Antibiotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 57.86 Billion |

| Market Size (2031) | USD 70.64 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

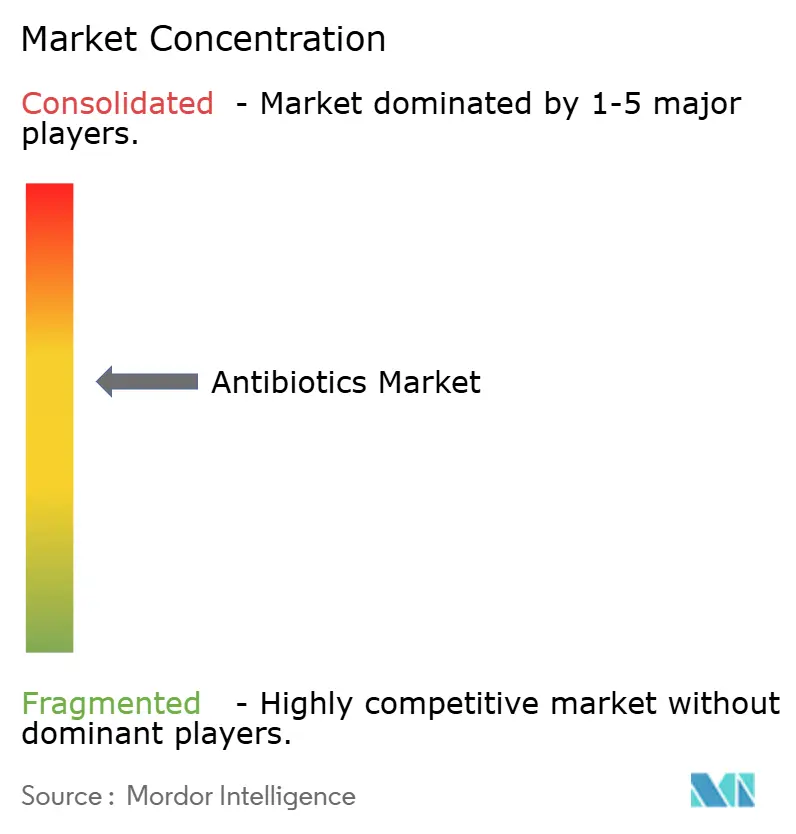

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibiotics Market Analysis by Mordor Intelligence

The Antibiotics Market size was valued at USD 55.60 billion in 2025 and is estimated to grow from USD 57.86 billion in 2026 to reach USD 70.64 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031).

Demand is shifting toward β-lactamase inhibitor combinations and stewardship-favored narrow-spectrum agents, even as broad-spectrum drugs remain indispensable for empiric care. Regulatory approvals such as cefepime-enmetazobactam in 2024 and aztreonam-avibactam in 2025 confirm that incremental innovation around legacy scaffolds is the near-term R&D focus. Fluoroquinolone uptake continues despite boxed warnings because of their role in multidrug-resistant tuberculosis regimens, while payer policies rewarding stewardship are nudging hospitals to document culture-guided de-escalation within 48 hours. Regionally, North America retains revenue leadership on the back of high unit prices, but Asia-Pacific posts the fastest volume growth as public reimbursement expands in India and China.

Key Report Takeaways

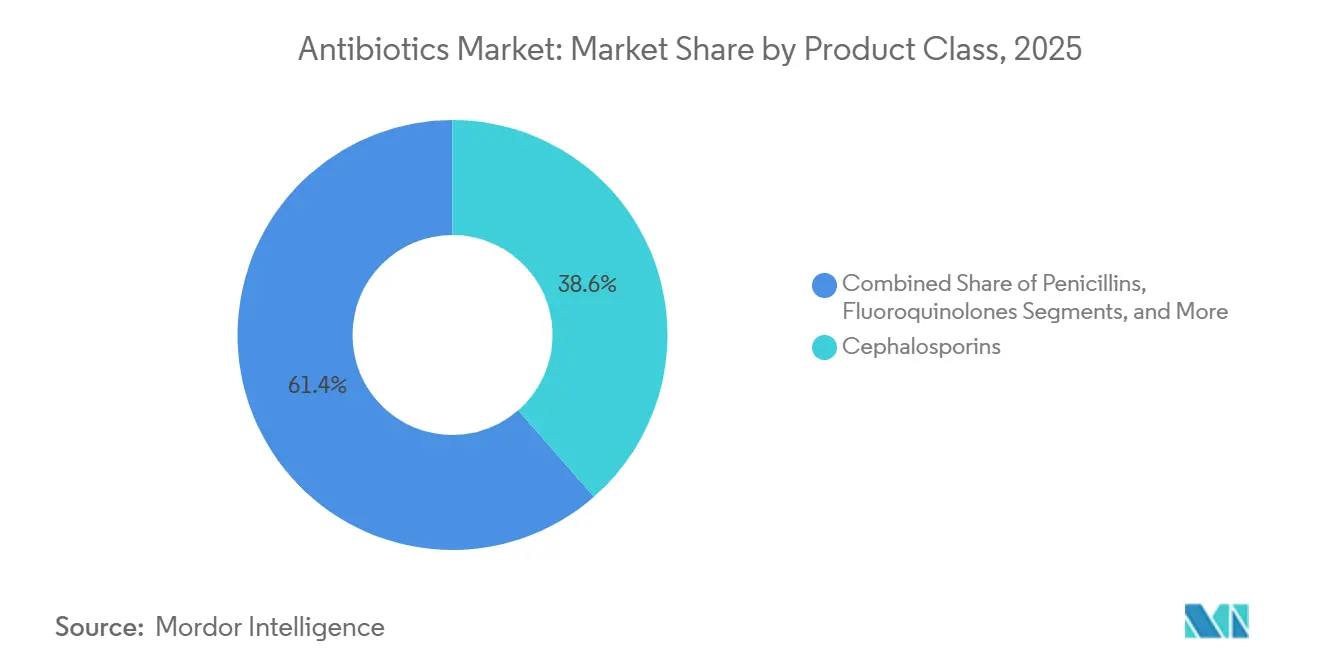

- By product class, cephalosporins led with 38.56% revenue share in 2025, whereas fluoroquinolones are advancing at a 5.25% CAGR through 2031.

- By spectrum, broad-spectrum agents accounted for 65.53% of the antibiotics market share in 2025, while narrow-spectrum drugs are expanding at a 4.85% CAGR to 2031.

- By route of administration, oral formulations captured 56.63% of the antibiotics market size in 2025 and topical formats are projected to grow at a 4.87% CAGR during 2026-2031.

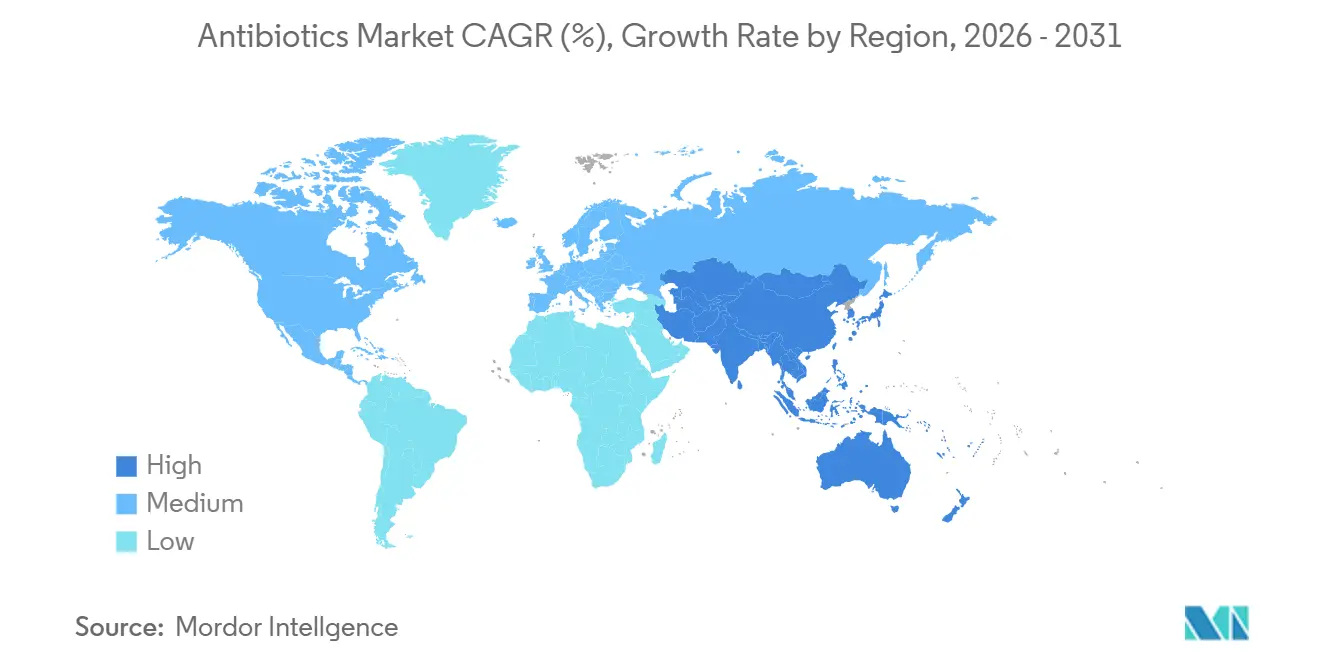

- By geography, North America held 33.13% revenue share in 2025, whereas Asia-Pacific is forecast to post the fastest 4.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antibiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antimicrobial resistance necessitating continual antibiotic innovation and stockpiling | +1.2% | South Asia, Sub-Saharan Africa, Eastern Europe | Long term (≥ 4 years) |

| Rising incidence of hospital-acquired infections in tertiary-care settings across emerging economies | +0.9% | India, China, Indonesia, Middle East & Africa | Medium term (2-4 years) |

| Expansion of universal healthcare coverage and public reimbursement for essential antibiotics in high-burden regions | +0.8% | India, China, ASEAN, Sub-Saharan Africa | Medium term (2-4 years) |

| Technological advances in β-lactamase-inhibitor combinations and novel modalities improving outcomes | +0.6% | United States, EU, Japan | Short term (≤ 2 years) |

| Growing focus on pandemic preparedness and strategic national antibiotic reserves | +0.4% | United States, EU, Australia, GCC | Short term (≤ 2 years) |

| Surge in AI-enabled drug-discovery platforms shortening antibiotic R&D cycles | +0.3% | United States, EU, United Kingdom, Switzerland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Antimicrobial Resistance Necessitating Continual Antibiotic Innovation and Stockpiling

Carbapenem-resistant Enterobacteriaceae infections now carry case-fatality rates above 40%, prompting governments to hold 30-day strategic reserves of colistin and tigecycline[1]European Centre for Disease Prevention and Control, “Antimicrobial Resistance Surveillance in Europe 2025,” ecdc.europa.eu. BARDA directed USD 500 million to CARB-X in 2024, yet only two of 11 funded candidates reached Phase II by mid-2025, underscoring translational bottlenecks. The WHO AWaRe list added six new Reserve agents in 2024, stabilizing demand through advance-purchase agreements while compressing margins. U.S. hospitals must document Reserve-category inventory under updated Strategic National Stockpile rules, creating predictable base volumes. These policies together support steady but regulated uptake of novel drugs.

Rising Incidence of Hospital-Acquired Infections in Tertiary-Care Settings Across Emerging Economies

A 2024 Indian multicenter study recorded surgical-site infection rates of 12.3% versus the 4.1% benchmark in high-income countries, with MRSA isolated in 38% of samples. Overcrowded wards and sub-50% hand-hygiene compliance intensify empiric broad-spectrum prescribing. China reported ICU pneumonia at 18 cases per 1,000 patient-days in 2025, up from 14 in 2023, driven by an aging population and ventilator use. Vietnam’s 2024 surveillance found 22% of bloodstream infections involved ESBL-positive E. coli, shifting guidelines toward carbapenems. Joint Commission International accreditation is spreading in Southeast Asia, but compliance outside certified centers remains inconsistent.

Expansion of Universal Healthcare Coverage and Public Reimbursement for Essential Antibiotics in High-Burden Regions

India expanded Ayushman Bharat reimbursement to 12 more essential antibiotics in 2024, lifting public procurement by 23% year on year. Indonesia’s JKN raised ceftriaxone tariffs by 18% in 2024 to avert shortages across 14 provinces. Africa CDC pooled-procurement deals in 2025 trimmed prices by up to 40% while heightening single-supplier exposure. Thailand’s 2025 pay-for-performance pilot ties hospital bonuses to lower inappropriate fluoroquinolone use, showing reimbursement design can expand access and enforce stewardship.

Technological Advances in β-Lactamase-Inhibitor Combinations and Novel Modalities Improving Outcomes

Cefepime-enmetazobactam achieved 87% cure in complicated urinary-tract infection trials versus 73% for piperacillin-tazobactam, justifying a wholesale cost of USD 3,200 per 10-day course. Aztreonam-avibactam pairs a monobactam with a serine-β-lactamase inhibitor to neutralize metallo-β-lactamases, filling a critical resistance gap. Gepotidacin, cleared in March 2025, is the first new oral class in two decades, though its Gram-positive spectrum limits uptake. Despite setbacks such as early termination of tebipenem’s Phase III for comparator issues, incremental innovation continues to widen treatment options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multidrug-resistant pathogens outpacing commercial development timelines | -0.7% | South Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Stringent stewardship policies limiting use of “Watch” and “Reserve” classes | -0.5% | North America, EU, Australia, Japan | Medium term (2-4 years) |

| High late-stage clinical-trial failure rates and weak ROI deterring private funding | -0.4% | United States, EU | Long term (≥ 4 years) |

| Concentrated API supply chains vulnerable to geopolitical shocks | -0.3% | Global dependency on China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multidrug-Resistant Pathogens Outpacing Commercial Development Timelines

U.S. cases of carbapenem-resistant Acinetobacter doubled from 8,500 in 2022 to 17,200 in 2024 without a new late-stage agent in sight[2]Centers for Disease Control and Prevention, “Antibiotic Resistance Threats Report 2024,” cdc.gov. Plasmid-mediated colistin resistance spread to 47 countries by 2025, eroding the last-line safety net. Pew’s 2024 analysis shows antibiotic programs average 13.2 years from Phase I to approval—longer than oncology—while resistance can surface within three years of launch. MDR-TB strains resistant to bedaquiline and delamanid emerged in 14 nations by 2025. A Clinical Infectious Diseases study pegged the median net present value for a novel antibiotic at negative USD 50 million, deterring private capital.

Stringent Stewardship Policies Limiting Use of “Watch” and “Reserve” Classes

CMS docks 1% of Medicare payments from hospitals with excessive carbapenem use, trimming carbapenem days-of-therapy by 11% in 2024. NICE guidelines now recommend narrow-spectrum first-line treatment for 14 common infections, pushing fluoroquinolones to second-line status. France’s ANSM imposed prior authorization for Reserve drugs in 2025, cutting community prescriptions by 19% in six months. Australia added black-box warnings to fluoroquinolones in 2024, contributing to a 14% volume decline. Japan’s reimbursement penalty for prophylaxis beyond 24 hours aims to curb cephalosporin overuse, which comprised 38% of acute-care consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Class: Cephalosporins Anchor, Fluoroquinolones Accelerate

Cephalosporins delivered 38.56% of 2025 revenue, supported by ceftriaxone’s once-daily regimen and room-temperature stability that lower cold-chain costs in low-resource settings. Fluoroquinolones are projected to grow at 5.25% through 2031, buoyed by their indispensable role in MDR-TB protocols and high oral bioavailability that avoids hospitalization for complicated urinary infections, contributing to incremental antibiotics market growth. Penicillins maintain volume through public tenders, highlighted by Aurobindo’s 15,000-tonne Penicillin G plant commissioned in 2024. Carbapenems, though smaller in volume, command premium pricing but face stewardship caps limiting empiric use.

Fluoroquinolone safety warnings issued in 2024 have not dented uptake in TB-endemic regions, where alternatives are few. Macrolides remain steady thanks to mass azithromycin distribution for trachoma control in Africa, guaranteeing a baseline antibiotics market size for this class. Aminoglycosides retain hospital niches, and tetracyclines gain fresh interest after eravacycline’s label expansion, though its USD 4,500 price confines utilization to severe infections. Collectively, class diversification cushions manufacturers from resistance-driven declines in any single group.

By Spectrum: Broad Agents Dominate, Narrow Options Gain Stewardship Favor

Broad-spectrum drugs held 65.53% of revenue in 2025, reflecting their alignment with the Surviving Sepsis Campaign’s one-hour treatment mandate. Narrow-spectrum agents, growing at 4.85% CAGR, benefit from mandated de-escalation within 48 hours under CDC Core Elements, positioning them for steady share gains in the antibiotics market. The balance of empiric necessity and stewardship rigor sustains both segments, ensuring steady antibiotics market share even as policy tightens.

Penicillin G and ampicillin are resurging for confirmed streptococcal infections, while fidaxomicin’s narrow activity commands a USD 5,400 course price that payers accept for lower recurrence in C. difficile. A 2024 JAMA meta-analysis found every hour of treatment delay raises septic-shock mortality 7.6%, leaving broad-spectrum demand structurally intact. EMA’s 2025 adaptive-trial guidance may accelerate narrow-spectrum approvals, further reshaping prescriber behavior.

By Route of Administration: Oral Convenience Versus Topical Precision

Oral formulations represented 56.63% of 2025 sales as step-down therapy shortens hospital stays and frees beds, keeping the antibiotics market expanding. Topical antibiotics, forecast to grow 4.87% CAGR through 2031, ride WHO guidelines recommending mupirocin nasal decolonization before high-risk surgeries. Intravenous agents remain mandatory for severe infections demanding high serum levels, while intramuscular dosing persists in resource-constrained rheumatic-fever prophylaxis programs.

Retapamulin prescriptions climbed 22% year on year in 2024 as dermatology turned to topical therapy to reduce systemic exposure. Inhaled tobramycin generated USD 380 million on fewer than 30,000 cystic fibrosis patients, underscoring how rare-disease pricing preserves revenue share. FDA’s 2025 approval of a reformulated vancomycin with lower infusion reactions aims at premium positioning against commodity generics.

Geography Analysis

North America delivered 33.13% of 2025 revenue thanks to Medicare Part B mark-ups that price hospital IV drugs 200%–300% above ex-factory cost, underpinning high regional antibiotics market share. Asia-Pacific is expected to post the fastest 4.51% CAGR through 2031 as India’s Ayushman Bharat and China’s Healthy China 2030 digitize reimbursement and stewardship, enlarging the antibiotics market size across populous nations. Japan’s aging population drives steady pneumonia admissions that sustain ceftriaxone and fluoroquinolone uptake despite stewardship pressures.

Europe’s demand levels off under generic competition, but Germany’s 2025 pediatric approval of ceftazidime-avibactam opens a new revenue pocket. The U.K.’s subscription model pays Shionogi GBP 10 million annually for cefiderocol access, an experiment watched by other EU health systems. The GCC invests heavily in new hospitals; Saudi Arabia’s USD 2.4 billion program added 12,000 beds in 2024, boosting formulary volumes[3]Saudi Vision 2030, “Healthcare Infrastructure Investment Program,” vision2030.gov.sa.

South Africa centralized procurement in 2024, saving 28% on acquisition costs but hitting supply snags when a key supplier defaulted in early 2025. Brazil’s SUS purchased 1.8 billion defined daily doses in 2024, making it South America’s largest buyer. Argentina’s 2024 survey showed 41% of pharmacies still dispense antibiotics without prescriptions, undermining stewardship and accelerating resistance. Mexico added meropenem and linezolid to IMSS formularies in 2024, yet funding constraints limited procurement to 60% of need. PAHO is streamlining regional registration, aiming to cut new-drug approval time from 36 months to 18 months, but implementation remains early-stage.

Competitive Landscape

The antibiotics market remains moderately concentrated, with the top players collectively generating significant sales in 2025. Pfizer and GSK are divesting low-margin legacy brands to focus on high-value orphan-style assets, evidenced by Pfizer’s exploration of a hospital-unit sale in 2024. Indian manufacturers Aurobindo and Cipla pursue vertical API integration to hedge supply risk, as seen in Aurobindo’s INR 24 billion Penicillin G plant that went live in 2024. AI-enabled discovery partnerships proliferate, including GSK’s USD 43 million deal with Insilico Medicine to overcome Gram-negative permeability obstacles. FDA’s 2024 draft continuous-manufacturing guidance may trim sterile injectable costs by 20%–30%, but as of late 2025 no company has filed an application under the new pathway.

Oral carbapenems and next-generation inhibitor pairings for outpatient use represent white spaces, but GlaxoSmithKline’s Phase III tebipenem confusion shows comparator selection remains a development hurdle. Continuous globalization of supply chains and digitized stewardship together shape a competitive arena where both scale and specialization can coexist.

Antibiotics Industry Leaders

Pfizer Inc.

Merck & Co., Inc.

Bayer AG

Sandoz AG

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: India announced its first domestically discovered antibiotic, nafithromycin, active against resistant respiratory pathogens and especially useful in cancer and diabetes patients.

- March 2025: The FDA approved Blujepa (gepotidacin) for uncomplicated urinary-tract infections caused by E. coli, K. pneumoniae, C. freundii complex, S. saprophyticus, and E. faecalis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the human antibiotics market as the value of prescription and over-the-counter antibacterial drugs administered orally, parenterally, or topically to treat bacterial infections in people, regardless of brand or molecule generation. It includes original and generic products that are commercially manufactured and excludes active pharmaceutical ingredient (API) merchant sales.

Scope exclusion: Veterinary, feed, and probiotic antimicrobials are kept outside this assessment.

Segmentation Overview

- By Product Class

- Cephalosporins

- Penicillins

- Fluoroquinolones

- Macrolides

- Carbapenems

- Aminoglycosides

- Sulfonamides

- Tetracyclines

- Other Classes

- By Spectrum

- Broad-spectrum Antibiotics

- Narrow-spectrum Antibiotics

- By Route of Administration

- Oral

- Intravenous

- Intramuscular

- Topical

- Other Routes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease clinicians, hospital pharmacists, national procurement officers, and bulk distributors across North America, Europe, Asia-Pacific, Latin America, and the Middle East. These dialogues validated resistance-driven therapy switches, typical ASP pass-through, and pipeline probability-of-success filters, letting us fill obvious desk-research gaps and confirm directional growth drivers.

Desk Research

We began with structured reviews of freely available tier-1 sources such as WHO antimicrobial consumption dashboards, CDC AR Lab Network releases, EMA annual antibiotic sales reports, and OECD Health Data, which offer baseline demand, resistance, and pricing clues. National procurement portals, UN Comtrade shipment records, and patent families accessed through Questel complemented incidence trends with shipment and innovation signals. Company 10-Ks, quarterly earnings, and peer-reviewed journals then anchored cost, launch timing, and pipeline attrition assumptions. This list is illustrative; many other public and paid references were checked during data harvesting and clarification.

A second pass on Dow Jones Factiva, D&B Hoovers, and regional trade association bulletins supplied hospital formulary shifts, tender outcomes, and bulk-buy price corridors that helped us refine average selling prices (ASPs) and stocking cycles across key economies.

Market-Sizing & Forecasting

We applied a top-down incidence-to-treated-patient pool model that starts with country-level disease prevalence, therapy penetration, and treatment length, which are then costed using blended ASPs. Select bottom-up checks, supplier revenue roll-ups, and sampled hospital purchase audits tempered totals and flagged outliers. Key variables tracked include prescription volume per 1,000 population, hospital-acquired infection incidence, resistance-related switch rates, generic erosion velocity, and bilateral trade values. Forecasts to 2030 use multivariate regression on demographic growth, resistance acceleration, policy stewardship intensity, and R&D success probabilities, with scenario analysis guiding upside or downside bands.

Data Validation & Update Cycle

We triangulate model outputs against parallel data streams, rerun variance tests, and subject results to a two-level analyst peer review before sign-off. Updates occur annually, with mid-cycle refreshes triggered by regulatory approvals, sizable M&A, or guideline shifts. A final fact-check is completed just before publication so clients receive the latest view.

Why Mordor's Antibiotics Baseline Commands Credibility

Published estimates often diverge because each provider chooses its own coverage, price references, and refresh cadence. We acknowledge these gaps upfront.

Key divergence drivers include: some studies mingle veterinary or anti-infective classes, others rely on list prices without channel discounts, a few extrapolate historic CAGR instead of variable-based forecasting, and many refresh less frequently than the yearly cycle we follow.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 55.60 B (2025) | Mordor Intelligence | - |

| USD 53.07 B (2024) | Global Consultancy A | Includes branded-only ASPs; excludes emerging-market generics |

| USD 41.63 B (2024) | Industry Association B | Omits hospital tenders and uses fixed exchange rates |

The comparison shows that when scope, pricing realism, and update rhythm are aligned, as in Mordor's model, decision makers receive a balanced, transparent baseline that is traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the expected value of the antibiotics market in 2031?

The market is projected to reach USD 70.64 billion by 2031, growing at a 4.07% CAGR during 2026-2031.

Which product class currently leads global sales?

Cephalosporins lead with 38.56% of 2025 revenue.

Which region is forecast to grow fastest through 2031?

Asia-Pacific is projected to expand at a 4.51% CAGR thanks to expanding public reimbursement schemes in India and China.

Why are β-lactamase-inhibitor combinations gaining momentum?

They restore activity of older β-lactams against resistant organisms, as shown by recent approvals for cefepime-enmetazobactam and aztreonam-avibactam.

How do stewardship policies affect broad-spectrum antibiotic use?

Hospitals must document de-escalation within 48 hours, reducing unnecessary carbapenem and fluoroquinolone exposure.

What is the main supply-chain vulnerability for antibiotics?

Dependence on Chinese and Indian plants for β-lactam APIs poses disruption risk, prompting Western governments to subsidize domestic production.

Page last updated on: