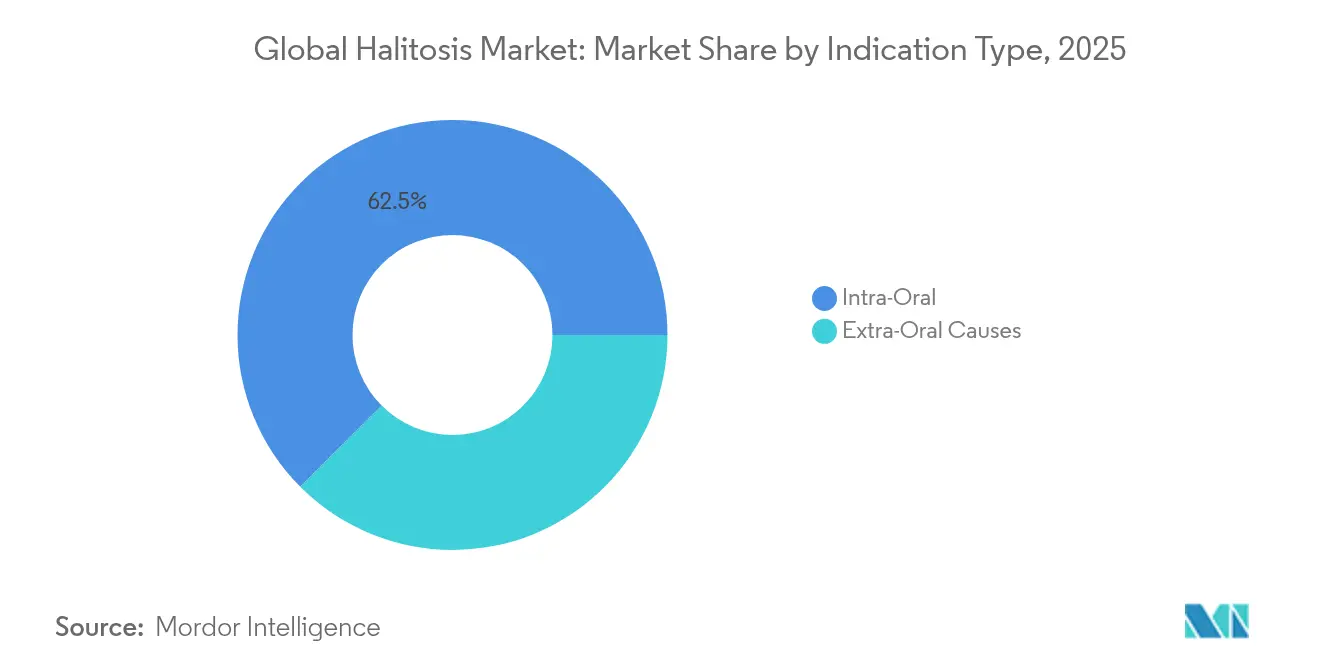

By Indication: Intra-Oral Causes Dominate

Intra-oral etiologies—tongue coating, plaque, periodontal pockets—generated 62.48% of 2025 treatment demand. Fluorescence-based tongue biofilm indices enable evidence-based monitoring, while chair-side oral-chromatography devices yield precise volatile-compound fingerprints in three minutes. Extra-oral malodor driven by chronic kidney disease or uncontrolled diabetes forms the remainder, with dimethyl sulfide levels highest in young CKD patients. Integrated medical-dental care pathways are emerging to tackle multifactorial cases.

By End User: Homecare Leads; CDMOs Grow Fastest

Homecare held 46.35% of 2025 revenue, as consumers equip bathrooms with smart brushes, tongue scrapers, and AI-guided rinses. CDMOs/CMOs log 12.21% CAGR by providing fermentation capacity and regulatory dossiers for probiotic brands. Dental clinics remain vital for persistent halitosis linked to periodontitis, while hospitals manage extra-oral cases in comorbid patients. Tele-dentistry platforms now integrate breath-sensor feeds, sending curated home-treatment packs directly to users.

Geography Analysis

North America controlled 41.85% of global sales in 2025, supported by venture-capital inflows of USD 400.2 million into oral-tech startups. US employers bundle breath checks into workplace wellness, driving corporate-bulk orders. Canada benefits from pilot reimbursement for low-income seniors.

Asia-Pacific represents the fastest-expanding halitosis market, poised for a 12.67% CAGR through 2031. China’s probiotic adoption accelerates thanks to nutraceutical-friendly rules, while Japan’s workforce embraces app-linked sensors. India’s health-supplement boom at 20.35% CAGR and ASEAN harmonization smooth cross-border product launches.

Europe remains a mature yet opportunity-rich arena: aging populations, strong universal coverage, and clinician pushback against chlorhexidine staining encourage zinc and probiotic alternatives. South America and Middle East & Africa together deliver double-digit growth, driven by urbanization and wider dental insurance uptake. Pack sizes and price points are localized—100 ml sachets and herbal rinses—to match purchasing power yet retain efficacy.

Competitive Landscape

The halitosis market is moderately consolidated: the top five brands—Johnson & Johnson, Colgate-Palmolive, Procter & Gamble, Church & Dwight, and Kenvue—held about half of 2024 revenue. Listerine Clinical Solutions, Colgate Total, Crest Scope, and TheraBreath dominate shelf visibility, leveraging mass marketing and cross-category loyalty programs.

Church & Dwight’s USD 580 million TheraBreath acquisition exemplifies value-chain consolidation aimed at alcohol-free, science-based segments. New-Zealand-based BLIS Technologies focuses on patented probiotic strains and licenses them to regional distributors in China and Southeast Asia. Meanwhile, US startups such as MintAI launch IoT breath sensors, collecting anonymized data sets that feed machine-learning models; Oral-B’s iO brushes already integrate third-party sensor APIs.

Patent activity is brisk: more than 600 fresh families citing “volatile sulfur compound neutralization” were filed from 2022 through 2024, a jump of 18% year-on-year according to WIPO’s PATENTSCOPE data. Pharmacy chains respond with private-label zinc rinses, squeezing mid-tier incumbents and steering the halitosis market toward a barbell structure of premium science-backed and value SKUs.

Global Halitosis Industry Leaders

Dabur India

Colgate Palmolive

Johnson & Johnson

P&G

Oracare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BLIS Technologies announced expansion of oral probiotic sales in China, focusing on BLIS K12 and BLIS M18 strains specifically targeting halitosis treatment.

- May 2024: Kenvue Professional introduced Listerine Clinical Solutions mouthwash with 67% more zinc than competing products, clinically proven to neutralize bad breath for 24 hours

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the halitosis market covers products and clinical solutions used to identify, manage, or reduce bad breath, across at home use and professional care settings, and reported as revenue generated from these offerings across regions.

Scope exclusions: Cosmetic oral care that is not positioned for breath management, and general dental consumables that do not address odor causes, are not counted.

Segmentation Overview

- By Product Type

- Antimicrobial Mouthrinses

- Toothpaste & Oral Gels

- Probiotic Sprays & Lozenges

- Chewing Gum & Mints

- By Drug Class

- Antiseptics (Chlorhexidine, CPC)

- Zinc & Metal Ion Formulations

- Chlorine Dioxide & Chlorite

- Others (e.g., Oxygenating Agents)

- By Indication

- Intra-Oral Causes

- Extra-Oral Causes

- By End User

- Dental Clinics

- Hospitals

- Homecare

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the core fact base, so the later market model stayed anchored to real world oral health and consumer care signals. We reviewed public health and dental statistics that show how common oral conditions are, and how treatment seeking tends to change by age and region.

Common reference sources included publications and data portals such as the World Health Organization, the US Centers for Disease Control and Prevention, national health ministries, and oral health bodies such as the FDI World Dental Federation and dental associations. We also used peer reviewed journals for prevalence ranges and clinical practice patterns, alongside company annual reports, investor presentations, and reputable press for product launches and geographic expansion cues. In addition, we checked patent databases and a paid subscription covering company financials and news to validate timelines and pricing narratives. This list is illustrative, and many other sources were also consulted for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming which solutions are actually used for halitosis management and what drives purchase frequency in each channel. We spoke with dental professionals, distributors, retail category managers, and product specialists across key regions to validate assumptions on adoption, typical price points, and the split between at home products and clinic based diagnostics or treatments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 43% |

| Mid tier: 49% | Functional/Unit leaders: 35% | EMEA: 30% |

| Smaller Players: 14% | Managers: 52% | Americas: 27% |

Market-Sizing & Forecasting

Sizing started with a top down build that reconstructs the demand pool using oral care spending patterns and condition driven usage, which is then filtered through how halitosis is treated in practice (self care versus professional care). Once the regional totals were formed, selective bottom-up checks were run using sampled volume by channel, typical prices, and a supplier and distributor roll up, and then the model was adjusted where gaps appeared.

Inputs that mattered most included: prevalence ranges for intra-oral and extra-oral causes, the share of consumers that actively purchase breath management products, typical purchase frequency by format (rinses, gels, lozenges, gum), average selling prices by channel, and the mix shift toward premium or medicated options. We also tracked dental visit rates and periodontal care trends, because these influence the professional pathway for diagnosis and treatment. Where a country level input was not available, values were bridged using proxy indicators like population age mix, oral hygiene penetration, and retail channel maturity, and then stress tested through interviews.

Forecasts were built using scenario analysis supported by exponential smoothing on key drivers, so short term volatility did not distort the long range outlook. Assumptions on pricing and mix were revisited region by region with expert feedback, and then the final forecast path was aligned with realistic adoption ceilings rather than a straight line growth curve.

Data Validation & Update Cycle

Validation was done through multiple passes, starting with checks against independent signals such as oral care category growth, clinic footfall direction, and pricing movement seen in the market. When a region showed unusual jumps or an out of pattern share shift, we revisited the inputs, rechecked conversions, and contacted sources again if the variance could not be explained.

Before sign off, the full model is reviewed by another analyst to confirm logic consistency, year to year coherence, and that inputs used are traceable to sources or interview learnings. Reports are refreshed annually, and interim updates are made when material events occur that can change pricing, availability, or channel mix. Right before delivery, a final data pass is completed so clients receive the most current view.

Mordor Intelligence's Global Halitosis Market Sizing Compared With Other Published Estimates

Published market values for halitosis often differ because the counted items are not always the same, and because pricing and channel coverage are handled in different ways. Differences also come from which year is treated as the current baseline, and whether the estimate is anchored to observed oral care demand signals or to broad category assumptions.

Diagnostic devices and clinical tests are where the spread usually starts, since some sources group them into adjacent dental equipment buckets, while others treat them as part of treatment revenue. By keeping currency conversion timing consistent, checking price ranges by channel, and validating the homecare versus clinic split through interviews, the estimate stays closer to what is actually bought and used, and that is where Mordor Intelligence differs the most for this market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.41 B (2025) | |

| Industry Publisher A | USD 9.13 B (2024) | Uses a treatment-only definition that leans heavily on mouthwash revenue and tends to exclude diagnostics and some professional pathways, which lowers the total and changes the channel mix. |

| Market Publisher B | USD 8.95 B (2025) | Applies a narrower product basket and a more conservative pricing progression, with limited visibility into premium formats and clinic linked solutions, which compresses the market value. |

The table shows that most of the gap is explained by what gets counted, especially whether diagnostics and professional care related solutions are included alongside consumer products. When the scope is aligned and pricing is checked against channel realities, the resulting market value becomes easier to trace back to clear variables, and it becomes more repeatable to update year after year.

Key Questions Answered in the Report

How large is the halitosis market today?

The halitosis market size reached USD 15.93 billion in 2026 and is projected to hit USD 26.36 billion by 2031.

Which product type sells the most?

Antimicrobial mouthrinses lead the halitosis market, accounting for 53.78% of 2025 revenue.

Why is Asia-Pacific experiencing the fastest growth?

Rising disposable income, favorable nutraceutical regulations, and high periodontal-disease prevalence drive a forecast 12.67% CAGR for the region.

What factors restrain wider treatment adoption?

Taste alteration and staining from chlorhexidine, lack of insurance reimbursement, and cultural stigma continue to limit therapy uptake.

Page last updated on: