Global Retail Pharmacy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.83 Trillion |

| Market Size (2030) | USD 1.29 Trillion |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

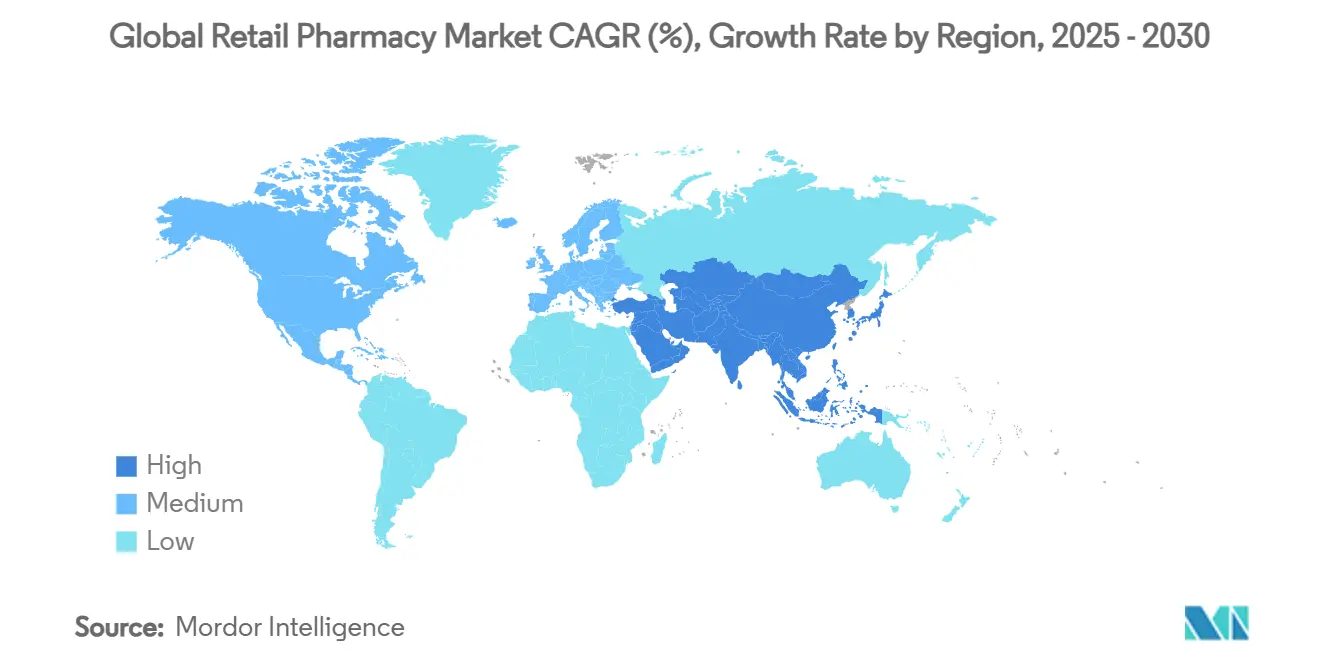

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

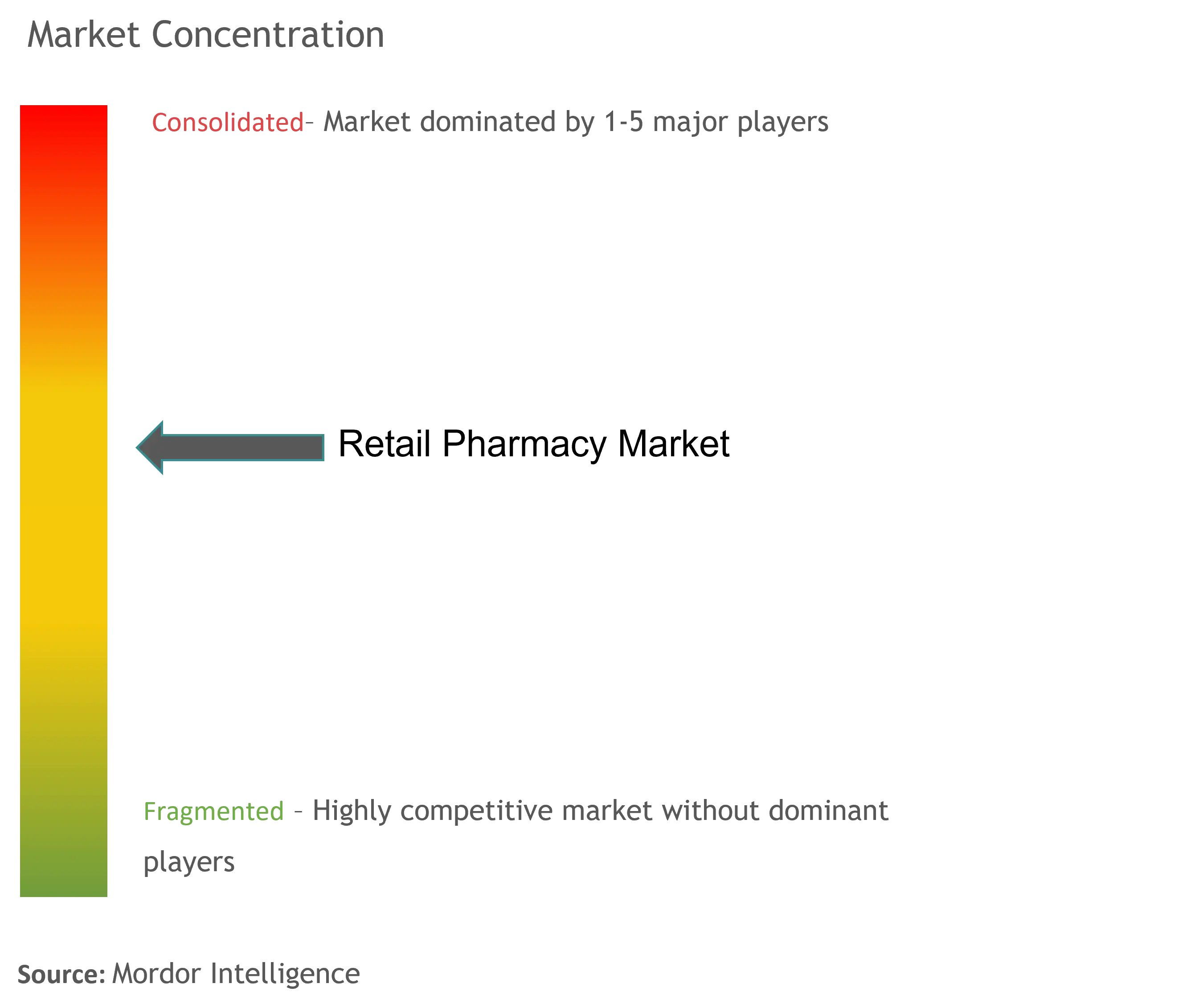

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Retail Pharmacy Market Analysis by Mordor Intelligence

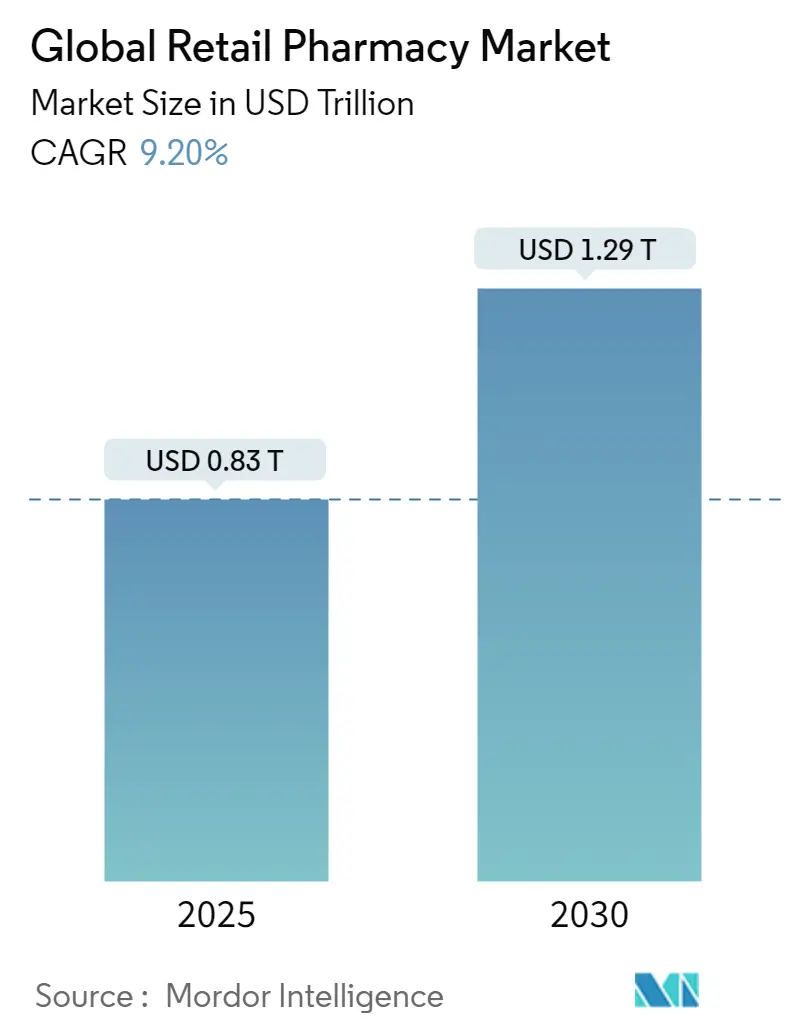

The Retail Pharmacy market size stood at USD 0.83 trillion in 2025 and is forecast to climb to USD 1.29 trillion by 2030, advancing at a 9.2% CAGR. Steady demand for prescription drugs among aging populations, widening adoption of pharmacy-based clinical services, and aggressive digital investments by leading chains collectively underpin this growth trajectory. Chain operators continue to leverage scale advantages in store density, distribution, and data analytics, whereas pure-play online platforms are winning share with transparent pricing and rapid delivery options. Regulatory latitude allowing pharmacists to immunize, test, and manage chronic conditions is broadening revenue streams beyond dispensing. Meanwhile, vertical integration between pharmacies, pharmacy benefit managers (PBMs), and insurers is reshaping margins and negotiating power across the value chain.

Key Report Takeaways

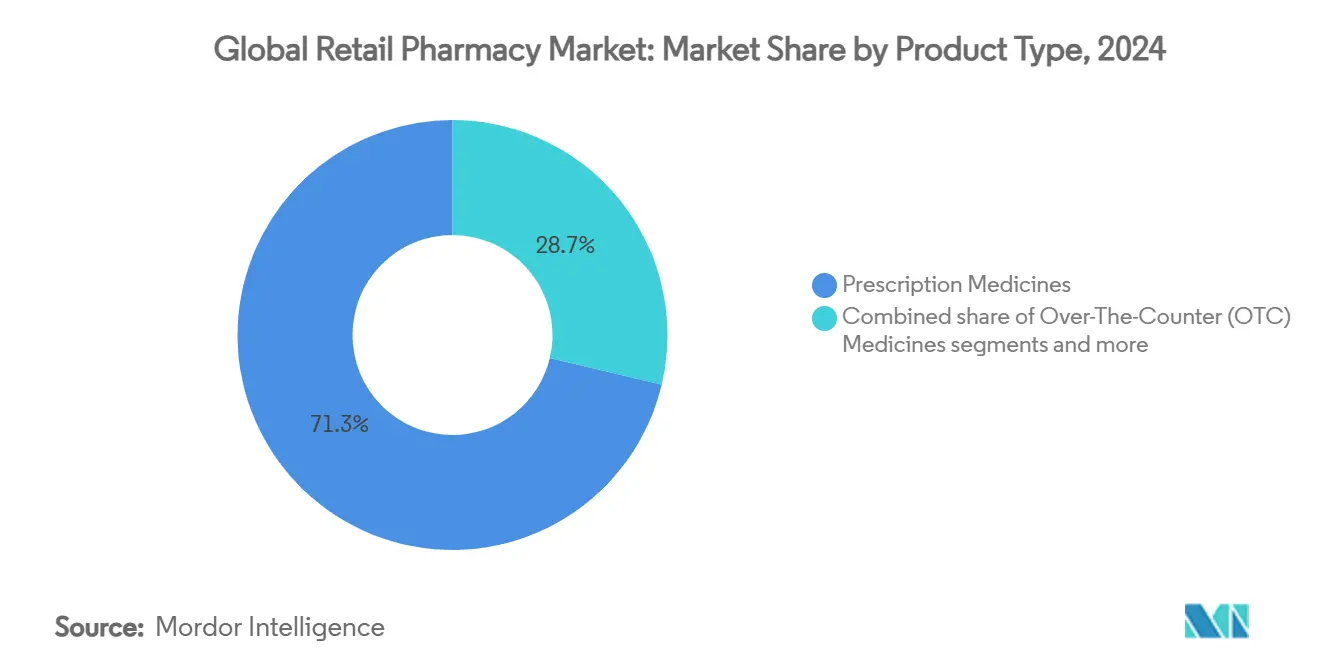

- By product type, prescription medicines held 71.29% of Retail Pharmacy market share in 2024, whereas over-the-counter medicines are expanding at a 9.78% CAGR through 2030.

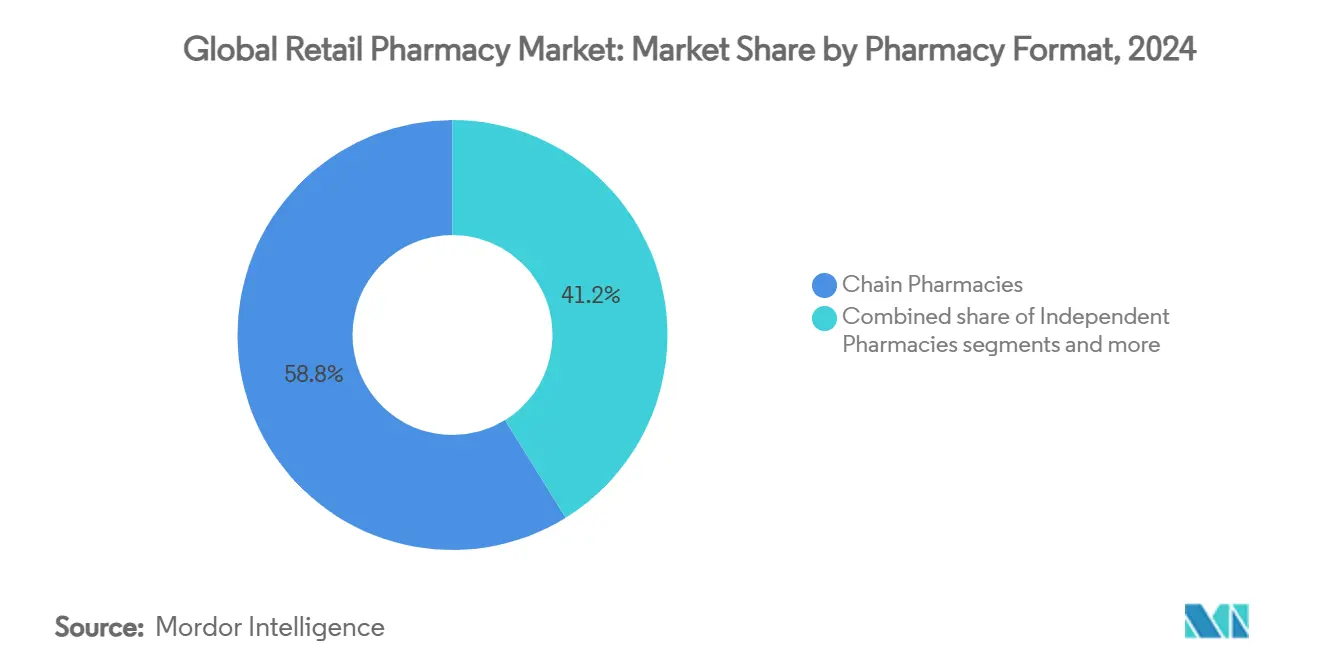

- By pharmacy format, chain pharmacies accounted for 58.82% of Retail Pharmacy market share in 2024, while online pharmacies are projected to post a 10.93% CAGR to 2030.

- By geography, North America commanded 38.23% of Retail Pharmacy market share in 2024, yet Asia-Pacific is projected to record a 10.56% CAGR during 2025-2030.

Global Retail Pharmacy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & chronic disease prevalence | +2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expansion of OTC self-medication trend | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Omnichannel & e-commerce pharmacy penetration | +1.5% | North America & APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Pharmacist scope-of-practice expansion | +1.2% | North America & EU primarily | Medium term (2-4 years) |

| Vertical integration with PBMs & insurers boosts profitability | +0.8% | North America primarily | Long term (≥ 4 years) |

| Data-driven loyalty programs lift basket size | +0.6% | Global, early adoption in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic Disease Prevalence

Older demographics are transforming the Retail Pharmacy Market as 84.7% of Americans aged 65 and above take prescription drugs regularly. Pharmacies are evolving into community health hubs that monitor adherence, deliver vaccinations, and provide point-of-care testing. Diabetes alone is a core driver because glucagon-like peptide-1 (GLP-1) drugs now account for 84% of retail pharmacy diabetes sales. Immunization services also flourish; pharmacies administered more than 60% of influenza shots in the 2023-2024 season. The Centers for Medicare & Medicaid Services intends to transition most fee-for-service programs to value-based care by 2030, positioning pharmacies as frontline coordinators in outcome-oriented reimbursement models. Consequently, the Retail Pharmacy Market continues to shift from transactional dispensing toward longitudinal care delivery.

Expansion of OTC Self-Medication Trend

Households increasingly rely on pharmacies for self-care, with US spending on over-the-counter remedies rising to USD 40 billion in 2024 and delivering USD 167.1 billion in avoided clinical visits. Consumers appreciate immediate access to pharmacists’ guidance coupled with lower treatment costs. Online channels already capture one-third of OTC sales, motivating store-based operators to expand click-and-collect services and subscription programs. Market prospects widened after the US Food & Drug Administration finalized the Additional Conditions for Nonprescription Use (ACNU) rule in January 2025, which ushers more complex therapies—such as respiratory inhalers—into the OTC aisle[1]. Pharmacies investing in decision-support kiosks and in-app symptom checkers are best placed to convert this regulatory opening into higher OTC revenues.

Omnichannel & E-Commerce Pharmacy Penetration

Same-day delivery, transparent pricing, and auto-refill reminders are redefining customer expectations within the Retail Pharmacy Market. Amazon Pharmacy’s RxPass, priced at USD 5 per month for unlimited generics, exemplifies how tech-centric entrants pressure conventional pricing structures. Walmart fuses prescription delivery with its general merchandise network, applying geospatial analytics to optimize drop-off routes and extend reach. CVS Health integrates Microsoft cloud services to deliver personalized promotions based on loyalty-card data, increasing basket conversion and shopper retention. Although digital orders still represent a modest slice of total prescription volume, hybrid consumers who toggle between online refills and in-store consultations now account for the fastest growing revenue pool.

Pharmacist Scope-of-Practice Expansion

All fifty US states authorize pharmacists to vaccinate, while many permit clinical services such as strep throat testing and chronic disease management. The Public Readiness and Emergency Preparedness (PREP) Act extends these permissions through 2029, supporting broader public health roles inside the Retail Pharmacy Market. Denmark’s July 2024 pharmacy reform added pharmacy-run immunizations and medication reviews, demonstrating similar momentum in Europe. Yet scaling these services hinges on reimbursement and workflow redesign: 94% of Ontario pharmacists still perform fewer than 10 travel vaccines each month despite legal authority. Chains such as Walgreens respond by deploying centralized robotics that cut dispensing workload by 50%, freeing pharmacists for consultative care and generating USD 500 million in annual savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement pressure from PBMs & payors | -2.3% | North America primarily, spreading globally | Medium term (2-4 years) |

| Price competition from pure-play online pharmacies | -1.7% | Global, led by developed markets | Short term (≤ 2 years) |

| Pharmacist & technician labour shortages | -1.4% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Retail crime & controlled-substance diversion | -0.9% | North America & Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Pressure from PBMs & Payors

Three vertically integrated PBMs now administer 80% of US prescription claims, often reimbursing independent pharmacies at rates far below acquisition cost. Analyses of 12 million Oregon claims show remuneration that fails to cover ingredient cost plus dispensing fees for many generics[1]Source: Eva Temkin, “FDA Finalizes Rule on ACNU Drugs,” Arnold & Porter, arnoldporter.com . Direct and Indirect Remuneration (DIR) claw-backs can erase USD 10,000 of margin on a single specialty prescription. Legislative efforts in all US states seek to regulate spread pricing and mandate transparency, yet profit compression persists and fuels closures in rural counties. The Retail Pharmacy Market must therefore innovate around service fees and clinical contracting to offset reimbursement risk.

Price Competition from Pure-Play Online Pharmacies

Digital platforms enjoy lower fixed overhead, centralized fulfillment, and algorithmic pricing that undercut brick-and-mortar peers by 10-40% on common generics. Amazon’s RxPass underscores the disruption by bundling unlimited medications for USD 5 monthly, eroding loyalty to local stores. Store operators respond by locking high-theft items in cabinets, but the practice drives 15-25% sales declines by frustrating shoppers and redirecting them online. Strategic differentiation thus hinges on immediate dispensing, in-person counselling, and payer-funded clinical services rather than retail price wars.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prescription Dominance and OTC Acceleration

Prescription medicines captured 71.29% of Retail Pharmacy market share in 2024, reflecting the indispensable role of chronic disease pharmacotherapy in aging societies. Multiple sclerosis, oncology, and diabetes therapies are increasingly dispensed through community outlets as integrated care models rely on pharmacists for adherence monitoring. The FDA’s ACNU rule, effective 2025, blurs traditional boundaries by permitting asthma inhalers and other formerly prescription-only products to transition over the counter. Consequently, over-the-counter remedies lead growth with a 9.78% CAGR, supported by consumer demand for self-care and insurers’ preference for lower-cost treatment pathways. The Retail Pharmacy market size for OTC lines is poised to widen further as retailers deploy digital symptom triage tools that recommend eligible ACNU products at checkout, thereby boosting customer conversion.

Continued expansion in health and wellness merchandise—including nutraceuticals, skincare, and home diagnostics—repositions pharmacies as holistic wellbeing destinations. Integrating blood-pressure kiosks and hemoglobin A1c tests at front-of-store further stimulates cross-category purchases, enhancing gross margin mix. Specialty pharmacy services also gain traction; Walgreens’ entry into cell and gene therapy distribution illustrates how traditional chains target high-value biologics to offset shrinking generic margins. Demand for at-home medical devices, from continuous glucose monitors to smart nebulizers, aligns with telehealth adoption and remote patient monitoring reimbursement. Collectively, these trends reinforce prescription scale while accelerating OTC and ancillary revenue, securing resilient multi-category growth within the Retail Pharmacy Market.

By Pharmacy Format: Chain Leadership Under Digital Pressure

Chain pharmacies retained 58.82% share in 2024 owing to dense networks, centralized procurement, and established payer contracts. Robotics-enabled central fill hubs reduce dispensing costs by up to 40%, allowing pharmacists to reallocate time toward vaccinations and medication therapy management. Independent operators, while valued for community connections, confront unfavorable PBM reimbursement differentials and escalating labor expenses that threaten viability unless they specialize in niche services such as compounding or long-term-care dispensing.

Online pharmacies, although still a minority channel, will post a 10.93% CAGR through 2030 as digital-native consumers seek doorstep fulfillment and transparent price comparisons. Hybrid formats gain momentum: supermarket in-store pharmacies expand loyalty schemes that reward medication adherence with fuel points or healthy food coupons, exemplified by Kroger’s agreement with Express Scripts covering over 100 million lives. Meanwhile, discounters and mass retailers integrate telemedicine booths and clinician-staffed walk-in clinics, narrowing the service gap with dedicated pharmacy chains. Formats that seamlessly connect e-prescribing, automated fulfillment, and personalized engagement will capture disproportionate growth in the evolving Retail Pharmacy Market.

Geography Analysis

North America held 38.23% of Retail Pharmacy market share in 2024, propelled by high per-capita drug spending, extensive insurance coverage, and sophisticated clinical offerings. Ongoing labor shortages, marked by a 64% decline in US pharmacy-school applications since 2012, create projected shortfalls of 3,000-4,000 pharmacists annually, challenging service expansion. The region also experiences pronounced PBM-driven reimbursement compression, fueling consolidation waves such as Walgreens’ USD 23.7 billion private-equity buyout and Rite Aid’s asset divestitures. Regulatory shifts—ranging from the FDA’s ACNU rule to Medicare Part D redesign requiring broader medication therapy management—sustain investment in clinical and digital capabilities.

Asia-Pacific is the fastest-growing cluster with a 10.56% CAGR thanks to rising middle-class incomes, government coverage expansion, and chain-store rollouts in populous markets like India. Apollo Hospitals alone aims to operate more than 6,000 pharmacies by 2027 while targeting INR 25,000 crore revenue, underscoring robust organized-retail runway. Japanese drugstore consolidation, highlighted by the Welcia-Tsuruha-Aeon alliance, establishes efficient procurement platforms to address elder-care medication needs. E-commerce penetration accelerates in China and Southeast Asia, where digital wallets and teleconsultations normalize online prescription fulfillment, further diversifying growth pathways.

Europe shows moderate expansion amid stringent reimbursement controls and distinct national regulations. Germany’s 2025 electronic patient record mandate embeds pharmacies into tele-medical workflows, while Denmark’s Pharmacy Act amendments introduce performance-based remuneration that separates prescription and retail margins. The UK’s Pharmacy First program reimburses minor-ailment consultations, enlarging professional-service revenues if adequate funding persists. Swiss deregulation foreshadows heightened online competition, compelling store operators to differentiate through counseling and rapid local delivery. Collectively, geographic strategies hinge on aligning service portfolios with reimbursement climates and demographic realities to maximize the Retail Pharmacy Market opportunity.

Competitive Landscape

Consolidation remains a central theme: Walgreens’ private-equity transaction aims to unlock operational flexibility, while CVS Health continues vertical integration via Oak Street Health primary-care clinics, deepening insurer-provider-pharmacy synergies. Amazon Pharmacy pushes transparent drug pricing, compelling incumbents to streamline supply chains and democratize e-commerce features.

Technology adoption is the most visible battleground. Walgreens’ micro-fulfillment robots fill 300 prescriptions per hour and enable pharmacists to devote more than half their shift to patient-facing services. CVS leverages Microsoft Azure to run predictive adherence algorithms that trigger targeted outreach, boosting script-refill rates and loyalty. Kroger’s partnership with Express Scripts aligns grocery loyalty data with formulary management, creating cross-category incentives that increase total basket value. Independent pharmacies partner with technology-enabled PBMs such as EmpiRx Health to secure value-based reimbursement, illustrating collaborative approaches to counter scale disadvantages.

Strategic emphasis increasingly lands on specialty therapeutics and clinical programs. Walgreens and CVS expand into cell and gene therapies, building high-touch distribution channels with embedded nursing services and temperature-controlled logistics. Chains also invest in pharmacy schools and technician apprenticeships to alleviate talent shortages and fortify future staffing pipelines. Across markets, sustainable advantage derives from integrating omnichannel convenience with credentialed clinical expertise, ensuring the Retail Pharmacy Market remains indispensable within the healthcare continuum.

Global Retail Pharmacy Industry Leaders

Walgreens Boots Alliance

CVS Health

MedPlus

Grupo Casa Saba

Walvax Biotechnology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: DoseSpot partnered with Amazon Pharmacy to enhance e-prescribing access and affordability

- July 2025: Apollo Hospitals outlined plans to restructure omni-channel pharmacy and digital ventures targeting INR 25,000 crore revenue by FY27

Global Retail Pharmacy Market Report Scope

As per the scope of the report, a retail pharmacy is an individual or chain pharmacy licensed by the state that dispenses drugs at retail pricing to the general public.

The retail pharmacy market is segmented by product, distribution channel, and geography. By product, the market is segmented into prescription drugs, over-the-counter (OTC) products, health and wellness products, medical devices and equipment, personal care products, and other products (home healthcare products and nutrition supplements). By distribution channel, the market is segmented into chain pharmacy, independent pharmacy, and other distribution channels (hospital pharmacy, supermarket pharmacy, mass merchandiser pharmacy, and mail-order pharmacy). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market size is provided for each segment in terms of value (USD).

| Prescription Medicines |

| Over-The-Counter (OTC) Medicines |

| Health & Wellness / Personal Care Products |

| Medical Devices & Supplies |

| Chain Pharmacies |

| Independent Pharmacies |

| Supermarket / Hypermarket In-Store Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Prescription Medicines | |

| Over-The-Counter (OTC) Medicines | ||

| Health & Wellness / Personal Care Products | ||

| Medical Devices & Supplies | ||

| By Pharmacy Format (Value) | Chain Pharmacies | |

| Independent Pharmacies | ||

| Supermarket / Hypermarket In-Store Pharmacies | ||

| Online Pharmacies | ||

| By Region (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Retail Pharmacy Market in 2025?

The Retail Pharmacy market size is USD 0.83 trillion in 2025 with a projected 9.2% CAGR to reach USD 1.29 trillion by 2030.

Which product category leads pharmacy sales?

Prescription medicines command 71.29% Retail Pharmacy market share, driven by chronic disease prevalence and expanding specialty therapies.

What is the fastest growing pharmacy format?

Online pharmacies are forecast to post a 10.93% CAGR between 2025-2030 as consumers adopt home delivery and transparent pricing models.

Which region will expand the quickest through 2030?

Asia-Pacific is projected to grow at a 10.56% CAGR due to rising middle-class incomes and rapid chain-store rollouts across India, China, and Japan.

How are pharmacies coping with shrinking reimbursement?

Leading chains invest in robotic fulfillment, value-based care contracts, and specialty pharmacy channels to offset PBM-driven margin pressure.

What strategic moves are shaping competition?

Recent deals include Walgreens USD 23.7 billion buyout by Sycamore Partners, CVS's Oak Street Health clinic roll-out, and Amazon Pharmacys RxPass subscription.

Page last updated on: