Sirolimus Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 299.98 Million |

| Market Size (2031) | USD 410.8 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sirolimus Market Analysis by Mordor Intelligence

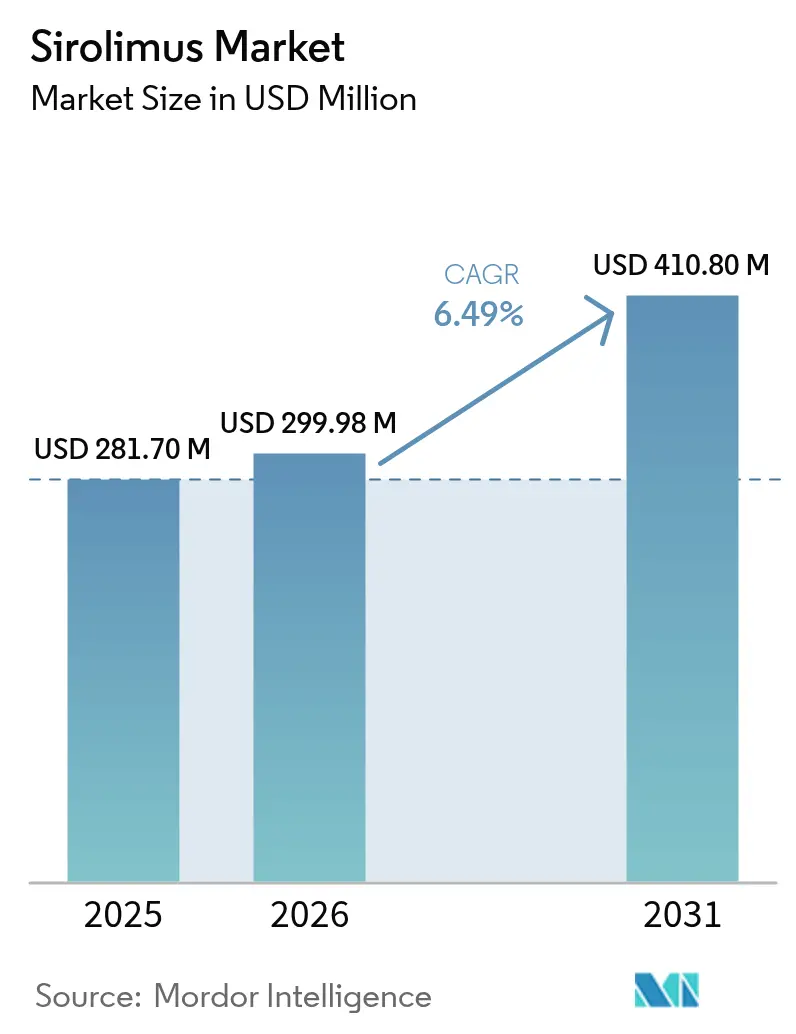

The Sirolimus market size is expected to grow from USD 281.70 million in 2025 to USD 299.98 million in 2026 and is forecast to reach USD 410.8 million by 2031 at 6.49% CAGR over 2026-2031.

Rapid uptake of drug-eluting devices, precision-oncology approvals, and expanding generic penetration are steering sustained revenue gains. Steady growth in global transplant volumes, coupled with maturing evidence for sirolimus’s cardiovascular and antiproliferative benefits, keeps immunosuppression the economic backbone of the sirolimus market. Device makers now leverage the compound’s mTOR-inhibition profile to curb restenosis, while specialty pharma firms pursue rare-disease and tumor indications that command premium pricing. Intensifying competition among Indian and Chinese manufacturers boosts affordable access yet heightens quality-control scrutiny, prompting originators to differentiate through nanotechnology-based formulations and depot systems.

Key Report Takeaways

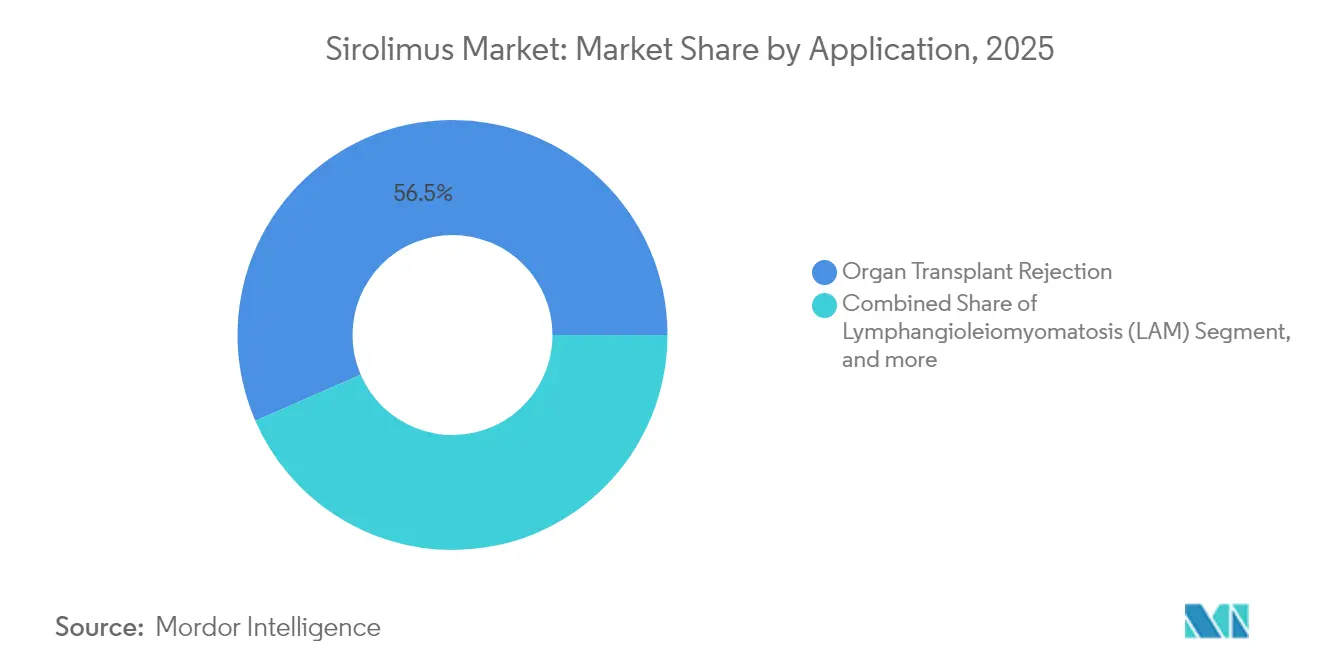

- By application, organ transplant rejection held 56.52% of the sirolimus market share in 2025, whereas sirolimus-coated medical devices are advancing at a 9.54% CAGR through 2031.

- By route of administration, oral formulations commanded 69.25% share of the sirolimus market size in 2025, while drug-coated devices are growing at an 8.41% CAGR to 2031.

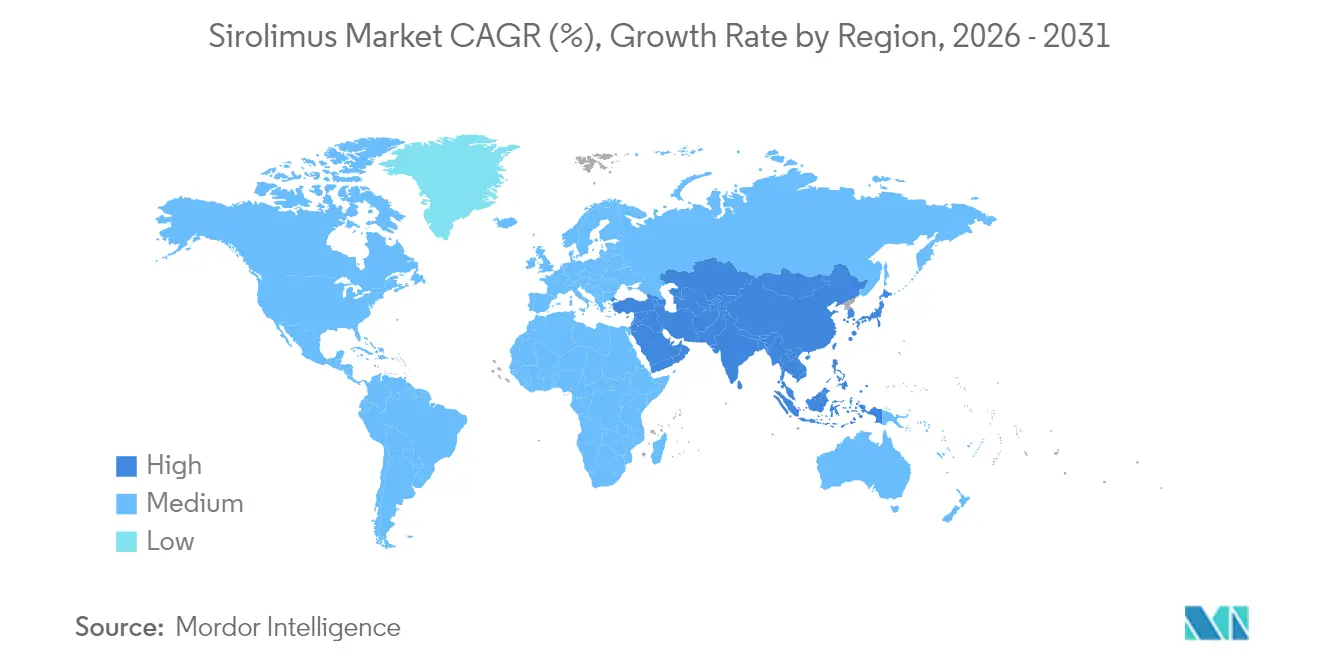

- By region, North America led with 41.60% revenue share in 2025; Asia-Pacific is forecast to expand at an 7.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sirolimus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Transplant Procedures and Lifestyle-Driven Organ Failure | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Proliferation of Generic Sirolimus Products | +0.8% | APAC core, spill-over to MEA and South America | Short term (≤ 2 years) |

| Widening Use of Sirolimus-Coated Balloons and Stents | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Advancements In Nanotechnology and Depot Delivery Systems | +0.9% | Global, early adoption in US and EU | Long term (≥ 4 years) |

| Growing Off-Label Use in Treating Rare Cancers and Vascular Anomalies | +0.7% | North America & EU | Medium term (2-4 years) |

| Increasing Utilization of Sirolimus in Drug-Eluting Devices | +1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Transplant Procedures and Lifestyle-Driven Organ Failure

Higher prevalence of diabetes, obesity, and hypertension accelerates chronic kidney and liver failure, leading to a visible rise in transplant volumes. Clinical experience shows that sirolimus-based regimens safeguard graft function and reduce calcineurin-inhibitor nephrotoxicity, encouraging protocol revisions at large transplant centers.[1]Siemens Healthineers Clinical Insights Team, “Advances in Transplant Care,” siemens-healthineers.com Post-transplant cardiovascular benefits linked to mTOR inhibition further underscore sirolimus’s appeal within multidisciplinary care teams.

Proliferation of Generic Sirolimus Products

Patent expiry has triggered robust generic supply, notably from India and China, where lower manufacturing costs support aggressive pricing. Hospital formularies in Southeast Asia report double-digit uptake of generics, broadening access for cost-sensitive patient groups. Regulatory agencies tighten active-pharmaceutical-ingredient inspections to ensure purity, prompting larger firms to invest in quality-management certifications.

Widening Use of Sirolimus-Coated Balloons and Stents

Interventional cardiology now favors sirolimus-eluting devices to mitigate restenosis in complex lesions. Twelve-month clinical data show target-lesion failure rates near 5% with sirolimus-coated balloons, matching drug-eluting stents while avoiding permanent implants.[2]EuroIntervention Editorial Board, “BIOFLOW-IV Five-Year Outcomes,” eurointervention.com Biodegradable polymer stents sustain comparable safety out to five years, reinforcing adoption in Europe and the United States.

Advancements in Nanotechnology and Depot Delivery Systems

Albumin-bound nanoparticles, cyclodextrin microparticles, and self-micro-emulsifying matrices markedly enhance sirolimus solubility and tissue targeting. The FDA’s approval of nab-sirolimus (FYARRO) for malignant PEComa illustrates how nanoformulations unlock oncology applications.[3]U.S. Food and Drug Administration, “FDA Approves Nab-Sirolimus for Malignant PEComa,” fda.gov Pipeline programs explore weekly depot injections that maintain therapeutic levels without daily oral dosing, reducing therapeutic-drug-monitoring frequency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Negative Effects on Metabolism and Delayed Wound Healing | -0.6% | Global | Short term (≤ 2 years) |

| Significant Costs Associated with Therapeutic Drug Monitoring (TDM) | -0.4% | North America & EU primarily | Medium term (2-4 years) |

| Stringent Regulatory Barriers Surrounding Use in Liver and Lung Transplant Cases | -0.3% | Global | Long term (≥ 4 years) |

| Fermentation-Based Active Ingredient (API) Supply Challenges | -0.5% | Global, particularly affecting generic manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Negative Effects on Metabolism and Delayed Wound Healing

Routine clinical observation confirms elevated cholesterol, triglycerides, and impaired wound repair in patients receiving sirolimus. Surgeons often switch to alternative immunosuppression for peri-operative periods to mitigate wound-healing risk. Endocrinology consults add complexity and cost, especially in elderly or diabetic cohorts.

Significant Costs Associated with Therapeutic Drug Monitoring

A narrow therapeutic window requires frequent serum assays, each costing more than USD 200 in tertiary hospitals. Over a typical first-year post-transplant regimen, monitoring expenses can contribute nearly one-fifth of total treatment spending. Rural centers in Latin America and Africa struggle with assay availability, restraining sirolimus adoption despite falling generic prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Device Applications Drive Innovation Beyond Transplant Medicine

Organ transplant rejection generated the highest revenue, reflecting 56.52% of the sirolimus market size in 2025 and growing steadily alongside global transplant volumes. Sirolimus’s long-term graft-survival benefit cements its position in kidney, heart, and combined-organ protocols, even as centers integrate newer induction agents. On the growth front, sirolimus-coated balloons and stents post an impressive 9.54% CAGR through 2031 as interventional cardiologists favor polymer-free drug delivery that avoids permanent implants. Real-world registries document target-lesion revascularization under 3% at three years, supporting procedural reimbursement in Europe. Oncology indications, spearheaded by FYARRO for malignant PEComa, generate high average selling prices, though current patient pools remain niche. Investigators test sirolimus in TSC1/2-mutant solid tumors and vascular sarcomas, potentially broadening future addressable demand. Off-label deployments in systemic lupus erythematosus and refractory vascular anomalies depict the therapeutic versatility that underpins steady pipeline expansion.

A secondary cohort, lymphangioleiomyomatosis, benefits from Rapamune’s orphan-drug designation, supplying predictable albeit limited volume, particularly in the United States and Japan. Small proof-of-concept trials explore sirolimus for post-acute sequelae of COVID-19, and early data suggest improvement in fatigue and exercise tolerance, hinting at untapped revenue streams if late-phase outcomes prove positive. Autoimmune specialists examine low-dose regimens in systemic sclerosis and inflammatory myopathies, further amplifying long-term optionality. Collectively, the widening application slate reinforces multi-year demand visibility that supports a diversified sirolimus market.

By Route of Administration: Device Delivery Challenges Oral Dominance

Oral formulations captured 69.25% of the sirolimus market size in 2025 due to entrenched prescription habits, convenient at-home dosing, and straightforward reimbursement pathways. Tablets and solutions remain first-line in chronic transplant management, where decades of clinical evidence back dosing protocols. Yet growth momentum shifts toward drug-coated devices, the fastest-rising delivery approach at an 8.41% CAGR to 2031. Coronary and peripheral balloons leverage micro-porous coatings that release sirolimus into vessel walls within minutes, reducing systemic exposure. Early success in de-novo small-vessel coronary disease prompts trials in intracranial and renal arteries, reinforcing cross-specialty enthusiasm.

Parenteral infusions retain relevance for hospital-initiated therapy in acute oncology or in patients with severe gastrointestinal dysfunction. Intravenous nano-suspensions demonstrate predictable pharmacokinetics and permit weight-based dosing adjustments during neutropenic episodes. Topical gels, highlighted by HYFTOR for tuberous-sclerosis angiofibromas, open dermatology revenue niches. Development pipelines feature biodegradable implants made of polylactic acid fibers that deliver sirolimus for six months, targeting glaucoma filtration surgeries and orthopedic implants. Collectively, diversified delivery modes stabilize supply-chain risk and future-proof sirolimus market positioning against formulation-specific disruptions.

Geography Analysis

North America dominated with 41.60% revenue in 2025, owing to sophisticated transplant networks, early oncology approvals, and high per-capita procedural volumes. United States academic centers maintain more than 300 active sirolimus trials, cementing clinical leadership and accelerating physician confidence. Canadian reimbursement agencies accept drug-eluting device premiums after cost-effectiveness reviews demonstrated fewer repeat interventions. Mexico, while smaller, records double-digit unit growth as generics lower barriers to immunosuppression.

Asia-Pacific is the fastest-growing territory, posting an 7.89% CAGR through 2031 as transplant capacity in China and India expands. Japanese cardiologists rapidly transition from paclitaxel to sirolimus coatings following favorable late-lumen-loss data. Indian contract-development-and-manufacturing organizations produce fermentation-based APIs at scale, enabling competitively priced finished-dose exports to Southeast Asia and Africa. Australia channels public-health budgets toward drug-eluting balloons for below-the-knee critical-limb-ischemia, reflecting high diabetes incidence in the region.

Europe sustains mid-single-digit growth through universal health coverage that supports transplant and complex-PCI volumes. Germany and France spearhead device adoption driven by outcome data from polymer-free stent registries. The European Medicines Agency streamlines centralized approvals, recently endorsing novel topical and nano-particulate formulations. Southern European countries leverage reference pricing to secure generic supply, widening patient access while preserving budget discipline. Post-Brexit United Kingdom maintains mutual recognition for immunosuppressants, avoiding supply disruption.

Competitive Landscape

The sirolimus market displays moderate concentration. Pfizer defends its Rapamune franchise through brand loyalty and post-marketing safety data. Generic entrants such as Dr. Reddy’s Laboratories, Zydus Lifesciences, and Biocon compete on price and regional distribution heft, collectively capturing meaningful oral-tablet volume. Boston Scientific and Surmodics lead the device arm via proprietary micro-porous coating technologies, each holding extensive clinical registries supporting reimbursement for complex lesions. Medtronic pursues polymer-free coronary stent designs aiming to displace incumbent everolimus platforms.

Specialty biotech players emphasize oncology and rare-disease white spaces. Aadi Bioscience’s nab-sirolimus secured FDA approval for malignant PEComa with orphan exclusivity and twelve issued United States patents valid through 2040. Annual treatment costs exceed USD 400,000, underpinning premium revenue per patient. Chimeric vector firms evaluate rapalog conjugates to cross the blood-brain barrier, while start-ups in Israel and Singapore explore inhaled formulations for bronchiolitis obliterans syndrome after lung transplantation. Supply-chain resilience forms a key battleground as fermentation yields above 8 g/L differentiate low-cost producers. Technology platforms that integrate drug and device expertise command strategic importance, evident in Boston Scientific’s Virtue balloon IDE pivotal trial and Concept Medical’s positive SIRONA randomized data.

Sirolimus Industry Leaders

Pfizer, Inc

Stentys SA

Dr. Reddy’s Laboratories Ltd.

Biocon Ltd.

Concept Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Orchestra BioMed received FDA investigational-device exemption to begin a United States coronary pivotal trial of the Virtue Sirolimus AngioInfusion Balloon, comparing outcomes against paclitaxel-coated alternatives.

- January 2025: Concept Medical announced favorable SIRONA RCT results showing non-inferiority of its MagicTouch PTA sirolimus-coated balloon versus paclitaxel devices in femoropopliteal disease.

- July 2024: Elixir Medical obtained FDA breakthrough-device designation for its DynamX sirolimus-eluting coronary bioadaptor system targeting symptomatic ischemic heart disease.

Global Sirolimus Market Report Scope

Sirolimus is a macrolide antibiotic produced by Streptomyces hygroscopicus with potent immunosuppressive activity. The Sirolimus Market is segmented By Application (Organ Transplant Rejection, Lymphangioleiomyomatosis, Sirolimus Coated Balloons, Catheter Devices) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Organ Transplant Rejection |

| Lymphangioleiomyomatosis (LAM) |

| Sirolimus-Coated Balloons & Catheter Devices |

| Oncology |

| Auto-immune & Other Emerging Uses |

| Oral |

| Parenteral / Intravenous |

| Topical |

| Drug-Coated Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Organ Transplant Rejection | |

| Lymphangioleiomyomatosis (LAM) | ||

| Sirolimus-Coated Balloons & Catheter Devices | ||

| Oncology | ||

| Auto-immune & Other Emerging Uses | ||

| By Route of Administration | Oral | |

| Parenteral / Intravenous | ||

| Topical | ||

| Drug-Coated Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the sirolimus market?

The sirolimus market stands at USD 299.98 million in 2026 and is projected to reach USD 410.8 million by 2031, reflecting a 6.49% CAGR.

Which application generates the highest revenue?

Organ transplant rejection remains the largest application, accounting for 56.52% of 2025 revenue.

Which sirolimus delivery route is growing the fastest?

Drug-coated devices are expanding at an 8.41% CAGR through 2031 as interventional cardiology shifts to polymer-free coatings.

Why is Asia-Pacific the fastest-growing region?

Rising transplant volumes in China and generics-led affordability in India support an 7.89% CAGR for Asia-Pacific.

What is FYARRO and why is it important?

FYARRO is an FDA-approved albumin-bound nanoparticle formulation of sirolimus for malignant PEComa, demonstrating how nanotechnology opens oncology opportunities.

What limits wider sirolimus adoption?

Metabolic side effects and the high cost of therapeutic drug monitoring curb usage in select patient groups, particularly in cost-constrained health systems.

Page last updated on: